Last week the Bank of England Governor raised the prospect of changes to the Deposit Insurance schemes which exists in many Western Economies. So we look at what he said, and consider the relative security of deposits in the banking system, in the light of recent failures, and Central Bank interventions.

For more on Deposit Bail-In see my recent posts here:

Is Deposit Bail-In A Thing In Australia? https://youtu.be/B8OC2izjKuA

Deposit Bail-In: Who’s Fact-checking The Fact-checkers? With Robbie Barwick https://youtu.be/CAXprMwMnyY

The Deposit Bail In Question… https://youtu.be/n8t-78n1Lrs

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

In the next part of our series Economist John Adams and Analyst Martin North consider the relationship between Deposit Insurance and Bail-In. Things are not straightforward.

As we commence a series on the Deposit Insurance Scheme and Deposit Bail-In, we reprise a show we recorded in 2018 on the DFA channel where Economist John Adams and Analyst Martin North looks at the bones of the scheme. What are the risks?

The New Zealand government’s plan to introduce deposit insurance is a welcome step. Last week, finance minister Grant Robertson announced a new deposit protection regime to make the banking system safer for customers and to strengthen accountability for banks’ actions.

Worldwide, 143 countries have deposit insurance schemes, and New

Zealand has long been an outlier. It is high time one was introduced.

How deposit insurance works

Currently, if a bank fails in New Zealand, depositors could lose all or some of their savings.

Deposit insurance would change that and protect depositors’ savings. It

operates like other types of insurance. If disaster strikes and a bank

fails, depositors’ savings would be repaid up to a set limit.

According to Reserve Bank data, New Zealand households store about NZ$177.98 billion of their cash resources in banks.

The proposed plan is important for all New Zealanders. Most people with

a bank account are retail depositors and may be unaware of the

vulnerable position they could find themselves in.

Under the Reserve Bank’s controversial open bank resolution policy,

if a bank is distressed and under statutory management, part of a

retail depositor’s savings may be frozen and used to recapitalise the

bank, if shareholder and subordinated creditor funds prove insufficient.

Essentially, New Zealand retail depositors would have to bail out their

banks, unlike retail depositors in other countries who are protected by

deposit insurance up to a set limit.

Apart from protecting depositors, the insurance helps to maintain

stability in the financial system. It operates primarily to stop bank

runs where depositors, afraid that they will lose their money, all

demand repayment at once. Images of people lining up outside banks and

at ATM machines all trying to get their money out were a feature of the

2007-2008 Global Financial Crisis (GFC).

If people are confident that they will get their money back quickly

from deposit insurance, they do not need to “run” on their banks.

Banks own the money you deposit

Depositors are vulnerable because once their money is with a bank, it

no longer legally belongs to them. It belongs to the bank which can use

it for its own commercial purposes. Typically, banks will lend this

money to individuals and businesses (for example, through mortgages),

making a profit by charging interest. In return, depositors get the

right to repayment of their savings on demand.

Banks have fragile business models because they borrow short (through

deposits which are repayable on demand) and lend long (through

mortgages and other loans that are repayable at a fixed date in the

future). Banks do not hold sufficient funds to repay all, or even most,

of their depositors at once. Bank regulation provides some protection

because banks are required to maintain certain levels of capital and

liquidity, but if depositors panic and enough of them demand repayment, a

bank can very quickly become insolvent.

Problems in one bank can pass to other banks and from banks to other

types of businesses like a virus (this process is known as contagion).

Eventually, this can build up to a financial crisis and lead to a

recession, just as the GFC did in New Zealand and in many other

countries. In a recession, almost everyone suffers, but the burden often

falls most heavily on the poorest in society who have few assets to

fall back on.

Protecting people and businesses

Retail depositors provide the bulk of bank funding in New Zealand (more than 60% of bank funding comes from households) and they currently carry a degree of risk of bank failure but are not properly protected by the law.

The Reserve Bank has traditionally opposed deposit insurance because of “moral hazard”.

Their argument has been that protecting retail depositors from bank

failure would discourage depositors from monitoring and disciplining

their banks by withdrawing their savings if banks engage in overly risky

activities.

This argument is based on the premise that retail depositors are

capable of monitoring their banks, which requires a high level of

financial literacy. The weakness in this argument was exposed during the

GFC when New Zealand was forced to establish a temporary deposit guarantee scheme

to reassure depositors that their savings were safe. Other countries,

like the UK, recognise this vulnerability and provide an appropriate

level of deposit insurance.

The New Zealand government has proposed a limit of between NZ$30,000 and NZ$50,000,

saying that this would cover up to 90% of depositors. But this is well

below the limits set by other comparable countries. For example, the

limit is about NZ$374,000 in the US, NZ$114,000 in Canada, NZ$161,000 in

the UK and NZ$262,000 in Australia.

If the limit is too low, the risk is that the deposit insurance

scheme will not stop bank runs and not protect financial stability and

the economy. It could even cause pre-emptive bank runs. If that

happened, the government would need to urgently increase the deposit

insurance limit and take other extraordinary measures, but this can lead

to other difficulties, including increased overall costs, which

ultimately fall back on the taxpayer.

The government should be given credit for raising the issue of

deposit insurance – a scheme should have been introduced years ago. But

the low limit was proposed without public consultation. That is wrong.

The deposit insurance limit should not be decided solely by the

Reserve Bank and Treasury. Other stakeholders have an important and

valuable contribution to make. The debate should be transparent and well

informed.

The second phase of the current review of the Reserve Bank Act will look at how a deposit insurance scheme should be funded. It should also include public consultation on the optimal level of deposit insurance. Having finally got the issue on the table, we should not squander the opportunity to do something important for New Zealanders.

Author: Helen Mary Dervan, Senior lecturer in law BCL(Oxon), TEP, Auckland University of Technology

In the Phase 2 document released today, Deposit Insurance, funded by a bank levy is proposed. Unlike the Australian $250k scheme (which is not activated until the Government says so, and is taxpayer funded initially), the NZ scheme is for a lower amount with a protection limit in the range of $30,000 – $50,000. Implementation will probably take at least two years.

One question so far not answered is the interaction with the deposit bail-in. Generally bail-in stops a failing bank from failing, whereas deposit guarantees are activated on failure. So bail-in might stop deposit guarantees even being called on…

Depositor Protection

Why is a range of $30,000 – $50,000 for the proposed depositor protection scheme proposed?

Available data suggests that a protection limit in the range of

$30,000 – $50,000 could fully protect from loss more than 90 percent of

individual bank depositors in New Zealand, while leaving the majority of

banks’ deposit funding exposed to risk. This would strike the right

balance between protecting small depositors from loss and enhancing

public confidence in the banking system on the one hand, while

maintaining private incentives to monitor bank risk taking on the other.

It would also be broadly consistent with international schemes in terms

of the share of deposits and depositors that would be fully protected

(albeit relatively low in terms of the absolute dollar value of

protections).

More work will be required to choose the limit within this range that

is the best for advancing the public policy objectives chosen for the

protection scheme. The consultation seeks feedback on these choices.

The Reserve Bank is proposing high capital requirements for

banks which should reduce the risk of bank failure. Why is depositor

protection required if the risk of bank failure is small?

Even with high capital requirements, banks can still fail for a

variety of reasons. Regulation, supervision, resolution, and deposit

protection all make up a ‘financial safety net’ that supports a stable

and resilient financial system and protects society from the damage

caused by bank failures. The safety net tools interact and overlap,

which can make it seem that not all of the tools are necessary. However,

if the safety net is incomplete, it will be difficult to find effective

solutions for dealing with serious problems in the banking system. This

means that capital tools that help to keep banks safe and sound at the

‘top of the cliff’, must be complemented by robust tools to deal with

banks that may still fall to the bottom.

The OECD and IMF have warned that, without depositor protection, New

Zealand is vulnerable to contagious bank runs. Bank runs can escalate

into banking crises that destroy social and financial capital. For New

Zealand’s safety net to be effective in good times and bad, the tools

within the net must each be strong in its own right, and work well

together.

How will the risks associated with moral hazard be addressed in the proposed depositor protection scheme?

Moral hazard arises when people are protected from the consequences

of their risky behaviour. If deposit protection is introduced,

depositors may take less care when assessing the risks associated with

their banks, and banks may take less care with depositors’ money. Moral

hazard costs are part of the reason why New Zealand has until now chosen

not to have a depositor protection regime.

There is considerable international experience on how to design an

effective deposit protection scheme, within the broader financial safety

net, that mitigates moral hazard. International experience demonstrates

that strong regulatory monitoring of deposit-takers’ corporate

governance and risk management systems goes a long way to addressing the

moral hazard of depositor protection. Maintaining private monitoring

incentives is also important, and can be achieved through carefully

calibrating the protection scheme’s scope of coverage. For example,

setting the protection limit at a level that fully covers most household

and small business depositors, but leaves large institutional

depositors exposed to risk, will support private monitoring incentives.

In conjunction, having effective resolution tools (that make it more

credible investors’ money is at risk should their institution fail) can

sharpen monitoring by institutional investors.

International practice and guidance, as well as the views of experts

and the public, will inform the design of New Zealand’s depositor

protection scheme.

What are the costs of funding the proposed depositor protection scheme and who will bear these costs?

A primary tool of the protection scheme will be insurance. Deposit

insurance transfers the risks and costs of bank failures away from

depositors onto an insurance scheme. This will come with upfront costs

of establishing a deposit insurer, and ongoing operational costs.

Modern deposit insurance schemes are normally funded by levies on

member banks, supported (where necessary) by temporary lending paid for

by taxpayers. If the insurance scheme is accompanied by a depositor

preference, this might also increase banks’ non-deposit funding costs as

risks are transferred from depositors onto institutional investors.

Details of the scheme, including costs, are still to be worked out in

the next phase of the work programme. To the extent that depositor

protection increases banks’ average costs, this might be passed on to

customers through higher mortgage rates or lower deposit rates.

Alternatively, costs might be absorbed by banks’ own margins and

retained earnings. The extent to which costs are shared between banks

and their customers depends on competition and contestability in the

sector.

A fuller cost-benefit analysis will follow as we learn more about the

specific design features of New Zealand’s depositor protection scheme.

When will the depositor protection scheme be introduced?

A work programme running alongside the Reserve Bank Review process

will develop a depositor protection scheme that is best for New Zealand.

The work programme will be guided by a framework setting out some key

design principles for an effective scheme, and will draw (where

relevant) on international standards and best practice. The work

programme will determine the:

mandates and powers

governance and decision making structure

coordination arrangements with other safety net providers

membership and coverage arrangements

funding and pay-out mechanics, and

design features to mitigate moral hazard

that are appropriate for New Zealand’s protection scheme. The Review

Team’s discussions with the global coordinating body for deposit

insurers indicates that the path from policy recommendations to scheme

implementation will probably take at least two years.

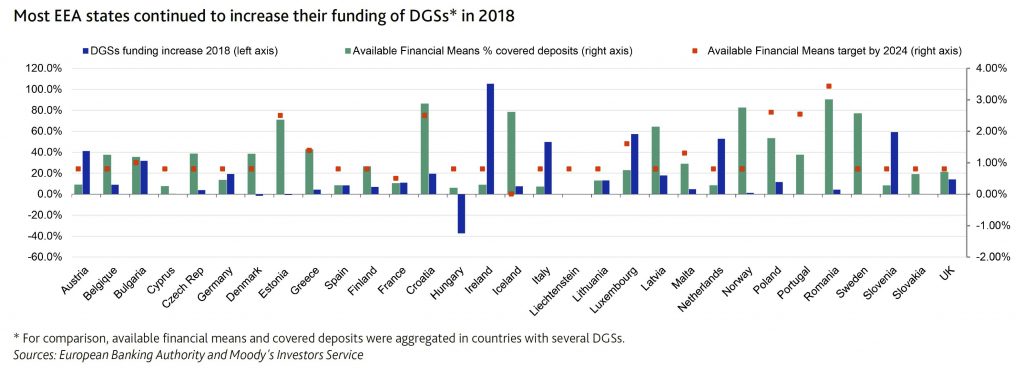

On 17 June, the European Banking Authority (EBA), published 2018 data on national Deposit Guarantee Schemes (DGSs) across the European Economic Area (EEA), which show that 32 of 43 DGSs increased their funds available to cover deposits in 2018 by levying banks.

Here of course the $250k deposit scheme is unfunded and currently inactive.

Moody’s says that the target of 0.8% of covered deposits by 2024 set out in the Deposit Guarantee Schemes Directive (DGSD) has already been achieved in 17 of the 43 DGSs in the EEA. The gradually increasing harmonisation of DGSs in Europe is credit positive for European banks because it improves European banking systems’ financial stability by better protecting depositors against the consequences of credit institution insolvency. As DGS funding increases and exceeds the 0.8% threshold, they also expect banks’ levies to moderate, which will benefit their profitability.

Since the 2009 financial crisis, European authorities developed policies and tools to buttress financial systems’ resiliency and help authorities prevent and, if needed, tackle bank distress without having to resort to taxpayers’ support. DGSs form one of these tools.

Under current EU legislation, depositors are protected by their national DGS up to €100,000 (or the equivalent in local currency). This protection applies regardless of whether ex ante funding has been accrued by DGS. Under the DGSD, all EEA banks are required to contribute to national DGSs so that at least 0.8% of covered deposits are funded by 2024 (and by exception, no less than 0.5% of the covered deposits, like in France2).

Nine member states have set up DGSs with higher funding targets such as Romania (3.43%) and Poland (2.6%). Some countries, such as Iceland, have not yet defined their national funding target, while others have defined numerous DGSs for different categories of banks and depositors, as in Germany for private, public, savings or cooperative banks, hence there are more DGS than there are EU countries.

As of year-end 2018, 16 countries had already reached the DGSD’s 0.8% minimum funding ratio for 2024, and 10 countries exceeded their national target. The levies banks paid increased by around 12% in 2018, while covered deposits grew only by 3.6%. As of year-end 2018, EEA member states had reached in aggregate a funding ratio of 0.65% of covered deposits, up from 0.6% in 2017.

Out of the 31 banking systems addressed in the EBA report, 25 increased the funding for the DGSs in 2018, with very large increases in Ireland (+105.2%), Slovenia (+59.2%) or Luxembourg (+57.3%). The diversity in funding efforts reflects different starting points since some countries did not have DGS or limited ex-ante funding when the DGSD was adopted. For instance Luxembourg had no funding in 2015 and a target of 1.6% of covered deposits.

Despite progress, the third pillar of the banking union – the European deposit insurance scheme (EDIS) proposal adopted in 2015 – is not yet in sight due to a lack of political consensus. The EDIS proposal builds on the system of national DGSs and would provide a stronger and more uniform degree of insurance cover in the euro area. This framework would reduce the vulnerability of national DGSs to large local shocks.

Blog")