The trend unemployment rate remained steady at 5.2 per cent in the month of September 2018 after the August figure was revised down, according to the latest figures released by the Australian Bureau of Statistics (ABS).

The 5% seasonally adjusted result will get all the attention, but these are very volatile, so it is best to work with the trend data, which shows a fall, although participation remains steady. But underemployment remains higher than post the GFC.

“Today’s figures continue to show a gradual decrease in the trend unemployment rate that began in late 2014. The trend unemployment rate of 5.2 per cent is the lowest it has been since mid 2012.” said the Chief Economist for the ABS, Bruce Hockman.

Employment and hours

Trend employment increased by around 26,000 persons in September 2018 with full-time employment increasing by over 21,000 persons.

The trend participation rate remained steady at 65.6 per cent in September 2018.

Over the past year, trend employment increased by over 290,000 persons or 2.4 per cent, which was above the average year-on-year growth over the past 20 years (2.0 per cent).

The trend monthly hours worked increased by 0.2 per cent in September 2018 and by 1.8 per cent over the past year. States and territories

The states and territories with the strongest annual growth in trend employment were New South Wales (3.4 per cent) and Victoria (2.6 per cent). New South Wales and Victoria were the only states and territories to record year-on-year growth above their 20-year averages. Seasonally adjusted data The seasonally adjusted number of persons employed increased by around 5,600 persons in September 2018. The seasonally adjusted unemployment rate decreased to 5.0 per cent and the labour force participation rate decreased to 65.4 per cent.

The net movement of employed in both trend and seasonally adjusted terms is underpinned by well over 300,000 people entering employment, and more than 300,000 leaving employment in the month.

New underemployment data

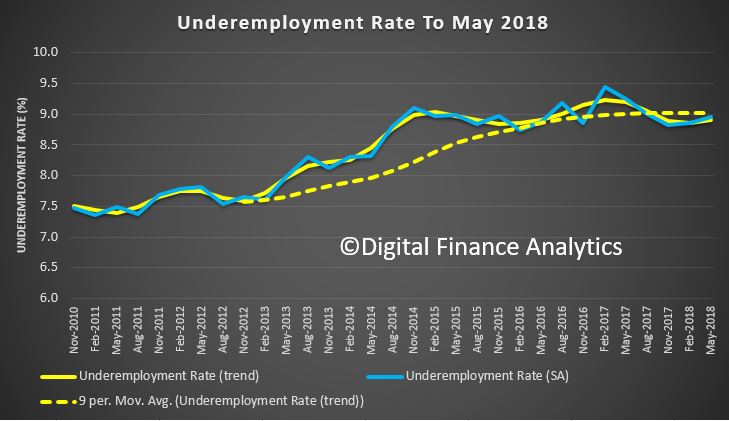

The trend underemployment rate decreased to 8.3 per cent in September 2018 and the trend underutilisation rate decreased to 13.5 per cent.

As of September 2018, Australia’s trended underemployment rate (the proportion of underemployed to the total labour force) remained high in historical terms at 8.3%, but below the peak of 8.8% recorded in March 2017.

The underemployment rate has been increasing since it was first recorded in the February 1978 reference period. Over the last four years, the rate has seen minimal fluctuation, remaining between 8.3% and 8.8% in trend terms. The underemployment rate showed large increases over economic downturns – most notably during the early 1990s and the Global Financial Crisis (GFC) (refer to Graph 1).

Graph 1, Underemployment and unemployment rates trended, February 1978 to September 2018

a. The monthly data for part-time workers who want to work more hours, between April 2001 and June 2014, is modelled as data during this period was collected quarterly.

The trend unemployment rate decreased from 5.4 per cent to 5.3 per cent in the month of August 2018, according to the latest figures released by the Australian Bureau of Statistics (ABS) today.

ABS Chief Economist Bruce Hockman said that “since last August, the trend unemployment and underemployment rates have both fallen. As a result, underutilisation in Australia was at its lowest level since late 2013, at 13.6 per cent.” Employment and hours

Trend employment increased by around 29,000 persons in August 2018 with full-time employment increasing by around 21,000 persons.

The trend participation rate remained steady at 65.6 per cent in August 2018, after the July figure was revised up.

“For those people aged 15 to 64 years, trend participation was the highest on record. Female participation in this age group, at 73.2 per cent, was also a record high,” Mr Hockman said.

Over the past year, trend employment increased by around 300,000 persons or 2.5 per cent, which was above the average year-on-year growth over the past 20 years (2.0 per cent).

The trend monthly hours worked increased by 0.1 per cent in August 2018 and by 1.8 per cent over the past year. States and territories

For most states and territories, year-on-year growth in trend employment was at or above their 20 year average, except for Western Australia, Tasmania and the Australian Capital Territory. Over the past year, the states and territories with the strongest annual growth in trend employment were New South Wales (3.6 per cent), the Northern Territory (3.0 per cent) and Victoria (2.5 per cent). Seasonally adjusted data

The seasonally adjusted number of persons employed increased by around 44,000 persons in August 2018. The seasonally adjusted unemployment rate remained steady at 5.3 per cent, the underemployment rate decreased to 8.1 per cent and the underutilisation rate decreased to 13.4 per cent. The labour force participation rate increased to 65.7 per cent.

The net movement of employed in both trend and seasonally adjusted terms was underpinned by well over 300,000 people entering employment, and more than 300,000 leaving employment in the month.

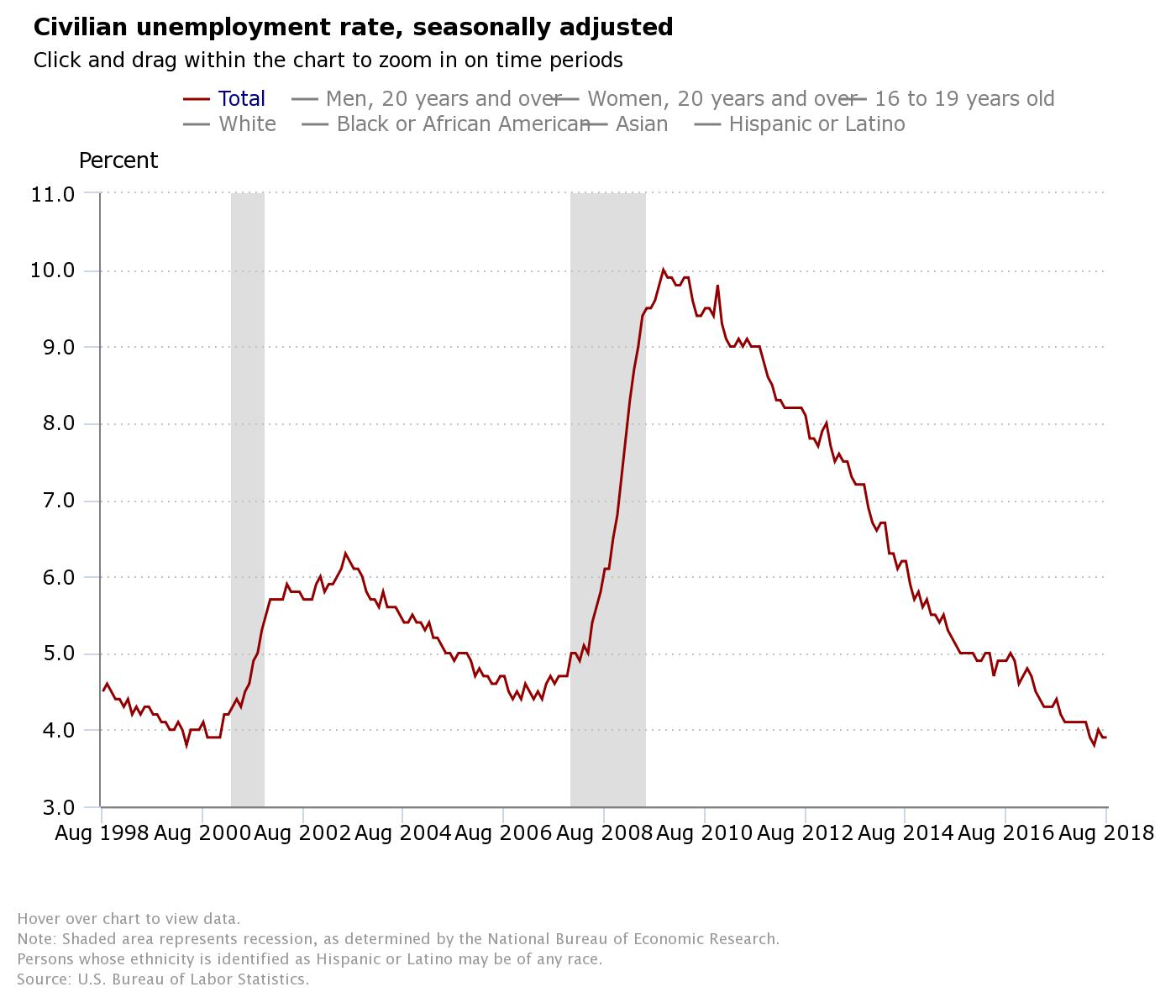

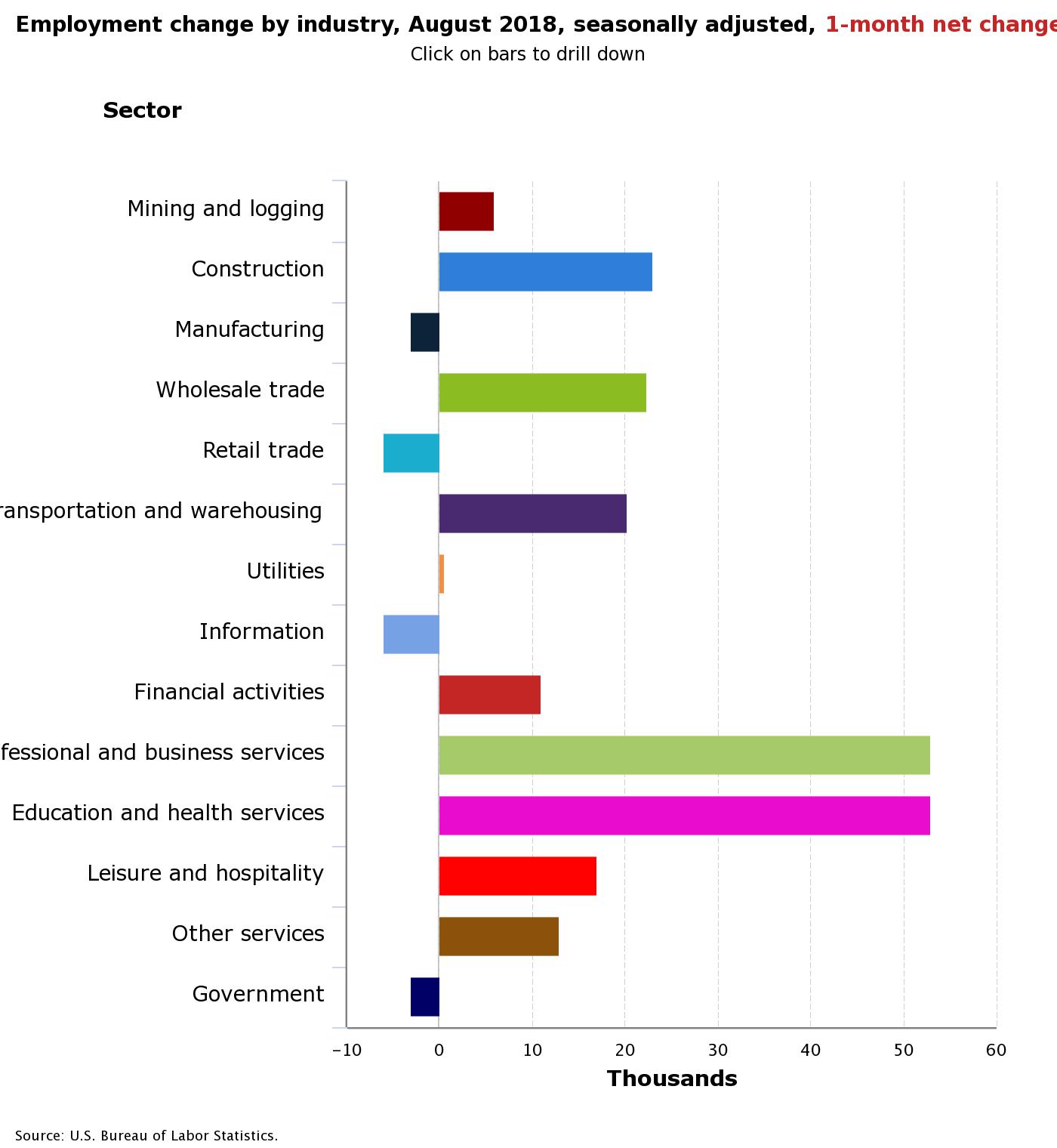

Total nonfarm payroll employment increased by 201,000 in August, and the unemployment rate was unchanged at 3.9 percent, the U.S. Bureau of Labor Statistics reported today.

Job gains occurred in professional and business services, health care, wholesale trade, transportation and warehousing, and mining. Household Survey Data The unemployment rate remained at 3.9 percent in August, and the number of unemployed persons, at 6.2 million, changed little.

Among the major worker groups, the unemployment rates for adult men (3.5 percent), adult women (3.6 percent), teenagers (12.8 percent), Whites (3.4 percent), Blacks (6.3 percent), Asians (3.0 percent), and Hispanics (4.7 percent) showed little or no change in August.

The number of long-term unemployed (those jobless for 27 weeks or more) was little changed in August at 1.3 million and accounted for 21.5 percent of the unemployed. Over the year, the number of long-term unemployed has declined by 403,000.

Both the labor force participation rate, at 62.7 percent, and the employment-population ratio, at 60.3 percent, declined by 0.2 percentage point in August.

The number of persons employed part time for economic reasons (sometimes referred to as involuntary part-time workers), at 4.4 million, changed little over the month but was down by 830,000 over the year. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs.

In August, 1.4 million persons were marginally attached to the labor force, little different from a year earlier. (Data are not seasonally adjusted.) These individuals were not in the labor force, wanted and were available for work, and had looked for a job sometime in the prior 12 months. They were not counted as unemployed because they had not searched for work in the 4 weeks preceding the survey.

Among the marginally attached, there were 434,000 discouraged workers in August, essentially unchanged from a year earlier. (Data are not seasonally adjusted.) Discouraged workers are persons not currently looking for work because they believe no jobs are available for them. The remaining 1.0 million persons marginally attached to the labor force in August had not searched for work for reasons such as school attendance or family responsibilities.

Total nonfarm payroll employment increased by 201,000 in August, in line with the average monthly gain of 196,000 over the prior 12 months. Over the month, employment increased in professional and business services, health care, wholesale trade, transportation and warehousing, and mining.

The trend unemployment rate was 5.4% in the month of June 2018, according to latest figures released by the Australian Bureau of Statistics (ABS) today. The trend participation rate remained steady at 65.6 per cent in June 2018, after the May figure was revised up.

“Over the year to June, the unemployment rate declined by 0.2 percentage points. This continues a gradual decrease in the trend unemployment rate from late 2014 and is the lowest rate since January 2013,” said the Chief Economist for the ABS, Bruce Hockman. Employment and hours

Trend employment increased by around 27,000 persons in June 2018 and the growth was evenly split between full-time and part-time employment, with both increasing by over 13,000 persons. The net increase of 27,000 persons comprised well over 300,000 people entering employment, and more than 300,000 leaving employment in the month.

Over the past year, trend employment increased by 318,000 persons or 2.6 per cent, which was above the average year-on-year growth over the past 20 years (2.0 per cent).

15 to 19 year olds have contributed around a third of trend employment growth since January 2018. Employment for 15 to 19 year olds increased by over 6,000 in June 2018 and grew by around 58,000 over the last year.

The trend monthly hours worked increased by 3.4 million hours or 0.2 per cent in June 2018, and by 2.6 per cent over the past year.

States and Territories

Year-on-year growth in trend employment was above the 20 year average in all states and territories except for Victoria and Western Australia. Over the past year, the states and territories with the strongest annual growth in trend employment were New South Wales (3.7 per cent), Australian Capital Territory (2.9 per cent) and Queensland (2.6 per cent).

Underemployment

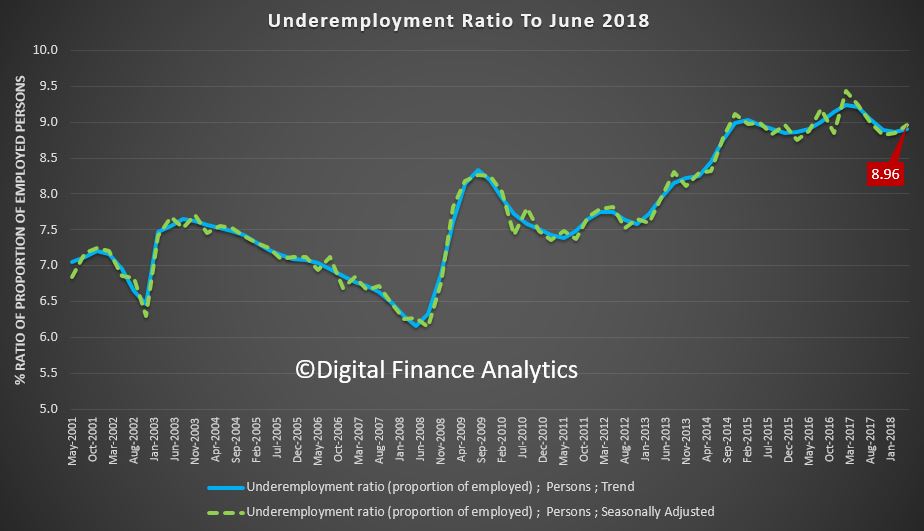

Underemployment (those in work who want more work) is at 9%, and is trending up a little. This is significantly higher than in 2011 when the employment rate was in a similar region, suggesting that more people feel the need for additional work.

Of course the stats are based on a wide definition of “employed” as even a small number of working hours a week shows as an employed person. Alternative measures of unemployment report much higher rates, so there is a question as to the significance and reliability of the numbers. But the trend remains down, which is good news, but in the region above 5%, the level at which the RBA says income growth may start to rise. So we are not there yet!

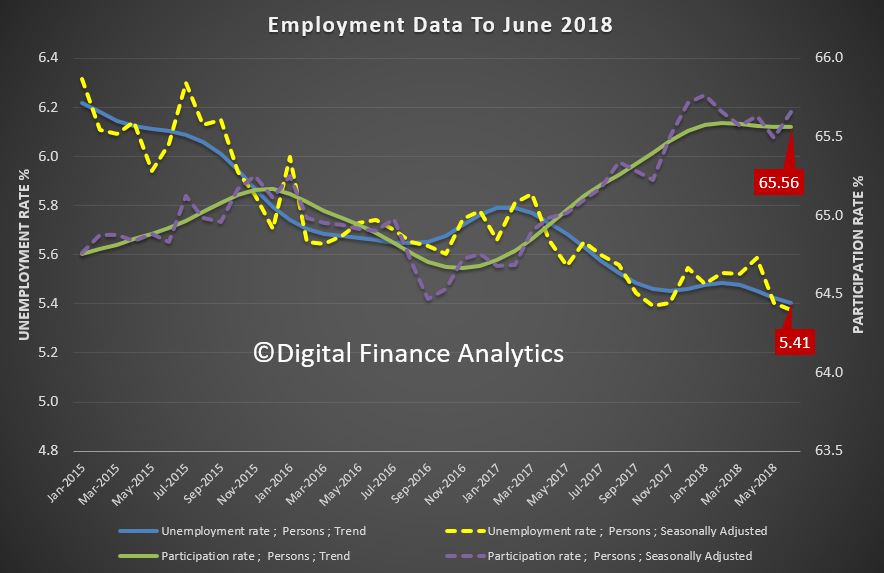

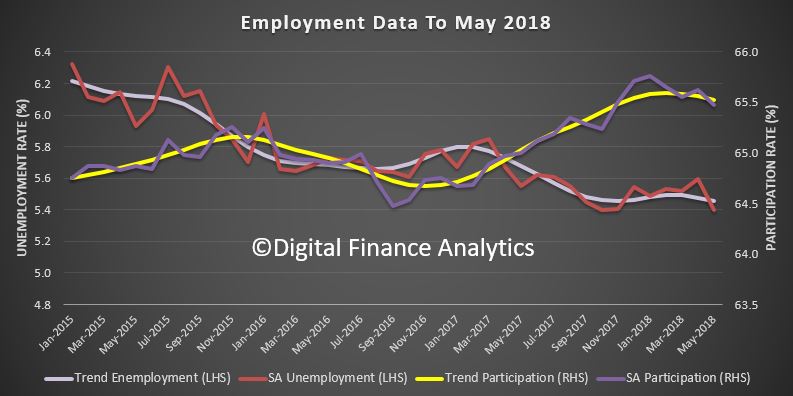

The ABS released their May 2018 employment data today. The Labour force statistics top line story looks pretty good, with an increase in the total number of jobs, and a fall in the seasonally adjusted rate of employment from 5.6% last month to 5.4% in May. But in fact we think this is another soft result, thanks to a slide in the number of hours worked, anemic and falling jobs growth, a further shift to part time employment, and a rise in underemployment.

The monthly trend unemployment rate remained steady at 5.5 per cent in May 2018, according to latest figures released by the Australian Bureau of Statistics (ABS) today.

Actually, it fell just a tad, from 5.48% to 5.46%, but then who’s counting, given the lack of precision in the data set. So lets agree with the ABS, trend, no change.

The trend participation rate decreased by less than 0.1 per cent to 65.5 per cent in May 2018, after the April figure was revised down. Over the past year, trend employment increased by 318,000 persons or 2.6 per cent, which was above the average year-on-year growth over the past 20 years (2.0 per cent).

In fact, its the fall in the participation rate which explains the fall in the unemployment rate stats. We are not seeing such strong growth in jobs, as we saw a few months back in fact.

The underlying trend really shows that underemployment is still very high.

The ABS said that over the year to May, the unemployment rate declined 0.2 per cent, while the underemployment rate also fell by 0.2 per cent over the year to 8.5 per cent. The underemployment rate, which is the proportion of people who are working but would like to work more hours, remains below the peak of 8.7 per cent seen in 2017. “The latest data tells us that over the past year both the trend unemployment rate and underemployment rate declined by 0.2 per cent, resulting in the underutilisation rate declining 0.4 per cent to 13.9 per cent”.

But the troubling thing is that there continues to be a slide towards more part time jobs, with trend employment increasing by around 16,000 persons in May 2018, with part-time employment increasing by 12,000 persons and full-time employment by 4,000 persons. This continued the recent slowing of employment growth, particularly full-time employment growth.

This is further evidence, as we discussed yesterday from our household survey results, that more and more people are in fractured or casual employment.

The net increase of 16,000 persons comprised of well over 300,000 people entering employment, and more than 300,000 leaving employment in the month. This was below the modest 19,000 increase expected by economists.

The trend monthly hours worked increased by 2.8 million hours or 0.2 per cent in May 2018, and by 2.7 per cent over the past year.

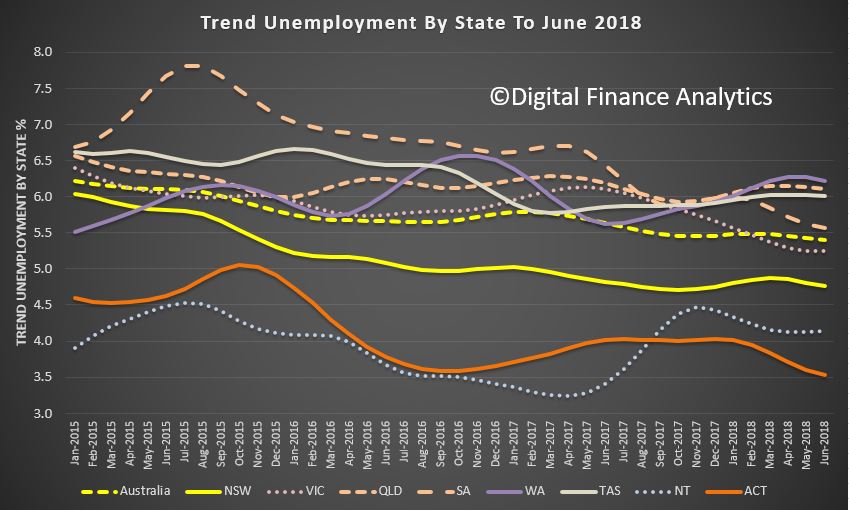

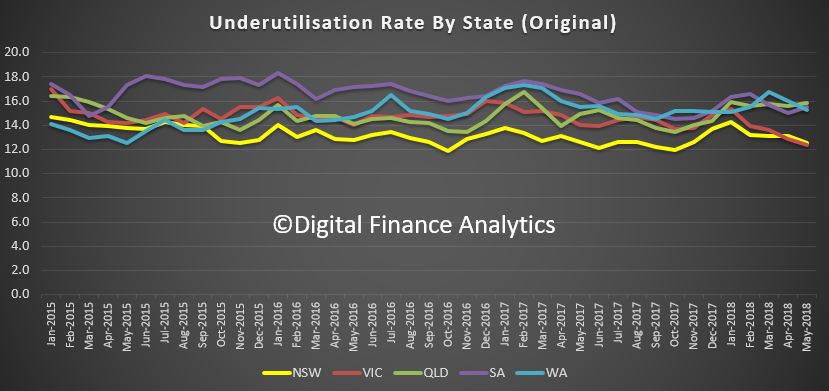

Over the past year, the states and territories with the strongest annual growth in trend employment were New South Wales (3.6 per cent), Queensland (2.9 per cent) and South Australia (2.4 per cent). NSW has led the growth in jobs. We see that NSW has an unemployment rate of 4.9%, in trend terms, just higher than the ACT at 3.7% and the Northern Territory at 4%. Victoria is sitting at 5.1%, South Australia at 5.7%, and Queensland plus Tasmania and Western Australia all well above 6%.

The longer term trends are also worth looking at, with Western Australia at the top of the list with highest rate, and trending higher, with Victoria and New South Wales in the middle of the pack, and the ACT and Northern Territories with the lowest rates of unemployment.

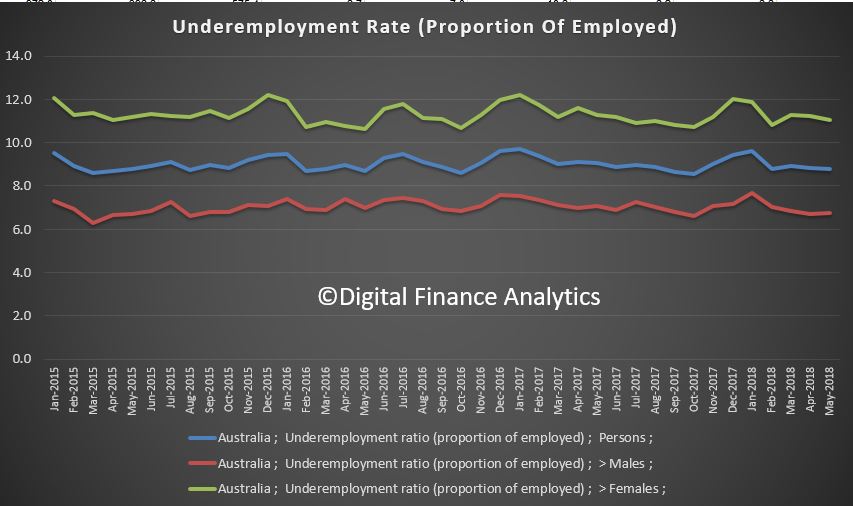

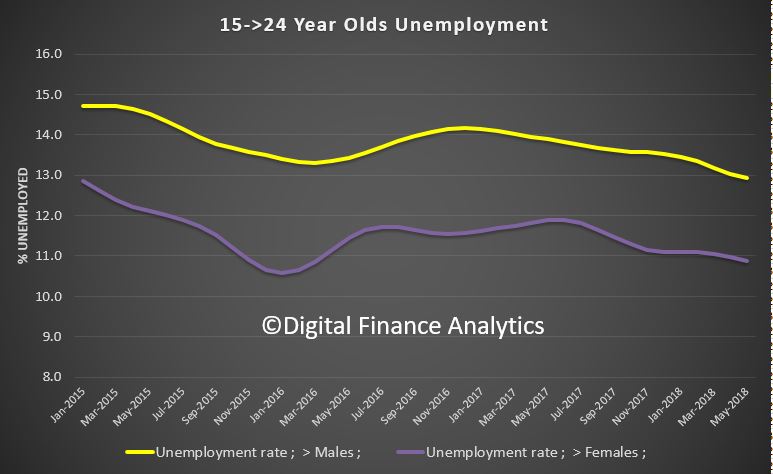

Also note the higher figures among younger Australians, with those between 15 and 24 sitting at 13% for males and 11% for females.

So, this suggests there is no reason to expect the employment rate to fall toward the “magic 5%” when the RBA says wages should start to rise. We think if anything unemployment may rise in the months ahead as jobs growth slows further.

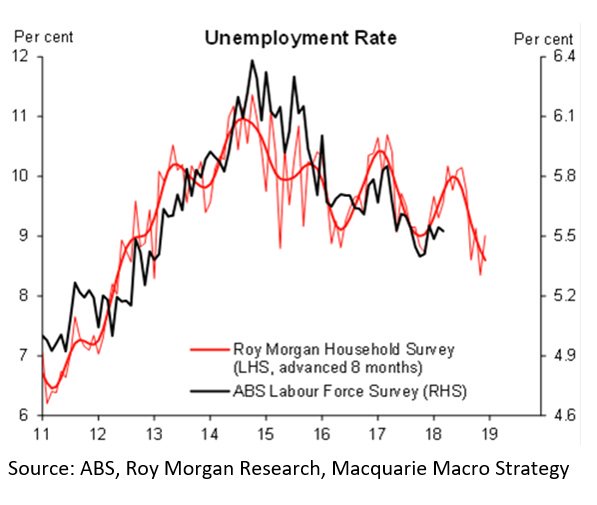

As you know we question the basis of the employment calculations, as even working for an hour or two takes people out of the count. The Roy Morgan alternative basis of calculation shows a much higher, and rising rate. This chart from Macquarie shows that there is a lagged relationship between the official figures and the Roy Morgan trends, and if this is true, then the unemployment rate is set to rise for the next few months.

Overall, even if the pace of job creation picks up again in the coming months, the excess slack and other structural forces are likely to prevent wage growth from increasing much above its current rate of 2.1% this year. This will continue to weigh on household spending and house prices and hamper the recovery.

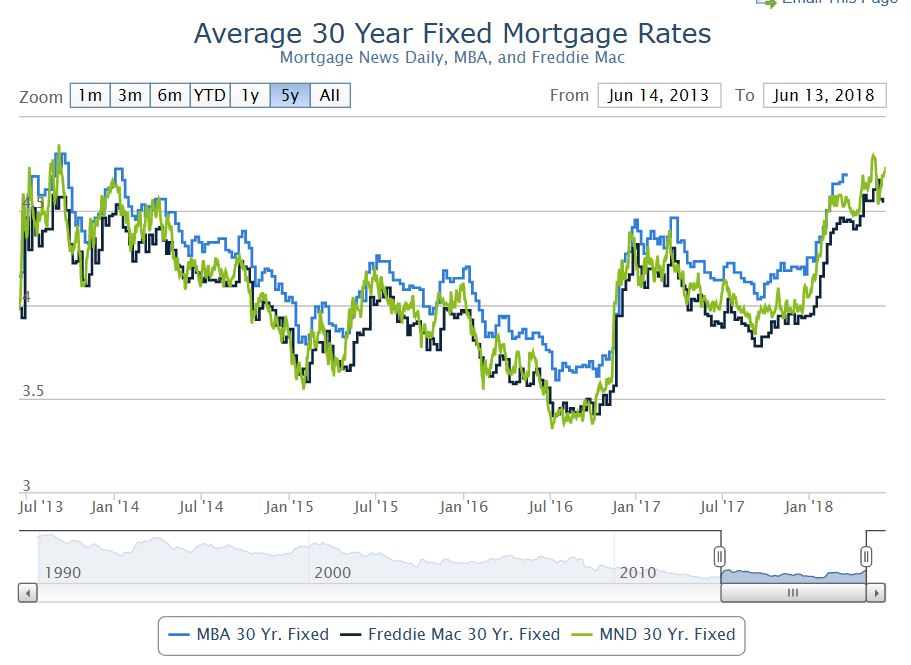

This probably puts an RBA inspired rate hike further down the track, but the US rate hike overnight means that there will be more pressure on international capital markets. The bond market moved higher. Specifically, a few of the Fed members who’d been holding out for slightly lower rates in 2018 moved their forecasts up enough to increase the odds of a 4th rate hike by December. This was already a strong possibility, but before today, those in the “3 hike” camp had a stronger case.

The FED said that in May the labor market has continued to strengthen and that economic activity has been rising at a solid rate. Job gains have been strong, on average, in recent months, and the unemployment rate has declined.

In fact the May 2018 figure has a three in front of it, a significantly lower number than our own, even allowing for a different basis of calculation.

The FED says …recent data suggest that growth of household spending has picked up, while business fixed investment has continued to grow strongly. On a 12-month basis, both overall inflation and inflation for items other than food and energy have moved close to 2 percent. Indicators of longer-term inflation expectations are little changed, on balance.

In view of realized and expected labor market conditions and inflation, the Committee decided to raise the target range for the federal funds rate to 1.75 to 2 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

But the kicker is probably another 2 hikes later in the year. US Mortgage Rates were higher again.

Watch for higher BBSW rates, which will be a harbinger of higher mortgage rates in Australia, despite the Reserve Bank and higher unemployment in the local market.

The employment and wage data from the ABS last week was not flash, with job growth momentum easing, unemployment higher and wages growth continuing at glacial speed.

So its worth asking what is really going on under the hood. To do that we have looked at ABS data over the last decade to drill into the detail. And frankly its not pretty.

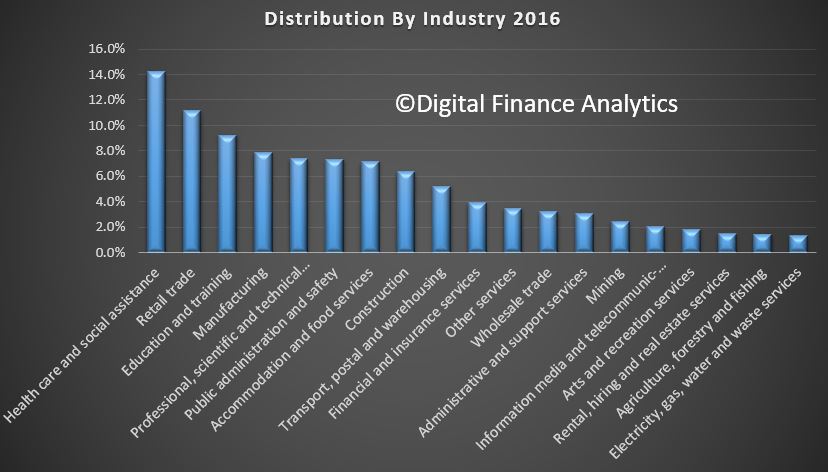

First we looked at employment across the industry sectors. Health care leads the way now at 14.2%, in terms of the number of people employed, followed by retail at 11.1%, education and training at 9.2% and manufacturing at 7.9%. For comparison purposes, about 12 % of the U.S. workforce is employed in the health care sector.

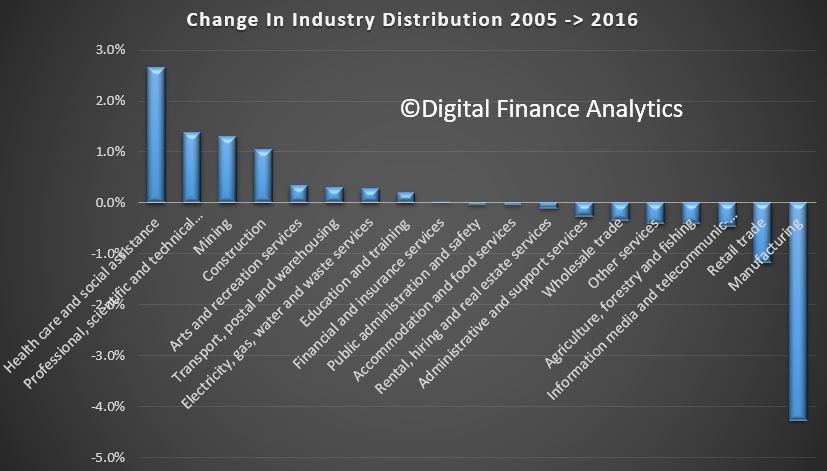

Then we compared the relative distribution by industry groups now, and back in 2005. Over that decade or so there has been a considerable shift in industry distribution.

The fastest growing sector in Health care, which have expanded relatively by 2.7%. The next largest growth sector was Professional and Technical Services at 1.4% and Mining at 1.3%. Construction grew relatively by 1.1%. At the other end of the spectrum, Manufacturing fell by a massive 4.3%, followed by Retail down 1.2% and information technology and media down 0.5%.

Or in other words, relativity more people are working in the health care sector than a decade ago. Drilling further into the data we also see a significant rise in the number of females working in this sector, as well as significant growth in part-time employment in the sector.

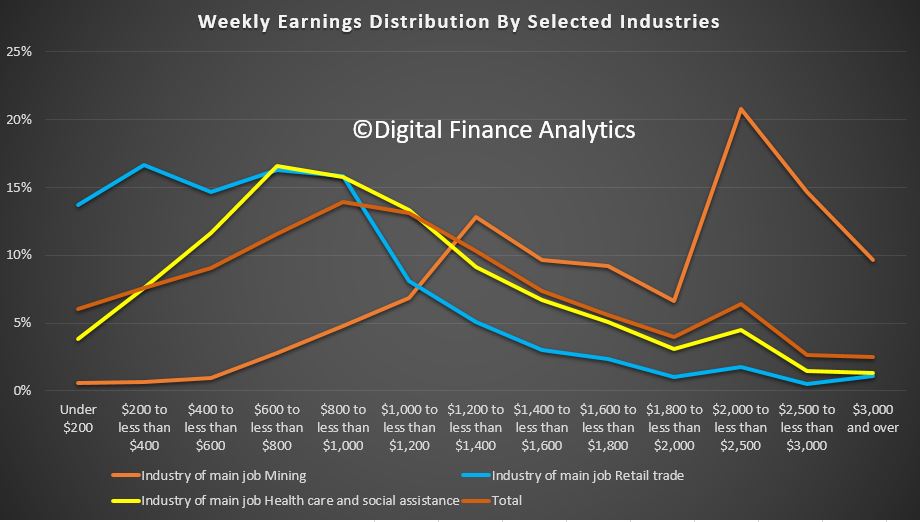

The final piece of analysis looks at relative weekly income across specific industry sectors. More than half of all people working in retail earn less than $600 a week. More than half of people in the healthcare sector earn less than $800 a week. Half the average of all industry sectors earns less than $1,000 a week, whilst half of those in the resource and mining sector earn more than $1,800 a week. So Retail and Health care sectors are intrinsically low paid.

Now lets put that together. All this goes some way to explain the shifts in employment and income. The health care sector has been an important generator of jobs in recent years, and health care is expected to continue to expand employment in coming years, but the jobs will continue to shift to low-paying support occupations reflecting changing demographics and greater demand. About 40 percent of the sector’s workers are not directly involved in treating a patient; instead, they work in jobs such as office or administrative work and food preparation. Others are working in health support occupations like home care and personal assistance. These jobs are paid significant less than care practitioners.

But, the health care sector is more labour intensive than other sectors, such as manufacturing, and this translates into a relatively lower share of output. So growth in health care does not guarantee broad-based prosperity because beyond the high pay of health care practitioners, the health care jobs in highest demand pay lower-than-average wages.

In fact the truth is the growth in jobs are in sectors which are service industries, and these to not really create new value, they simply circulate money in the system , perhaps from superannuation savings to pay for medical care.

Thus the growth in jobs in not assisting overall economic growth, and the lower average wages is depressing overall wage growth. Workers in the health care sector are also less likely to press hard for pay rises.

So the bottom line is we have a structural problem in the economy, where more people are doing important work helping those needing health care assistance, but the overall economic contribution impact is net negative, hence the low GDP growth and wages growth. Or in other words, more jobs are not necessarily good or well paid jobs. And that’s a structural problem, given the current demographic shifts. Welcome to the bed pan economy.

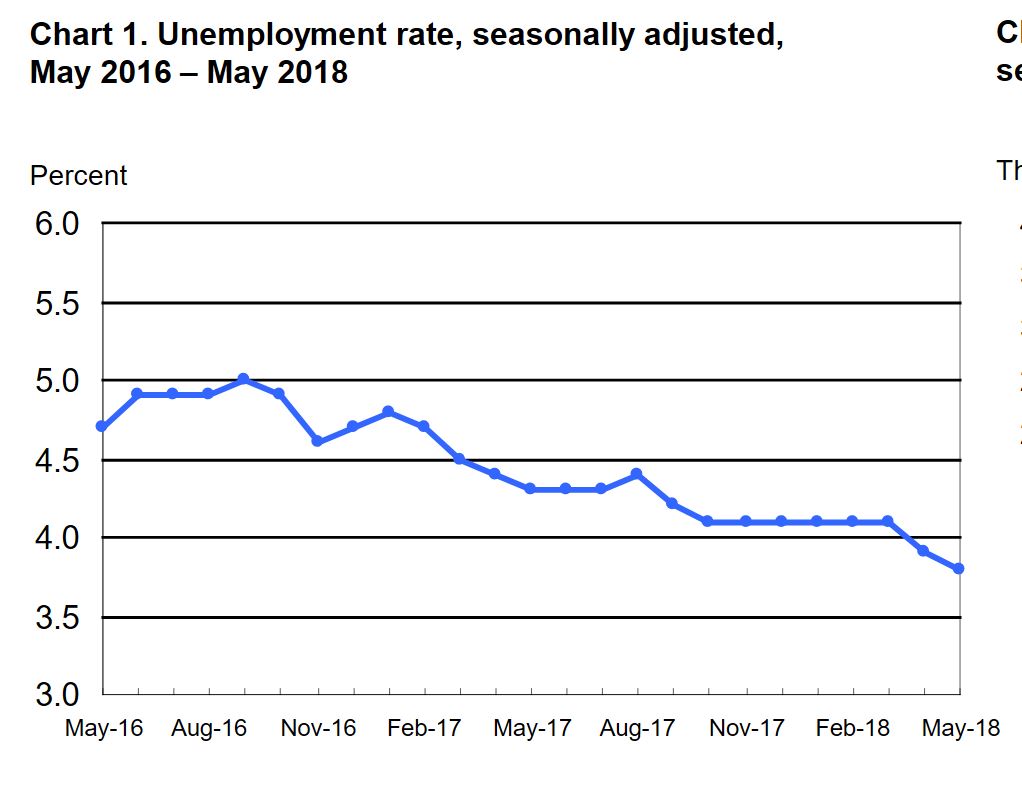

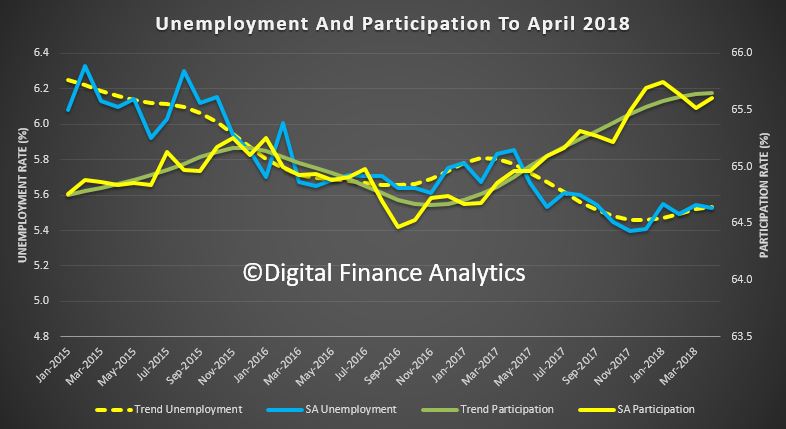

The latest data from the ABS covers April 2018 employment. The trend unemployment rate rose from 5.53 per cent to 5.54 per cent in April 2018 after the March figure was revised down, while the seasonally adjusted unemployment rate increased 0.1 percentage points to 5.6 per cent. In fact employment growth is stalling.

The trend participation rate increased to a further record high of 65.7 per cent in April 2018 and in line with the increasing participation rate, employment increased by around 14,000 with part-time employment increasing by 8,000 persons and full-time employment by 6,000 persons in April 2018. This continued the recent slowing of employment growth, particularly full-time employment growth. and the seasonally adjusted labour force participation rate increased slightly to 65.6 per cent.

Over the past year, trend employment increased by 355,000 persons or 2.9 per cent, which was above the average year-on-year growth over the past 20 years (2.0 per cent).

The trend hours worked increased by 4.7 million hours or 0.3 per cent in April 2018 and by 3.3 per cent over the past year.

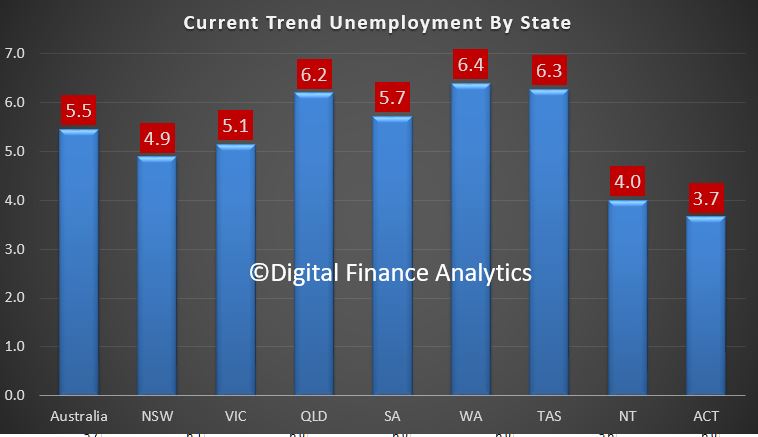

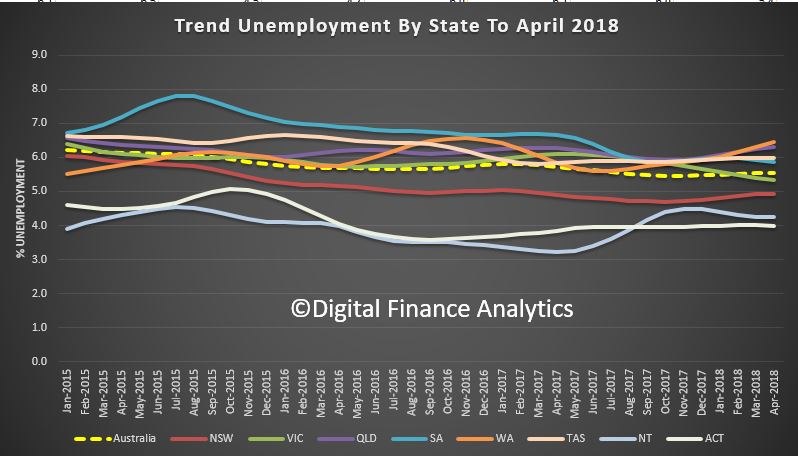

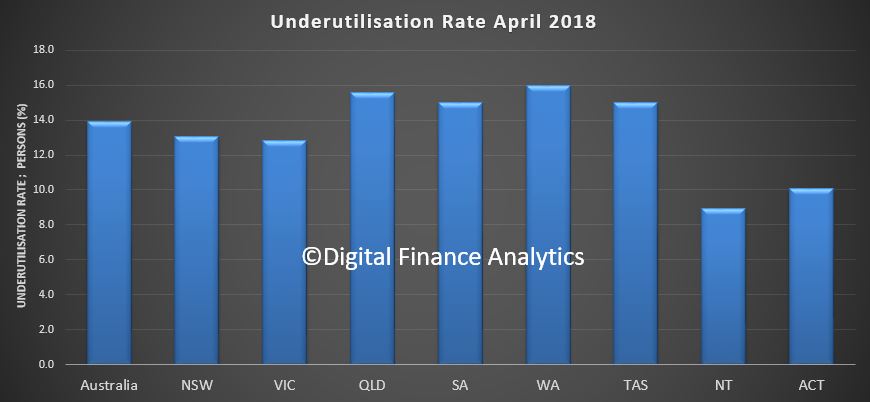

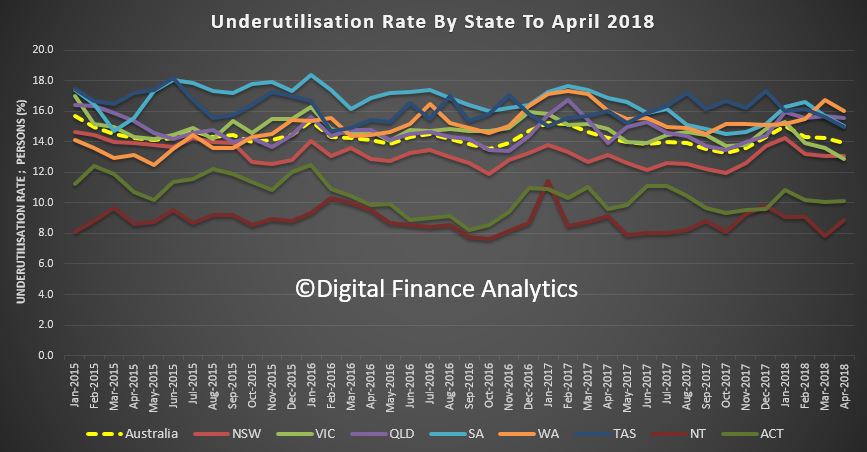

Over the past year, the states and territories with the strongest annual growth in trend employment were New South Wales (3.8 per cent), Queensland (3.5 per cent) and the Australian Capital Territory (2.7 per cent). But unemployment is highest in WA at 6.4 per cent, QLD 6.3 per cent, TAS 6.0 per cent and SA at 5.9 per cent.

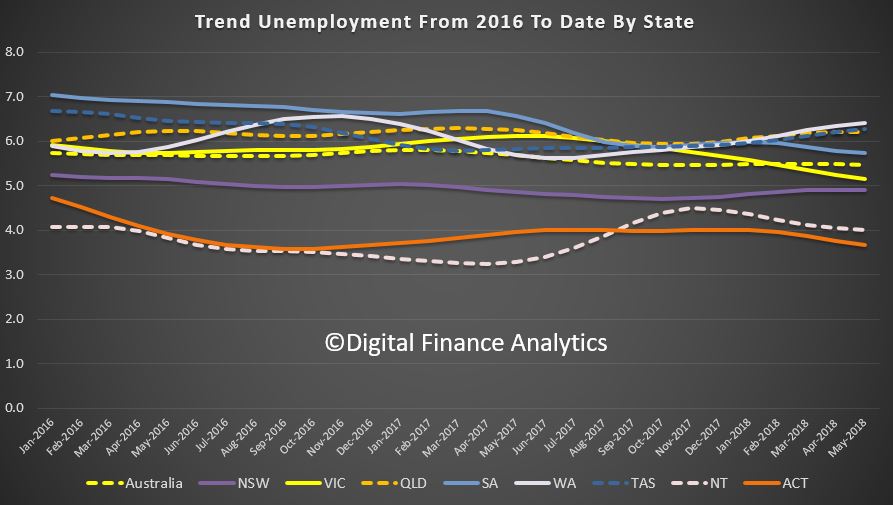

The critical perspective is looking at underutilisation – or those in work who want more work. This is essentially unused space capacity. The latest data for April shows the highest rate of underutilisation resides in WA (where unemployment is also highest). TAS and SA are also quite high, while VIC and ACT have the lowest rates.

And the trends really have hardly improved at all, taking account of seasonal variations.

It is this underutilisation which explains the relatively how unemployed number, and the low wage growth we discussed yesterday.

Finally, it is worth noting that as the ABS shift their samples, as they do each quarter, there is some variability in the baseline data, which introduces statistical noise into the system.

But the bottom line is there is nothing here to suggest we are going to see unemployment falling below 5%, which many believe is the rate at which wages growth may start to trend higher.

We are trapped in a low growth, low wage, high underutilised situation, and there is no easy way out given the current economic settings.

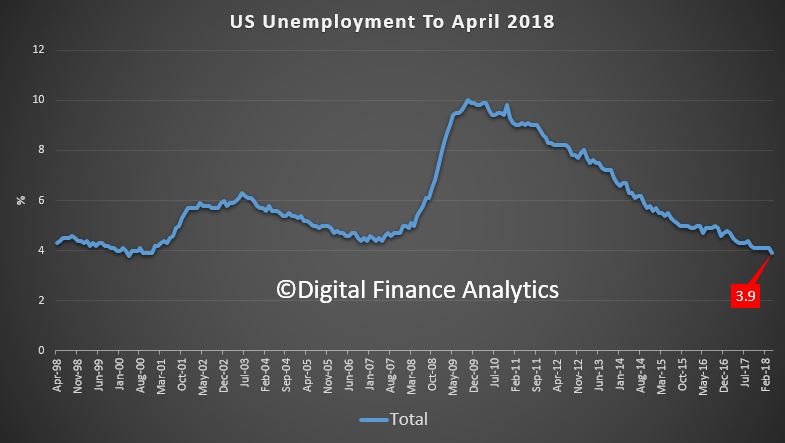

Total nonfarm payroll employment increased by 164,000 in April, and the unemployment rate edged down to 3.9 percent, the U.S. Bureau of Labor Statistics reported. This is the lowest number since 2000! Job gains occurred in professional and business services, manufacturing, health care, and mining.

The market reacted positively, with the lower number sitting in the “Goldilocks” zone meaning the FED’s programme of rate rises can continue as planned. Wages growth remains constrained, so inflation is controlled.

Household Survey Data

In April, the unemployment rate edged down to 3.9 percent, following 6 months at 4.1 percent. The number of unemployed persons, at 6.3 million, also edged down over the month. Among the major worker groups, the unemployment rate for adult women decreased to 3.5 percent in April. The jobless rates for adult men (3.7 percent), teenagers (12.9 percent), Whites (3.6 percent), Blacks (6.6 percent), Asians (2.8 percent), and Hispanics (4.8 percent) showed little or no change over the month.

Among the unemployed, the number of job losers and persons who completed temporary jobs declined by 188,000 in April to 3.0 million.

The number of long-term unemployed (those jobless for 27 weeks or more) was little changed at 1.3 million in April and accounted for 20.0 percent of the unemployed. Over the year, the number of long-term unemployed was down by 340,000.

Both the labor force participation rate, at 62.8 percent, and the employment-population ratio, at 60.3 percent, changed little in April.

The number of persons employed part time for economic reasons (sometimes referred to as involuntary part-time workers) was essentially unchanged at 5.0 million in April. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or because they were unable

to find full-time jobs.

In April, 1.4 million persons were marginally attached to the labor force, down by 172,000 from a year earlier. (The data are not seasonally adjusted.) These individuals were not in the labor force, wanted and were available for work, and had looked for a job sometime in the prior 12 months. They were not counted as unemployed because they had not searched for work in the 4 weeks preceding the survey.

Among the marginally attached, there were 408,000 discouraged workers in April, little changed from a year earlier. (The data are not seasonally adjusted.) Discouraged workers are persons not currently looking for work because they believe no jobs are available for them. The remaining 1.0 million persons marginally attached to the labor force in April had not searched for work for reasons such as school attendance or family responsibilities.

Establishment Survey Data

Total nonfarm payroll employment increased by 164,000 in April, compared with an average monthly gain of 191,000 over the prior 12 months. In April, job gains occurred in professional and business services, manufacturing, health care, and mining.

In April, employment in professional and business services increased by 54,000. Over the past 12 months, the industry has added 518,000 jobs.

Employment in manufacturing increased by 24,000 in April. Most of the gain was in the durable goods component, with machinery adding 8,000 jobs and employment in fabricated metal products continuing to trend up (+4,000). Manufacturing employment has risen by 245,000 over the year, with about three-fourths of the growth in durable goods industries.

Health care added 24,000 jobs in April and 305,000 jobs over the year. In April, employment rose in ambulatory health care services (+17,000) and hospitals (+8,000).

In April, employment in mining increased by 8,000, with most of the gain occurring in support activities for mining (+7,000). Since a recent low in October 2016, employment in mining has risen by 86,000.

Employment changed little over the month in other major industries, including construction, wholesale trade, retail trade, transportation and warehousing, information, financial activities, leisure and hospitality, and government.

The average workweek for all employees on private nonfarm payrolls was unchanged at 34.5 hours in April. In manufacturing, the workweek increased by 0.2 hour to 41.1 hours, while overtime edged up by 0.1 hour to 3.7 hours. The average workweek for production and nonsupervisory employees on private nonfarm payrolls increased by 0.1 hour to 33.8 hours.

In April, average hourly earnings for all employees on private nonfarm payrolls rose by 4 cents to $26.84. Over the year, average hourly earnings have increased by 67 cents, or 2.6 percent. Average hourly earnings of private-sector production and nonsupervisory employees increased by 5 cents to $22.51 in April.

The change in total nonfarm payroll employment for February was revised down from +326,000 to +324,000, and the change for March was revised up from +103,000 to +135,000. With these revisions, employment gains in February and March combined were 30,000 more than previously reported. (Monthly revisions result from additional reports received from businesses and government agencies since the last published estimates and from the recalculation of seasonal factors.) After revisions, job gains have averaged 208,000 over the last 3 months.