We look at the latest in the “repo” drama.

Blog")

/

RSS Feed

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

We look at the latest in the “repo” drama.

We look at the latest in the “repo” drama.

The news from the New York Federal Reserve indicates that the “one-off” spike in repo rates is more structural than many thought – many pundits blamed the timing of tax payments and the like.

But the latest tranches of both the term and overnight operations are now at $60 billion and $100 billion respectively. All up this is now ~$250 billion in funding, and counting. And the target rate is still on the high side, and the offers over subscribed.

If this continues then the Fed’s balance sheet will be growing again, and fast (remember when they were planning to shrink?).

In essence, more of the US economy will be supported by a larger FED, a larger and market distorting Fed to boot.

But the underlying question, still open, is, are these measures signs of a deeper malaise, signalling banks are not trusting some of their counter-parties? Without constant liquidity support will the markets fall over? And in the light of events over the past week plus, do the remarks from the Fed pass muster? We think not. This is significantly more serious than they admit.

According to the Fed, they will conduct another $75 billion worth of repurchase operations on Friday to help keep the federal funds rate within the target of 1 3/4 to 2.0 per cent. So things are still looking out of kilter – perhaps because of the Fed’s earlier balance sheet reduction?

In accordance with the FOMC Directive issued September 18, 2019, the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York will conduct an overnight repurchase agreement (repo) operation from 8:15 AM ET to 8:30 AM ET tomorrow, Friday, September 20, 2019, in order to help maintain the federal funds rate within the target range of 1-3/4 to 2 percent.

This repo operation will be conducted with Primary Dealers for up to an aggregate amount of $75 billion. Securities eligible as collateral in the repo include Treasury, agency debt, and agency mortgage-backed securities. Primary Dealers will be permitted to submit up to two propositions per security type. There will be a limit of $10 billion per proposition submitted in this operation. Propositions will be awarded based on their attractiveness relative to a benchmark rate for each collateral type, and are subject to a minimum bid rate of 1.80 percent.

We look at today’s data, the Fed cut, the repo issue, and locally the engineered balanced budget and higher unemployment. Many echos of a decade back, is history repeating?

We look at the latest data from the local economy, the recent FED rate cut and the issues surrounding repos. Is history trying to tell us something?

If today’s second consecutive repo was supposed to calm the stress in the secured lending market and ease the funding shortfall in the interbank market, it appears to have failed says Zerohedge.

As the WSJ said on Tuesday:

For the first time in more than a decade, the Federal Reserve injected cash into money markets Tuesday to pull down interest rates and said it would do so again Wednesday after technical factors led to a sudden shortfall of cash.

The pressures relate to shortages of funds banks face resulting from an increase in federal borrowing and the central bank’s decision to shrink the size of its securities holdings in recent years. It reduced these holdings by not buying new ones when they matured, effectively taking money out of the financial system.

Bloomberg said while the spike wasn’t evidence of any sort of imminent financial crisis, it highlighted how the Fed was losing control over short-term lending, one of its key tools for implementing monetary policy. It also indicated Wall Street is struggling to absorb record sales of Treasury debt to fund a swelling U.S. budget deficit. What’s more, many dealers have curtailed trading because of safeguards implemented after the 2008 crisis, making these markets more prone to volatility.

And Bloomberg today signals more intervention ahead.

The Federal Reserve made crystal clear that it doesn’t want U.S. money market rates to spike again like they did early this week, announcing it will — for the third day in a row — inject cash into this vital corner of finance.

On Thursday, the New York Fed will offer up to $75 billion in a so-called overnight repurchase agreement operation, adding another dose of temporary liquidity to restore order in the banking system. It made the same offer Tuesday and Wednesday, deploying a tool it hadn’t used in a decade. This latest action follows the Fed’s reduction in the interest rate on excess reserves, or IOER, another attempt to quell money-market stresses.

The prior operations have calmed markets, with repo rates declining Wednesday to more normal levels after jumping to 10% on Tuesday, four times where it was last week.

In addition, as Credit Swiss points out, Basel changed the rules:

The longer term issue is that the definition of “excess reserves” has changed in a Basel III environment. Previously excess reserves were defined by the Fed’s standard. If banks held more in the Federal Reserve accounts than they needed to settle transactions with one another, they had excess reserves. Now, under Basel III, excess reserves are defined by a global standard. Banks not only need enough reserves to settle accounts with one another at the end of each day – they also need to hold enough reserves for liquidity and capital buffer purposes. Indeed, reserves are better “high quality liquid assets” (HQLA) than even US Treasuries. In this context, at the beginning of 2017 (when Basel III really kicked in), banks found themselves with excess reserves by Fed standards, but deficient reserves by Basel III standards. Making matters worse for a little while were the Fed’s balance sheet reduction efforts, draining reserves from the system

This could be a signal of a potential liquidity crisis (echoes of 2007?).

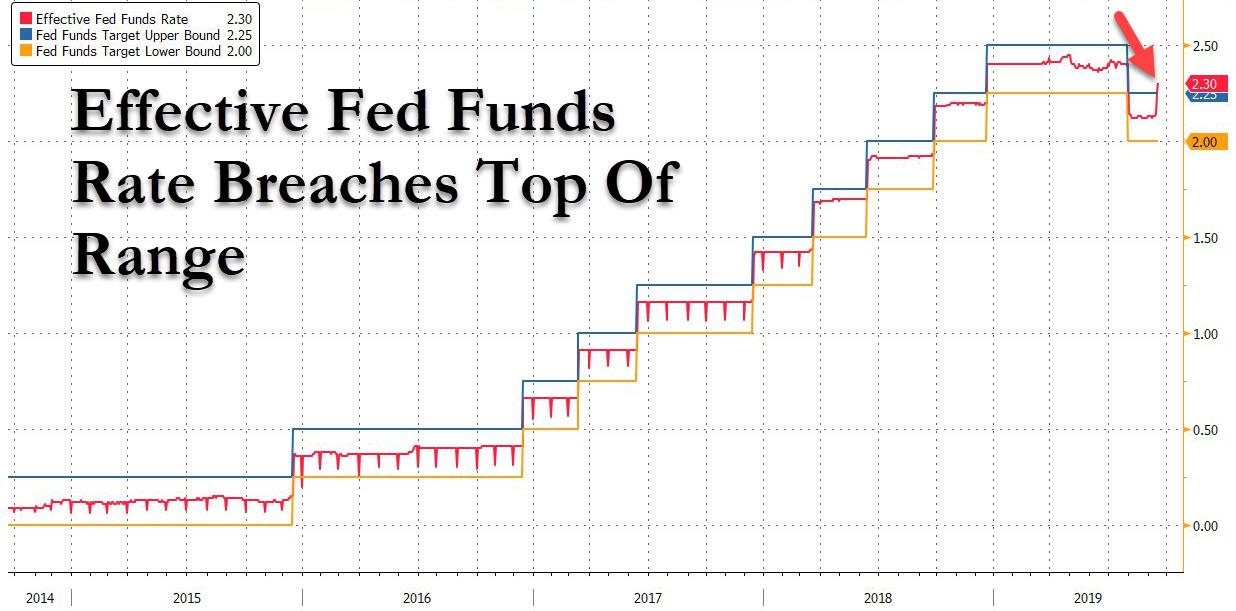

Zerohedge says not only did O/N general collateral print at 2.25-2.60% after the repo operation, confirming that repo rates remain inexplicably elevated even though everyone who had funding needs supposedly met them thanks to the Fed, but in a more troubling development, the Effective Fed Funds rate printed at 2.30% at 9am this morning, breaching the Fed’s target range of 2.00%-2.25% for the first time.

And yes, it is quite ironic that on the day the Fed is cutting rates, the Fed Funds was just “pushed” above the top end of the target range for the first time ever.

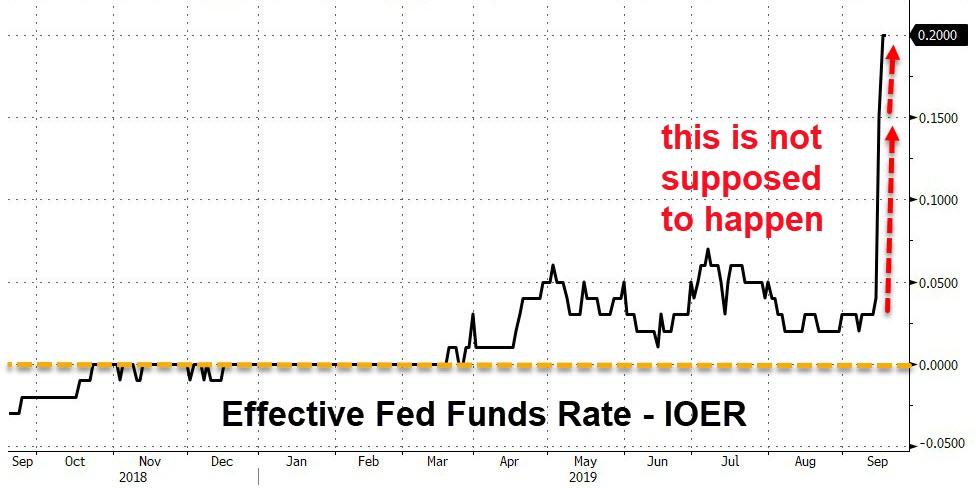

This also means that the EFF-IOER spread has now blown out to an unprecedented 20bps, yet another indication that the Fed has lost control of the rates corridor.

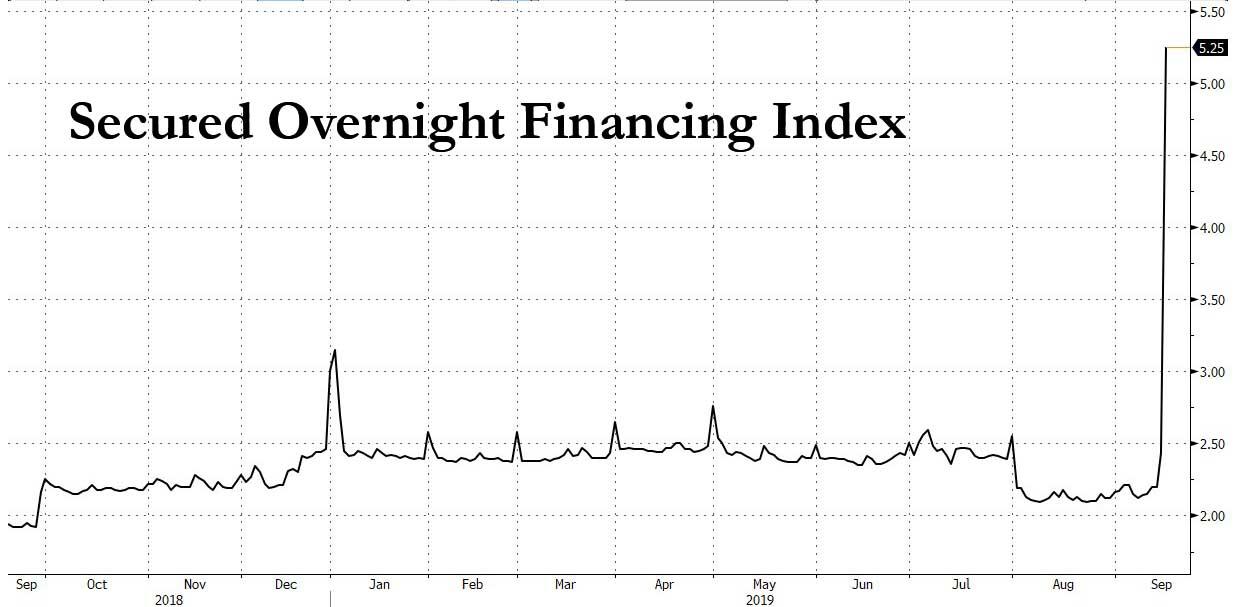

But in what may be the most concerning move, today’s print for the Secured Overnight Financing Index (SOFR), which is widely expected to be Libor’s replacement, exploded higher by 282bps to a record 5.25%.

Commenting on the blow out in the SOFR, Goldman had this to say on the “extremely volatile” price action in the key funding index:

The SOFR market saw extremely volatile price action over the course of the day…. Almost 20k in SERU9 blocks printed from 11:15am through the afternoon, pushing SERFFU9 from -10 to -21.5. Shortly after 4pm the market was given another jolt of adrenaline as news of a second Fed operation to be conducted tomorrow morning at 8:15am caused the spot-6mo curve to go bid into the close.

The problem here is that since SOFR is expected to replace LIBOR as the reference rate for several hundred trillions in fixed income securities, a spike such as this one would be perfectly sufficient to wreak havoc across market if indeed it had been the key reference rate.

Finally, courtesy of BMO’s Jon Hill, here is some commentary on today’s oversubscribed, and clearly insufficient, repo operation by the Fed:

Today’s emergency repo operation was oversubscribed with $51.6 bn in Treasury and $22.8 bn in MBS collateral accepted. The weighted average in USTs was 2.215%, with a high rate of 2.36% and a low of 2.10%. This should help alleviate some stress in USD funding markets, and the fact that it’s occurring earlier in the morning than Tuesday should help keep daily averages more subdued than yesterday – SOFR printed at a remarkable 5.25% (a stunning 282 bp spike) with fed funds still unknown but scheduled to be released at 9:00 AM ET and likely to print outside of the target range.

If Powell is successful at guiding the market toward assuming a mid-cycle adjustment, one specific repricing that will occur is in 2020 forwards, which are still factoring in one and a half 25 bp cuts next year as shown in the attached (admittedly, precision here is difficult due to the illiquidity of the Jan ’21 contract). This contrasts with the FOMC’s desire to execute a more modest drop in overnight rates and the price response here will be a focal point in determining how markets are responding to the impending Fed communication. If Powell is effective, look for that area of the curve to steepen sharply.

The Fed chair Jerome Powell said after the decision ” We don’t see a recession, we’re not expecting a recession, but are are making monetary policy more accommodative”, saying it is a mistake to hold onto your firepower until a downturn has gathered moment. This was seen by the market as “hawkish”, much to Trump’s annoyance! The US dollar was stronger after the announcement.

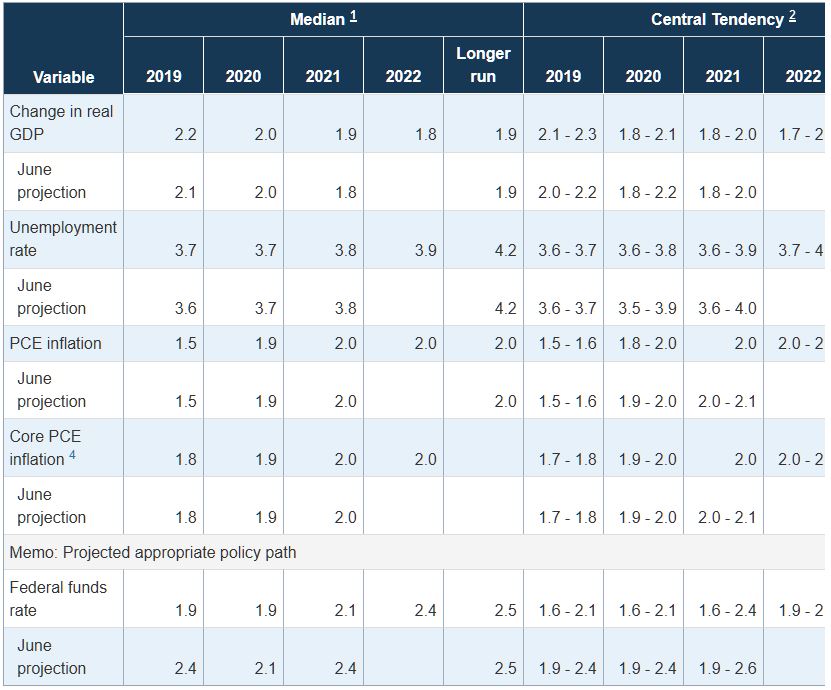

Information received since the Federal Open Market Committee met in July indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although household spending has been rising at a strong pace, business fixed investment and exports have weakened. On a 12-month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In light of the implications of global developments for the economic outlook as well as muted inflation pressures, the Committee decided to lower the target range for the federal funds rate to 1-3/4 to 2 percent. This action supports the Committee’s view that sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes, but uncertainties about this outlook remain. As the Committee contemplates the future path of the target range for the federal funds rate, it will continue to monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair, John C. Williams, Vice Chair; Michelle W. Bowman; Lael Brainard; Richard H. Clarida; Charles L. Evans; and Randal K. Quarles. Voting against the action were James Bullard, who preferred at this meeting to lower the target range for the federal funds rate to 1-1/2 to 1-3/4 percent; and Esther L. George and Eric S. Rosengren, who preferred to maintain the target range at 2 percent to 2-1/4 percent.

The accompanying data flags lower rates ahead.

We consider the point in the economic cycle we are in, given the Fed’s move last week. Meantime, in Australia, how close to the brink are we now?

We consider the point in the economic cycle we are in, given the Fed’s move last week. Meantime, in Australia, how close to the brink are we now?