Real US gross domestic product increased at an annual rate of 3.5 percent in the third quarter of 2016, according to the “third” estimate released by the Bureau of Economic Analysis. In the second quarter, real GDP increased 1.4 percent.

The GDP estimate released today is based on more complete source data than were available for the “second” estimate issued last month. In the second estimate, the increase in real GDP was 3.2 percent. With this third estimate for the third quarter, nonresidential fixed investment, personal consumption expenditures (PCE), and state and local government spending increased more than previously estimated, but the general picture of economic growth remains the same.

Real gross domestic income (GDI) increased 4.8 percent in the third quarter, compared with an increase of 0.7 percent in the second. The average of real GDP and real GDI, a supplemental measure of U.S. economic activity that equally weights GDP and GDI, increased 4.1 percent in the third quarter, compared with an increase of 1.1 percent in the second.

The increase in real GDP in the third quarter primarily reflected positive contributions from PCE, exports, private inventory investment, nonresidential fixed investment, and federal government spending that were partly offset by negative contributions from residential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.

The acceleration in real GDP in the third quarter primarily reflected an upturn in private inventory investment, an acceleration in exports, a smaller decrease in state and local government spending, an upturn in federal government spending, and a smaller decrease in residential investment, that were partly offset by a smaller increase in PCE and an acceleration in imports.

Current-dollar GDP increased 5.0 percent, or $225.2 billion, in the third quarter to a level of $18,675.3 billion. In the second quarter, current dollar GDP increased 3.7 percent, or $168.5 billion.

The price index for gross domestic purchases increased 1.5 percent in the third quarter, compared with an increase of 2.1 percent in the second quarter (table 4). The PCE price index increased 1.5 percent, compared with an increase of 2.0 ercent. Excluding food and energy prices, the PCE price index increased 1.7 percent, compared with an increase of 1.8 percent.

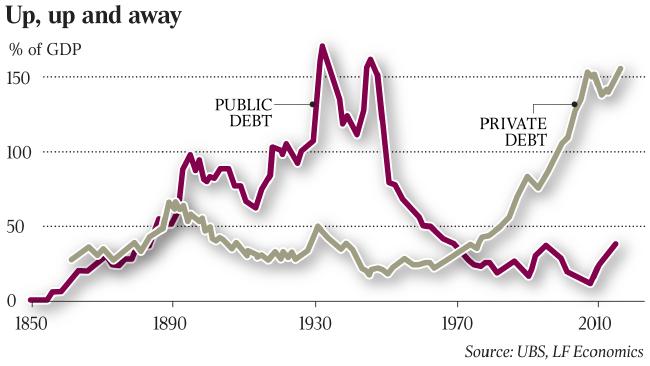

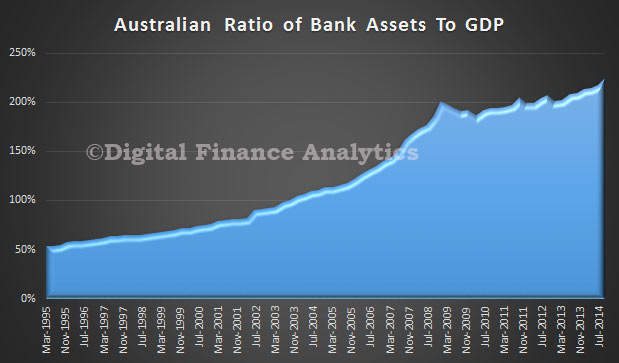

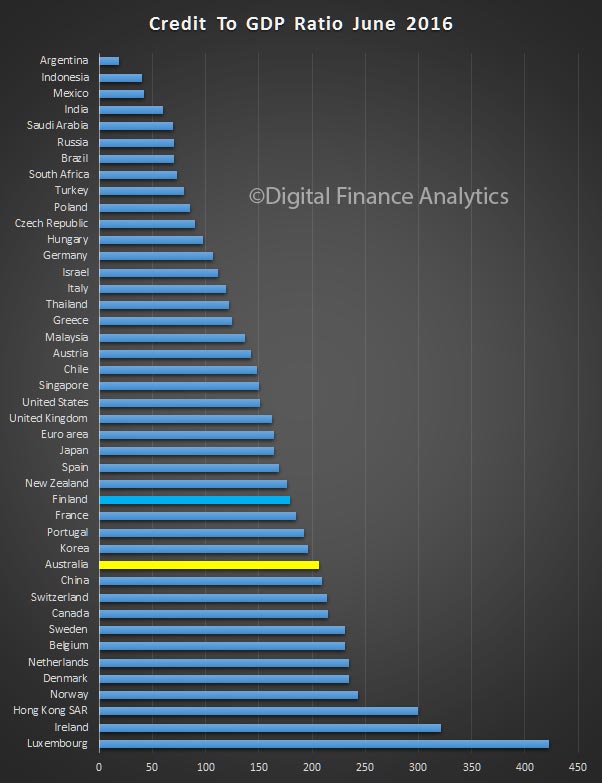

The BIS says

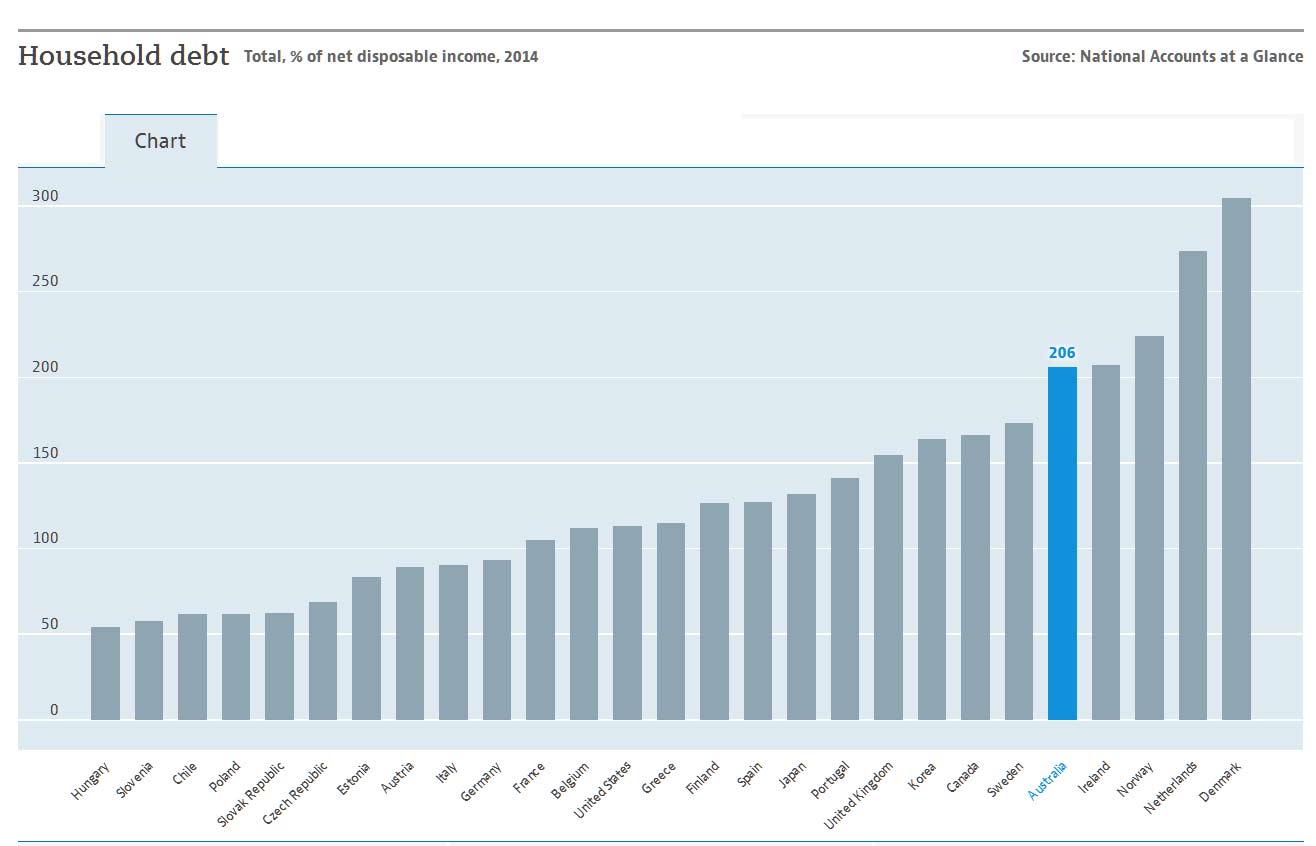

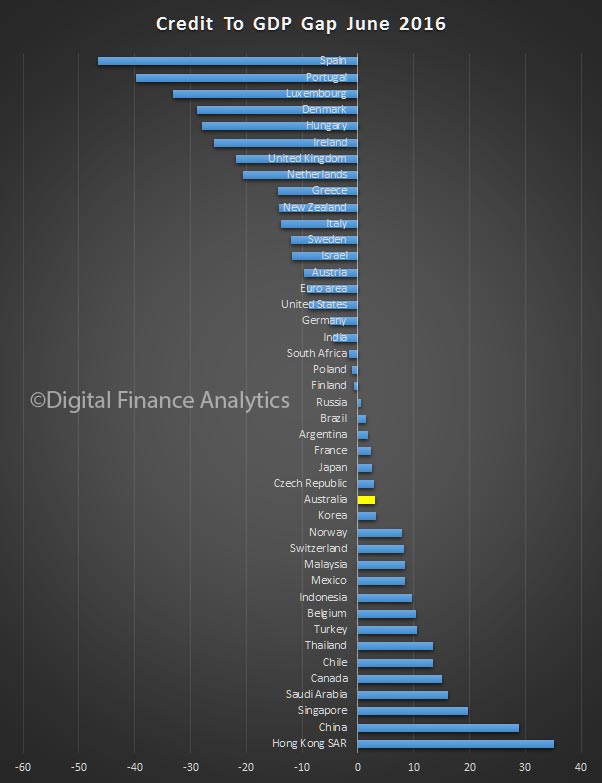

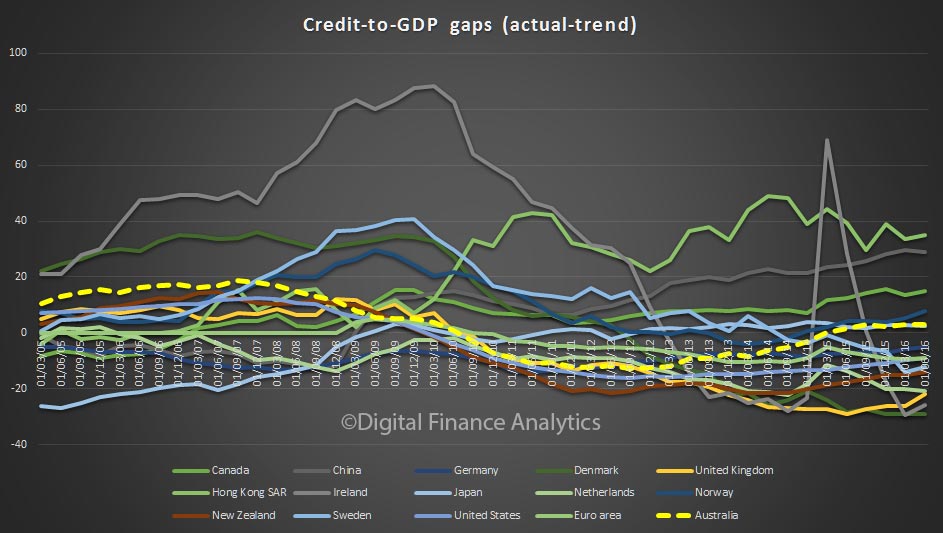

The BIS says