No free lunch: higher super means lower wages uses

administrative data on 80,000 federal workplace agreements made between

1991 and 2018 to show that about 80 per cent of the cost of increases

in super is passed to workers through lower wage rises within the life

of an enterprise agreement, typically 2-to-3 years. And the longer-term

impact is likely to be even higher.

‘This trade-off between more

superannuation in retirement but lower living standards while working

isn’t worth it for most Australians,’ says the lead author, Grattan’s

Household Finances Program Director, Brendan Coates.

‘This new empirical analysis reinforces

that the planned increase in compulsory super, from 9.5 per cent now to

12 per cent July 2025, should be abandoned. Most Australians are already

saving enough for their retirement.’

The paper directly measures the

super-wages trade-off for nearly a third of Australian workers – those

on federal enterprise agreements. But it shows that other workers are

also likely to bear the cost of higher compulsory super in the form of

lower wages growth.

Despite the claims of some in the

superannuation industry, it is unlikely that future super increases will

be different from past increases.

It’s true that wages growth has slowed in

recent years, but nominal wages are still growing by more than 2 per

cent a year, so employers have plenty of scope to slow the pace of wages

growth if compulsory super contributions are increased.

And none of the plausible explanations for

lower wages growth – whether slower growth in productivity,

technological change, globalisation, an under-performing economy, or

weaker bargaining power among workers – helps explain why employers

would foot any more of the bill for higher compulsory super this time

around.

If employers aren’t willing to offer large

pay rises today, it’s hard to imagine why they would pay for higher

super. In fact, if workers’ bargaining power has fallen, employers are

even less likely to pay for higher compulsory super than in the past.

Grattan’s 2018 report, Money in retirement: more than enough, found that the conventional wisdom that Australians don’t save enough for retirement is wrong.

Now this working paper finds that the conventional wisdom that higher super means lower wages is right.

‘Together, these findings demand a rethink of Australia’s retirement incomes system,’ Mr Coates says.

As we come to the end of 2019, you’d be forgiven for being confused about the health of the economy. Via The Conversation.

Treasurer Josh Frydenberg regularly points

out that jobs growth is strong, the budget is heading back to surplus,

and Australia’s GDP growth is high by international standards.

The opposition points to sluggish wages growth, weak consumer spending and weak business investment.

Monday’s Mid-Year Economic and Fiscal

Outlook (MYEFO) provides an opportunity for a pre-Christmas stock-take

of treasury’s thinking.

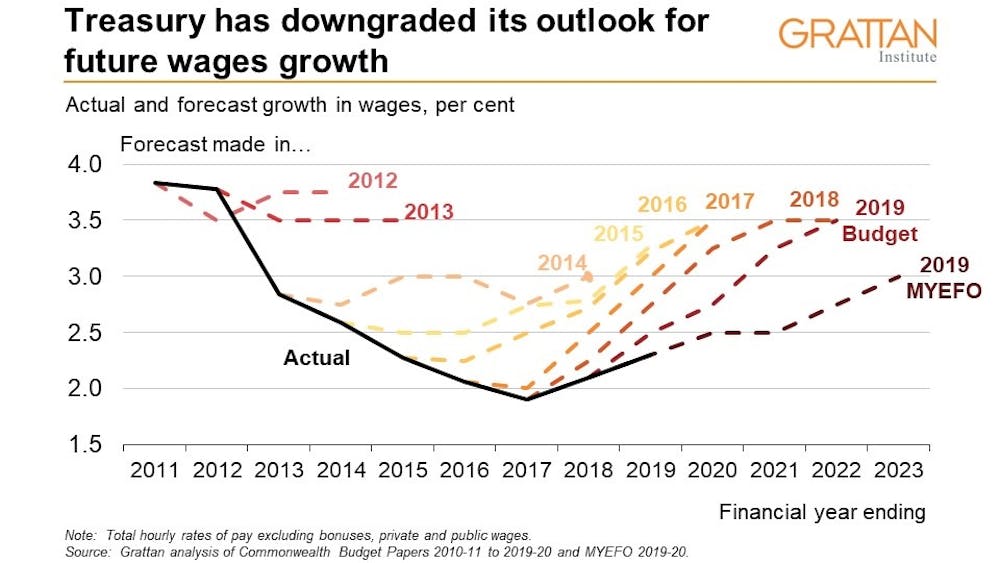

1. Low wage growth is the new normal

Rightly grabbing the headlines is yet another downgrade to wage growth.

In the April budget, wages were forecast to grow this financial year by 2.75%. In MYEFO, the figure has been cut to 2.5%.

Three years ago, when Scott Morrison was treasurer, the forecast for this year was 3.5%.

Each time wages forecasts missed, treasury assumed future growth would be even higher, to restore the long-term trend.

Today’s MYEFO is a long-overdue admission

from treasury that labour market dynamics have shifted – in other words,

lower wage growth is the “new normal”.

Even by 2022-23, wages are projected to

grow at only 3% (and even that would still be a substantial turnaround

compared to today).

Of course, wages are still rising in real terms (that is, faster than inflation), a fact Finance Minister Mathias Cormann is keen to emphasise.

But Australians will have to adjust to a world of only modest growth in their living standards for the next few years.

2. Economic growth is underwhelming, especially per person

Economic growth forecasts have received a pre-Christmas trim.

Treasury now expects the economy to grow by 2.25% this financial year, down from the 2.75% it expected in April.

Particularly striking is the sluggishness

of the private economy, with consumer spending expected to grow by just

1.75%, despite interest rate and tax cuts, and business investment

idling at growth of 1.5%, down from the 5% forecast in April.

The longer term picture looks somewhat

better, with growth forecast to rise to 2.75% in 2020-21 and 3% in

2021-22, although treasury acknowledges there are significant downside

risks, particularly from the global economy.

The government has made much of the fact

our economy is strong compared to many other developed nations. But much

more relevant to people’s living standards is per-person growth.

Australia’s international podium finish looks less impressive once you

account for the fact Australia’s population is growing at 1.7%.

As one perceptive commentator

has noted, while Australia is forecast to be the fastest growing of the

12 largest advanced economies next year, it is expected to be the slowest in per-person terms.

3. The government is at odds with the Reserve Bank

You can imagine the government’s

collective sigh of relief that it is still on track to deliver a surplus

in 2019-20, albeit a skinny A$5 billion instead of the the $7 billion

previously forecast.

Given the treasurer declared victory early

by announcing the budget was “back in the black” in April, missing

would have been awkward, to say the least.

And another three years of slim surpluses are forecast ($6 billion, $8 billion and $4 billion respectively).

The real issue for the treasurer is how to

deal with the growing calls for more economic stimulus, including from

the Reserve Bank.

Depending on what happens to growth and

unemployment in the first half of 2020, he will come under increased

pressure to jettison the future surpluses to support jobs and living

standards.

4. High commodity prices are a gift for the bottom line

High commodity prices are the gift that keeps on giving for the Australian budget.

Iron ore prices in excess of US$85 per

tonne, well above the US$55 per tonne budgeted for, have helped to keep

company tax receipts buoyant.

Treasury is maintaining the conservative approach it has taken in recent years by continuing to assume US$55 per tonne.

This provides some potential upside should

prices stay high – Treasury estimates a US$10 per tonne increase would

boost the underlying cash balance by about A$1.2 billion in 2019-20 and

about A$3.7 billion in 2020-21.

The budget bottom line remains tied to the whims of international commodity markets for the near future.

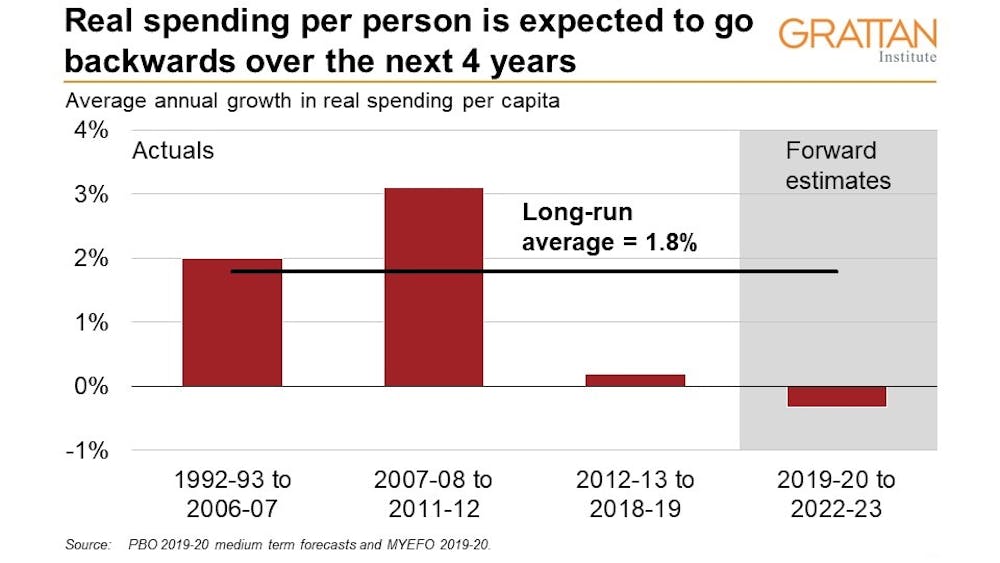

5. The surplus depends on running a (very) tight ship

The forecast surpluses over the next four years are premised on an extraordinary degree of spending restraint.

This government is expecting to do

something no government has done since the late-1980s: cut spending in

real per-person terms over four consecutive years.

The budget dynamics are helping. Budget

surpluses and low interest rates reduce debt payments, and low inflation

and wage growth reduce the costs of payments such as the pension and

Newstart.

But the government is also expecting to

keep growth low in other areas of spending, in almost every area other

than defence and the expanding national disability insurance scheme.

As the Parliamentary Budget Office points out, it is hard to keep holding down spending as the budget improves.

It is even more true while long term

spending squeezes on things such as Newstart and aged care are hurting

vulnerable Australians.

Where does it leave us?

The real lesson from MYEFO is that

Australians are right to be confused: there is a disconnect between the

health of the budget and the health of the economy.

MYEFO suggests both that the government is

on track to deliver a good-news budget surplus underpinned by high

commodity prices and jobs growth, and that the economy is in the

doldrums with low wage growth in place for a long time.

Top of Frydenberg’s 2020 to do list: how to reconcile the two.

Authors: Danielle Wood, Program Director, Budget Policy and Institutional Reform, Grattan Institute; Kate Griffiths, Senior Associate, Grattan Institute

The Grattan Institute published an interesting article in The Conversation. They argue that Labor’s policies are more likely to impact housing affordability than The Coalition. But right at the end of the article, they still preach lack of supply is the problem. This is not the case.

First, we have more than 1 million vacant properties in Australia, according to the last census. Just walk around some of the high-rise areas of an evening and see the darkened dwellings.

Next, the ABS shows the number of people per household has not changed in more than 20 years, you would expect this to change if supply was a problem.

Third there are more than 200,000 units under construction, and more to come (developers are panicking as sales drop off). Much of the demand from investors has left the scene as prices fell and regulation tightened,

Finally, the migration myth needs to be considered as many coming into the country come as part of a family unit, so the actual demand from migration is significantly lower than the generally quoted 300,000. Average family say 2.5 means close to a third less, of whom some will live with existing relatives.

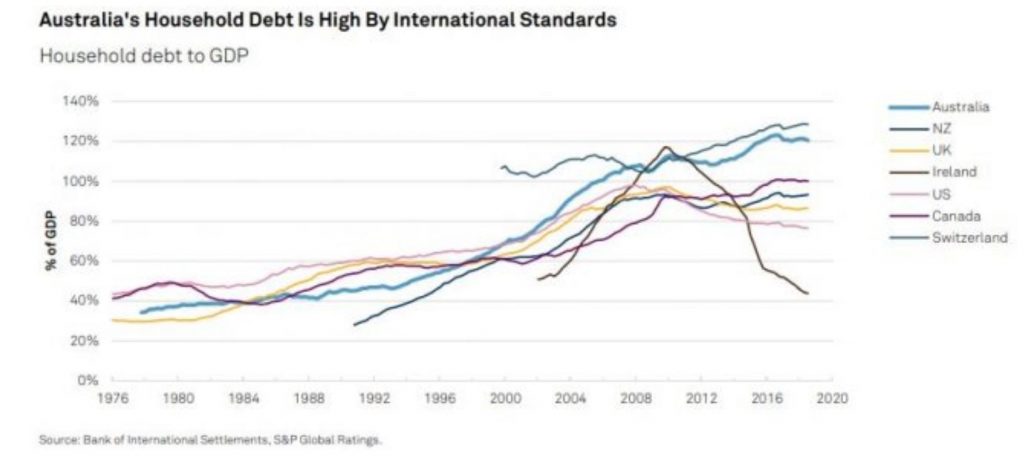

The debt machine has been used to bloat the economy, bank balance sheets and home prices, and that is now (rightly) unwinding. The wealth effect is now in reverse. The choice is between letting the debt continue to fall, and home prices will follow, easing affordability later, or reinflating the debt, and make the problem even worse. Remember we have the second highest household debt to GDP ratio in the world.

Neither party has discussed the debt bomb, the impact of over-lending, and the necessary correction. Rather they play at the edges.

That said, here is the article, which is still worth reading!

On housing, the contrast between the two major parties couldn’t be clearer.

The Coalition is still pretending that you can help first homebuyers without hurting anyone. Labor isn’t.

This matters, because Australian governments have been pretending

for decades that there are easy and costless ways to make housing more

affordable. And over that time the problems have become worse.

The Coalition’s First Home Loan Deposit Scheme is the latest plan that is supposed to arrest the decline in home ownership among younger Australians.

The Coalition’s First Home Deposit Scheme

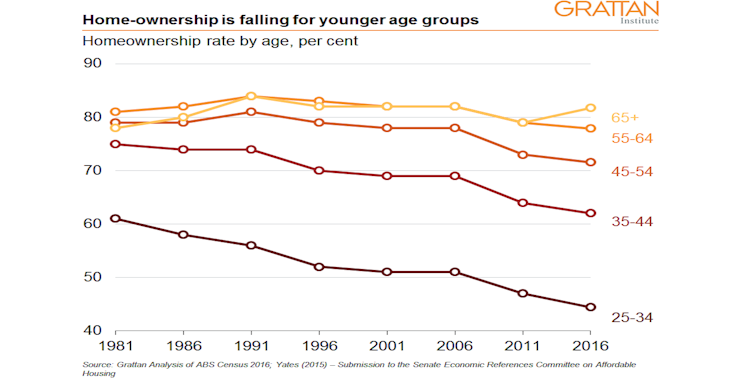

Housing costs are a big problem for young people. Home ownership is falling fast

in Australia, especially among the young and poor. Fewer than half of

25-34 year olds own their home today. Home ownership among the poorest

20% of that age group has fallen from 63% in 1981 to 23% today. At this

rate almost half of retirees will be renters in 40 years time.

Saving a deposit is the biggest hurdle.

In the early 1990s it took six years to save a 20% deposit on the

average home. Today it takes 10 years. That’s bad news for younger

Australians without access to the “Bank of Mum and Dad”.

The Coalition’s new plan seeks to arrest the decline by lending

would-be buyers up to 15% of the purchase price, provided they’ve saved

at least 5% for themselves.

It would also mean that single first home buyers on less than $125,000 a year, or couples earning less than $200,000, could save $10,000 or more by not having to pay the lenders mortgage insurance

that is normally required when a purchaser has a deposit of less than

20%. There would be a cap on the value of homes purchased through the

scheme, still unannounced, which would vary by region.

The Coalition is budgeting just $500 million for the guarantees. Labor was quick to match the scheme, partly because it doesn’t cost very much (unless there are unexpected losses).

Most likely, the scheme won’t have much impact.

It would increase home ownership, but only a little. It might also

push up prices – but by even less. Some people saving for their first

home might buy earlier. Others just priced out of the market at the

moment could afford to pay a little more for a house given that they

would not have to pay lenders mortgage insurance.

Most of those taking up the scheme would probably have bought anyway.

Those with access to the Bank of Mum and Dad already have already been

able to use such a scheme. And the income thresholds are set too high,

cutting off only the top 10-15% of income earners. The New Zealand scheme, upon which the Coalition’s plan is based, cuts out at incomes of only $85,000 for singles or $130,000 for couples.

The biggest barrier for many first home owners isn’t the deposit. Their problem is qualifying

for a mortgage when banks assess their ability to repay the loan

assuming an interest rate of 7%, much higher than the typical 4%.

The Coalition has capped uptake at 10,000 loans every year, or about

one in every ten loans (based on loans last year to first homebuyers).

Even if none of them would have bought a home without the scheme (most

unlikely), home ownership would be only 1% higher in a decade’s time.

But a bigger scheme might well be worse. If it “succeeded” in rapidly

expanding demand from first home buyers, it would push up prices for

everyone, not least all the other first home buyers trying to get into

the market. Instead of being ineffective, it’d become counterproductive.

And the bigger the scheme, the greater the risks of dodgy lending, which could leave the government on the hook if buyers default.

The underlying problem with the Coalition’s latest plan – like the

First Home Super Saver Scheme it introduced in 2017, or the Howard and

Rudd Government’s first homeowners grants – is that it tries to fix the

housing affordability problem by adding to demand for housing.

Because it costs the budget less, the new scheme is less bad than its

predecessors. But it shares their critical flaw: it pretends we can

make housing more affordable without hurting anyone.

Its political virtue might be that it sends a signal to first home buyers that government is on their side.

Yet the Coalition won’t pursue the one thing happen that would actually help home buyers the most: letting housing prices fall.

Labor’s negative gearing plan

Labor’s plan to abolish negative gearing on existing homes and halve the capital gains tax discount creates losers.

Labor would prevent new investors in existing homes from writing off the losses from their property investments against the tax they pay on their wages. And investors would pay tax on 75% of their gains, up from 50% now.

Its plan takes away tax breaks worth $1 billion to $2 billion a year in the short term, and more in the long term.

Existing homeowners would lose a little: The Grattan Institute estimates that house prices would be 1% to 2% lower under the Labor plan. The Commonwealth treasury and NSW treasury have reached similar conclusions.

Prospective investors who had planned to buy and negatively gear an

existing house would miss out on a lot. Some might buy anyway, others

wouldn’t. Despite the noise, the bulk of these people would be among the top 10% of income earners.

By reducing investor demand for existing houses, Labor’s policy could

provide a genuine boost to “genuine” home ownership, by owner

occupiers. Fewer investors would mean more first home buyers winning at

auctions.

Recent restrictions on lending to investors imposed by the Australian Prudential Regulation Authority have already resulted in an increase in the share of lending to first homebuyers. Labor’s policies would accelerate it.

The bottom line on housing? Changing rules on negative gearing and

capital gains tax is more likely to increase home ownership than

guaranteeing part of the deposit.

But no policy proposed in this Commonwealth election affects the really big lever for home ownership: increasing housing supply.

Authors: Brendan Coates, Fellow, Grattan Institute; John Daley, Chief Executive Officer, Grattan Institute

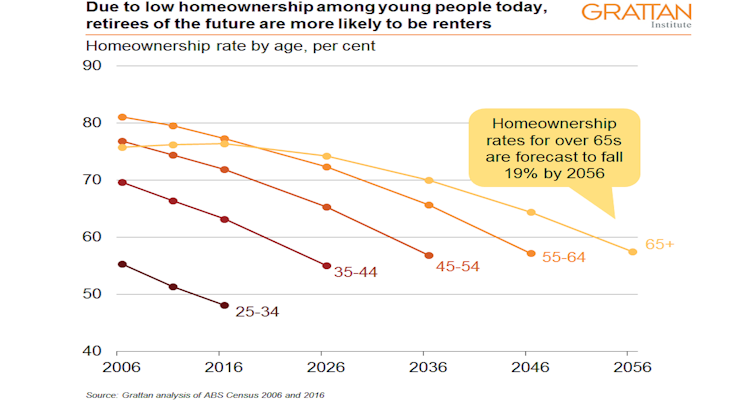

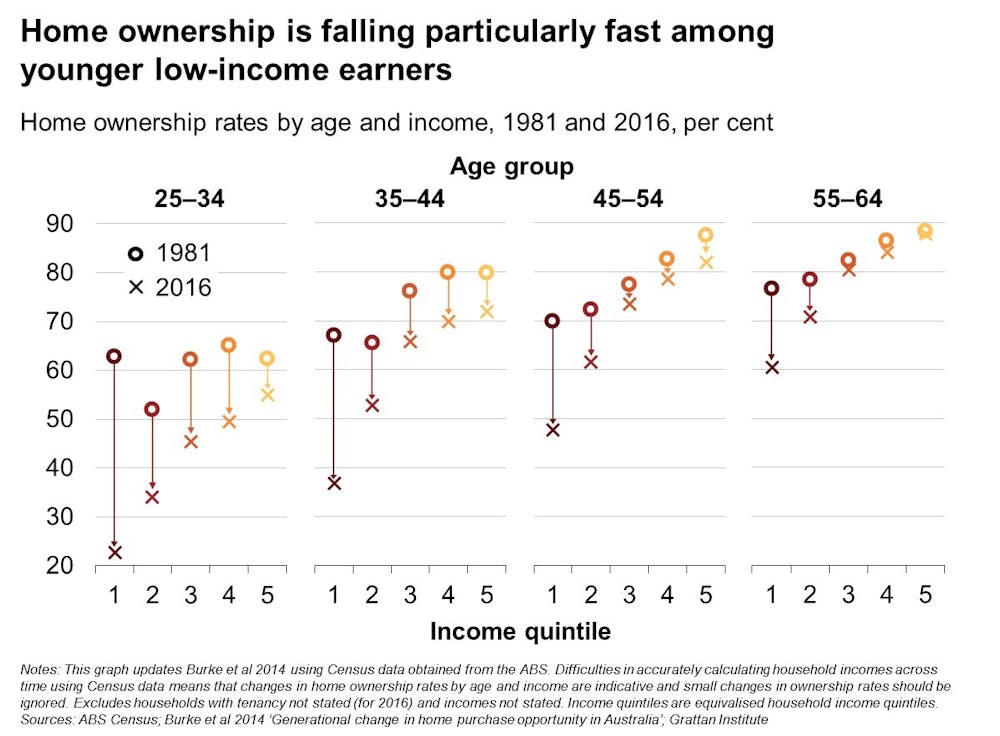

Australia’s retirement incomes system has been built on the assumption that most retirees would own their home outright. But new Grattan Institute modelling shows the share of over 65s who own their home will fall from 76% today to 57% by 2056 – and it’s likely that less than half of low-income retirees will own their homes in future, down from more than 70% today.

Home ownership provides retirees with big benefits: they have

somewhere to live without paying rent, and they are insulated from

rising housing costs. Retirees who have paid off their mortgage spend

much less of their income on housing (on average 5%) than working

homeowners or retired renters (25% to 30%). These benefits – which

economists call imputed rents – are worth more than A$23,000 a year to

the average household aged 65 or over, roughly as much again as the

maximum pension.

You’ll be OK if you own

Our 2018 report Money in Retirement

showed that while Australia’s retirement income system is working well

for the vast majority of retirees, it’s at risk of failing those who

rent. They are more than twice as likely as homeowners to suffer

financial stress, as indicated by things such as skipping meals, or

failing to pay bills.

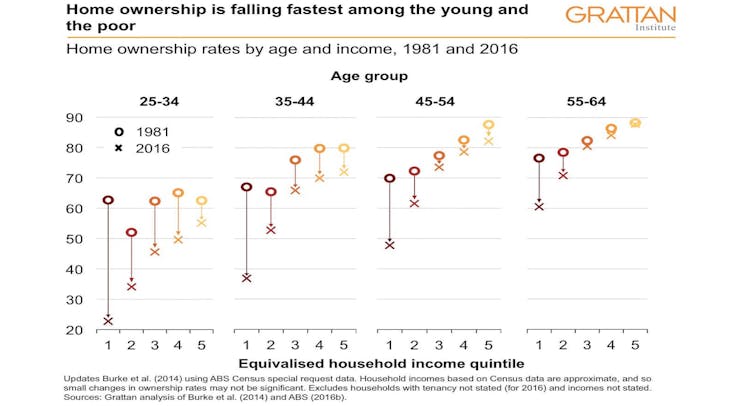

This is not surprising – renters typically have lower incomes. But the rising deposit hurdle and greater mortgage burden risks means rates of home ownership are falling fast among the presently young and the poor.

The share of 25 to 34 year olds who own their home has fallen from

more than 60% in 1981 to 45% in 2016. For 35 to 44 year olds it has

fallen from 75% to about 62%.

And home ownership now depends on income much more than in the past:

among 25-34 year olds, home ownership among the poorest 20% has fallen

from 63% to 23%.

But fewer will

Home ownership is likely to fall further in coming years. Using

Grattan Institute modelling, we find that on current trends, the share

of over 65s who own their home will fall from 76% today to 74% in 2026,

to 70% by 2036, 64% by 2046, and 57% by 2056.

And while we don’t project home ownership rates for different income

groups due to data limitations (we have the necessary Census data on

home ownership rates by age and income only for 1981 and 2016), it is

more than likely that less than half of low income retirees will own

their homes in future, down from more than 70% today.

Today’s younger Australians will become tomorrow’s retirees.

Worsening housing affordability means renting will become more widespread

among retirees. As a result, more retirees will be at risk of poverty

and financial stress, particularly if rent assistance does not keep pace

with future increases in rents paid by low-income renters.

And rent assistance won’t much help

The maximum rent assistance payment is indexed in line with the

consumer price index, but rents have been growing faster than the

consumer price index for a long time. Between June 2003 and June 2017,

the consumer price index climbed by 41%, while average rents climbed by

64%.

That’s why our Money in Retirement

report recommended boosting Commonwealth Rent Assistance by 40%, at a

cost of $300 million a year in today’s dollars. That would restore it to

the buying power it had 15 years ago. It should be indexed in future to

changes in the rents typically paid by the people who get it, so its

value is maintained, as recommended by the Henry Tax Review.

There’s another important implication. Retirement incomes are likely to become more unequal in future. Money in Retirement

found that in general future retirees will have adequate retirement

incomes. Most workers today can expect a retirement income of at least

89% of their pre-retirement income, well above the 70% benchmark used by

the Organisation for Economic Co-operation and Development, and more

than enough to maintain pre-retirement living standards.

But a retirees who rent will have much less for living on.

There will be ‘haves’ and more ‘have nots’

Among home-owners, an increasing proportion will be still paying off

their mortgages when they retire – the proportion of 55 to 64 year olds

who own their home outright fell from 72% in 1995-96 to 42% in 2015-16.

Some will (quite rationally) use some or all of their super to pay off

their mortgage.

And rising housing costs will in time force retirees to draw down on more of the value of their home to fund their retirement.

Currently, few retirees downsize or borrow against the equity of

their home while continuing to live in it. But that will have to change.

House prices have outstripped growth in incomes.

Median prices have increased from around four times median incomes in

the early 1990s to more than seven times median incomes today (and more

than eight times in Sydney).

Government policy should continue to encourage these retirees to draw

down on the increasingly valuable equity of their homes to help fund

their retirement. They are not the ones who will need government help.

The government’s recent expansion of the Pension Loans Scheme that allows all retirees to borrow against the value of their homes is a step in that direction.

Retirement is going to change in the years ahead. Most retirees will be far from poor, many of them better able to support themselves than ever before. But an increasing number will not. They are the ones who will need our help.

Authors: Brendan Coates, Fellow, Grattan Institute; Tony Chen, Researcher, Grattan Institute

In its long-awaited final report on the efficiency and competitiveness of Australia’s leaky superannuation system, Australia’s Productivity Commission provides a roadmap.

Weeding out scores of persistently underperforming funds, clamping

down on unwanted multiple accounts and insurance policies, and letting

workers choose funds from a simple list of top performers would give the

typical worker entering the workforce today an extra A$533,000 in retirement.

Even Australians at present in their mid fifties would gain an extra A$79,000.

If this government or the next cares about the welfare of Australians

rather than looking after the superannuation industry it’ll use the

recommendations to drive retirement incomes higher.

So why the continued talk (from Labor) about lifting compulsory super

contributions from the present 9.5% of salary to 12%, and then perhaps an unprecedented 15%?

It’s probably because (and Paul Keating, the former treasurer and

prime minister who is the father of Australia’s compulsory

superannuation system says this) they think the contributions don’t come

from workers, but from employers.

To date, they’ve been dead wrong. And with workers’ bargaining power arguably weaker than in the past, there’s no reason whatsoever to think they’ll be right from here on.

Past super increases have come out of wages

Australia’s superannuation system requires employers

to make the compulsory contributions on behalf of their workers. Right

now that contribution is set at 9.5% of wages and is scheduled to

increase incrementally to 12% by July 2025.

So, for workers, what’s not to like?

It’s that while employers hand over the cheque, workers pay for

almost all of it via lower wages. Bill Shorten, then assistant

treasurer, made this point in a speech in 2010:

Because it’s wages, not profits, that will fund super increases in

the next few years. Wages are the seedbed of the whole operation. An

increase in super is not, absolutely not, a tax on business.

Essentially, both employers and employees would consider the

Superannuation Guarantee increases to be a different way of receiving a

wage increase.

The Henry Tax Review and other investigations

have found this is exactly what happens. Increases in the compulsory

super contributions have led to wages being lower than they otherwise

would have been.

Even Paul Keating, speaking in 2007, made this point. Compulsory super contributions come out of wages, not from the pockets of employers:

The cost of superannuation was never borne by employers. It was

absorbed into the overall wage cost […] In other words, had employers

not paid nine percentage points of wages, as superannuation

contributions, they would have paid it in cash as wages.

This is more than mere theory. Compulsory super was designed to

forestall wage rises. Concerned about a wages breakout in 1985, then

Treasurer Paul Keating and ACTU President Bill Kelty struck a deal to defer wage rises in exchange for super contributions.

When the Super Guarantee climbed from 9% to 9.25% in 2013, the Fair Work Commission stated

in its minimum wage decision of that year that the increase was “lower

than it otherwise would have been in the absence of the super guarantee

increase”.

The pay of 40% of Australian workers is based

on an award or the National Minimum Wage and is therefore affected by

the Commission’s decisions. For these people, there is no question:

their wages are lower than they would’ve been if super hadn’t increased.

Where’s the evidence employers pay for super?

If wage rises came from the pockets of employers then we should see a

spike in wages plus super when compulsory super was introduced, and

again when it was increased. But there wasn’t one when compulsory super

was introduced – a point Bill Shorten has made in the past.

When compulsory super was introduced via awards in 1986, workers’

total remuneration (excluding super) made up 63.3% of national income.

By 2002, when the phase-in was complete, it made up 60.1%.

Out of the 26 countries for which the Organisation for Economic Co-operation and Development has data, Australia recorded the tenth largest slide in the labour share of national income during the period compulsory super contributions were ramped up.

Of course, changes in super aren’t the only thing that affects workers’ share of national income.

But the size of the fall in the labour share in Australia over the

period when the super guarantee was increasing isn’t consistent with the

idea that employers picked up the tab for super.

Would it be different this time?

Paul Keating argues that while in the past lifting compulsory super to 9.5% was paid for from wages, a future increase to 12% today would not be:

Workers are not getting real wage increases anywhere, and can’t get

them. The Reserve Bank governor makes the point every week. So the award

of an extra 2.5% of super to employees via the super guarantee will

give them a share of productivity they will not get in the market –

without any loss to their cash wages.

But such claims are difficult to square with concerns that workers’ weak bargaining power is one of the reasons current wage growth is so weak..

If employers don’t feel pressed to give wage rises, why would they feel

pressed to absorb an increase in the compulsory Super Guarantee?

And while real wages (wages adjusted for inflation) haven’t grown

particularly quickly, the dollar value of wages continues to grow: by 2.2%

a year over the past five years. It would be easy for employers to

simply reduce those increases to offset any increase in compulsory super

– as they have in the past.

And no, more contributions won’t help workers

The Grattan Institute’s recent report, Money in Retirement,

showed increasing the compulsory super would primarily benefit the top

20% of Australians. It would hurt the bottom half during working life a

lot more than it helps them once retired.

Their higher super contributions would not improve their retirement

outcomes: their extra super income would be largely offset by lower

part-pensions. What’s more, the age pension is indexed to wages. If wages grew by less (as they would as compulsory super contributions were increased) pensions would grow by less too.

Lifting compulsory super would also cost the budget A$2 billion a year in extra tax breaks, largely for high-income earners, because it is lightly taxed.

That would mean higher taxes elsewhere, or fewer services.

For low-income Australians, increasing compulsory super contributions

would be a thoroughly bad deal. It means giving up wage increases in

return for no boost in their retirement incomes.

A government that wanted to boost the living standards of working Australians both now and in retirement would consider carefully all of the Productivity Commission’s suggestions including this one: an independent inquiry into the whole idea and effectiveness of Australia’s regime of compulsory contributions, to be completed ahead of any increase in the Superannuation Guarantee rate .

The Grattan Institute has rejected the ‘fear factor’ of the financial service industry that encourages Australians to stress about their retirement, via InvestorDaily.

A recently released report by the Grattan Institute, Money in Retirement: More than Enough, reveals that most Australians will be financially comfortable in retirement.

The report shows that retirees are less likely than working-age Australians to suffer financial stress and more likely to have extras like annual holidays.

Grattan Institute chief executive John Daley said that the institute’s models showed that Australians would actually be able to retire in comfort.

“The financial services industry ‘fear factory’ encourages Australians to worry unnecessarily about whether they’ll have enough money in retirement,” he said.

The Institute modelling, even allowing for inflation showed that workers today could expect a retirement income of 91 per cent of their pre-retirement income.

Grattan’s report called on the government to scrap the plan to increase compulsory contributions from 9.5 per cent to 12 per cent as most Australians would be comfortable in retirement.

The report instead called for a 40 per cent increase in the maximum rate of Commonwealth Rent Assistance and for a loosening of the Age Pension assets test which would boost retirement incomes for 70 per cent of future retirees.

The Association of Superannuation Funds of Australia denounced the report calling it an unprecedented attack on the retirement aspirations of ordinary Australians.

ASFA chief executive Dr Martin Fahy said the report was about two Australia’s, one with fully-funded, high-earning retirees and the rest with reliance on the state.

“The Grattan Institute wants to dismantle our world class retirement funding system and replace it with a model that has two thirds of the population relying on the Age Pension,” said Dr Fahy.

Dr Fahy also slammed the reports recommendation that the retirement age be raised to 70 and that the government reviewing the adequacy of Australians’ retirement incomes.

The institute’s report did recommend the government review the adequacy of Australians’ retirement income and called for a new standard.

“The Productivity Commission should establish a new standard for retirement income adequacy and assess how well Australians of different ages and incomes will meet that standard. References to the ASFA comfortable retirement standard should be removed,” the report read.

“The ASFA Retirement Standard provides a detailed account of living expenses in retirement.

“The Grattan analysis in effect wants people in retirement not to have heating in winter, not to take vacations, to get rid of the car, and skimp on prescriptions and other out-of-pocket health care costs,” said Dr Fahy.

The report for its part has said that reform is needed by the government to be able to fund aged care and health in the future.

“Unless governments have the courage to make these reforms, future budgets will not be able to fund aged care and health at the same level as today, which is the real threat to adequate retirement incomes in future,” it said.

State-owned power networks have spent up to A$20 billion more than was needed on the electricity grid, and households and businesses in New South Wales, Queensland and Tasmania are paying for it in sky-high power bills.

A new Grattan Institute report, Down to the Wire, shows that electricity customers in these states would be paying A$100-A$400 less each year if the overspend had not happened.

The problem is that state governments, worried about blackouts and growing demand for electricity, encouraged the networks to spend more in the mid-2000s. But the networks overdid it, and now consumers are paying for a grid that is underused, overvalued, or both.

Why we built too much

The grid includes high-voltage transmission lines that carry electricity over large distances, as well as low-voltage poles and wires that connect to homes and businesses. Networks are built to cope with those times of highest demand for electricity. Yet the growth in the value of network assets has far exceeded growth in customer numbers, total demand, or even peak demand.

Demand for electricity did grow rapidly in the early 2000s, but since then it has slowed substantially as more and more households have installed solar panels, and appliances have become more energy efficient. Networks may have overbuilt because they expected that demand would continue to grow.

Yet the overbuilding has occurred almost exclusively in the public networks. Why would government ownership lead to such high costs?

There are two main reasons. First, investment in electricity networks boosts state government revenues because public networks pay a fee to the state to neutralise their lower borrowing costs (as well as the dividend they pay to the state as the owner). Second, a government-owned business might come under political pressure to prioritise goals such as reliability or job creation over cost.

Of course governments worry about reliability – they cop the blame if anything goes wrong. In 2005, the NSW and Queensland governments required their network businesses to build excessive back-up infrastructure to protect against even the most unlikely events. Reliability did improve a bit in some networks, but at significant cost: on average, customers got an extra 45 minutes of electricity a year at a cost of A$270 each.

State governments should take responsibility

Successive state governments in NSW, Queensland and Tasmania are responsible for overinvesting in their networks and, in NSW and Queensland, for setting reliability standards too high.

State governments can’t turn back the clock but they can still fix the mistakes of the past. And they should, because if they don’t, consumers will be paying for decades to come.

Households and businesses that can afford to buy solar panels and batteries will reduce their reliance on the grid. Meanwhile, those left behind – including the most vulnerable Australians – will be stuck with the burden of paying for the grid.

In Down to the Wire we recommend that where network businesses are still in government hands, the government should write down the value of the assets. This would mean governments forgoing future revenue in favour of lower electricity bills. For recently privatised businesses in NSW, a write-down could create more issues than it solves, so in those cases the state government should refund consumers the difference through a rebate.

At a time when governments are concerned about energy affordability, NSW, Queensland and Tasmania have a real opportunity to do something about it. They should seize it.

How to prevent this happening again

There will always be pressure to spend more. At the moment, concerns about South Australia’s reliability could very well lead to further investment in network infrastructure.

Policymakers must also deal with the risk that, in future, parts of the network may no longer be needed. The grid may need to be reconfigured as new technologies emerge, some communities go off-grid, and new energy sources arise in new locations.

For now, consumers bear this risk: they are locked into paying for assets whether or not they are needed. In future, the risk should be shared between consumers and businesses; this would encourage businesses to avoid overbuilding in the first place and instead consider alternative solutions.

With the focus on reliability right now, governments are at risk of repeating mistakes of the past. The truth is that Australia already has a very reliable grid.

On average across the National Electricity Market, consumers experience less than two-and-a-half hours in unplanned outages per year. Reducing that by a few minutes of supply each year is very expensive. Politicians typically value reliability more than consumers, but ultimately it is consumers who foot the bill.

State governments now have an opportunity to reset the clock – to pay off the mistakes of the past and let consumers guide choices about our future grid.

Author: Kate Griffiths, Senior Associate, Grattan Institute

So much of Australia’s history and success is built on immigration. Migrants have benefited incumbent Australians by raising incomes, increasing innovation, contributing to government budgets, smoothing over population ageing and diversifying our social fabric. But it is also true that immigration is affecting house prices and rents.

Australian governments are squandering the gains from migration with poor housing and infrastructure policies. Our new report, Housing affordability: re-imagining the Australian dream, shows what’s at stake. Unless the states reform their planning systems to allow more housing to be built, the Commonwealth should consider tapping the brakes on Australia’s migrant intake.

Since 2005, net overseas migration – which includes the increase in temporary migrants – has averaged 200,000 people per year, up from 100,000 in the previous decade. It is predicted to be around 240,000 per year over the next few years.

Immigrants are more likely to move to Australia’s big cities than existing residents, which increases demand for scarce urban housing. In 2011, 86% of immigrants lived in major cities, compared to 65% of the Australian-born population.

Chart 1. Migration has jumped, and so have capital city populations

Grattan Institute, Author provided

Not surprisingly, several studies have found that migration increases house prices, especially when there are constraints on building enough new homes.

The pick-up in immigration coincides with Australia’s most recent housing price boom. Sydney and Melbourne are taking more migrants than ever. Australian house prices have increased 50% in the past five years, and by 70% in Sydney.

Chart 2: Net overseas migration into NSW and Victoria is at record levels

Grattan Institute (Data source: ABS 3101.0 – Australian Demographic Statistics), Author provided

Of course immigration isn’t the only factor driving up house prices and rents. Housing also costs more because incomes rose, interest rates fell and banks made it easier to get a loan. But adding 2 million migrants in the past decade has clearly increased how many new homes are needed.

We haven’t built enough homes

Housing demand from immigration shouldn’t lead to higher prices if enough dwellings are built quickly and at low cost. In post-war Australia, record rates of home building matched rapid population growth. House prices barely moved.

But over the last decade, home building did not keep pace with increases in demand, and prices rose. Through the 1990s, Australian cities built about 800 new homes for every extra 1,000 people. They built half as many over the past eight years.

We estimate somewhere between 450 and 550 new homes are needed for each 1,000 new residents, after accounting for demolitions. And because more families are breaking up and the population is ageing, more homes are needed to accommodate households with fewer members.

Chart 3: Housing construction lagged population in the last decade, but has picked up

Grattan Institute, Author provided

Only in the past couple of years has construction started to match population growth, especially in Sydney. It’s no coincidence that Sydney house prices have finally moderated in the past six months.

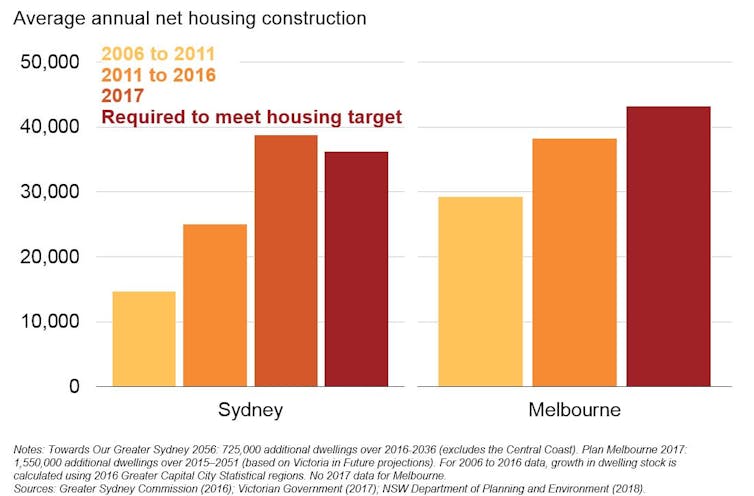

But the backlog of a decade of undersupply remains. Development at today’s record rates is the bare minimum needed to meet record population growth built into Sydney’s and Melbourne’s housing supply targets over the next 40 years.

Chart 4: Strong housing construction will need to be maintained to meet city plan housing targets

Grattan Institute

So what should governments do?

Building more housing will improve affordability the most – but slowly. Even at current record construction rates, new housing increases the stock of dwellings by only 2% each year. But building an extra 50,000 homes a year nationwide for a decade would lead to national house prices between 5% and 20% lower than otherwise. Do it for longer and prices will fall even further.

State governments need to fix planning rules to allow more housing to be built in inner and middle-ring suburbs. More small-scale urban infill projects should be allowed without council planning approval. And state governments should allow denser development “as of right” along key transport corridors. The Commonwealth can help with financial incentives for these reforms.

But the politics of planning in our major cities is fraught. Most people in established middle suburbs already own their houses. Prospective residents who don’t already live there can’t vote in council elections, and their interests are largely unrepresented.

If we want to maintain current migration levels, along with their economic, social and budgetary benefits, we need to do better at planning to allow more housing to be built.

What does this mean for the migrant intake?

The Australian government should develop a population policy, as the Productivity Commission recommended. It should articulate the appropriate level of migration given its economic, budgetary and social benefits and costs. This should include how it affects the Australian community living with the reality of land use planning policy – and contrasting this with the effect of optimal planning policy.

If planning and infrastructure policies don’t improve, the government should consider cutting the migration intake. This would reduce demand for housing, but would also reduce the incomes of existing residents.

The best policy is probably to continue with Australia’s demand-driven, relatively high-skill migration and to build enough homes for the growing population. But Australia is in a world of third-best policy: rapid migration and restricted housing supply are imposing big costs on people who don’t already own their homes. If the states are not going to reform planning rules to increase the number of homes built, then the Australian government should consider whether reducing migration is the lesser evil.

Any reduction should be modest and targeted at the parts of the migration program that provide the smallest benefit to Australian residents and migrants themselves. Balancing these interests is difficult, because each part of the program has different economic, social and budgetary costs and benefits.

Cutting back family reunion visas would have substantial social costs. Limiting skilled migration would hurt the economy and many businesses. Restricting growth in international students would reduce universities’ incomes.

There are also broader costs to cutting the migrant intake. It would hit the Commonwealth budget in the short term. Most migrants are of working age and pay full rates of personal income tax. And many temporary migrants, such as 457 visa holders, can’t draw on a range of government services and benefits, including welfare and Medicare. More importantly, cutting back on younger, skilled migrants is likely to hurt the budget and the economy in the long term.

But there is no point denying that housing affordability is worse because of a combination of rapid immigration and poor planning policy. Rather than tackling these issues, much of the debate has focused on policies that are unlikely to make a real difference. Unless governments own up to the real problems, and start explaining the policy changes that will make a real difference, Australia’s housing affordability woes are likely to get worse.

Authors; John Daley, Chief Executive Officer, Grattan Institute; Brendan Coates, Fellow, Grattan Institute; Trent Wiltshire, Associate, Grattan Institute

When we see excessive spikes in fuel prices, rapid annual increases in health insurance premiums, and a confusing array of electricity options to choose from, it is easy to conclude that big companies are using their market power to gouge their customers.

But the latest report from the Grattan Institute finds claims about Australia being dominated by oligopolies are overblown. Only about 15% of the economy is dominated by large firms.

In the “natural monopolies”, such as electricity distribution, a single firm typically serves the market. And where the largest firms enjoy strong scale advantages, such as in mobile telecoms, just a handful of options are available to consumers.

Then there are sectors where competition is constrained by regulation, such as banking and pharmacies. In such sectors, the largest four firms earn more than two-thirds of revenue, on average.

Australians have long been concerned about oligopoly power. But in the largest sectors with barriers to entry, markets are not much more concentrated in Australia than they are in other economies of a similar size. Supermarkets in Australia are the exception to this rule.

While the United States is less concentrated at a national level, much of this is explained by its larger population. In Florida, for example, a state with a population of 21 million, its sectors are typically just as concentrated as Australia’s, if not more so.

The report also finds no clear trend toward higher concentration in Australia, unlike the case in the US. The revenue of the top 100 Australian listed firms relative to GDP has changed little since the early 1990s.

While the market share of Australia’s big four banks increased through mergers and acquisitions, Coles’ and Woolworths’ dominance appears to be in decline with the rise of Aldi and Costco.

Whether high concentration in Australia is a problem depends on its impact on consumers. Our report finds that sectors with high barriers to entry are about 20% more profitable than sectors with no significant barriers, although there is plenty of variation.

The most profitable sectors include supermarkets, telecommunications (wireless and fixed-line), internet publishing, electricity distribution and transmission, airports and gambling. The banks’ profitability has fallen since the global financial crisis, while their cost of equity has risen due to increased risk.

In some regulated sectors, consumers could clearly do better. Banking regulations push up costs and can weigh heavily on smaller firms as well as on consumers. In the pharmacy sector, competition is directly restricted.

In natural monopoly sectors, where super-profits account for 10% of what consumers pay, on average, it’s also difficult to conclude that consumers benefit.

But less concentrated markets may not make consumers better off. Many profitable big firms must have lower costs than smaller ones; otherwise they would lose market share.

For example, average prices at Coles and Woolworths are lower than IGA, even while profits are higher: it seems that some of the large chains’ scale economies are passed on to consumers. Regulation that limits the size of the largest firms might reduce profits, but could push costs and prices up.

What can policymakers do to get better outcomes for consumers? In the natural monopolies, regulators need to get tougher. For example, they could start regulating prices at airports, rather than just monitoring them.

Across the economy, regulators should continue to focus on protecting competition and preventing the misuse of market power. Government should increase the penalties for cartels and other concerted practices.

Governments could help cut entry barriers, for example by harmonising product standards to reduce trade costs, or freeing up zoning to make it easy for competing supermarkets to expand. And they should make it easier for consumers to switch between providers and control their own data in sectors like banking and even social networks.

There is also much that can be done where retail competition is not working well, such as in superannuation and in retail electricity.

But overall, Australia’s oligopoly problem is a lot smaller than many believe. It’s also not getting worse; our competition policy and regulation is broadly working well.

Authors: Jim Minifie, Productivity Growth Program Director, Grattan Institute; Cameron Chisholm, Senior Associate, Productivity Growth, Grattan Institute; Lucy Percival, Associate, Grattan Institute

Rising housing costs are hurting low-income Australians the most. Those at the bottom end of the income spectrum are much less likely to own their own home than in the past, are often spending more of their income on rent, and are more likely to be living a long way from where most jobs are being created.

Low-income households have always had lower home ownership rates than wealthier households, but the gap has widened in the past decade. The dream of owning a home is fast slipping away for most younger, poorer Australians.

As you can see in the following chart, in 1981 home ownership rates were pretty similar among 25-34 year olds no matter what their income. Since then, home ownership rates for the poorest 20% have fallen from 63% to 23%.

Home ownership rates also declined more for poorer households among older age groups. Home ownership now depends on income much more than in the past.

Lower home ownership rates mean more low-income households are renting, and for longer. But renting is relatively unattractive for many families. It is generally much less secure and many tenants are restrained from making their house into a home.

For poorer Australians who do manage to purchase a home, many will buy on the edges of the major cities where housing is cheaper. But because jobs are becoming more concentrated in our city centres, people living on the fringe have access to fewer jobs and face longer commutes, damaging their family and social life.

Prices for low-cost housing have increased the fastest

The next chart shows that the price for cheaper homes has grown much faster than for more expensive homes over the past decade. This has made it much harder for low-income earners to buy a home.

If we group the housing market into ten categories (deciles), we can see the price of a home in the lowest (first and second) deciles more than doubled between 2003-04 and 2015-16. By contrast, the price of a home in the fifth, sixth and seventh deciles only increased by about 70%.

Tax incentives for investors may explain why the price of low-value homes increased faster. Negative gearing remains a popular investment strategy; about 1.3 million landlords reported collective losses of A$11 billion in 2014-15.

Many investors prefer low-value properties because they pay less land tax as a proportion of the investment. For example, an investor who buys a Sydney property on land worth A$550,000 pays no land tax, whereas the same investor would pay about A$9,000 each year on a property on land worth A$1.1 million.

Rising housing costs also hurt low-income renters

As this last chart shows, more low-income households (the bottom 40% of income earners) are spending more than 30% of their income on rent (often referred to as “rental stress”), particularly in our capital cities. In comparison, only about 20% of middle-income households who rent are spending more than 30% of their income on rent.

Why are more low-income renters under rental stress?

Secondly, rents for cheaper dwellings have grown slightly faster than rents for more expensive dwellings. Finally, the stock of social housing – currently around 400,000 dwellings – has barely grown in 20 years, while the population has increased by 33%.

As a result, many low-income earners who would once have been in social housing are now in the private rental market.

What can be done about it?

Increasing the social housing stock would improve affordability for low-income earners. But the public subsidies required to make a real difference would be very large – roughly A$12 billion a year – to return the affordable housing stock to its historical share of all housing.

In addition, the existing social housing stock is not well managed. Homes are often not allocated to people who most need them, and quality of housing is often poor. Increased financial assistance by boosting Commonwealth Rent Assistance may be a better way to help low-income renters meet their housing costs

Boosting Rent Assistance for aged pensioners by A$500 a year, and A$500 a year for working-age welfare recipients would cost A$250 million and A$450 million a year respectively.

Commonwealth and state governments should also act to improve housing affordability more generally. This will require policies affecting both demand and supply.