I discuss how Ireland navigated their financial crisis a decade ago with Eddie Hobbs, the financial writer, adviser and. broadcaster, who lived through the crash and commented on the events in Ireland.

He wrote and presented a programme on state broadcaster RTE entitled Rip-Off Republic in 2005.

Specifically we discuss how Australia should be preparing…. now….

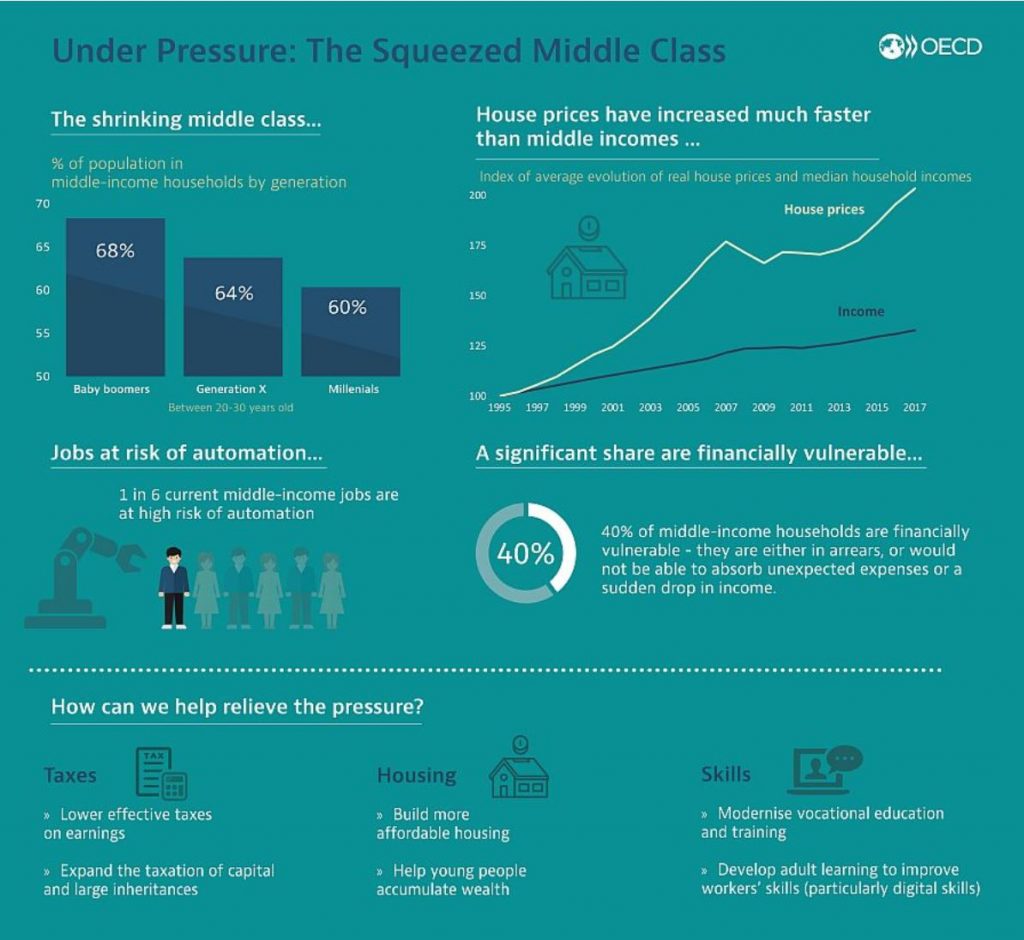

The OECD has released a report Under Pressure: The Squeezed Middle Class which underscores the fact that relative to the more affluent, those in the middle are getting squeezed. 40% are financially at risk. Timely given the current Australian election!

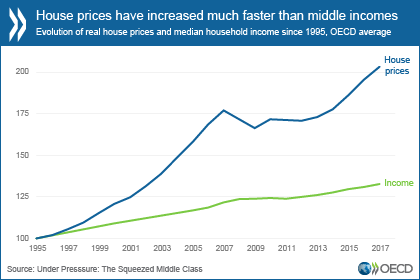

Much of this is because of the high costs of housing relative to incomes.

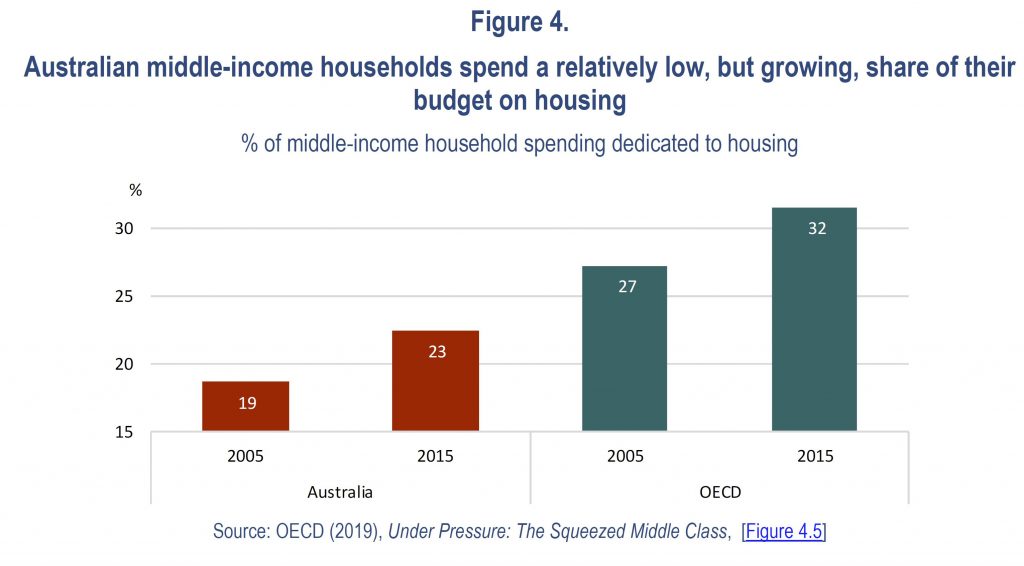

The cost of a middle class lifestyle has increased faster than inflation. Housing, for example, makes up the largest single spending item for middle-income households, at around one third of disposable income, up from a quarter in the 1990s. House prices have been growing three times faster than household median income over the last two decades

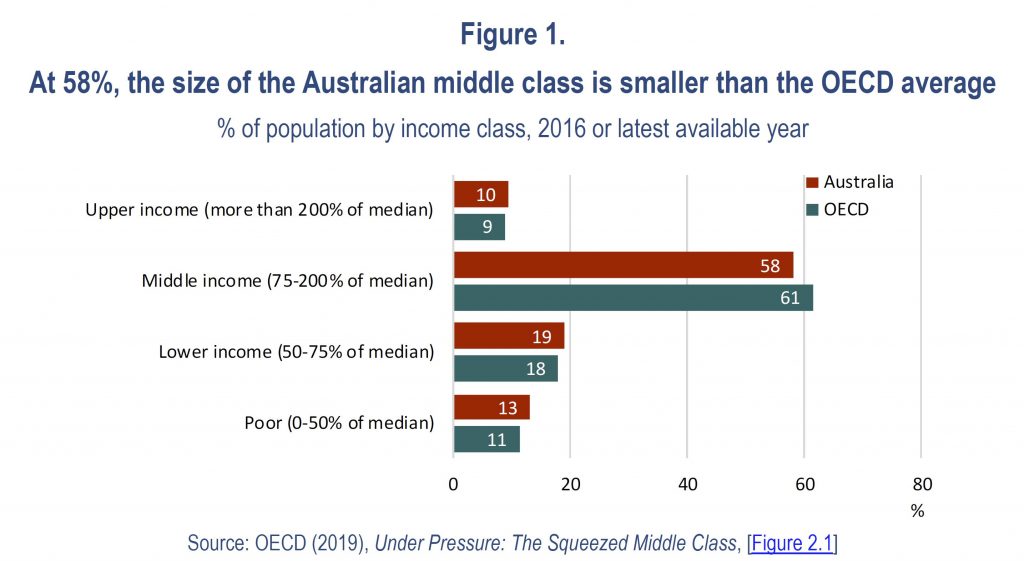

The report includes Australian specific data. At 58%, the size of the Australian middle class is smaller than the OECD average.

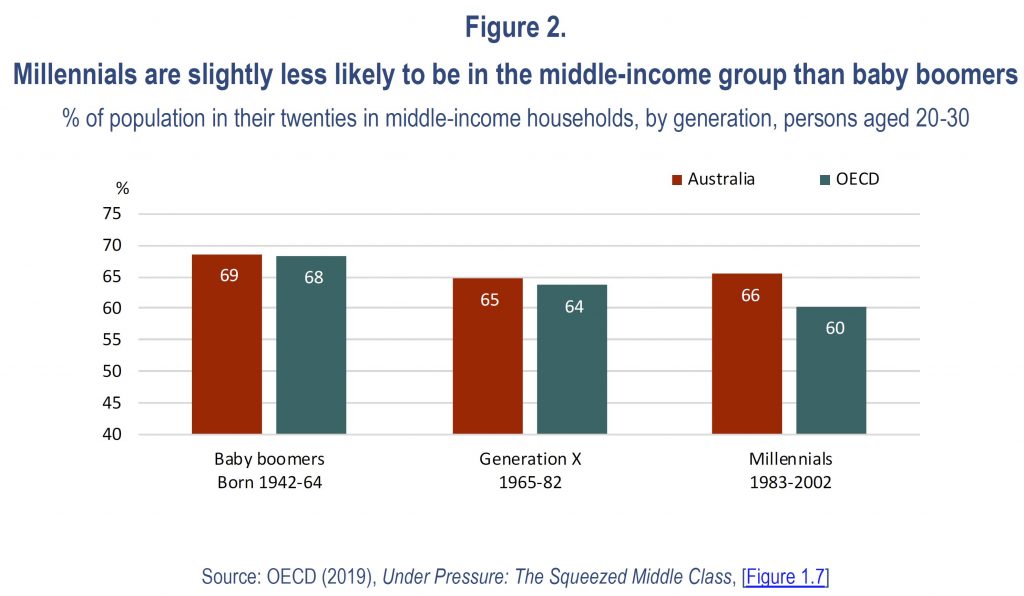

Millennials are slightly less likely to be in the middle-income group than baby boomers.

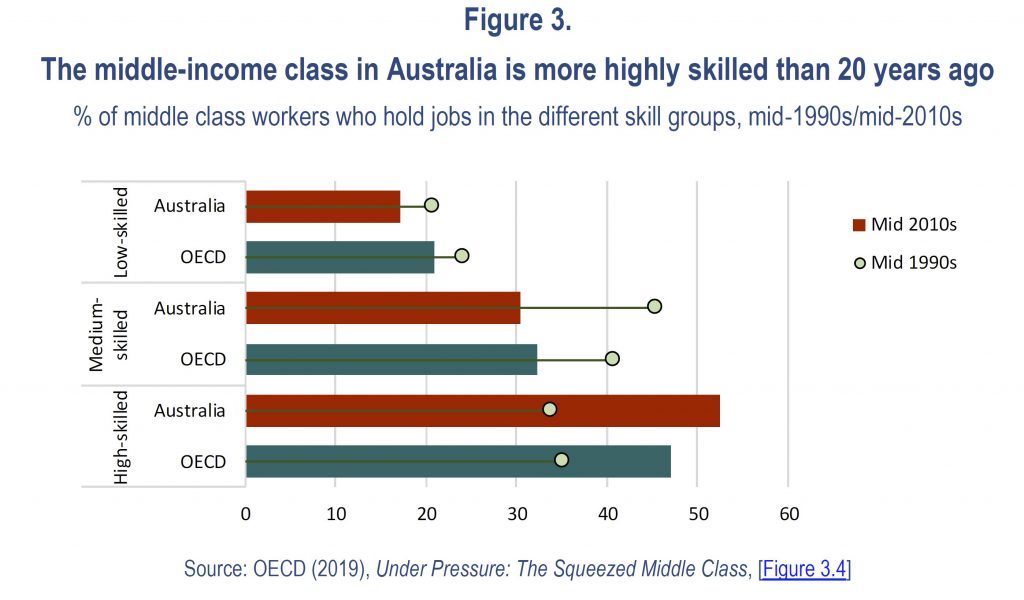

The middle-income class in Australia is more highly skilled than 20 years ago

Australian middle-income households spend a relatively low, but growing, share of their budget on housing.

More generally, the report says that the middle class has shrunk in most OECD countries as it has become more difficult for younger generations to make it to the middle class, defined as earning between 75% and 200% of the median national income. While almost 70% of baby boomers were part of middle-income households in their twenties, only 60% of millennials are today

The economic influence of the middle class has also dropped sharply. Across the OECD area, except for a few countries, middle incomes are barely higher today than they were ten years ago, increasing by just 0.3% per year, a third less than the average income of the richest 10%

“Today the middle class looks increasingly like a boat in rocky waters,” said OECD Secretary-General Angel Gurría, launching the report in New York with Luis Felipe Lopéz-Calva, Assistant Secretary General, Latin America and the Caribbean, United Nations Development Programme. “Governments must listen to people’s concerns and protect and promote middle class living standards. This will help drive inclusive and sustainable growth and create a more cohesive and stable social fabric.

Gabriela Ramos, OECD Chief of Staff and Sherpa overseeing the

Organisation’s work on Inclusive Growth, presented in more details the

main findings of the report, saying “our analysis delivers a bleak

picture and a call for action. The middle class is at the core of a

cohesive, thriving society. We need to address their concerns regarding

living costs, fairness and uncertainty.”

More than one in five middle-income households spend more than they earn and over-indebtedness is higher for them than for both low-income and high-income households. In addition, labour market prospects have become increasingly uncertain: one in six middle-income workers are in jobs that are at high risk of automation, compared to one in five low-income and one in ten high-income workers

To help the middle class, a comprehensive action plan is needed, according to the OECD. Governments should improve access to high-quality public services and ensure better social protection coverage. To tackle cost of living issues, policies should encourage the supply of affordable housing. Targeted grants, financial support for loans and tax relief for home buyers would help lower middle-income households. In countries with acute levels of housing-related debt, mortgage relief would help overburdened households get back on track

As temporary or unstable jobs – often offering lower wages and job security – increasingly replace traditional middle-class jobs, more investment is needed in vocational education and training systems. Social insurance and collective bargaining coverage for non-standard workers, such as part-time or temporary employees or self-employed, should be extended

Finally, to foster fairness of the socio-economic system, policies

need to consider shifting the tax burden from labour income to income

from capital and capital gains, property and inheritance, as well as

making income taxes more progressive and fair.

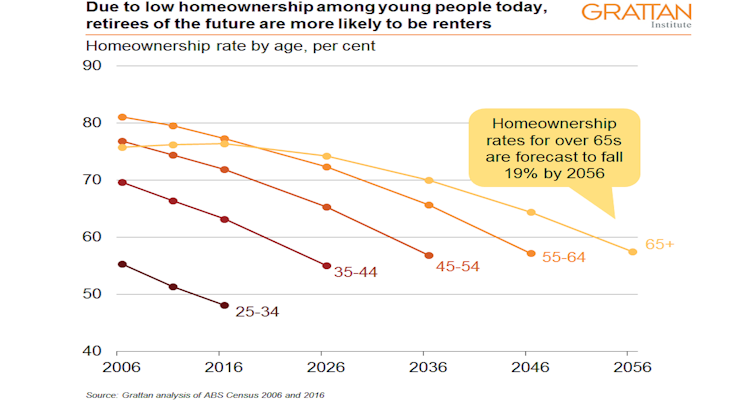

Australia’s retirement incomes system has been built on the assumption that most retirees would own their home outright. But new Grattan Institute modelling shows the share of over 65s who own their home will fall from 76% today to 57% by 2056 – and it’s likely that less than half of low-income retirees will own their homes in future, down from more than 70% today.

Home ownership provides retirees with big benefits: they have

somewhere to live without paying rent, and they are insulated from

rising housing costs. Retirees who have paid off their mortgage spend

much less of their income on housing (on average 5%) than working

homeowners or retired renters (25% to 30%). These benefits – which

economists call imputed rents – are worth more than A$23,000 a year to

the average household aged 65 or over, roughly as much again as the

maximum pension.

You’ll be OK if you own

Our 2018 report Money in Retirement

showed that while Australia’s retirement income system is working well

for the vast majority of retirees, it’s at risk of failing those who

rent. They are more than twice as likely as homeowners to suffer

financial stress, as indicated by things such as skipping meals, or

failing to pay bills.

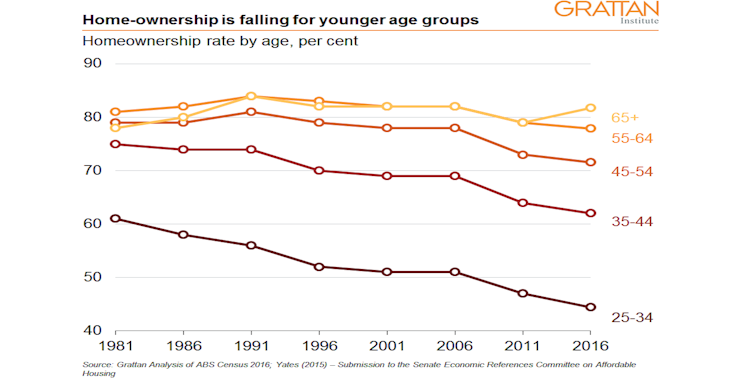

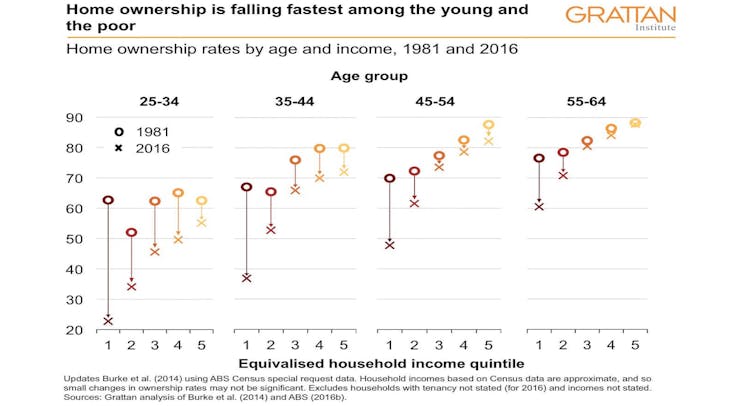

This is not surprising – renters typically have lower incomes. But the rising deposit hurdle and greater mortgage burden risks means rates of home ownership are falling fast among the presently young and the poor.

The share of 25 to 34 year olds who own their home has fallen from

more than 60% in 1981 to 45% in 2016. For 35 to 44 year olds it has

fallen from 75% to about 62%.

And home ownership now depends on income much more than in the past:

among 25-34 year olds, home ownership among the poorest 20% has fallen

from 63% to 23%.

But fewer will

Home ownership is likely to fall further in coming years. Using

Grattan Institute modelling, we find that on current trends, the share

of over 65s who own their home will fall from 76% today to 74% in 2026,

to 70% by 2036, 64% by 2046, and 57% by 2056.

And while we don’t project home ownership rates for different income

groups due to data limitations (we have the necessary Census data on

home ownership rates by age and income only for 1981 and 2016), it is

more than likely that less than half of low income retirees will own

their homes in future, down from more than 70% today.

Today’s younger Australians will become tomorrow’s retirees.

Worsening housing affordability means renting will become more widespread

among retirees. As a result, more retirees will be at risk of poverty

and financial stress, particularly if rent assistance does not keep pace

with future increases in rents paid by low-income renters.

And rent assistance won’t much help

The maximum rent assistance payment is indexed in line with the

consumer price index, but rents have been growing faster than the

consumer price index for a long time. Between June 2003 and June 2017,

the consumer price index climbed by 41%, while average rents climbed by

64%.

That’s why our Money in Retirement

report recommended boosting Commonwealth Rent Assistance by 40%, at a

cost of $300 million a year in today’s dollars. That would restore it to

the buying power it had 15 years ago. It should be indexed in future to

changes in the rents typically paid by the people who get it, so its

value is maintained, as recommended by the Henry Tax Review.

There’s another important implication. Retirement incomes are likely to become more unequal in future. Money in Retirement

found that in general future retirees will have adequate retirement

incomes. Most workers today can expect a retirement income of at least

89% of their pre-retirement income, well above the 70% benchmark used by

the Organisation for Economic Co-operation and Development, and more

than enough to maintain pre-retirement living standards.

But a retirees who rent will have much less for living on.

There will be ‘haves’ and more ‘have nots’

Among home-owners, an increasing proportion will be still paying off

their mortgages when they retire – the proportion of 55 to 64 year olds

who own their home outright fell from 72% in 1995-96 to 42% in 2015-16.

Some will (quite rationally) use some or all of their super to pay off

their mortgage.

And rising housing costs will in time force retirees to draw down on more of the value of their home to fund their retirement.

Currently, few retirees downsize or borrow against the equity of

their home while continuing to live in it. But that will have to change.

House prices have outstripped growth in incomes.

Median prices have increased from around four times median incomes in

the early 1990s to more than seven times median incomes today (and more

than eight times in Sydney).

Government policy should continue to encourage these retirees to draw

down on the increasingly valuable equity of their homes to help fund

their retirement. They are not the ones who will need government help.

The government’s recent expansion of the Pension Loans Scheme that allows all retirees to borrow against the value of their homes is a step in that direction.

Retirement is going to change in the years ahead. Most retirees will be far from poor, many of them better able to support themselves than ever before. But an increasing number will not. They are the ones who will need our help.

Authors: Brendan Coates, Fellow, Grattan Institute; Tony Chen, Researcher, Grattan Institute

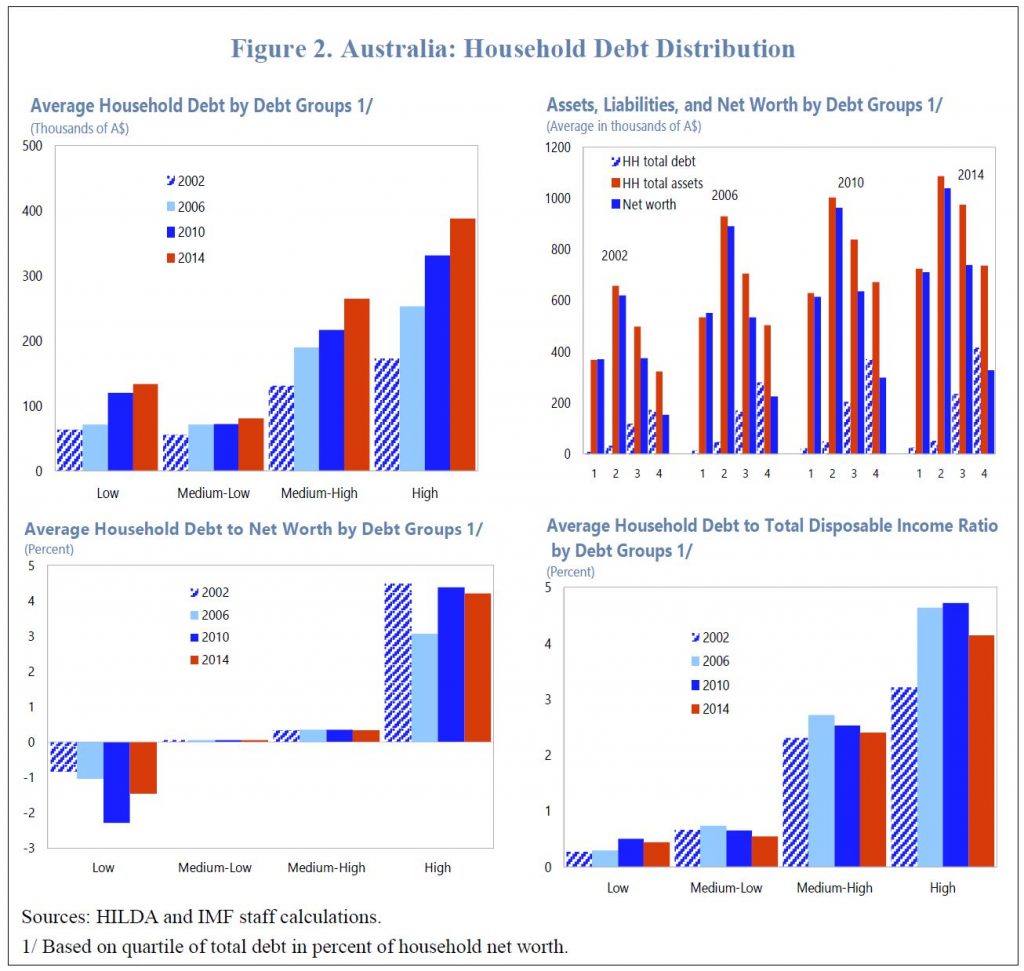

Within its 39 pages, the paper discusses the evolution of the household debt in Australia and finds that while higher-income and higher-wealth households tend to have higher debt, lower-income households may become more vulnerable to rising debt service over time.

Then, the paper analyzes the impact of a monetary policy shock on households’ current consumption and durable expenditures depending on the level of household debt. The results corroborate other work that households’ response to monetary policy shocks depends on their debt and income levels. In particular, households with higher debt tend to reduce their current consumption and durable expenditures more than other households in response to a contractionary monetary policy shocks. However, households with low debt may not respond to monetary policy shocks, as they hold more interest-earning assets.

And we should say at this point that IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and to encourage debate. The views expressed in IMF Working Papers are those of the author(s) and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

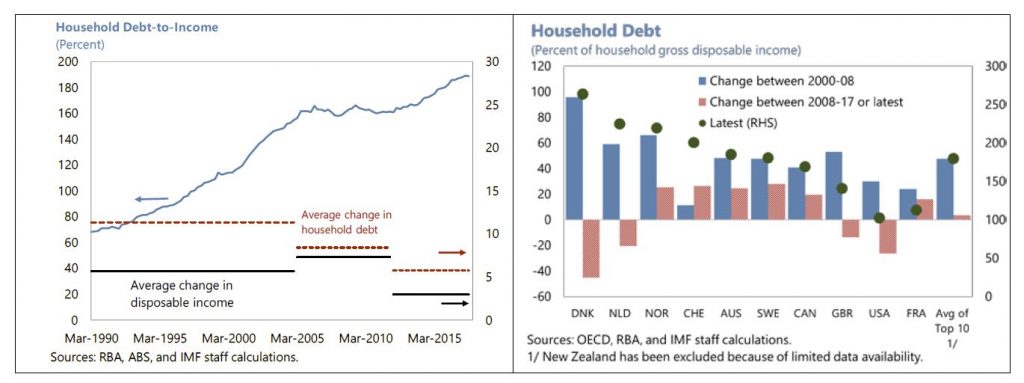

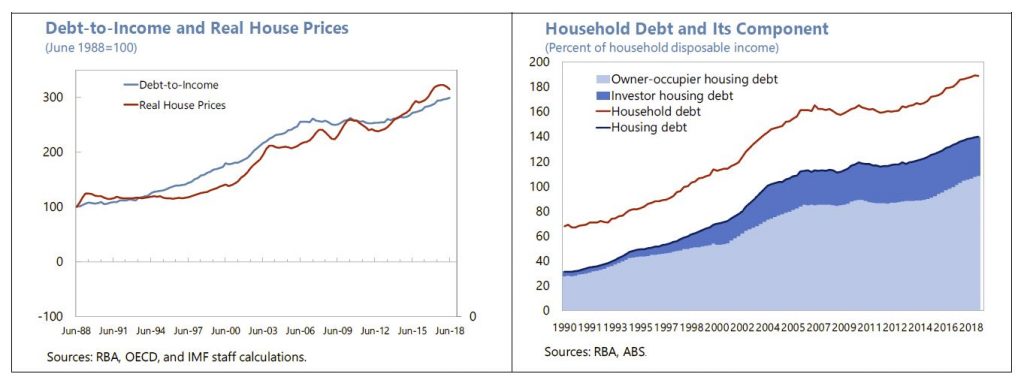

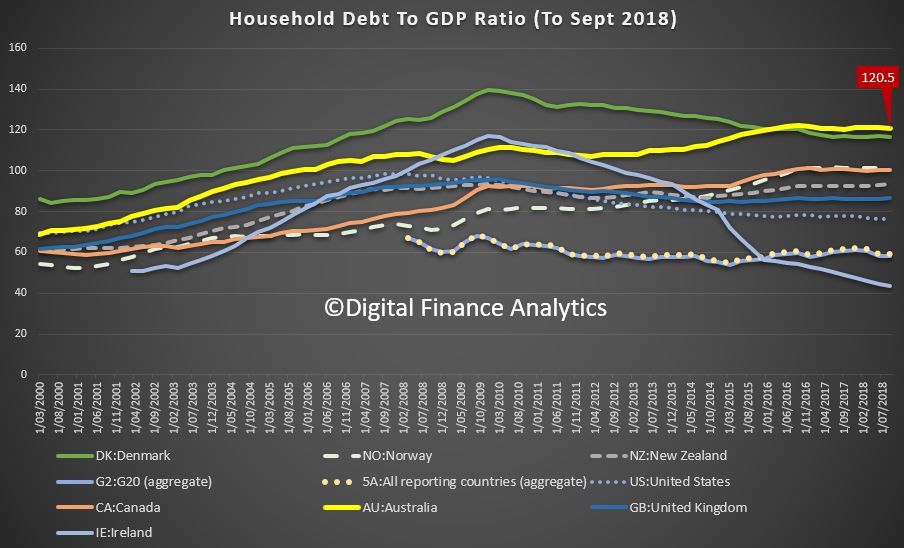

Household debt in Australia has increased to comparatively high levels over the last three decades, a period during which housing prices also have risen rapidly. By end-September 2018, the ratio of household debt to household gross disposable income reached 189 percent, among the highest in advanced economies. High levels of household debt are widely considered to be risky, as they can amplify the impact of external and domestic shocks and, thereby, increase a country’s economic and financial vulnerabilities and pose risks to financial stability. In addition to amplifying financial and economic vulnerabilities, high household debt can also intensify the ongoing corrections in the housing market in Australia.

The macroeconomic impact of and the risks from household debt depend not only on the average debt level but also its distribution across households. Higher-income households might be at lower risk of debt default than lower-income households, for example. The latter might also be more likely to be finance-constrained in times of debt distress. From a monetary policy perspective, a key consideration is the extent to which household debt levels and distribution affect monetary policy transmission.

Household debt in Australia has been rising faster than household disposable income for the past three decades. As a result, the household debt ratio has risen to one of the highest levels among advanced economies.

The housing boom has also played a significant role in the rapid accumulation of household debt. High housing demand due to income and population growth in conjunction with relatively inelastic supply have pushed up house prices, and expectations of future capital gains has encouraged investment demand for housing.

The interaction between the long-term upswing in housing prices and relatively easy mortgage financing has therefore led to the buildup of a high level of residential mortgage debt.

High household debt also reflects the preference for home ownership and housing investment in Australia. Housing debt at 140 percent of household disposable income accounted for about three-quarters of household debt outstanding as of September 2018, with owner-occupied housing debt accounting for a relatively stable share of about one half.

The rise in the share of investor housing debt since 2000 has also contributed to the fast increase in household debt, while other personal debt has remained broadly stable (one quarter of household debt outstanding) at about 46 percent of household disposable income since 2000.

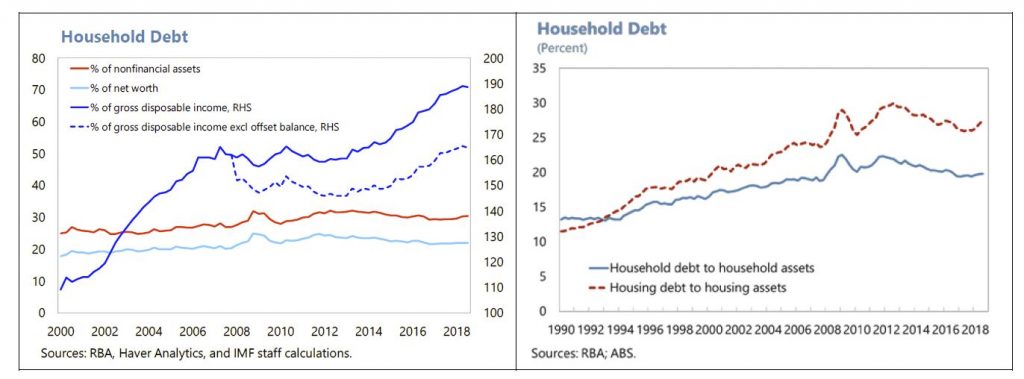

For financial stability, as well as monetary and macroprudential policies, it is not only the level of household debt that matters but also the speed of debt accumulation or leverage increases, the extent of leverage, and, more importantly, the distribution of debt.

The IMF uses old data, from the HILDA survey, which has been running with annual frequency from 2001 to 2016 to make their assessment – clearly the debt position has deteriorated since then, yet they show that debt has grow across the cohorts and segments. The RBA analysis has the same fundamental flaw.

The paper finds that high debt exposure is more prevalent among higher-income and higher-wealth households. Nevertheless, the debt exposure of lower-income and more vulnerable households has also increased over time, and thereby more exposed to risks from rising debt service. The presence of over-indebted households at both low- and higher-income quintiles suggests that macro-financial risks have increased, suggesting a need for close monitoring.

Despite the high debt level, households’ debt service burden has remained manageable due to historical low mortgage interest rates and given that financial institutions assess mortgage serviceability for new mortgage lending with interest rate buffers above the effective variable rate applied for the term of the loans. However, downside risks on debt service capacity and consumption remain with regards to a sharp tightening of global financial conditions which could spill over to higher domestic interest rates.

The empirical analysis investigates the transmission of monetary policy shocks to the current consumption and durable expenditures of households with different debt-to-wealth ratios. With reasonable assumptions and using the large sample of households available in the HILDA survey for 2001-16, the results corroborate that households’ response to monetary policy shocks will vary, depending on both their debt and income levels.

In particular, the results suggest that households with high debt tend to reduce their current consumption and durable expenditures relatively more than other households in response to a contractionary monetary policy shocks. At the same time, households with low debt may not respond to monetary policy shocks, as they hold more interest-earning assets and thereby can smooth their consumption using the higher interest income, suggesting that for these households, the income effect dominates the intertemporal substitution effect.

The results of the analysis suggest that, with a larger share of high-debt households and given their high responsiveness to a monetary policy shock, it may take a smaller increase in the cash rate for the RBA to achieve its policy objectives, compared to past episodes of policy rate adjustments. It corroborates recent RBA research, which suggests that the level and the distribution of the household debt will likely alter monetary policy transmission, in other words, more bang for the buck. By responding gradually, the RBA can still meet its mandates.

The implications of higher household debt for monetary policy have also required that the RBA addresses this challenges in its communication. The results of the textual analysis show that the RBA’s communication has increasingly focused on the impact of household debt on monetary conditions and financial stability over the past decade, consistent with the rise in debt-to-income ratios. Markets have also started to take into account household debt in their assessment of monetary policy and market expectation analysis. Therefore, continuing with a transparent and strengthened communication strategy on issues related to the household debt and household consumption will further improve predictability and efficiency of monetary policy in Australia.

My take is the household debt burden is larger, and more exposed to potential risks than many accept. Nothing new perhaps, but the IMF highlighting the issues is one more piece of the too-high debt narrative!

And according to the AFR, in an exclusive interview, the International Monetary Fund’s lead economist for Australia, Thomas Helbling said Australia’s housing market contraction is worse than first thought, leaving the economy in what he called a “delicate situation” that boosts the need for faster infrastructure spending and even potential interest rate cuts.

Australia’s housing market contraction is worse than first thought!

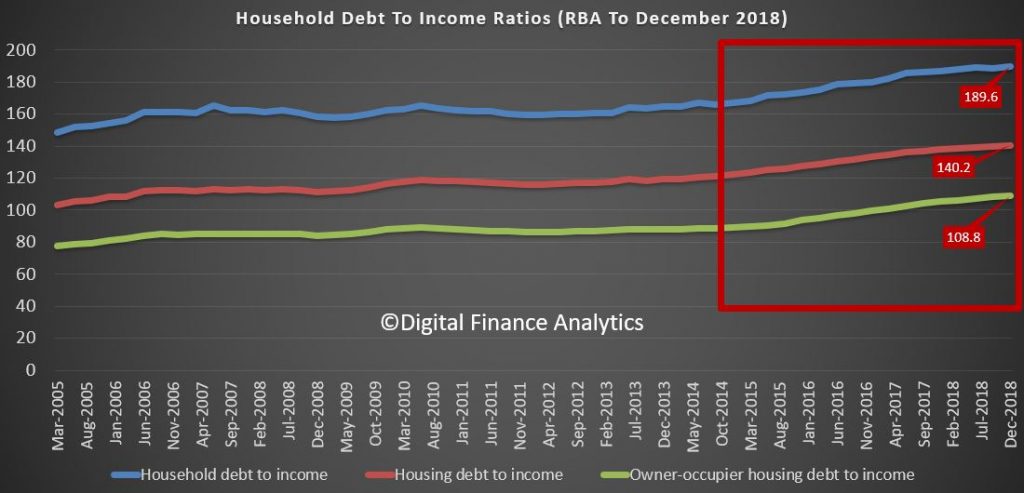

In the latest RBA data series (E2) we get an update on household debt to income and debt to asset ratios, and they are ALL moving in the wrong direction. This is to December 2018.

The household debt to income moved higher to a new record of 189.6, and housing debt to income to a new record of 140.2.

The change in trajectory from 2014/5 is significant, as lending standards were weakened, and interest rates cut (forcing home prices higher).

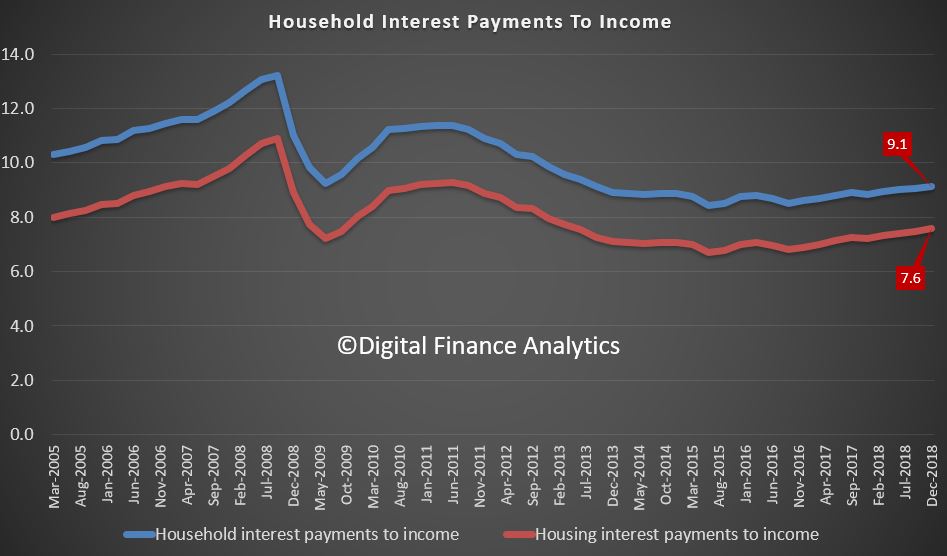

The interest payments to income also rose, thanks to bigger mortgages, slightly higher interest rates, and little income growth.

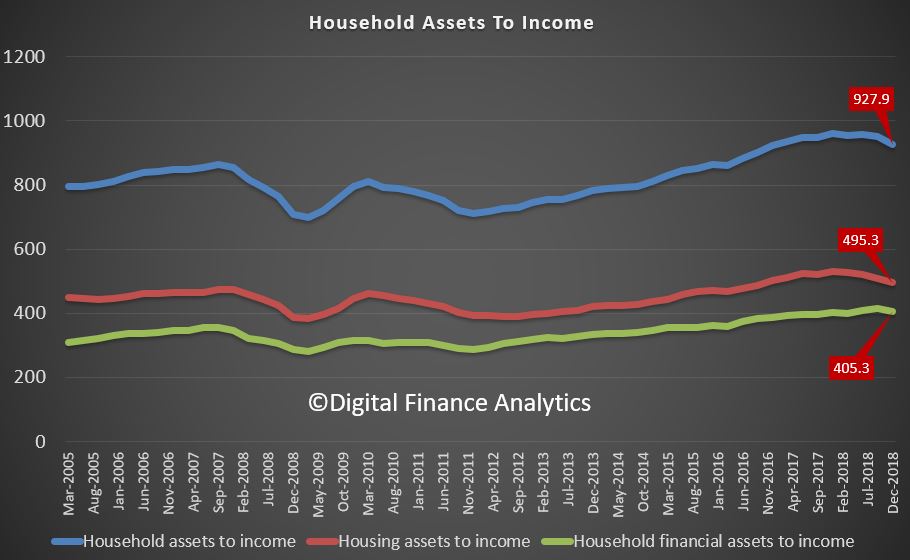

But in contrast, the asset values are falling, so the asset to income ratios are falling. Housing assets in particular are dropping.

All pointing to a higher burden of debt on households. And remember only one third, or there about, have a mortgage, so in fact the TRUE ratios are much much worst. But the trends do not lie in relative terms, and by the way these are extended ratios compared with most western economies. We are drowning in rivers of debt!

My ON THE GROUND METRICS are not as conventional as the MSM economists – then again, I have found these to be great indicators over the years. They haven’t failed me yet and they continue to repeat themselves over the property cycles. The difference with this fall is that it is the MOTHER LOAD the downturn on steroids. And do note, we don’t sit in plush offices with only Eastern Suburbs Data to make up rosy charts and graphs….

1) Shopping centers are running at 60%-70% rental arrears with their tenants. Yes Westfields being one.

2) For-Lease signs popping up like mushrooms in strip-shop areas and malls.

3) Coffee consumption over 13 cafes we have polled has dropped by almost 40% across them and is growing over the months.

4) Pawnshops are seeing an increase in people selling household items, jewelry and the electrical tools.

5) We will see more and more cars with FOR-SALE signs parking along roads and in front of homes.

6) Increase listings on Gumtree and other sights, like I have been receiving more sale notifications on FaceBook pages.

7) More and more calls to assist solicitors with property disputes due to financial tress.

These are my on the ground indicators combined with the property sales and listing data we receive from over 150 agencies across NSW. Hope it helps and please do share what you are seeing on the ground as you go for daily jog…

In an article, released by the US FED via the first issue of Consumer & Community Context, they explore the impact that rising student loan debt levels may have on home ownership rates among young adults in the US. They suggest that higher debt overall helps to explain lower home ownership.

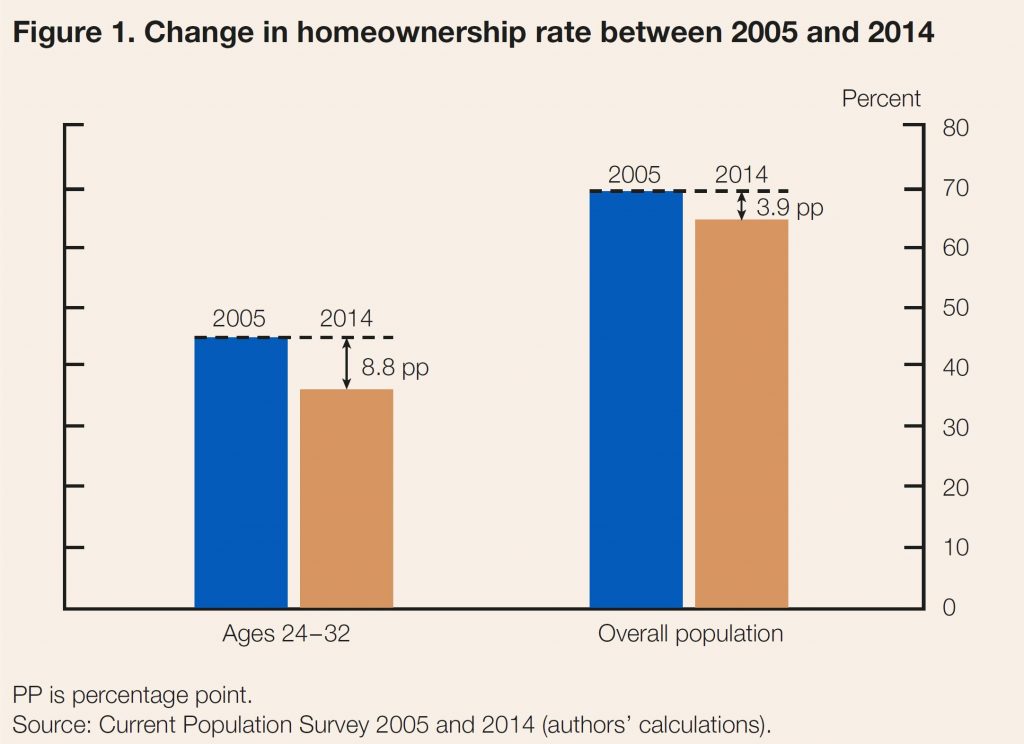

The home ownership rate in the United States fell approximately 4 percentage points in the wake of the financial crisis, from a peak of 69 percent in 2005 to 65 percent in 2014. The decline in home ownership was even more pronounced among young adults. Whereas 45 percent of household heads ages 24 to 32 in 2005 owned their own home, just 36 percent did in 2014—a marked 9 percentage point drop

While many factors have influenced the downward slide in the rate of home ownership, some believe that the historic levels of student loan debt have been particular impediments. Indeed, outstanding student loan balances have more than doubled in real terms (to about $1.5 trillion) in the last decade, with average real student loan debt per capita for individuals ages 24 to 32 rising from about $5,000 in 2005 to $10,000 in 2014.3 In surveys, young adults commonly report that their student loan debts are preventing them from buying a home.

They estimate that roughly 20 percent of the decline in home ownership among young adults can be attributed to their increased student loan debts since 2005. Our estimates suggest that increases in student loan debt are an important factor in explaining their lowered home ownership rates, but not the central cause of the decline.

Estimating the Effect of Student Loan Debt on Home ownership

The relationship between student loan debt and home ownership is complex. On the one hand, student loan payments may reduce an individual’s ability to save for a down payment or qualify for a mortgage. On the other hand, investments in higher education also, on average, result in higher earnings and lower rates of unemployment. As a result, it is not immediately clear whether, on balance, the impact of student loan debt on home ownership would be positive or negative.

Since we are interested in isolating the negative effect of increased student loan burdens on home ownership from the potential positive effect of additional education, our analysis aims to estimate the effect of debt on home ownership holding all other factors constant. In other words, if we were to compare two individuals who are otherwise identical in all aspects but the amount of accumulated student loan debt, how would we expect their home ownership outcomes to differ?

To estimate the effect of the increased student loan debt on home ownership, we tracked student loan and mortgage borrowing for individuals who were between 24 and 32 years old in 2005. Using these data, we constructed a model to estimate the impact of increased student loan borrowing on the likelihood of students becoming homeowners during this period of their lives. We found that a $1,000 increase in student loan debt (accumulated during the prime college-going years and measured in 2014 dollars) causes a 1 to 2 percentage point drop in the home ownership rate for student loan borrowers during their late 20s and early 30s. Our estimates suggest that student loan debt can be a meaningful barrier preventing young adults from owning a home. Next, we apply these estimates to another interesting question: How much of the 9 percentage point drop in the home ownership rate of 24 to 32 year olds between 2005 and 2014 can be attributed to rising student loan debt?

The Rise in Student Loan Debt and Decline in Home ownership since 2005 Answering this question requires two steps. First, we calculate an expected probability of home ownership in 2005 for each individual in our sample using the estimated model from our previous research. Second, we produce a simulated scenario for the probability of home ownership by increasing each individual’s debt to match the student loan debt distribution of this age group in 2014. The difference between the probabilities calculated in these two steps determines the effect of the increased debt on the home ownership rate of the young, holding demographic, educational, and economic characteristics fixed.

This exercise captures two key dimensions of the shifts in the distribution of student loan debt between 2005 and 2014, in addition to the overall increase in the average amounts borrowed. First, the fraction of young individuals who have borrowed to fund post secondary education with debt has increased by roughly 10 percentage points over this period, from 30 to 40 percent. Second, the amounts borrowed at the upper end of the distribution increased more rapidly than in the middle.

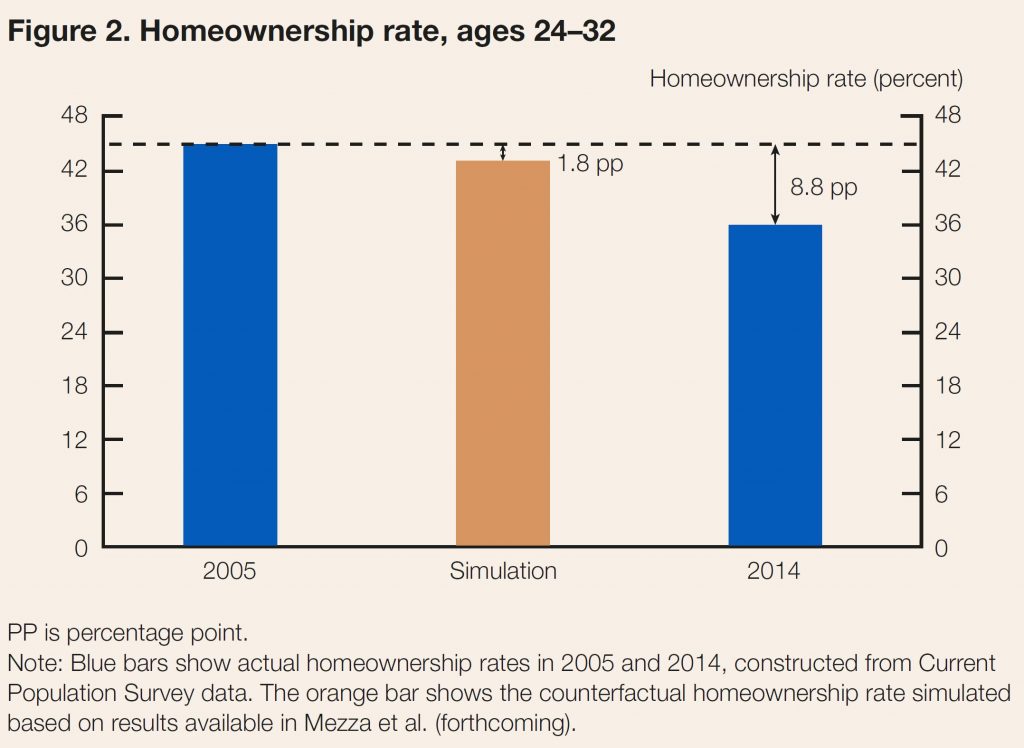

According to our calculations, the increase in student loan debt between 2005 and 2014 reduced the home ownership rate among young adults by 2 percentage points. The home ownership rate for this group fell 9 percentage points over this period (figure 2), implying that a little over 20 percent of the overall decline in home ownership among the young can be attributed to the rise in student loan debt. This represents over 400,000 young individuals who would have owned a home in 2014 had it not been for the rise in debt.

An important caveat to keep in mind when interpreting our estimates is the difference in mortgage market conditions before and after the financial crisis. The model used to develop these estimates was built using data for student loan borrowers who were between 24 and 32 years old in 2005, so a large fraction had made their home-buying decisions before 2008, when credit was relatively easier to obtain. Following the crisis, loan underwriting may have become more sensitive to student loan debt, increasing its importance in explaining declining home ownership rates.

Student Loan Debt May Have Even Broader Implications for Consumers

There are multiple channels by which student loans can affect the ability of consumers to buy homes. One we would like to highlight here is the effect of student loan debt on credit scores. In our forthcoming paper, we show that higher student loan debt early in life leads to a lower credit score later in life, all else equal. We also find that, all else equal, increased student loan debt causes borrowers to be more likely to default on their student loan debt, which has a major adverse effect on their credit scores, thereby impacting their ability to qualify for a mortgage.

This finding has implications well beyond home ownership, as credit scores impact consumers’ access to and cost of nearly all kinds of credit, including auto loans and credit cards. While investing in post secondary education continues to yield, on average, positive and substantial returns, burdensome student loan debt levels may be lessening these benefits. As policymakers evaluate ways to aid student borrowers, they may wish to consider policies that reduce the cost of tuition, such as greater state government investment in public institutions, and ease the burden of student loan payments, such as more expansive use of income-driven repayment.

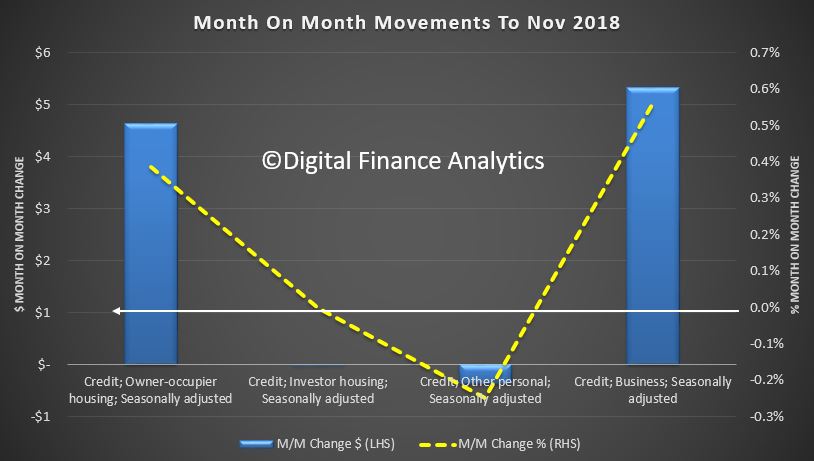

As we approach the end of the year, we got some stats from the RBA on credit to the end of November. Whilst the debt is growing the value of the housing assets are falling, this is a nasty pincer movement!

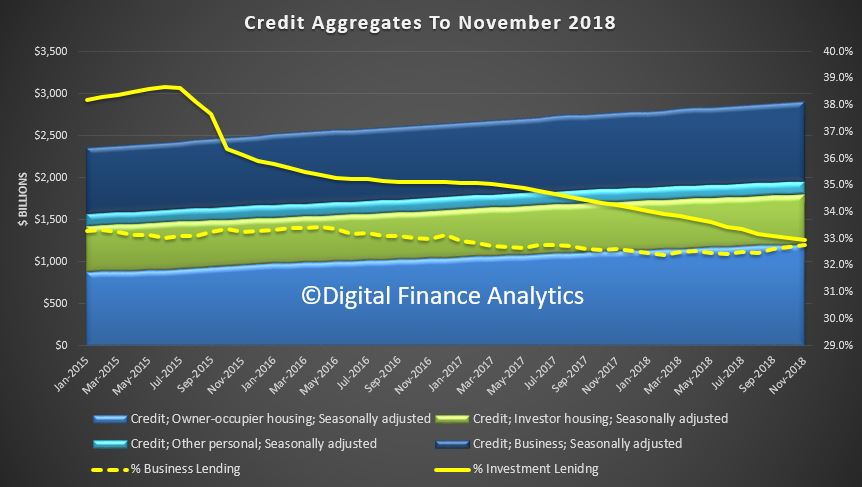

Their credit aggregates reveals that in seasonally adjusted terms total credit rose by 0.34% or $9.9 billion dollars, to a new record of $2.9 trillion dollars.

Within that credit for owner occupied housing rose 0.38%, or $4.63 billion to a new record $1.21 trillion dollars, lending for property investment was flat, standing at $0.59 trillion dollars and lending for business rose 0.56%, or $5.32 billion to $0.95 trillion dollars, another record. The proportion of business lending to all lending rose to 32.8%, while the share of residential property lending for investment property fell to 32.9%, the lowest in years (but still too high in my book!). Credit growth is too fast.

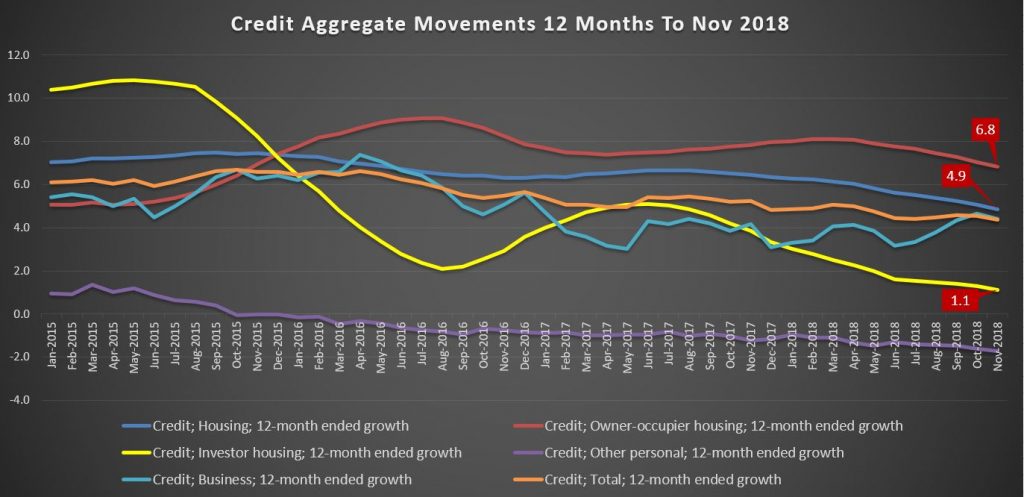

The trend charts show that on a 12 month basis, investment lending has now only growth 1.1%, while owner occupied lending is still running at 6.8%, still faster than business lending. Personal credit continues to fall.

This indicates that despite all the hype about tight lending, loans are still being written, at a growth rate which is well above inflation and income. As a result the total debt burden is still rising. RBA please note.

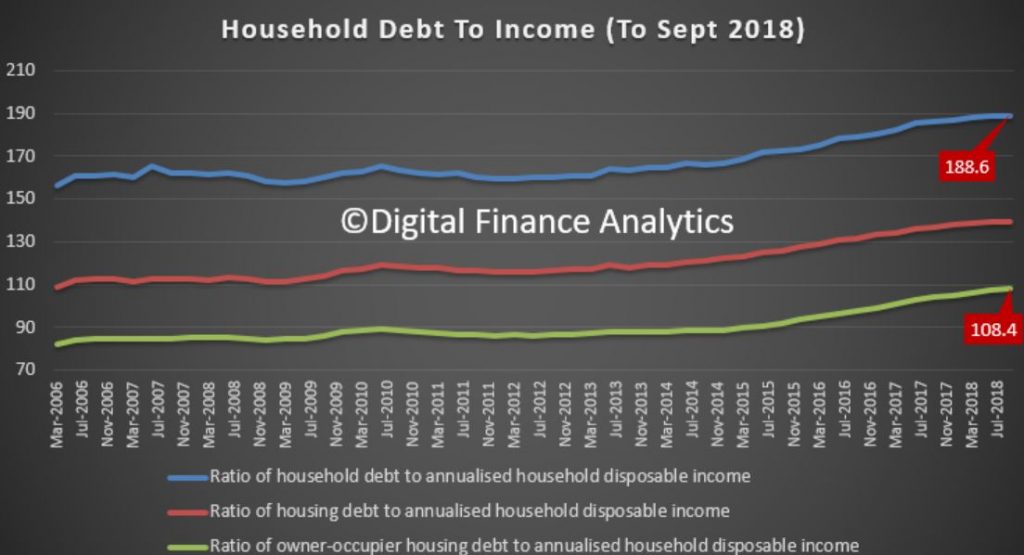

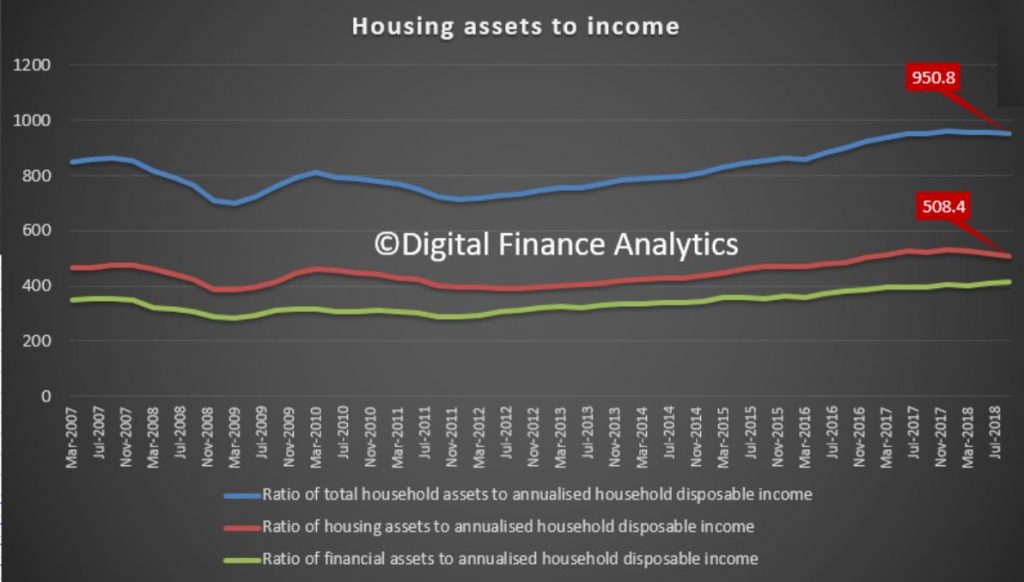

We can see the consequences working out by looking at the latest Household Finance Ratios from the RBA, using ABS data

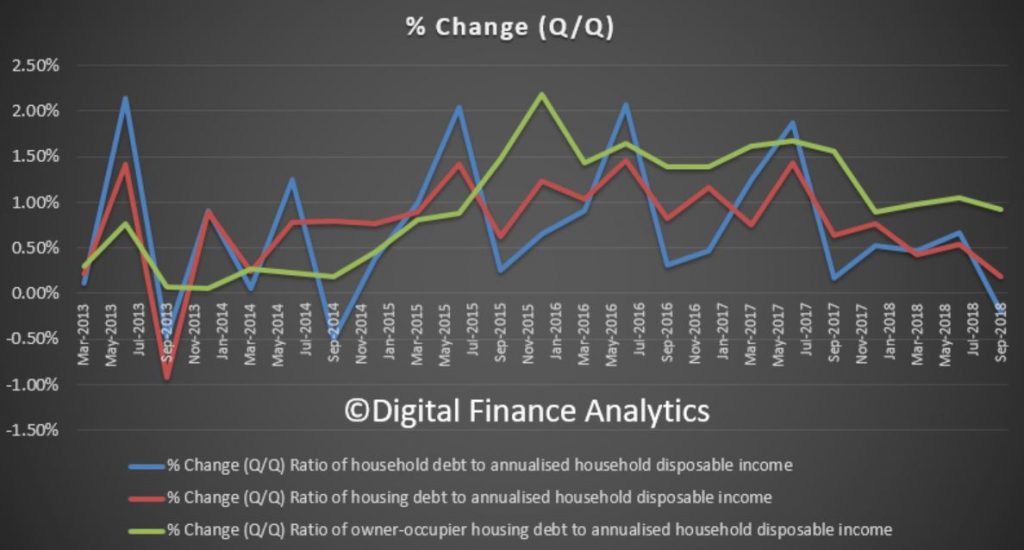

This shows that total household debt to income to September 2018 fell from 189 to 188.6, whilst the housing debt to income rose from 139.4 to 139.6 and the owner occupied ratio rose from 107.4 to 108.4. Now this ratio includes households and unincorporated businesses – small businesses essentially. So we see the continued consolidation of debt around housing, while other forms of debt, such as credit cards, diminished. In fact, the change quarter on quarter for owner occupied housing debt is close to 1%, so have no doubt, debt relative to income for housing is still rising.

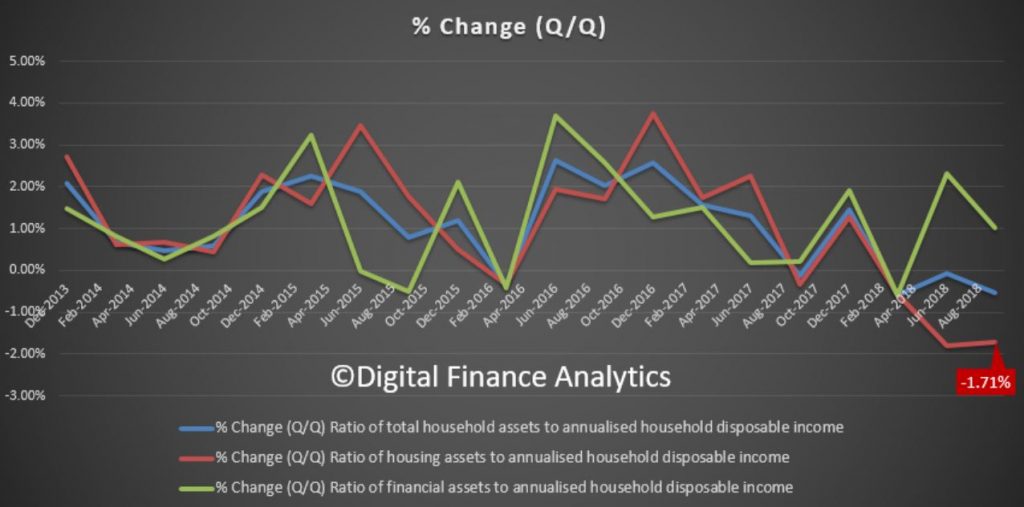

The assets to income data in the same series fell, thanks to the fall in value of housing.

The ratio of household assets to income fell from 956.0 to 950.8, the ratio of housing assets to income fell from 517.3 to 508.4, down 1.7% in the quarter and 2.7% for the year to date, while the ratio of financial assets (stocks etc.) lifted from 410.3 to 414.5 (though will be lower now thanks to the recent market falls). In other words, whilst the debt is growing the value of the housing assets are falling – a double whammy.

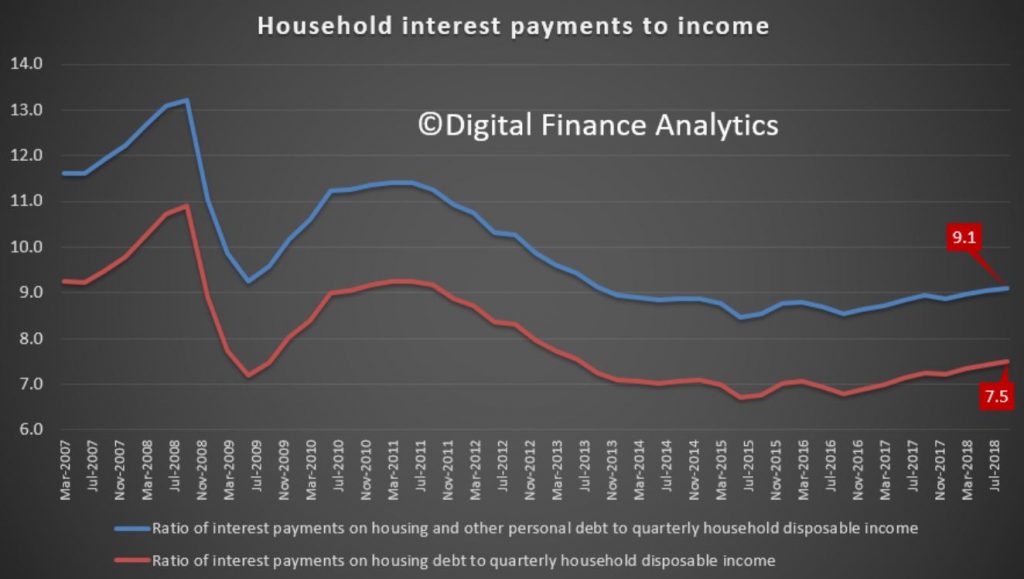

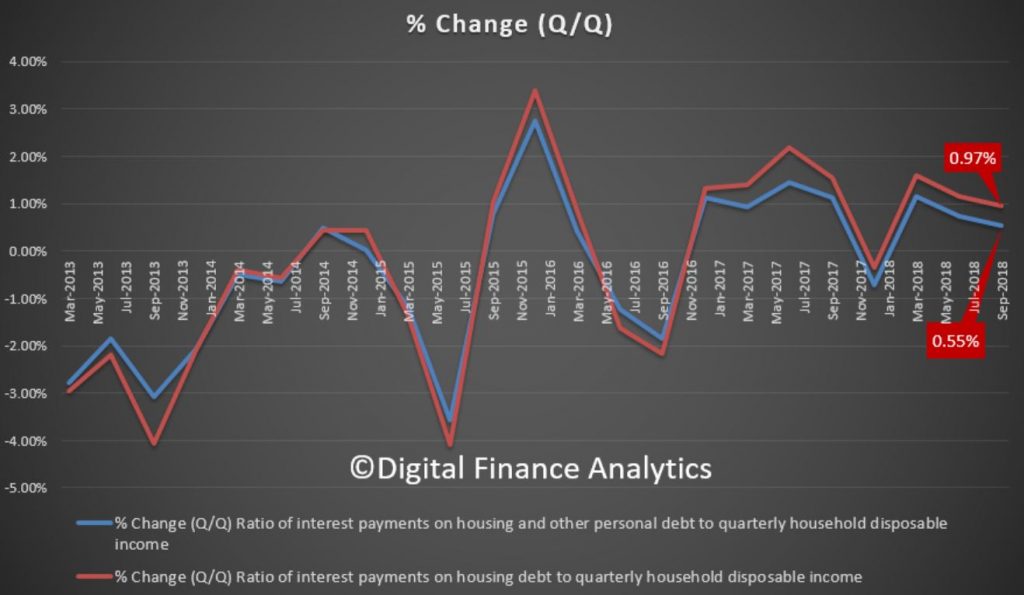

The final dimension is interest payments to debt, both of which are higher (thanks to bigger loans and only small changes in mortgage rates).

The ratio of housing debt interest repayments to income rose from 7.4 to 7.5 per cent and interest payments on all debt rose from 9.0 to 9.1 percent. This is confirming the growth trend since 2016, where the out of cycle interest repayments hit.

The point to note here is that the one third of households with mortgage debt are seeing a rise in the share of income going to support the interest repayments – at these extremely low, emergency interest rates. And that is the point, the averages mask the marginal borrower who remains under extreme pressure, which is why mortgage stress continues to rise. We will report on the December data in a week or so.

So the key take away as we move into 2019 is the debt machine is still working, more households are being encouraged to get deeper into debt, despite the clear evidence of massive over borrowing. A strategy applauded by the RBA, the Treasury and the Banks!

We really need a change in strategy because debt fueled household consumption and property speculation will be one of the nails in the economies coffin down the track. Interest rates will rise. The other is sporty corporate borrowing, but that is a story for another day!

Finally, seasons greetings to all our followers, and our best wishes for (a debt free) 2019!

Interesting research from the US, which shows that households who get into financial difficulty may make up a minority of all households, but they tend to stay in this state for an extended period. This is exacerbated by high default fees and charges, and an impatience to consume.

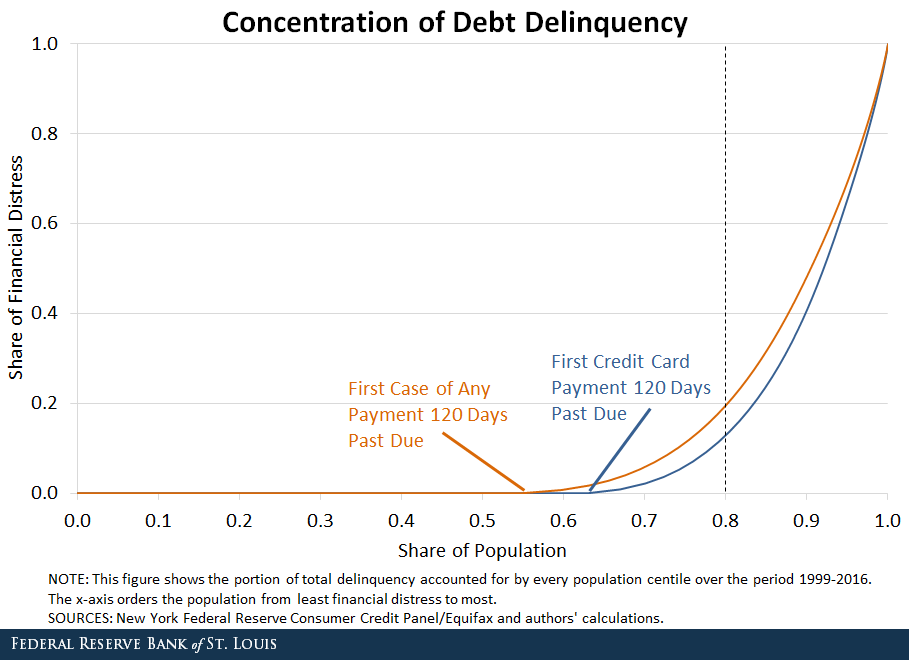

When households lose income unexpectedly, they may skip debt payments (such as credit card payments) rather than lower their consumption. Given that most everyone will experience unanticipated income changes at some point, one may expect that a majority of households fell (at least temporarily) into financial distress sometime between 1999 and 2016. The findings in this post challenge that view: The data show financial distress to be highly concentrated in a relatively small share of the population.

Measuring Financial Distress

We used data from the New York Federal Reserve Consumer Credit Panel/Equifax to show the concentration of debt delinquency across a nationwide sample of people with credit reports. “Total delinquency” refers to the total number of quarters in which people in our sample had debt payments that were 120 days delinquent or more.

The graph below orders the population from least financial distress to most and presents the portion of total delinquency accounted for by every population centile. This is done in two separate lines for credit card debt and for any kind of debt.1

Debt Delinquency Concentration

The first major fact to emerge is that debt delinquency was highly concentrated over the period 1996-2016. About 60 percent of people never have debt payments 120 days late. On the other extreme, 20 percent of people accounted for 80 percent of financial distress, and around 10 percent of people accounted for 50 percent.

This points to the fact that delinquency is frequent among those who experience it. In fact, more than 30 percent of people who had debt 120 days delinquent at any point in our sample spent at least a quarter of their time in that state.

Effect of Credit Card Delinquency

A second major fact to emerge is that much of the trend in financial distress concentration was driven by credit card delinquency. This makes sense given that credit cards are a widely used debt instrument.

Addressing Financial Distress

In light of the remarkable concentration and persistence of financial distress, it is important for policymakers to be able to disentangle the causes. What factors drive some people to be in financial distress for so long and others to never experience it?

In a working paper titled “The Persistence of Financial Distress,” Fed economists Juan M. Sánchez, José Mustre-del-Río and Kartik Athreya examined this question.2 Specifically, they showed that while traditional economic models of defaultable debt cannot account for the observed concentration and persistence of financial distress, a model which also accounts for high penalty rates on delinquent debt and individuals’ heterogeneity in impatience to consume can do so with a high degree of accuracy.