The statement delivered today by RBA Governor, Philip Lowe, to the House of Representatives Standing Committee on Economics contains the now familiar nod towards risks associated with high household debt. “Too much borrowing today can create problems for tomorrow, because debt does have to be repaid”. Exactly!

One area that we are watching closely is the cycle in residential construction activity, as the upswing has helped support the economy over recent years. The rate of new building approvals has slowed, but there is a large amount of work still in the pipeline, particularly for apartments, so we still expect some further growth in this part of the economy this year. There has, however, been some tightening in conditions for property developers in some markets.

In the broader housing market, the picture remains quite complicated. There is not a single story across the country. In parts of the country that have been adjusting to the downswing in mining investment or where there have been big increases in supply of apartments, housing prices have declined. In other parts, where the economy has been stronger and the supply-side has had trouble keeping up with strong population growth, housing prices are still rising quickly. In most areas, growth in rents is low. And recently we have seen a pick-up in growth in credit to investors, which needs to be watched carefully.

In terms of consumer prices, a year ago we had expected the inflation rate to remain above 2 per cent. It has turned out to be lower than this last year, at around 1½ per cent. Wage growth has been quite subdued, reflecting spare capacity in the labour market and the adjustment to the unwinding of the mining investment boom. We anticipate the subdued outcomes to continue for a while yet. Increased competition in retailing is also having an effect on prices, as is the low rate of increase in rents.

We do not expect the rate of inflation to fall further. Our judgement is that there are reasonable prospects for inflation to rise towards the middle of the target over time. The recent improvement in the global economy provides some extra assurance on this front. Headline inflation is expected to be back above 2 per cent later this year, boosted by higher prices for petrol and tobacco. The pick-up in underlying inflation is expected to be more gradual.

Since we appeared before this Committee last September, the Reserve Bank Board has kept the cash rate unchanged at 1.5 per cent.

At its recent meetings the Board has been paying close attention to the outlook for inflation as well as two other issues: trends in household borrowing and in the labour market.

One of the ways in which monetary policy works is to make it easier for people to borrow and spend. But there is a balance to be struck. Too much borrowing today can create problems for tomorrow, because debt does have to be repaid. At the moment, most households with borrowings do seem to be coping pretty well. But the current high level of debt, combined with low nominal income growth, is affecting the appetite of households to spend, and we are seeing some evidence of this in the consumption figures. The balance that is required is to support spending in the economy today while avoiding creating fragilities in household balance sheets that could cause problems for the economy later on. This is also something we need to watch carefully.

Trends in the labour market are also important. As in the housing market, the picture in the labour market varies significantly around the country. Overall, the unemployment rate has been steady now for a little over a year at around 5¾ per cent. In a historical context this would have been considered a good outcome, although, today, a sustainably lower unemployment rate should be possible in Australia. The other aspect of the labour market that is worth noting is the continuing trend towards part-time employment. Over the past year, all the growth in employment is accounted for by part-time jobs. There is a structural element to this, but it is also partly cyclical. We expect that the unemployment rate will remain around its current level for a while yet.

The Reserve Bank Board continues to balance these various issues within the framework of our flexible medium-term inflation target, which aims to achieve an average rate of inflation over time of 2 point something. Our judgement is that the current setting of the cash rate is consistent with both this and achieving sustainable growth in our economy. We will continue to review that judgement at future meetings.

The RBA Governor gave a speech comparing aspects of the Australian and Canadian economies. I found the comparisons relating to housing interesting. In summary, high prices, high debt, and high risk.

We have both had strong housing markets over recent years and there are concerns about the level of household indebtedness. There are some similarities in the factors at work.

One is that our populations have been growing quickly for advanced industrialised countries. In Australia, population growth has averaged 1.7 per cent over the past decade, while in Canada it has averaged 1.1 per cent. Over the past couple of years the growth rates have moved closer together.

Another similarity is that there has been strong demand from overseas residents for investments in residential property, particularly in our wonderful Pacific-rim cities. Not only are these cities attractive places to live, but we also offer investors security of property rights and economic and financial stability. Given the strong demand and its impact on prices in some areas, some state and provincial governments have recently levied additional taxes on foreign investors in residential property.

Our housing markets have also been affected by the global monetary environment. We both run independent monetary policies, but the level of our interest rates is influenced by what happens elsewhere in the world. With interest rates so low and our economies being resilient, it is not so surprising that people have found it an attractive time to borrow to buy housing.

Another characteristic that we have in common is that at a time of strong demand from both residents and non-residents, there are challenges on the supply side. I understand that zoning is an issue in Canada, just as in Australia. In some parts of Australia, there has also been underinvestment in transport infrastructure, which has limited the supply of well-located land at a time when demand for such land has been growing quickly. The result is higher prices.

We are also both experiencing large differences across the various sub-markets within our countries. The strength in housing markets in our major cities contrasts with marked weakness in the mining regions following the end of the mining investment boom.

The increase in overall housing prices in both our countries has gone hand in hand with a further pick-up in household indebtedness. In both countries the ratio of household debt to income is at a record high, although the low level of interest rates means that the debt-servicing burdens are not that high at the moment.

In Australia, the household sector is coping reasonably well with the high levels of debt. But there are some signs that debt levels are affecting household spending. In aggregate, households are carrying more debt than they have before and, at the same time, they are experiencing slower growth in their nominal incomes than they have for some decades. For many, this is a sobering combination.

Reflecting this, our latest forecasts were prepared on the basis that growth in consumption was unlikely to run ahead of growth in household income over the next couple of years; in other words the household saving rate was likely to remain constant. This is a bit different from recent years, over which the saving rate had trended down slowly.

This interaction between consumption, saving and borrowing for housing is a significant issue and one that I know both central banks are watching carefully. It is one of the key uncertainties around our central scenario for the Australian economy. It was also cited as one of the key risks for the inflation outlook in the Bank of Canada’s latest Monetary Policy Report. We are still learning how households respond to higher debt levels and lower nominal income growth.

When we published our sensitivity analysis on mortgaged households, which shows that more than 20% were on the edge financially speaking even at current low rates, a number of people asked why this was so, given the assumed affordability buffers and other underwriting safeguards.

Well, apart from the obvious issues of static incomes, rising costs of living, and potentially higher interest rates ahead, many mortgaged households also have other debts to repay. So today we run through some of our survey results looking at these other household debts. And it is not pretty.

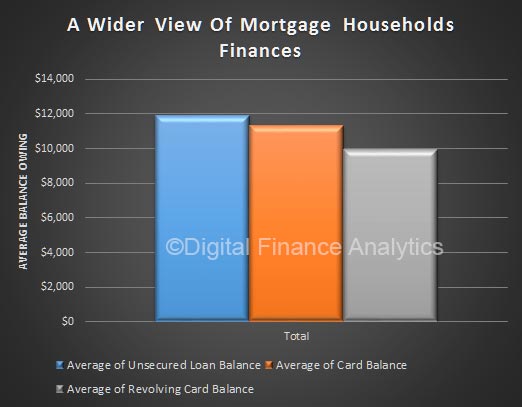

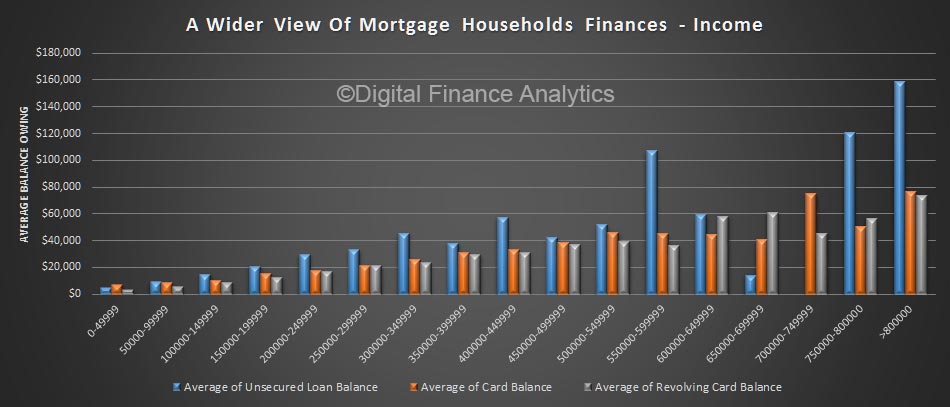

To start, here is the average balances for mortgaged households, looking at their use of unsecured credit (e.g. personal loans, store cards etc) and credit cards. In the case of credit cards, we show two balances, first the current outstanding balance, and second the average revolving (hard core) debt outstanding. Households with debts, on average and on top of the mortgage have $12,000 in unsecured loans, $11,000 in card debt, of which $10,000 is revolving. These can cost as much to service each month as the mortgage repayment!

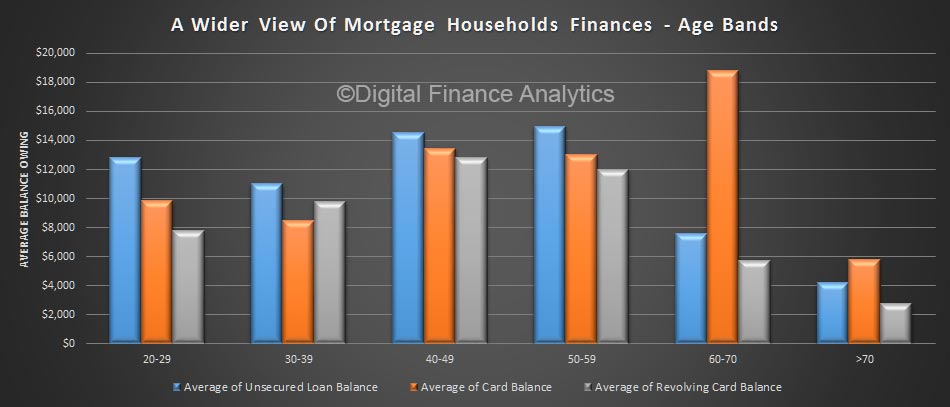

We can slice and dice the households, using some of our custom SQL views. For example, here are the average balances by household age bands. Households between 40 and 59 have the larger loan and revolving balances, though interestingly, those 60-70 have the largest card balances.

As incomes rise, debt levels also rise, so some of the debt is owned by households with more ability to repay. However, remember the larger number of households are in the first three bands, where debt is still rife.

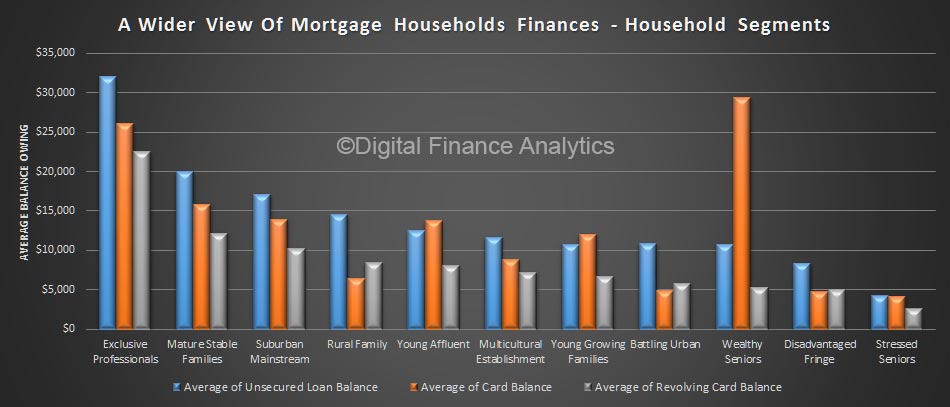

We can examine this debt by our master household segments. Once again, more affluent households have larger debts, but young growing families have on average close to $20,000 in debt, including some on revolving cards (where interest is charged at a high rate).

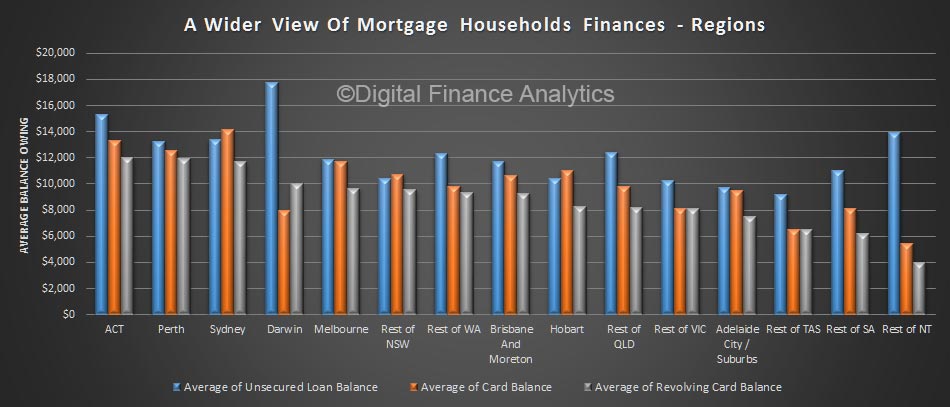

We can examine the data across our regions. Urban centres, including ACT, Greater Sydney and Melbourne have the highest debt levels. Many of these households also hold the largest mortgages.

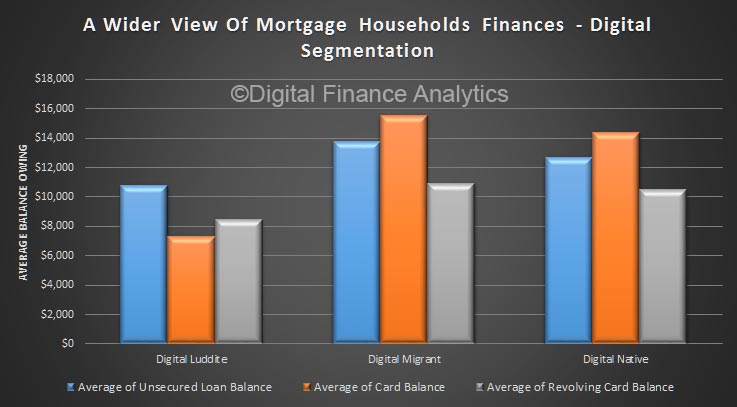

Finally, it is interesting to note that from a digital behaviour standpoint, those younger households who are online most of the time and prefer to use digital channels (Natives) borrow more than Luddites (those who prefer not to go online, but the larger debts are held by households who have migrated online. These Migrants are progressively using online channels more than ever. You can read more about our channel use inour report The Quiet Revolution.

So, to sum up. Many households have large mortgages AND other debts, including credit cards and personal loans. This entire portfolio of debt must be considered when looking at their sensitivity to rising rates, and when comparing static incomes with rising debt repayments. Just looking at the mortgage gives only part of the full picture.

Much of this debt would not exist when the bank made their mortgage underwriting decision. That point in time view however does not necessarily still hold true. Should ongoing affordability testing be required by the regulators?

The Reserve Bank today kept interest rates at a record low of 1.5%. Such low rates create economic uncertainty – and if Australia’s historical GDP growth is anything to go by, consumers face more uncertainty than the bottoming out of interest rates would usually suggest.

This is because high house prices lead home-owners to feel wealthy, yet the economy as a whole does not convey a message of wealth to all consumers.

Boom and bust come and go, and sometimes you can be forgiven for feeling economic déjà vu. But how might Australians react to record low rates this time around? Business moves in cycles over time, so economists sometimes look to history as a guide to what might happen next.

A flattening out of interest rates can mean many possibilities for consumers and businesses. Historical GDP growth rates would indicate that the business cycle is at the same stage as in 2011. But what this means for consumers depends on how the other economic “stars” align. The indicators from 2011 are able to provide a model of how consumers may react over the coming years.

Does 2011 provide a model?

The relationship between interest rates and unemployment has been of interest since target interest rates were introduced in 1990.

The rise in unemployment from 4% to 6% between July 2008 and May 2009 occurred at the same time as the Reserve Bank rapidly slashed the target interest rates.

However, with the Reserve Bank now unlikely to reduce interest rates any further, the impact on unemployment and other pointers for consumer behaviour may be different this time compared to 2011.

To predict consumer behaviour in the current uncertain conditions, the most appropriate method would be to consider past situations where GDP has gone up, and reflect on changes to key consumer indicators.

Based on Australia’s current GDP growth rates, and those of the last few decades, we are most likely at the “February 2011” stage of the business cycle – when growth was at 1.9%.

Based on the business cycle method of anticipating future consumer indicators, we would expect the trend to continue. Consumers would save the same or less of their income. And consumer sentiment would remain flat.

However, with property prices at all-time highs in capital cities, it is possible this will counteract rising interest rates when it comes to consumer expectations because there are conflicting messages. On the one hand, consumers feel wealthy because of property prices. However, they are expecting their mortgage repayments to increase when interest rates start to tick up.

In this environment it is expected that unemployment remains steady, as it has since 2009, with the sharemarket remaining flat. It is expected that as the sharemarket remains flat (or modestly increases) across developed countries, the price of gold continues to rise.

We can make these sorts of predictions, if 2011 is a guide to what will happen in the coming years.

ASX

But using 2011 as a benchmark to help predict future trends relies on the basic academic assumption that the points of reference (2011 and 2017) are identical. The world of 2011 was vastly different from the world today – it was almost naively uncomplicated.

Further dampening effects?

The differences between 2011 and 2017 will likely result in further dampening effects on the economic recovery. One of the major potential dampeners is Australia’s relatively high level of government debt.

The reduction in government debt in 2007 occurred almost simultaneously with the global financial crisis, higher consumer saving rates and a steady decline in GDP growth each quarter.

Hence, core economic fundamentals (such as how cutting government spending when the economy is already shaky will likely result in a greater negative GDP impact than when the economy is strong) deem that if the current government takes steps to reduce debt, this could have further dampening effects on the economy. This is despite a bottoming out of interest rates, which indicates the economy is projected to be on the way up.

Today’s world poses many challenges to forecasting how consumers will behave. One of the primary issues is high levels of debt (both for consumption and for property), which means a rise in interest rates will directly impact Australians. However, high property markets give consumers a feeling of wealth, despite the extreme lack of diversification across asset classes, and property that is hard to sell.

These competing forces mean consumers are likely to view formal government announcements with more scrutiny. As statements are made about improving economic prospects, individual consumers are feeling financial strain.

Combine these forces with increasing market complexity, product advances, geopolitical issues and climate change, and a certain level of unease is weighing on Australian minds, which goes over and above the likely increase in mortgage repayments.

A lot has changed since 2011

Technology disruptions are likely to further reduce trust in institutions, particularly banks, but may ultimately give consumers a greater feeling of empowerment and control.

In 2011, technological financial disruption was just a sparkle in Bitcoin’s eye. Now, technological disruption covers every sector imaginable. Many consider the future economy will be the collaborative economy.

The collaborative economy is one in which consumers and businesses share their resources (for a fee). This increases efficiency and saves cost to the end consumer.

For example, AirBnB (the largest accommodation provider in the world, which owns no accommodation) connects people who have extra space with travellers who are seeking an authentic, low-cost experience while travelling.

If the shift toward the collaborative economy continues, large institutions – particularly banks – will find it more difficult to make the significant profits they are used to.

Since 2011, consumers across the world have shifted to more community-based banking systems and have lent directly to others to achieve higher interest rates than bank deposits – particularly in a low-interest-rate environment. This trend is likely to continue.

Coupled with decreasing trust in institutions, it makes it unlikely that the predicted trends will be identical to those in 2011.

Author: Katherine Hunt , Lecturer in Accounting, Finance and Economics, Griffith University

A 1 percentage point increase in the household debt-to-GDP ratio tends to lower growth in the long run by 0.1 percentage point. Our results suggest that the negative long-run effects on consumption tend to intensify as the household debt-to-GDP ratio exceeds 60%. For GDP growth, that intensification seems to occur when the ratio exceeds 80%.

Moreover, the negative correlation between household debt and consumption actually strengthens over time, following a surge in household borrowing. What is striking is that the negative correlation coefficient nearly doubles between the first and the fifth year following the increase in household debt.

This is explained by massive amounts of borrowing for housing (both owner occupied and investment) whilst unsecured personal debt is not growing. Such high household debt, even with low interest rates sucks spending from the economy, and is a brake on growth. The swelling value of home prices, and paper wealth (as well as growing bank balance sheets) do not really provide the right foundation for long term real sustainable growth.

Note: BIS Working Papers are written by members of the Monetary and Economic Department of the Bank for International Settlements, and from time to time by other economists, and are published by the Bank. The papers are on subjects of topical interest and are technical in character. The views expressed in them are those of their authors and not necessarily the views of the BIS.

Here is a segment in which we discuss our latest research into the probability of default modelling in a rising interest rate environment. We highlight the rise of the “Affluent Stressed” households.

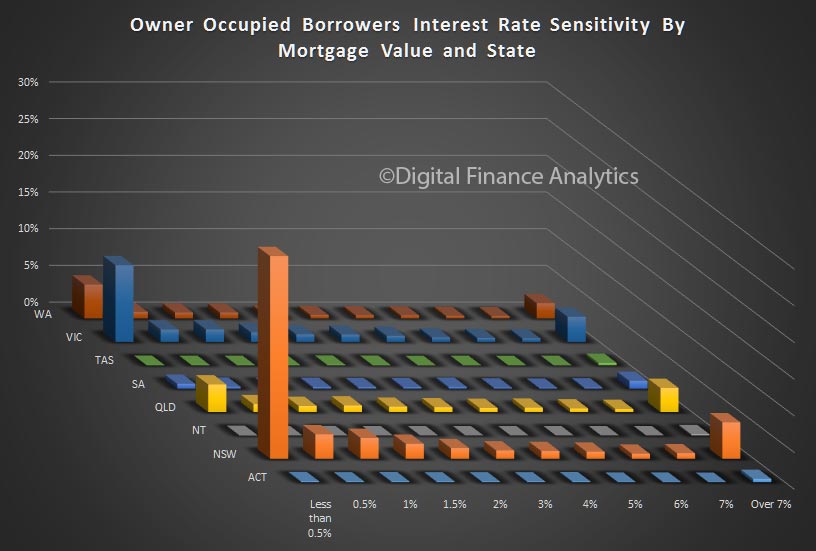

Yesterday we took a deep dive looking at how sensitive borrowing households are to a prospective rise in their owner occupied mortgage rates. A fundamental, though valid assumption we made was to look at the relative number of households impacted. This distribution led the analysis.

However, we can look at the data through a lens of relative mortgage value, not household count. This changes the perspective somewhat and today we explore this additional dimension.

We use the same movement in rate scenarios, from under 0.5% up, to more than 7% and show the relative portfolio distribution by value of outstanding loans and the tipping point where the household would fall into mortgage stress.

Using this lens, we immediately see that from a value perspective, a significant proportion of value resides in NSW (larger home prices, bigger loans). Within the NSW portfolio, more than 20% of the value would be impacted by a small incremental rise in mortgage rates. We also see some value impacted in VIC and WA, but to a lessor degree. In other words, the more highly leveraged state of households in NSW means a small rise in real mortgage rates will bite hard here. This despite all the focus in the press on WA and QLD!

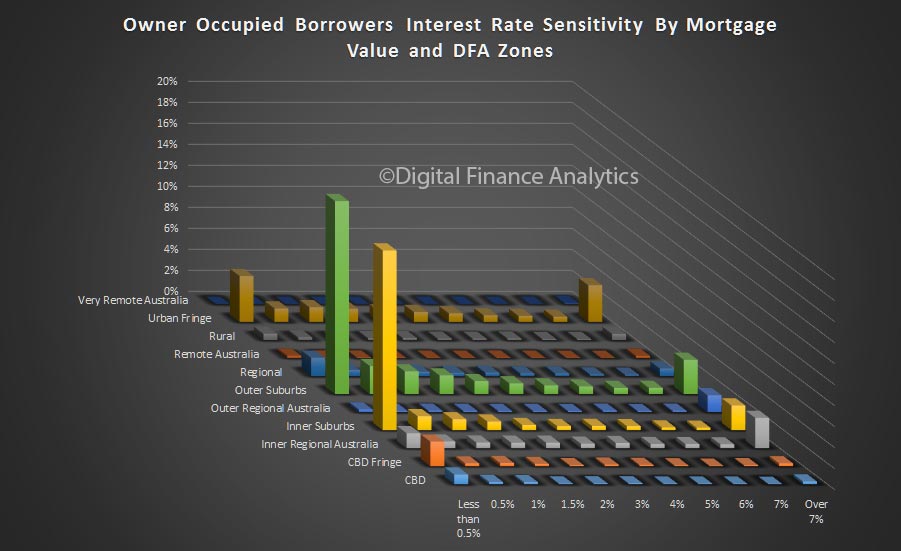

Another interesting view is created by using our geographic zoning definitions, radiating from the central business district (CBD) in the middle, in concentric rings, out to the suburbs, and into the regions beyond. The areas where sensitivity is highest to small rate rises are the inner and outer suburbs, plus the urban fringe. This is because mortgages are quite large, relative to incomes. In other words, there is a geographic concentration risk which needs to be taken into account.

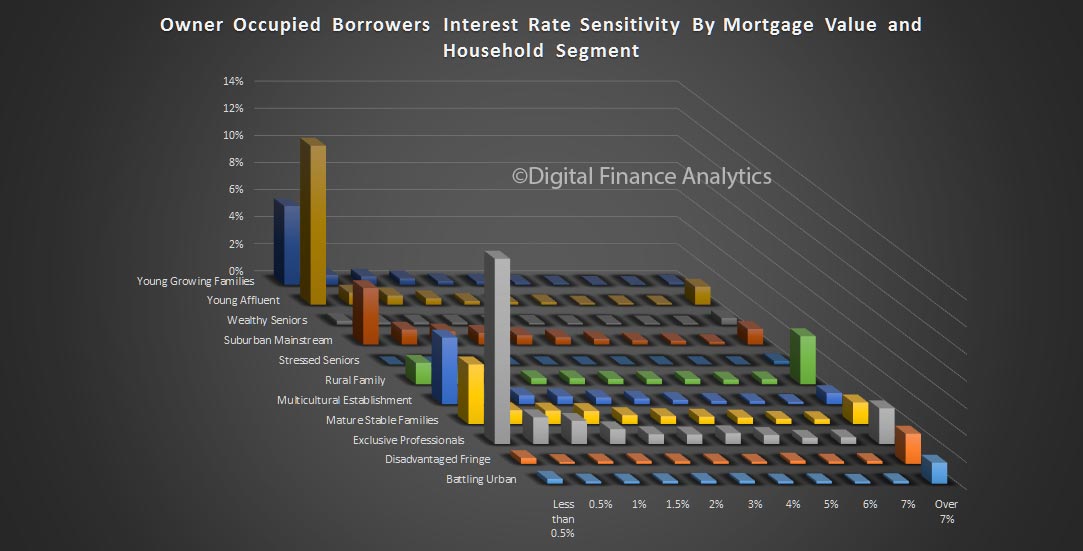

Our household segmentation models highlights that from a value perspective, young affluent and exclusive professionals have a dis-proportionally large share of value, and a significant proportion of this would be at risk from even a small rise.

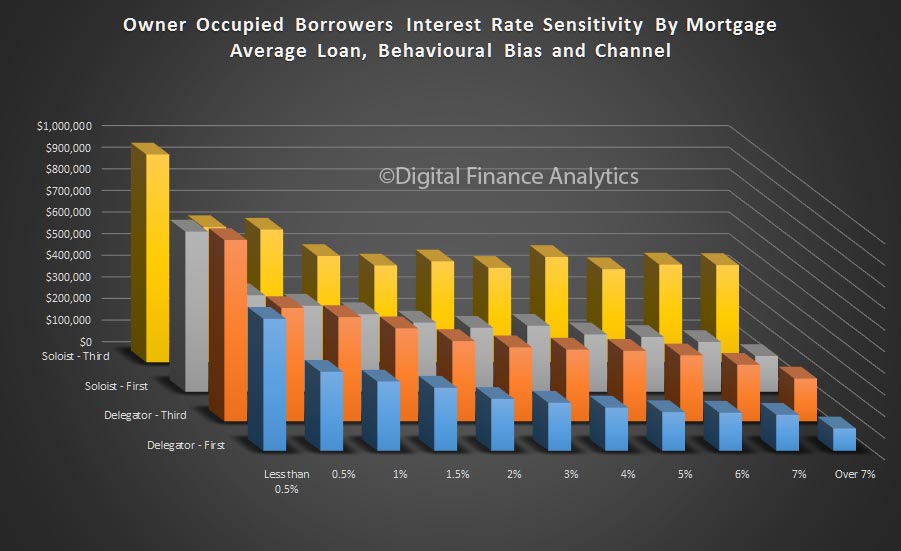

Finally, again using our value lens, we can see that the largest segment which would be impacted by a 0.5% or less rate rise are soloists (see our earlier post for definitions) who got their mortgage via mortgage brokers. In comparison, delegators who get their loans direct from the bank, without an intermediary, are least exposed.

So, we conclude it is essential to look at the mortgage portfolio both from a value AND count perspective. But in fact, it is the value related lens which provides the best view of relative risk. This is how risk capital should be allocated.

Larger loans, via brokers are inherently more risky in a rising rate environment.

Given the recent data, no surprise the latest RBA chart pack includes the updated household finances data to December 2016, and shows a further rise in the debt to disposable income ratio. Given that lending growth is around 6.5% over the past year and income growth much lower, this trend is likely to continue.

However, the debt has to be repaid at some point. Also worth noting that the interest paid now reflects the lower effective interest rates following the RBA cash rate cut. However, we expect effective rates to rise in coming months.

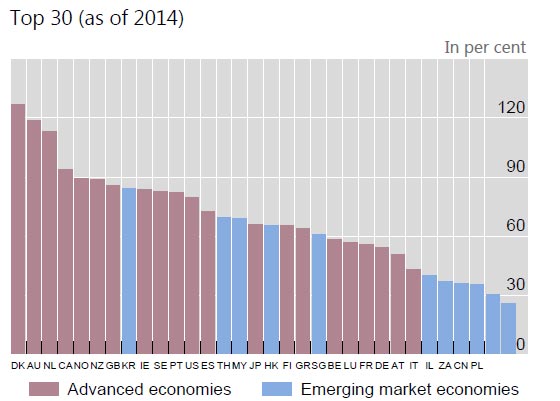

The OECD has once again warned that rising borrowing costs could wreak havoc on global property markets this year.

Chief economist of the Organisation for Economic Co-operation and Development, Catherine Mann, told the UK’s The Telegraphthat property prices had soared in Canada, New Zealand and Sweden in a way “not consistent with a stable real estate market”.

What she didn’t mention is that the OECD’s own research puts Australia in the middle of that pack based on house-price-to-income ratios – making it at least as likely to be affected by the US Federal Reserve-led rise in global interest rates.

In its last economic outlook, the Paris-based think tank rated Sweden at 22 per cent above its long-term price-to-income ratio, Australia 29.4 per cent above, Canada at 30.5 per cent and New Zealand at 31.9 per cent.

In the UK market, where that ratio is only 21.3 per cent, the London market is already cooling rapidly thanks in part to Brexit uncertainty.

Ms Mann said it would be “interesting” to see “who bears the burden – who bears the adjustment cost”.

There are mixed opinions as to whether the Reserve Bank will cut official rates again this year, but even if it does it will be fighting a tide of rising rates in wholesale funding markets.

Those rates affect a third of our banks’ borrowing costs and are likely to force more out-of-cycle mortgage rate hikes.

Who will bear that pain?

To understand what Catherine Mann, the OECD’s chief economist, means by “adjustment costs”, both asset prices and lending rates have to be taken into account.

That’s because banks lend money based on two main criteria: the income the borrower has to service debt at a given interest rate, and the likelihood of the asset increasing or decreasing in value.

Re-mortgaging to cover extravagant spending is coming to an end. Photo: Getty

They were so confident the market would continue rising, that they were happy for the safety buffer of equity to build up in the months or years after the loan was made.

Likewise, serviceability ratios were stretched to the limit at lenders such as Bankwest, because the mining boom was inflating wage packets relatively quickly.

The GFC changed all that. The lenders that were pushing those ratios too far, such as Bankwest, St George and Rams Home Loans, came close to collapse in 2009 and were snapped up at bargain prices by the bigger banks.

While the worst excesses of the GFC have not been repeated, banks and borrowers have once again become too comfortable with the idea that rising property prices and wages will get overstretched borrowers out of trouble.

Ms Mann is essentially warning us not to get too comfortable, as the era of ultra-low interest rates comes to an end.

Debt as ‘income’

To illustrate the point, I’ll go back to the example of the “completely disorganised” borrower described to me by a lending manager last year.

“[What’s] interesting in terms of the implications … is who bears the burden,” said Catherine Mann. Photo: Getty

Such borrowers, he said, would bumble along with maxed-out credit cards, a personal loan for their last holiday, a leased car, and a fairly opulent lifestyle overall.

In a rising market, they could, and did, remortgage every few years and use equity in their home to pay for their extravagance.

What’s changed? Well firstly, many Australian households are seeing a big slowdown in the capital growth of their homes.

The latest all-cities average dwelling price from CoreLogic, released on Tuesday, shows a national increase of 10.8 per cent over 12 months.

However, that is overwhelmingly concentrated in Sydney (up 15.5 per cent) and Melbourne (13.7 per cent).

For “disorganised” borrowers living in Perth, where values have actually fallen 4.3 per cent, there’ll be no more remortgaging to pay off their other debts – the era of equity withdrawal is over, for some years at least.

Higher mortgage costs will make the end of debt-funded spending an even bigger shock. Photo: Getty

The situation is similar in Darwin, where prices rose less than inflation in the past 12 months (0.9 per cent), or Brisbane where prices were just a bit ahead of inflation (3.6 per cent).

If out-of-cycle rate increases start to bite into their budgets, households in many areas are facing a double-whammy – no more debt-financed consumption, plus higher monthly outgoings just to keep a roof over their heads.

As economist Steve Keen has argued for years, household consumption is financed by two things: wages, plus the net change in debt.

We are now going into an era when a growing number of households will have only their wages to spend.

With wage growth at record lows and mortgage rate increases on the medium-term horizon, for the over-indebted that’s going to come as quite a shock.

We can slice and dice the households, using some of our custom SQL views. For example, here are the average balances by household age bands. Households between 40 and 59 have the larger loan and revolving balances, though interestingly, those 60-70 have the largest card balances.

We can slice and dice the households, using some of our custom SQL views. For example, here are the average balances by household age bands. Households between 40 and 59 have the larger loan and revolving balances, though interestingly, those 60-70 have the largest card balances. As incomes rise, debt levels also rise, so some of the debt is owned by households with more ability to repay. However, remember the larger number of households are in the first three bands, where debt is still rife.

As incomes rise, debt levels also rise, so some of the debt is owned by households with more ability to repay. However, remember the larger number of households are in the first three bands, where debt is still rife. We can examine this debt by our master household segments. Once again, more affluent households have larger debts, but young growing families have on average close to $20,000 in debt, including some on revolving cards (where interest is charged at a high rate).

We can examine this debt by our master household segments. Once again, more affluent households have larger debts, but young growing families have on average close to $20,000 in debt, including some on revolving cards (where interest is charged at a high rate). We can examine the data across our regions. Urban centres, including ACT, Greater Sydney and Melbourne have the highest debt levels. Many of these households also hold the largest mortgages.

We can examine the data across our regions. Urban centres, including ACT, Greater Sydney and Melbourne have the highest debt levels. Many of these households also hold the largest mortgages. Finally, it is interesting to note that from a digital behaviour standpoint, those younger households who are online most of the time and prefer to use digital channels (Natives) borrow more than Luddites (those who prefer not to go online, but the larger debts are held by households who have migrated online. These Migrants are progressively using online channels more than ever. You can read more about our channel use inour report The Quiet Revolution.

Finally, it is interesting to note that from a digital behaviour standpoint, those younger households who are online most of the time and prefer to use digital channels (Natives) borrow more than Luddites (those who prefer not to go online, but the larger debts are held by households who have migrated online. These Migrants are progressively using online channels more than ever. You can read more about our channel use inour report The Quiet Revolution. So, to sum up. Many households have large mortgages AND other debts, including credit cards and personal loans. This entire portfolio of debt must be considered when looking at their sensitivity to rising rates, and when comparing static incomes with rising debt repayments. Just looking at the mortgage gives only part of the full picture.

So, to sum up. Many households have large mortgages AND other debts, including credit cards and personal loans. This entire portfolio of debt must be considered when looking at their sensitivity to rising rates, and when comparing static incomes with rising debt repayments. Just looking at the mortgage gives only part of the full picture.

This is explained by massive amounts of borrowing for housing (both owner occupied and investment) whilst unsecured personal debt is not growing. Such high household debt, even with low interest rates sucks spending from the economy, and is a brake on growth. The swelling value of home prices, and paper wealth (as well as growing bank balance sheets) do not really provide the right foundation for long term real sustainable growth.

This is explained by massive amounts of borrowing for housing (both owner occupied and investment) whilst unsecured personal debt is not growing. Such high household debt, even with low interest rates sucks spending from the economy, and is a brake on growth. The swelling value of home prices, and paper wealth (as well as growing bank balance sheets) do not really provide the right foundation for long term real sustainable growth. Another interesting view is created by using our geographic zoning definitions, radiating from the central business district (CBD) in the middle, in concentric rings, out to the suburbs, and into the regions beyond. The areas where sensitivity is highest to small rate rises are the inner and outer suburbs, plus the urban fringe. This is because mortgages are quite large, relative to incomes. In other words, there is a geographic concentration risk which needs to be taken into account.

Another interesting view is created by using our geographic zoning definitions, radiating from the central business district (CBD) in the middle, in concentric rings, out to the suburbs, and into the regions beyond. The areas where sensitivity is highest to small rate rises are the inner and outer suburbs, plus the urban fringe. This is because mortgages are quite large, relative to incomes. In other words, there is a geographic concentration risk which needs to be taken into account. Our household segmentation models highlights that from a value perspective, young affluent and exclusive professionals have a dis-proportionally large share of value, and a significant proportion of this would be at risk from even a small rise.

Our household segmentation models highlights that from a value perspective, young affluent and exclusive professionals have a dis-proportionally large share of value, and a significant proportion of this would be at risk from even a small rise. Finally, again using our value lens, we can see that the largest segment which would be impacted by a 0.5% or less rate rise are soloists (see our earlier post for definitions) who got their mortgage via mortgage brokers. In comparison, delegators who get their loans direct from the bank, without an intermediary, are least exposed.

Finally, again using our value lens, we can see that the largest segment which would be impacted by a 0.5% or less rate rise are soloists (see our earlier post for definitions) who got their mortgage via mortgage brokers. In comparison, delegators who get their loans direct from the bank, without an intermediary, are least exposed. So, we conclude it is essential to look at the mortgage portfolio both from a value AND count perspective. But in fact, it is the value related lens which provides the best view of relative risk. This is how risk capital should be allocated.

So, we conclude it is essential to look at the mortgage portfolio both from a value AND count perspective. But in fact, it is the value related lens which provides the best view of relative risk. This is how risk capital should be allocated. However, the debt has to be repaid at some point. Also worth noting that the interest paid now reflects the lower effective interest rates following the RBA cash rate cut. However, we expect effective rates to rise in coming months.

However, the debt has to be repaid at some point. Also worth noting that the interest paid now reflects the lower effective interest rates following the RBA cash rate cut. However, we expect effective rates to rise in coming months.Re-mortgaging to cover extravagant spending is coming to an end. Photo: Getty

“[What’s] interesting in terms of the implications … is who bears the burden,” said Catherine Mann. Photo: Getty

Higher mortgage costs will make the end of debt-funded spending an even bigger shock. Photo: Getty