The latest IMF working paper analyses the recent growth dynamics in China, evaluating both cyclical positions and long-term growth prospects. The analysis shows that financial cycles play a more important role than traditional inflation-based cycles in shaping the dynamics of growth.

China’s impressive growth record speaks for itself, and the country’s policymakers have won additional accolades for the timely response to the Global Financial Crisis. The Chinese GDP has been growing at the average rate of nearly 10 percent per year in the past four decades. The well-timed policy relaxation supported growth in the immediate aftermath of the crisis. Several analysts pronounced the arrival of a goldilocks economy in China—not too hot to fuel inflation and not too cold to slip into recession —and some see a continuation of the stable economic growth as the most likely scenario for China.

A key question is how much of China’s slowdown is temporary (cyclical) versus long lasting (structural). Growth fluctuations in developing and emerging markets often follow a pattern of spans of impressive growth followed by long periods of stagnation. The concern is therefore not only about a cyclical growth slowdown typically experienced by mature economies, but a prolonged slump so often experienced in emerging markets. These fears are also fed by the observation that structural ‘imbalances’ in the Chinese economy—exceptionally high investment rates associated by some with ‘forced savings’ —have further grown since the GFC, reducing investment efficiency and total factor productivity (TFP) growth.

Headline growth in China has slowed from the pre-GFC peak of 14 percent to less than 8 percent in 2013. China benefitted from the pre-crisis global expansion, but its export-based model suffered a blow when global demand collapsed. At the same time, the authorities embarked on a massive credit-cum-investment stimulus, which cushioned the impact of the global slowdown.

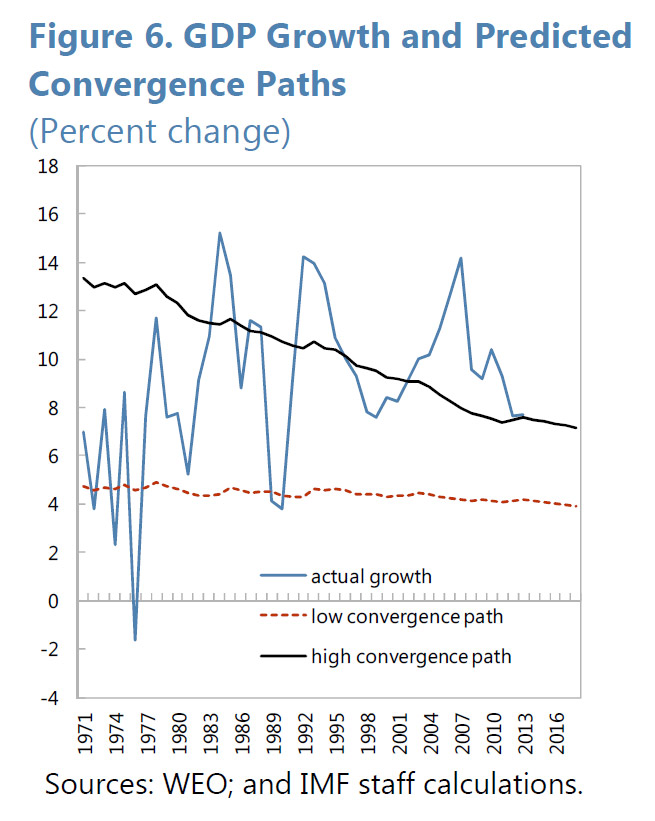

The paper simulates theoretical convergence growth paths by substituting China’s data to two versions of the estimated model. The actual growth path for China is significantly above the convergence path simulated from the full model (‘low convergence path’) and is oscillating around the Asian Tigers’ path (‘high-convergence path’) since the dismantling of the strict central-planning system in 1979.

The paper simulates theoretical convergence growth paths by substituting China’s data to two versions of the estimated model. The actual growth path for China is significantly above the convergence path simulated from the full model (‘low convergence path’) and is oscillating around the Asian Tigers’ path (‘high-convergence path’) since the dismantling of the strict central-planning system in 1979.

In summary, the paper contributes to the ongoing growth debate by identifying the cyclical position and assessing the degree of potential output slowdown in China. The main results are:

- Expect growth to slow down in the near-term. Financial cycles in China play a significant role in shaping growth dynamics, and the economy is now likely near the peak of a powerful cycle propelling the economy since the GFC. An adjustment is therefore both likely and needed to bring the economy closer to equilibrium.

- Potential growth is slowing. This is expected as China makes progress on the long journey of converging to advanced economy income levels. As it moves closer to this technology frontier, growth will continue to slow. However, the pace of convergence, and thus China’s medium-term growth rate, will depend on structural reforms. With success in implementing reforms, China can follow the historical experience of other fast-growing Asian economies.

Currently, the ‘finance-neutral’ gap—a measure of the financial cycle—is large and positive, reflecting imbalances accumulated in the economy since the Global Financial Crisis. A period of slower growth is therefore both likely and needed in the near term to restore the economy to equilibrium. In the medium term, growth will slow as China moves closer to the technology frontier, but a steadfast implementation of reforms can ensure that China follows the path of the “Asia Tigers” and achieves successful convergence to high-income status.

Note The views expressed in this Working Paper are those of the author(s) and do not necessarily represent those of the IMF or IMF policy. Working Papers describe research in progress by the author(s) and are published to elicit comments and to further debate.