Global growth is forecast at 3.0 percent for 2019, its lowest level since 2008–09 and a 0.3 percentage point downgrade from the April 2019 World Economic Outlook.

Growth is projected to pick up to 3.4 percent in 2020 (a 0.2 percentage point downward revision compared with April), reflecting primarily a projected improvement in economic performance in a number of emerging markets in Latin America, the Middle East, and emerging and developing Europe that are under macroeconomic strain.

Yet, with uncertainty about prospects for several of these countries, a projected slowdown in China and the United States, and prominent downside risks, a much more subdued pace of global activity could well materialize. To forestall such an outcome, policies should decisively aim at defusing trade tensions, reinvigorating multilateral cooperation, and providing timely support to economic activity where needed. To strengthen resilience, policymakers should address financial vulnerabilities that pose risks to growth in the medium term. Making growth more inclusive, which is essential for securing better economic prospects for all, should remain an overarching goal.

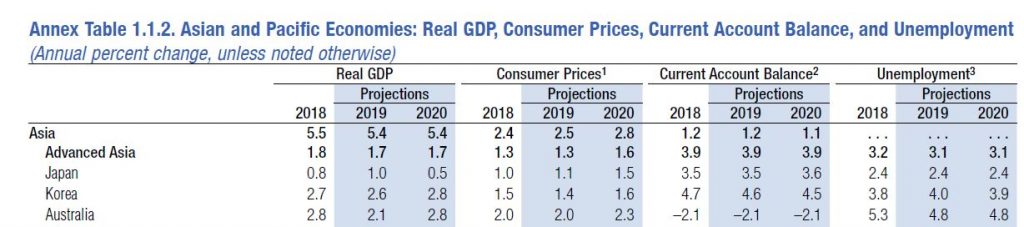

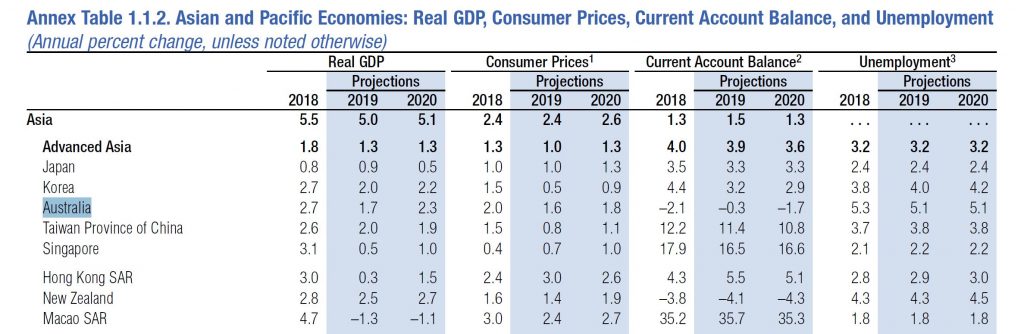

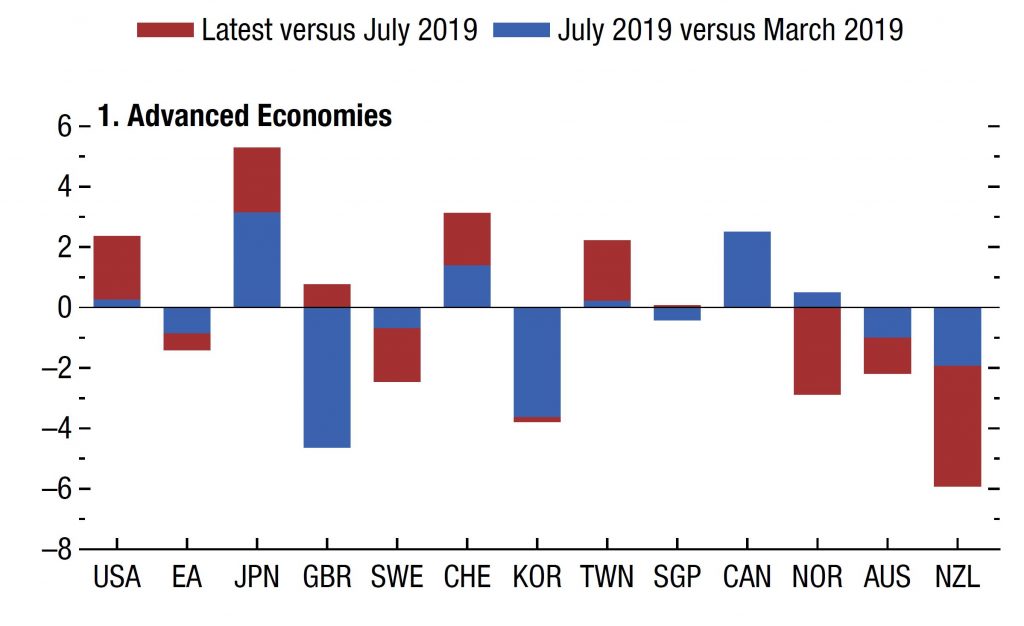

Australian growth is downgraded to 1.7%

Bearing in mind our dependency on iron ore, they say: Iron ore prices increased 6.7 percent between February 2019 and August 2019. Widespread disruptions—including the Vale dam collapse in Brazil and tropical cyclone Veronica in Australia— coupled with record-high steel output in China pushed iron ore prices to five-year highs during the first half of 2019. However, the normalization of previously disrupted operations and escalating trade tensions between the United States and China triggered a sharp correction in August, partially offsetting the gains since the beginning of the year.

In the IMF’s July update of the World Economic Outlook they revised downward projections for global growth to 3.2 percent in 2019 and 3.5 percent in 2020. While this is a modest revision of 0.1 percentage points for both years relative to projections in April, it comes on top of previous significant downward revisions. The revision for 2019 reflects negative surprises for growth in emerging market and developing economies that offset positive surprises in some advanced economies. From The IMF Blog.

Growth is projected to improve between 2019 and 2020. However, close to 70 percent of the increase relies on an improvement in the growth performance in stressed emerging market and developing economies and is therefore subject to high uncertainty.

Global growth is sluggish and precarious, but it does not have to be this way because some of this is self-inflicted. Dynamism in the global economy is being weighed down by prolonged policy uncertainty as trade tensions remain heightened despite the recent US-China trade truce, technology tensions have erupted threatening global technology supply chains, and the prospects of a no-deal Brexit have increased.

Global growth is sluggish and precarious, but it does not have to be this way because some of this is self-inflicted.

The negative consequences of policy uncertainty are visible in the diverging trends between the manufacturing and services sector, and the significant weakness in global trade. Manufacturing purchasing manager indices continue to decline alongside worsening business sentiment as businesses hold off on investment in the face of high uncertainty. Global trade growth, which moves closely with investment, has slowed significantly to 0.5 percent (year-on-year) in the first quarter of 2019, which is its slowest pace since 2012. On the other hand, the services sector is holding up and consumer sentiment is strong, as unemployment rates touch record lows and wage incomes rise in several countries.

Among advanced economies—the United States, Japan, the United Kingdom, and the euro area—grew faster than expected in the first quarter of 2019. However, some of the factors behind this—such as stronger inventory build-ups—are transitory and the growth momentum going forward is expected to be weaker, especially for countries reliant on external demand. Owing to first quarter upward revisions, especially for the United States, we are raising our projection for advanced economies slightly, by 0.1 percentage points, to 1.9 percent for 2019. Going forward, growth is projected to slow to 1.7 percent, as the effects of fiscal stimulus taper off in the United States and weak productivity growth and aging demographics dampen long-run prospects for advanced economies.

In emerging market and developing economies, growth is being revised down by 0.3 percentage points in 2019 to 4.1 percent and by 0.1 percentage points for 2020 to 4.7 percent. The downward revisions for 2019 are almost across the board for the major economies, though for varied reasons. In China, the slight revision downwards reflects, in part, the higher tariffs imposed by the United States in May, while the more significant revisions in India and Brazil reflect weaker-than-expected domestic demand.

For commodity exporters, supply disruptions, such as in Russia and Chile, and sanctions on Iran, have led to downward revisions despite a near-term strengthening in oil prices. The projected recovery in growth between 2019 and 2020 in emerging market and developing economies relies on improved growth outcomes in stressed economies such as Argentina, Turkey, Iran, and Venezuela, and therefore is subject to significant uncertainty.

Financial conditions in the United States and the euro area have further eased, as the US Federal Reserve and the European Central Bank adopted a more accommodative monetary policy stance. Emerging market and developing economies have benefited from monetary easing in major economies but have also faced volatile risk sentiment tied to trade tensions. On net, financial conditions are about the same for this group as in April. Low-income developing countries that previously received mainly stable foreign direct investment flows now receive significant volatile portfolio flows, as the search for yield in a low interest rate environment reaches frontier markets.

Increased downside risks

A major downside risk to the outlook remains an escalation of trade and technology tensions that can significantly disrupt global supply chains. The combined effect of tariffs imposed last year and potential tariffs envisaged in May between the United States and China could reduce the level of global GDP in 2020 by 0.5 percent. Further, a surprise and durable worsening of financial sentiment can expose financial vulnerabilities built up over years of low interest rates, while disinflationary pressures can lead to difficulties in debt servicing for borrowers. Other significant risks include a surprise slowdown in China, the lack of a recovery in the euro area, a no-deal Brexit, and escalation of geopolitical tensions.

With global growth subdued and downside risks dominating the outlook, the global economy remains at a delicate juncture. It is therefore essential that tariffs are not used to target bilateral trade balances or as a general-purpose tool to tackle international disagreements. To help resolve conflicts, the rules-based multilateral trading system should be strengthened and modernized to encompass areas such as digital services, subsidies, and technology transfer.

Policies to support growth

Monetary policy should remain accommodative especially where inflation is softening below target. But it needs to be accompanied by sound trade policies that would lift the outlook and reduce downside risks. With persistently low interest rates, macroprudential tools should be deployed to ensure that financial risks do not build up.

Fiscal policy should balance growth, equity, and sustainability concerns, including protecting society’s most vulnerable. Countries with fiscal space should invest in physical and social infrastructure to raise potential growth. In the event of a severe downturn, a synchronized move toward more accommodative fiscal policies should complement monetary easing, subject to country specific circumstances.

Lastly, the need for greater global cooperation is ever urgent. In addition to resolving trade and technology tensions, countries need to work together to address major issues such as climate change, international taxation, corruption, cybersecurity, and the opportunities and challenges of newly emerging digital payment technologies.

New

Zealand’s economic expansion lost momentum recently. The near-term

growth outlook is expected to improve on the back of a timely increase

in macroeconomic policy support. Downside risks to the growth outlook

have increased but New Zealand has the policy space to respond should

such risks materialize.

Macroeconomic

policy settings are broadly appropriate, while macroprudential policy

settings are attuned to macrofinancial vulnerabilities in the household

sector, which have started to decline but remain elevated.

Financial

sector reform in the context of the Review of the Capital Adequacy

Framework and the Review of the Reserve Bank of New Zealand Act should

provide for a welcome further strengthening of the resilience of the

financial system and regulatory framework.

The government’s structural policy agenda appropriately focuses on reducing infrastructure gaps, increasing human capital, and lifting productivity, while seeking to make growth more inclusive and improve housing affordability.

Within the statement they warn that:

Risks to the outlook are increasingly tilted to the downside. On the domestic side, the fiscal stimulus could be less expansionary if policy implementation were to be more gradual than expected, and the domestic housing market cooling could morph into a downturn, either because of external shocks or diminished expectations. On the external side, global financial conditions could be tighter and dairy prices could be lower. Risks to global trade and growth from rising protectionism have increased, and this could have negative spillovers to the New Zealand economy, including through the impact on China and Australia, two key trading partners. High household debt remains a risk to economic growth and financial stability, and it could amplify the effects of large, adverse shocks. On the upside, in the near term, growth could be stronger if net migration were to decrease more slowly than expected or if the terms of trade were to be stronger.

With regard to macroprudnetial they warn:

The scope for easing macroprudential restrictions is limited, given still-high macrofinancial vulnerabilities. The shares of riskier home loans in bank assets (those with very high LVRs, high debt-to-income, and investor loans) has moderated due to the combined impact of the LVR settings and tighter bank lending standards. However, with the RBNZ’s recent easing of the LVR restrictions, improvements in some macroprudential risk factors such as credit growth have recently stalled or started to reverse. Further easing of LVR restrictions should consider the possible impact on banks’ prudential lending standards, as well as the risks to financial stability from elevated household debt.

Global growth appears to be stabilizing, and is generally projected to pick up moderately later this year and into 2020. This recovery is supported by the continuation of accommodative financial conditions, stimulus measures taking effect in some countries, and one-off factors dissipating. However, growth remains low and risks remain tilted to the downside. Most importantly, trade and geopolitical tensions have intensified. We will continue to address these risks, and stand ready to take further action.

We reaffirm our commitment to use all policy tools to achieve strong, sustainable, balanced and inclusive growth, and safeguard against downside risks, by stepping up our dialogue and actions to enhance confidence. Fiscal policy should be flexible and growth-friendly while rebuilding buffers where needed and ensuring debt as a share of GDP is on a sustainable path. In line with central banks’ mandates, monetary policy should ensure that inflation remains on track toward, or stabilizes around targets. Central bank decisions need to remain well communicated. Continued implementation of structural reforms will enhance our growth potential. We reemphasize that international trade and investment are important engines of growth, productivity, innovation, job creation and development. We reaffirm our Leaders’ conclusions on trade at the Buenos Aires Summit. We will continue to take joint action to strengthen international cooperation and frameworks. We also reaffirm our exchange rate commitments made in March 2018.

Global current account imbalances have narrowed in the aftermath of the global financial crisis, notably in emerging and developing economies and they have become increasingly concentrated in advanced economies. However, they remain large and persistent, and stock positions continue to diverge. In assessing external balances, we note the importance of monitoring all components of the current account, including service trade and income balances. We acknowledge that external balances reflect a combination of cyclical factors, domestic policies and fundamentals, as well as spillovers from abroad. We share the view that, while some of the external imbalances may be in line with economic fundamentals, others may be excessive and pose risks. Factors underlying excessive imbalances may include excess corporate savings, miscalibrated fiscal policies, and barriers to trade in goods and services. In the spirit of enhancing cooperation, we affirm that carefully calibrated macroeconomic and structural policies tailored to country-specific circumstances are necessary to address excessive imbalances and mitigate the risks to achieving the G20 goal of strong, sustainable, balanced and inclusive growth. Meanwhile, we recognize that the composition of funding also should be carefully monitored as some forms (such as foreign direct investment) provide more stable funding than others. We look forward to the IMF’s further analytical work on global imbalances.

Demographic changes, including population aging, pose challenges and opportunities for all G20 members. Given the complex nature of this agenda, we held a comprehensive discussion on aging-related issues at break-out sessions, which grouped countries according to their demographic profiles. Demographic changes will require policy actions that span fiscal, monetary, financial, and structural policies. In this regard, countries should consider, as relevant:

Further enhancing productivity and growth, including by investing in skills, and encouraging labor market participation in particular of women and older people and promoting elderly-friendly industries;

Enhancing the efficiency and effectiveness of public spending as well as a well-functioning and fiscally sustainable social safety net with due consideration to intra- and inter-generational equity;

Designing the tax system in an equitable and growth-friendly manner, so as to better respond to the challenges posed by aging;

Better understanding the implications of aging for monetary policy;

Assisting financial institutions to make any needed adjustments to their business models and services;

Managing the cross-border implications of demographic changes, such as capital and migratory flows.To strengthen financial inclusion in the aging society, we endorse the G20 Fukuoka Policy Priorities on Aging and Financial Inclusion, prepared by the Global Partnership for Financial Inclusion (GPFI) and OECD. We endorse the Proposed GPFI Work Program, and ask the GPFI to streamline its structure based on the Roadmap to 2020.

We reaffirm our commitment to a strong, quota-based, and adequately resourced IMF, to preserve its role at the center of the global financial safety net. We remain committed to concluding the 15th General Review of Quotas no later than the 2019 Annual Meetings, and call on the IMF to expedite its work on IMF resources and governance reform as a matter of the highest priority. We support the progress made on work to follow up the Eminent Persons Group (EPG) proposals. We welcome the progress made towards developing possible principles for effective country platforms and look forward to further work to consolidate our views and build consensus. In addition, we welcome ongoing efforts by the Multilateral Investment Guarantee Agency to enhance risk insurance in development finance, including the release of new standardized contracts and cooperation agreements with several MDBs. We welcome the discussion of development finance issues, in response to the relevant EPG proposals, as experienced this year at Deputies’ level in April and at Ministers’ level yesterday. We welcome the work undertaken by the international organizations on capital flows. The OECD has completed a review of its Code of Liberalisation of Capital Movements, which modernizes the Code to support the liberalization of capital flows and financial stability. We also welcome the MDBs’ report on value for money and look forward to further work on indicators where harmonization is relevant, affordable and provides clear benefits. We will continue our work on the EPG’s proposals, recognizing their multi-year nature.

We reiterate the importance of joint efforts undertaken by both borrowers and creditors, official and private, to improve debt transparency and secure debt sustainability. We welcome an IMF-World Bank Group (WBG) Update on the recent progress of their multi-pronged approach for addressing emerging debt vulnerabilities, and support its further implementation. In particular, we call on the IMF and WBG to continue their efforts to strengthen borrowers’ capacity in the areas of debt recording, monitoring, and reporting, debt management, public financial management, and domestic resource mobilization. In the context of the review of the Debt Limits Policy and Non-Concessional Borrowing Policy, we encourage the IMF and WBG to continue their efforts to deepen their analysis of collateralized financing practices. We welcome the completion of the voluntary self-assessment of the implementation of the G20 Operational Guidelines for Sustainable Financing and the IMF-WBG note on the survey results and policy recommendation. We applaud the G20 and non-G20 members who completed the survey. We will continue to discuss the issues highlighted by this note, aiming to improve financing practices. We support the work of the Institute of International Finance on the Voluntary Principles for Debt Transparency to improve debt transparency and sustainability of private financing and look forward to follow up. We support the ongoing work of the Paris Club, as the principal international forum for restructuring official bilateral debt, towards the broader inclusion of emerging creditors. In that regard, we welcome India associating voluntarily with the Paris Club to cooperate in its work on a case-by-case basis.

Infrastructure is a driver of economic growth and prosperity. An emphasis on quality infrastructure is an essential part of the G20’s ongoing efforts to close the infrastructure gap, in accordance with the Roadmap to Infrastructure as an Asset Class. In this context, we stress the importance of maximizing the positive impact of infrastructure to achieve sustainable growth and development while preserving the sustainability of public finances, raising economic efficiency in view of life-cycle cost, integrating environmental and social considerations, including women’s economic empowerment, building resilience against natural disasters and other risks, and strengthening infrastructure governance. Based on this understanding, and welcoming inter-thematic collaborations, we endorse the G20 Principles for Quality Infrastructure Investment as our common strategic direction and high aspiration. We thank the international organizations for preparing the Reference Notes on quality infrastructure investment and a new Database of Facilities and Resources, which will help effective implementation. We look forward to continuing advancing the elements to develop infrastructure as an asset class, including by exploring possible indicators on quality infrastructure investment.

We acknowledge the importance of disaster risk financing and insurance schemes as a means to promote financial resilience against natural disasters. These schemes can help governments effectively leverage private sector resources and thereby manage financial risks arising from natural disasters in a timely manner. In this regard, the WBG’s report, Boosting Financial Resilience to Disaster Shocks: Good Practices and New Frontiers, will help broaden knowledge of disaster risk financing methods, including through macro-fiscal planning.

Moving towards Universal Health Coverage (UHC) contributes to human capital development, sustainable and inclusive growth and development, and prevention, detection and response to health emergencies, such as pandemics and anti-microbial resistance, in developing countries. In this context, we affirm our commitment to the G20 Shared Understanding on the Importance of UHC Financing in Developing Countries. As articulated in the Shared Understanding document, a multi-sectoral approach, in particular the collaboration between finance and health authorities, with the appropriate contribution of the private sector and non-government organizations, is crucial for strengthening health financing, building on work by international organizations. In this regard, we look forward to a joint session of Finance and Health Ministers in the margins of the Leaders’ Summit. We appreciate the World Bank Group’s report, High-Performance Health Financing for Universal Health Coverage: Driving Sustainable, Inclusive Growth in the 21st Century.

We underline our continued support for the Compact with Africa (CwA). This should involve closer engagement with private sector investors and enhanced bilateral engagement, including coherent contributions from development finance institutions as well as enhanced roles for participating international organizations (WBG, AfDB, IMF) based on a clear understanding of their roles in implementing the CwA.

We will continue our cooperation for a globally fair, sustainable, and modern international tax system, and welcome international cooperation to advance pro-growth tax policies. We reaffirm the importance of the worldwide implementation of the G20/OECD Base Erosion and Profit Shifting (BEPS) package and enhanced tax certainty. We welcome the recent progress on addressing the tax challenges arising from digitalization and endorse the ambitious work program that consists of a two-pillar approach, developed by the Inclusive Framework on BEPS. We will redouble our efforts for a consensus-based solution with a final report by 2020. We welcome the recent achievements on tax transparency, including the progress on automatic exchange of financial account information for tax purposes. We also welcome an updated list of jurisdictions that have not satisfactorily implemented the internationally agreed tax transparency standards. We look forward to a further update by the OECD of the list that takes into account all of the strengthened criteria. Defensive measures will be considered against listed jurisdictions. In this regard, we recall the 2015 OECD report inventorying available measures. We call on all jurisdictions to sign and ratify the multilateral Convention on Mutual Administrative Assistance in Tax Matters. We continue to support tax capacity building in developing countries, including coordinating through the Platform for Collaboration on Tax (PCT) and by applying the experience with medium-term revenue strategies and tailoring efforts to support domestic resource mobilization in countries with limited capacities. We welcome the first progress report of the PCT, as well as the Asia-Pacific Academy for Tax and Financial Crime Investigation in Japan.

An open and resilient financial system, grounded in agreed international standards, is crucial to support sustainable growth. We remain committed to the full, timely and consistent implementation of the agreed financial reforms. We continue to evaluate their effects and welcome the FSB’s public consultation report on SME financing. We will continue to monitor and, as necessary, address vulnerabilities and emerging risks to financial stability, including with macroprudential tools. While non-bank financing provides welcome diversity to the financial system, we will continue to identify, monitor and address related financial stability risks as appropriate. We welcome the reports from the FSB and International Organization of Securities Commissions (IOSCO) on market fragmentation, and look forward to receiving progress updates in October including on ongoing work. We will address unintended, negative effects of market fragmentation, including through regulatory and supervisory cooperation. We continue to monitor and address the causes and consequences of the withdrawal of correspondent banking relationships, and issues on remittance firms’ access to banking services. Mobilizing sustainable finance and strengthening financial inclusion are important for global growth. We welcome private sector participation and transparency in these areas.

Technological innovations, including those underlying crypto-assets, can deliver significant benefits to the financial system and the broader economy. While crypto-assets do not pose a threat to global financial stability at this point, we remain vigilant to risks, including those related to consumer and investor protection, anti-money laundering (AML) and countering the financing of terrorism (CFT). We reaffirm our commitment to applying the recently amended FATF Standards to virtual assets and related providers for AML and CFT. We look forward to the adoption of the FATF Interpretive Note and Guidance by the FATF at its plenary later this month. We welcome IOSCO’s work on crypto-asset trading platforms related to consumer and investor protection and market integrity. We welcome the FSB’s directory of crypto-asset regulators, and its report on work underway, regulatory approaches and potential gaps relating to crypto-assets. We ask the FSB and standard setting bodies to monitor risks and consider work on additional multilateral responses as needed. We also welcome the FSB report on decentralized financial technologies, and the possible implications for financial stability, regulation and governance, and how regulators can enhance the dialogue with a wider group of stakeholders. We also continue to step up efforts to enhance cyber resilience, and welcome progress on the FSB’s initiative to identify effective practices for response to and recovery from cyber incidents.

We welcome the United Nations Security Council Resolution 2462, which stresses the essential role of the FATF in setting global standards for preventing and combatting money laundering, terrorist financing and proliferation financing. We reiterate our strong commitment to step up efforts to fight these threats. We call for the full, effective and swift implementation of the FATF Standards. We welcome the achievement of the FATF Ministerial Meeting in April this year that has given the FATF an open-ended mandate and led to strengthening the FATF’s governance, including the biennial ministerial meeting and the FATF Presidency’s term extensions. We look forward to the FATF’s Strategic Review. We welcome FATF’s commitment to monitor the risks and opportunities of financial innovation, and to ensure the FATF standards remain relevant and responsive. We ask the FATF to report back on progress in 2021. We look forward to further action by the FATF to strengthen the global response to proliferation financing.

The latest World Economic Outlook warns of slower growth though sees a possible acceleration later in the year (thanks to the Fed’s recent change in tune!).

Australian growth is forecast to fall to 2.1% in 2019, with CPI at 2% and unemployment at 4.8%. In 2020, GDP is forecast at 2.8%, CPI 2.3% and unemployment at 4.8%.

One year ago economic activity was accelerating in almost all regions of the world and the global economy was projected to grow at 3.9 percent in 2018 and 2019.

One year later, much has changed: the escalation of US–China trade tensions, macroeconomic stress in Argentina and Turkey, disruptions to the auto sector in Germany, tighter credit policies in China, and financial tightening alongside the normalization of monetary policy in the larger advanced economies have all contributed to a significantly weakened global expansion, especially in the second half of 2018. With this weakness expected to persist into the first half of 2019, the World Economic Outlook (WEO) projects a decline in growth in 2019 for 70 percent of the global economy. Global growth, which peaked at close to 4 percent in 2017, softened to 3.6 percent in 2018, and is projected to decline further to 3.3 percent in 2019. Although a 3.3 percent global expansion is still reasonable, the outlook for many countries is very challenging, with considerable uncertainties in the short term, especially as advanced economy growth rates converge toward their modest long-term potential.

While 2019 started out on a weak footing, a pickup is expected in the second half of the year. This pickup is supported by significant policy accommodation by major economies, made possible by the absence of inflationary pressures despite closing output gaps. The US Federal Reserve, in response to rising global risks, paused interest rate increases and signaled no increases for the rest of the year. The European Central Bank, the Bank of Japan, and the Bank of England have all shifted to a more accommodative stance. China has ramped up its fiscal and monetary stimulus to counter the negative effect of trade tariffs. Furthermore, the

outlook for US–China trade tensions has improved as the prospects of a trade agreement take shape. These policy responses have helped reverse the tightening of financial conditions to varying degrees across countries.

Emerging markets have experienced a resumption in portfolio flows, a decline in sovereign borrowing costs, and a strengthening of their currencies relative to the dollar. While the improvement in financial markets has been rapid, those in the real economy have yet to materialize. Measures of industrial production and investment remain weak for most advanced and emerging economies, and global trade has yet to recover. With improvements expected in the second half of 2019, global economic growth in 2020 is projected to return to 3.6 percent. This return is predicated on a rebound in Argentina and Turkey and some improvement in a set of other stressed emerging market and developing economies, and therefore subject to considerable uncertainty. Beyond 2020 growth will stabilize at around 3½ percent, bolstered mainly by growth in China and India and their increasing weights in world income. Growth in advanced economies will continue to slow gradually as the impact of US fiscal stimulus fades and growth tends toward the modest potential for the group, given ageing trends and low productivity growth. Growth in emerging market and developing economies will stabilize at around 5 percent, though with considerable variance between countries as subdued commodity prices and civil strife weaken prospects for some.

While the overall outlook remains benign, there are many downside risks. There is an uneasy truce on trade policy, as tensions could flare up again and play out in other areas (such as the auto industry) with large disruptions to global supply chains. Growth in China may surprise on the downside, and the risks surrounding Brexit remain heightened. In the face of significant financial vulnerabilities associated with large private and public sector debt in several countries, including sovereign-bank doom loop risks (for example, in Italy), there could be a rapid change in financial conditions owing to, for example, a risk-off episode or a no-deal Brexit.

With weak expansion projected for important parts of the world, a realization of these downside risks could dramatically worsen the outlook. This would take place at a time when conventional monetary and fiscal space is limited as a policy response. It is therefore imperative that costly policy mistakes are avoided. Policymakers need to work cooperatively to help ensure that policy uncertainty doesn’t weaken investment. Fiscal policy will need to manage trade-offs between supporting demand and ensuring that public debt remains on a sustainable path, and the optimal mix will depend on country-specific circumstances. Financial sector policies must address vulnerabilities proactively by deploying macroprudential tools. Low-income commodity exporters should diversify away from commodities given the subdued outlook for commodity prices. Monetary policy should remain data dependent, be well communicated, and ensure that inflation expectations remain anchored.

Across all economies, the imperative is to take actions that boost potential output, improve inclusiveness, and strengthen resilience. A social dialogue across all stakeholders to address inequality and political discontent will benefit economies. There is a need for greater multilateral cooperation to resolve trade conflicts, to address climate change and risks from cybersecurity, and to improve the effectiveness of international taxation.

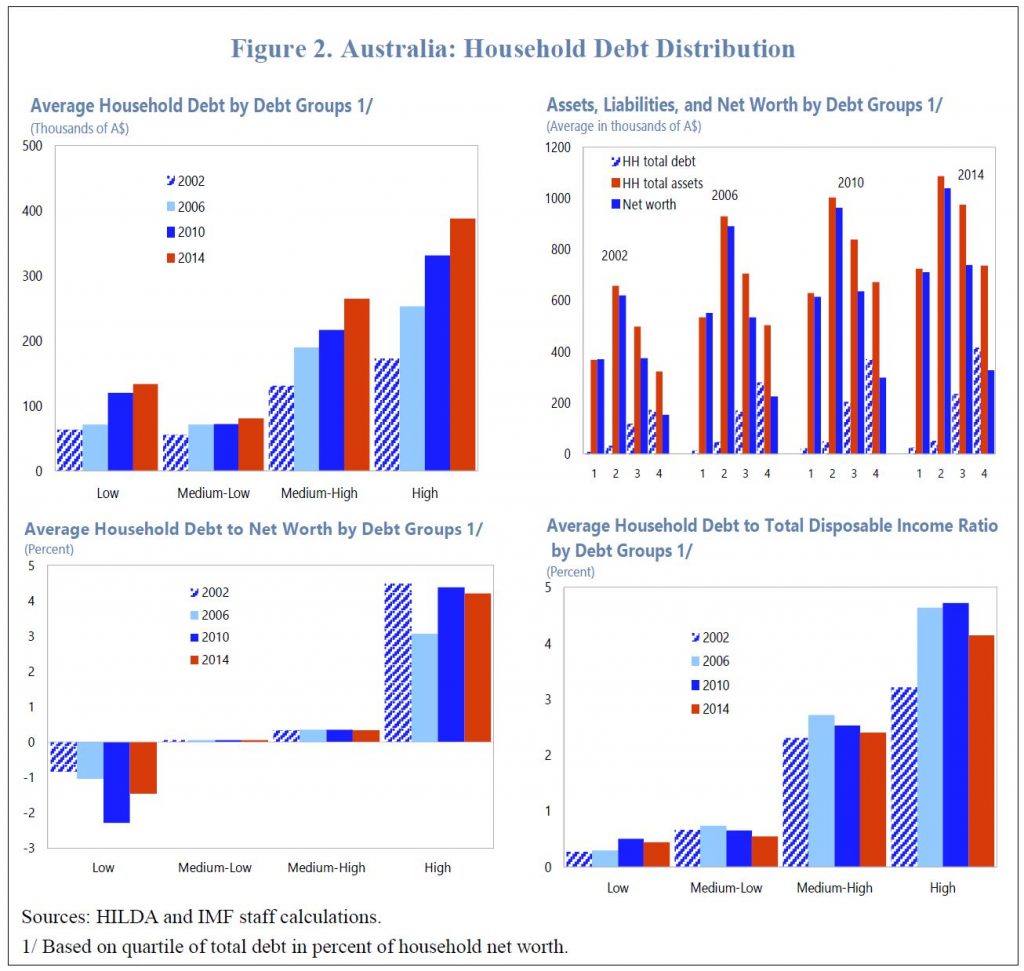

Within its 39 pages, the paper discusses the evolution of the household debt in Australia and finds that while higher-income and higher-wealth households tend to have higher debt, lower-income households may become more vulnerable to rising debt service over time.

Then, the paper analyzes the impact of a monetary policy shock on households’ current consumption and durable expenditures depending on the level of household debt. The results corroborate other work that households’ response to monetary policy shocks depends on their debt and income levels. In particular, households with higher debt tend to reduce their current consumption and durable expenditures more than other households in response to a contractionary monetary policy shocks. However, households with low debt may not respond to monetary policy shocks, as they hold more interest-earning assets.

And we should say at this point that IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and to encourage debate. The views expressed in IMF Working Papers are those of the author(s) and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

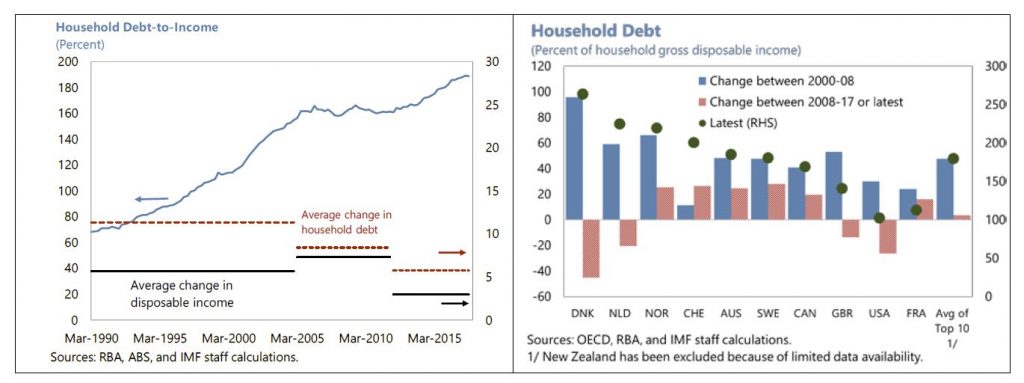

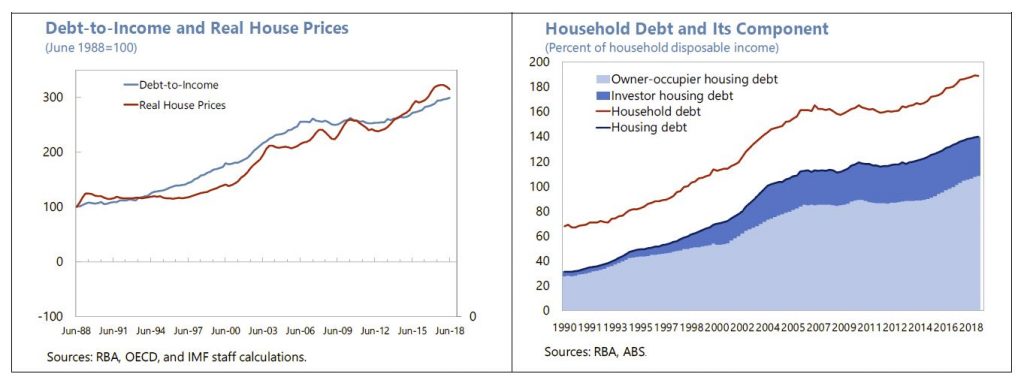

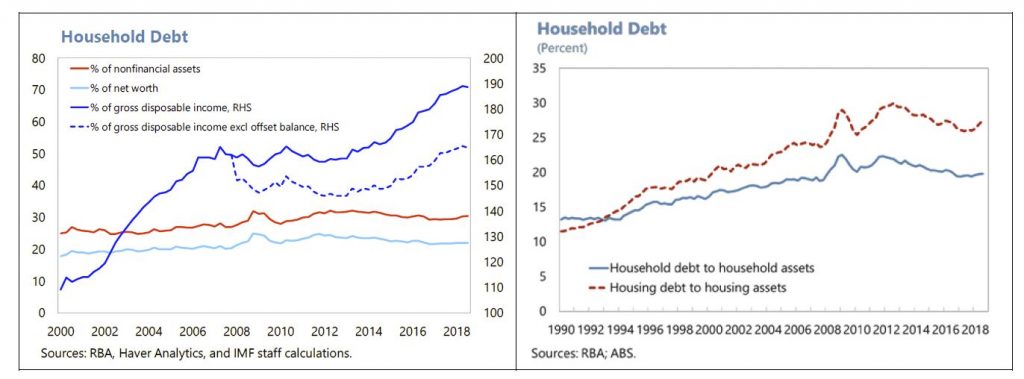

Household debt in Australia has increased to comparatively high levels over the last three decades, a period during which housing prices also have risen rapidly. By end-September 2018, the ratio of household debt to household gross disposable income reached 189 percent, among the highest in advanced economies. High levels of household debt are widely considered to be risky, as they can amplify the impact of external and domestic shocks and, thereby, increase a country’s economic and financial vulnerabilities and pose risks to financial stability. In addition to amplifying financial and economic vulnerabilities, high household debt can also intensify the ongoing corrections in the housing market in Australia.

The macroeconomic impact of and the risks from household debt depend not only on the average debt level but also its distribution across households. Higher-income households might be at lower risk of debt default than lower-income households, for example. The latter might also be more likely to be finance-constrained in times of debt distress. From a monetary policy perspective, a key consideration is the extent to which household debt levels and distribution affect monetary policy transmission.

Household debt in Australia has been rising faster than household disposable income for the past three decades. As a result, the household debt ratio has risen to one of the highest levels among advanced economies.

The housing boom has also played a significant role in the rapid accumulation of household debt. High housing demand due to income and population growth in conjunction with relatively inelastic supply have pushed up house prices, and expectations of future capital gains has encouraged investment demand for housing.

The interaction between the long-term upswing in housing prices and relatively easy mortgage financing has therefore led to the buildup of a high level of residential mortgage debt.

High household debt also reflects the preference for home ownership and housing investment in Australia. Housing debt at 140 percent of household disposable income accounted for about three-quarters of household debt outstanding as of September 2018, with owner-occupied housing debt accounting for a relatively stable share of about one half.

The rise in the share of investor housing debt since 2000 has also contributed to the fast increase in household debt, while other personal debt has remained broadly stable (one quarter of household debt outstanding) at about 46 percent of household disposable income since 2000.

For financial stability, as well as monetary and macroprudential policies, it is not only the level of household debt that matters but also the speed of debt accumulation or leverage increases, the extent of leverage, and, more importantly, the distribution of debt.

The IMF uses old data, from the HILDA survey, which has been running with annual frequency from 2001 to 2016 to make their assessment – clearly the debt position has deteriorated since then, yet they show that debt has grow across the cohorts and segments. The RBA analysis has the same fundamental flaw.

The paper finds that high debt exposure is more prevalent among higher-income and higher-wealth households. Nevertheless, the debt exposure of lower-income and more vulnerable households has also increased over time, and thereby more exposed to risks from rising debt service. The presence of over-indebted households at both low- and higher-income quintiles suggests that macro-financial risks have increased, suggesting a need for close monitoring.

Despite the high debt level, households’ debt service burden has remained manageable due to historical low mortgage interest rates and given that financial institutions assess mortgage serviceability for new mortgage lending with interest rate buffers above the effective variable rate applied for the term of the loans. However, downside risks on debt service capacity and consumption remain with regards to a sharp tightening of global financial conditions which could spill over to higher domestic interest rates.

The empirical analysis investigates the transmission of monetary policy shocks to the current consumption and durable expenditures of households with different debt-to-wealth ratios. With reasonable assumptions and using the large sample of households available in the HILDA survey for 2001-16, the results corroborate that households’ response to monetary policy shocks will vary, depending on both their debt and income levels.

In particular, the results suggest that households with high debt tend to reduce their current consumption and durable expenditures relatively more than other households in response to a contractionary monetary policy shocks. At the same time, households with low debt may not respond to monetary policy shocks, as they hold more interest-earning assets and thereby can smooth their consumption using the higher interest income, suggesting that for these households, the income effect dominates the intertemporal substitution effect.

The results of the analysis suggest that, with a larger share of high-debt households and given their high responsiveness to a monetary policy shock, it may take a smaller increase in the cash rate for the RBA to achieve its policy objectives, compared to past episodes of policy rate adjustments. It corroborates recent RBA research, which suggests that the level and the distribution of the household debt will likely alter monetary policy transmission, in other words, more bang for the buck. By responding gradually, the RBA can still meet its mandates.

The implications of higher household debt for monetary policy have also required that the RBA addresses this challenges in its communication. The results of the textual analysis show that the RBA’s communication has increasingly focused on the impact of household debt on monetary conditions and financial stability over the past decade, consistent with the rise in debt-to-income ratios. Markets have also started to take into account household debt in their assessment of monetary policy and market expectation analysis. Therefore, continuing with a transparent and strengthened communication strategy on issues related to the household debt and household consumption will further improve predictability and efficiency of monetary policy in Australia.

My take is the household debt burden is larger, and more exposed to potential risks than many accept. Nothing new perhaps, but the IMF highlighting the issues is one more piece of the too-high debt narrative!

And according to the AFR, in an exclusive interview, the International Monetary Fund’s lead economist for Australia, Thomas Helbling said Australia’s housing market contraction is worse than first thought, leaving the economy in what he called a “delicate situation” that boosts the need for faster infrastructure spending and even potential interest rate cuts.

Australia’s housing market contraction is worse than first thought!

David Lipton, the deputy director of the Washington-based International Monetary Fund, delivered a stark warning about the depleted power of central banks and governments to combat another sharp economic shock.

“ The bottom line is this: the tools used to confront the Global Financial Crisis may not be available or may not be as potent next time. The space for additional monetary policy accommodation will surely be more constrained; fiscal resources may not be as available in many countries; and political resistance to bailouts may be greater because many people feel that those who brought about the last crisis did not shoulder their share of the burden.”

So, in short, the emergency tool kit that helped to pull the global economy out of the Great Financial Crisis might not work a second time, the world’s lender of last resort has warned.

Global Challenges

Obviously, this is not a matter for Europe alone. The U.S. needs to

get its fiscal house in order as well. U.S.-China trade tensions pose

the largest risk to global stability. Beijing needs to continue its

shift toward high-quality growth and should support a sustainable

globalization. All emerging markets should face up to external shocks

and volatile capital flows.

While most baseline forecasts show some recovery ahead for Europe,

many have been surprised by the size and pace of the recent

deceleration. So, it is important to acknowledge the continuing

uncertainty about the coming year, including with the crucial issue of

Brexit still unresolved.

Each country should act now to strengthen their defenses ahead of a

potential downturn. That includes those who have not addressed glaring

vulnerabilities, most notably Italy. A serious recession could be very

damaging for these countries, because they will be shown to be ill

prepared. Their weaknesses could present a serious setback for Europe’s

goal of convergence—of standards of living, productivity, of national

well-being.

On the other hand, there are countries that are in a strong position to face a downturn—most notably Germany.

He warned that many countries need to drive reforms to deal with the emerging risks.

Blog")