Today I catch up with CEO and Founder of Ro&, an Australian based AI application which is bringing real world capability to the video intelligence and security industry, Roanne Monte.

Link: https://www.roand.ai/

We discuss the origin of the business idea, its development and launch via Armatec Global, and the broader questions about the future of AI and how it plays into current world events.

This is a remarkable story which shows Australia can innovate and lead!

http://www.martinnorth.com/

Details of our one to one service are here: https://digitalfinanceanalytics.com/blog/dfa-one-to-one/

Go to the Walk The World Universe at https://walktheworld.com.au/

Today I catch up with CEO and Founder of Ro&, an Australian based AI application which is bringing real world capability to the video intelligence and security industry, Roanne Monte.

Link: https://www.roand.ai/

We discuss the origin of the business idea, its development and launch via Armatec Global, and the broader questions about the future of AI and how it plays into current world events.

This is a remarkable story which shows Australia can innovate and lead!

http://www.martinnorth.com/

Details of our one to one service are here: https://digitalfinanceanalytics.com/blog/dfa-one-to-one/

Go to the Walk The World Universe at https://walktheworld.com.au/

Neo-Bank Volt has closed its doors and is returning deposits to its customers and selling its mortgage book. We look at why this happened, and whether other banks are at risk in this rising rate environment.

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

Volt Bank Loses Its Spark! Others May Follow.... [Podcast]

More about innovation from Zoran from SmarterLite.

SmarterLite’s Chief Technology Officer, Zoran Ovuka, explains the innovation journey the company has been on as it has created a next generation luminosity product. https://smarterlite.com/.

SmarterLite’s Chief Technology Officer, Zoran Ovuka, explains the innovation journey the company has been on as it has created a next generation luminosity product. https://smarterlite.com/.

Proof Australian firms have the capacity to be innovative, despite the many barriers in play.

Go to the Walk The World Universe at https://walktheworld.com.au/

I chat with Des Vary from Bentley Power Equipment, a Western Australian business which has been leading the way in terms of innovate green lighting solutions. But the journey has not been straightforward and yet the potential is significant. We tell his story, as part of our innovation series.

Three years ago, then prime minister Malcolm Turnbull went to an

election spruiking the wonders of innovation. “There has never been a

more exciting time to be an Australian,” government advertising had

enthused in the months before.

But the public wasn’t enthused, and Turnbull’s government barely scraped back into office.

Since then innovation policy has spooked the political class. They

see it as a vote loser, and a threat to jobs – mostly their own.

Consequently, innovation and industry policy has received the least attention just when the decline of investment in research and development may matter most to our economic future.

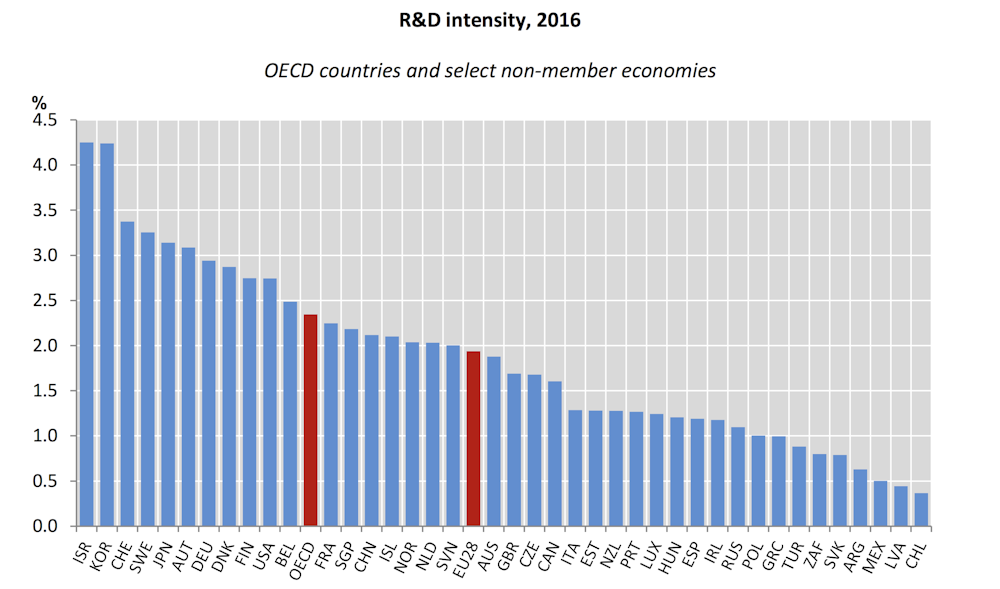

The red bars show the average

intensity of the member states of the OECD and the European Union. Data

for Argentina, Australia, New Zealand, Poland, Switzerland, Turkey, and

South Africa is from 2015; data for Singapore is from 2014.

OECD Main Science and Technology Indicators Database

Here’s how we got to where we are.

A deafening, blinding boom

After the terms of trade downturn of the 1980s and the economic

reforms of the 1990s, Australia enjoyed the biggest, unanticipated

mining boom in our history, thanks to the rise of China. John Howard

wanted us to be “relaxed and comfortable” and we were, at least while it

lasted.

Increased commodity prices boosted our terms of trade, without any extra effort on our part. By contrast with Norway,

which prepared for its post-oil future with a 76% resource rent tax and

sovereign wealth fund, Australians enjoyed tax cuts and a spending

splurge.

However, the underlying structural problem of our economy had not gone away.

Measured by the research intensity of our exports, Australia’s “economic complexity” ranks at 59, between Kazakhstan and Lebanon.

This index compiled by MIT’s Observatory of Economic Complexity is topped by Japan, Switzerland and Germany. Our position in global innovation rankings is no less dismal, especially when it comes to turning ideas into products.

While recent domestic growth has been driven by services, retail and

construction, our future living standards will depend on how we pay our

way in the world. This means identifying new, more sustainable sources

of export income.

Of course, resources will still have a part to play, but not as

unprocessed raw materials. For example, we have everything we need for

renewable energy production, battery manufacture and hydrogen exports.

And how could anyone contemplate continuation of the barbaric live

animal trade?

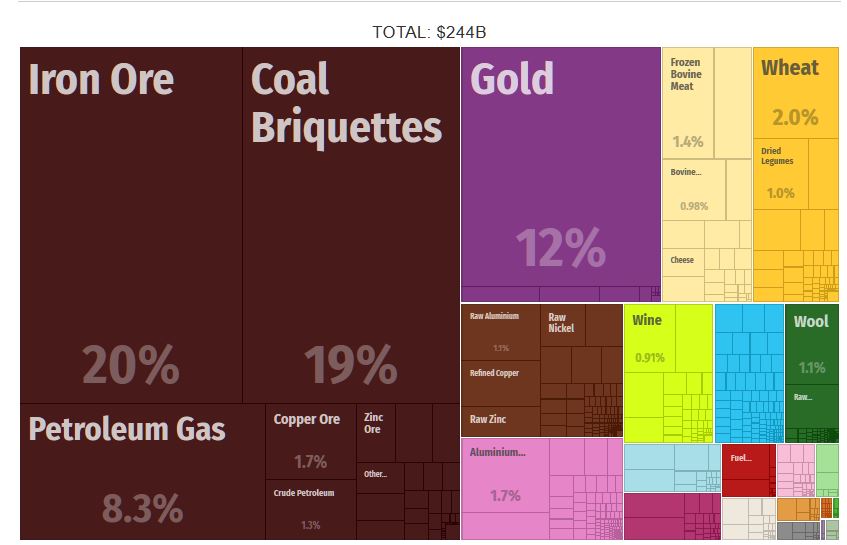

The graphic below shows Australia’s export profile in 2017. Of US$244

billion in total exports, US$131 billion were mineral products.

This rebalancing won’t happen automatically through the market. It will require active intervention

to manage the post-mining boom transition to an inclusive and dynamic

knowledge-based economy. And to reverse the slowdown in productivity

growth associated with current wage stagnation.

Too obvious to ignore

During the boom, high prices for coal and iron ore masked Australia’s deteriorating productivity performance. Now mining no longer contributes to growth, the impact on our national income has become all too obvious.

That’s why it was so important to Malcolm Turnbull to reinvigorate the national innovation and science agenda with a focus on startups and business-university collaboration, after Tony Abbott’s $3 billion cuts to Labor’s programs.

And why it was then so disappointing he could not build on his agenda for an “ideas boom” to replace the mining boom.

The Coalition government has cycled through three prime ministers and

six industry ministers. It continues to cut science and innovation

programs. Its latest budget “savings” included $4 billion from the

Research and Development Tax Incentive scheme, $3.8 billion from the

Education Investment Fund and $2.2 billion from higher education.

As a result, Australia’s total spending on research and development

is now just 1.88% of GDP, from 2.11% five years ago. The government

contribution (0.57%) is where it was in the 1980s. Meanwhile Japan and

Sweden are committing more than 3%, and Korea and Israel more than 4%.

Small target strategies

For any mention of innovation and industry policy in the current election campaign, you have to look hard.

The Coalition has confined itself to some low-key announcements on a

new space agency, defence innovation, genomics, food, marine science and

manufacturing.

It has rejected or parked the recommendations of its own Innovation and Science Australia 2030 strategy, including using any savings from winding back the R&D Tax Incentive to promote high-growth export opportunities.

Labor has committed to a “collaboration premium”

to encourage business engagement with universities and the CSIRO as

part of a restructured R&D Tax Incentive (another key recommendation

of the 2030 strategy).

However, it will also “bank” the Coalition’s savings to achieve its

budget surplus. In this context, it will be all the more challenging for

a new Labor government to achieve its R&D target of 3% of GDP,

given that this will require additional investment of at least $20

billion.

In addition, Labor has announced an “off-budget” $1 billion

Manufacturing Future Fund and a series of initiatives on renewable

technologies, biofabrication, food and fibre, artificial intelligence,

blockchain, space, hydrogen, electric vehicles and “digital skills

hubs”. In an important symbolic gesture, it has also promised to rescue

CSIRO climate science.

These initiatives are clearly worthwhile, but do not restore the funding that has been lost, let alone increase it.

If new policy must be paid for, why not cut expenditure that actually impedes economic transition? The diesel fuel tax rebate,

for example. This $6 billion scheme, whereby taxpayers subsidise fuel

costs for the resources sector, is equivalent to almost half the entire

annual budget outlay for research and innovation.

Weighing the costs

Most successful economies around the world use “knowledge foresights”

to identify national priorities in areas of existing or potential

competitive advantage. They have long-term, coherent policy frameworks for pursuing these priorities.

Australia’s next government will have a chance to devise such a framework, in cooperation with business, unions and research organisations. Of course, it will require substantial public as well as private investment. But we can no longer afford a “do nothing” approach.

Author: Roy Green, Emeritus Professor & UTS innovation adviser, University of Technology Sydney

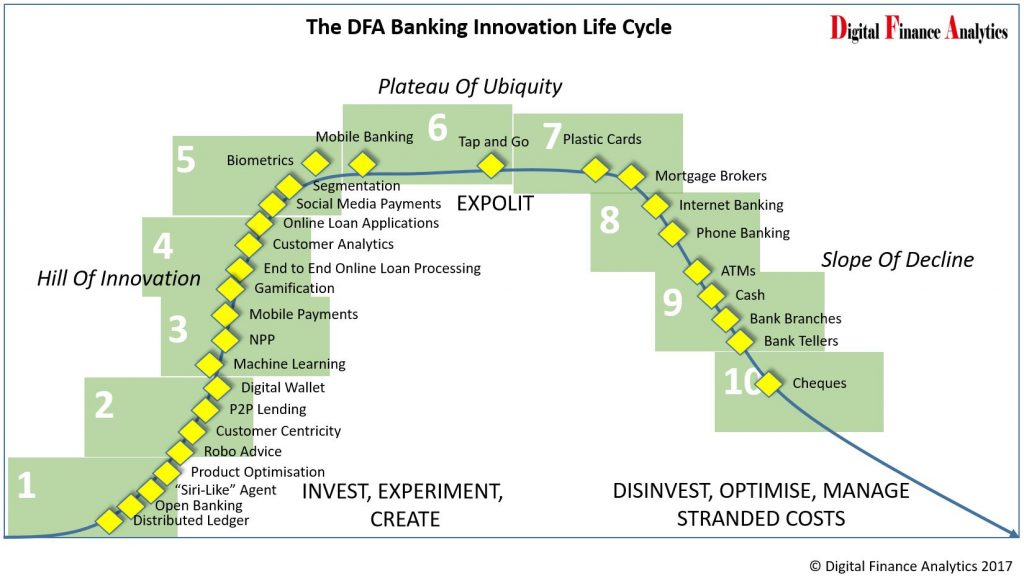

Given the tenor of the Royal Commission responsible lending inquiries this week, which focussed on the complexities of brokers and lenders complying with their responsible lending obligations, we believe the future will be distinctly digital. Our banking innovation life cycle road map calls this out.

To illustrate the point, there was a timely announcement from the Opica Group who have a new, and they claim Australia’s first responsible lending engine” (RELIE). This from The Adviser.

A new artificial intelligence-based expenses verification engine has been launched for brokers and lenders to ensure responsible lending and compliance obligations are met.

Billing the tech as “Australia’s first responsible lending engine” (RELIE), the Opica Group has launched the platform to help “protect any broker or lender from a breach of their responsible lending requirements”.

According to Opica Group founder Brett Spencer, the platform is needed because “lenders traditionally have been very quick to put blame on brokers for any application that goes sour”.

Mr Spencer said that following a tighter regulatory environment and “greater scrutiny being placed on our industry by regulators”, the group identified that “brokers needed something that provided them some protection”.

As such, it built the RELIE platform to enable brokers (and lenders) to perform a “RelieCheck” that could prove they had done the adequate checks into expenses and the consumer’s ability to service the loan.

How it works

The RELIE engine makes use of a specially built artificial intelligence engine, Sherlock™, which analyses a consumer’s banking and credit card transaction data over a period of 12 months and automatically provides “income verification, an understanding of the client’s mandatory expenditure, and therefore their ability to service a loan”.

According to the group, the key differentiator of the RELIE platform when compared to credit checks is that it uses machine learning to categorise transactions, allowing for the differentiation of transaction types, including mandatory versus discretionary expenditure and recurring versus one-off spending.

It also automatically highlights areas of concerns within the transaction data such as undisclosed debts, spikes in expenditure of high-risk categories such as gambling, and possible changes in life circumstances such childbirth.

Mr Spencer commented: “With the advancements in technology and legislation crackdown, we saw an opportunity to protect brokers and automate significant components of an applicant’s income and expense verification process…

“We believe that running a RelieCheck will protect any broker or lender from a breach of their responsible lending requirements.”

Speaking to The Adviser, Mr Spencer elaborated: “While a credit check simply looks at your credit worthiness, a RelieCheck looks at the consumer’s 365-day spending and income transactions and interrogates the data from a responsible lending perspective.

“It then presents back to the broker or lender a summary of exactly what, when and where an applicant’s income and expense are positioned.”

However, the Opica Group founder said that while the AI engine “does all the grunt work” to auto categorise and allocate spends to a range of buckets (such as mandatory versus discretionary expenses), the broker is able to review each category of spend and re-allocate expenses to a different category as part of their responsible lending discussions with the customers.

Each change made is then notated by the broker in order to meet their responsible lending requirements.

Revealing that the engine has been 16 months in the making, Mr Spencer said that the group wanted to “create a platform that a broker could use to protect themselves from any unintended breach of their responsible lending requirements”.

He added: “We also wanted to speed up the physically demanding process of paper-based statement reviews so that a broker could reduce the amount of time it takes to process a loan, and in the process providing a far greater service to the customer.”

Opica Group revealed that “early indications” have shown that by performing a RelieCheck on an applicant, a broker or lender could reduce processing times by approximately 90 minutes per application (when compared to manual assessment of the applicant’s banking and credit card transactions).

Mr Spencer concluded: “We want to create a new industry standard.

“Data is a commodity, but what you do with the data is the key ingredient.”

He added that he did not believe anyone else was thinking about “what we do with the data to aid the lending process”.

Opica Group is reportedly working with a number of aggregators and lenders to establish whether the engine could be integrated into their customer relationship management (CRM) systems. The service costs $15 (plus GST) per applicant for a broker account, or $10 (plus GST) per applicant for an aggregator or lender account.

The Financial Conduct Authority (FCA) is the conduct regulator for 56,000 financial services firms and financial markets in the UK and the prudential regulator for over 18,000 of those firms. The FCA recently published feedback on its Discussion Paper on Distributed Ledger Technology (DLT).

In April 2017 The FCA announced that it was seeking stakeholder views on the potential for future development of DLT in the markets the FCA regulates.

The FCA received 47 responses from a wide range of market participants including regulated firms, national and international trade associations, technology providers, law firms and consultancies.

DLT has come to greater public prominence as it underpins digital currencies such as Bitcoin. This paper is not about Bitcoin or other so-called cryptocurrencies. Rather its remit is to consider the range of ways that DLT can impact on financial services and the regulatory implications.

Respondents expressed particular support for the FCA maintaining a ‘technology-neutral’ approach to regulation and welcomed the FCA’s open and proactive approach to new technology, including our Sandbox and RegTech initiatives.

The feedback also suggested that current FCA rules are flexible enough to accommodate the use of DLT by regulated firms and no changes to specific rules were proposed. Many respondents suggested that DLT solutions could deliver regulatory requirements more efficiently than current systems, substantially reducing costs for firms and regulators alike.

However, some respondents doubted the compatibility of permissionless networks (permissionless networks allow general public visibility of transactions online and are open for broad participation whilst permissioned networks typically feature a ‘gatekeeper’ who controls access) with our regulatory regime. Based on the feedback and its own work, overall the FCA is open to all forms of deployment of DLT (including both permissioned and permissionless DLT networks) provided the operational risks are properly identified and mitigated.

The FCA will continue to monitor DLT-related market developments, and keep its rules and guidance under review in the light of those developments. It will work collaboratively with industry, HM Treasury, the Bank of England, the Information Commissioner’s Office and other UK bodies to ensure a co-ordinated approach towards DLT in the UK. At an international level, the FCA will work closely with national and international regulatory bodies to shape regulatory developments and standards.

On the Initial Coin Offering (ICO) market, the FCA will gather further evidence and conduct a deeper examination of the fast-paced developments. Its findings will help to determine whether or not there is need for further regulatory action in this area beyond the consumer warning issued in September. In the meantime, the FCA highlights how an ICO-related business proposition needs to be designed to satisfy the ‘consumer benefit’ condition for access to the FCA’s Innovate facilities.

Christopher Woolard, Executive Director of Strategy and Competition at the FCA, said:

“The original paper opened a discussion about DLT and the volume and breadth of responses we received from the industry demonstrates the significance of this issue. DLT has the potential to transform practices across a number of markets, sharpening competition and improving risk management. At the same time we have to be alive to the risks of certain applications of it. We will continue to work with a range of agencies and firms to ensure a co-ordinated approach to the use of DLT in financial services.”

Blog")