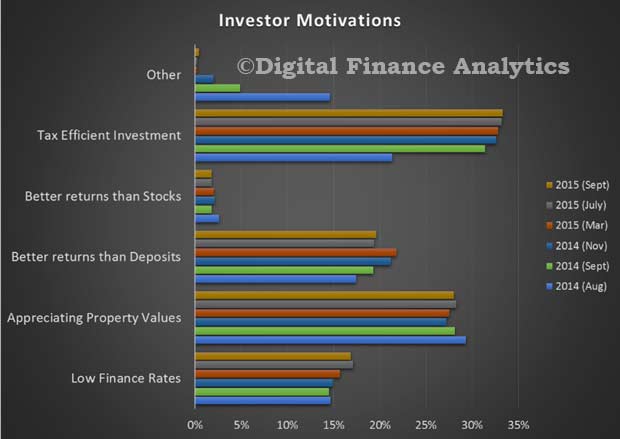

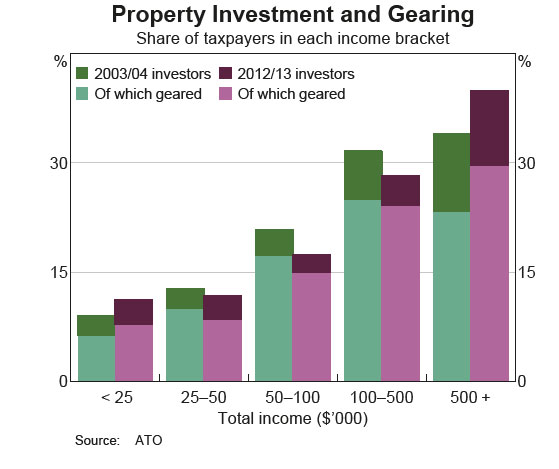

Continuing our series on the latest findings from The Property Imperative, we look at property investors today. We find that they are seriously optimistic about the future of property (and recent capital gains have fueled their future expectations).

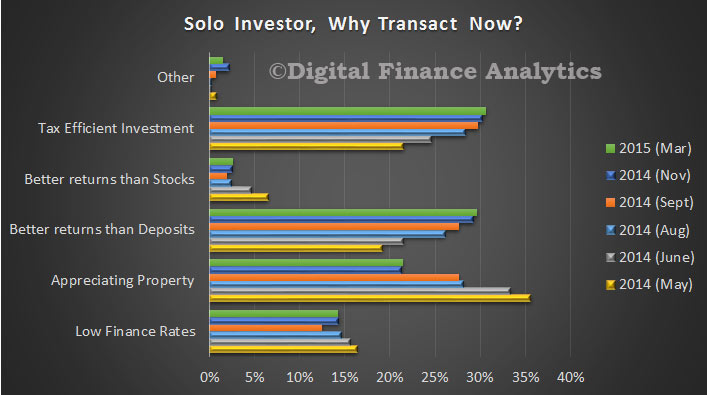

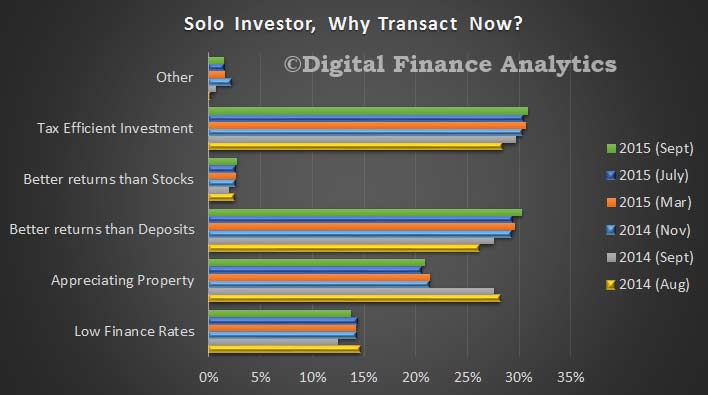

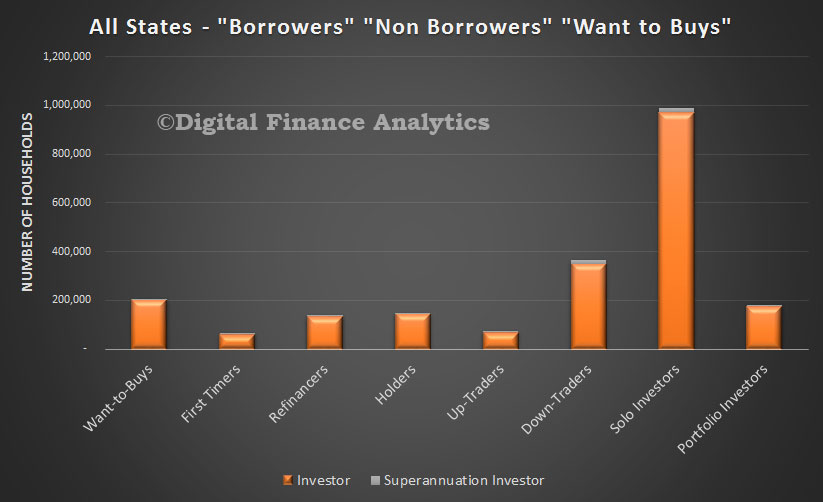

Looking first at what we call solo investors, about 987,000 households only hold investment property, 2.2% of which are held within superannuation. Households in this segment will often own one or two properties, but do not consider they are building an investment portfolio.

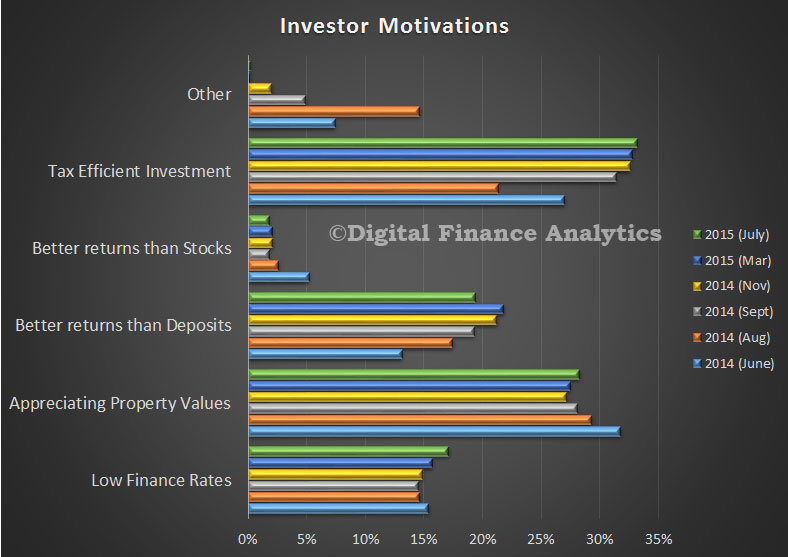

They are strongly driven by the tax efficient nature of property investment via negative gearing and capital gain concessions. They also have enjoyed low finance rates, strong capital appreciation, and better returns than from bank deposits.

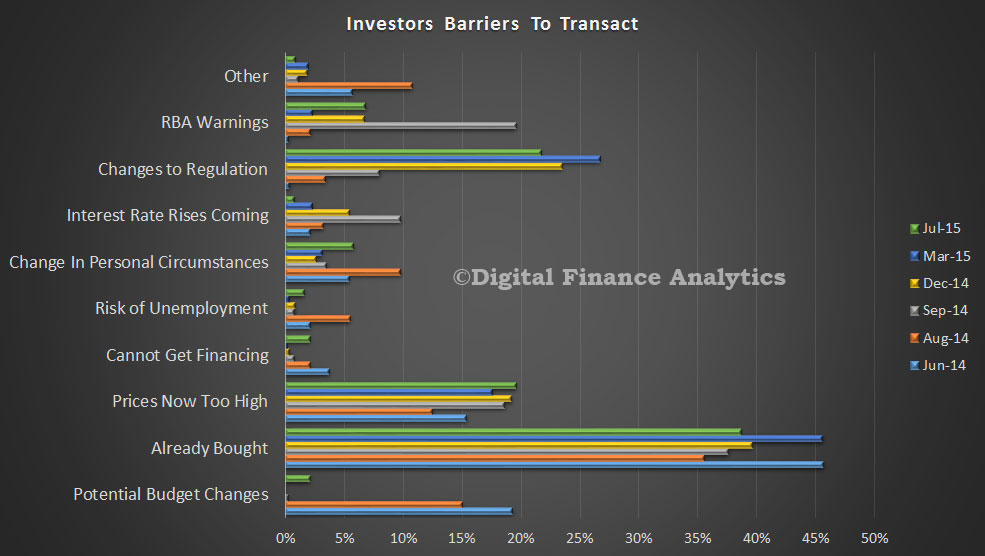

Around 84% of households expect prices to rise in the next 12 months, 42% of households expect to transact within the next year, 51% will need to borrow more, and 39% will consider the use of a mortgage broker.

Around 84% of households expect prices to rise in the next 12 months, 42% of households expect to transact within the next year, 51% will need to borrow more, and 39% will consider the use of a mortgage broker.

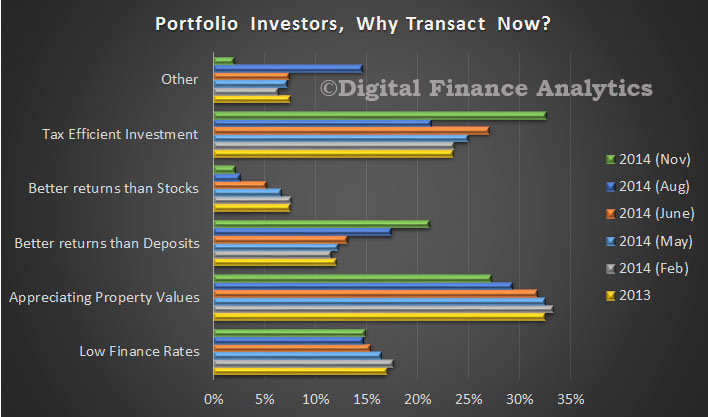

Turning to portfolio investors who are households who are portfolio investors maintain a basket of investment properties. There are 178,000 households in this group.We see somewhat similar motivations as discussed above, with tax efficiency being the strongest driver, followed by appreciating property values and good returns. We see a number of these households devoted to property investment as a full-time occupation.

Indeed, the median number of properties held by these households is seven. Most households expect that house prices will rise in the next 12 months (88%), and 77% said they will transact in the next 12 months.

Indeed, the median number of properties held by these households is seven. Most households expect that house prices will rise in the next 12 months (88%), and 77% said they will transact in the next 12 months.

Many will borrow more to facilitate the transaction (85%), and 53% will use a mortgage broker. Significantly we now see about 21% of portfolio investors looking to their property investments as the main source of income, it has in effect become their full time job.

Next time we look at those investing via a self managed superannuation fund.

Go here to request a copy.

Go here to request a copy.