The final set of ABS data on finance for July 2016 includes all forms of lending, and does not tell a good story. Whilst investment housing lending grew, lending for productive business growth fell, again.

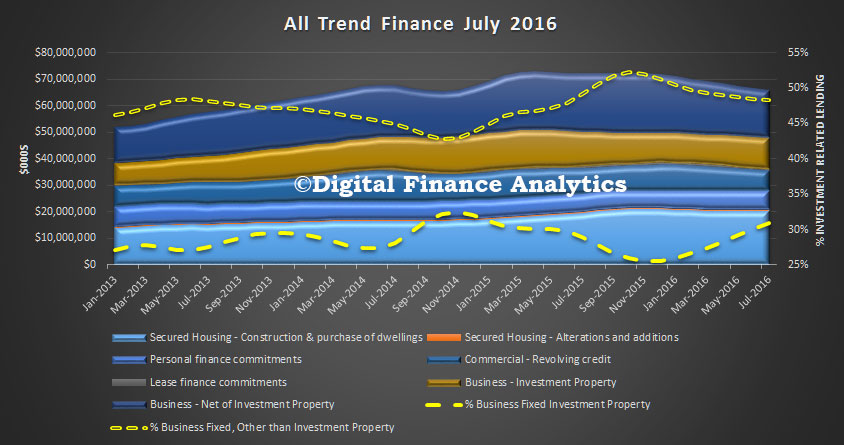

Here is the summary, having separated business lending for housing investment purposes, versus the rest. As normal we will focus on the trend data, which irons out some of the noise in the data, to see through to the underlying movements.

Lending for secured construction and purchase of dwellings fell 0.1%, or $20m, month on month, secured alterations rose just a little, personal finance rose 0.1% or $6m and overall commercial lending fell 1.75% or $671m compared with last month, and continues to fall.

Within the business or commercial flows, lending for investment property rose 1.1% or $127m, compared with last month, whilst lending for other commercial purposes fell 2% or $384m. Revolving commercial credit fell 5% down $416m.

So productive lending to business continues to fall, and overall lending is being supported by more investment housing. As a result, the proportion of business lending for investment housing rose again to 31% of commercial lending, whilst lending for other commercial purposes fell again to 48.2% of all commercial lending. These trends need to be reversed if we are to get real productive economic growth to kick in.

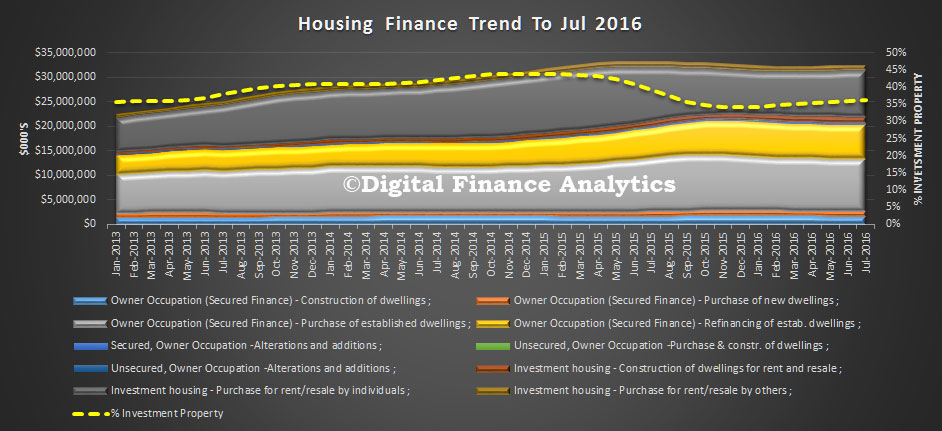

Finally, for completeness, here is the housing data, once again showing the ongoing rise in the proportion of investment housing lending, up 1.1% or $127m on last month, and up from 35.9% to 36.1% of total flows.

Finally, for completeness, here is the housing data, once again showing the ongoing rise in the proportion of investment housing lending, up 1.1% or $127m on last month, and up from 35.9% to 36.1% of total flows.

We think tighter macroprudential measures are overdue.

We think tighter macroprudential measures are overdue.