The latest edition of our finance and property news digest with a distinctively Australian flavour.

CONTENTS 0:00 Introduction 1:09 Westpac Says Home Prices Will Grow 3:30 Rising Yields A Risk 7:36 NAB Cuts Mortgage Rates 9:39 NAB;s Troubles Loans 10:40 ME Bank Sold To Bank Of Queensland 13:31 NZ Cash Rate May Rise – Soon 17:22 Conclusions

Go to the Walk The World Universe at https://walktheworld.com.au/

A reprise of the current market moves, and a discussion about the underlying drivers, as well as the top 5 issues we get asked about. Plus a quick preview of a new intro…

0:00 Start 0:30 Market Moves 0:26 Nucleus Wealth Article On Capitalism 8:53 Markets 16:14 Drivers 17:33 Top 5 Topics 20:42 New Intro Candidate 21:06 Outro

A reprise of the current market moves, and a discussion about the underlying drivers, as well as the top 5 issues we get asked about. Plus a quick preview of a new intro…

0:00 Start 0:30 Market Moves 0:26 Nucleus Wealth Article On Capitalism 8:53 Markets 16:14 Drivers 17:33 Top 5 Topics 20:42 New Intro Candidate 21:06 Outro

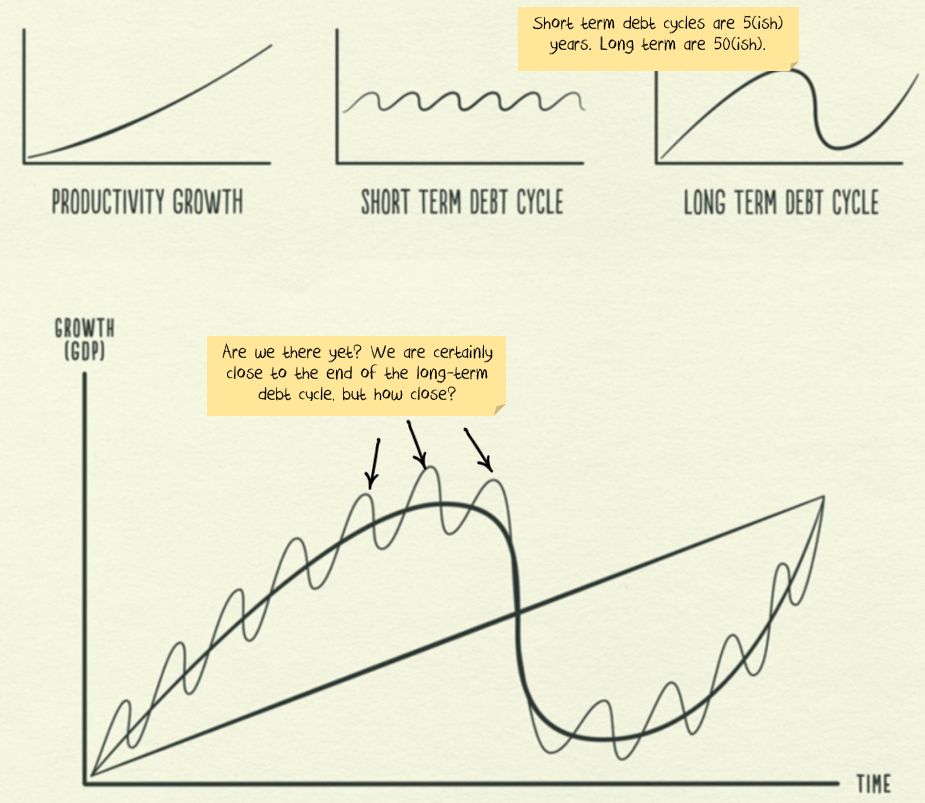

Ray Dalio has a series of explanatory videos that talk about debt cycles and in particular the contrast between a short debt cycle and a long debt cycle.

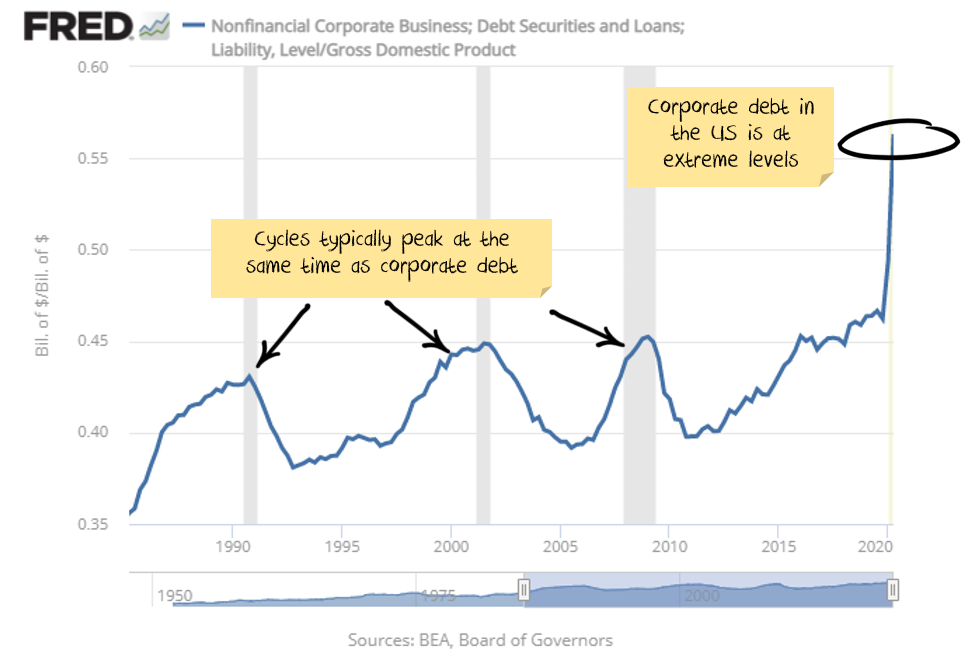

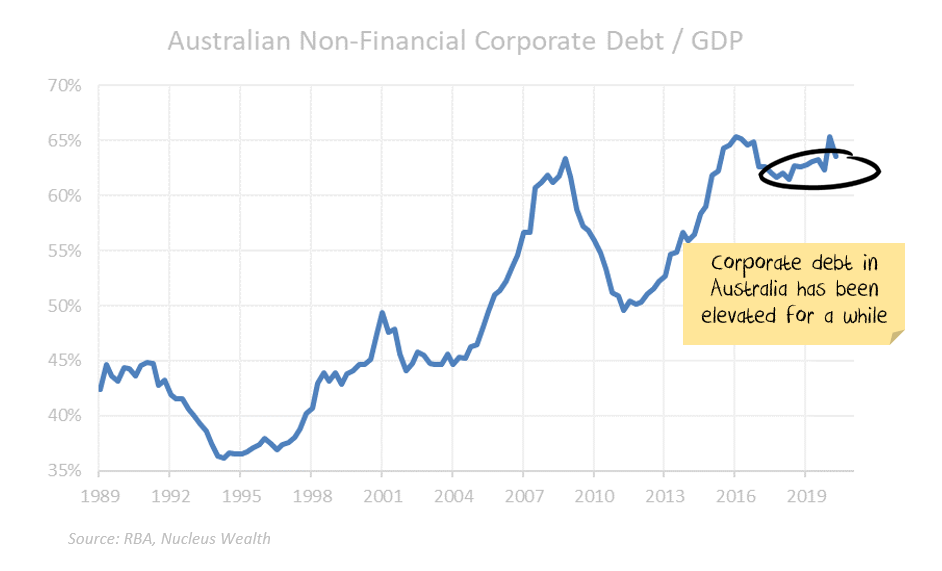

With record levels of corporate debt around most of the globe:

COVID-19 lockdowns suggested that this would be the end of the current short term debt cycle and potentially the end of the current long term debt cycle.

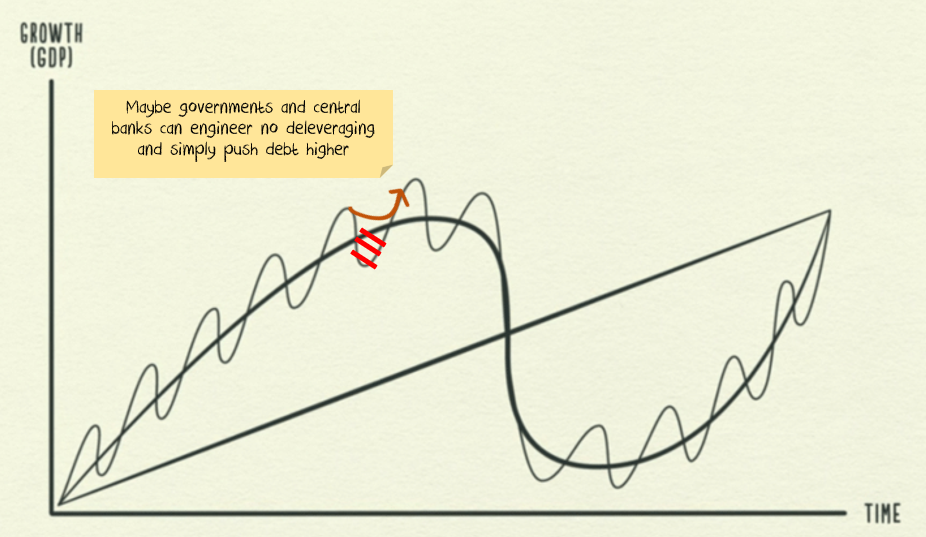

Governments and central banks to the rescue

Swift intervention by central banks and governments hit pause on the start of deleveraging. In effect they threw a lot of money at the economy, most ended up cushioning the blow for people who suffered from the shutdown. But a significant amount also ended up with people who didn’t suffer. Also, without travel, many more affluent people travelled less and consequently increased their saving and investment.

Also, evictions and bankruptcies were made more difficult, and interest-rate holidays on loans given. The new rules prevented negative outcomes while encouraging positive ones. The stock market boomed.

Is capitalism finished?

We have been cautious on risk for months, avoiding the crisis at the start, but with minimal participation in the market recovery. And, to date, we have been wrong. We did identify the most likely reason to be wrong would be if governments would take ever more extreme steps to cancel capitalism. And that is what happened.

In many countries, “extend and pretend” has replaced the threat of bankruptcy. Someone who can’t pay their rent is not evicted but allowed to accrue debt. Don’t foreclose on those who can’t pay their interest. Instead, build up their interest payments into a larger debt burden.

The end game seems to be a cohort of zombie consumers and businesses. Weighed down by debt burdens too massive to ever pay off, but supported by interest rates low enough to keep them from defaulting.

US Treasury Secretary Mnuchin is letting several minor lending programs expire at the end of the year, to the loud complaints of many – including the US central bank. Many programs will likely be re-instated once Biden is in power. In other countries, there is very little consideration given to finishing similar programs.

It would seem we have a zombie future.

Can the debt cycle blast higher?

The question from here is whether a new debt boom can be launched without the old one ever having peaked.

Until recently, I thought the odds favoured the end of the cycle. I was wrong.

I’m still sceptical of a debt boom for businesses. Governments and central banks will try, but debt levels are already high and further interest rate reductions will be limited.

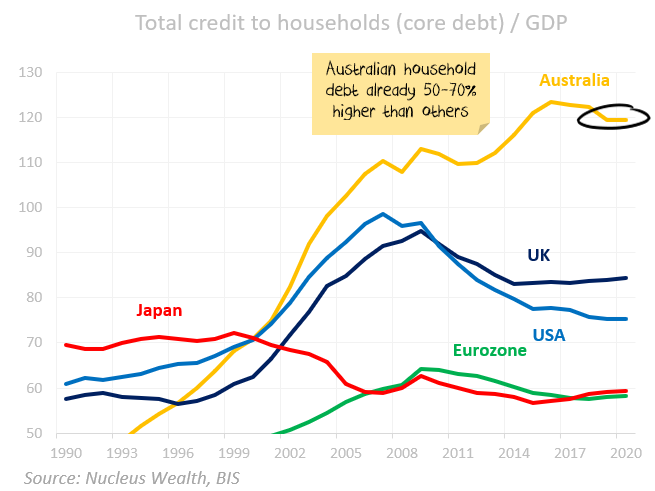

Another household debt boom is possible. Although Australia has already played this card:

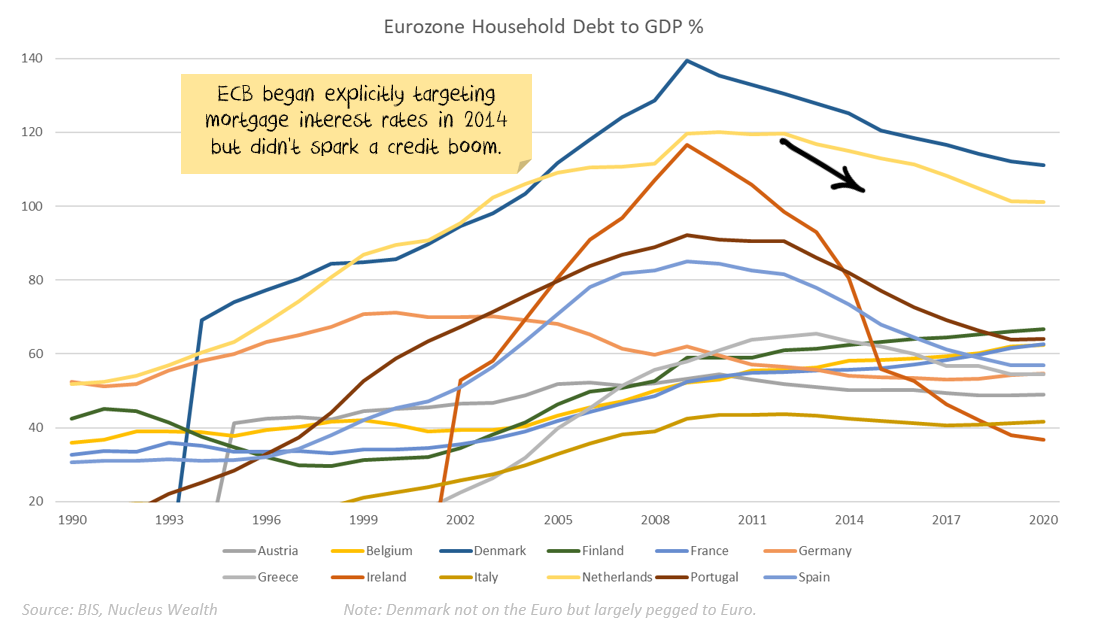

The other difficulty is that despite the European Central Bank’s best efforts, household debt has been declining across much of the Eurozone.

The most likely outcome now appears to be continued increases in government debt, but limited increases in corporate debt. Household debt is an open question.

Are we reduced to watching governments and central banks?

Mostly. It seems clear that policymakers have decided on zombification. Limit bankruptcies. Increase debt. Never raise interest rates again.

It doesn’t make for a healthy economy. But it limits short term pain which appears to be the current goal of every politician.

The economic plan is to try to get a debt-funded consumer boom going so that bankruptcy protection and consumer support can be removed.

Policy mistakes are what matters from here. The goal? Prevent a business cycle from occurring.

Indications that a normal business cycle is occurring will be a sign to sell. Too much support and markets will grind higher.

Damien Klassen is Head of Investments at Nucleus Wealth.

We overview the recent shows on Walk The World, where I discussed deflation and inflation with Steve Van Metre and the recent In The Interests Of The People show with John Adams following his article on the question of Quantitative Easing and deflation.

I caught up with Steve Van Metre to discuss the latest macro outlook.

Steven Van Metre, Certified Financial Planner™ Professional, (CA Insurance License #0D45202 & Investment Advisory Representative with Atlas Financial Advisors, Inc., a Registered Investment Advisory firm.) is a financial planner, portfolio manager, and President of Steven Van Metre Financial. He specializes in retirement income strategies and the direct management of client assets.

I caught up with Economist and Author Harry Dent, ahead of his debate on Friday (Sydney time) with Peter Schiff, who I also interviewed last week. https://youtu.be/iIDp1le35bU

Debate between Harry Dent and Peter Schiff 20th November 2020 http://crisisdebate.com

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

Gold Inflation Deflation With Harry Dent [Podcast]

I caught up with Steve Van Metre to discuss the latest macro outlook.

Steven Van Metre, Certified Financial Planner™ Professional, (CA Insurance License #0D45202 & Investment Advisory Representative with Atlas Financial Advisors, Inc., a Registered Investment Advisory firm.) is a financial planner, portfolio manager, and President of Steven Van Metre Financial. He specializes in retirement income strategies and the direct management of client assets.

Blog")