Welcome to our latest post covering finance and property news with a distinctively Australian flavour. Given the current market gyrations, we are going to examine the latest critical data each day, because a week is a long time in politics but a lifetime on the markets at the moment…

As Australia’s financial system adjusts to the coronavirus (COVID-19), financial

regulators and the Australian Government are working closely together to help ensure

that Australia’s financial markets continue to operate effectively and that credit

is available to households and businesses. (Refer to earlier Council of Financial Regulators’ (CFR)

press release.)

Australia’s financial system is resilient and it is well placed to deal with the

effects of the coronavirus. At the same time, trading liquidity has deteriorated in some

markets.

In response, the Reserve Bank stands ready to purchase Australian government bonds in

the secondary market to support the smooth functioning of that market, which is a key

pricing benchmark for the Australian financial system. The Bank will also be conducting

one-month and three-month repo operations in its daily market operations until further

notice to provide liquidity to Australian financial markets. In addition the Bank will

conduct longer term repo operations of six-months maturity or longer at least weekly, as

long as market conditions warrant. The Reserve Bank and the AOFM are in close liaison in

monitoring market conditions and supporting continued functioning of the market.

The Bank will announce further policy measures to support the Australian economy on Thursday.

DFA is expecting a 0.25% rate cut, and formal QE to go alongside the repo operations already in train.

In addition the Federal Reserve on Sunday announced it would purchases $700 billion in bonds and securities to stabilize financial markets and support the economy.

The emergency rate cut and push to flood the Treasury bond market with liquidity comes as the coronavirus pandemic forces businesses across the U.S. and world to shutter, likely plunging the global economy into a recession.

The Bank of Canada, the Bank of England,

the Bank of Japan, the European Central Bank, the Federal Reserve, and

the Swiss National Bank are today announcing a coordinated action to

enhance the provision of liquidity via the standing U.S. dollar

liquidity swap line arrangements.

These central banks have agreed to lower

the pricing on the standing U.S. dollar liquidity swap arrangements by

25 basis points, so that the new rate will be the U.S. dollar overnight

index swap (OIS) rate plus 25 basis points. To increase the swap lines’

effectiveness in providing term liquidity, the foreign central banks

with regular U.S. dollar liquidity operations have also agreed to begin

offering U.S. dollars weekly in each jurisdiction with an 84-day

maturity, in addition to the 1-week maturity operations currently

offered. These changes will take effect with the next scheduled

operations during the week of March 16.1

The new pricing and maturity offerings will remain in place as long as

appropriate to support the smooth functioning of U.S. dollar funding

markets.

The swap lines are available standing

facilities and serve as an important liquidity backstop to ease strains

in global funding markets, thereby helping to mitigate the effects of

such strains on the supply of credit to households and businesses, both

domestically and abroad.

The coronavirus outbreak has harmed communities and disrupted economic activity in many countries, including the United States. Global financial conditions have also been significantly affected. Available economic data show that the U.S. economy came into this challenging period on a strong footing. Information received since the Federal Open Market Committee met in January indicates that the labor market remained strong through February and economic activity rose at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although household spending rose at a moderate pace, business fixed investment and exports remained weak. More recently, the energy sector has come under stress. On a 12‑month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation have declined; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the

Committee seeks to foster maximum employment and price stability. The

effects of the coronavirus will weigh on economic activity in the near

term and pose risks to the economic outlook. In light of these

developments, the Committee decided to lower the target range for the

federal funds rate to 0 to 1/4 percent. The Committee expects to

maintain this target range until it is confident that the economy has

weathered recent events and is on track to achieve its maximum

employment and price stability goals. This action will help support

economic activity, strong labor market conditions, and inflation

returning to the Committee’s symmetric 2 percent objective.

The Committee will continue to monitor the

implications of incoming information for the economic outlook,

including information related to public health, as well as global

developments and muted inflation pressures, and will use its tools and

act as appropriate to support the economy. In determining the timing and

size of future adjustments to the stance of monetary policy, the

Committee will assess realized and expected economic conditions relative

to its maximum employment objective and its symmetric 2 percent

inflation objective. This assessment will take into account a wide range

of information, including measures of labor market conditions,

indicators of inflation pressures and inflation expectations, and

readings on financial and international developments.

The Federal Reserve is prepared to use its

full range of tools to support the flow of credit to households and

businesses and thereby promote its maximum employment and price

stability goals. To support the smooth functioning of markets for

Treasury securities and agency mortgage-backed securities that are

central to the flow of credit to households and businesses, over coming

months the Committee will increase its holdings of Treasury securities

by at least $500 billion and its holdings of agency mortgage-backed

securities by at least $200 billion. The Committee will also reinvest

all principal payments from the Federal Reserve’s holdings of agency

debt and agency mortgage-backed securities in agency mortgage-backed

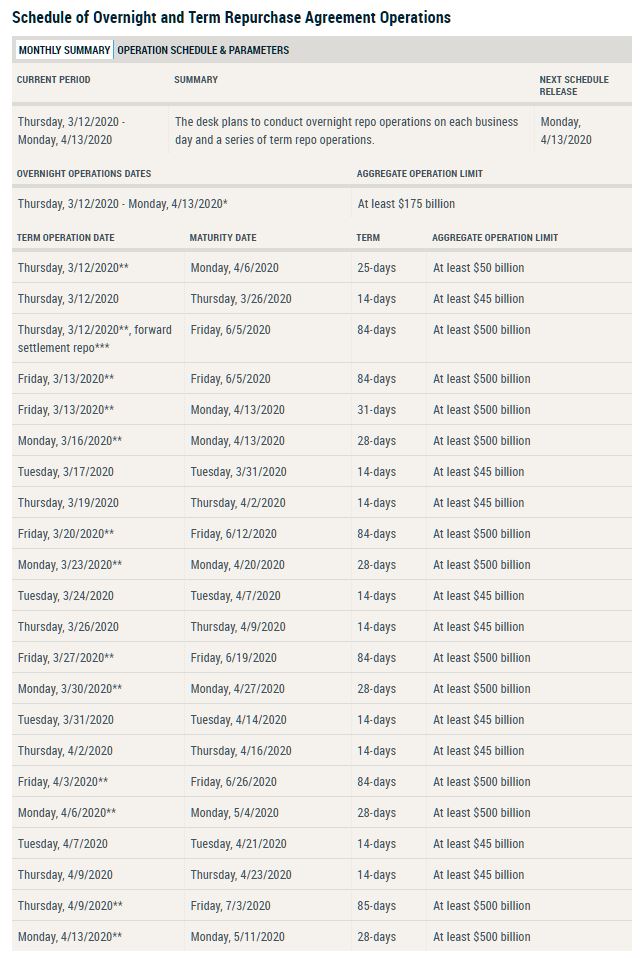

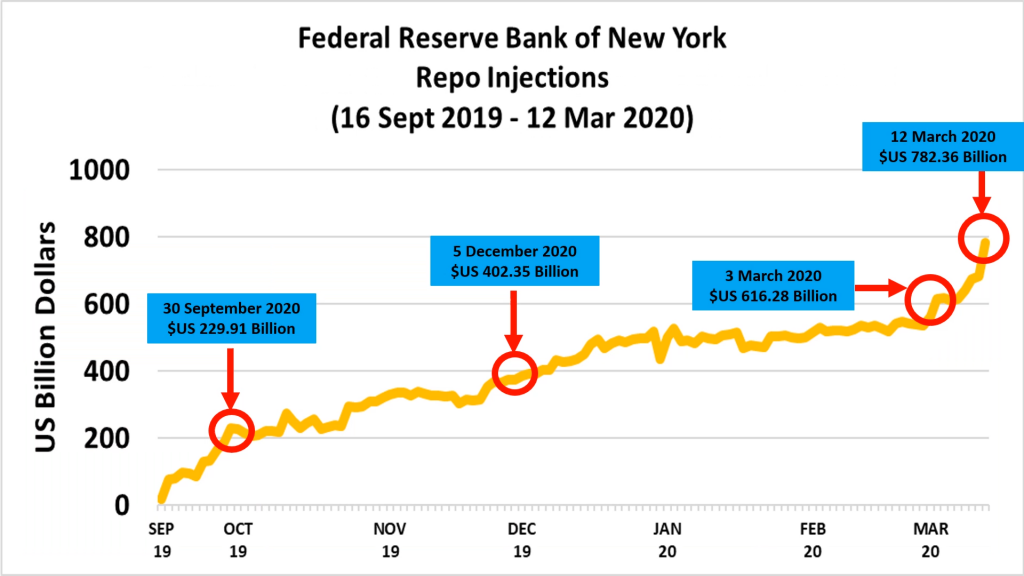

securities. In addition, the Open Market Desk has recently expanded its

overnight and term repurchase agreement operations. The Committee will

continue to closely monitor market conditions and is prepared to adjust

its plans as appropriate.

Voting for the monetary policy action were

Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michelle W.

Bowman; Lael Brainard; Richard H. Clarida; Patrick Harker; Robert S.

Kaplan; Neel Kashkari; and Randal K. Quarles. Voting against this action

was Loretta J. Mester, who was fully supportive of all of the actions

taken to promote the smooth functioning of markets and the flow of

credit to households and businesses but preferred to reduce the target

range for the federal funds rate to 1/2 to 3/4 percent at this meeting.

In a related set of actions to support the

credit needs of households and businesses, the Federal Reserve

announced measures related to the discount window, intraday credit, bank

capital and liquidity buffers, reserve requirements, and—in

coordination with other central banks—the U.S. dollar liquidity swap

line arrangements. More information can be found on the Federal Reserve

Board’s website.

In a statement, the Reserve Bank of New Zealand says New Zealand’s financial system is sound, with strong capital and liquidity buffers, but faces significant uncertainties from the impacts of COVID-19. The Reserve Bank is announcing additional measures to support the provision of credit and market functioning.

Reserve Bank Deputy Governor

Geoff Bascand says the situation around COVID-19 is evolving rapidly, and there

is much uncertainty.

“To support credit

availability, the Bank has decided to delay the start date of increased capital requirements for banks by 12 months –

to 1 July 2021. Should conditions warrant it next year, the Reserve Bank will

consider whether further delays are necessary.”

“We are taking this action

now to help support lending in the economy at time when there is a lot of

uncertainty. The Reserve Bank’s expectation is that banks will utilise this

flexibility to maintain lending to households and businesses. Banks have

significant buffers above current regulatory minimums, and we encourage them to

use them,” Mr Bascand said.

“Deferring the capital

framework implementation provides banks with significant capital headroom. We

estimate that this headroom will enable banks to supply up to around $47

billion more lending than would have been the case, had the decisions been

implemented as planned.”

Mr Bascand said the Reserve

Bank is currently identifying other regulatory initiatives that can be deferred,

to reduce the burden on financial institutions at this time of uncertainty.

These will be announced in coming days. The Reserve Bank is working closely

with the Council of Financial Regulators and international regulators.

Assistant Governor Christian

Hawkesby said the Bank is also ensuring there is sufficient liquidity in the

financial system, through regular market operations.

“The Bank has a number of

operational tools at its disposal to support liquidity and market functioning

in New Zealand. This has helped the domestic cash market and foreign exchange

swap market to continue to function effectively over recent weeks,” Mr Hawkesby

says.

“Banks currently have robust

liquidity and funding positions and can manage short-term disruptions to

offshore funding markets. We will continue to monitor developments closely and

engage regularly with market participants to ensure we are ready to provide

support if needed.”

The Reserve Bank also

announced the following changes to the pricing of its standing facilities and

ESAS accounts, in part to assist cash market functioning at a lower OCR:

Cash that ESAS account holders have on deposit at the Reserve Bank that is in excess of their allocated ESAS credit tier will be remunerated at the OCR less 25 basis points (from OCR less 75 basis points).

Bonds lent through the Bond Lending Facility well be lent at the OCR less 50 basis points (from OCR less 75 basis points).

A maximum rate will be set for bonds lent through the Repo Facility at the OCR less 50 basis points (from OCR less 75 basis points).

Cash will continue to be lent via the Overnight Reverse Repo Facility at the OCR plus 25 basis points until further notice.

The Reserve Bank has a

number of tools to provide additional liquidity, and support to market

functioning, should these be required in the future:

The ability to provide term funding through a Term Auction Facility (TAF) which can provide collateralised loans out to 12 months. This facility was previously provided from 2008 to 2010.

The Bank has an established role to provide liquidity in the New Zealand dollar foreign exchange market in periods of illiquidity or dysfunction, and is operationally ready to undertake this role if required.

The ability to provide liquidity to the NZ government bond market to support market functioning.

Mr Hawkesby says the Reserve

Bank continues to monitor developments, and is ready to act to ensure markets

and the financial system operate in a stable and efficient manner.

The Reserve Bank New Zealand announced today that following an emergency meeting yesterday, the Official Cash Rate (OCR) is 0.25 percent, reduced from 1.0 percent, and will remain at this level for at least the next 12 months. The also signalled the likelihood of QE to follow.

The negative economic

implications of the COVID-19 virus continue to rise warranting further monetary

stimulus.

Since the outbreak of the

virus, global trade, travel, and business and consumer spending have been

curtailed significantly. Increasingly, governments internationally have imposed

a variety of restraints on people movement within and across national borders

in order to mitigate the virus transmission.

Financial market pricing has

responded to these events with declining global equity prices and increased

interest rate spreads on traditionally riskier asset classes.

The negative impact on the

New Zealand economy is, and will continue to be, significant. Demand for New

Zealand’s goods and services will be constrained, as will domestic production.

Spending and investment will be subdued for an extended period while the

responses to the COVID-19 virus evolve.

Several factors will

continue to assist and support economic activity in New Zealand.

New Zealand’s financial

system remains sound and our major financial institutions are well capitalised

and liquid. The Reserve Bank is also ensuring that the banking system continues

to function normally.

The Government is operating

an expansionary fiscal policy and has imminent intentions to increase its

support with a fiscal package to provide both targeted and broad-based economic

stimulus.

The New Zealand dollar

exchange rate has also depreciated against our trading partners acting as a

partial buffer for export earnings.

And, the Monetary Policy

Committee agreed to provide further support with the OCR now at 0.25 percent.

The Committee agreed unanimously to keep the OCR at this level for at least 12

months.

The Committee also agreed that should further stimulus be required, a Large Scale Asset Purchase programme of New Zealand government bonds would be preferable to further OCR reductions.

The members discussed the broad range of Official Cash Rate (OCR)

settings that would be suitable. Staff briefed the Committee on the scale of

policy stimulus required given deteriorating global conditions and the impact

of travel restrictions. The Committee discussed the relative contributions of

planned fiscal and financial stability measures in consideration of the

monetary policy response. Staff also advised that an OCR of 0.25 percent was

currently the lower limit, given the operational readiness of the financial

system for very low or negative interest rates.

Subsequent Committee

discussion focused on two scenarios:

a 0.5 percentage point cut in the OCR to 0.5 percent, followed by an assessment of the rapidly developing COVID-19 situation, with the ability to follow up with more stimulus as needed at the scheduled March OCR review

A 0.75 percentage point reduction in the OCR to 0.25 percent.

Members noted that lower

interest rates would likely support the soundness of the financial system – in

the context of the Committee’s Remit.

Given views on the required

level of stimulus given the economic impact of COVID-19, the committee agreed a

0.75 percentage point reduction in the OCR would be a more suitable option.

To address temporary disruptions

in the market for Treasury securities, the Open Market Trading Desk

(the Desk) at the Federal Reserve Bank of New York has updated the

current monthly schedule of Treasury purchase operations.

Today, the Desk will conduct purchases

in each of five maturity sectors below at the times indicated, subject

to reasonable prices.

20 to 30 year sector at 10:30 – 10:45 am and 2:15 to 2:45 pm for around $4 billion each

7 to 20 year sector at 11:15 – 11:30 am for around $5 billion

4.5 to 7 year sector at 12:00 – 12:15 pm for around $8 billion

2.25 to 4.5 year sector at 12:45 – 1:00 pm for around $8 billion

0 to 2.25 year sector at 1:30 – 1:45 pm for around $8 billion

These purchases are intended to address highly unusual disruptions in the market for Treasury securities associated with the coronavirus outbreak. These purchases are part of the $80 billion of planned monthly purchases, including both $60 billion of reserve management purchases and $20 billion of reinvestments of principal payments received from the Federal Reserve’s holdings of agency debt and agency mortgage-backed securities. In these purchases, the Desk will include securities that are cheapest to deliver into active Treasury futures contracts as eligible securities for purchase. The Desk intends to further bring forward remaining purchases for this monthly calendar and adjust terms of operations as needed to foster smooth Treasury market functioning and efficient and effective policy implementation. A revised schedule will be posted.

In order to support the continuous functioning of financial markets through the provision of liquidity, the Bank of Canada announced two measures on Thursday.

First, acting as fiscal agent, the Bank

will broaden the scope of the current Government of Canada bond buyback

program. This is intended to add market liquidity and support price

discovery. Until further notice, buybacks will extend across all

benchmark maturity sectors and will be conducted at least weekly.

Regular weekly operations will be conducted on a switch basis. Cash

buybacks will be conducted following nominal bond auctions.

The first operation will be a $500 million

switch operation in the 30-year sector held on Monday March 16.

Additional program details are forthcoming, including the timing of the

first operation.

Second, to proactively support interbank

funding, the Bank of Canada will temporarily add new Term Repo

operations with terms of 6 and 12 months. These operations will occur

bi-weekly starting with the first operation on Tuesday, 17 March 2020.

Details of the first Term Repo operation are as follows:

Amount

Auction Date

Settlement Date

Term (Days)

Maturity Date

$4 billion

17 March 2020

19 March 2020

168

3 September 2020

$3 billion

17 March 2020

19 March 2020

350

4 March 2021

Regular 1-month and 3-month Term Repo

operations will remain in effect but could change with regards to size,

frequency and term depending on prevailing market conditions.

Term Repo terms and conditions remain in effect. The results of the 6- and 12-month operations will be announced on the Bank’s web site by Market Notice.

The Bank of Canada continues to closely

monitor global market developments and remains committed to providing

liquidity as required to support the functioning of the Canadian

financial system.

Given the current market gyrations, we are going to examine the latest critical data each day, because a week is a long time in politics but a lifetime on the markets at the moment…

Digital Finance Analytics (DFA) Blog

Let's Throw Some Money About - The Property Imperative DAILY 12 March 2020 [Podcast]

Given the current market gyrations, we are going to examine the latest critical data each day, because a week is a long time in politics but a lifetime on the markets at the moment…

Blog")