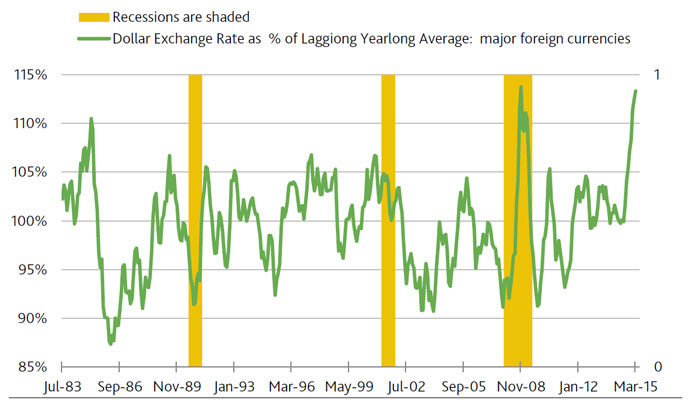

According to Moody’s, recently markets discovered that there was only a limited speculative demand for 10-year European government bonds yielding less than 1%. Unless forced to do so by an investment mandate, it’s highly unlikely that many long-term investors had been loading up on European government debt yielding less than 1%. Despite their latest climb, European government bond yields remained low compared to what otherwise might be inferred from fundamental drivers excluding European Central Bank (ECB) demand. ECB purchases have been substantial and are scheduled to be so. For example, the ECB still intends to purchase another one trillion euro of European bonds by the autumn of 2016.

Over the past week, the 10-year German government bond yield rose by 22 bp to 0.38%. In near lock step fashion, the 10-year US Treasury yield increased by 19 bp to 2.10%. The unexpected rise by Treasury bond yields helped to trigger an accompanying 0.9% drop by the market value of US common stock.

We still hold that the forthcoming upswing by US bond yields will more closely resemble a mild rise, as opposed to a jarring lift-off. Though financial markets are likely to overreact to the first convincing hint of a higher fed funds rate, the record shows that the market value of US common stock does not peak until several years after the initial rate hike. Yes, payrolls are growing, but the quality of new jobs may be lacking, according to the subpar growth of employee compensation and below-trend income expectations. Thus, the reaction of household expenditures, including home sales, to the expansion of payrolls and still extraordinarily low mortgage yields falls considerably short of what occurred during previous business cycle upturns. In turn, the upside for Treasury bond yields is limited. The 10-year US Treasury yield is likely to spend 2015’s final quarter in a range that is no greater than 2.25% to 2.50%.

When the federal funds rate target was first lowered to its current range of 0.00% to 0.25% in December 2008, nobody dared to predict that this record low target would hold well into 2015. Few, if any, appreciated the extent to which the drivers of expenditures growth had been weakened not only by a diminution of business and household credit quality, but also by heightened global competition and an aging population. Three overlapping and unprecedented episodes of quantitative easing have made the length of the nearly 6.5year stay by the Fed’s zero interest rate policy all the more remarkable. Neither the Fed’s $3.8 trillion net purchase of bonds since mid-2008 nor roughly $800 billion of fiscal stimulus was able to spur expenditures by enough to allow for the removal of an ultra-low fed funds rate target.

In stark contrast, fed funds’ previous bottom of 1% in 2003-2004 lasted for only 12 months. And when fed funds troughed at the 3% during late 1992 into early 1994, its duration was slightly longer at 17 months. The US economy’s decidedly positive response to each earlier bottoming of fed funds helps to explain their much shorter durations.Long-term growth slows markedly

Amazingly, despite humongous monetary stimulus, as well as considerable fiscal stimulus, the moving yearlong sum of real GDP has grown by only 2.2% annualized since the Great Recession ended in June 2009. For comparably measured serial comparisons, 23 quarters following the expiry of the three downturns prior to the Great Recession, the average annualized rates of real GDP growth were 2.9% as of Q3-2007, 3.4% as of Q4-1996, and 4.8% as of Q3-1988. The downshifting of the average annual rate of growth by the 23rd quarter of an upturn lends credibility to the secular deceleration argument. If there is any good news it may be that the prolonged deceleration of US economic growth may be bottoming out. That being said, Q1-2015’s lower than expected estimate of real GDP increases the likelihood that 2015 will be the 10th straight year for which the annual rate of US economic growth failed to reach 3%. Such a stretch lacks recent precedent.

US real GDP will probably average a 1.5% annualized increase during the 10-years-ended 2015. Previous 10year average annualized rates of real GDP growth averaged 3.4% as of 2005, 3.0% as of 1995, and 3.5% as of 1985. Beginning and concluding with the spans-ended 1957 through 2007, the 10-year average annualized rate of real GDP growth averaged 3.4%. Most baby boomers will not live long enough to observe another average annual growth rate of at least 3% over a 10-year span.

Corporate credit heeds the diminished efficacy of stimulus

The corporate credit market is well aware of how so much monetary and fiscal stimulus supplied so little lift to business activity. In turn, credit spreads are wider than otherwise given a benign default outlook, partly because of a loss of confidence in the ability of policy actions to quickly spur expenditures out of a macroeconomic slump. In the event an adverse shock rattles the US economy, just how effective would additional monetary stimulus be at reviving growth?

Moreover, a still elevated ratio of US government debt to GDP might delay the implementation of fiscal policy by a Congress that remains skeptical of the effectiveness of increased government spending and a Presidency that is adverse to tax cuts. Also, even if Washington were to agree on fiscal stimulus, foreign investors, who now hold 47% of outstanding US Treasury debt, may be unwilling to take on more obligations of the US government unless compensated in the form of higher US Treasury bond yields. In all likelihood, an accompanying rise by private-sector borrowing costs would reduce the lift supplied by fiscal stimulus.