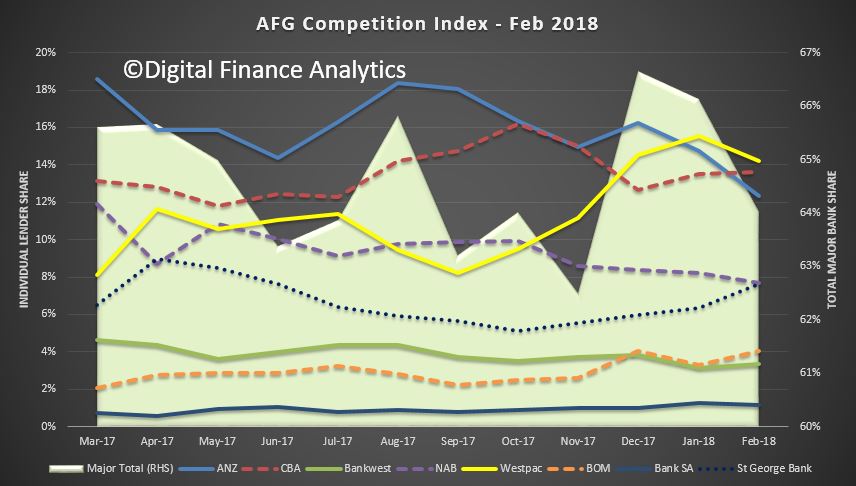

AFG has released their latest Competition index, based on flows through their systems. Myopic it may be, but it does give us another reference point on the market. Major bank share of new loans drifted lower, but also with significant shifts between lenders. The non-majors’ market share is now at 35.97%

AFG General Manager Broker & Residential, Mark Hewitt explained the results: “The gap between the first placed major lender, Westpac at 14.21% of the market and third placed ANZ at 12.32%, is the closest it has been for some time.

“As AFG has stated many times, a consumer dealing directly with a lender has limited negotiating power or knowledge of the interest rates and lending criteria offered by competitors. This has been further validated by the findings of the interim ACCC Residential Mortgage Price Inquiry. The presence of the mortgage broking channel is one of the few drivers of competitive tension in the Australian lending market.

“Whilst the majors’ market share lifted a couple of percentage points across the quarter, rising from 62.51% in November 2017 to 64.03% at the end of February, three of the four majors went backwards.

“ANZ dropped from 14.93% in November 2017 to 12.32% at the close of the last quarter. CBA’s share of the market dropped from 14.99% to 13.63%, and their subsidiary Bankwest dropped from 3.74% to 3.35%. NAB also recorded a drop, from 8.57% in November 2017 to finish the last quarter at 7.67% of the market.

“Only the Westpac group of brands, Westpac, St George, Bank of Melbourne and BankSA grew, with their market share lifting from 20.28% in November 2017 to 27.05% at the close of the last quarter,” he said.

“Interestingly, the Westpac group’s major gain came in the area of fixed rate loans with their share of that product type increasing from 23.63% to 44.24% of the market.

In a sign the majors are again open for business for investors, their share of that segment of the market has lifted from 64.82% in November 2017 to finish February at 66.78%.

The non-majors’ market share is now at 35.97%. “Amongst the non-majors AMP recorded an increase in market share and lifted from 2.27% to 4.62% and Homeloans recorded an increase from 0.14% to 0.33%.

With the royal commission’s first round of hearings now over, industry leaders have taken a step back to assess what happened and how the latest revelations will impact the third-party channel.

The commission covered a lot of ground over the last two weeks examining the banks and their dealings in the home loans sector, and brokers are a big part of that. The commission identified issues with how household expenses are verified, questioned CBA about its broker accreditation process, scrutinised upfront and trail, and zeroed in on Aussie Home Loans for broker misconduct.

There’s no doubt that brokers will be included in the interim report due by the end of September. So what should brokers know and takeaway from what just happened?

Higher expectations for living expenses and trail

Connective’s group legal counsel, Daniel Oh, said living expenses and how they’re verified will be heavily scrutinised following the royal commission’s examination of ANZ. During that hearing, it was revealed that ANZ failed to follow processes to verify customers’ financial situations. Stating living expenses at or below HEM can no longer be a mechanical process on loan applications, he said.

“You need to ensure that you have done the work to verify and have the necessary evidence to support this figure. If the figure is at or below HEM, expect greater scrutiny,” Oh said.

On trail, Oh expects that at a minimum there will be more scrutiny as to what brokers do post-settlement to justify their earnings.

“Our position on the topic is that you should speak or meet your existing clients at least once a year, if not more, to ensure that client’s needs continue to be met.”

Customer at the centre of everything

William Lockett, managing director of Specialist Finance Group, said the most important takeaway from the royal commission is to always ensure that the customer and their needs are the sole focus of the bank, financial planner or finance broker.

Banks and brokers need to work more constructively together to ensure they are achieving the best outcome for the consumer, he said.

But he also said both need to fess up if they’re at fault. “Banks also need to take sole responsibility for their own failings and shortfalls and likewise finance brokers need to do the same.”

Both groups also need to embark on a mission to restore trust with customers.

“All parties within the financial services industry should continue to look at improving their business model and how they engage with all other parties and ultimately the consumer,” he said.

Accountability and transparency need to be restored

Peter White, executive director of the FBAA, said the banks need to be completely transparent about the issues being revealed at the royal commission and then put positive actions in place to remedy them.

“It doesn’t matter how big you are or how well recognised your brand is, you are accountable for your actions every single time.”

“Also as much as there are issues on our own doorstep, the banks need to make some serious cultural and process changes and ensure those who should be are held very much accountable,” White said.

What’s next for brokers and banks?

Influenced by the quest for ever greater profits, cultural norms in banking have strayed too far from good customer outcomes, and as a result, some households are in strife, said Martin North, principal at Digital Finance Analytics.

The royal commission has and will continue to examine the root causes of this— some of which have been known for a long time— but North said it seems “we need considerable changes”.

“I also feel that the role of brokers will change on the back of this – still a role for them – but on a different basis. Also it raises questions about vertical integration.”

North believes there is still more to come out, and that the focus will be on the cultural practices and remuneration models of the executives in these banks.

“There has been a credit fest, and it’s time for this to be normalised. Regulators were also asleep at the wheel and only reactive to events as they appeared. No one is the customer’s champion – that’s what we need.”

During the royal commission’s last two weeks of public hearings into the consumer and home lending space, the banks have regularly pointed the finger at mortgage brokers over such things as trail commissions leading to poor consumer outcomes and poorly verified expenses in customers’ loan applications.

Not only did this look bad for brokers, but it also demonstrated the gaps in bank executives’ knowledge of what their banks have or still do, and forced them to confront how they have— or have failed— to deal with those breaches. Overall, it revealed a major lack of transparency among the banks, which brokers were inevitably linked.

How did banks and brokers fare?

William Lockett, managing director of Specialist Finance Group, said brokers were perceived by the banks as an “easy target” to take the heat and blame off their own conduct, particularly in a forum where brokers had no way of defending themselves.

“Given that the banks ultimately have the one and only say when approving any loan application, loan size and purpose of the loan, yet the banks still unfairly attack finance brokers at most given opportunities,” he said.

Tanya Sale, CEO of Outsource Financial, said it was frustrating that the facts about the industry didn’t surface to the top.

“Our industry has just been through two years of working with our regulator ASIC to provide them with all the information and data they required to understand our complex industry. One gets tired of reading and listening to ill-informed critics who clearly have not done their homework and are only looking for sensationalism,” she said.

Martin North, principal at Digital Finance Analytics, a research and consulting firm covering the financial services sector, said the major impact for brokers was that the royal commission highlighted “the inherent conflicts based on the remuneration model”. The commission made a strong case for a fee-for-service model and a switch to the ‘best interest’ legal duty from ‘not unsuitable’, which could significantly alter the current broking landscape.

But North said the banks fared even worse than brokers.

“They were criticised for not providing all the information required by the royal commission, relying on brokers to satisfy their responsible lending obligations, and in some cases ignoring expenditure information, and relying on HEM, a poor substitute for real analysis. As a result, we can certainly conclude that there have been loans written which should not have been written.”

So what now?

Executive director of the FBAAPeter White said brokers need to take careful note of how these matters could play out when the commission formalises its position to government in its interim report, which is expected no later than 30 September.

In the meantime, brokers must ensure they are looking after their clients with ongoing support and annual reviews of facilities to ensure these are still appropriate for the client’s circumstances, which is why trail is paid, White said.

Fraud is another issue that needs to be addressed with zero tolerance.

“We must work even harder to see this eradicated from our industry and those minority that do not accurately or fraudulently construct applications need to be, at a minimal level, permanently removed from our industry and the full recourse of the law applied,” he said.

While most headlines focused on the royal commission, two other significant things occurred over the last two weeks, AFG’s CEO David Bailey pointed out.

The ACCC released its interim report revealing the lack of transparency around how the big banks set interest rates on mortgage products and APRA revealed the closure of 100 bank branches over the last 12 months.

Bailey said these matters raise two questions: Without a broker helping their client to navigate the more than 3,800 offerings in the marketplace, how are they expected to get the right product? And if the proprietary channel is an efficient means of origination, why are branches being shut down?

“It is important that any proposed changes to the structure of our industry should not result in an economic drift away from the broker to the lender,” he said.

“Devaluing the service provided by brokers would have significant and long term detrimental effects for consumers by lessening the competitive tensions that currently exist in the credit industry. It is essential that anticompetitive conduct is not permitted to proliferate under the guise of regulatory reform.”

The first round of hearings at the Royal Commission into Financial Services Misconduct closed out after two weeks of frankly amazing evidence. Their live streaming of the hearings was well worth watching. Of the 2,386 submissions received so far 69% related to banking alone!

The case study approach looked at issues across residential mortgages, car finance, credit cards, add-on insurance products, credit offers and account administration. We discuss the findings so far. Watch the video or read the transcript.

The litany of potential breaches of both the law, company policy and regulatory guides were pretty relentless, with evidence from various bank customers as well as representatives from ANZ, CBA, NAB and Westpac, plus others. It looks to me as if many of these breaches will possibly force the banks to pay sizeable remediation costs and penalties. Weirdly, NAB who was first up, probably came out the least damaged, despite the focus on their Introducer program. Their own whistleblower programme brought the issues of fraud inside the bank and beyond to light.

Some of the other players were clearly caught out trying to avoid scrutiny, and seeking to bend the rules systematically to maximise profitability, despite the severe impact on customers. They also tried to blame systems, or brokers, or executional issues. It was pretty damming. We should expect extra remediation costs and even fines together with a heightened risk of further individual or group actions. It is not over yet.

A number of industry practices will be changed, centred on responsible lending, including a further tightening of lending standards and so credit will be harder to get – this will continue to drive credit growth, especially for housing, lower still.

In the final session, in addition to legal breaches, there was also discussion of what conduct below community standards and expectations might mean. The case study approach brought the issues to the fore.

Specific areas included mortgage broking where we think it is likely remuneration models will change, with a focus on fees rather than commissions, and this will shake up the industry. Insiders are already saying this could reduce competition, but we do not agree. Also take note that the banks tended to blame the brokers and aggregators, but they ALL have responsible lending obligations, and they cannot outsource them.

If there is a move towards meeting customer best interest as opposed to not unsuitable, this could lead to a consolidation of brokers and financial planners, something which makes sense, in that a mortgage, or wealth building is part of the same continuum, and credit is not somehow other – the two regimes are an accident of history because the credit laws evolved separately from individual state laws. They should be merged, in the best interests of customers.

But now to those unknown unknowns. I do not think the poor behaviour resides only in the large players which were examined. Arguably, it is endemic across smaller banks and non-banks too. In fact, many smaller players are very active broker users. This means that the proportion of loans held by customers which are unsuitable is considerable. We must not let this become a big bank, or broker bashing exercise. We need structural and comprehensive reform across the board.

Next we need to remember that half of all loans are originated in the banks themselves, and the same underwriting weaknesses are sure to reside there too – the banks will try to deflect attention beyond their boundaries, but they need to look inside too (and evidence suggests they prefer to look away!). Have no doubt, liar loans are found in loans written by bankers themselves. But the case studies in this sector are harder to find, for obvious reasons.

The same drivers are also apparent in the growing non-bank sector, where regulation is weaker. We need to look there too – including the car loans, and pay day loans, plus the strong growth in interest only mortgages by some players. APRA only now has new powers of oversight, but they are still pretty weak.

At its heart we need to rebalance the cultural norms in finance from profit at all costs, to serving the customer at all costs. The fact is, do that, put the customer first, and profitability follows. We discussed this in our recent Customer Owned Banking post.

Now, recalling the terms of reference of the Royal Commission, they will need to look beyond bank practice to think about completion, access to banking services and even the broader impact on the economy.

As we have argued, credit growth has been the engine of GDP growth, – the RBA has used this growth in credit to drive household consumption to replace mining investment. As lending practices are progressively tightened this has the potential to slow growth significantly at a time when rates are rising. We expect the rate of slowing to speed up ahead. I also think the confused roles of the regulators – ACCC, APRA, ASIC, RBA and The Council of Financial Regulators, where they all sit round the table (minus the ACCC) with The Treasury – are partly to blame. As the recent Productivity Commission review called out there needs to be change here too. But that is probably beyond the Commissions ambit, for now.

The bottom line is this, the economic outfall of the Royal Commission, even based on just round one will be significant. Credit growth may well slow. Bank share valuations will be hit (they have already fallen) and as the size of the costs of remediation emerge, this could get worse. But lending practices will not get fixed anytime soon. There is a long reform journey ahead.

And in three weeks, we are back, this time looking at financial planning and wealth management, the $2 trillion plus sector.

A senior manager of the Commonwealth Bank (CBA) has admitted that upfront and trailing commissions for mortgage brokers can lead to poor customer outcomes, as reported in the Australian Broker.

During his 15 March testimony before the Royal Commission, executive general manager of home buying Daniel Huggins said the commission structure is linked to the size of the loan. The longer loan takes to pay off, the larger the trailing commission will be. “[T]hat can lead to a conflict – well, there is a conflict between – between the customer, you know, and – and the broker,” he added.

Huggins confirmed to Senior Counsel Assisting Rowena Orr that brokers can maximise their income by getting the largest possible loan approved to extend over the longest period of time for the customer to repay.

The bank knew about this as early as February 2017, according to a confidential letter by outgoing CBA CEO Ian Narev to Stephen Sedgwick, who was the independent reviewer for the Retail Banking Remuneration Review back then. Orr presented the confidential letter during the hearing.

“We agree with the reviewer’s observations that while brokers provide a service that many potential mortgagees value, the use of loan size linked with upfront and trailing commissions for third parties can potentially lead to poor customer outcomes,” said Narev in the letter.

“We would support elevated controls and measures on incentives relates to mortgages that are consistent with their importance and the nature of the guidance that is provided,” Narev added. These initiatives include delinking of incentives from the value of the loan across the industry, and the potential extension of regulations such as future and financial advice to mortgages in retail banking.

Another CBA submission attached to Narev’s letter said that broker loans are reliably associated with higher leverage compared to those applied through proprietary channels. “[E]ven for customers with an identical estimate of ex ante risk, loans through the broker channel have higher leverage… [and] loans written through the broker channel have a higher incidents of interest only repayments,” it added.

Huggins agreed with Orr that CBA’s submission lends some support to the case for discontinuing the practice of volume-based commissions for third parties. But he said there are a range of considerations that the bank would have to make.

“There is a first mover problem, in that the person who moved first would likely lose a lot of volume. The second problem is you create a conflict if one person, or half of the people move, and the other half don’t,” Huggins said.

According to Huggins, CBA has not stopped paying volume based commissions to brokers. He also confirmed the lender has not taken any steps towards ceasing its practice.

AFG, a major Mortgage Broker Aggregator says that introducing fees for service would cause a “major disruption” in the finance industry, be a “clear disincentive” for borrowers to use brokers and “further entrench the oligopoly powers of the major banks”, in a response to the Productivity Commission, as reported by The Adviser.

In its response to the Productivity Commission’s (PC) draft report into competition in the Australian financial system, the Australian Finance Group (AFG) responded to the call for more information on the effect of replacing broker commissions with a fee-for-service model.

The group pulled no punches in warning that the introduction of such a model would “provide a clear disincentive for consumers to use brokers and would inevitably cause a major disruption in the finance industry”.

“The four major banks would be the only beneficiaries of a change of this kind as they would gain an additional competitive advantage over competing lenders that do not have extensive direct distribution channels,” the broking group said.

“This would further entrench the oligopoly powers of the major banks, which, coupled with the commission’s observations concerning the regulatory advantage of D-SIBs, ha[s] a negative impact on competition in the finance sector and [will] lead to a loss of the pricing benefits that resulted from the development of the mortgage broking industry.”

AFG also predicted that should such a change occur, it would not necessarily mean that any savings would be passed on (i.e. that loans would be repriced or that consumers would save money), as banks would have to distribute their products and would have additional costs (including increased staffing) “to deal with direct applications that have not been professionally compiled and pre-assessed by a broker to meet the lender’s requirements”.

“It is AFG’s contention that the presence of the mortgage broking channel is one of the few drivers of competitive tension in the Australian lending market,” the response reads.

“A consumer dealing directly with a lender has limited negotiating power or knowledge of the interest rates and lending criteria offered by competitors. A mortgage broker with access to a panel of lenders drives competition between lenders to the benefit of all consumers, not just their own clients.”

Touching on trail, AFG said that it “strongly supports” the removal of trail that increases over time, but that it does not agree that the standard trail commission operate as a disincentive to switching.

It said: “When a broker assists a consumer to refinance, trail commissions that cease with respect to the repaid loan will be replaced with the trail commissions payable on the new loan. As a result, it is AFG’s view that, in the absence of increasing trail commission rates over time, trail commissions per se are not likely to have a negative impact on broker behaviour.”

It concluded: “It is important that any changes should not result in an economic drift away from the broker to the lender, as devaluing the service provided by brokers would have significant and long-term detrimental effects for consumers by lessening the competitive tensions that currently exist in the credit industry.

“It is essential that anticompetitive conduct is not permitted to proliferate under the guise of regulatory reform.”

Best interests duty

In regard to the PC’s suggestion that a duty of care be implemented on lender-owned aggregators to act in the consumer’s best interests, AFG said that it was “very concerned” about introducing a test that would be applied to only one section of the industry “as it is likely to result in market distortions and unintended consequences”.

For example, it suggested that lender-owned aggregators could suggest that consumers are at risk if they use a broker that is not subject to the same test (and assert that the safest course for consumers is to only use brokers that are subject to the additional “best interests duty”).

Noting that the Combined Industry Forum has been working on a reform package, AFG added that “before considering additional law reform proposals, sufficient time must be allowed for those proposals to be implemented and embedded into the processes, procedures and culture of individual broker businesses”.

“Once that has occurred, it will be an appropriate time to again review the extent to which community expectations are met and good consumer outcomes are achieved,” the group said.

Lack of data on costs “disingenuous”

Noting that the commission found it difficult to ascertain from lenders the costs and benefits of using brokers rather than branches to source home loans, AFG said that the lack of information from lenders “should be considered to be disingenuous”.

“It is difficult to accept that entities that are sophisticated enough to develop and manage banking products and meet complex legal and regulatory obligations do not have information about product costs that would be needed to price those products,” the group said.

“However, absent a willingness to publicise that information, AFG submits that the willingness of lenders to embrace broker distribution should be considered reasonably reliable evidence that brokers provide an efficient and cost-effective means of distributing lending products.”

It added: “Brokers provide a variable cost base for lenders, with payment only required when a loan is settled and while it remains undischarged and not in default. This means that the risk of non-completion by a prospective borrower is substantially borne by the broker. As a result, lenders using broker distribution (as opposed to fixed-cost branch networks) can more easily price loans in a way to ensure that they are profitable.”

AFG also outlines that it believes ASIC should be responsible for advancing competition in the financial system, that consumers would receive “an inferior standard of service” should financial advisers also offer credit advice, and that ASIC could produce a best practice guide on disclosure requirements.

NAB, the owner of three of the larger mortgage aggregators, says Broker-originated loans are refinanced at “more than double” the rate of direct-channel loans in its new submission to the Productivity Commission; reports The Adviser.

In its second submission to the Productivity Commission (PC), released on Wednesday (21 March), the National Australia Bank (NAB) stated that it has found “no evidence” which suggests that the payment of trail commission has limited “switching” for broker-originated loans.

The big four bank responded to draft finding 13.1 of the PC’s draft report, which alleged: “The payment of trail commissions creates perverse incentives for brokers by rewarding them for keeping customers in their existing loan. Broker loyalty appears skewed towards the institution, not the customer, and thus likely discourages refinancing.”

In its submission, NAB noted that in the 2017 financial year (FY17), switching was more prevalent among borrowers with broker-originated loans.

“NAB has no evidence that incidence of switching is lower for mortgage broker-originated borrowers compared to those originated via direct channels,” the submission reads.

“In fact, refinance out rates for NAB’s mortgage broker-originated loans was more than double the rate of direct channels in FY17.”

The submission echoed the views put forward by NAB COO Anthony Cahill in his address to the PC on 5 March, stating that brokers are, in fact, rewarded for refinancing a client’s loan.

“[If] a broker were to assist a customer to move the loan to another lender, they would cease receiving a trail commission from the incumbent, but earn upfront and trail commission from the new lender.”

Further, the bank reiterated its view that trail commissions are paid as an incentive for brokers to “service customers on an ongoing basis” (which PC chair Peter Harris has questioned recently).

NAB highlighted the work the Combined Industry Forum was doing to improve commission structures and raise standards.

NAB concerned over “best interests duty”

The PC has also suggested that the Australian Securities and Investments Commission (ASIC) could impose a legal duty of care obligation on brokers and called for increased broker disclosure requirements.

In its submission, NAB said that a best interests duty “may be difficult to achieve practically” as “both mortgage products and customers themselves are not homogeneous and price is not the sole determinate of a good customer outcome”.

NAB added that it was “concerned” that applying a legal best interests duty only to brokers operating under lender-owned aggregators would create an “uneven playing field”.

The bank reiterated that bringing in a fee for service would be “detrimental to competition in the mortgage market” as it would see brokers “become unaffordable for customers”.

NAB also pointed out that proposals have already been put forward by the Combined Industry Forum (CIF) to improve broker and aggregator transparency.

The major bank also said that it does not believe the publication of median interest rates would benefit consumers, as it would “create unreasonable expectations, whereby all consumers anticipate receiving an interest rate at or below the median”.

“There are legitimate, risk-based reasons for customers to receive a price that is above a median rate; for example, high-risk loans require significantly more capital compared with low-risk loans, necessitating a different price strategy,” the major bank said.

ABC Radio National Breakfast did a segment on Mortgage Brokers, in the light of the Royal Commission, including DFA commentary.

A prominent finance industry expert has warned we’re witnessing the beginning of the end of the mortgage broking industry as new technology makes it easier for consumers to apply for a loan on their own.

But it’s not the only pressure facing these middlemen between lender and borrower.

The mortgage broking industry has faced intense questioning about its practices during the first round of the Banking Royal Commission, with evidence of conflicts of interest and outright fraud being brought to light.

But the sector’s hit back saying critics are seeking to disparage an entire industry made up of predominantly honest small business owners.

The chairman of the Productivity Commission has restated his concern regarding the payment of trail commission, warning that “someone is going to have to deal with this question of commission”.

Despite ASIC’s remuneration review finding that ongoing trail “usually provides an incentive to aggregators and brokers to put forward higher-quality loans where consumers are less likely to default on their obligation”, and despite several industry figures — including FBAA head Peter White, MoneyQuest managing director Michael Russell and National Australia Bank CEO Antony Cahill — giving evidence at the public hearings last month of the benefits and necessity of trail commissions, the PC’s chairman suggested that trail could instead be paid to borrowers.

Speaking at ASIC’s Annual Forum on Tuesday (20 March), Peter Harris argued that he had not been convinced that trail commission benefits customers.

He told delegates that while the commission “didn’t make a clear statement saying they’re rotten and evil”, they do believe that trail commissions are “quite odd”.

“[It] is purported to be the case that [trail commissions] are either paid by the banks in order for the broker to look after you during the period of the loan. But when we ask the banks, ‘Are there any performance standards that go with this in return for your money? Have you asked them if they’ve spoken to the customer in the last 12 months?’, the answer generally appears to be ‘no’.

“[There’s] a good chunk of money out there paying for service for which there is no performance standard, which is an interesting development. The other rationalisation is [that] it’s there to stop churn.”

However, Mr Harris stated that there was “conflicting evidence” given surrounding churn.

“In some cases, exactly the same broker representative who told us that churn wasn’t relevant [was] in a public statement, on record, saying it was exactly the reason why [brokers are] getting these payments,” the chairman said.

“Somewhere, someway, someone is going to have to deal with this question of commission.”

Remarkably, Mr Harris suggested that instead of banks paying brokers trail commission, the payment could be made direct to a borrower.

He said: “There are alternatives into the idea of a [trail] commission paid to a broker. The average $665 a year payment could be paid to the consumer not to switch loans,” Mr Harris suggested.

The commissioner noted that the final draft of the Productivity Commission’s report (due in July) is likely to address the impact that trail commission has had on competition.

“Has the revolution been captured by the establishment?”

Mr Harris also suggested that while brokers may have disrupted the mortgage market, he questioned who now held the most market power.

“The question is who’s exhibiting the market power? That is the most important issue,” Commissioner Harris said.

“There are a number of potential suspects starting from, of course, the banks themselves, but equally it is possible that mortgage brokers themselves have substantial market power in this marketplace.

“[What] are [brokers] doing today with that particular power? [I] think a number of people haven’t focused on [that] in exactly the way we would in a competition inquiry. We would say: ‘Gee, that’s interesting, these banks don’t appear to be able to push back on the brokers’.”

Commissioner Harris referred to testimony made by the major banks to the financial services royal commission and suggested that the banks’ ability to “re-determine payment arrangements in the customer’s best interests” has been diminished by the broking industry’s increased market share.

“Even the Commonwealth Bank can’t act on its own, which is an astonishing reflection of apparent market power,” Mr Harris said in reference to the bank’s appearance before the royal commission.

Mr Harris acknowledged the role that the “broker revolution” played in enhancing competition when the industry first emerged, but he questioned whether brokers still work in the best of interest of customers.

“Brokers are potentially wonderfully competitive forces. The question is, has the revolution been captured by the establishment?” the chairman said.

Mr Harris asked: “After 20 years, has this degree of change now being turned around from being a potential benefit to consumers to being potentially acting somewhat against their interest and that is clearly within scope for us — that is a competition issue.”

The Productivity Commission’s draft report was widely criticised by the broking industry, with the associations calling some of its views on broking “limited”, “amateur” and — in some cases — “nonsense”.

Mortgage brokers believe that tighter prime lending policies and changing customer needs will drive up demand for non-conforming mortgages over the next 12 months, according to new data.

A Pepper Money-commissioned survey of 948 mortgage brokers has revealed that 70 per cent expect to write more non-conforming loans in the coming year, while 66 per cent predict a decline in the number of prime loans written.

Surveyed respondents expect the demand for non-conforming loans to rise as a result of tighter prime lending criteria (22 per cent), changing customer needs (21 per cent) and changing legislation/regulations (13 per cent).

“The survey shows clearly there is a greater awareness and understanding of non-conforming loans among brokers,” Pepper Group’s Australian CEO, Mario Rehayem, said.

“Brokers and consumers no longer see non-conforming loans only for people who’ve experienced a credit event; instead they realise they are a valid alternative for consumers who are self-employed, who generate income outside of normal work scenarios, are seeking investor loans or have a high LVR.”

The CEO believes that brokers are servicing increased demand from Australians for flexible lending alternatives.

Mr Rehayem said: “With the big banks tightening their lending criteria on an almost daily basis, they are excluding a whole segment of credit-worthy ordinary Australians from accessing finance. That’s why more brokers are discovering the benefits of a flexible lender with a consistent approach to credit provision.

“We also know more Australians are working for themselves or on a part-time basis, and brokers are looking to provide their growing self-employed customer base with suitable lending options.”

Moreover, the survey found that the number of brokers who have yet to write a non-conforming loan has also reduced, falling by 6 per cent from 18 per cent in 2016 to 12 per cent in 2018.

“We know brokers who have previously written a non-conforming loan for a customer are more comfortable in recommending them in the future, that’s why we have established ourselves as a leader in broker education and the provision of tools that allow them to confidently recommend a non-conforming loan in the future,” Mr Rehayem concluded.