DFA research was featured in a number of the weekend papers, discussing the rising number of mortgage loan applications which are being rejected by lenders due to tighter lending standards, meaning that many households are unable to access the low refinance rates currently on offer.

NEARLY half of all homeowners are now shackled to their mortgage, with refinance rejections up significantly cent in less than a year as banks rattled by the royal commission drastically tighten borrowing rules.

NEARLY half of all homeowners are now shackled to their mortgage, with refinance rejections up significantly cent in less than a year as banks rattled by the royal commission drastically tighten borrowing rules.

Loan sizes are being slashed by 30 per cent, trapping many financially stressed customers including some who have been slugged with “out of cycle” interest rate rises. House hunters are also being hit by the credit crunch, with dramatic implications for property markets. The crunch stems from two big shifts in the way banks judge borrowers.

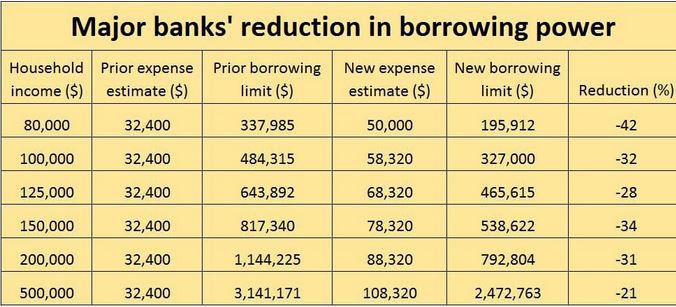

Expense estimates have been raised substantially — the minimum outgoings for an average household are now assumed to be a third higher, according to bank analysts UBS.

On top of this, granular cost breakdowns must be provided. After the royal commission revealed in March that expense checks were so lax as to be borderline illegal, new tests have been imposed requiring in some cases detail of weekly, fortnightly, monthly, quarterly and annual spending in as many as 37 categories from alcohol and haircare to shoes and pets, as well as doctor visits.

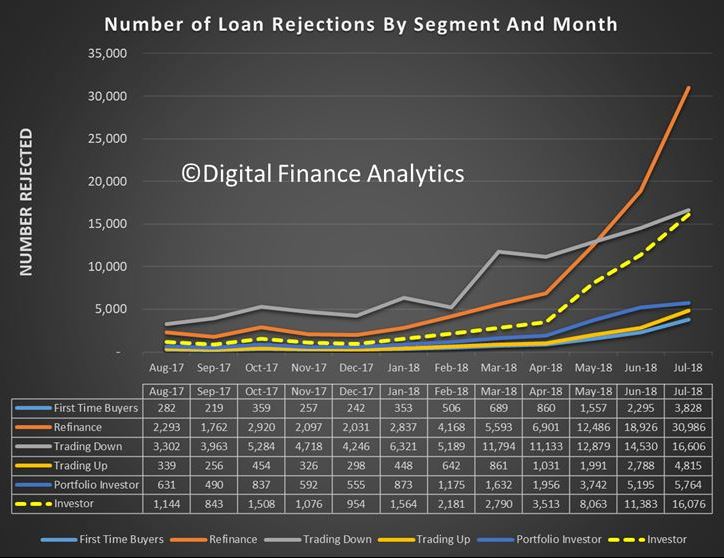

As a result, we think that now four in 10 households would now have difficulty refinancing. That means you are basically a prisoner in the loan you’ve currently go. This is based on our 52,000 household surveys plus data from a range of official sources. We estimate that 31,000 households’ refinance applications were rejected in July versus 2,300 in August last year.

As a result, we think that now four in 10 households would now have difficulty refinancing. That means you are basically a prisoner in the loan you’ve currently go. This is based on our 52,000 household surveys plus data from a range of official sources. We estimate that 31,000 households’ refinance applications were rejected in July versus 2,300 in August last year.

Comparison service Mozo’s lending expert Steve Jovcevsk said . “There’s such a huge pool of people who are in that boat.” The most common motivation among those seeking to refinance was to save money by finding a better deal. Many were feeling the pinch because living costs were rising faster than wages and rates on interest-only or investment loans had increased.

Comparison service Mozo’s lending expert Steve Jovcevsk said . “There’s such a huge pool of people who are in that boat.” The most common motivation among those seeking to refinance was to save money by finding a better deal. Many were feeling the pinch because living costs were rising faster than wages and rates on interest-only or investment loans had increased.

The main issue these households are facing in seeking a new deal was banks’ definition of a “suitable loan now is different to six months ago because of the royal commission” and a clampdown by the Australian Prudential Regulation Authority. So there has been a big rise in loan rejections, particularly refinancing.

The borrowing power of hosueholds are being crimped, as shown on the banks website mortgage calculators. Those calculators, compared to a year or 18 months ago, are now on average showing a 30 per cent lower number. For some, the reduction in borrowing power is even greater. The head of UBS’s bank analysis team Jon Mott said that for a household with pre-tax income of $80,000 would get 42 per cent less from a bank; for a $150,000-a-year household, would get 34 per cent less.

Mozo’s Mr Jovcevski said in one example he was personally aware of, a person pre-approved to borrow $630,000 last year was recently offered just $480,000. The would-be borrower’s job and income hadn’t changed.

Mozo’s Mr Jovcevski said in one example he was personally aware of, a person pre-approved to borrow $630,000 last year was recently offered just $480,000. The would-be borrower’s job and income hadn’t changed.

The implications for property markets were severe, Mr Jovcevski said. “There are fewer qualified buyers,” Reduced borrowing power would drag down selling prices and eventually cut valuations.

“It’s a double whammy for those mortgage prisoners,” Mr Jovcevski said. “Their valuations come in lower so their equity may end up being less than 20 per cents so they have to pay lenders mortgage insurance again” if they refinance.

Australian Banking Association CEO Anna Bligh said banks had to make reasonable inquiries to satisfy APRA’s strengthened mortgage lending standards but she said the term ‘home loan prisoners’ does not represent the facts of a fiercely competitive home loan market where everyday banks are seeking to attract new customers.

Mozo’ Jovcevski said homeowners seeking to give themselves the best chance of successfully refinancing should reduce their expenses in the months prior to applying and ensure all bills have been paid on time.

Mark Hewitt — general manager of broker and residential at AFG which arranges 10,000 home loans a month — said would-be borrowers whose budgets were at breaking point or beyond could still get a loan if they had equity, a clean repayments history and the ability to ditch key expenses such as fees for private school if under the pump.

Some people seeking their first home loan are signing documents in which they promise to cut their spending if a new loan is approved.

“When you get a mortgage you make sacrifices — you continue some of your discretionary spending but not all of it,” said Brett Spencer, head of Opica Group, which sells software to brokers that works out how much a prospective customer can cut back.

A figure is agreed between the broker and the would-be borrower which is then provided to the bank, which would otherwise rely on the higher, raw expense figures.

This makes in interesting point, mortgage brokers will be diving into household expenses more than ever before, but of course, household saying they will cut their expenses to get a loan is not the same a clear cash flow.

Thus even in this tighter market, the industry is still trying to find ways to bend the affordability rules. And it’s worth remembering that according to the latest figures from APRA more than 5% of new loans currently being written are outside standard assessment criteria.

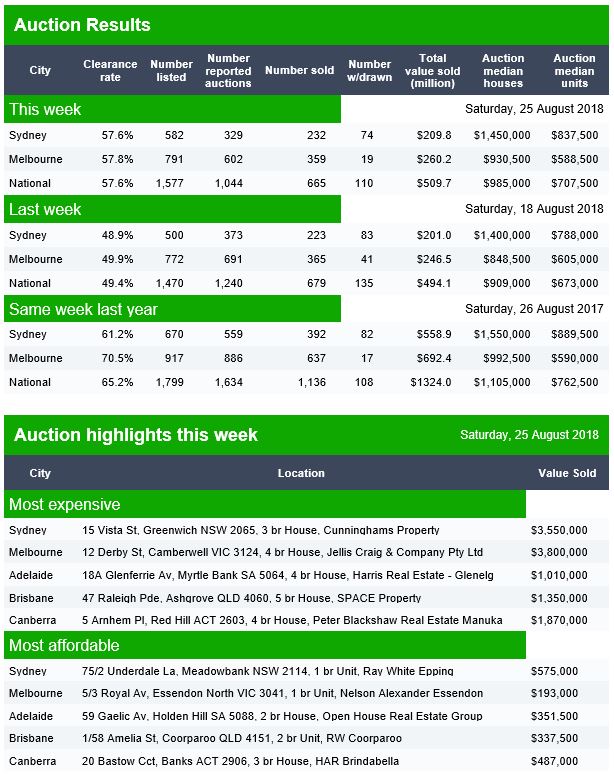

This suggests that even now; bank lending standards are still too lose. All this points to more home prices falls ahead. This is reinforced by the latest Domain auction clearance rate data which was released yesterday, and shows that the final auction clearance rate last week in Sydney, Melbourne and Nationally ended up below 50% way lower on both volume and clearance rates than a year ago.

This suggests that even now; bank lending standards are still too lose. All this points to more home prices falls ahead. This is reinforced by the latest Domain auction clearance rate data which was released yesterday, and shows that the final auction clearance rate last week in Sydney, Melbourne and Nationally ended up below 50% way lower on both volume and clearance rates than a year ago.

Yet despite all this, some are still sprooking the market, saying it’s a great time to buy. We do not agree.

Yet despite all this, some are still sprooking the market, saying it’s a great time to buy. We do not agree.