AFG has released their mortgage index today including Q3 2017. The overall volume of lodgements fell again, though volumes are still higher than last year at this time.

This data provides additional insights into the market, with the caveat, it reflects transactions via the AFG channel only.

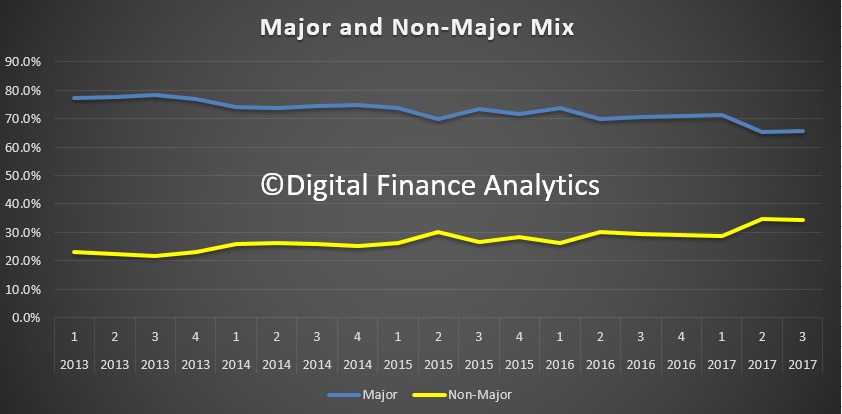

The mix between majors and non-majors remained similar to last quarter, when the non-majors share grew a little.

The mix between majors and non-majors remained similar to last quarter, when the non-majors share grew a little.

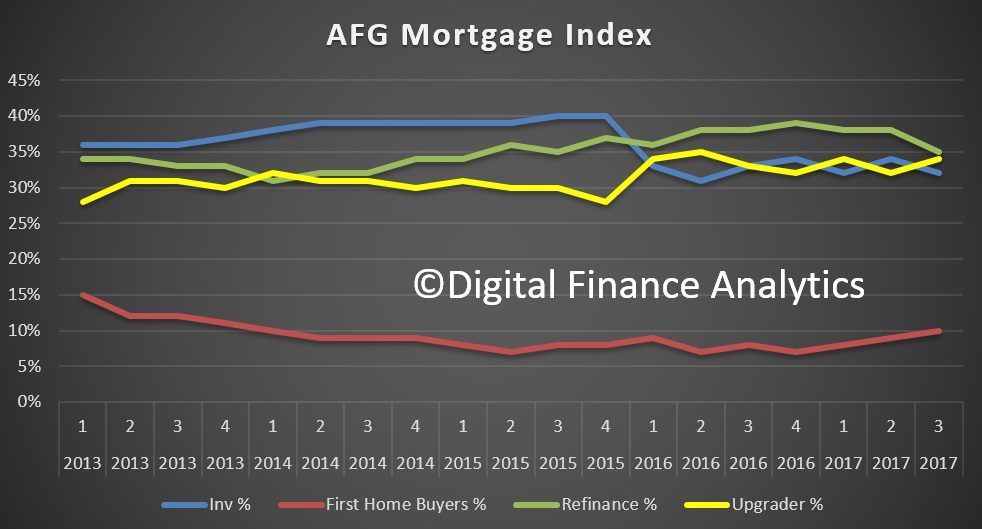

The volumes of first time buyers rose a little, whilst refinanced transactions fell a little.

The volumes of first time buyers rose a little, whilst refinanced transactions fell a little.

The national First Home Owner Grant (FHOG) scheme funded by the states and territories has largely been hailed a success as it seeks to ease the hefty upfront costs for new entrants to the market. The effectiveness of the scheme however has been questioned of late and it appears this may have encouraged governments to act. “The Victorian state government has recently announced a number of changes to the scheme in that state and New South Wales is currently examining their options to help counter rising house prices in those states,” said AFG Interim CEO David Bailey.

AFG data shows positive signs amongst the FHB market with lodgments lifting back up to 10% for the first time since the first quarter of 2014.

“First home buyer numbers have been in the single digits for some time. It is good to see state governments looking to support those trying to get a foot on the property ladder. Time will tell if the proposed changes to the scheme go far enough to assist those looking to buy their first home in our two most populous states.”

APRA-imposed lender policy changes have had an impact on both the investor market and refinancers as many lenders lift interest rates for borrowers.

“Lenders have been told by the regulator to rein in their exposure to the investor market and APRA continues to monitor growth in lending to investors,” said Mr Bailey. “As a result many lenders have embarked upon a series of rate increases and a tightening of credit policy for investors to comply with APRA’s guidelines.

“This activity has seen investor loans drop from 34% to 32% across the quarter.”

Those looking to refinance have also been impacted, with that segment of the market dropping from 38% to 35% last quarter – its lowest level since the third quarter of 2015.

In overall lodgment numbers, AFG has reported a lift of 8% on Quarter 3 last year driven primarily by increasing activity of upgraders. “With a significant amount of changes being made to the appetites and pricing of lenders, help from a mortgage broker can be vital for consumers trying to navigate the dynamic market that is home lending,” said Mr Bailey.

“A result that should please the regulators is a drop in the loan to value ratio (LVR) in all states apart from South Australia where a marginal increase of 0.4% was evident. The national LVR is now down to 68.6%, the lowest level since the first quarter of 2013,” he concluded.