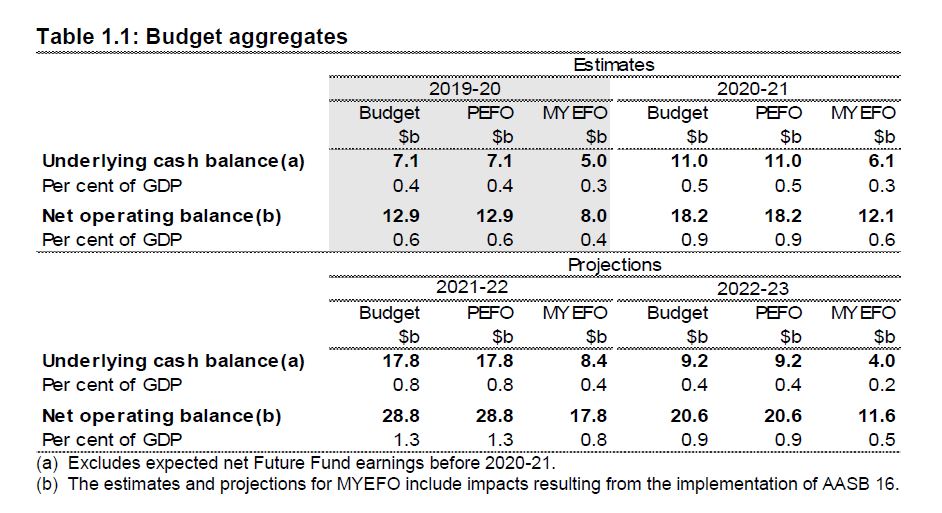

Total budget revenue is cumulatively higher by about $380 billion over five years compared with Treasury’s forecasts on the eve of the May 2022 election.

Yet, at a time when revenue is booming and the economy is operating around full capacity, the deficit in underlying terms is forecast to be $26.9 billion (1 per cent of gross domestic product), a $1.3 billion improvement since the May budget.

Cumulative underlying deficits over four years are projected to blow out to $144 billion, $21.7 billion worse than expected seven months ago.

Where are the adults in the room because from the budget point of view, they appear to have left years ago, and the result will be more pressure on ordinary households and businesses across the country.

http://www.martinnorth.com/

Details of our one to one service are here: https://digitalfinanceanalytics.com/blog/dfa-one-to-one/

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

Wanted Adults In The Budget Room, As Deficits Roar And Games Are Played!

So we got the Mid Year economic Forecast today from the Treasurer, and there was plenty of spin about necessary uplifts in spending, recent tax cuts and government support, and even that the Government is supporting women more than ever.

They were also keen to compare their own efforts with the previous Governments efforts (through they were including the COVID years), and international comparison which showed Australia’s economy still has more capacity, and is in some respects still the best dirty shirt.

But as I discussed with Leith van Onselen just yesterday in our live show, all is not well with this budget, and there will be consequences.

One notable issue was that federal government has cut company tax receipts for the first time since the pandemic because of weaker profits from the mining sector.

But the treasurer maintained most of the government’s long-run commodity price assumptions from the May budget. Iron ore, coking coal, thermal coal and LNG were unchanged at respectively $US60 a tonne, $US140 a tonne, $US70 a tonne and $US10 a metric million British thermal unit. Are these too conservative, and does it represent a hollow log for more spending – probably.

Then there is the so called off-budget issues. Today’s Mid-Year Economic and Fiscal Outlook (MYEFO), which showed that the federal government will spend a record $90 billion “off-budget” over the next four years, obscuring the true situation facing the budget. This off-budget spending does not show up in the underlying budget deficit or surplus despite it imposing a significant cost on taxpayers.

The underlying budget balance that treasurers prefer to focus on hides a heap of so-called “off-budget” spending, such as taxpayer money for the Clean Energy Finance Corporation, the $12 billion Snowy Hydro 2.0 project, wiping 20 per cent off student debts and the $15 billion National Reconstruction Fund.

Tax and other government revenue are hovering near a sustained record high of 25.5 per cent of the economy thanks to once-in-a-generation windfalls. The unemployment rate is a very low 3.9 per cent and personal income tax is on track for a record $335 billion this year, despite the stage 3 income tax cuts shaving off about $23 billion.

Company tax of $133 billion is just a bit below its all-time high last year, amid elevated commodity export prices.

Total budget revenue is cumulatively higher by about $380 billion over five years compared with Treasury’s forecasts on the eve of the May 2022 election.

Yet, at a time when revenue is booming and the economy is operating around full capacity, the deficit in underlying terms is forecast to be $26.9 billion (1 per cent of gross domestic product), a $1.3 billion improvement since the May budget.

Cumulative underlying deficits over four years are projected to blow out to $144 billion, $21.7 billion worse than expected seven months ago.

Where are the adults in the room because from the budget point of view, they appear to have left years ago, and the result will be more pressure on ordinary households and businesses across the country.

http://www.martinnorth.com/

Details of our one to one service are here: https://digitalfinanceanalytics.com/blog/dfa-one-to-one/

Go to the Walk The World Universe at https://walktheworld.com.au/

The Mid-Year Economic and Fiscal Outlook (MYEFO) update released on Wednesday estimates the Australian economy is expected to expand by a low 1.75% in 2023–24 before regaining momentum in 2024-25, when improved real incomes are expected to support a recovery in household consumption. It also notes inflation – although moderating – is still too high.

The outlook attributes that mainly to global oil prices and Treasury has not changed its forecast timetable for inflation’s return to the 2-3% target band, with 2.5% hit in mid 2025, so the Government is more optimistic than the RBA when it comes to expected progress on inflation. The RBA expects inflation to be at 3.0% by mid-2025.

Treasury’s analysis of the structural budget position suggests that the budget in 2023-24 is neutral with respect to inflation – it is neither adding nor reducing inflationary pressures.

Treasury continues to expect the economy will slow over the next few years to grow below trend with the unemployment rate drifting higher to 4.5% in 2025-26.

The migration intake has been a hot topic recently. As expected, the MYEFO forecasts upgrade the outlook for net overseas migration (NOM) in 2023-24 by 60k to 375k. We suspect that this will likely undershoot the eventual outcome. In 2024-25, forecasts for NOM have been marked down slightly to 250k, likely reflecting the expected impact of the Government’s recently announced migration strategy.

Gross debt is expected to peak at 35.4% of GDP in 2027-28, this is 0.2 percentage points lower than projected in the May Budget. While debt is expected to be lower, the expected cost of capital has also increased since the May Budget, reflecting the rise in government bond yields. Overall, these counteracting forces net out to a slight increase in interest payments as a share of GDP over the medium term.

Sadly, in a blow for budget transparency, there is still a line for decisions taken but not yet announced. We don’t know what decisions these are, but they are significant – the estimates start at $270 million in 2023-24 and rise to $1.8 billion in 2026-27. It is impossible to tell what this spending is for. If the government were to reverse those decisions between now and the next budget update, we will never know.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

The Mid-Year Economic and Fiscal Outlook (MYEFO) update released on Wednesday estimates the Australian economy is expected to expand by a low 1.75% in 2023–24 before regaining momentum in 2024-25, when improved real incomes are expected to support a recovery in household consumption. It also notes inflation – although moderating – is still too high.

The outlook attributes that mainly to global oil prices and Treasury has not changed its forecast timetable for inflation’s return to the 2-3% target band, with 2.5% hit in mid 2025, so the Government is more optimistic than the RBA when it comes to expected progress on inflation. The RBA expects inflation to be at 3.0% by mid-2025.

Treasury’s analysis of the structural budget position suggests that the budget in 2023-24 is neutral with respect to inflation – it is neither adding nor reducing inflationary pressures.

Treasury continues to expect the economy will slow over the next few years to grow below trend with the unemployment rate drifting higher to 4.5% in 2025-26.

The migration intake has been a hot topic recently. As expected, the MYEFO forecasts upgrade the outlook for net overseas migration (NOM) in 2023-24 by 60k to 375k. We suspect that this will likely undershoot the eventual outcome. In 2024-25, forecasts for NOM have been marked down slightly to 250k, likely reflecting the expected impact of the Government’s recently announced migration strategy.

Gross debt is expected to peak at 35.4% of GDP in 2027-28, this is 0.2 percentage points lower than projected in the May Budget. While debt is expected to be lower, the expected cost of capital has also increased since the May Budget, reflecting the rise in government bond yields. Overall, these counteracting forces net out to a slight increase in interest payments as a share of GDP over the medium term.

Sadly, in a blow for budget transparency, there is still a line for decisions taken but not yet announced. We don’t know what decisions these are, but they are significant – the estimates start at $270 million in 2023-24 and rise to $1.8 billion in 2026-27. It is impossible to tell what this spending is for. If the government were to reverse those decisions between now and the next budget update, we will never know.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

As we come to the end of 2019, you’d be forgiven for being confused about the health of the economy. Via The Conversation.

Treasurer Josh Frydenberg regularly points

out that jobs growth is strong, the budget is heading back to surplus,

and Australia’s GDP growth is high by international standards.

The opposition points to sluggish wages growth, weak consumer spending and weak business investment.

Monday’s Mid-Year Economic and Fiscal

Outlook (MYEFO) provides an opportunity for a pre-Christmas stock-take

of treasury’s thinking.

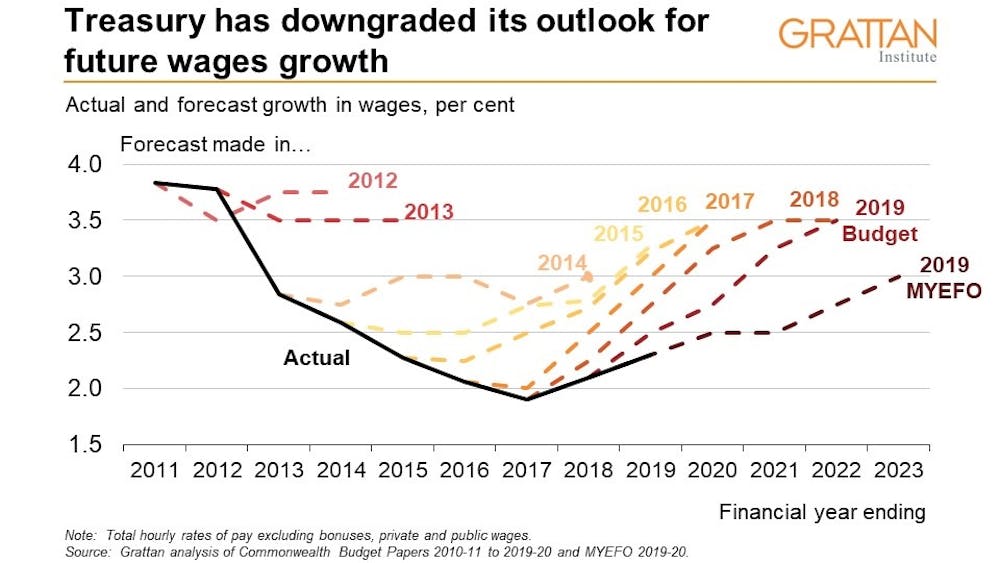

1. Low wage growth is the new normal

Rightly grabbing the headlines is yet another downgrade to wage growth.

In the April budget, wages were forecast to grow this financial year by 2.75%. In MYEFO, the figure has been cut to 2.5%.

Three years ago, when Scott Morrison was treasurer, the forecast for this year was 3.5%.

Each time wages forecasts missed, treasury assumed future growth would be even higher, to restore the long-term trend.

Today’s MYEFO is a long-overdue admission

from treasury that labour market dynamics have shifted – in other words,

lower wage growth is the “new normal”.

Even by 2022-23, wages are projected to

grow at only 3% (and even that would still be a substantial turnaround

compared to today).

Of course, wages are still rising in real terms (that is, faster than inflation), a fact Finance Minister Mathias Cormann is keen to emphasise.

But Australians will have to adjust to a world of only modest growth in their living standards for the next few years.

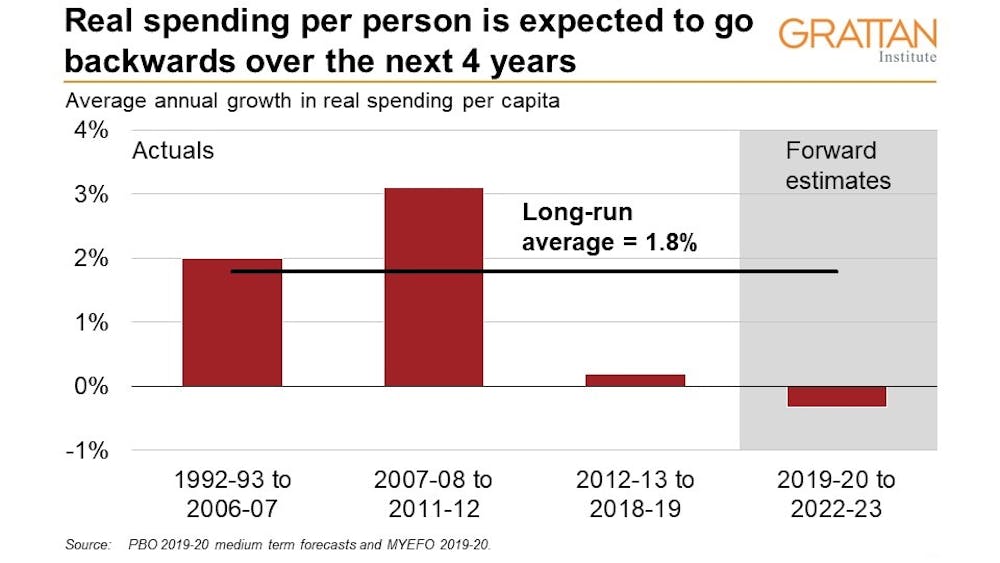

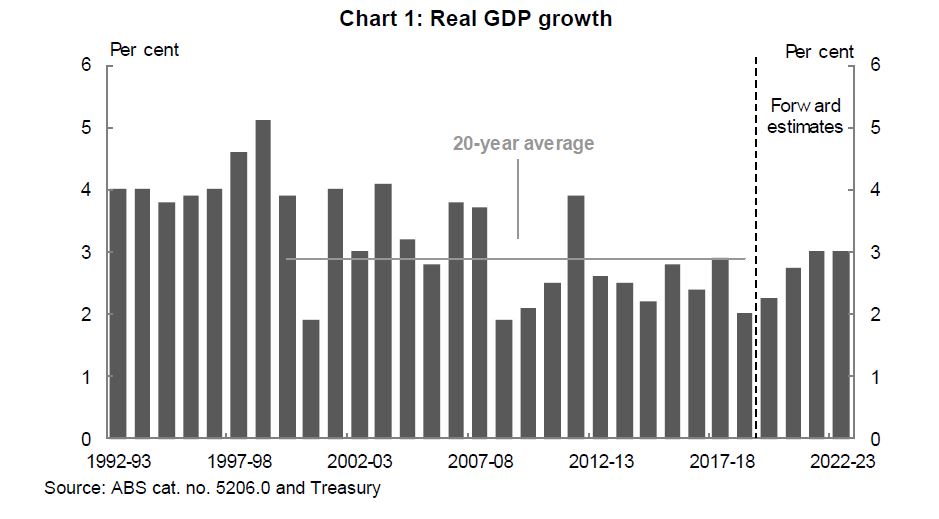

2. Economic growth is underwhelming, especially per person

Economic growth forecasts have received a pre-Christmas trim.

Treasury now expects the economy to grow by 2.25% this financial year, down from the 2.75% it expected in April.

Particularly striking is the sluggishness

of the private economy, with consumer spending expected to grow by just

1.75%, despite interest rate and tax cuts, and business investment

idling at growth of 1.5%, down from the 5% forecast in April.

The longer term picture looks somewhat

better, with growth forecast to rise to 2.75% in 2020-21 and 3% in

2021-22, although treasury acknowledges there are significant downside

risks, particularly from the global economy.

The government has made much of the fact

our economy is strong compared to many other developed nations. But much

more relevant to people’s living standards is per-person growth.

Australia’s international podium finish looks less impressive once you

account for the fact Australia’s population is growing at 1.7%.

As one perceptive commentator

has noted, while Australia is forecast to be the fastest growing of the

12 largest advanced economies next year, it is expected to be the slowest in per-person terms.

3. The government is at odds with the Reserve Bank

You can imagine the government’s

collective sigh of relief that it is still on track to deliver a surplus

in 2019-20, albeit a skinny A$5 billion instead of the the $7 billion

previously forecast.

Given the treasurer declared victory early

by announcing the budget was “back in the black” in April, missing

would have been awkward, to say the least.

And another three years of slim surpluses are forecast ($6 billion, $8 billion and $4 billion respectively).

The real issue for the treasurer is how to

deal with the growing calls for more economic stimulus, including from

the Reserve Bank.

Depending on what happens to growth and

unemployment in the first half of 2020, he will come under increased

pressure to jettison the future surpluses to support jobs and living

standards.

4. High commodity prices are a gift for the bottom line

High commodity prices are the gift that keeps on giving for the Australian budget.

Iron ore prices in excess of US$85 per

tonne, well above the US$55 per tonne budgeted for, have helped to keep

company tax receipts buoyant.

Treasury is maintaining the conservative approach it has taken in recent years by continuing to assume US$55 per tonne.

This provides some potential upside should

prices stay high – Treasury estimates a US$10 per tonne increase would

boost the underlying cash balance by about A$1.2 billion in 2019-20 and

about A$3.7 billion in 2020-21.

The budget bottom line remains tied to the whims of international commodity markets for the near future.

5. The surplus depends on running a (very) tight ship

The forecast surpluses over the next four years are premised on an extraordinary degree of spending restraint.

This government is expecting to do

something no government has done since the late-1980s: cut spending in

real per-person terms over four consecutive years.

The budget dynamics are helping. Budget

surpluses and low interest rates reduce debt payments, and low inflation

and wage growth reduce the costs of payments such as the pension and

Newstart.

But the government is also expecting to

keep growth low in other areas of spending, in almost every area other

than defence and the expanding national disability insurance scheme.

As the Parliamentary Budget Office points out, it is hard to keep holding down spending as the budget improves.

It is even more true while long term

spending squeezes on things such as Newstart and aged care are hurting

vulnerable Australians.

Where does it leave us?

The real lesson from MYEFO is that

Australians are right to be confused: there is a disconnect between the

health of the budget and the health of the economy.

MYEFO suggests both that the government is

on track to deliver a good-news budget surplus underpinned by high

commodity prices and jobs growth, and that the economy is in the

doldrums with low wage growth in place for a long time.

Top of Frydenberg’s 2020 to do list: how to reconcile the two.

Authors: Danielle Wood, Program Director, Budget Policy and Institutional Reform, Grattan Institute; Kate Griffiths, Senior Associate, Grattan Institute

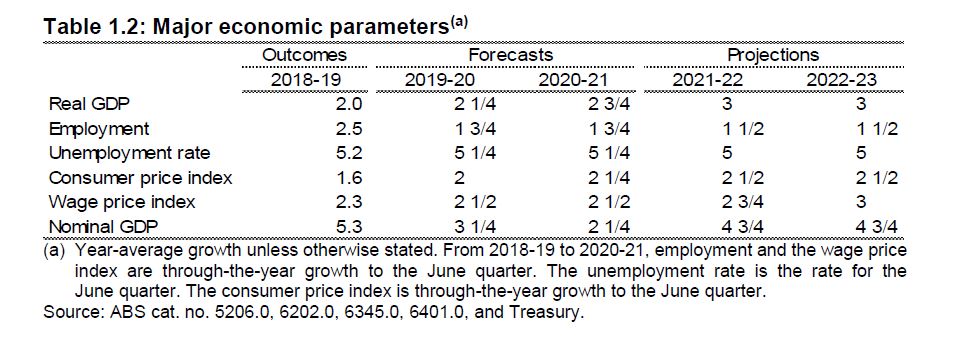

MYEFO has been released, and as expected the Government is still forecasting a surplus, this year down from $7.1 billion to $5 billion, but still a surplus for the first time in 12 years. The surplus for 2020/21 is now seen at $6.1 billion instead of $11 billion as previously estimated. Tax receipts are down 32.6b over 4 years.

Wage growth forecasts were reduced, but are still too optimistic, while the unemployment rate was expected to be higher than hoped at 5.25 per cent, rather than five per cent for this financial year and next.

Treasury still is sticking with a 5% employment threshold below which inflation is expected to rise, while the RBA has this at 4.5%.

The forecast for economic growth has reduced from 2.75 per cent, to 2.25 per cent. The downgrade to growth was blamed on weak momentum in the global economy, as well as domestic challenges such as the effects of drought and bushfires. The drought in Australia that had already taken a quarter of a percentage point off GDP growth and reduced farm output by a significant amount over the last two years. Growth is then expected to strengthen to 2¾ per cent in 2020-21.

They have shrunk the expected surpluses over the next four years due to a downgrade of tax receipt expectations, with total receipts revised down by $3 billion in 2019/20 and by $32.6 billion over the four years to 2022/23. GST to the states is down nearly 2 billion in the next year, due to weaker activity.

Australia’s interest bill on its debt will fall from $19 billion last year to $14.5 billion (thanks to lower interest rates). Over the next four years this amounts to $13.5 billion savings.

While the

mid-year update included a $623.9 million aged care package, there were

no other new major spending measures to lift economic growth. This will

keep the pressure on the Reserve Bank of Australia to reduce the cash

rate even further next year.

In essence, the Treasury is leaving the action to the Reserve Bank, further confirmation we are likely to get more cuts next year.

But they are also counting on stronger house prices leading to a positive wealth effect.

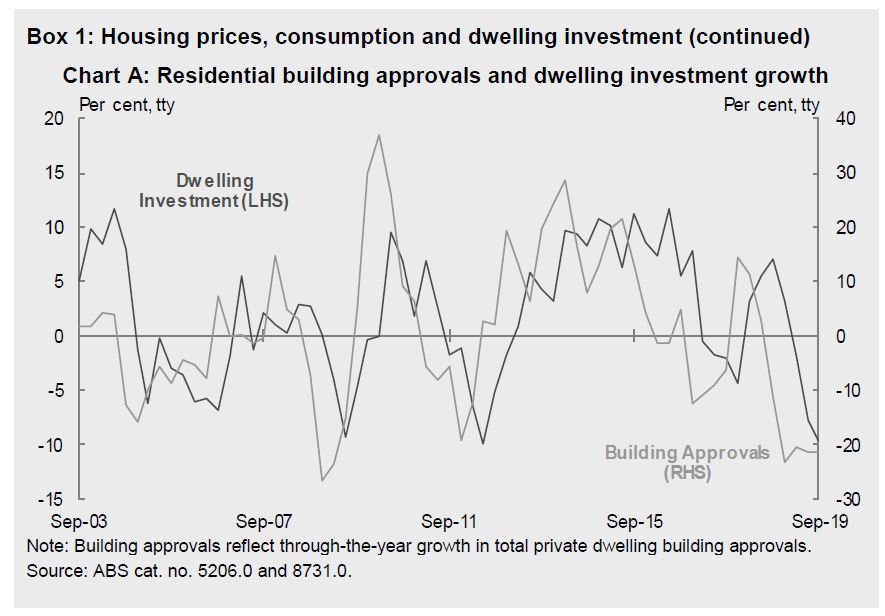

After a recent period of significant falls in housing prices from mid-late 2017 to mid-2019, the established housing market has stabilised. In July 2019, combined capital city housing prices rose for the first time in almost two years, and this has continued in recent months. Although increases have been largest in Sydney and Melbourne, increases have now spread to all cities except Darwin. Overall, combined capital city housing prices are now almost 6 per cent higher than their recent trough in June, although they are still around 5 per cent lower than their peak in September 2017.

This increase in housing prices is expected to support the outlook for household consumption, particularly as corresponding increases in housing turnover should see a pick-up in spending on household goods such as furnishings. More broadly, continued rises in housing prices should provide a boost to confidence and household wealth, as well as increasing borrowing capacity given changes in collateral.

Ownership transfer costs — various fees incurred when fixed assets such as dwellings are sold (including legal and real estate agent fees, stamp duty, and other government charges) — were negatively affected by low rates of housing market turnover in 2018-19 and detracted from real GDP growth. Ownership transfer costs rose by 4.5 per cent in the September quarter 2019 and a further increase supported by stronger housing turnover and prices should contribute to economic growth over the forecast period.

Movements in housing prices impact dwelling investment activity through changes to expected returns to residential construction. However, recent price gains will affect new dwelling investment with a delay. This is because planning and approval processes take time to work their way through into new construction. On average, depending on the type of dwelling, it can take around 2 to 5 months for new dwellings to commence following approval, and a further 6 to 20 months for activity to be completed. High-density dwellings have the longest approval and construction times, and houses the shortest on average.

New dwelling approvals have trended down since late 2017, with the total number of building approvals over the year to October 2019 down by more than 20 per cent from the preceding 12 months and below the 10-year average. The falls in building approvals have been particularly stark in medium-high density dwellings, which also have the longest lag between approval and completion. This means that further moderation in dwelling investment is likely over the forecast period (Chart A). This weakness should be partly offset by a solid pipeline of housing construction work yet to be done.

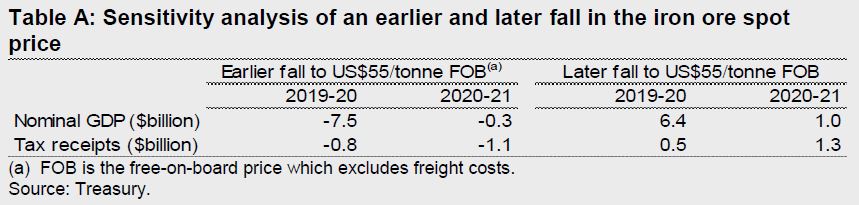

The other area of sensitivity is the iron ore price and commodity prices in general.

Iron ore spot prices increased sharply in the first half of 2019, mainly due to supply issues in Australia and Brazil, and stronger-than-expected demand from China. Iron ore prices peaked in early July at almost US$120 per tonne free-on-board (FOB). Prices have since fallen, but remain above the price assumed at PEFO. The decline in the price has mainly been due to uncertainty about demand from Chinese steel mills and the recovery in supply. As such, prudent assumptions have been retained and the iron ore spot price is assumed to decline to reach US$55 per tonne FOB by the end of the June quarter 2020. This is one quarter later than was assumed at PEFO.

Coal prices have fallen since PEFO. Metallurgical coal prices have fallen faster and further than had been assumed at PEFO, with the spot price below US$150 per tonne FOB since October 2019. The fall in the spot price is due in large part to uncertainty about demand from Chinese steel mills and policy changes in China. The metallurgical coal price is assumed to remain around recent levels of US$134 per tonne FOB over the forecast period. This is lower than the PEFO assumption, which was for the price to fall to US$150 per tonne FOB by the end of the March quarter 2020.

After reaching a peak of just over US$125 per tonne FOB in mid-2018, thermal coal prices have trended lower, mainly due to increases in seaborne supply and softer global demand. The thermal coal price is assumed to remain around recent levels of US$64 per tonne FOB over the forecast period, below the PEFO assumption of US$91 per tonne FOB.

If the iron ore price were to fall immediately to US$55 per tonne FOB, two quarters earlier than assumed, nominal GDP could be around $7.5 billion lower than forecast in 2019-20 and $0.3 billion lower in 2020-21. This would have a negative flow-on impact to company tax receipts estimated at around $0.8 billion in 2019-20 and $1.1 billion in 2020-21.

By contrast, if the iron ore price remained elevated for two quarters longer than currently assumed, before falling immediately to US$55 per tonne FOB, nominal GDP could be around $6.4 billion higher than forecast in 2019-20 and $1.0 billion higher in 2020-21. This would have a flow-on impact to company tax receipts estimated at around $0.5 billion in 2019-20 and $1.3 billion in 2020-21.

The actual impact on company tax receipts may vary due to timing of tax collections and the availability of tax losses.

On Monday the Australian government will release the Mid-Year Economic and Fiscal Outlook (MYEFO). This will – as required by the Charter of Budget Honesty – provide an update on the key assumptions made in this year’s budget, and track the implications of decisions made since the budget for the projected surplus. Via The Conversation.

There are two things you can count on about MYEFO.

First, the government will have to pare back its forecasts for economic growth, wages growth and employment growth.

Second, no matter what the economic reality is, the forecast for a budget surplus will remain.

The government has made economic

management – as measured by the rather dubious criterion of budget

balance – the central plank of its electoral strategy. As the Australian

National University’s 2019 Australian Election Study

revealed, voters preferred the government’s economic policies to

Labor’s by a wide margin (47% to 21%, with 17% thinking there was no

difference). On the management of government debt, the margin was 44% to

18%.

But the economy isn’t doing very well. GDP annual growth is 1.7%, not the 2.75% forecast in the budget. The unemployment rate is 5.3%, compared to the forecast of 5.0%. Wage growth is 2.2%, not the 2.75% forecast.

Iron ore supplements

The forecast budget surplus for the fiscal

year to June 2020 will be made to hang together, thanks to a

higher-than-forecast iron ore price.

That price – which determines the dollar

value of Australia’s biggest export and hence the tax revenue it

generates – is not reflected in the GDP figure, which only takes into

account volumes.

The iron-ore price is now US$92.50 a tonne. The budget assumed the average price would be $US88 for the 2020 budget year, thanks to a reduction in the international supply of iron ore caused by a tailings dam bursting in January at the Córrego do Feijão mine near the town of Brumadinho in southeastern Brazil.

The dam’s collapse released a tsunami of sludge that destroyed farms, houses, roads and bridges, and killed 272 people.

The river of sludge released by the dam spill in Brumadinho, Minas Gerais, Brazil, January 26 2019.

Antonio Lacerda/EPA

Ensuing mine shutdowns reduced iron ore

output from operator Vale (the world’s biggest iron ore miner) by about a

third. This in turn led to the price of iron ore this year being very

high, as the following chart illustrates.

The Australian government sensibly assumed

the Brazilian mine would come back online and the ore price would

revert to $US55 per tonne by March 2020.

But just think about the 2020-21 fiscal year. The government’s own sensitivity analysis

shows for the full 2020-21 budget year a difference in the iron ore

price of US$10 a tonne translates to a A$3.7 billion difference in the

budget bottom line.

That has helped this year, but it also

shows how dependent the budget’s relatively small A$7.1 billion

“underlying cash balance” is on a commodity price that’s out of our

control.

Yet, given the political non-negotiability

of the surplus, we can expect assumptions that stretch credulity to

maintain a surplus forecast.

Some action?

This is all against a backdrop of calls

for fiscal stimulus from the governor of the Reserve Bank of Australia,

the Business Council, every mainstream economist and recently Australia’s top chief executives.

But any stimulus meaningful enough to

boost the ailing economy would blow the budget surplus. And the

assumptions have already been stretched to breaking point, so there’s

very little room for the government to manoeuvre.

The government will probably announce some

sort of “investment allowance” – where companies get a modest tax break

for specific types of investments in the short term. As I have argued before,

this will do something to boost investment and the economy generally,

but not nearly as much as a full-scale reduction in the company tax rate

to 25% for all businesses.

But the government can’t afford to do a proper tax cut because of its devotion to a wafer-thin surplus.

The danger of too little action

In the end, what the government ends up

announcing will really be an allocation of responsibilities. It will

determine how much of the work of economic recovery it will do itself,

and how much it will want to palm off to the Reserve Bank.

The downside of the former is losing the budget surplus.

The downside of the latter is that the

Reserve Bank will have no choice but to cut the cash rate to 0.25% in

early 2020 and then embark upon a bond-buying program – i.e.

“quantitative easing” or “QE”.

As even Reserve Bank governor Philip Lowe

has himself admitted, more aggressive monetary policy brings with it the

(further) risk of asset-price bubbles and financial instability.

Right now the government is putting all its chips on the surplus. Will that turn out to be a good bet? Time will tell.

2020 will reveal much about the future of

the Australian economy and whether we manage to escape dramatic problems

like a recession.

We live in interesting times – but perhaps more in the “Ancient Chinese curse” kind of way than any of us would like.

Author: Richard Holden, Professor of Economics, UNSW

But the numbers in MYEFO show it has failed to hit many of its own targets.

Target 1: Surpluses on average over the cycle

The government’s overarching fiscal objective is to deliver budget

surpluses: not just in one year but on average over the economic cycle.

MYEFO indicates the government is expecting a $5.2 billion deficit in 2018-19 (0.3% of GDP).

It will be the 11th consecutive deficit for the Commonwealth budget.

Deficits have averaged $33.2 billion (2.1% of GDP) over those 11 years.

Yes, a $4.1 billion surplus is forecast for next year, with surpluses projected to reach $19 billion (0.9% of GDP) by 2021-22.

But so big have the recent deficits been, that even if everything

goes well and the fiscal position continues to improve, the budget would

need to be in surplus for decades to produce a surplus on average over

each year, far longer than what most economists consider a typical

economic cycle.

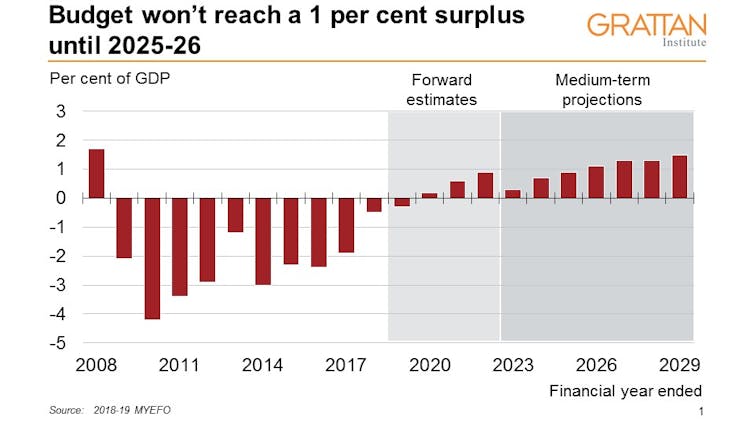

A related fiscal target is that budget surpluses will build to at least 1% of GDP as soon as possible.

Despite revenue windfalls from income and company taxes (discussed

below), the government is still forecasting it won’t reach that 1% of

GDP surplus target until 2025-26.

Policy decisions in this year’s budget and MYEFO – including income

and company tax cuts, additional funding for independent and Catholic

schools, and changes to the GST formula to placate Western Australia –

have weakened the bottom line in 2021-22 by $10.5 billion.

Hardly the actions of a government in a hurry to deliver a sizeable surplus.

Verdict: Fail.

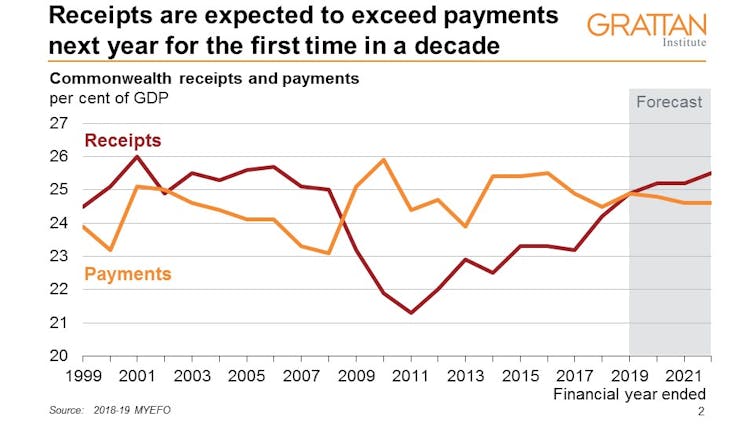

Target 2: Reduce the payments-to-GDP ratio

The government’s policy is also to maintain strong fiscal discipline

by controlling expenditure, with a falling payments-to-GDP ratio its

measure of success.

Whether it has met the target depends on the starting year.

Governments payments are forecast to reach 24.9% of GDP in 2018-19, up

from 23.9% in 2012-13 before the Coalition took office.

The government prefers the starting point of its first year in office 2013-14 where payments were 25.5% of GDP.

Either way, payments in 2018-19 remain above the 30-year historical average of 24.7% of GDP.

While the government projects that spending will fall slightly

further to 24.6% of GDP by 2021-22, this relies on spending growth

across the government’s major programs falling substantially compared to the previous four years – without major policy changes to help facilitate the fall.

Verdict: Debateable pass.

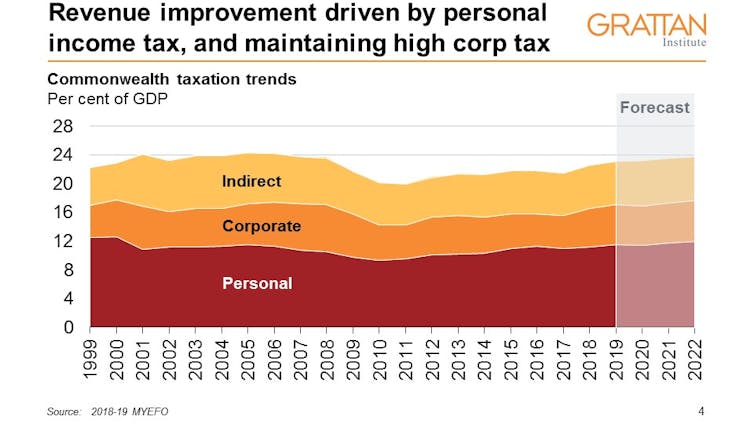

Target 3: Tax-to-GDP ratio below 23.9% of GDP

In last year’s budget, the government introduced a new target of capping tax collections at 23.9% of GDP.

Why 23.9%? That was the average level of tax during the final two terms of the Howard/Costello government.

While the Coalition is understandably keen to follow the lead of one

of its most electorally successful governments, that was also a period

where tax collections were historically high.

Tax collections are projected to reach 23.8% of GDP in 2022, on the

back of stronger than forecast personal income tax and company tax

receipts.

Verdict: Pass.

MYEFO Chart.

Target 4: New spending measures more than offset by reductions in spending elsewhere

Since becoming prime minister, Scott Morrison has sent mixed signals

about whether his government will adhere to the longstanding budget rule

that all new spending proposals be matched with budget savings.

At the MYEFO press conference, Finance Minister Matthias Cormann said it was a “matter of balancing competition priorities”.

Here’s the straight answer – the net effect of policy changes

announced in MYEFO are an additional $12.2 billion in spending over four

years.

In other words, the government has not offset new spending with cuts

to other spending programs. The Turnbull government similarly failed to

offset its new spending in 2017-18 (although it succeeded in prior

years).

There have been some reductions in spending because of improvements

in the economy. The government claims these reductions offset its recent

spending announcements. But genuine offsets come from policy changes,

not economic good luck.

Verdict: Fail.

Target 5: Shifts due to changes in the economy banked as an improvement in budget bottom line

This objective is key to the government’s fiscal conservative credentials.

If it has some economic good luck, it commits to use the proceeds for budget repair rather than new spending or tax cuts.

This rule has been irrelevant for most of the past decade, because

almost every budget had revenue collections falling short of forecast.

But the Morrison government is in the middle of a mini revenue boom –

revenue collections were higher than forecast in both the 2018-19

budget and MYEFO.

Company tax collections are higher largely due to strong commodity

prices. Income tax collections are up and government spending is down

because of improvements in the economy.

So has the government used this chance to show off its fiscal prudence?

Not exactly. It will spend around $11.8 billion of this windfall,

give away another $19.3 billion in tax cuts and bank just over half of

it ($35.2 billion) to the bottom line.

And in the shadow of an election, we can almost certainly expect

further spending. The $9 billion in decisions taken but not announced –

potentially a pre-election warchest – suggests that more tax cuts could

also be on the way.

Verdict: Fail.

Our final verdict

The challenge in assessing budget management is separating good luck

from good management. Governments will always seek to take credit for

economic upswings that boost the bottom line.

Fiscal targets are there to keep them on the straight and narrow.

An objective assessment of the government’s performance against its

own key targets suggests its good news budget is more mirage than

magnificent management.

Authors: Danielle Wood, Program Director, Budget Policy and Institutional Reform, Grattan Institute; Kate Griffiths Senior Associate, Grattan Institute

Blog")