The trends are clear, in many western countries around the world, home prices have been rising, and in recent years rising fast. The underlying drivers are the freeing up of mortgage markets, and lower interest rates, allowing more people to borrow more, which is why debt has been rising too. As you know I have long argued the rise in home prices to stupid levels is all due to the deregulation of the financial system, driven by neo-liberal thinking which leaves ordinary people in the dust. Greater debt driven demand lifts prices.

Of course, the Government is fixated on the supply side story. And we can expect they will peddle this hard into the election. The government’s housing policies include 1.2 million new homes built by mid-2029, a $9.3 billion agreement with states and territories to support social housing and homelessness services, a scheme to help 40,000 households purchase a new or existing home, and tax incentives to support investment in new build-to-rent developments. One of those latter tax incentives includes increasing the capital works tax discount depreciation rate from 2.5 per cent to four per cent.

The other factor in play is high migration, another demand driver, with another 2 million people expected to land in the country over the next few years. This was subject to interesting questioning from Senator Bragg in Estimates recently. Astonishingly, Treasury has not considered the impact of high migration on housing demand (and implicitly) price.

But what of the tax breaks for investors? Well according to a new report from Australian Council of Social Service (ACOSS), Two tax breaks are “disproportionately” benefiting Australia’s richest while simultaneously fuelling the housing affordability crisis. The report criticises the capital gains tax deduction for property, where only 50 per cent of capital gains made from an asset are taxed when it is sold, and negative gearing, which allows investment expenses to be deducted from income.

ACOSS says the wealthiest 10% of households own two-thirds of all investment properties and are receiving 82% of the $16 billion in tax relief the two breaks provide.

While I absolutely agree the investor tax breaks are part of the problem, unless we address too high migration, control unsustainable lending growth, and also work on building enough new homes to meet new demand, the affordability situation will continue to deteriorate.

As a result, many will choose to leverage up just to get into the market and out of the rental sector. Government policy is at fault here. And they appear to be avoiding the elephants in the room. Address too high migration, and control unsustainable lending growth.

I wonder if this is because many politicians are also property investors?

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

Find more at https://digitalfinanceanalytics.com/blog/ where you can subscribe to our research alerts

Today’s post is brought to you by Ribbon Property Consultants.

Digital Finance Analytics (DFA) Blog

Are Investors The Reason Home Prices Are Rising Into Unaffordability?

When you want to take back a multibillion-dollar giveaway to the country’s wealthiest, expect them to put up a fight.

The Labor Party’s proposal to reduce the tax advantages of being a

landlord by limiting negative gearing to new homes has become the new

enemy of the landlord class, who are arming themselves for policy

combat.

Luckily, the modern way we fight over resources requires no weapons, nor bloodshed, but it is nevertheless a strategic Game of Homes, with subplots, twists, surprises.

Negative gearers use losses made from investments such as renting out

properties to cut their taxable incomes. If they make an eventual

profit by selling out of the investment, the capital gains tax rules

mean only half of it is taxed.

allow existing negative gearing arrangements to continue

restrict new negative gearing to investment income, meaning

investors could subtract investment losses from investment income but

not wage income

allow an exemption for investments in newly constructed housing,

meaning those losses could still be deducted from wage income as they

can at present

cut the capital gains tax discount from 50% to 25%, meaning

three-quarters of each capital gain would be taxed instead of one half

as at present

exempt existing investments from the change, meaning the capital

gain on selling them would be only half taxed as at present whenever

they were sold.

The changes would allow it to claw back more than A$30 billion over

ten years, most of it from the higher earners in a position to take

advantage of negative gearing.

Among the weapons being deployed against its plans are untruths. Here are some of them.

Untruth: it’ll cost us our AAA credit rating

No less an authority then the prime minister has claimed Labor’s

negative gearing and capital gains tax proposal — that would recoup

billions in taxes — would somehow make Australia’s public debt less manageable.

It would, for some reason, make rating agencies remove the letter A

from rating documents that lenders pay little attention to.

This is untrue on two fronts. First, increasing taxes by A$10 billion

per year would make public debt more manageable, not less.

Second, ratings by agencies who proved to be unable to judge risk

during the global financial crisis don’t matter much to borrowers.

Morrison would be as well served by claiming that he has three fully

grown and trained dragons that would roast the grandchildren of people

who vote Labor.

How effective it is depends on how much our media has become a clickbait farm rather than a news reporting service.

Hint for journalists: it is not news when a politician repeats

untruths. It is newsworthy when one tells the truth. If you have to

report untruths, simply write a headline along the lines of “politician

lies again”. You will better inform the public.

Untruth: mums, dads, teachers and nurses will suffer

The unspoken rule in Australia is that policy changes cannot hurt

“Mums and Dads”. Add in teachers, nurses and police, and there’s an

untouchable alliance.

Putting aside for one moment that the claim is misleading (the occupations most likely to negatively gear are surgeons and anaesthetists),

the inconvenient truth for those claiming that mums and dads will be

hurt is that is that will still be able to negatively gear (new properties) under Labor’s policy.

It is hard to believe that a government that presided over a two-year pay freeze for the 6,500 staff of the Australian Federal Police, and who recently cut its budget, wants its officers to have more money.

To be part of the Game of Homes you apparently need not just to be a

police officer, or a Mum or a Dad, but to be landlord as well.

Untruth: we won’t build more houses

In an unlikely claim, Master Builders Australia has asserted that a policy designed to channel funding into newly built housing won’t help build more houses.

It’s becomes easier to understand when you realise that the

association is part of the Game of Homes. Actual builders have been

leaving it, in some cases because of concern that it doesn’t represent their interests and in others because of concern that it has ties to the Coalition.

the Labor Party’s plan to limit negative gearing tax breaks to new

housing would put a rocket under the business of residential developers

because demand from investors would surge

Untruth: housing will be cheaper, or more expensive

Opponents of Labor’s proposal have claimed housing will be both cheaper and more expensive, as if each is a bad thing.

Sometimes, as with Treasurer Josh Frydenberg, they claim both in the same speech, in the same sentence:

Under the policy, everyone who owns a home will see it be worth less,

and under that policy, everyone who rents a house will end up paying

more.

At least he has pulled back somewhat from the claims made by then

Prime Minister Malcolm Turnbull during the last election campaign.

It isn’t what the Treasury was telling the government. We now know, from documents released under the Freedom of Information Act, that it had told it

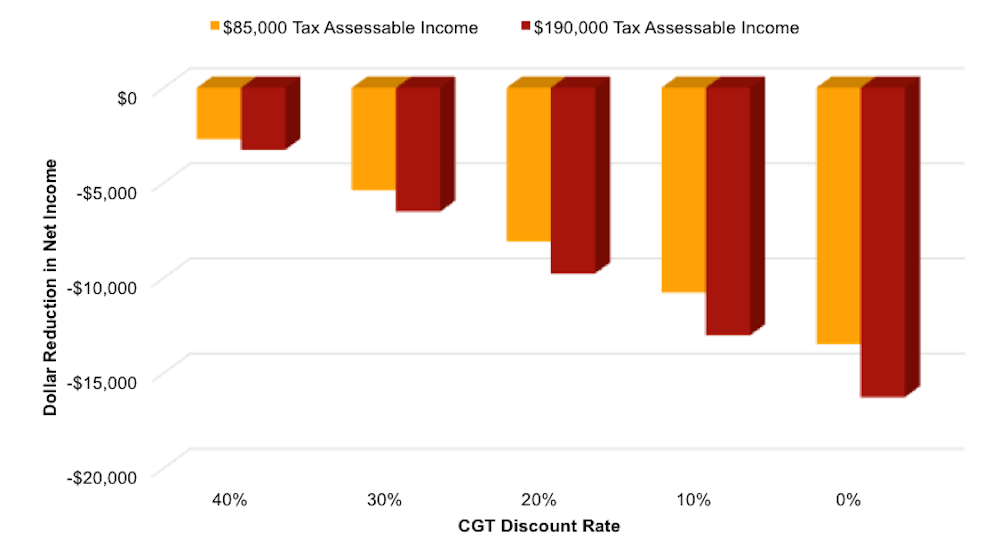

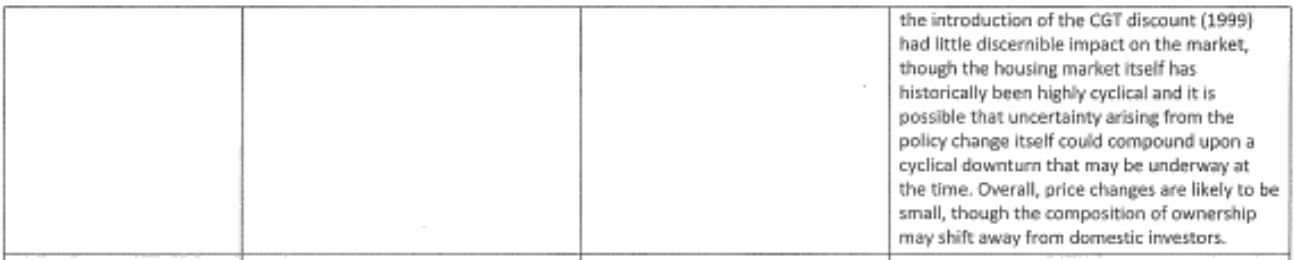

overall, the price changes are likely to be small, though the composition of ownership may shift away from domestic investors

Last year the government asked whether it could at least say the Treasury thought Labor’s plan would reduce house prices.

Treasury replied that it could not, in strikingly blunt terms:

We did not say that the proposed policies “will” reduce house

prices. We said that they “could” put downward pressure on house prices

in the short-term depending on what else was going on in the market at

the time, but in the long-term they were unlikely to have much impact.

There is unlikely to be much impact on rents either. When Labor cut

back negative gearing in the mid-1980s in the same way as it plans to

now rents rose sharply in Perth and rose somewhat in Sydney. They fell

in Adelaide and Brisbane and remained steady in real terms in Melbourne.

The Grattan Institute sums up the likely impact this time by saying

rents “won’t change much”.

Untuth: the government wants Labor to win the election

listen to the critics of its policy, cut its losses and abandon the changes to negative gearing and capital gains tax

The lie here is that Frydenberg is trying to help Labor out, that he

would want it to cut its “losses”. In political battles, parties

generally celebrate the other side’s losses rather than steer them away

from them.

As a rule, the more vested interests organise their strategic

alliances and myth-making battle plans to stop your policy, the better

it is. We saw it the mining super-profit tax, we saw it with gold tax

(yes, until 1991 the profits made from mining gold used not to be taxed) we saw it with fringe benefits tax, we saw it with capital gains tax itself.

Stay tuned

I can’t predict what will happen next season on Australia’s Game of

Homes, but there’s a chance some of the characters in this story will

dramatically meet their demise, perhaps at the election.

Winter is coming.

Author: Cameron Murray, Lecturer in Economics, The University of Queensland

Reforming negative gearing could save the federal government A$1.7 billion without hurting “mum and dad investors”, according to our new modelling, by focusing tax deductions on investors with smaller property portfolios and removing them for richer investors.

Combined with changes to capital gains tax, reforming negative gearing could make the Australian housing market more sustainable and equitable.

Negative gearing allows investors to claim a tax deduction if their rental income is less than their expenses. It cost the federal government A$3.04 billion in 2013-14, according to our calculations.

Our report also confirms that negative gearing and the capital gains tax discount incentivise housing investors to take on debt. This potentially makes the housing market less stable and crowds out first home buyers.

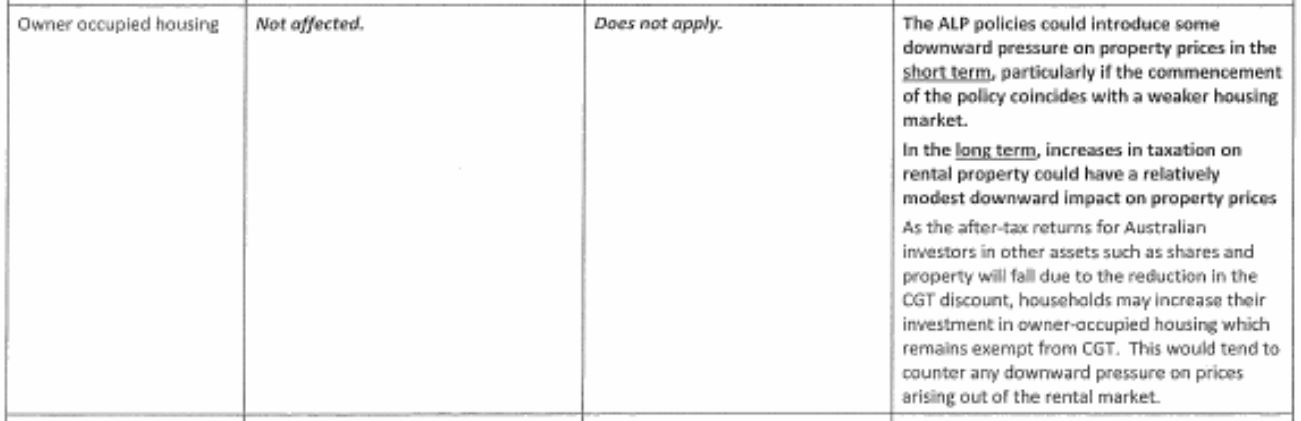

According to Treasury modelling, the Labor Party’s plan to limit negative gearing deductions on newly acquired rental housing would put relatively modest downward pressure on house prices. Preliminary research from Melbourne University has found that eliminating negative gearing would result in an increase in home ownership.

But using data on the distribution of property and incomes makes it possible to differentiate between poorer and wealthier investors, allowing the government to target reforms to cushion the blow for investors on lower incomes.

Targeted negative gearing reform

In our example, investors in the bottom half of the income and property distributions could be allowed to claim tax deductions for all allowable rental expenses. Those in the 51st–75th income percentiles could deduct 50% of those expenses, while negative gearing would be eliminated for those in the top 25% of incomes.

Our modelling of this scenario shows this would save the federal government A$1.7 billion, or 57.3% of the current cost to the budget, each year. If negative gearing deductions were limited based on property values, the saving would be A$1.5 billion (or 48.3%).

Given this reform would be less likely to hurt poorer investors, they would be less likely to withdraw from the rental market than if negative gearing was eliminated. This would also mitigate the impact of negative gearing reform on renters.

Our modelling does not focus on the impact negative gearing reform might have on the housing market, house prices, rents, or how investors might respond, but our modelling does show the impact of changing who can claim negative gearing deductions, as well as capping it at different levels.

Home owners who also own at least one rental property receive the highest capital gains tax benefits. Our analysis showed this group has an average property portfolio valued at over A$730,000.

These home owners also have an average taxable income of A$82,000 per person, which is more than 250% of the average taxable income of renters (A$31,000).

We modelled some alternative capital gains tax scenarios reducing the discount – which would increase the tax payable on net capital gains. Our calculations show that reducing the discount would lead to higher income earners paying more capital gains tax.

This would reduce the difference between the tax payable by higher and lower income rental investors, and therefore reduce inequities in the current system.

Author provided

Our modelling shows benefits of negative gearing are skewed towards more affluent investors in middle age and in full-time employment. Investors aged over 55 or who aren’t in the labour market (those who are unemployed, retired or not working) benefit the least from negative gearing.

We need to change the way we tax housing to create a more equitable and sustainable housing market. But this needs to be done (and communicated to investors) in a way that limits the risk of a shock to the market if investors exit the housing market.

Policymakers have been reluctant to change the fundamental settings of the tax system, but our modelling shows it can be done in a way that limits the impact on poorer investors.

The main limitation on this reform is behavioural, determining how investors will react to the effects of tax changes. Housing reform is complex, involving a range of market factors as well as the tax drivers.

Authors: Helen Hodgson, Associate Professor, Curtin Law School and Curtin Business School, Curtin University; Alan Duncan, Director, Bankwest Curtin Economics Centre and Bankwest Research Chair in Economic Policy, Curtin University; John Minas, Lecturer, Griffith University; Rachel Ong, Professor of Economics, School of Economics and Finance, Curtin University

More evidence that negative gearing should be revised was contained in a preliminary paper released recently, having been discussed with the RBA in November. Melbourne University researchers Yunho Cho, Shuyun May Li, and Lawrence Uren suggest their modelling shows that the removal of negative gearing would potentially lift homeownership rates by 5.5%, and that “renters and owner-occupiers are winners, but landlords, especially young with high earning landlords, lose”. They stress this is preliminary, but nevertheless it adds to the weight of evidence that negative gearing should be reformed. Their data also again shows how a small number of affluent landlords are benefiting disproportionately at the expense of the tax payer .

The welfare analysis suggests that eliminating negative gearing would lead to an overall welfare gain of 1.5 percent for the Australian economy in which 76 percent of households become better off.

This is significant, given the annual government expenditure

on negative gearing is estimated to be $2 billion, or 5 percent of the budget deficit for the year 2016. Eliminating negative gearing would reduce housing investments and house prices, and increase the average home ownership rate. The supply of rental properties falls, rents increase but only marginally because its demand also falls.

The data in their report also underlines the significant growth in property investors, and the consequential rise in mortgage lending and negative gearing.

The left panel in Figure 1 shows that the proportion of landlords has risen by around 50 percent over the last two decades. The right panel in Figure 1 shows that the real housing loan approvals have also increased dramatically during the same period. In particular, the loan approvals for investment purposes increased more sharply than that for owner-occupied purposes, surpassing it by around $0.5 billion in the early 2010s.

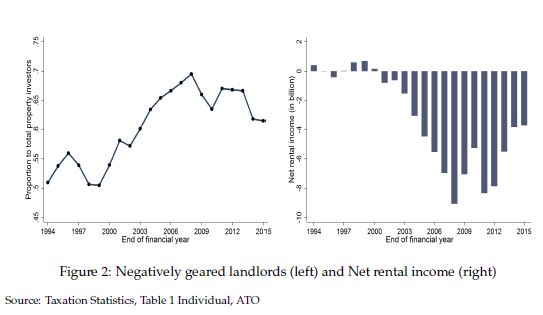

Figure 2 documents the proportion negatively geared landlords and the aggregate net rental income across the period from 1994 to 2015. The left panel in Figure 2 shows that the proportion of negatively geared landlords has increased from 50 percent in 1994 to around 60 percent in 2015. The right panel in Figure 2 shows that the aggregate net rental income became large negative from the early 2000s onwards. Evidence shown in Figures 1 and 2 suggest that Australian households increasingly participate in the residential property investment and take advantage of negative gearing, reducing tax obligations with the flow loss incurred from their housing investment.

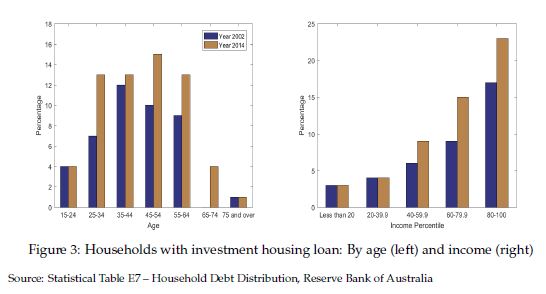

Figure 3 compares the share of households with home loans for investment by age (left panel) and income percentile (right panel) for the years 2002 and 2014. There has been a significant increase in the share, particularly among young to middle-aged households.

The largest increase was occurred in the age group 25 – 35, increased by 85 percent from 7 percent to 13 percent. From the right panel, we find that the share of households with investment housing loans has increased mainly among those in upper income percentiles.

These evidence are in line with the arguments by opponents of negative gearing that the policy essentially benefits the rich households who borrow and speculate in the property market. The fact that the distribution of housing investment loans is different across age and income also motivates our use of a heterogeneous agents incomplete markets model to study the implications of negative gearing.

Finally, of course is the important point, should interest rates rise then the value of negative gearing claimed will rise, putting a heavier burden on the Treasury, at a time when the cost of Government borrowing would be also rising. A double whammy – a multiplier effect.

Labor MPs might be rubbing their hands together with glee at a Treasury memo that shows the federal opposition’s negative gearing policy will have a “small” impact on the property market. But insights from behavioural public policy, as highlighted by the 2017 Economics Nobel laureate – Richard Thaler and his colleague Cass Sunstein, tell us that how people respond to this policy will be more about how the government frames it.

The Treasury memo showed the Labor policy of limiting negative gearing to existing homeowners will have a limited impact as the changes are unlikely to encourage investors to sell quickly. Also, owner-occupiers dominate the housing market and the costs of selling are high.

However, this assumes that people are forward-looking, well-informed, good with numbers and perfectly responsive to new information. Behavioural economics shows us that people do not always think so deeply and logically about their choices.

How any changes to negative gearing are sold to us – as a loss or gain, as a one-off or ongoing, in terms of short versus long term costs and benefits – will impact how Australians react.

Most of us aren’t whizzes with mathematics. As Nobel prize winner Herbert Simon has shown, in place of complex mathematical algorithms we use heuristics. These are simple rules of thumb that draw on our intuitions, experience and gut feel.

Heuristics and biases

One common example of a heuristic is the availability heuristic. This is when we make decisions based on easily available information such as recent events and highly emotive experiences. Our brains work better with narratives and stories than with facts and figures.

Nobel economics laureates George Akerlof and Robert Shiller have applied a similar insight to analyse people’s perceptions of housing market fluctuations. They noted that we hear lots of stories about how house prices are on an upward trend. Via the availability heuristic, we easily remember these emotionally engaging stories, much better than we can remember the dry facts about the history of house price instability and housing market crashes.

This leads us to overestimate the chances of continuing house price rises, and to underestimate the chances of a fall, driving unsustainable house price increases – as witnessed, for example, in the American sub-prime property markets before the global financial crisis.

While heuristics can help us to decide quickly, they sometimes lead us into systematic mistakes – “behavioural biases”. This does not mean that we’re all hopelessly irrational. But for negative gearing it matters how a potential change is framed, and how that fits into our heuristics and biases.

Most economists (including those at Treasury) assume that one dollar is a perfect substitute for any other dollar. Whether we save A$100 via a tax break, win A$100 from a scratch card or earn A$100 from working overtime, it makes no difference.

Contrary to this view, behavioural economics has shown that the way we treat money is different depending on the contexts in which we earn and spend it. We have different “mental accounts” for consumption, wealth, regular income and windfalls. We are more likely to splurge money we’ve won from a scratch card than money we’ve earnt doing overtime.

This is another reason why framing is important. How the government frames a negative gearing change will determine the mental account to which we assign it, and therefore how we respond.

If negative gearing changes are considered a one-off hit – the opposite of a scratch card windfall – then property owners won’t worry so much. On the other hand, if the change to negative gearing is seen as an ongoing drain on our incomes, then they will worry a lot.

Another factor that will come into play is loss aversion – people are much more likely to worry about losses than gains. Evidence from behavioural experiments shows that home-owners over-estimate the value of their properties. This makes them reluctant to sell at reduced prices in a falling market.

It also means that Australians will resist negative gearing changes if these are framed as a loss, creating political pressures for a policy u-turn. It is difficult to predict how people might respond, but behavioural economics shows that any ructions might be avoided if the negative gearing change is framed as a gain.

For instance, Treasury predicts that the additional revenue raised from restricting negative gearing could be up to A$3.9 billion. Therefore, the negative gearing changes could cover more than 80% of federal government expenditure on veterans and their families.

In the long and short term

Treasury’s modelling notes there might be downward pressure on house prices in the short term from changing negative gearing, but that this will be small overall.

But a range of models and experiments have shown that people are disproportionately focused on tangible, short-term outcomes. For example, most of us find it hard to persuade ourselves to go the gym: the short-term costs are inconvenience and discomfort and the benefits seem intangible and distant. This is called “present bias”.

Recent work in behavioural economics confirms that framing (alongside a range of other socio-psychological influences) has a strong impact on our choices. Framing will determine how we perceive the policy, which mental account we will use to process it and how the various heuristics and biases identified by economics and psychologists will play out.

In the debates around negative gearing policy changes, these behavioural insights have not been highlighted. So perhaps Treasury could have added some psychology, alongside the economics, in arguing that house price falls are likely to be limited.

Author: Michelle Baddeley , Research Professor at the Institute for Choice, University of South Australia

The FOI release, which the ABC covered yesterday, highlighted “the Coalition’s phoney defence of negative gearing and capital gains tax discounts before the last election”.

A number of economists at the time disputed the claims that winding back those two tax write-offs would “take a sledgehammer” to property prices because “a third of demand” would disappear from the market.

But as the excellent Rob Burgess has highlighted in the New Daily today, there are two consequential questions which need answering:

The two questions that need answering, is why were Mr Turnbull and Mr Morrison making such obviously false claims, and why were those claims not torn apart by the Canberra press gallery?

The answer to the first question is straightforward. They were either responding to an ideological commitment from the right-wing of their own party room that tax is somehow optional for asset-rich Australians, or they were following the advice of party strategists who could not see them re-winning government if wealthier Australians did not hear them loudly condemning Labor’s plans.

Historians will not doubt tell us which of those it was in years to come.

The answer to the second question is more complicated.

Journalists were not brazenly siding with the banks who had profited so much from the negatively-geared property investment mania, and they were not simply playing partisan politics in favour of a Liberal-led government.

Rather, the get-rich-quick culture of the then 16-year-old property boom, and the gradually normalised claim that tax avoidance is somehow a basic human right, has infected Canberra policy makers and fourth-estate critics alike.

That’s why in 2016 it was so refreshing to hear NSW planning minister Rob Stokes lay out the moral case against these tax write-offs.

He said at the time: “We should not be content to live in a society where it’s easy for one person to reduce their taxable contribution to schools, hospitals and other critical government services – through generous federal tax exemptions and the ownership of multiple properties – while a generation of working Australians find it increasingly difficult to buy one property to call home.”

While he told the truth, his federal colleagues were telling lies.

They lied on behalf of the 10 per cent of Australians who profit from the tax write-offs, and against the interests of the other 90 per cent.

Perhaps now that the nation’s best-equipped economic modellers have highlighted the benefits of these reforms – around $6 billion a year returned to the budget bottom line – the news media will finally call these laws out for what they are.

They are grossly unfair. They have helped pump up the Australian housing bubble. And they have redistributed tens of billions of dollars from poorer to wealthier Australians.

As interest rates start to rise around the world, and the interest-payment write-offs of property investors start to bite even harder into the federal budget, these laws need urgent reform.

A news media that vigorously holds the defenders of these laws to account would be a good start.

The ABC is reporting that a Treasury FOI request has shown that Federal Labor’s negative gearing overhaul would likely have a “small” impact on home values, official documents reveal, contradicting Government claims the policy would “smash” Australia’s housing market.

The previously confidential advice to Treasurer Scott Morrison from his own department said the Opposition’s plan might cause “some downward pressure” and could have “a relatively modest downward impact” on prices.

KPMG warns any increase in Australia’s historically low interest rates would cause serious economic problems and affect households across the entire financial spectrum, from rich to poor.

The industry consultant said one of its biggest concerns is that Australian households have progressively increased debt levels at rates faster than their disposable incomes have grown.

Most notably, KPMG economists highlight some of Australia’s poorest citizens are taking on negatively geared property investments when there’s a clear inability to manage the financial risks.

Analysing the incomes and spending of Australian households over the past 20 years, KPMG said household income has primarily grown because of investment income and government transfers, not rising wages and salaries.

The firm added that more than one-third of the income of the poorest 20% of Australian households is received through government transfers.

Its report finds the bottom 20% of households recorded the highest rate of growth in investment income, at 8.5% per annum, compared to an average of 2.3% over the past decade for other households.

KPMG Australia chief economist Brendan Rynne said: “While it is perhaps understandable that the poorest members of our society want to diversify and increase their incomes, this group is the least able to take on the financial risk associated with geared investment activity.”

The second 20% of lowest-income households, or those slightly better-off, are getting relatively more than the lowest bracket in terms of (government) dollar transfers received per dollar tax paid. KPMG said this suggests policies to deliver welfare to the poorest members of society are less effective than to slightly better-off recipients.

“The proportion of households that end up paying no net tax – but via an administratively costly money-go-round of paying income tax and then getting it all or more sum back via income support payments, has now reached 60%,” Rynne said.

He says the answer is not further ratcheting up marginal tax rates for higher tax earners.

“Our analysis shows that the top 20% of households already pays 50% more income tax than the bottom 80% combined,” he said.

The federal government is considering limiting the number of properties investors can buy, as it struggles with ways it can reign in property prices in booming markets only a few weeks out from the May budget.

According to an article in The Australian Financial Review, the government is looking at ways it can cap the value of tax breaks for property investment as it tackles housing affordability problems, which vary widely around the country.

Since 2012-2013, there has been a 9.2% increase in the number of property investors that own five or more properties, according to The Guardian’s analysis of recent Australia Tax Office data.

The federal government has ruled out getting rid of negative gearing according to Labor’s policy, and has indicated that it will consider more ‘surgical’ measures.

The government appears to have moved away from an earlier idea to allow first-home buyers to access their superannuation funds to accumulate enough money for a deposit.

Malcolm Gunning, president of the Real Estate Institute of Australia, told SCHWARTZWILLIAMS the percentage of investors in the market that own three or more investment properties is only very small, and therefore capping the number of properties those investors can own is only “clipping around the edges”.

Gunning said capping the number of properties investors could own would mainly be “political posturing”, and warned it could decrease the supply of new properties coming onto the market, which in turn could cause rents to rise.

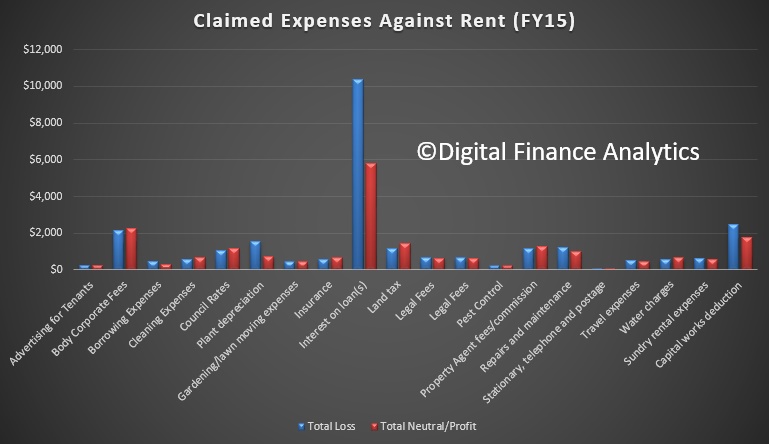

The ATO released their summary FY15 data this week, and included quite comprehensive summaries of the range of costs those with rental properties have offset income. They also divide rentals into those functioning at a loss, and those who make a profit.

Of the 2.9 million rentals, 1.1 million made a profit, the rest a loss (which can be offset against other categories of income). That means 60% of rentals are under water.

We can also see the categories of costs claimed and the average amounts. Not all households claim all categories.

Significantly, the major factor between loss and profit is the interest amount. Those reporting a loss had bigger interest payments (presumably larger loans?). But it is also worth looking at the 20 categories (yes 20!!) which can be claimed. Behold the wonders of our generous tax system, and the reason why so many do not want it to stop.

Blog")