KiwiSaver default funds have been banned from investing in fossil fuels and certain weapons under new legislation. Via InvestorDaily.

Default

funds will be banned from investing in fossil fuel production to negate

the risk of New Zealanders’ retirement savings being invested in

stranded assets as the world moves to reduce emissions.

“No

New Zealander should have to worry about whether their retirement

savings are causing the climate crisis,” said Climate Change Minister

James Shaw.

“That’s why our government is moving default KiwiSaver funds away from fossil fuels, putting people and the planet first.”

KiwiSaver

members are allocated to a default provider if they don’t actively

choose a KiwiSaver fund when commencing their employment. Around 690,000

people remain in a default fund, with approximately 400,000 of those

having not made an active choice to stay there.

The New Zealand government also believes that the switch to more responsible investment will also improve member outcomes.

“In

2017, the $47 billion NZ Superannuation Fund adopted a climate change

investment strategy that resulted in it removing more than $3 billion

worth of stocks that exceed thresholds for either emissions intensity or

fossil fuel reserves, without negatively affecting performance,” said

Commerce and Consumer Affairs Minister Kris Faafoi.

“So we know that moving away from investments in fossil fuels doesn’t have to mean lower returns.”

The

changes will also prevent default fund providers from investing in

weapons like cluster munitions and anti-personnel landmines (which are

subject to the Convention on Cluster Munitions and the Ottawa Treaty

respectively). While default fund providers were already moving away

from investment in weapons, the changes now enshrine that requirement in

default fund settings.

The Reserve Bank of New Zealand today released its final decisions following its comprehensive review of its capital framework for banks, known as the Capital Review. The trajectory will be over a longer period, with more flexibility, but the banks will still need to hold more capital.

Governor Adrian Orr said the

decisions to increase capital requirements are about making the banking system

safer for all New Zealanders, and will ensure bank owners have a meaningful

stake in their businesses. The changes will be implemented over seven years,

giving plenty of time for banks to manage a smooth transition and minimise any

adjustment costs.

“Our decisions are not just

about dollars and cents. More capital in the banking system better enables

banks to weather economic volatility and maintain good, long-term, customer

outcomes,” Mr Orr says.

“More capital also reduces

the likelihood of a bank failure. Banking crises cause not only harmful

economic costs but also distressful social issues, such as the general decline

in mental and physical health brought about by higher rates of unemployment.

These effects are felt for generations,” Mr Orr says.

The key decisions, which start to take effect from 1 July 2020, include banks’ total capital increasing from a minimum of 10.5% now, to 18% for the four large banks and 16% for the remaining smaller banks. The average level of capital currently held by banks is 14.1%.

Relative to the Reserve

Bank’s initial proposals, the final decisions also include:

More flexibility for banks on the use of specific capital instruments;

A more cost-effective mix of funding options for banks;

A lesser increase in capital for the smaller banks consistent with their more limited impact on society should they fail;

A more level capital regime for all banks – with the four large banks having to measure the risks of their exposures (lending) more conservatively, more in line with the smaller banks; and

More transparency in capital reporting.

The adjustments to the original proposals reflect our analysis and industry feedback over the past two years. All of these changes will be phased in over a seven-year period, rather than over five years as originally proposed, in order to reduce the economic impacts of these changes.

Deputy Governor and General

Manager of Financial Stability Geoff Bascand says the decisions were shaped by

valuable public input and insight received through an unprecedented number of

submissions as well as public focus groups. Three international experts also

provided supportive perspectives on the proposals.

“We’ve listened to feedback

and reviewed all the data, and are confident the decisions are the right ones

for New Zealand,” Mr Bascand says.

“We have amended our

original proposals in a number of ways so we achieve a high level of resilience

at lower potential cost, with a smoother transition path for all participants.

Our analysis shows that the benefits of these changes will greatly outweigh any

potential costs.”

“Following the Global

Financial Crisis, many regulators around the world have been taking steps to

improve the safety of their banking systems. We’re confident we have the

calibrations right for New Zealand conditions. These changes will be subject to

monitoring, with the Reserve Bank reporting publicly on implementation during

the transition period,” Mr Bascand says.

The Australian Prudential Regulation Authority (APRA) has launched a review of the capital treatment of authorised deposit-taking institutions’ (ADIs’) investments in their banking and insurance subsidiaries. It is open for consultation until 31 January 2020. APRA intends to finalise the changes to the Prudential Standard in early 2020 with the updated Prudential Standard to come into force from 1 January 2021.

At first review, this looks like some of the Australian majors will large New Zealand subsidiaries will need to hold more capital (which costs), or shrink their off-shore operations in New Zealand. But more analysis will be required to determine the true impact relative to their Australian businesses and capital holdings.

This review was prompted in part by recent proposals by the Reserve

Bank of New Zealand (RBNZ) to materially increase capital requirements

in New Zealand. The RBNZ’s proposals and APRA’s processes are a natural

by-product of both regulators working to protect their respective

communities from the costs of financial instability and the regulators

continue to support each other as these reforms are developed.

APRA is proposing to change the capital treatment for these exposures

and this particular proposal is the most significant amendment to APS

111. In developing the proposal, APRA has considered long-established

trans-Tasman arrangements provided for in the Australian Prudential

Regulation Authority Act 1998 and the RBNZ’s enabling legislation, under

which the agencies assist each other in the performance of their

regulatory responsibilities. This is particularly important given the

four major Australian banks are the shareholders of the major banks in

New Zealand.

APRA’s capital requirements currently permit ADIs to leverage their investments in banking and insurance subsidiaries, whether domestic or offshore, and as such do not require dollar-for-dollar capital for these investments at the parent company level. This treatment raises the risk that capital held by the parent ADI is not sufficient to support risks to its depositors. Any reforms by other regulators to materially increase their capital requirements, including those proposed by the RBNZ, could exacerbate this risk.

At current levels of equity investment, APRA estimates the existing treatment provides an uplift to the average Common Equity Tier 1 (CET1) Capital ratio across the four major Australian banks of around 100 basis points for their equity investments in New Zealand banking subsidiaries. As a consequence, capital available to support risks to Australian depositors could be overstated.

As APRA is more concerned about large concentrated exposures, it is proposing to limit the amount of the exposure to an individual subsidiary that can be leveraged to 10 per cent of an ADI’s CET1 Capital. This means capital requirements are increasing for large concentrated exposures, as amounts over the 10 per cent threshold would be required to be met dollar-for-dollar by the ADI parent company. APRA is less concerned about small equity exposures in banking and insurance subsidiaries and so capital requirements will decrease for small exposures. Amounts under the 10 per cent threshold would be risk weighted at 250 per cent and included as part of the related party limits detailed in APRA’s recently finalised Prudential Standard APS 222 Associations with Related Entities (APS 222).

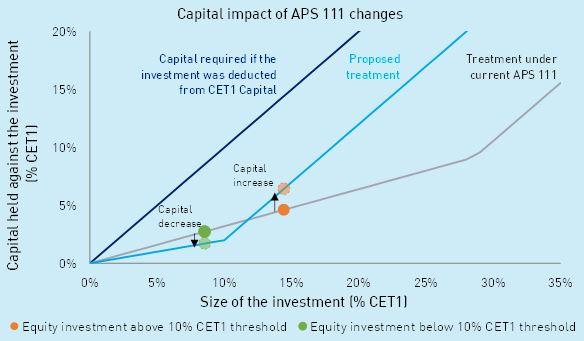

The diagram outlines the boundaries between a full

deduction approach (dark blue line), the current treatment (grey line)

and the treatment proposed in this Discussion Paper (light blue line).

These represent the boundaries that balance the size of the investment

with the capital required under the limits in APRA’s prudential

framework for equity investments (APS 111) and related entities (APS

222).

A full deduction approach will result in

dollar-for-dollar capital for this investment, regardless of the size of

the investment. The treatment under the current APS 111 is a 300 per

cent (if the subsidiary is unlisted) or 400 per cent (if the subsidiary

is unlisted) risk weight for this investment. The proposed treatment in

this Discussion Paper for this investment will depend on the size of the

investment; for an equity investment below 10 per cent CET1 Capital,

the investment is risk weighted at 250 per cent, with amounts above the

10 per cent CET1 Capital threshold deducted from CET1 Capital. Under the

proposed treatment, capital requirements are decreasing for small

exposures and increasing for large concentrated exposures.

APRA has calibrated the proposed capital requirements so they are

broadly consistent with the Basel treatment of a banking group’s equity

investments in non-consolidated financial entities, and also with the

current capital position of the four major Australian banks, in respect

of these exposures (i.e. preserving most of the existing capital

uplift).

APRA is not proposing a full dollar-for-dollar capital requirement for an ADI’s equity investments in these subsidiaries, in recognition of the benefits of subsidiaries that are subject to prudential regulation, and that ownership of banking and insurance subsidiaries generally provides some beneficial diversification. However, as these exposures increase in size, the concentration risk associated such investments start to outweigh the diversification benefits. Requiring dollar-for-dollar capital for amounts above 10 per cent CET1 Capital reduces the risks to Australian depositors of increasing levels of these exposures.

The finalisation of the RBNZ’s proposed capital reforms, will, in all likelihood, require higher capital requirements for banks in New Zealand. Should Australian ADIs fund higher capital requirements in New Zealand by retaining the profits of their New Zealand subsidiary banks in those subsidiaries, no material additional capital, in aggregate, is likely to be required by Australian ADIs.

Other proposed changes to APS 111 include:

promoting simple and transparent capital issuance by removing the

allowance for the use of special purpose vehicles (SPVs) and stapled

security structures; and

clarifying and simplifying various parts of APS 111, which comprise the bulk of the proposed changes.

APRA does not consider its proposal to remove the use of SPVs and

stapled security structures as material as these structures have not

been a feature of ADI capital issuance since 2013 and, in the case of

stapled security structures, less attractive for ADIs under the Basel

III capital reforms.

APS 111 is open for consultation until 31 January 2020. APRA intends to finalise the changes to the Prudential Standard in early 2020 with the updated Prudential Standard to come into force from 1 January 2021. APRA is open to working with impacted ADIs on appropriate transition.

Cash system participants and the wider public are being

asked for their views about the Reserve Bank of New Zealand taking a more

active role in the cash system.

A consultation paper has been released today as part of the

Bank’s ongoing Future of Cash – Te Moni Anamata programme which is considering

the implications for New Zealanders of falling cash use for every-day

transactions, including the impacts on the system that supplies, moves and

stores it.

Assistant Governor Christian Hawkesby says the Reserve Bank

is just one cog in a cash system machine which includes the banking system,

armoured truck companies, retailers, and independent ATM providers. “We see

roles for all parts of the system – along with interest groups, whānau and

individuals – in ensuring people who want or need to access or use cash can do

so.”

The consultation paper proposes that the Reserve Bank take

on a stewardship role in the cash system, providing system-wide oversight and

coordination. It also proposes two tools which, though not currently required,

may be needed in the future to respond flexibly to changes in the cash industry

and the evolving needs of the public:

The Reserve Bank be given the power to set standards for machines that process and dispense cash.

The Reserve Bank Act set out regulation-making powers that enable the government and the Reserve Bank to require banks to provide access to cash deposits and withdrawals.

“These proposals are not the complete answer, but they would

help create a foundation for the Reserve Bank to be more than the issuer of

notes and coins when it comes to how we use cash which is an important

component of our social and economic activity,” Mr Hawkesby says.

Mr Hawkesby says the Reserve Bank is grateful to the large

numbers of individuals, groups, banks and other cash system providers, business

and community organisations, and public sector agencies who are participating

in the Future of Cash programme and sharing their views.

“Nearly 2400 individuals and groups gave feedback on our

earlier issues paper discussing the potential impacts from a fall in cash use,

particularly for people who are already financially or digitally excluded for

whatever reasons. Meanwhile 3100 people randomly selected from the electoral

roll have responded to a scientific survey updating our understanding of how New

Zealanders are using cash and how this use is changing. We expect to publish

results from both these efforts in November, and these will also feed into

final recommendations in respect of the proposals released today.

”The changes in our latest consultation document would have

significant consequences for all participants in the cash system. Banks,

cash-in-transit providers, independent ATM operators, and the broader retail

sector would likely be particularly affected. We want to continue to hear views

and feedback from everyone about the purpose and desired attributes for the

mechanics of the cash system, and how we could collectively improve it,” says

Mr Hawkesby.

The paper is published on the The Future of the Cash System – Te Pūnaha Moni Anamata page, and feedback closes on 6 November 2019.

The Reserve Bank of New Zealand (RBNZ) and Financial Markets

Authority (FMA) today released their findings on life insurers’ responses to

the joint Conduct and Culture Review.

Overall, the regulators were

disappointed by the responses. Significant work is still needed to address the

issues of weak governance and ineffective management of conduct risk,

identified in the regulators’ report earlier this year.

Rob Everett, FMA Chief

Executive, said: “While we’re disappointed, we’re not surprised as the

responses confirm what we found in our original review. It’s clear that

progress has been slow and not as far-reaching as required.

Some providers have started

work to identify the customer and conduct issues they face, others have not

provided any detail on this.”

Sixteen life insurers were

asked to provide work plans outlining the steps they will take to improve their

existing processes and address the regulators’ findings and recommendations.

There was wide variance in

the comprehensiveness and maturity of the plans provided.

Adrian Orr, Reserve Bank

Governor, said, “We’re disappointed the industry’s response has been

underwhelming. The sector has failed to demonstrate the necessary urgency and

prioritisation, around investment in systems, to provide effective governance

and monitoring of conduct risk.”

There was also a wide

variance in the quality and depth of the systematic review of policyholders and

products. Some did not complete this exercise and others did not provide data

on the number of policyholders affected or the estimated cost of remediation

activities. Insurers that completed the exercise identified at least 75,000

customer issues requiring remediation, with a value of at least $1.4 million.

Some of the new issues identified included:

Overcharging of premiums and benefits not being updated due to system errors, human errors and under-reporting of deaths

Poor customer conversations overlooking eligibility criteria and poor post-sale communications, which lead to declined claims and underpayment of benefits

Poor value products were identified, where premiums charged were not fair value for the cover provided.

Sales incentives and

commissions

The FMA and RBNZ committed

to report back on staff incentives and commissions for intermediaries. Previous

reports by the FMA reflected the concerns with conflicted conduct associated

with high up-front commissions and other forms of incentives, (like overseas

trips) paid to advisers.

Although some insurers have

committed to removing sales incentives for employees and their managers, not

all committed to removing or altering indirect sales incentives.

Those providers that have

removed sales incentives for employees don’t typically use external advisers to

distribute products. Providers using external advisers told the regulators that

changing long-held business arrangements and distribution models is difficult

and will take time to implement.

Mr Everett said, “We’re

ready to work with life insurers to ensure they prioritise their focus on

serving the needs of their customers, while at the same time balancing the need

to remunerate advisers for the important work they do to help these customers.

But we do not think high up-front commissions create confidence that insurers

and advisers are acting in the best interests of customers.”

Mr Orr said, “Good

governance within insurance firms requires the effective management of conflicts

of interest. We need to see much better systems and controls in place to manage

the inherent conflicts where advisers or sales staff are offered incentives to

sell or replace insurance policies.”

Next steps

Those companies that have

not undertaken comprehensive systematic reviews of policyholders and products

have been asked to complete further reviews of their systems to identify

issues, and to develop mature plans to respond and remediate any of their

findings. These plans must be completed by December 2019.

The FMA and RBNZ will

continue to monitor how the insurers are responding to recommendations and

implementing their work plans. Life insurers are currently not legally required

to become more customer-focused and the FMA and RBNZ found that the sector has

a weak appetite for change.

Deficiencies in some of the

plans received, and some insurers’ lack of commitment to implementing the

regulators’ recommendations, further demonstrates the need for additional

obligations to be included in the regulation of conduct of life insurers.

Non-bank lender Pepper Money has launched mortgage lending operations in New Zealand, offering advisers in New Zealand the technology and tools to write its prime, near-prime and specialist loans. Via The Adviser.

Following more

than a year of consultation with advisers and intermediaries, lending

partners, regulators and borrowers, Pepper Money has today (16

September) opened its business in New Zealand.

This builds on the international reach of the non-bank lending group, which already operates in Australia, the UK, Spain, Ireland and Asia.

New Zealand-born Aaron Milburn,

Pepper Money’s director of sales and distribution in Australia, will

head up the New Zealand business from today. His new job title will be director of sales and distribution for Australia and New Zealand.

Speaking to The Adviser about the new

business, Mr Milburn said that Pepper Money will primarily distribute

through the third-party channel, as it does in Australia.

Mr Milburn added that while while the

company may look to launch mortgages directly in future, “the initial

plan – and for the foreseeable future – is to utilise the adviser

network over there”.

He explained: “We will initially

distribute through the adviser network in NZ through all of the major

aggregators that operate in New Zealand.

“Pepper’s business is 95 per cent

driven through brokers in Australia and in the UK, and we see no need to

change that model as we enter NZ.”

He continued: “We think that advisers

do a wonderful job in New Zealand, and we would like to continue to

support that area of distribution as we enter NZ, as we do in

Australia.”

Mr Milburn told The Adviser that his

first priority in his expanded role will be to launch the suite of

products in New Zealand and “deliver what advisers have been asking for

at our various feedback sessions and study tours”.

According to the director of sales and distribution for Australia and New Zealand, this largely focuses around filling a “significant

gap in the near-prime space in New Zealand, where families are

potentially paying too much or have been in the wrong products due to a

lack of choice” and providing advisers with supporting tools to help

deliver these products.

He explained: “We had advisers in New

Zealand contacting Pepper asking us to go over there and really inject

some competition into the market and make it easier for advisers and,

ultimately, Kiwi families to realise their goals.”

Pepper Money will therefore also offer advisers the Pepper Product Selector (PPS)

tool in New Zealand, which will enable brokers to “get indicative

offers for their customers in under two minutes”, as well as a “fully

online integrated submission platform for brokers,” the marketing

toolkit, the social media toolkit and the Pepper Insights Roadshow.

Pepper Money to pay trail

Notably, while the majority of lenders in New

Zealand went through a “no trail” period starting in 2006 (when

payments went from 0.65 of a percentage point in upfront commission plus

0.20 of a percentage point in trail commission to an average of 0.85 of

a percentage point in upfront only), several lenders have begun returning to trail commission to reduce instances of churn.

According to Mr Milburn, Pepper Money in New Zealand will be offering advisers an upfront and trail commission.

He told The Adviser: “Overwhelmingly, the feedback was that an upfront and trail model was preferred.

“A number of banks have either

re-implemented trail in NZ or are looking to in the near future, so we

took the opportunity to put trail back into the New Zealand market with

our products.”

Mr Milburn concluded that the new operation in New Zealand would build on the practice and service offerings built in Australia.

He said: “We will continue to deliver

the level of service and solutions that we do today and continue to

really focus on that technology improvement side of things.

“We want to make it easier and faster

for brokers to provide solutions for their customers and help build

their brand out in the community and the focus will continue in the back

end of 2019 to 2020.”

An important discussion about credit creation, why banks are talking interest rates down, and what economists are prepared to say and what they are not, courtesy of Joe Wilkes. Refers to my earlier post:

Blog")