Nucleus Wealth’s Head of Investments Damien Klassen, Head of Operations Tim Fuller, as well as ex-fund manager, Analyst, and blogger Kevin Muir of ‘The Macro Tourist’ discuss ‘Is Inflation back from the Dead?’

Topics this week include a background on world markets and why growth and inflation have been so stagnant, Modern Monetary Policy, why Kevin believes inflation is just around the corner and the best option to deal with global debt, and their outlook on where China and Australia’s economy moving to.

The information on this podcast contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen and Tim Fuller are an authorised representative of Nucleus Wealth Management. Nucleus Wealth is a business name of Nucleus Wealth Management Pty Ltd (ABN 54 614 386 266 ) and is a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796.

Note: DFA has no commercial relationship with Nucleus.

In the latest from Nucleus Wealth, Head of Investment Damien Klassen, and Head of Operations Tim Fuller, chat with Economist and Hon. Prof. of the University College of London, Steve Keen.

Topics include credit creation and its limits, weighing up its pro’s and con’s, central banks reaching the end of the road for interest rate cuts with debt being at near record highs, the drivers of weak demand and inflation globally, Modern Monetary Theory (MTT) and its differences with Keynesian Stimulus, which countries are closest to incorporating MMT, Steve’s ideas for central banks depositing directly into citizens bank accounts and “Universal Basic Carbon.” Nucleus Wealth is a Melbourne based investment house that can help you reach your financial goals through transparent, low cost, ethically tailored portfolios.

Disclaimer: The information on this podcast contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen and Tim Fuller are an authorised representative of Nucleus Wealth Management. Nucleus Wealth is a business name of Nucleus Wealth Management Pty Ltd (ABN 54 614 386 266 ) and is a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796

Courtesy of Nucleus Wealth’s Damien Klassen. Damien runs the investment side of Nucleus, selecting stocks suggested by analysts and implementing the asset allocation

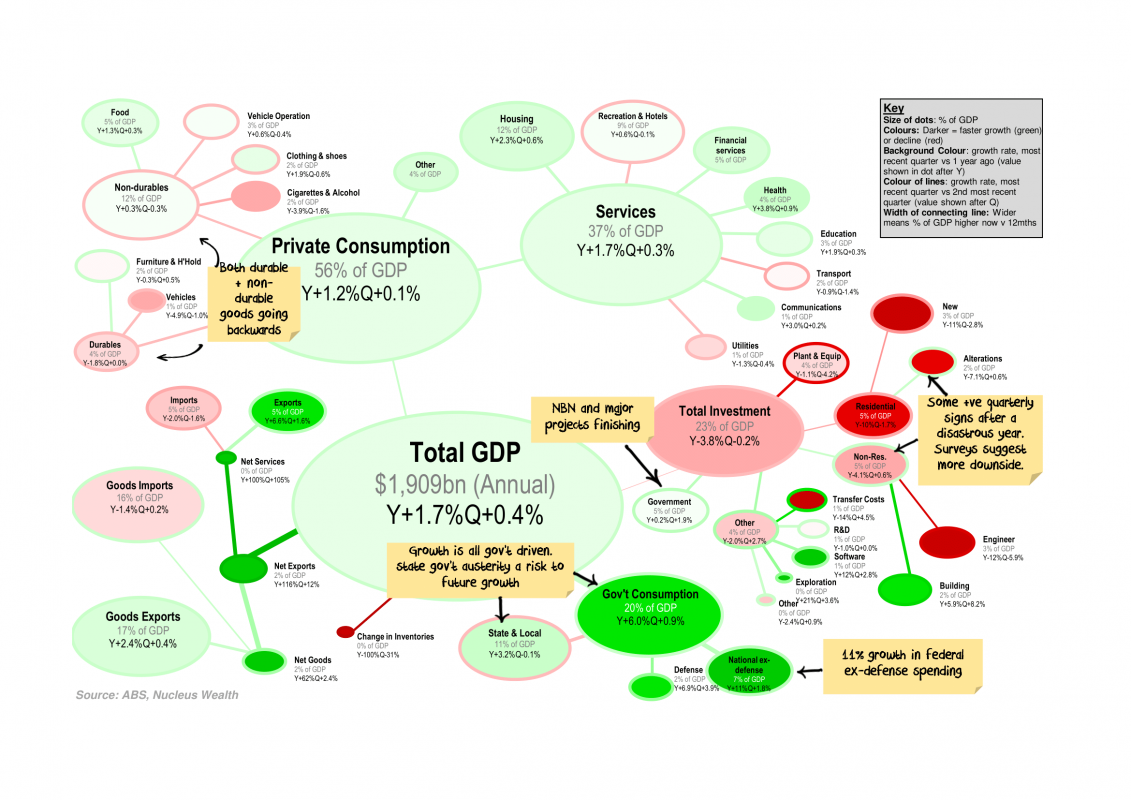

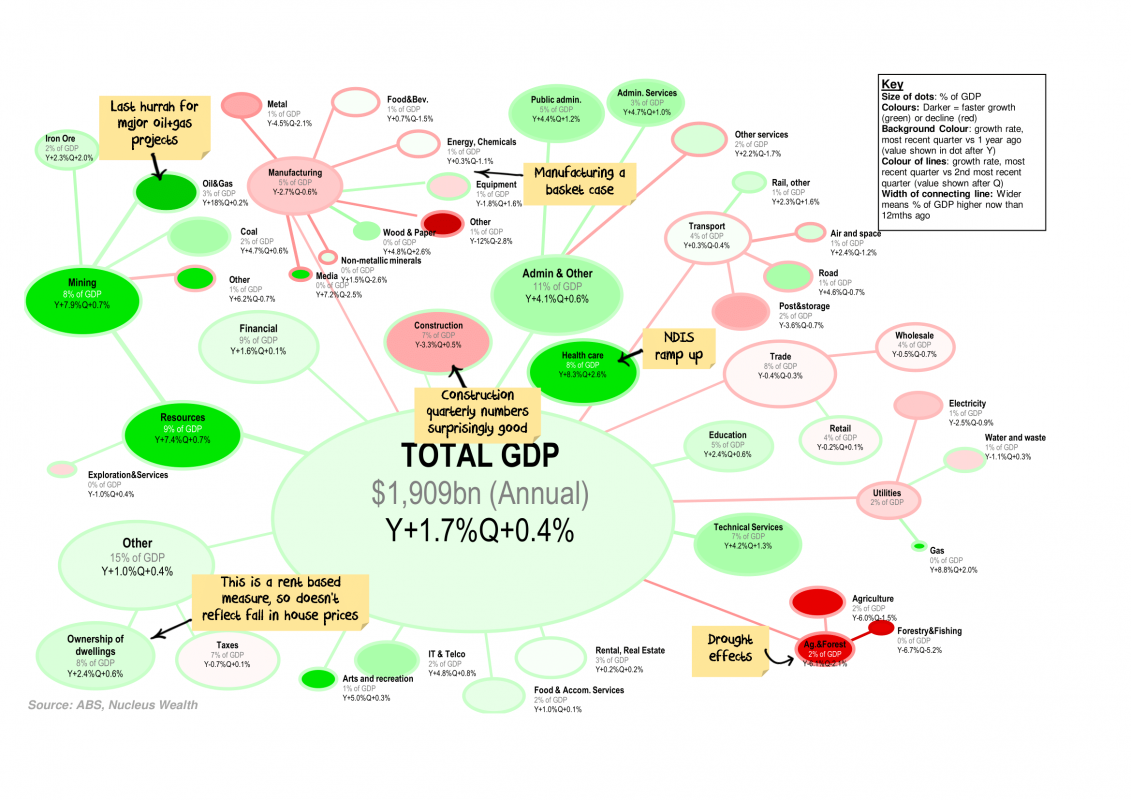

Every quarter I like to look at the changes in Australian GDP

and which categories are responsible for the growth / decline. Each

bubble represents a category of GDP proportionate to its size, colours

represent the growth rate.

Click the charts for a large version and commentary:

Federal Government spending (+11% for non-defence, 7% for defence over the year) the only thing keeping GDP above zero.

Investment

growth was not good, but I was expecting worse. Possibly there are

green shoots, but capex surveys and investment forward indicators

suggest there is still more downside.

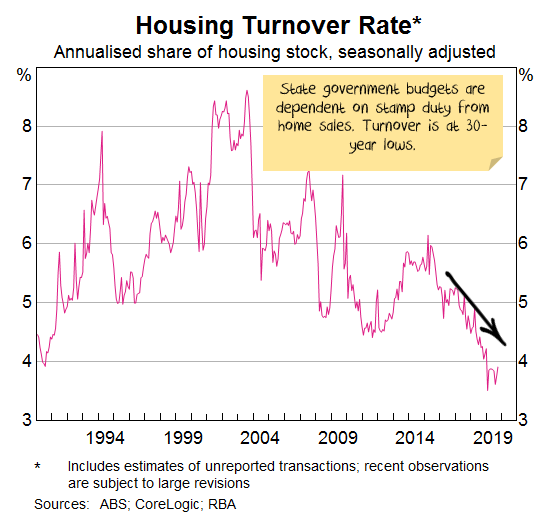

State & Local

government spending has turned negative – with a low number of property

transactions this is likely to remain a feature

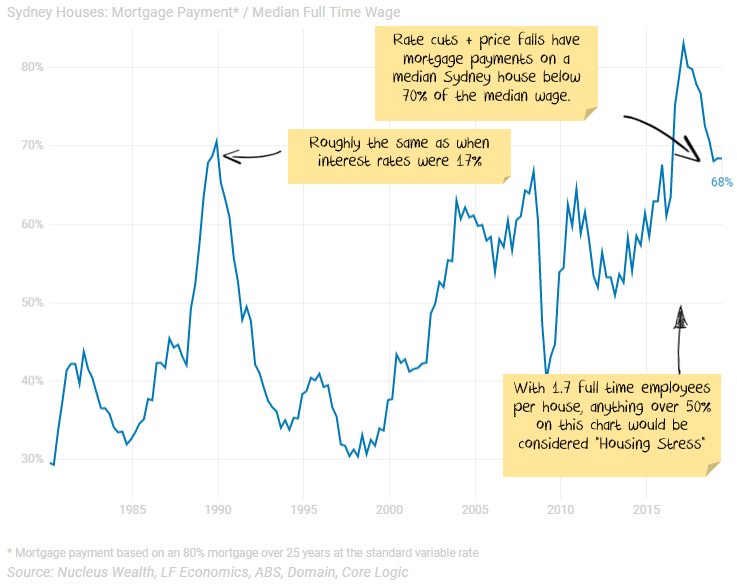

Damien Klassen from Nucleus Wealth penned this recently. It is an excellent summary of the critical issue in play – Can rising house prices drive the rest of the economy on their own without a construction boom? Note the disclaimer below.

I’ve written a few times recently about the imbalances in the Australian economy and how messed up the Australian housing cycle

is. It looks as if the Australian economy is hanging on to positive

growth based on one factor. Without that factor, there is significant

economic downside. The one economic question that matters:

Can rising house prices drive the rest of the economy on their own without a construction boom?

There are three main areas to indicate if this is the case. Two have come out with more negative data since I last posted. One is a glass half empty: better current conditions, worse future conditions.

Upside Case

Can rising house prices drive the rest of the economy on their own without a construction boom?

For

the optimists, the answer is a resounding yes. House prices have not

only stopped falling but have risen over the last few months. Buyer

queues are out the door for limited supply which will inevitably mean

rising house prices. And Morrison’s 95% lending for first home buyers

hasn’t even begun yet. Investors will follow first home buyers, which

will lead prices higher and then upgraders will start buying again.

Rising property prices will mean consumers will start spending once

more, construction will recommence, and a new Australian economic growth

cycle will begin.

It would appear that the Federal Government has this belief.

Downside Case

Can rising house prices drive the rest of the economy on their own without a construction boom?

The

poorer arguments mounted by pessimists tend to have a moral angle:

house prices are too high for children to afford, they will have to come

down to a level that an ordinary person on a regular salary can afford.

If that occurs, house prices will fall 30-40%. While these arguments

are compelling from a social justice perspective, or on a long term

basis, the same arguments have been valid for 15 years. Timing is

important:

Other

weak arguments base the downturn on extrapolating no intervention from

governments. We know the current government is hell-bent on intervening

in the housing market.

The

better argument is that even if construction approvals rebound,

employment would fall for at least another year as the construction

decisions made over the past two years affect the number of people

employed. And construction approvals are not rebounding.

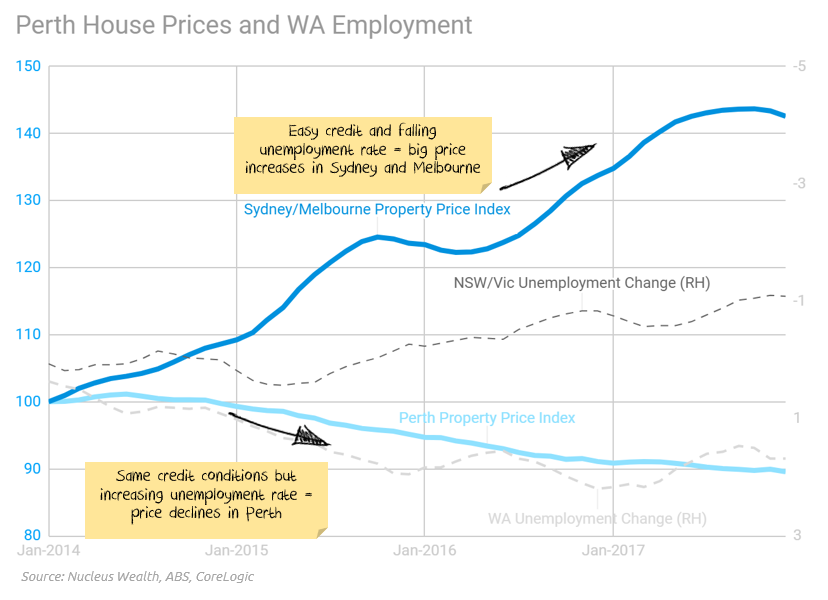

Rising

unemployment in Perth led to a 10% house price fall in the 2012-2017

period while Sydney/Melbourne house prices boomed. What is to stop the

same fate for Australia as a whole?

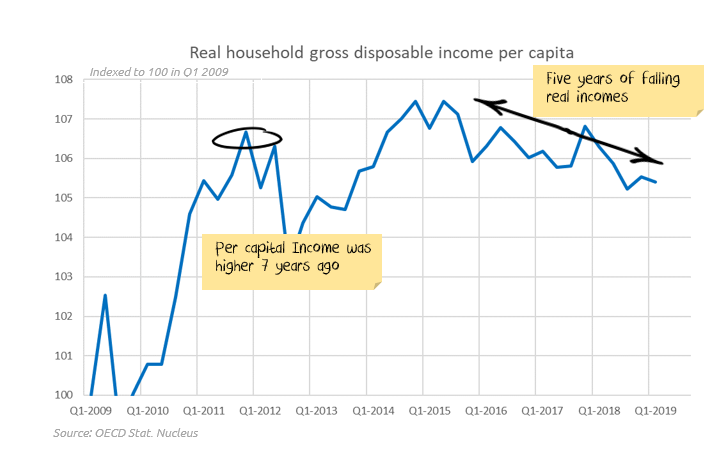

Per capita income has gone nowhere for 7 years, so it is hard to see any rescue coming from that front:

If

rising unemployment does mean house prices fall further, then there are

a range of probable adverse effects. There are some seriously negative

economic effects if the effects snowball. And we won’t even get started

about the impact on a fragile Australian housing market if an

international shock (Brexit, Trade wars, Hong Kong unrest, corporate

debt accidents, European recession) hits.

It doesn’t need to be one or the other

You

don’t need to buy into the entire negative story to be cautious. If

employment holds up, then the positive story has a chance (assuming

benign international conditions). But, if unemployment rises, then

Australia won’t need a global shock to see house prices resume a

downward path.

When

presented with an asset class that has limited upside in positive

scenarios and significant downside in adverse scenarios, I usually opt

to avoid the asset class and look for returns elsewhere.

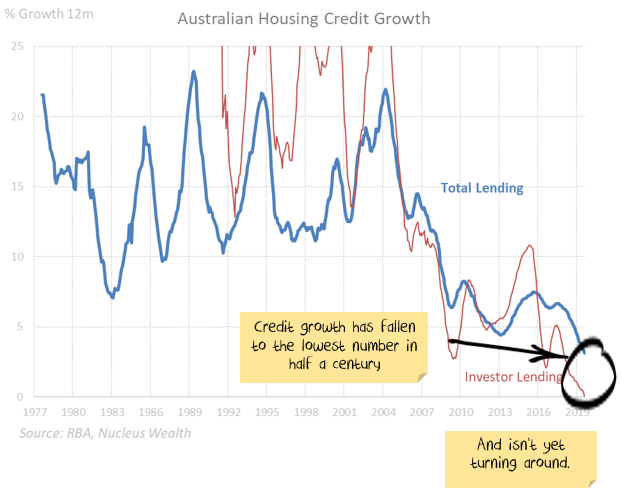

Update 1: Australian Credit growth:

The

Royal Commission into banking reversed the credit boom and was enough

to see house prices down around 10%. This came even while most other

factors affecting house prices were still positive.

Will

the Morrison government manage to get the already over-levered

Australian households to take on even more debt? If I am too bearish,

particularly in the short term, this is where you will see the effects.

So far there are none:

On

the regulatory front, the Westpac v ASIC responsible lending court case

win for Westpac has the potential to lead to easy lending conditions.

ASIC is taking the case to the Federal court, so we are in limbo for

some time.

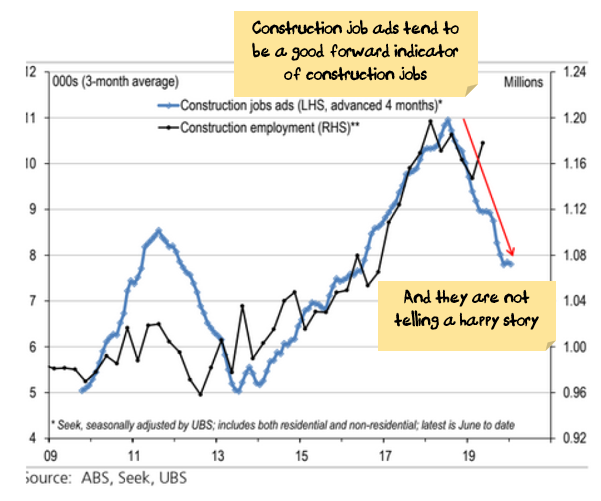

Update 2: Unemployment

There

is not enough space here to go into the detailed links between house

prices and unemployment. Indicatively, during the 2012 to 2017 housing

boom years, the Perth market faced mostly the same factors as

Sydney/Melbourne except for (a) slightly weaker population growth and

(b) rising unemployment. And Perth property prices fell more than 10%

while the rest of Australia boomed.

We are expecting considerable job losses in the construction sector.

Having

said that, construction jobs have been resilient so far. Forward

indicators (job ads and approvals) continue to point to sizeable job

losses.

Source: ABS, Seek, UBS

Add

to this scenario, job losses from state government austerity as budgets

have been struck by falling transaction numbers in the housing market:

Finally,

any global shock (trade wars, recessions, debt crises) is likely to be

transmitted to the housing market through higher unemployment.

Update 3: Foreign Buyers

Foreign demand was substantial for both the boom and the bust:

China

cracking down on its capital account and deteriorating relations

between Australia and China suggests foreign investment will remain low.

The question is whether Hong Kong unrest translates to increased demand for Australian property.

The Answer

So, the answer to the one question

Can rising house prices drive the rest of the economy on their own without a construction boom?

will be found in whether increases in unemployment remain contained.

I’m skeptical. But if I’m wrong, the charts above will be where we will see the signs.

Recent data suggest my skepticism is warranted.

Disclaimer

This blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796.