The open banking regime officially began yesterday with the four major banks offering data on a variety of products as part of the regime’s roll-out, via InvestorDaily.

The

four major banks had a deadline of 1 July to make product data

available on all credit and debit card, deposit and transaction accounts

with more products to follow.

By February, first mortgage data

will have to be available, with eventually all products being available

for the major banks by 2020. 1 July 2020 is the start date for all other

banks to begin offering their credit and debit card product data with

an end date of 2021.

Customer data will be included in the regime

by 1 February 2020, which will allow consumers to more fully control

their data and enable greater transparency and competition throughout

the industry.

Open banking has been sweeping across the world, with the most relatable example for Australia being the UK open banking regime.

The

UK introduced theirs following an exposure of poor practice, not

dissimilar to Australia. Where it differs though is that the UK regime

applies to only nine banks, whereas Australia’s will apply to all ADIs.

The

Australian regime only grants read-only access to data with reciprocal

obligations and an eventual plan to open to other industries, such as

utilities.

What it will eventually mean is that customers of a

bank can request or give consent for their data to be shared with an

accredited third party, such as a bank, financial services provider,

utility provider or a telecommunications provider.

The regime will

break down the barriers consumers have faced in finding the best

banking products and eventually switching to that provider.

Commonwealth

Bank’s general manager of digital banking, Kate Crous, told Investor

Daily that the bank was supportive of the model that puts customers in

control and had worked hard to ensure they were ready.

“We have

worked hard with regulators and other industry participants to ensure

the Consumer Data Right regime will be successful, particularly in

building consumer trust and confidence around the use and exchange of

their data.

“The first milestone is publishing product information

via an application programming interface (API) from 1 July 2019. This

will enable an easier comparison of banking products from financial

institutions and allow the industry to test the APIs before sharing

consumer data next year,” she said.

Ms Crous said developers are now able to access information on how to integrate with the CBA APIs.

Westpac’s chief data and strategy officer, Jamie Twiss, said keeping data safe was crucial and the pilot was an important step.

“Westpac

is focusing on creating a trusted open banking regime that is secure,

flexible and easy to use for all Australians. The pilot program will lay

initial foundations to test the performance, reliability and security

of the system before any personal consumer data is shared. It will also

give software developers and fintechs a network of financial

institution’s data to build and improve financial services.”

Westpac

will provide generic information on product data as of today, which

will include interest rates, discounts, eligibility criteria, product

features and descriptions plus fees and charges.

A NAB

spokesperson told Investor Daily that their focus was on ensuring that,

as an industry, open banking worked for the consumer.

“This is a

complex change to the industry and the timelines are challenging, but we

firmly believe that speed shouldn’t compromise safety and customer

experience; getting it right is paramount to consumer trust and

confidence in the system,” NAB said.

The spokesperson

said NAB had actively started to develop processes since back in 2017 to

be ready for open banking and would continue to work with Data 61 and

ACCC.

Fintech response

Deputy chief

executive of neobanks Volt Luke Bunbury said it will mean that the

incumbent banks will need to innovate to compete with newer entrants.

“This

means the incumbent banks will have to innovate to compete, as there

will be a long line of fintechs and neobanks like Volt wanting to

harness this data to offer customers a superior banking experience.

“Customers

will be the masters of their data, and third parties will have to earn

it by being innovative and trustworthy,” he said.

Part of this was changing the narrative by offering an improvement to lives and not just the sale of products, said Mr Bunbury.

“Volt

and other innovative banks will be able to help Australians find and

secure better deals on a range of banking and even non-banking services,

like utilities and travel.

“By enabling data to be shareable

across financial institutions, it will be also possible for customers to

manage multiple bank accounts from one mobile app, regardless of

whether the accounts are held with rival banks,” he said.

Chief executive of Verrency David Link said the regime was going to eventually drive greater innovation.

“While

1 July 2019 will not drastically change the way Australians bank – as

only product, rather than customer, data will be available until 1

February 2020 – this is a huge step towards that much more

transformative change,” Mr Link said.

Banks would have to start to

offer a personalised consumer offering, said Mr Link, and those that

are agile were going to thrive.

“The effective use of data and

access to new value-added services will slowly become a major

decision-driver for consumers when it comes to choosing or changing who

‘owns their relationship’.

“Banks which don’t take this extremely

seriously are going to slowly struggle to remain competitive. On the

other hand, those which take steps to become more agile – especially in

their ability to deliver value around the consumer relationship – are

going to thrive in the post-open banking landscape,” he said.

According to Moody’s, on 11 January, the Canadian government published a consultation paper on its previously announced open banking initiative to foster competition within its banking industry. The initiative will provide policy recommendations on how best to allow retail bank customers to share their financial transaction data with fintechs and other financial services providers such as small and mid-sized banks to facilitate application development so that retail clients can compare financial products and change bank accounts more easily.

The government initiative is credit negative for the largest Canadian banks’ retail operations because it has the potential to incrementally weaken the industry’s favorable industry structure of a few concentrated players, and therefore the banks’ retail franchise strength and associated high profitability.

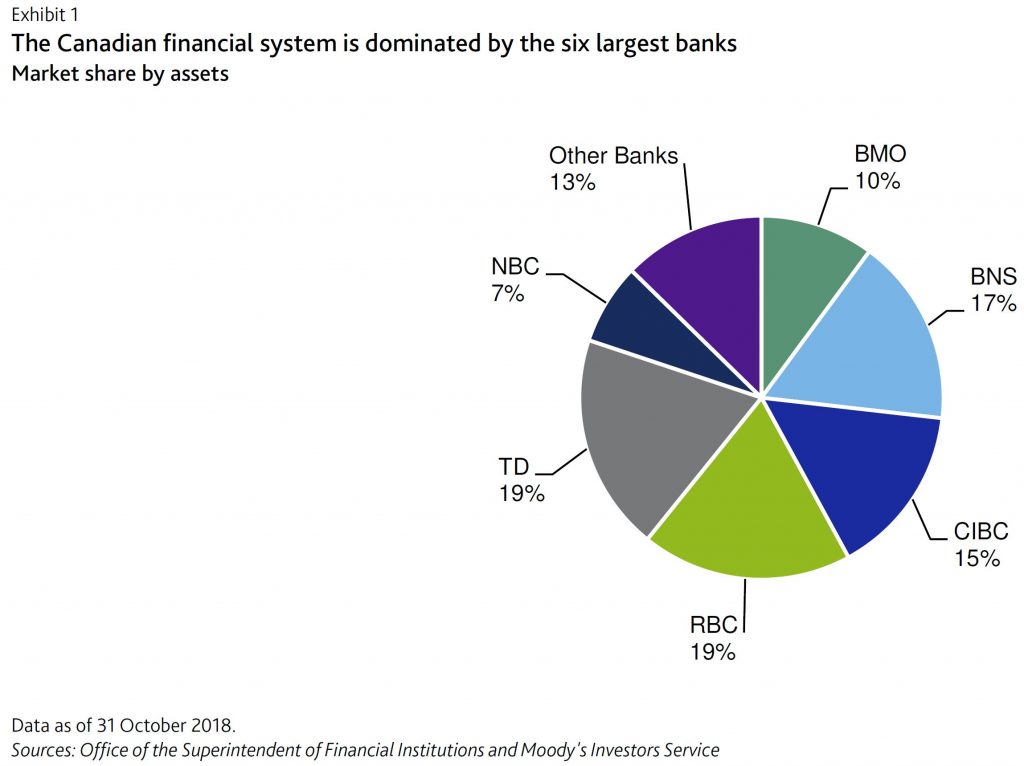

The largest Canadian banks are Bank of Montreal (BMO, Bank of Nova Scotia (BNS), Canadian Imperial Bank of Commerce (CIBC), Royal Bank of Canada (RBC), The Toronto-Dominion Bank (TD) and National Bank of Canada (NBC). As of 31 October 2018, these six banks held 87% of Canada’s banking assets.

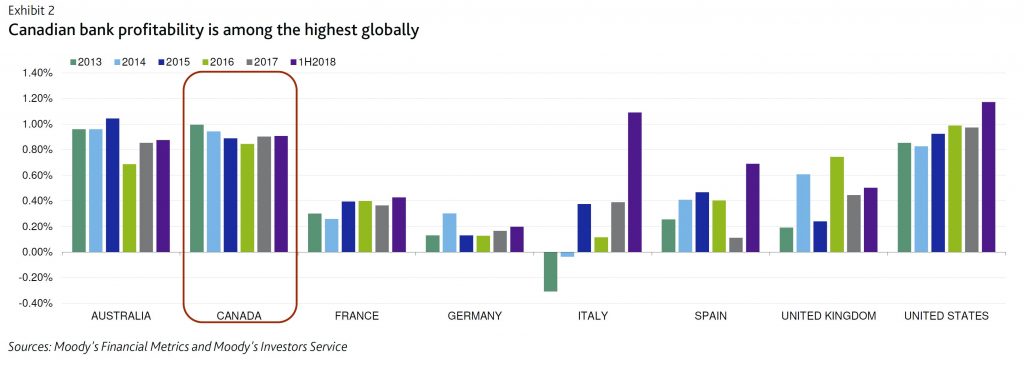

Canada’s banking system is highly concentrated and more profitable for the largest incumbents than in other banking jurisdictions.

Moody’s says “we believe the six largest banks have sufficient financial resources and fintech expertise to adapt to innovation in consumer banking. Nonetheless, technological disruption is likely to erode the incumbents’ profitability in certain retail lending products, such as credit cards, and/or payments over the long term as smaller, more agile banks achieve competitive advantages”.

On 9 May 2018, the Government agreed to the recommendations of the Review, both for the framework of the overarching Consumer Data Right and for the application of the right to Open Banking, with a phased implementation from July 2019.

The Government will phase in Open Banking with all major banks making data available on credit and debit card, deposit and transaction accounts by 1 July 2019 and mortgages by 1 February 2020.

Data on all products recommended by the Review will be available by 1 July 2020. All remaining banks will be required to implement Open Banking with a 12-month delay on timelines compared to the major banks. The Australian Competition and Consumer Commission (ACCC) will be empowered to adjust timeframes if necessary.

The Treasury will be consulting on draft legislation, the ACCC will be consulting on draft rules, and Data61 will be consulting on technical standards over the coming months.

From The Budget

The government has unveiled its 2018-19 federal budget, which revealed plans to support an open banking framework; the acceleration of the GovPass program; exploring the use of blockchain for government; and the promotion of the industry.

The government will pledge $44.6 million across four years from 2018-19 for the creation of a “national consumer data right”.

The CDR will help “consumers and small to medium enterprises to access and transfer their data between service providers in designated sectors,” the budget papers said.

Over four years, the $44.6 million – which also includes $1.4 million in capital funding in 2018-19 – will be split across three government agencies:

The Australian Competition and Consumer Commission (ACCC) will receive $19.6 million;

CSIRO will receive $11.6 million; and

The Office of the Australian Information Commissioner (OAIC) will receive $12.1 million.

A fact sheet from industry body FinTech Association said the ACCC’s role would be to “oversee sectors that will be subject to the CDR”.

Meanwhile, CSIRO would set data standards, with the funds going into innovation centre Data 61; and the OAIC will “assess the privacy impact” of the CDR.

The open banking regime could lead to more competition within financial services provided it doesn’t flood Australians with countless options, according to King & Wood Mallesons.

A panel of industry representatives at the ASIC Forum 2018 in Sydney this week discussed the characteristics of a strong open banking regime, arguing that the customer’s best interests must be kept in mind.

Panellist and head of the government’s Review into Open Banking, King & Wood Mallesons partner Scott Farrell, said the nascent data industry should be working towards creating greater convenience for customers.

“I hope the creative and innovative data industry can provide something that helps customers, rather than bombard them just with information,” Mr Farrell said.

“That’s a measure for its success. If the best that that industry can do is just bombard people with a thousand choices, then it’s failed Australian customers.”

He pointed out that competition alone was not significant in and of itself, but rather a means to an end.

“[Competition] doesn’t actually mean anything for a customer. It’s the choice and convenience that means something for a customer.

“That might come from competition, but you can’t feed your family with competition,” Mr Farrell said.

Co-panellist and ‘neobank’ Xinja co-founder and customer innovation director Van Le said the open banking regime should provide data in order to help customers make informed decisions.

However, the data or information should not be “so much that consumers get confused” such that “the whole benefit of open banking is lost and becom[es] a morass of indecision”.

“The real challenge for us, I think as an entire industry, is: how do we facilitate those choices with enough information, in the right context, giving customers control, so that in the end of the day, decisions that people make are decisions that people can be satisfied with?” Ms Le said.

Recent events have the potential to create a revolution in Australian Finance. We explore the 72 hours that changed banking forever.

Welcome to the Property Imperative Weekly to 10th February 2018.Watch the video or read the transcript.

In our latest weekly digest, we start with the batch of new reports, all initiated by the current Australian Government – and which combined have the potential to shake up the Financial Services sector, and reduce the excessive market power which the four major incumbents have enjoyed for years.

On Wednesday, the Productivity Commission, Australian Government’s independent research and advisory body released its draft report into Competition in the Australian Financial System. It’s a Doozy, and if the final report, after consultation takes a similar track it could fundamentally change the landscape in Australia. They leave no stone unturned, and yes, customers are at a significant disadvantage. Big Banks, Regulators and Government all cop it, and rightly so. They say, Australia’s financial system is without a champion among the existing regulators — no agency is tasked with overseeing and promoting competition in the financial system. It has also found that competition is weakest in markets for small business credit, lenders’ mortgage insurance, consumer credit insurance and pet insurance. The report demonstrates the inter-linkages between difference financial entities, and their links to the four majors. They criticised mortgage brokers and financial advisers for poor advice (influenced by commission and ownership structures) and the regulatory environment, where the shadowy Council of Finance Regulators (RBA, ASIC, APRA and Treasury) do not even release minutes of the meetings which set policy direction. You can watch our separate video blog on this.

On Thursday, the Treasurer released draft legislation to require the big four banks to participate fully in the credit reporting system by 1 July 2018. They say this measure will give lenders access to a deeper, richer set of data enabling them to better assess a borrower’s true credit position and their ability to pay a loan. This removes the current strategic advantage which the majors have thanks to the credit data asymmetry, and the current negative reporting. We note that there is no explicit consumer protection in this bill, relating to potential inaccuracies of data going into a credit record. This is, in our view a significant gap, especially as the proposed bulk uploading will require large volumes of data to be transferred. It does however smaller lenders to access information which up to now they could not, so creating a more level playing field. Consumers may benefit, but they should also beware of the implications of the proposals.

On Friday, Treasurer Morrison released the report by King & Wood Mallesons partner Scott Farrell in to open banking which aims to give consumers greater access to, and control over, their data and which mirrors developments in the UK. This “open banking” regime mean that customers, including small businesses, can opt to instruct their bank to send data to a competitor, so it can be used to price or offer an alternative product or service. Great news for smaller players and fintechs, and possibly for customers too. Bad news for the major players. The report recommends that the open banking regime should apply to all banks, though with the major banks to join it first. For non-banks and fintechs, the report wants a “graduated, risk-based accreditation standard”. Superannuation funds and insurers are not included for now. In terms of implementation, data holders should be required to allow customers to share information with eligible parties via a dedicated application programming interface, not screen scraping. A period of approximately 12 months between the announcement of a final Government decision on Open Banking and the Commencement Date should be allowed for implementation. From the Commencement Date, the four major Australian banks should be obliged to comply with a direction to share data under Open Banking. The remaining Authorised Deposit-taking Institutions should be obliged to share data from 12 months after the Commencement Date, unless the ACCC determines that a later date is more appropriate.

Then of course the Royal Commission in Financial Services starts this coming week. We discussed this on ABC The Business on Thursday. Lending Practice is on the agenda, highly relevant given the new UBS research (they of liar loans) suggesting that incomes of many more affluent households are significantly overstated on mortgage application forms. And The BEAR – the bank executive behaviour regime legalisation – passed the Senate, and as a result of amendments, Small and medium banking institutions have until 1 July 2019 to prepare for the BEAR while it will commence for the major banks on 1 July 2018.

APRA Chairman Wayne Byers spoke at the A50 Australian Economic Forum, Sydney. Significantly, he says the temporary measures taken to address too-free mortgage lending will morph into the more permanent focus on among other things, further strengthening of borrower serviceability assessments by lenders, strengthened capital requirements for mortgage lending, and the comprehensive credit reporting being mandated by the Government.

Adelaide Bank is ahead of the curve, as it introducing an alert system that will monitor property borrowers that are struggling with their repayments. The bank and its subsidiaries and affiliates will compare monthly mortgage repayments with borrowers’ income ratios. In addition, extra scrutiny will be applied where the loan-to-income ratio exceeds five times or monthly mortgage repayments exceed 35% of a borrower’s income.

But combined, data sharing, positive credit and banking competition and regulation are all up in the air, or are already coming into force and in each case it appears the big four incumbents are the losers, as they are forced to share customer data, and competition begins to put their excessive profitability under pressure. It highlights the dominance which our big banks have had in recent years, and the range of reforms which are in train. The face of Australian Banking is set to change, and we think customers will benefit. But wait for the rear-guard actions and heavy lobbying which will take place ahead.

Of course the RBA left the cash rate on hold this week, and signalled the next move will likely be up, but not for some time. Retail turnover for December fell 0.5% according to the ABS seasonally adjusted. This is the headline which will get all the coverage, but the trend estimate rose 0.2 per cent in December 2017 following a rise of 0.2 per cent in November 2017. Compared to December 2016 the trend estimate rose 2.0 per cent. This is in line with average income growth, but not good news for retailers.

The latest Housing Finance Data from the ABS shows a fall in flows in December. In trend terms, the total value of dwelling finance commitments excluding alterations and additions fell 0.1% or $31 million. Owner occupied housing commitments rose 0.1% while investment housing commitments fell 0.5%. Owner occupied flows were worth $14.8 billion, and down 0.3% last month, while owner occupied refinancing was $6.2 billion, up 1.2% or $73 million. Investment flows were worth 11.9 billion, and fell 0.5% or $62 million. The percentage of loans for investment, excluding refinancing was 45%, down from 49% in Dec 2016. Refinancing was 29.5% of OO transactions, up from 29.2% last month. Momentum fell in NSW and VIC, the two major states. In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments fell to 17.9% in December 2017 from 18.0% in November 2017 – the number of transactions fell by 1,300 compared with last month. But the ABS warns that the First Time Buyer data may be revised and users should take care when interpreting recent ABS first home buyer statistics. The ABS plans to release a new publication which will see Housing Finance, Australia (5609.0) and Lending Finance, Australia (5671.0) combined into a single, simpler publication called Lending to Households and Businesses, Australia (5601.0).

We continue to have data issues with mortgage lending, with the RBA in their new Statement on Monetary Policy saying it now appears unnecessary to adjust the published growth rates to undo the effect of regular switching flows between owner occupied and investment loans as they have been doing for the past couple of years. So now investor loan growth on a 6-month basis has been restated to just 2%. More fluff in the numbers! Additionally, the RBA will publish data on aggregate switching flows to assist with the understanding of this switching behaviour.

More data this week highlighting the pressures on households. National Australia Bank’s latest Consumer Behaviour Survey, shows the degree of anxiety being caused by not only cost of living pressures but also health, job security, retirement funding as well as Australian politics. Of all the things bothering Australian households in early 2018, nothing surpasses cost of living pressures. Over 50% of low income earners reported some form of hardship, with almost one in two 18 to 49-year-olds being effected.

Despite improved job conditions and households reporting healthier financial buffers, the overall financial comfort of Australians is not advancing, according to ME’s latest Household Financial Comfort Report. In its latest survey, ME’s Household Financial Comfort Index remained stuck at 5.49 out of 10, with improvements in some measures of financial comfort linked to better employment conditions – e.g. a greater ability to maintain a lifestyle if income was lost for three months – offset by a fall in comfort with living expenses.

We released the January 2018 update of our Household Financial Confidence Index, using data from our rolling 52,000 household surveys. The news is not good, with a further fall in the composite index to 95.1, compared with 95.7 last month. This is below the neutral setting, and is the eighth consecutive monthly fall below 100. Costs of living pressures are very real, with 73% of households recording a rise, up 1.5% from last month, and only 3% a fall in their living costs. A litany of costs, from school fees, child care, fuel, electricity and rates all hit home. You can watch our separate video on this.

We also published updated data on net rental yields this week, using data from our household surveys. Gross yield is the actual rental stream to property value, net rental is rental payments less the costs of funding the mortgage, management fees and other expenses. This is calculated before any tax offsets or rebates. The latest results were featured in an AFR article. The results are pretty stark, and shows that many property investors are underwater in cash flow terms – not good when capital values are also sliding in some places. Looking at rental returns by states – Hobart and Darwin are the winners; Melbourne, and the rest of Victoria, then Sydney and the rest of NSW the losers. The returns vary between units and houses, with units doing somewhat better, and we find some significant variations at a post code level. But we found that more affluent households are doing significantly better in terms of net rental returns, compared with those in more financially pressured household groups. Batting Urban households, those who live in the urban fringe on the edge of our cities are doing the worst. This is explained by the types of properties people are buying, and their ability to select the right proposition. Running an investment property well takes skill and experience, especially in the current rising interest rate and low capital growth environment. Another reason why prospective property investors need to be careful just now.

Finally, we saw market volatility surge, as markets around the world gyrated following the “good news” on US Jobs last week, which signalled higher interest rates. In our recent video blog we discussed whether this is a blip, or something more substantive. We believe it points to structural issues which will take time to play out, so expect more uncertainly, on top of the correction which we have already had. This will put more upward pressure on interest rates, and also on bank funding here.

Overall then, a week which underscores the uncertainly across the finance sector, and households. This will not abate anytime soon, so brace for a bumpy ride. And those managing our large banks will need to adapt to a fundamentally different, more competitive landscape, so they are in for some sleepless nights.

If you found this useful, do like the post, add a comment and subscribe to receive future updates. Many thanks for taking the time to watch.

Treasurer Morrison has release the report by King & Wood Mallesons partner Scott Farrell today in to open banking which aims to give consumers greater access to, and control over, their data. It mirrors recent UK developments, and is another nail in the competitive advantage the large players currently have. Later the scheme could be widened to other industry sectors, such as energy or telecommunications.

This “open banking” regime mean that customers, including small businesses, can opt to instruct their bank to send data to a competitor, so it can be used to price or offer an alternative product or service.

The report recommends that the open banking regime should apply to all banks, though with the major banks to join it first. For non-banks and fintechs, the report wants a “graduated, risk-based accreditation standard”. Superannuation funds and insurers are not included for now.

In fact, all authorised deposit-taking institutions (ADIs) will automatically be accredited to receive data.

There are exclusions. For example, value added data which is created by banks as a result of their analysis will not be included in the regime. Know your customer data though should be sharable. De-identified aggregate data would not be sharable.

Data provided under the regime will initially be “read only”, but the successful adoption of open banking “could also lead to ‘write access’ reforms” in the future. The following products are called out as in scope.

Transfer of data should be made free of charge, the report says.

Safeguards will be important, including under the Privacy Act, and a customer’s consent under Open Banking must be explicit, fully informed and able to be permitted or constrained according to the customer’s instructions. Joint accounts will need some special considerations in terms of authority, and advice.

An appropriate data standard will need to be agreed, and a clear and comprehensive framework for the allocation of liability between participants in Open Banking should be implemented. This framework should make it clear that participants in Open Banking are liable for their own conduct, but not the conduct of other participants. To the extent possible, the liability framework should be consistent with existing legal frameworks to ensure that there is no uncertainty about the rights of customers or liability of data holders.

In terms of implementation, data holders should be required to allow customers to share information with eligible parties via a dedicated application programming interface, not screen scraping.

The starting point for the Standards for the data transfer mechanism should be the UK Open Banking technical specification.

A period of approximately 12 months between the announcement of a final Government decision on Open Banking and the Commencement Date should be allowed for implementation. From theCommencement Date, the four major Australian banks should be obliged tocomply with a direction to share data under Open Banking. The remaining AuthorisedDeposit-taking Institutions should be obliged to share data from 12 months after the

Commencement Date, unless the ACCC determines that a later date is more appropriate.

The ACCC as lead regulator should coordinate the development and implementation of a timely consumer education programme for Open Banking. Participants, industry groups and consumer advocacy groups should lead and participate, as appropriate, in consumer awareness and education activities.

The ABA welcomed the report:

Banks are excited to enter the Open Banking age that will spark new innovations and deliver cutting edge products, with customers the big winner.

The Farrell Report into Open Banking released by the Treasurer today recognises both the opportunities and challenges that data sharing will bring. While the Australian Bankers’ Association has some concerns surrounding the implementation, the report lays out a broadly sensible path to Open Banking. Mr Farrell’s report should be commended for its focus on customers and its commitment to work with stakeholders to design a safe and secure data sharing framework.

Giving customers greater access to their own data will boost choice in banking and further simplify the application process for a financial product.

Australians have one of the most innovative and technologically advanced banking systems in the world. Examples of this is 24-hour banking, payWave and the soon to be launched PayID and New Payments Platform.

As the Productivity Commission affirmed this week, Australian banks are at the forefront of global innovation which has delivered a superior customer experience. Investments in how banks use data are already leading to new innovations that are improving the customer experience and this is set to continue under Open Banking.

A reform as large as Open Banking must be carefully considered and properly implemented.

Research shows that Australians trust their banks with personal information, more than online retailers, social media companies and even governments. It’s important that banks maintain this trust and ensure that the open data reforms don’t place personal information at risk.

Banks will continue to work with stakeholders like consumer groups, FinTech’s, regulators and government to get this right so it is a good model for all industries and customers are protected.

The ABA looks forward to carefully analysing Mr Farrell’s report and working with members and stakeholders to address any challenges to ensure its success. Banks would also like to thank Mr Farrell for his thorough and thoughtful inquiry

Open banking launched on January 13 in the UK. It requires major banks to share data with third party financial providers. This will bring a new level of transparency and encourage competition, shaking up the financial services industry and levelling the playing field for new challengers to take on the more established high street banks.

The reforms follow a 2016 investigation by the Competition and Markets Authority into retail banking. Its report concluded that the existence of barriers to entry for smaller and newer banks made the banking market less competitive.

This paved the way for open banking, which requires banks to securely share customers’ financial data with other financial institutions – provided customers give their permission. This should boost the range of products and deals made available to people and facilitate more switching, with offers better tailored to individuals, based on their past spending habits.

It will also enable people to bring together their financial information from different providers so they can, for example, open one app and see a list of their accounts with other banks.

All in all open banking is set to change the financial services industry in several ways.

Better banking options

The launch of open banking will be a turning point for large retail banks in the UK. The traditional retail banking business model will be transformed from a closed one to a modern, open source one.

The basis is a united financial platform that has been designed to provide users with a network of their financial data. This will disrupt the existing advantages that big banks in the UK have where they have a monopoly on customers’ data, not making it easy for customers to see the alternatives that are out there.

With more access to customers’ data, new financial technology (fintech) start ups, which are able to provide innovative solutions and modern financial products, will develop and challenge the traditional industry. Meanwhile, the increased competition and narrower profit margins will force existing big banks to adopt new technologies, improve their customer services and open up new revenue streams to keep up.

Better payment systems

Open banking will enable financial institutions to launch easy, fast and innovative global payment methods. Linked with the EU’s Second Payment Services Directive, which also comes into force this year, open banking also aims to boost competition in payment methods, which has been in need of a modernisation in the digital era.

The open access to people’s financial data means that new payment services can be developed. New providers will be able to initiate online payments (whether to friends, retailers, charities) directly from the payer’s bank account, avoiding the use of intermediaries like banks. Paying bills and transferring money will become as easy as sending a message.

As well as the emergence of new services that are more efficient, they should also be secure. Key to the new open banking standards is enhancing financial safety. Third party financial services providers will be required to obtain licenses and to meet the rules set by the main UK bank regulator, the Financial Conduct Authority.

Collaboration between banks and fintech

Open banking will digitise UK banking and strengthen UK fintech. Under the new regulation, fintech firms will play a more important role in the financial services industry and a huge number of fintech startups will enter into competition with existing major banks.

In a world of digital financial systems, big banks will have to rethink their position. Until now, collaboration between banks and fintech firms has mostly involved the financing of acquisition of fintech firms by big banks or partnership agreements, which enable a bank to use or acquire a digital solution developed by the fintech company.

Collaboration needs to become more customer focused – providing people with better products and solutions. Plus, a successful strategy for banks lies in greater cooperation with fintech firms to improve their own, often older technology to help them lower costs and improve customer experience, as well as developing new income streams so they can compete in the long term.

There are still unanswered questions about how open banking will play out. Security and privacy is fundamental to its successful implementation. Nonetheless, it is a revolutionary experiment aimed at boosting retail banking competition and will help new challengers in the financial services space to grow.

Authors: Ru Xie, Senior Lecturer in Finance, University of Bath;

Philip Molyneux, Professor of Banking and Finance, University of Sharjah

Open Banking, where customers can elect to share their banking transaction information with third parties went live in the UK.

This initiative is designed to lift completion across financial services, and of course in Australia, there are early moves in this direction, though the shape of those here are not yet clear. An issues paper from August 2017 outlines the questions being considered by the Australian Review into Open Banking.

What data should be shared, and between whom?

How should data be shared?

How to ensure shared data is kept secure and privacy is respected?

What regulatory framework is needed to give effect to and administer the regime?

Implementation – timelines, roadmap, costs

The report was due to report end 2017. So the UK experience is useful.

In essence, consumers (if they choose to) are able to give access to the data on their bank accounts to selected third parties, which allows them potentially to offer new and differentiated banking and financial services products. In practice, whilst some firms rely on simple (and risky) “screen scraping” the idea is that banks will provide a standard application programme interface (API) to allow selected third parties to access agreed data. Screen scraping is based on sharing the standard internet banking password and credentials, whilst API’s are more selective, using special passwords, which can time-limit access. This is more secure.

In addition, customers give access by logging on to their bank account, and establishing the data share from there, so again is more secure. Also, in the UK, firms wanting to access the data must be registered, and will be listed on an FCA directory. This is to avoid fraud. In addition, there is some protection for consumers if validly shared credential are misused, unlike the current state of play, where if banking passwords are shared, banks may avoid liability.

It is too soon to know whether this is truly a banking revolution, or something more incremental, but in the light of the emerging Fintech wave, we think the opportunities could be large, and the impact disruptive.

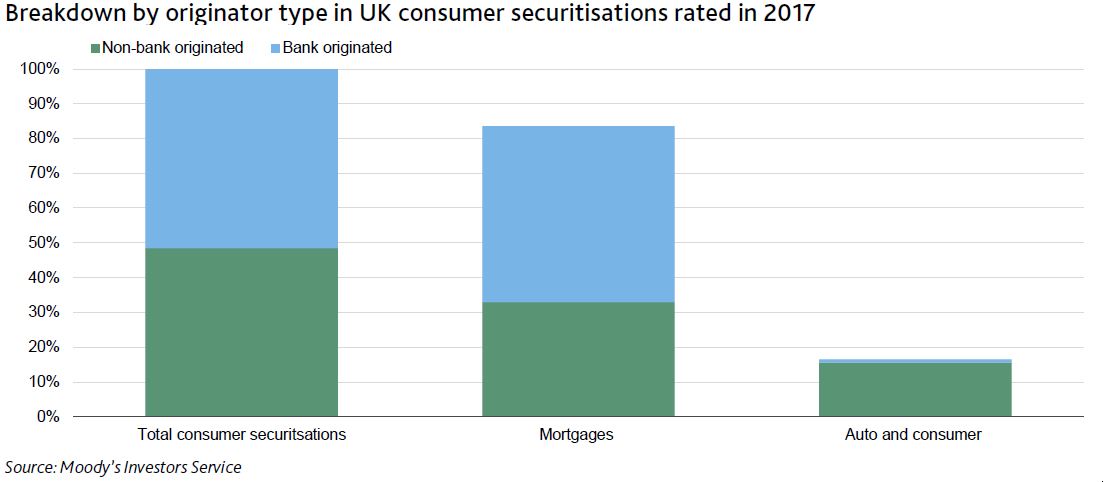

For example, Moody’s says the UK’s Open Banking initiative is credit positive for consumer securitisations.

By directly accessing current accounts, the lenders will gain valuable data about its customers’ disposable income and spending patterns. This data will complement the less detailed data that credit reference agencies provide and will result in stronger underwriting and better risk-adjusted returns when prudently applied.

The improved access to information also will benefit the debt collection process. Data on disposable income provides a realistic picture of a consumer’s debt repayment patterns. A clearer picture of consumers’ repayment patterns increases the probability of successful debt collection while ensuring compliance with the UK’s Financial Conduct Authority’s guidelines on fair treatment of customers.

Of the approximately £32 billion of UK consumer securitisations that we publicly rated in 2017, around half were backed by pools solely originated by non-banks. The exhibit below shows that auto and consumer pools, which will benefit most from improved underwriting, are almost entirely originated by non-banks lenders. We include auto-captive bank lenders in the non-bank category since they do not have a material current account presence.

The nine banks with the largest current accounts market share in the UK that will be obliged to share their data are Allied Irish Banks, Bank of Ireland (UK), Barclays Bank , Danske Bank, HSBC Bank, Lloyds Bank, Nationwide Building Society, The Royal Bank of Scotland and Santander UK plc. Four of the nine banks have been granted an extension of six weeks and the Bank of Ireland has until September to meet the technical requirements.

There is an initial six weeks trial during which only bank staff and third parties will be able to test new services.

Moody’s also notes that “the Open Banking requirements coincide with the European Union’s (EU) Second Payment Services Directive (PSD2), which requires all payment account providers across the EU to provide third-party access. For as long as the UK remains part of the EU, it will need to comply with the EU’s legal framework. However, the regulatory technical standards on customer authentication and secure communication under PSD2 have yet to be agreed, meaning that full data sharing under PSD2 likely will be applied no earlier than third-quarter 2019”.

A recent survey has found that Australians believe that banks are better at keeping their personal data secure than government agencies, online retailers or social media platforms.

And while men and women were fairly even, the Galaxy research found that those in regional centres trust their bank to protect their data even more than their metro counterparts (70 per cent regional vs 61 per cent for metro areas).

Those with the highest level of trust are aged between 40 and 49 years old.

Australian Bankers’ Association CEO, Anna Bligh said banks take data security and privacy very seriously, spending millions to ensure their systems are safe.

“With the introduction of Open Data across the Australian economy next year, consumer privacy and security is front of mind.

“Open banking will enable customers to get more value out of their data by opening it up to be easily shared with other banks and finance providers. In the future, a customer will be able to open their mobile phone app and with the touch of a button, direct their bank to transfer their data to another finance provider.

“Giving customers the ability to share their data more easily will help them to shop around for deals and get the best product for their needs.

“This represents a significant change from the current system and puts the power squarely in the hands of the customer, allowing them to decide how and when, or if, their information is shared,” she said.

Open data will also make comparing bank products and services easier as financial institutions standardise such things as terms and conditions and pricing.

Small businesses can also benefit from being able to share their transaction data with their accounting software packages. Bank transaction data could be tied to their invoices and receipts so businesses can readily track their finances.

The ABA will host its second Open Data Symposium today, aimed at continuing the discussion around the benefits to consumers and what the industry needs to do to prepare for the change.

The Galaxy research surveyed 1000 Australians online earlier this month for the Australians’ Attitudes to Digital Innovation & Data Security poll.

Macquarie Bank has started a trial, giving customers access to the data the bank has collected on them. These might include the number and types of account held, average balances, regular payments and income and credit score information. This information helps to determine both the need for products and the risk of a customer.

This idea is called open banking and will see customers use their data in a whole range of ways – to ensure they are getting a good deal on their credit cards or mortgages, to see how they are faring financially against people in similar situations, and even to make paying taxes easier. Until recently our banks have had exclusive access to all of this data. The banks used it for marketing and product design. That is, your data was used to increase their profits.

The absence of sharing meant the data was a hurdle to customer switching. But the Productivity Commission has said consumers should be given a “comprehensive right” to their data.

In fact, you can already see some of use cases for your data in services the banks themselves provide. For example, Ubank has a tool that allows customers to work out a budget, and compare themselves to others of similar ages, household types etc. And many banks and credit card companies allow you to dive into your spending habits, to see where your money is going.

Treasury is currently examining how open banking should work in practice, and the Productivity Commission is looking at competition in the financial services sector. So this Macquarie Bank trial is just the beginning of open banking in Australia.

Is it safe?

You might be worried about how these other services will access you data. You don’t have to share your passwords or bank login, rather the data is shared using a standardised application programming interface or API.

An API creates a standard for connecting to a service, similar to how there is a standard for writing down your home address. To mail a letter you write down a street number, street name, suburb, state, postcode. If you write down the latitude and longitude of the person’s house then the letter won’t get there, because it doesn’t abide by the standard.

API’s have security standards as well, with two elements. One is authentication – making sure that the machine seeking access is the machine it says it is – and the other is authorisation – making sure that the machine is permitted to access the API. In practice, the authentication component could be done by a trusted third party, such as Facebook or Google.

An open banking API would need to allow enough information about a customer to be accessed to allow for service comparisons. However, the data must not contain enough information to identify an individual. This is essential under Australian privacy law and proposed standards would also need to comply with the European General Data Protection Regulation (GDPR).

What will I use the data for?

The fact that all this data has largely been held by the banks until now means there aren’t a lot of services for us to connect to immediately.

The most immediate example is to use your data to make sure you are getting the best deal you can on your loans. This is one of the reasons the British Competition and Markets Authority decided that open banking was necessary.

Under this scheme, if you want to compare service providers, you can download your anonymised data in a standard form and then upload it to a bank, a price comparison website or an app. In the case of the app, it would present to you your best options, given your current banking profile. This would include staying with your current bank or changing one or more accounts to a different institution.

This data could also be used to get approval for a new loan. Your anonymous data, in combination with identity information, includes enough material for a lender to decide whether to give you a loan for a specific purpose.

These tools will foster more competition between banks as customers will find it easier to compare services and switch, but it will also mean customers can make sure they are getting the best product available at the bank they are currently at.

But beyond comparison and switching, there are a number of interesting examples of how you can benefit from the data in your bank.

A budgeting app connected to your bank account, for example, can use your anonymous data to help you plan your finances. Using both your banking and “tap and go” payment history, it can help you analyse your spending and set goals. These services can even tap into outside data, such as interest rates, to help you determine what to do if rates go up. It’s that spooky moment when your phone becomes your conscience.

Online accounting software such as Xero or MYOB allows daily reconciliation of business accounts. These software systems already use APIs provided by the major banks to reconcile current accounts, loan accounts and credit card services. One variant on the open banking API could let customers “mark” transactions that are employment related expenses or health related expenses to simplify tax returns.

Going beyond fintech

But beyond these examples there are any number of possibilities for what we can do with this data. For instance, we could see an app that helps you make shopping decisions to increase the amount of loyalty points you earn. That is, using data on prices, goals and financial history to benefit consumers and not just sellers.

There are already limited examples of such schemes. The Coles “Fly Buys” scheme is connected to Virgin Velocity points. Both Coles and Velocity prompt members to earn points. Adding an overlay of which credit card to use at the checkout is currently up to you. However, it would be perfectly feasible for an app in your phone to choose which credit card the phone uses to pay at the supermarket to give you maximum points.

There’s also an opportunity here to connect your stream of financial data to what might seem like unrelated data. For example, what if your smart watch prompted you to walk home if you’ve spent more on eating out than your budget allowed? That is, open banking might actually improve your fitness, or at least make you feel guilty about overspending.

Author: Rob Nicholls, Senior lecturer in Business Law, UNSW