PayPal’s announcement this week may well mark a step-up in digital currency adoption – we look at the implications.

Blog")

/

RSS Feed

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

PayPal’s announcement this week may well mark a step-up in digital currency adoption – we look at the implications.

PayPal’s announcement this week may well mark a step-up in digital currency adoption – we look at the implications.

AUSTRAC has ordered the appointment of an external auditor to examine ongoing concerns in regard to PayPal Australia’s compliance with the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (the AML/CTF Act).

These concerns relate to PayPal Australia’s compliance with its International Funds Transfer Instruction reporting obligations, which require regulated entities to report the transfer of funds or property to or from Australia.

International Funds Transfer Instructions reported by the financial services sector provide AUSTRAC with vital intelligence that enables AUSTRAC and its partners to combat serious crimes such as child sex exploitation.

AUSTRAC Chief Executive Officer, Nicole Rose PSM said the AML/CTF regime is in place to protect businesses, the financial system and the Australian community from criminal threats.

“Regulated businesses like PayPal Australia, who facilitate payments and transactions for millions of Australian customers every year, play a critical role in helping AUSTRAC and our law enforcement partners stop the movement of money to criminals and terrorists,” Ms Rose said.

“PayPal is an important partner in the fight against crime. However, when we suspect non-compliance AUSTRAC will take action to protect the Australian community.”

The external auditor must report to AUSTRAC within 120 days of being appointed and will examine PayPal Australia’s compliance with its:

The outcomes of the audit will assist PayPal with its compliance, but also inform AUSTRAC whether any further regulatory action is required.

“We will continue to work closely with PayPal during this process to address any compliance concerns,” Ms Rose said.

The extent of the auditor’s examination is determined by AUSTRAC and will be at PayPal Australia’s expense.

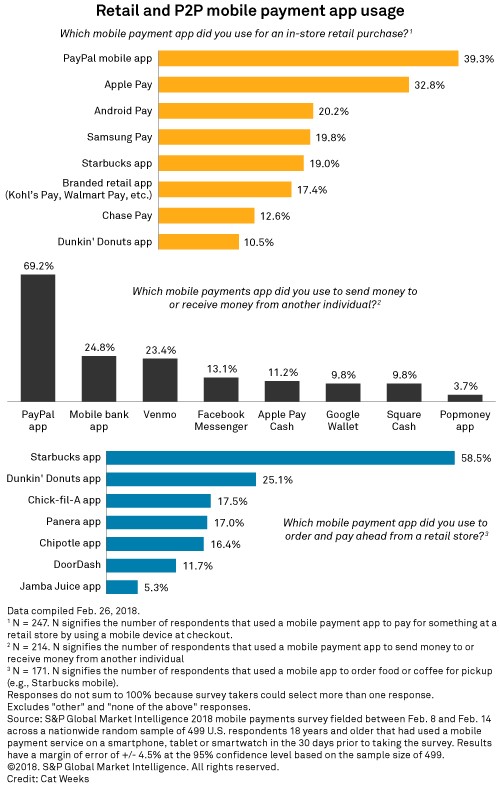

JPMorgan Chase & Co. has work to do if it wants Chase Pay to have the same kind of customer adoption as PayPal Holdings Inc.’s digital wallet, based on the results of a recent survey commissioned by S&P Global Market Intelligence.

About 39% of the individuals that used a mobile payment app to pay for an in-store retail purchase in the 30 days prior to taking the survey had used PayPal, versus 13% for Chase Pay.

This was one of several findings of the survey, which began with 904 respondents. Of those, 405 had not used a mobile payment app in the past 30 days, which gave us insight into why respondents would not want to use such services. The 499 that did use mobile payment services, meanwhile, yielded clues on what people do with their apps, such as the aforementioned in-store retail purchases.

Despite offering alternative services, Chase Pay recently partnered with PayPal, letting clients link their cards to their PayPal accounts through Chase Pay to access the PayPal wallet. This is not uncommon, as PayPal partners with other large banks and credit card issuers, such as Bank of America Corp. and Citigroup Inc., to link customer cards to their app. And as our survey data illustrated, respondents often used more than one wallet service.

PayPal also dominated in the survey question regarding person-to-person payments. Nearly 70% of those that had transferred money to an individual used PayPal, and the third most-used app was Venmo, which PayPal also owns.

Based on our survey, bank apps were slightly more popular than Venmo for person-to-person payments, with about 25% of respondents saying they had used a mobile bank app and about 23% saying they had used Venmo.

PayPal has announced the rollout of a new product designed for customers operating larger online marketplaces, like ride-sharing platforms, crowdfunding portals, peer-to-peer e-commerce sites, room rentals platforms, and others, starting in the USA.

They say that PayPal for Marketplaces is a comprehensive payments solution for marketplaces, crowdfunding platforms, and other environments where people buy and sell goods and services or raise money. The solution is ideal if you run a multi-party commerce platform and want a flexible, end-to-end solution for processing payments.

PayPal for Marketplaces supports a variety of common business types, including:

The platform can be tailored to the business’s needs, based on how much risk they want to manage with regard to their transactions. So for example, a business can decide if they want to handle payment disputes and chargebacks themselves, or if they want to turn over that responsibility to PayPal to manage instead.

The platform can be tailored to the business’s needs, based on how much risk they want to manage with regard to their transactions. So for example, a business can decide if they want to handle payment disputes and chargebacks themselves, or if they want to turn over that responsibility to PayPal to manage instead.

Over the past few years, we’ve seen impressive growth in marketplaces and other platforms with unique payment needs. Marketplaces have become the center of ecommerce activity. Today, more than half of consumers who shop online are making purchases on marketplaces, and global marketplaces are expected to own nearly 40 percent of the global online retail market by 2020.

PayPal has long served marketplaces — from its origins with eBay to Uber and Airbnb — but until now, we’ve supported these customers with a variety of different solutions. Today, we’re excited to share that we’ve launched PayPal for Marketplaces, an end-to-end global payment solution that can help businesses harness the capabilities of the world’s best known marketplaces. We’re beginning to roll this out globally and expect to be available to all markets in the coming months. Marketplaces like Grailed and Rocketr are already using PayPal for Marketplaces today.

PayPal for Marketplaces is a comprehensive and flexible payment solution for businesses accepting and disbursing funds — whether consumers pay using their PayPal wallet, credit cards or debit cards. Marketplace businesses—from ride sharing and room-rental platforms, to online crowdfunding portals and peer-to-peer e-commerce sites—have unique needs, like collecting commissions and fees, setting payouts and multi-party disbursements. And because of PayPal’s global reach, we can support buyers in more than 200 markets and sellers in more than 120 markets. We can also tailor our solution based on the marketplace’s need. For example, for marketplaces that don’t want to take on all of the risk, we offer solutions that allow PayPal to help manage the risk. But we also offer a solution for other marketplaces that want more control and risk ownership.

As always, PayPal offers value-added benefits like buyer and seller protection, risk- and fraud-detection capabilities and seamless checkout solutions that drive conversion for merchants. This includes One Touch, which enables more than 70 million of consumers around the world to skip logging in to PayPal at eligible merchant sites.

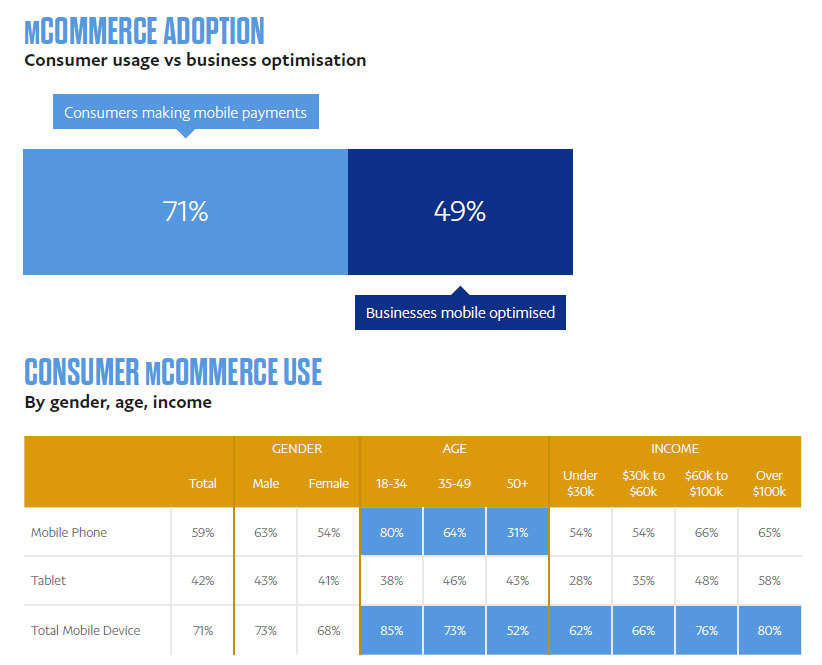

PayPal Australia have just released their first report on mobile payments in Australia, and highlight there is a significant gap between consumer willingness to use mobile payments, compared with business capability to receive them. Once again, in the digital disruption stakes, consumers are ahead of the curve!

Almost three-quarters (71%) of respondents are using their mobiles to make payments, however only 49% of businesses are optimised to accept them.

The number of consumers transacting on mobile is perhaps not surprising, considering that Australia is a country with one of the highest levels of mobile penetration globally with 80% of the Australian 18+ population having a smartphone. Among consumers aged 18-34 the use of mobile devices for payments at 85% is significantly higher than the 71% average.

Despite these impressive consumer mCommerce levels, 51% of businesses state that they are not optimised for mobile sales. Furthermore, almost one-third (31%) of businesses state they have no plans to change this. This gap is reflected in the proportion (26%) of businesses which have zero sales via mobile device.

When it comes to the devices that Australians prefer for making online purchases, desk and laptop computers are almost equally the favoured choice with 69% of respondents preferring to make payments on them. The remaining 31% of consumers prefer to make payments on their mobile phones (18%) or tablets (14%).Of those who prefer to use a mobile phone, those aged 18-34 dominate at 30% preference, compared to 15% preference for those aged 35-49 and 7% for the 50+ demographic.

The PayPal mCommerce Index finds that those with an income of over $100k show the highest preference for mobile payments, at 37%. Nonetheless, those with incomes under $30k make up almost one-quarter (24%) of those preferring to use their mobiles for payments.

More than a third (36%) of respondents are making mobile payments at least once a week, while one in five (22%) make mobile payments more than once a week. Millennial consumers (18-34) are the most prolific mobile shoppers with nearly half of this group (47%) making a mobile payment at least once per week. High frequency mobile payments are not limited to the young, one quarter (24%) of 50+ respondents are making mobile purchases and payments at least once a week.

The average mCommerce spend is $330 per month and 22% of respondents are spending more than $500 per month. These figures establish a benchmark against which we will continue to track in ongoing PayPal mCommerce Index reports.

When reflecting on levels of consumer mCommerce spending, age is not a strong contributing factor to high spend. In fact, across the age groups surveyed, consumers who are spending more than $500 per month, were notably similar at 23%, 26% and 19% across the 18-34, 35-49 and 50+ age groups, respectively.

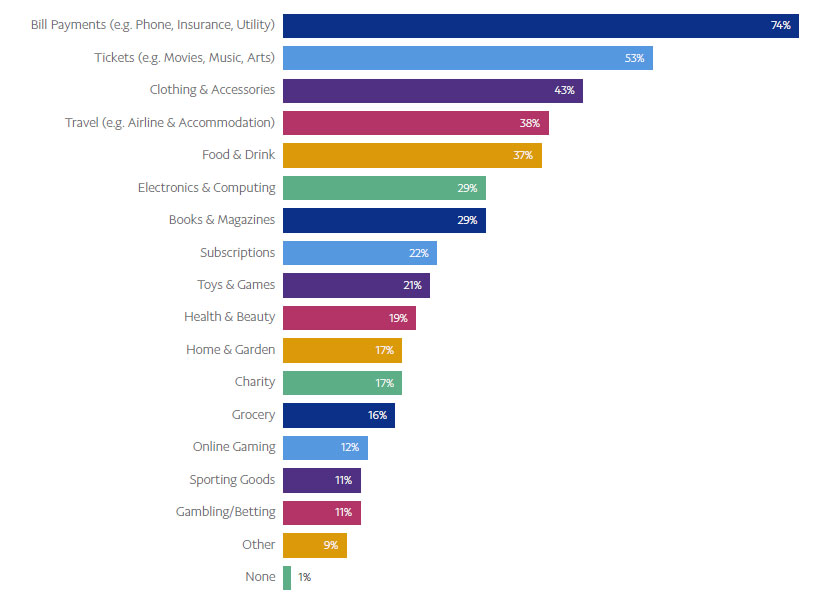

Bill payments is the category dominating mobile transactions. Almost three-quarters (74%) of respondents made phone, utility, insurance and other bill payments via a mobile device over the last six months. Other categories strongly supported by mCommerce are Tickets (53%), Clothing & Accessories (43%) and Travel (38%).

These top performing categories represent consumer transactions with major, mainstream businesses with well-established online commerce platforms. Regular and familiar use, plus lessened concerns for security by consumers, are believed to be factors in promoting mCommerce within these categories.

When Australian consumers get time to themselves, they are more inclined to make an online purchase or payment by mobile device – with ‘dual-screening’ being commonplace. Eighty-two percent of respondents said they engaged in mCommerce when relaxing at home or watching TV; almost half (45%) noted that they were engaged in mCommerce when taking a break at work or school; and just over one-quarter (26%) used the time when commuting on public transport for mobile purchasing or payments.

The data shows that although the majority of consumers do not indicate that a mobile is their preferred device for online purchases, they are using their mobile devices to shop when they are at home, presumably when they also have access to a laptop or desktop computer. Understanding the prevalence of dualscreening can help to inform future mCommerce positioning, marketing and consumer targeting.

Social commerce is rapidly emerging as the new frontier for online commerce. Already, 11% of respondents have made a purchase via a social platform. As channels including Facebook, Twitter and Pinterest, where consumers are highly engaged, emerge as commercial avenues, Australian businesses need to adapt if they want to maximise their online commerce opportunities.

Currently, 7% of surveyed businesses accept payments via social media sites or apps.

Despite consumer appetite, the PayPal mCommerce Index finds that 89% of businesses have no intention of accepting payments via social media within the next 6 months.

The survey was executed through Roy Morgan Research Ltd based on the survey responses of 996 consumers and 106 businesses using an online self-completion survey.

Xero is making huge strides towards a great online revolution in small business: to build a financial web that connects small businesses, banks, accountants and bookkeepers, and online software, that really allows businesses to grow by zeroing in on what they do best — building their own business.

But it’s hard for businesses to do that when they’re spending their time doing important yet time-sucking tasks like chasing payments, instead of innovating and growing. For example, we’ve found that Xero customers have sent almost 9.5 million invoices over the last 30 days alone. That’s a sure sign of healthy small businesses. Yet based on our current data, over 60% of those invoices will be paid late.

Xero + PayPal

With unpaid invoices causing a major headache for small business owners, we are pleased to announce at Xerocon San Francisco a slick new integration with PayPal, which is due to be released later this month.

This update will deliver a seamless new checkout experience for customers that will make it easy for invoices to get paid as soon as they are received, using Xero’s online invoices and PayPal Express Checkout. In addition to a fast payment experience, Xero users will now be able to see real-time status updates on outstanding invoices. Payment reconciliation will also be a breeze, with Xero doing all the heavy-lifting for you by auto-matching payments and fees.

I’m excited to have PayPal join us on our journey to rewire the small business economy. As small businesses move to simple, easy-to-use online tools like this latest integration in our ecosystem/App Marketplace, financial institutions and large enterprises are being made aware of the fundamental architectural shift. They’re connecting to these new platforms and as a result, the financial web is evolving quickly, especially where shared transactional services have become the expectation, shifting the focus on to revenue, opportunity, compliance, and risk management.

PayPal are a major online player. They’re providing an open and secure payments ecosystem across more than 188 million active accounts using 100+ currencies in over 200 countries.

Paypal Express Checkout offers a quicker, easier payment experience meaning customers can complete a payment in just 3 clicks once they receive an online invoice, removing the barriers of completing payment.

According to The Australian Business Review, PayPal Working Capital has extended more than $85m to about 3,000 small businesses since launching in Australia in late 2014.

In contrast, Prospa — the biggest “fintech” online small business lender — in May revealed it had cracked the $150m mark after four years of operations.

SocietyOne, the biggest “marketplace” lender, which has also been in business for four years, pushed through $100m personal loans in April.

PayPal’s product is also different as we described in an earlier post, with the unsecured loan of up to $97,000 being offered only to merchants that use its payments network, so borrowed funds can be instantly distributed following a five-minute application.

There’s a one-off upfront fee and repayments come out of daily sales, typically between 10 per cent and 30 per cent of turnover.

Interest rates are typically in the “teens and 20 per cent” range, differing based on merchants’ repayment choices and risk.

Including the US and Britain, PayPal Working Capital recently surpassed $US2 billion ($2.6bn) in loans. While Australia makes up a small piece of the pie, the business is profitable.

eftpos today announced that PayPal had become the latest payments company to join the eftpos membership, with plans to connect directly to the company’s new real time, centralised payments infrastructure, the eftpos Hub, in 2016.

eftpos Managing Director, Mr Bruce Mansfield, said PayPal was a popular payment option for Australian consumers and merchants and was a welcome addition to the eftpos Membership.

Mr Mansfield said eftpos had recently upgraded its infrastructure for Online payments and would work with PayPal and other Members to ensure that eftpos would be available to consumers and merchants as a payment option for online transactions. PayPal is only the fourth new eftpos Member to join since the inception of eftpos as a payment system in 2009, following ING Direct, Tyro and Adyen.

“We are very pleased that PayPal has decided to join eftpos and directly access the real-time processing capabilities of the eftpos Hub infrastructure and other benefits of being a Member,” Mr Mansfield said. “PayPal plays an important role in Australian Online payments and eftpos should be available as a payments choice for PayPal users. “eftpos is happy to work with PayPal to make eftpos payments available to more Australian consumers and merchants on new platforms.”

The eftpos Hub is a robust, reliable, secure and scalable centralised infrastructure that aims to provide the industry with cost effective, real time payments processing, as well as an enhanced capability to implement new products and services.

Since being launched in September 2014, the Hub is already processing almost 3 million eftpos CHQ and SAV transactions a day. Ms Libby Roy, Vice President and Managing Director of PayPal Australia said, “eftpos is an established and important part of the payments landscape in Australia with a strong consumer base. We’re very happy to be working together to enable eftpos payments through the PayPal network. “Our membership of eftpos takes us one step closer to giving consumers the ability to use any funding mechanism through PayPal to transact securely and conveniently online and via mobile devices.”

eftpos is the most widely-used card system in Australia, accounting for more than 2.3 billion CHQ and SAV transactions in 2015 worth more than $140 billion.

The payments landscape is set to change in Australia as PayPal continues to develop its PayPal Here small business card payment solution by launching a new Tap and Go enabled version of its PayPal Here Chip and PIN card reader. As highlighted previously, expect to see more disruption to the payments landscape, at the expense of incumbents.

PayPal Australia has announced it is launching a new Tap and Go enabled version of its popular PayPal Here Chip and PIN card reader. The PayPal Here app turns a smartphone into a complete payments solution, allowing businesses to capture every sale, regardless of the payment method, and coupled with the new PayPal Here Tap and Go card reader will allow businesses to accept card payments faster than ever.

The new card reader will enable businesses to accept contactless card payments from debit and credit cards and continue to support chip and PIN payments. With PayPal Here businesses can also accept PayPal payments via PayPal’s Check-in technology, generate and distribute invoices and send receipts.

In response to a changing retail landscape, the new card reader has been engineered specifically for Australian small businesses, service providers and casual sellers who need to accept card payments on-the-go. PayPal Here is also suitable for in-store retailers looking to diversify their payments offering and provides an innovative, pay-as-you-go solution for taking payments.

The launch of PayPal Here reflects an increasing appetite amongst Australians for NFC enabled technologies: “There is an expectation of choice from Australian consumers who are looking for the flexibility to pay via whatever method they choose and we’re increasingly seeing that customers are looking for the convenience offered by contactless payment,” said Emma Hunt, Director of Small Business, PayPal Australia.

“We need to ensure we arm businesses with the technology and resources needed to adapt to the ever-changing payments landscape. Our new payments solution will allow businesses to take advantage of the popularity of contactless payments here in Australia, as well as continue to take secure Chip and PIN payments on-the-go,” she continued.

As with the current PayPal Here Chip and PIN solution, a business simply pairs the new card reader via Bluetooth with a smartphone or tablet (for iOS and Android) and accepts secure payments through the PayPal Here app anywhere they’re trading.

There are no monthly subscription fees to use PayPal Here, just a one-off charge for the card reader and then a small fee per transaction.*

“The current PayPal Here card reader has proven to be really popular, with tens of thousands of Australian businesses accepting payments from market stalls, ute trays and garages across the country,” continued Hunt.

“The smartphone has well and truly become the mission control device for running a small business and the new iteration of the PayPal Here device provides businesses with another way for consumers and businesses to pay and get paid.”

Businesses can sign up to PayPal Here at www.paypal.com.au/here. The new card reader will be generally available later in 2015.

*Fees: 1.95% for payments through the PayPal Here Chip and PIN card reader, or PayPal check-in payments, 2.6% + $0.30c for invoices, and 2.90% + 0.30c for card payments manually entered into the PayPal Here app. For more information please see PayPal’s Combined Financial Service and Product Disclosure Statement at: https://www.paypal.com/au/webapps/mpp/ua/cfsgpds-full#18_Fees_and_charges