Property insider Edwin Almeida and I discuss the rental property sector from the point of view of the agencies, and investors. There are traps for the unwary!

In the latest in our “from the front line series”, I caught up with Carl, a property investor from Perth, and we discussed the shape of the market there, including falling rental returns and prices.

I caught up with property expert Edwin Almeida and we discussed the pressure on property investors and their property portfolios. Is the property investment party over?

Given the falling values, the dilapidation of much of the stock, and falling demand, it may just be the case. At very least, Edwin suggests holding off as prices will fall further! Then the question becomes, how far and how fast?

In their latest release, HIA is essentially calling for an easing of lending practices, suggesting that investors need encouragement to come back into the market.

“A growing list of disincentives are deterring investors from Australia’s housing market,” stated HIA economist, Diwa Hopkins.

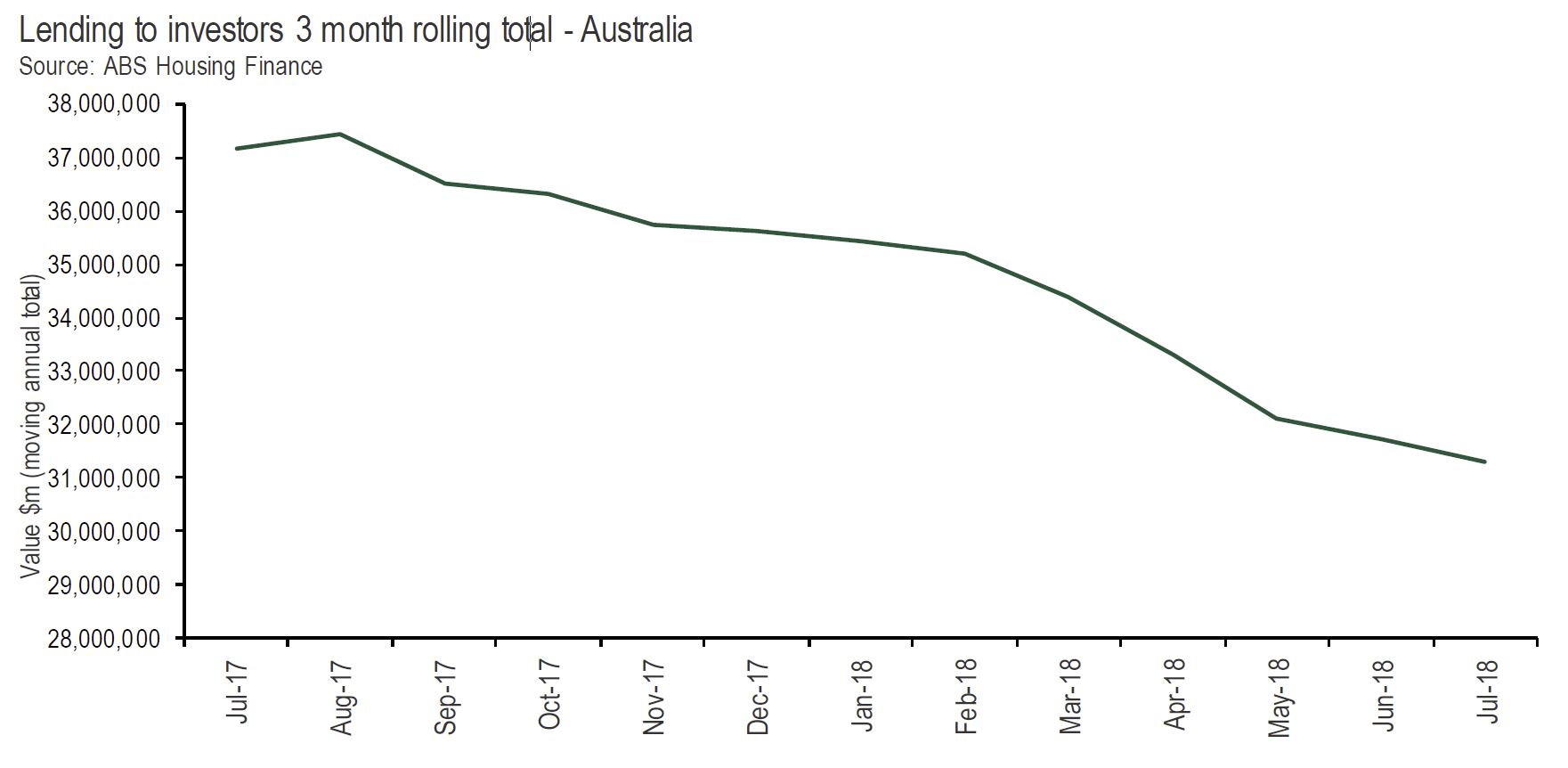

Today the ABS released data on housing finance for the month of July 2018. These figures show the value of lending to investors declined by a further 1.3 per cent in the month. The value of lending in July 2018 is now 15.7 per cent lower than in July 2017.

“Investors played a significant role in the record levels of new home building that occurred in recent years. By the same token their retreat from the market will weigh on activity over the near to medium term,” said Ms Hopkins.

“The exiting of investors from the housing market can be traced back to well-documented APRA interventions at the end of 2014 and then again in early 2017.

“In addition, state and federal governments have acted to deter foreign investors by levying additional taxes and charges on their investments in the domestic market.

“More recently the Banking Royal Commission has seen lenders further tighten their practices beyond APRA’s initial requirements and yesterday two of the other major banks joined Westpac in raising their variable mortgage rates.

“Add to this, a situation of falling dwelling prices in the key Sydney and Melbourne markets as well as the prospect of increased taxes on investment housing through negative gearing restrictions and increased capital gains tax, and the list of deterrents to investors in the housing market is comprehensive.

“Overall, most of these factors are having the effect of limiting credit availability.

“The concern now is APRA’s interventions appear to have run beyond their usefulness,” said Ms. Hopkins.

Property investors are more likely to support foreign investment in the property market than people without such investments, we have found in a survey of Sydneysiders’ views about foreign real estate investment. Perhaps more surprising, would-be buyers, who might be expected to worry about demand pushing up prices, were also more likely to be supportive than those who were not looking to buy a property.

We reported previously that over 60% of Sydneysiders do not want more individual foreign investment in residential real estate in Sydney.

Within this context, we surveyed almost 900 people in Sydney to examine the relationships between home ownership, real estate investment, housing stress and views about foreign investment. Our analysis shows:

Those who have property market investments are more likely to be supportive of foreign investment than those who don’t have such investments.

Comparing those who are in housing stress to those who are not in housing stress, there are no significant differences in the two groups’ beliefs about foreign real estate investment.

One group with a strong interest in Sydney’s real estate market are local real estate investors. We were interested in whether those with investment properties and those without differed in their views about individual foreign investment in residential real estate.

We found those with investment properties were likely to be more supportive of foreign investment in Sydney’s housing market than those without investment properties.

For example, 29% of the investment property owners agreed that “foreign investors should be able to buy properties in Sydney” compared to 17% of those without investment properties. They were similarly supportive of foreign students being allowed to buy properties while studying in Australia, with 32% agreeing with this compared to 19% among those without investment properties.

Property investors were more positive about the government’s regulation of foreign investment as well: 28% agreed it has been effectively regulated, compared to 16% of those without investment properties.

House hunters’ views

House prices in Greater Sydney have increased rapidly over the last decade and household debt has grown too.

We might expect people who are actively looking to buy a property to be particularly concerned about foreign real estate investment, as they may feel they are competing against and being priced out of the market by foreign buyers.

For this reason, we asked survey participants whether they were actively looking to buy a property. In response, 23% said they were. Of this group, 31% agreed that foreign investors should be able to buy properties in Sydney, compared to 15% of those not looking for a property.

Housing-stressed households’ views

Increasing mortgage and rental costs are a source of discontent within Sydney’s population. Measurements of housing stress are disputed, but are nonetheless used to give a comparative value to how hard it is for a household to meet housing costs. A ratio of housing costs to income of 30% and above is a common benchmark for housing stress.

Using this measure, we found that more than half (52%) of our survey participants were experiencing housing stress. Another 33% spent less than 30% of their income on their housing and 15% indicated they did not know.

Comparing those over the 30% threshold with those who spend less of their income on housing, we found no significant differences in beliefs about foreign real estate investment.

Other drivers of concern

We found those who are active in the local real estate market remain concerned about foreign investment in general.

If housing stress levels do not lead to differences in attitudes to foreign investment, as our findings suggest, cultural or other factors may be at work in the general discontent about foreign investors in Sydney.

We need to investigate further how being active in the housing market informs Sydneysiders’ views about the right of foreign investors to use real estate as a vehicle for growing capital.

Sydneysiders with equity in the housing market, such as home owners or investors, might view foreign buyers pushing up housing values as positive. As a result, they might fear that restricting foreign investors might depress their assets.

If this type of shared commitment to real estate investment were present across the domestic-foreign investor divide, this could reinforce the idea of treating real estate as an asset class at the global scale, while cultural tensions between foreign and local investors remain at the local level.

Authors: Dallas Rogers, Program Director, Master of Urbanism. School of Architecture, Design and Planning, University of Sydney; Alexandra Wong, Engaged Research Fellow, Institute for Culture and Society, Western Sydney University; Jacqueline Nelson, Chancellor’s Postdoctoral Research Fellow, University of Technology Sydney

More data showing the impact of the fleeing of property investors on the property market. We suspect the decline will continue as credit rules are tightened.

The HIA begs for no further constraints on this sector of the market, but with one third of loans for investment purposes, it is still too high. Remember the Bank of England got twitchy at 16%.

“Investors have been the target of a number of regulatory interventions and we are now seeing this impact on residential building activity,” said HIA Senior Economist, Geordan Murray.

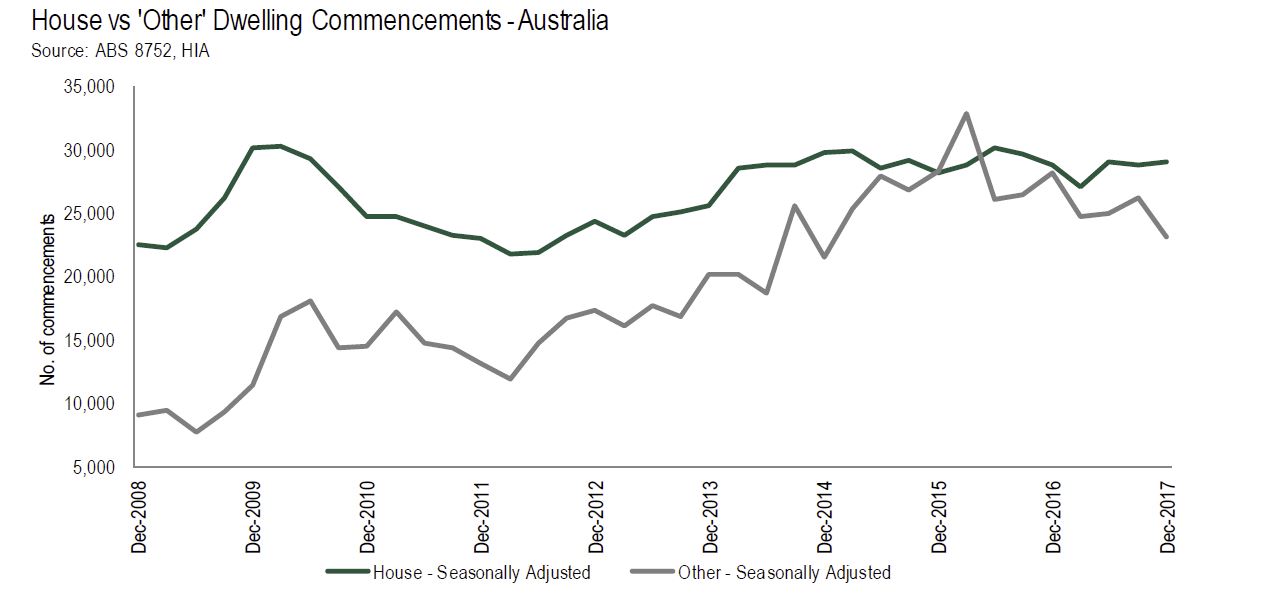

The ABS today released building activity data for the final quarter of 2017. Detached house commencements increased by 0.7 per cent over the December 2017 quarter, while starts for other dwelling types (predominantly apartments) declined by 11.2 per cent.

“The decline in multi-unit dwelling starts has dragged down the total number of new home starts during the final quarter of 2017. The total number of dwellings starts fell by 5.0 per cent in the December 2017 quarter and was down by 8.3 per cent on the level recorded a year earlier,” added Mr Murray.

“In contrast to the decline in multi-unit starts, the resilience of the detached house market continued to shine through. The number of detached house starts during the December quarter of 2017 increased by 0.7 per cent over the quarter and was up by a similar amount compared with the level of a year ago.

“Despite the soft starts result in the quarter, the pipeline of multi-unit activity remains quite large. There were still over 150,000 multi-unit dwellings under construction at the end of the 2017, which is only slightly below the 155,000 level at the peak of the cycle. There are a further 33,800 dwellings in projects that have been approved and are yet to start work, this is a record high.

“The combination of falling commencements and the build-up of dwellings in projects awaiting commencement is somewhat concerning. It is likely to indicate a slowdown in pre-sales activity. New projects will not commence construction until they achieve a satisfactory level of pre-sales.

“Pre-sales to investors, both domestic and from overseas, have been important for many multi-unit developments. With additional taxes on foreign investors and regulators clamping down on investor lending, investors have retreated from the market.

“If we see investors return to the market and the approved projects continue to progress through to work on the ground then residential building work could potentially make a stronger contribution to economic growth this year than we are expecting.

“Now is not the time to impose additional taxes or constraints on investors,” concluded Geordan Murray.

More people are becoming heavily indebted by buying rental properties and shared accommodation is flourishing, as third party tech platforms help people find a place without a real estate agent.

A new report from the Australian Housing and Urban Research Institute explains how the private rental market is changing over time for both landlords and tenants.

Over the 10 years to 2016, the number of renters grew 38% – twice the rate of household growth. More renters now are couples, or couples with children, so it seems the sector is shaking its image of unstable housing or perhaps these people are left with few other options.

Households by type, 2006 and 2016

Author provided (No reuse)

The report analyses data from the 2016 Census, the 2013-14 Survey of Income and Housing and the 2014 Household, Income and Labour Dynamics in Australia (HILDA) Survey. It also draws on interviews conducted with 42 people involved in all aspects of the private rental sector: financing, provision, access and management.

Rental property ownership also grew. We found the number of households with an interest in a rental property grew and the number that own multiple properties grew slightly as well.

But the typical landlord is still the conventional “mum and dad” investor. Two-thirds of rental investor households have two incomes, and 39% have children.

However they are also mostly high-income and high-wealth households: 60% are in both the highest income and highest wealth bracket. Interestingly, about one in eight landlords is themselves a private renter.

Housing finance ($A), 2000 – 2016

Author provided (No reuse)

The biggest change in ownership is in finances: owners of rental properties are relying more heavily on debt.

Financing rental properties

The people we interviewed highlighted the Australian Prudential Regulation Authorities’ (APRA) guidance to lenders on loan serviceability calculations as having the greatest impact on overall investment levels and investor decisions.

Adding to the complexity is the proliferation of intermediaries, such as mortgage brokers and wealth advisers. These advisers are telling borrowers what lenders and loan products to use to maximise their borrowing power and negotiate lender and regulator requirements.

Houses are the most commonly rented in Australia, but everywhere rental markets are moving away from this and towards dwellings like apartments.

There’s now more diversity in rental properties too. For example the building of high-rise student accommodation, “new generation boarding houses” and granny flats.

These allow landlords to house more people in the one building, increasing revenue and making management more efficient.

The informal sector of shared accommodation appears to be flourishing, like improvising shared rooms and lodging-style accommodation in apartments and houses.

Finding a rental

People have moved from finding rentals in real estate agents’ high street offices and onto online platforms. New third-parties like apps and other digital platforms offer non-cash alternative bond products, schedule property inspections, collect rents, and organise repairs.

Even though these technological innovations avoid agents, they have in fact increased their share of private rental sector management. Agents themselves are use these platforms to change their businesses, and the structure of their industry.

Our research found that revenue from an agency’s property management business (its “rent roll”) has become increasingly important. Some players in the industry are consolidating their businesses around it, to make higher profits from tech-enabled efficiencies.

However, the real estate business still depends on building personal relationships, particularly in high-end markets.

The new tech platforms of the private rental sector raise issues for tenants too, particularly in terms of the personal information they collect. For example, one of the online platform operators told us they looked forward to using applicants’ information to score or rank applicants. Another one of the new alternative bond providers uses automatic “trust scoring” of personal information to price its product.

These innovations may be convenient to use, and may give some tenants an advantage in accessing housing – but at the expense of others who are already disadvantaged.

Rental properties meeting demand?

If the private rental sector is going to meet the demand for settled housing, governments will have to intervene. This can’t be left to technological innovation, or higher income renters exercising their consumer power.

Federal or state governments could create public registers of landlords, or licensing requirements, to police landlords who are not “fit and proper” and exclude them from the sector.

There could also be stronger laws around tenancy conditions and protections for tenants against retaliatory action. The Poverty Inquiry in the 1970s set the basic model of our present laws and they haven’t changed much.

Tenants’ personal information also needs to be protected, to properly take account of the rise of the online application platforms; another is the informal sector, which is currently in a regulatory blindspot.

The popular emphasis on “mum and dad” investors diminishes expectations of landlords. Rental property investment should be regarded as a business that requires skill and effort. As for-profit providers of housing services, landlords should be held to standards that ensure the right to a dignified home life.

Author: Chris Martin, Research Fellow, City Housing, UNSW

Today we continue our analysis of the latest results from our Household Surveys by drilling down into the segment specific analysis, having in our previous post looked at the changing dynamics across our household segments.

We start with the Property Investor segments, which are becoming significantly less active thanks to a tightening of lending standards, higher mortgage rates and more limited capital growth. As a reminder the latest available ABS data shows that lending flows to investors is slowing, and especially interest only loans, and the number with interest only loans who are now being forced to move to the more expensive principle and interest loans is rising.

Yesterday we showed how their buying intentions were tanking.

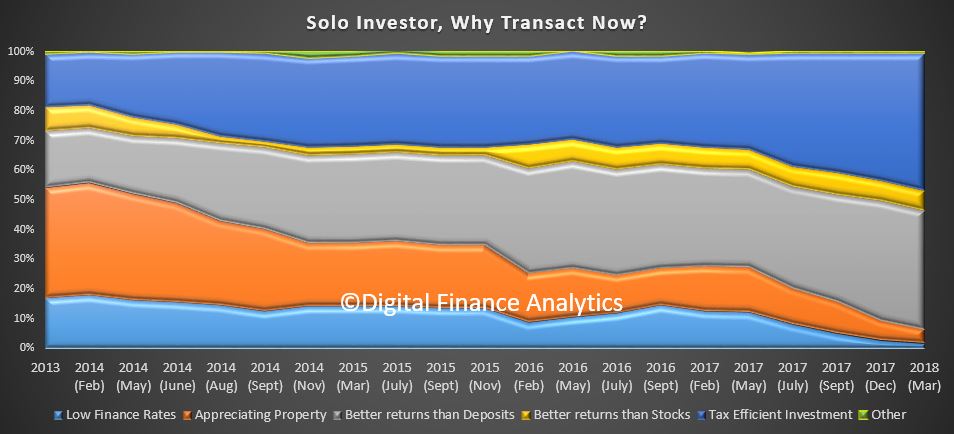

So now lets go deeper into the data, starting with solo investors – those with just one or two properties, and their motivations. The predominate reason for investors to hold property now relate to the tax benefits which can be accessed at 46%, up 3% from December 2017. This includes the ability of offset costs (including interest costs) against tax, as well as access to the very beneficial capital gains. The other driver is the perceived better returns compared with bank deposits at 39%, despite the fact that it you tot up all the various costs of an investment property, including returns from rentals, half the properties are under water! Other factors, such as access to low finance rates (1.9%) and appreciating property values (4.7%) are becoming less significant.

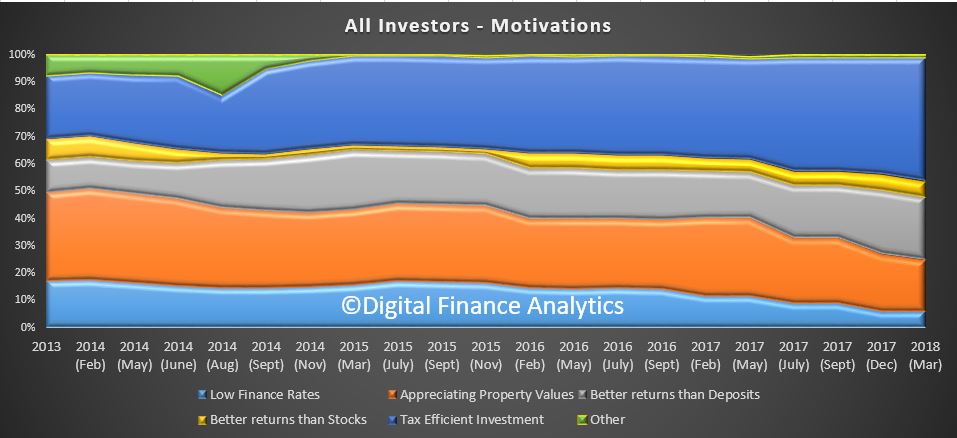

The pattern for portfolio investors is vary similar. So looking across all investors, we see a similar footprint, with the drive to gain tax efficiency (45%, up 2.4%), better returns than deposits (23%) and low finance rates down to 6.1%. Appreciating property values account for 18% of the motivation, down 2% on the previous quarter and continues to slide.

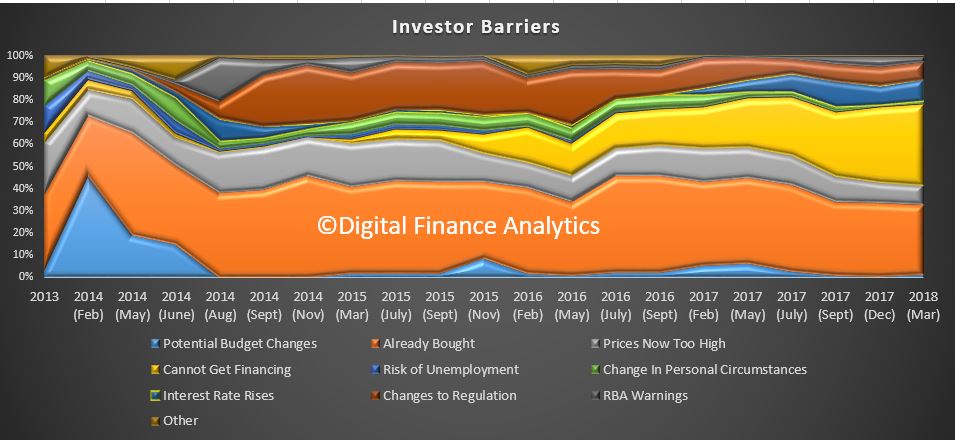

Turning to the investor barriers, we see a significant rise in the number of investors who are unable to get finance, up 3% to 36.7%, a trend which started in 2015, but is now accelerating. A further 10% see potential interest rate rises a barrier, up more than 1% from December 2017. We note that RBA warnings have only a small impact, at 2.5%, down 2% from our last surveys.

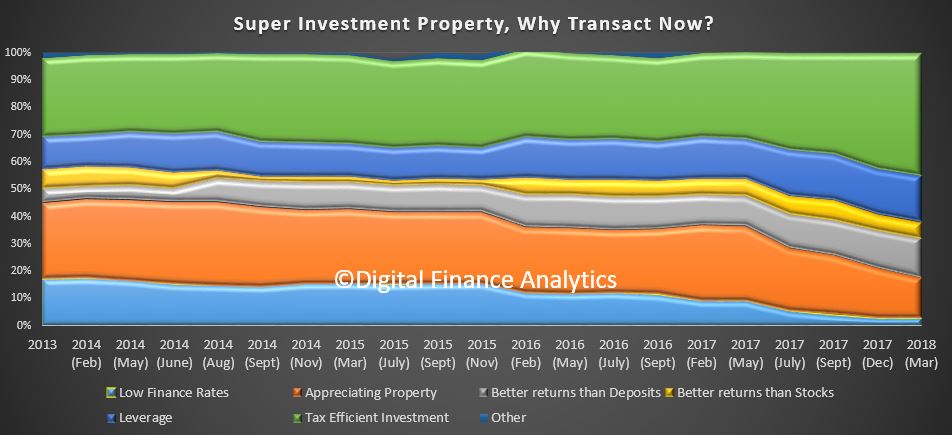

Looking across to property investment via a self- managed superannuation fund, once again tax benefits at 45%, up 2%, and better returns than deposits at 14%, plus leverage 17% account for the majority of the motivations to transact. 14.6% of SMSF property investors are still expecting further property gains, but this is down more than 2% from last time. Low finance rates accounted for only 2% of motivations.

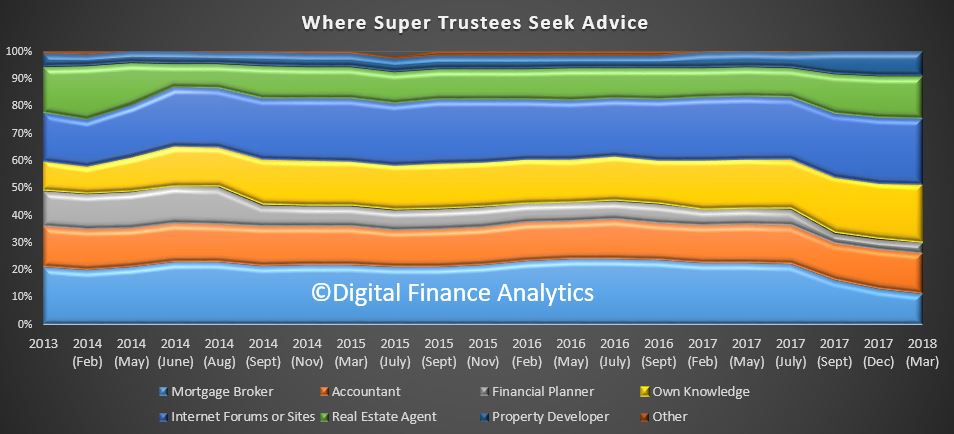

We also examine where trustees of SMSF’s obtain property investment advice. 24% obtain advice online from internet forums, 21% use their own knowledge, 15% use a real estate agent, 15% also use an accountant and 11% use a mortgage broker. We noted a 2% drop in those using a mortgage broker compared with December.

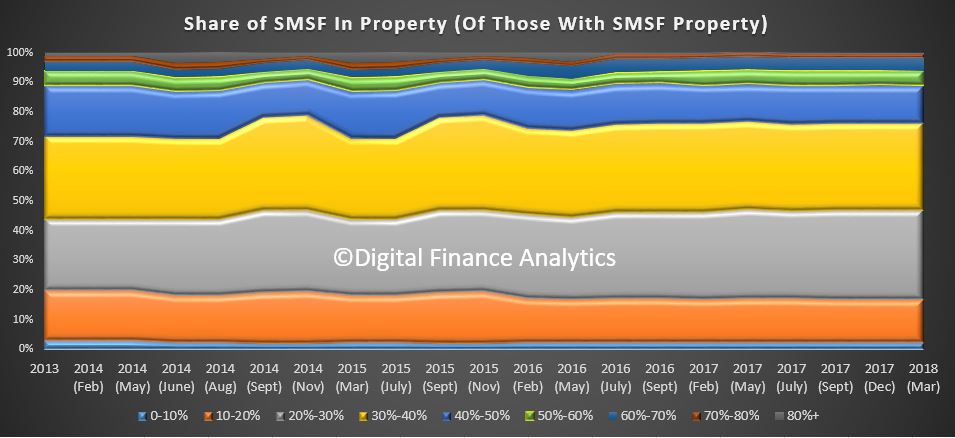

Finally, the asset allocation of a SMSF into property varies, with 30% holding 20-30% of their funds in property, 29% holding 30-40%, and more than 11% holding more than half of their SMSF assets in property. Only a very small proportion hold more than 80% of their funds in property. The mix has not really varied significantly over time, but the proportion of all super funds with property assets has risen from just over 3% to more than 5%, and rising. Such non- recourse borrowing has been identified by APRA as higher risk, so in their new guidelines, banks will need to hold higher capital against these loans. In addition of course David Murray’s Financial System Inquiry (FSI) recommended that SMSF’s should not be able to leverage into property. We support that recommendation, which the Government rejected.

So standing back, it is clear that investors are getting skittish, hence the lower demand for property, as well as difficulty in gaining access to finance. This is why we think investment property demand will continue to fall. As they account for more than one third of all loans, this will put downward pressure on property prices.

Finally, the number of first time buyer investors – those who are going direct to the investment sector continues to fall, as can be seen from our analysis of ABS and DFA datasets.

The UK Property Investment Market could be a leading indicator of what is ahead for our market. But in the UK just 15% of all mortgages are for investment purposes (Buy-to-let), compared with ~35% in Australia. Yet, in a down turn, the Bank of England says investment property owners are four times more likely to default than owner occupied owners when prices slide and they are more likely to hold interest only loans. Sounds familiar?

According to a report in The Economist, “one in every 30 adults—and one in four MPs—is a landlord; rent from buy-to-let properties is estimated at up to £65bn ($87bn) a year. But yields on rental properties are falling and government policy has made life tougher for landlords. The age of the amateur landlord may be”.

Investing in the housing market has seemed like a one-way bet, with prices trending upwards in real terms for four decades, mainly because government after government has failed to loosen planning restrictions on building new houses. Now, however, there are signs that regulatory changes have begun to send the buy-to-let boom into reverse.

Yields on rental properties have fallen. House prices have risen faster than rents, in part because buy-to-letters have reduced the supply of housing available to prospective owner-occupiers while simultaneously increasing the supply of places to rent. Britain’s ratio of house prices to rents is now 50% above its long-run average. All this makes buy-to-let investment less lucrative. Data from the Bank of England suggest that yields in September were below 5%, their joint-lowest rate since records began in 2001, when they were above 7.5%.

One consequence of this could be a more stable financial system. Roughly 15% of mortgage debt is on buy-to-let properties. The Bank of England has warned that there are risks associated with this. One problem is that property investors buy when house prices are rising but sell when they are falling, making house prices more volatile. Buy-to-let landlords are also more likely to default than owner-occupiers. One reason is that doing so does not force them out of their home. Another is that buy-to-let mortgages are more likely to be interest-only (ie, where the principal is not repaid). That can be tax-efficient but it means that monthly repayments can jump sharply if interest rates rise. The Bank of England’s stress tests last month showed that the rate at which landlords’ loans turn sour could be four times greater than the rate for owner-occupiers’ loans. All things considered, the shrinking of the buy-to-let sector may come as a relief to regulators.

The future for buy-to-letters will not get much brighter. In January a tweak to the rules on capital-gains tax will increase the liabilities of landlords who register as businesses. Large institutional investors are moving on to buy-to-letters’ turf, hoping to benefit from their economies of scale to offer better-quality housing to tenants. It was good while it lasted, but the golden age for the amateur landlord may be over.