From The Conversation: The Reserve Bank cut interest rates on Tuesday because we aren’t spending or pushing up prices at anything like the rate it would like. And things are even worse than it might have realised.

As the board met in Martin Place in Sydney, in Canberra at 11.30 am

the Bureau of Statistics released details of retail spending in April,

one month beyond the March quarter figures the bank was using to make

its decision.

They show the dollars spent in shops fell in April, slipping 0.1%,

notwithstanding weakly growing prices and a more strongly growing

population.

The March quarter figures the board was looking at were adjusted for

prices. They show that the volume of goods and services bought, but not

the amount paid for them, fell in seasonally adjusted terms during the

March quarter.

Adjusted for population, the volume bought would have fallen further.

We’ll know more on Wednesday

The Bureau of Statistics will release population-adjusted figures as part of the national accounts on Wednesday.

The figures for the September quarter show that income and spending

per person barely grew. The figures for the December quarter show income

and spending per person fell.

A second fall in the March quarter will mean two in a row – what some people call a per capita recession.

We’ve been doing it by ourselves. As Reserve Bank Governor Philip Lowe said in announcing the rates decision on Tuesday:

The main domestic uncertainty continues to be the outlook for

household consumption, which is being affected by a protracted period of

low income growth and declining housing prices.

The bank wants both inflation and employment higher, and it wants us

to spend more in order to do it. Lower rates should help, although not for everybody.

Lowe acknowledged this is a speech to a Sydney business audience on

Tuesday night, but he said households paid two dollars in interest for

every one dollar of interest they received. So while rate cuts hurt

savers, they benefit borrowers by more, and over time should benefit all

households by boosting the economy. They also drive the dollar lower,

making Australian businesses more competitive.

Tuesday’s cut should free up an extra A$60 a month for a typical mortgage holder. Another one will free up a total of $120.

It’s not much, and there’s doubt about whether it will do much, but

interest rates are about the only tool the Reserve Bank has.

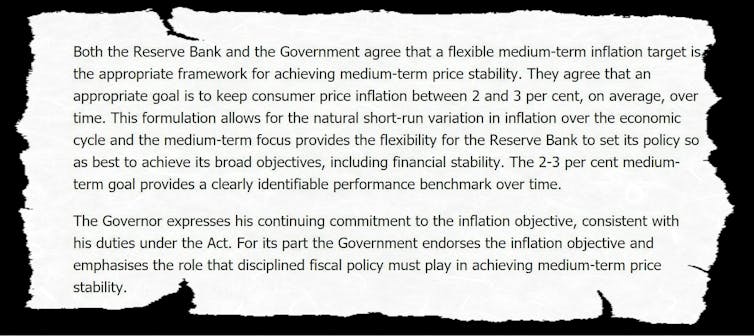

It is required by its agreement with the government to aim for an inflation rate of between 2% and 3%, “on average, over time”.

Treasurer and Reserve Bank Governor, Statement on the Conduct of Monetary Policy, September 19, 2016.

Reserve Bank of Australia

Uncomfortably for Governor Lowe, underlying inflation (abstracting

from unusual moves which are quickly reversed) has been below 2% ever

since he was appointed governor in late 2016.

Explaining his push for higher inflation to a business audience in

Sydney on Tuesday night he said that while adherence to the target was

intended to be flexible, that flexibility was “not boundless”.

If inflation stays too low for too long, it is possible that inflation

expectations move lower – that Australians come to expect sub-2% inflation

on an ongoing basis. If this were to happen, it would be harder to achieve the

medium term inflation goal. So we need to guard against this possibility.

He told the business audience that while for some years the bank and

others had thought full employment meant an unemployment rate of 5%, the

absence of inflation at 5% and the persistence of underemployment

(where people wanted more hours) meant it could and should go lower.

Our judgement now is that we can do better than this – that we can sustain an

unemployment rate of 4 point something.

Lower interest rates should help by making it easier to businesses to

borrow to expand, and giving consumers something in their pockets to

buy from them.

If you don’t succeed…

If that doesn’t happen, the bank will cut again.

Tuesday’s statement as good as said so:

The board will continue to monitor developments in the labour market

closely and adjust monetary policy to support sustainable growth in the

economy and the achievement of the inflation target over time.

Tuesday’s cut and the next will take the bank into uncharted waters,

where its so-called cash rate – what it pays to banks to deposit money

with it overnight – is close to zero.

As far as can be discerned it has never been that low in the 100+

years the Reserve Bank has been in operation, originally as the

Commonwealth Bank of Australia.

Should inflation still not pick up and employment still not fall as

far as it believes it could, it will have to effectively cut its cash

rate below zero, forcing cash into the hands of banks by aggressively

buying government bonds, giving them little choice but to lend it to

households and businesses, in a process known as quantitative easing. It

has been done in the United States, Europe, the United Kingdom and

Japan, and is by now anything but unconventional.

Governor Lowe would prefer the government to pull its weight by

cutting tax and boosting spending, especially on infrastructure, and by

policies that make Australia more productive.

He said so on Tuesday night

the best approach to delivering lower unemployment and a stronger

economy is through structural policies that support firms expanding,

investing, innovating and employing people. As we ease monetary policy,

it is in the country’s interest that other policy options are considered

too.

Treasurer Josh Frydenberg gets it.

He pointed out on Tuesday that the yet-to-be-approved tax offsets in

the budget will give Australians on up to $126,000 a cash bonus of up to

$1,080 when they submit this year’s tax return, far more than the rate

cut.

His biggest concern, and the biggest concern of the governor, might

be that they don’t spend it. Another concern would be that the banks

don’t pass the rate cut on.

The ANZ has said it will only cut mortgage rates by 0.18 points

instead of the full 0.25, a decision Frydenberg said “let down”

customers. Westpac has cut by only 0.20 points. The National Australia

and Commonwealth banks have passed on the cut in full.

On Tuesday night in Sydney Governor Lowe addressed the question of whether the banks should have passed on the full cut head on:

My usual practice in answering this question has been to explain that there are a

range of other factors that influence mortgage pricing, and then say “it all depends”.

Today, though, I would like to break with my usual practice and

provide a clearer

answer. And that is: Yes. There has been a substantial reduction in the

cost of banks raising funds in wholesale markets. Average rates on

retail deposits have also come down.

This means that the lower cash rate should be fully passed through

into standard variable mortgage rates. Full pass-through would also mean

that the economy receives the full benefit of today’s policy decision.

The Governor is concerned that, for their own reasons, lenders such

as ANZ and Westpac are forcing him to cut rates lower than he should and

making an already difficult job harder.

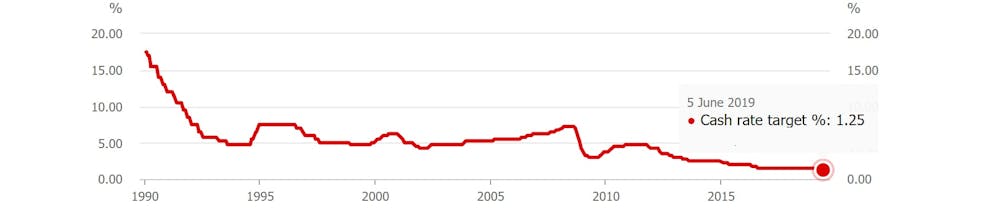

If he has to cut further he will, but with the cash rate at just 1.25%, he would dearly love not to have to.

Author: Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University

Governor Lowe explains. In summary: Expect more cuts. Banks should pass on the cuts. Borrowers will benefit more than savers in the interests of the economy. The exchange rate will fall. Spare capacity in the economy needs to be utilised.

At its core, today’s decision was taken to support employment growth and to provide greater

confidence that inflation will be consistent with the medium-term target.

I want to emphasise that the decision is not in response to a deterioration in our economic outlook since the previous update was published in early May. The economic outlook remains reasonable, with the main downside risk being the international trade disputes, which have intensified recently. The Australian economy is still expected to strengthen later this year, supported by the low level of interest rates, a pick-up in growth in household disposable income, ongoing investment in infrastructure and a brighter outlook for the resources sector. So today’s decision does not reflect a weaker outlook. Rather it reflects the fact that, even with the expected pick-up in growth, the Australian economy is likely to have spare capacity for a while yet.

Today’s easing of monetary policy will help us make further inroads into that spare capacity.

It will assist with faster progress on reducing unemployment and will help achieve more assured

progress towards the inflation target. So that is our rationale.

I know that many of you are likely to have questions about today’s decision. I would like to

take this opportunity to provide answers to some of your probable questions. I am also happy to

answer your other questions after my prepared remarks.

The four questions that I thought it would be useful to answer are the following:

Why did the Board act today, after having held the cash rate steady for more than 2½ years?

Are there more interest rate reductions to come?

Should today’s reduction be fully passed through to mortgage rates? and

What about the savers – has the Board forgotten about them?

First, why move now, after holding steady for so long?

The answer is the accumulation of evidence. As you would expect, the Board is constantly sifting

through masses of data and seeking to understand what are often conflicting signals about the

economy. As we have gone about this task over recent times, there has been a progressive

accumulation of evidence in support of two conclusions.

The first is that inflation pressures are subdued and they are likely to remain so.

And the second and related conclusion is that there is still significant spare capacity in the

Australian labour market.

The most recent batch of data has provided further evidence in support of both conclusions. The

March quarter CPI was low and it was below expectations, as was the previous reading on

inflation. In addition, the wage data for the March quarter confirmed that wages growth remains

subdued, although it has picked up from a year ago. And the recent labour market report also

confirmed that strong employment growth is not making material inroads into spare capacity in

the labour market. The Board judged that the accumulation of this further evidence meant that it

was now appropriate to adjust monetary policy.

Given the importance of these two conclusions, I would like to elaborate a little on them and

explore their implications.

The subdued inflation pressures reflect a number of factors. These include slow growth in wages,

increased competition in retailing, the adjustment in the housing market – with rents

increasing at the slowest pace in decades – and various government initiatives to reduce

the cost of living pressures on households. These factors are all putting downward pressure on

prices and they are likely to remain with us for some time yet.

Collectively, these factors have contributed to delayed progress in returning inflation to the 2–3 per cent

target range. In underlying terms, inflation has now been below 2 per cent for three

years and the latest reading was 1½ per cent. Looking forward, inflation is still

expected to increase, but it is unlikely to be comfortably within the 2–3 per cent

range for some time yet. So the progress on returning inflation to target is more gradual than

we had hoped.

It is important to remember, though, that our inflation target is intentionally flexible and that

the Australian economy has benefited from this flexibility over the past 25 years. The

Board is aiming to ensure that Australia has an average inflation rate of between 2 and 3 per cent

over time. The focus is on the average and the medium term.

We have never sought to have inflation always between 2 and 3 per cent. The RBA adopted flexible inflation targeting before other central banks, and this flexibility has served us well. It has allowed the Board to set monetary policy so as best to achieve its broad objectives, with the ultimate aim of contributing to the economic prosperity and welfare of the people of Australia. It has also allowed the Board to look through temporary factors affecting inflation.

This flexibility, however, is not boundless. The point of our inflation target is to provide a

strong medium-term anchor that helps deliver low and stable inflation, which, in turn, is an

important precondition to sustainable growth in employment and incomes. If inflation stays too

low for too long, it is possible that inflation expectations move lower – that Australians

come to expect sub-2 per cent inflation on an ongoing basis. If this were to happen,

it would be harder to achieve the medium-term inflation goal. So we need to guard against this

possibility.

Moving on to our conclusion about spare capacity in the labour market.

For some years, most estimates of full employment, including our own, equated to an unemployment

rate of around 5 per cent – it was thought that if unemployment went below that

for too long, inflation would rise and become a problem. But, given the combination of the

labour market and inflation outcomes we have seen of late, our judgement now is that we can do

better than this – that we can sustain an unemployment rate of 4 point something.

It is also worth noting that the supply side of the labour market is turning out to be more

flexible than we had earlier expected. The recent evidence is that when jobs are there, more

people join the labour force and other Australians stay in work longer. Reflecting this, the

participation rate is currently at a record high, despite demographic shifts that we anticipated

would reduce participation. It is also the case that people are prepared to work extra hours

when there is strong demand for their labour. Together, these observations support the

conclusion that there is still spare capacity in the labour market and this is likely to remain

the case for a while yet. The recent data have given us more confidence in this assessment and

we have responded to this.

Over the past few years, one concern has been that lower interest rates could add to the

medium-term risks facing the Australian economy as a result of high household debt. We need to

keep a close eye on this issue, but this concern has receded recently. Lending practices have

been tightened considerably and many lenders have become quite risk averse. The demand for

credit has also slowed due to the changed dynamics of the housing market and slower income

growth. So the risks on this front look to be less than they were previously.

This brings me to the second question: are interest rates going to be reduced further?

The answer here is that the Board has not yet made a decision, but it is not unreasonable to expect a lower cash rate. Our latest set of forecasts were prepared on the assumption that the cash rate would follow the path implied by market pricing, which was for the cash rate to be around 1 per cent by the end of the year. There are, of course, a range of other possible scenarios and much will depend on how the evidence evolves, especially on the labour market.

If you accept the argument that a sustainably lower rate of unemployment in Australia is

achievable, the question that we should all be thinking about is: how do we get there?

It is possible that the current policy settings will be enough – that we just need to be

patient. But it is also possible that the current policy settings will leave us short. Given

this, the possibility of lower interest rates remains on the table. Monetary policy does have an

important role to play and we have the capacity to play that role if needed.

In saying that, I also want to recognise that monetary policy is not the only option. There are

certain downsides from relying just on monetary policy and there are limitations on what,

realistically, can be achieved. So, as a country, we should also be looking at other options to

reduce unemployment.

One option is for fiscal support, including through spending on infrastructure. This spending not only adds to demand in the economy, but it also adds to the economy’s productive capacity. So it works on both the demand and supply side.

Another option is structural policies that support firms expanding, investing, innovating and

employing people.

All three options are worth thinking about.

From my perspective, the best option is the third one – structural policies that support

firms expanding, investing, innovating and employing people. A strong dynamic business sector is

the best way of creating jobs. Structural policies not only help with job creation, but they can

also help drive the productivity growth that is the main source of improvement in our living

standards. So, as a country, it is important that we keep focused on this.

I will now change tack and move to the third question: should today’s reduction in the cash

rate be fully passed through to mortgage rates?

My usual practice in answering this question has been to explain that there are a range of other

factors that influence mortgage pricing, and then say ‘it all depends’. There are

often reasonable explanations for why the standard variable mortgage rate does not move in

lock-step with the cash rate.

Today, though, I would like to break with my usual practice and provide a clearer answer. And that is: Yes, this reduction in the cash rate should be fully passed through to variable mortgage rates.

This answer is based on recent reductions in bank funding costs. Not only have these costs

declined as a result of the change in monetary policy, but they have also declined because of

movements in market-based spreads. Last year, these spreads increased and most lenders responded

by increasing their standard variable rates by around 15 basis points. Over recent months,

these spreads have reversed all the increase that occurred last year and returned to their 2017

levels. The result is that there has been a substantial reduction – at both the short end

and the long end – in the cost of banks raising funds in wholesale markets. Average rates

on retail deposits have also come down. This means that the lower cash rate should be fully

passed through into standard variable mortgage rates. Full pass-through would also mean that the

economy receives the full benefit of today’s policy decision.

That brings me to the final question: what about the savers, have we forgotten about them?

I know this question is on the minds of a lot of Australians, especially older Australians. I am

reminded of this daily as people write to me telling me how the already low deposit rates are

affecting their income. I am expecting to receive more such letters and emails after today’s

decision.

The Board had a thorough discussion of this issue at our meeting today. We recognise that many Australians have saved hard and rely on interest from term deposits to support their income and spending. Today’s decision will reduce their income from this source and we understand why they would be disappointed with the outcome of today’s meeting.

At the same time as paying close attention to this issue, the Board considered what was best for the overall economy. Our judgement is that lower interest rates will help the economy as a whole. At the moment, this benefit is likely to come mainly through two channels. The first is a lower value of the exchange rate than otherwise would have been the case. The second is a boost to the disposable income of the household sector. In aggregate, the household sector pays around two dollars in interest for every dollar it receives in interest income. So, in aggregate, lower interest rates reduce the net interest payments of the household sector and so boost overall disposable income.

In time, we would expect the lower exchange rate and the boost to disposable income to lead to more jobs, lower unemployment and a stronger economy. This should benefit us all, although I recognise that in the short run the effects are felt unevenly across the community.

It is partly because of this unevenness that I want to repeat a point I made in answering the

second question. And that is: the best approach to delivering lower unemployment and a stronger

economy is through structural policies that support firms expanding, investing, innovating and

employing people. These policies can have distributional effects too, but the benefits are more

broadly based. So, as I said, as we ease monetary policy, it is in the country’s interest

that other policy options are considered too.

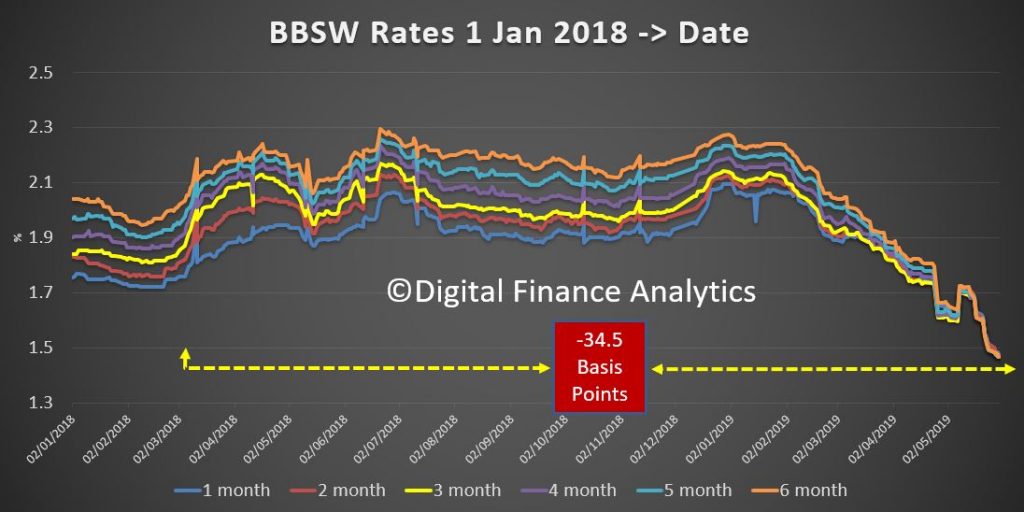

Given the BBSW has moved towards the banks in recent times, there is no excuse not to pass the full cut to existing borrowers. The question is, will they?

The RBA will continue to look at the labour figures, which suggests a rise in unemployment (which we expect) will lead to more rate cuts.

The Aussie USD rate rose, which is not what the RBA intended.

This is what the RBA said:

At its meeting today, the Board decided to lower the cash rate by 25 basis points to

1.25 per cent. The Board took this decision to support employment growth and provide greater

confidence that inflation will be consistent with the medium-term target.

The outlook for the global economy remains reasonable, although the downside risks stemming from the

trade disputes have increased. Growth in international trade remains weak and the increased uncertainty

is affecting investment intentions in a number of countries. In China, the authorities have taken steps

to support the economy, while addressing risks in the financial system. In most advanced economies,

inflation remains subdued, unemployment rates are low and wages growth has picked up.

Global financial conditions remain accommodative. Long-term bond yields and risk premiums are low. In

Australia, long-term bond yields are at historically low levels. Bank funding costs have also declined

further, with money-market spreads having fully reversed the increases that took place last year. The

Australian dollar has depreciated a little over the past few months and is at the low end of its narrow

range of recent times.

The central scenario remains for the Australian economy to grow by around 2¾ per cent in

2019 and 2020. This outlook is supported by increased investment in infrastructure and a pick-up in

activity in the resources sector, partly in response to an increase in the prices of Australia’s

exports. The main domestic uncertainty continues to be the outlook for household consumption, which is

being affected by a protracted period of low income growth and declining housing prices. Some pick-up in

growth in household disposable income is expected and this should support consumption.

Employment growth has been strong over the past year, labour force participation has been increasing,

the vacancy rate remains high and there are reports of skills shortages in some areas. Despite these

developments, there has been little further inroads into the spare capacity in the labour market of

late. The unemployment rate had been steady at around 5 per cent for some months, but ticked

up to 5.2 per cent in April. The strong employment growth over the past year or so has led to

a pick-up in wages growth in the private sector, although overall wages growth remains low. A further

gradual lift in wages growth is expected and this would be a welcome development. Taken together, these

labour market outcomes suggest that the Australian economy can sustain a lower rate of

unemployment.

The recent inflation outcomes have been lower than expected and suggest subdued inflationary pressures

across much of the economy. Inflation is still however anticipated to pick up, and will be boosted in

the June quarter by increases in petrol prices. The central scenario remains for underlying inflation to

be 1¾ per cent this year, 2 per cent in 2020 and a little higher after

that.

The adjustment in established housing markets is continuing, after the earlier large run-up in prices

in some cities. Conditions remain soft, although in some markets the rate of price decline has slowed

and auction clearance rates have increased. Growth in housing credit has also stabilised recently.

Credit conditions have been tightened and the demand for credit by investors has been subdued for some

time. Mortgage rates remain low and there is strong competition for borrowers of high credit

quality.

Today’s decision to lower the cash rate will help make further inroads into the spare capacity

in the economy. It will assist with faster progress in reducing unemployment and achieve more assured

progress towards the inflation target. The Board will continue to monitor developments in the labour

market closely and adjust monetary policy to support sustainable growth in the economy and the

achievement of the inflation target over time.

An “overwhelming majority” of economists are forecasting that the

Reserve Bank of Australia will alter the cash rate tomorrow for the

first time since August 2016. Below, two analysts explain the ripple

effects likely to spread across the economy as a result.

The good news

Martin North, principal of Digital Finance Analytics, expects there

will not only be a cut tomorrow, but another to follow later in the year

due to the underperforming economy and dramatic drop in household

consumption.

He believes it is highly likely the banks would pass along the savings to their customers, attributing his confidence to three major factors: the Bank Bill Swap Rate (BBSW) “dropping dramatically” over the last several months, the “heavy pressure” the RBA has put on banks to ensure they would pass a rate cut on, and the banks’ need to bolster consumer goodwill.

“The PR effect if the banks didn’t respond when rates were cut would be dramatic. The banks are in reputation-rebuilding mode. I think they would want to show that they are responsive to signals from the Reserve Bank,” North explained.

According to the financial analyst, the RBA hopes that banks would

lower interest rates even for existing borrowers – a departure from the

trend evidenced in the last several months – improving discretionary

household spending and stimulating the economy at large.

The bad news

Unfortunately, North has expressed significant doubt that cutting the rate will achieve this goal.

“The overall economic impact of the RBA’s adjustment will likely only have a marginal effect,” he said.

“In fact, it may have an unintended consequence because cutting that

rate basically signals weakness. Sentiment might turn negative,

particularly from international investors.”

“The exchange rate will go down, which means we’re likely to import

inflation from overseas – high oil prices and high import costs. That

may have a limiting impact on the Reserve Bank’s ability to cut further.

But I suspect they might be forced to,” he continued.

Potentially rising unemployment, flat income growth, and the rising

cost of living seem likely to claim any savings created by a rate cut.

The unexpected outcome

While CoreLogic research analyst Cameron Kusher

believes a cut is the most likely decision to be made at tomorrow’s

meeting, he could understand if the RBA chose to hold this month.

The housing market may be exhibiting the earliest signs of recovery,

but according to Kusher, “It’s not a cut about housing. It’s a cut

related to economic growth and inflation.”

He added, “Waiting another month would allow the RBA to gather more

evidence as to whether the housing market is truly improving, and it

will afford them the luxury of seeing the March quarter GDP figures

which are released the day after their board meeting on June 5.”

If the report was to show another weak quarter of economic growth, it

would “surely trigger the need for a 25 basis point or even 50 basis

point cut to the cash rate in July.”

Waiting would also allow for another month’s data regarding the

labour force to be examined, with an increase in the unemployment rate

more solidly proving it’s a trend.

Given the “slow and measured approach” that the RBA has shown in its

cash rate considerations thus far, it would not be shocking for it to

wait for the above data to be accessible before taking action.

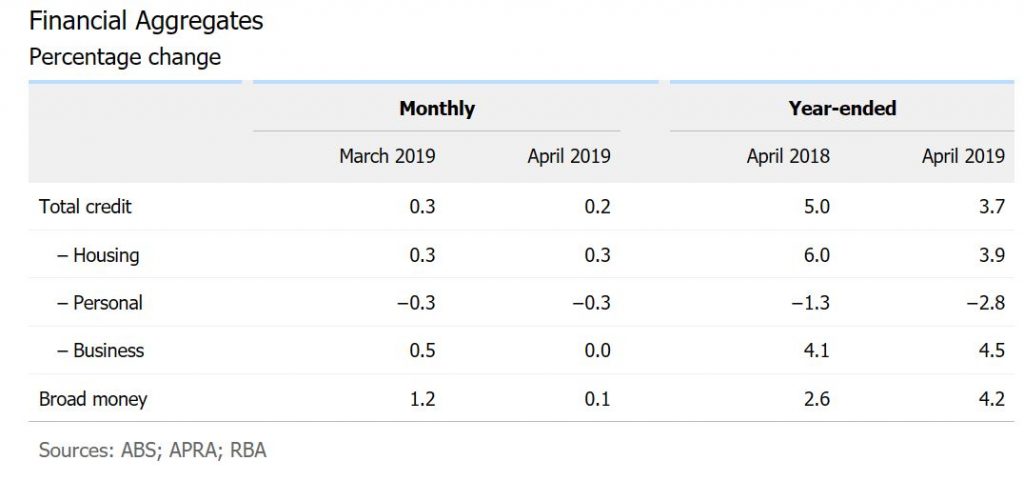

We look at the latest stats from RBA and APRA on credit growth. Home lending is STILL growing at 3.9% per annum – yet we are about to stir up the monster some more – “you cannot be serious!”

Once again on the last working day we get the latest credit

data from both the RBA and APRA. And fair enough, this is before the election,

and the recent spate of “unnatural acts designed to kick start credit growth,

but the trends before this are clearly down.

Here we are talking about the net stock of loans – rather than new loan

flows (so we see the net of old loans closed, refinanced, and new loans written).

We will need to wait for the ABS series in a couple of weeks to get the flow stats.

The RBA provides an overview, and a seasonally adjusted

series, including the non-bank sector. APRA provides data for the banking

sector – ADI’s or authorised depository institutions.

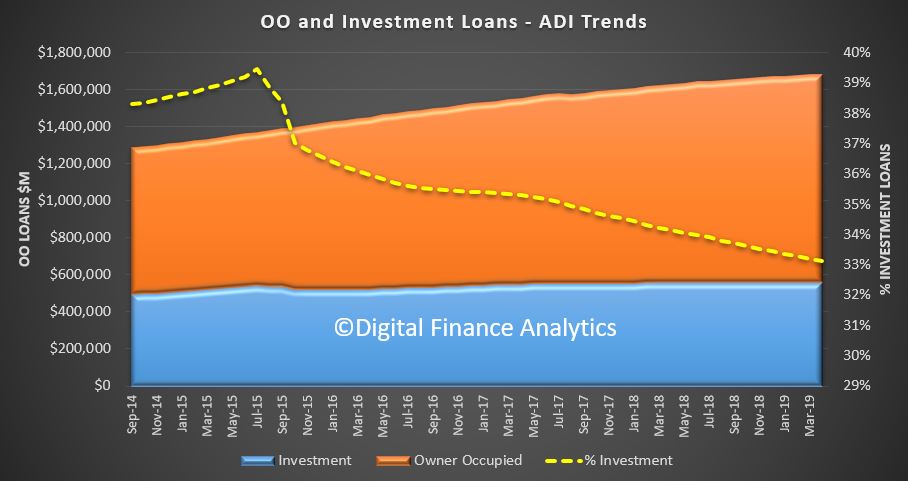

Total credit in the system, is still growing, with housing

lending up to $1.83 trillion dollars, with owner occupied lending accounting

for $1.23 trillion and investor loans 0.59 trillion. Business lending was 0.96

Trillion dollars and personal credit was $146 million dollars. So, you can see

how significant housing credit – and yes, it is STILL growing.

Of that $1.83 trillion dollars for housing, $1.68 trillion

comes from the banks, as reported by APRA.

Of that $1.12 trillion dollars is for owner occupied housing, and 0.55

trillion dollars for investors. The rest is non-banks, institutions who can

lend, but do not fund these loans from holding bank deposits. APRA now have

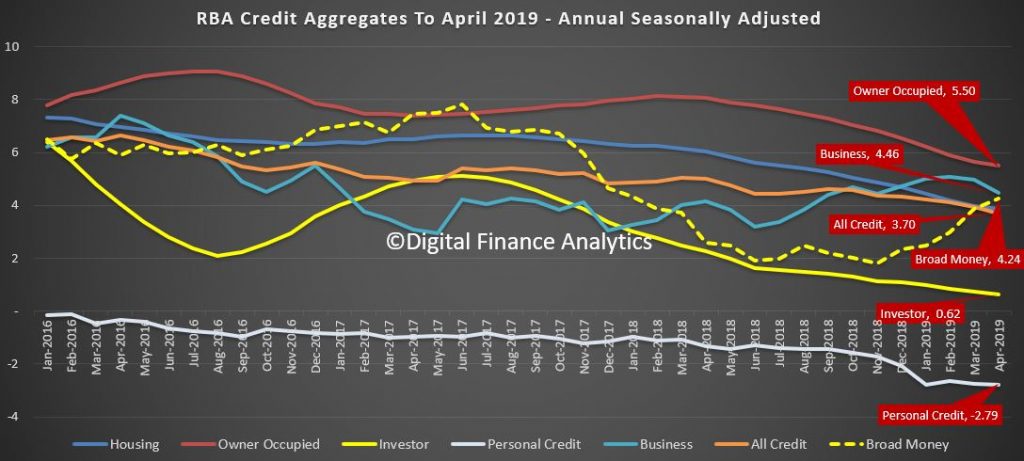

responsibility for these too but is not that actively engaged. So, to the rate of change of credit growth.

We know that housing credit growth has been slowing as

demand has slowed, and lending standards tightened, in response to APRA’s

interventions and the Royal Commission. But the stark reality is that business

lending is also flat according to the RBA.

In fact, last month, total credit grew by only 0.16% and

this is the weakest since early 2013.

Overall housing credit was up by 0.28% in the month, and personal

credit declined by 0.3%

Annual credit growth slowed to 3.7%, the weakest since November

2013 and the trends are clear.

Slowing Housing credit growth is a large element in the

numbers, as we have been tracking. The latest annual figure is just 3.9%, and

this is the lowest ever in the series which started back in the late 1970s.

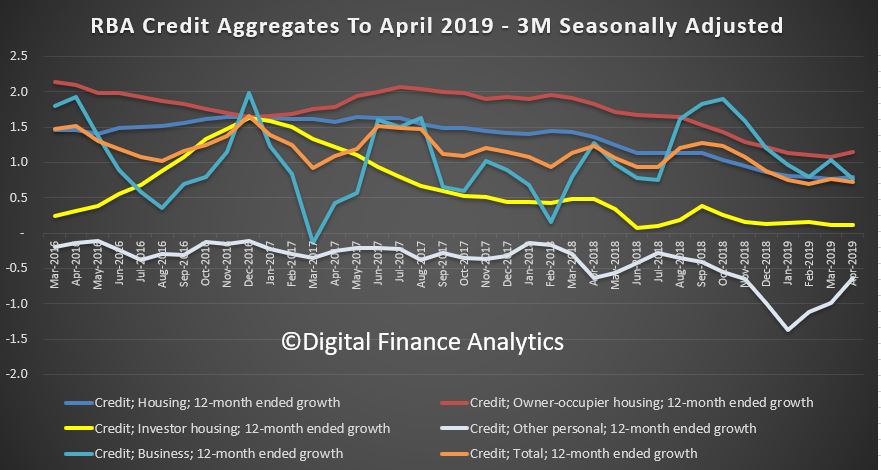

Looking at the three-month series you might argue that the

rate of decline is easing just a little, there is not much here really to get

excited about. Of course, most of the commentators are now looking ahead

following the Coalitions return to power. The RBA I think cut rates on Tuesday,

which is the first cut since August 2016. And of course, APRA is consulting on

a proposal to loosen the interest rate buffer test.

I won’t repeat here the significant downside forces which

will make a rebound in housing lending difficult, other than to say, the

Coalition has promised a home price recovery, so they have to try and engineer

it any cost – even if the debt balloon inflates further.

Investor housing momentum is still very weak, and there is

little to suggest this will change soon – though some might try to sell into

any more optimistic season. So, its down to first time buyers, and those

seeking to trade-up.

Turning to business credit, this grew by 4.5% over the past

year, up from 3.0% for 2017 but is easing back from gains of 6.4% in 2015 and

5.5% in 2016. In fact, this is an

important issue, as business lending and confidence are easing back – not a

good sign.

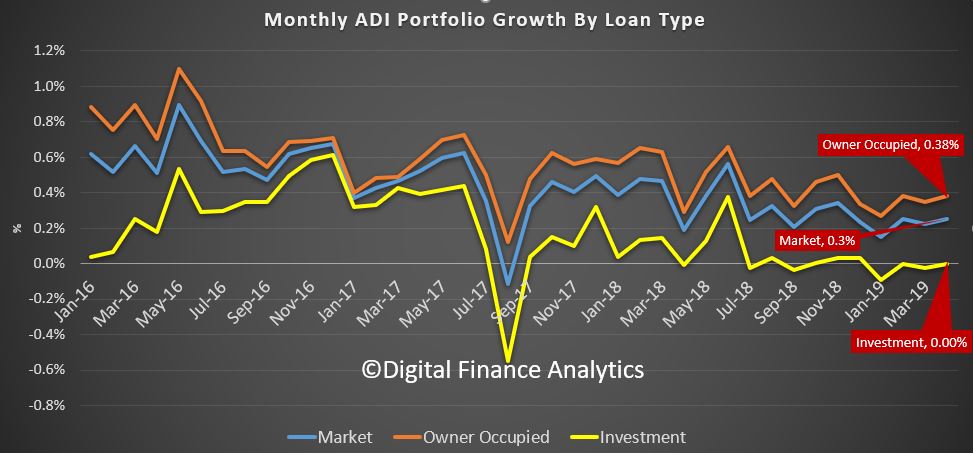

APRA’s data showed that owner occupied lending rose 0.38% in

the month, investor lending was flat, and the market growth was 0.3%.

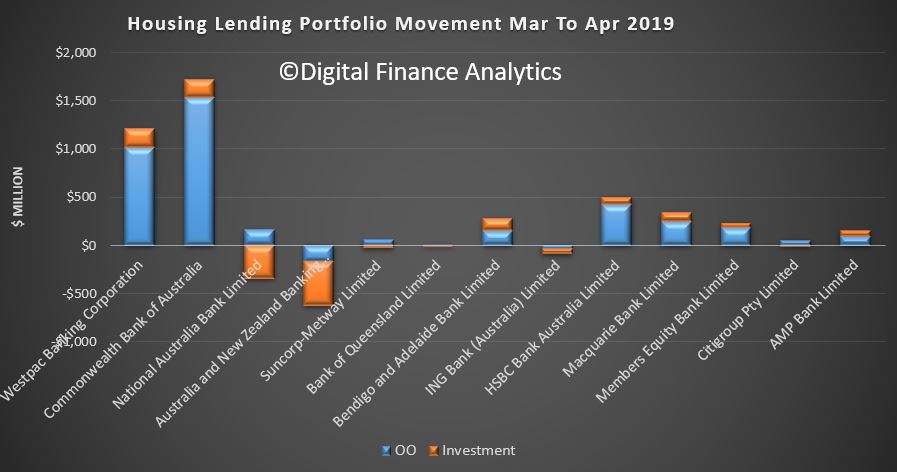

And our analysis of the individual bank data shows that housing market shares did not change that much, although CBA and Westpac were more active in net terms last month, though mainly in owner occupied lending. NAB and ANZ dropped more investor loans.

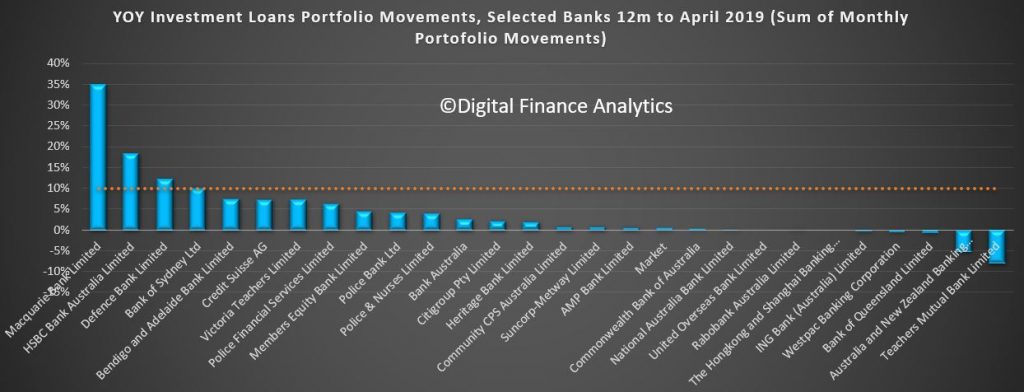

The 12-month portfolio moves for investor loans reveals the majors below the market. Macquarie and HSBC are leading the charge.

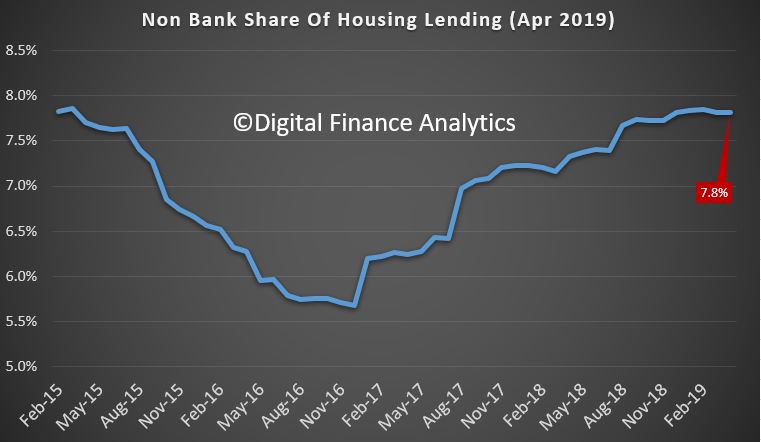

But a comparison of the gap between the Bank lending and RBA data shows the non-banks are still growing their books faster. Overall, they are running at an annualised 7.8%.

And analysis of owner-occupied lending by the non-banks shows it is still at 12.8%, compared with 2.1% for investor loans, but both above system.

So, standing back, the pre-election trends were weakening,

the non-banks were making hay, and investors are still on the sidelines. Now it

will be interesting to see if the so-called sentiment swing, and hype shows up

in the numbers in the next couple of months.

But to state the obvious, a growth rate of 3.9%

for credit for households even now is way stronger than wages growth or

inflation, so the debt burden is building further, and yet the policy settings

are about to be shifted to encourage more of the same. Hardly sensible.

The RBA’s aggregates to April 2019 shows s further slowing, with housing credit over 12 months down to a growth rate of 3.9%.

We will publish more analysis on this later, but no surprise given the unnatural acts now in the pipeline to try and reverse the trend. Plus an analysis of the APRA data, which also looks pretty weak.

The RBA released their minutes today, and things are looking less rosy, even though their rose-tinted glasses.

International Economic Conditions

Members commenced their discussion of the international economy by observing that global growth had

eased in the second half of 2018 and looked to have continued at around this more moderate rate in 2019.

Growth in Australia’s major trading partners was also expected to continue at around this slower

pace over 2019 and 2020. Members also observed that the outlook for China continued to be a significant

uncertainty for the global growth outlook, as were trade tensions, which had escalated again between the

United States and China immediately prior to the meeting. Global financial conditions had become more

accommodative since the turn of the year. Members noted that this could lead to stronger growth than

expected, although there were still risks of events occurring that could lead to both tighter financial

conditions and lower global growth.

March quarter GDP growth had been stronger than expected in the United States and the euro area, but

had been quite weak in a number of trade-intensive economies in east Asia. The latest monthly data had

shown that growth in Chinese industrial production, fixed asset investment and total social financing

had increased, suggesting momentum had picked up in response to targeted policy easing by the Chinese

authorities. Conditions in Chinese property markets had also strengthened. Members noted that economic

sentiment in China had improved since the beginning of the year, partly because small to medium-sized

businesses were obtaining improved access to finance and government infrastructure spending was boosting

demand.

Members noted that the sharp slowing in global trade had been related to slowing growth in China. The

decline in the value of Chinese imports had been broadly based across regions, although the large

decline in the value of trade with the United States suggested that trade diversion as a result of new

tariffs had also been a factor. Growth in China was expected to slow gradually over the forecast period

to the middle of 2021. This was expected to continue to weigh on external demand for trade-intensive

economies in east Asia and the euro area; recent data on export orders in east Asia had been

subdued.

Members discussed various longer-term policy initiatives in China, including policies on investment

abroad and modernisation of China’s manufacturing sector. China’s infrastructure

investment abroad had served to support land and sea trade routes, although there had been some

challenges that Chinese authorities had been addressing. Members also noted the authorities’

efforts to promote innovation, particularly in China’s technology sector, and to upgrade the

Chinese manufacturing sector significantly.

For some economies, the slowing in external demand had been accompanied by lower investment and

investment intentions. In some east Asian economies in particular, including South Korea, the turn in

the cycle in the global electronics industry had dampened exports and investment. Members noted that

firms would also be less likely to commit to long-term investments given the uncertainty around the

evolution of international trade policy.

In many economies, domestically focused sectors, such as services and retail trade, had been more

resilient than externally focused sectors. This was particularly the case in the advanced economies,

where tight labour market conditions had supported growth in spending. Unemployment rates had remained

around multi-decade lows in many advanced economies and wages growth had increased noticeably. In the

United States and Japan, recent wage increases had been larger for low-wage earners than high-wage

earners.

Core inflation had remained subdued in most economies and, following weaker inflation data in the

United States, was below target in the three major advanced economies.

There had been some large movements in commodity prices over recent months. Iron ore prices had

remained high as a result of supply disruptions in Brazil and Australia. Oil prices had also risen,

which had led to higher headline consumer price inflation in most economies and was expected to flow

through to higher prices for Australian liquefied natural gas exports over the following couple of

quarters. As a result, the forecast for Australia’s terms of trade had been revised higher, but

they were still expected to decline over the forecast period to the middle of 2021.

Domestic Economic Conditions

Members commenced their discussion of the domestic economy by noting that growth had been subdued in

the second half of 2018. Indicators of household consumption suggested that growth had remained subdued

in the March quarter. In addition, demand for new dwelling construction was expected to have remained

weak. These factors had been the main drivers of a downward revision to the domestic growth outlook in

the near term. Beyond 2019, these effects were broadly offset by upward revisions to export growth and

some newly announced mining investment projects. Members noted that, overall, the Bank expected

year-ended GDP growth to be 2¾ per cent over 2019 and 2020.

Growth in consumption had been weaker than expected in the second half of 2018 and retail sales data

for the March quarter suggested that this weakness had continued into 2019. Members noted that, as had

been the case for some time, the outlook for growth in consumption was a key uncertainty for the overall

growth outlook. The risks to consumption were tilted to the downside, given the extended period of low

income growth and the adjustment occurring in housing markets. The forecast for an improvement in growth

in consumption depended on an increase in growth in household disposable income over the forecast

period. The forecast increase in household disposable income growth was supported by employment growth,

a pick-up in wages growth and lower growth in tax payments, partly because of the introduction of the

low- and middle-income tax offsets announced in the Australian Government 2019-20 Budget. Members noted

that there was uncertainty about the outlook for fiscal policy and how this might affect the outlook for

growth in household disposable income.

Housing markets had remained weak in the preceding month. The rental vacancy rate in Sydney had

increased to the highest level in around 15 years and housing prices in established markets had

continued to decline. More positively, the pace of price declines had moderated and the modest recovery

in auction clearance rates since the start of the year had been sustained.

Information obtained through the Bank’s liaison program continued to indicate that sales

conditions for off-the-plan apartments and new detached housing had been difficult. The spike in

residential building approvals in February had largely been unwound in March, confirming that underlying

conditions for new dwelling activity remained weak. Data released since the previous meeting had shown

that the pipeline of residential work to be done had decreased in the December quarter, but remained

high. Members noted

that the forecasts for dwelling investment suggested that population growth could exceed growth in the

stock of housing towards the end of the forecast period, and that this possibility had been suggested by

a number of the Bank’s liaison contacts.

Survey measures of business conditions had moved a little higher in March and April and had remained

slightly above average, though well below the high levels that had prevailed throughout most of 2018.

Forward-looking indicators of non-mining business investment had been mixed; non-residential building

approvals had declined, but the pipeline of infrastructure work remained high. Non-mining business

investment was expected to support growth in output over the forecast period.

Mining investment had declined in the December quarter, but was expected to increase over the forecast

period, reflecting investment required to sustain current production levels and an expectation that a

number of new projects would commence towards the end of the forecast period. Recent trade data

suggested resource exports would contribute to output growth in the March quarter, and exports were

expected to contribute to output growth throughout the forecast period. Members noted that the forecast

pick-up in rural exports from 2020 depended on a return to normal weather conditions.

Public demand was expected to continue to support aggregate growth over the forecast period; a

significant share of this expenditure was associated with delivering goods and services to households,

such as the National Disability Insurance Scheme. Members noted that the Victorian Government had

announced measures to contain growth in labour costs in an environment of expected lower stamp duty

revenues.

Growth in employment in the March quarter had been strong, following similar outcomes over much of

2018. Most of the growth in employment since mid 2018 had been in full-time employment. The

unemployment rate had remained around 5 per cent in March. Members observed that conditions in

the labour market had signalled a significantly stronger pace of economic activity since mid 2018

than indicated by the GDP data. Leading indicators of labour demand had eased over recent months and

provided a mixed picture of the near-term outlook. As a result, employment growth was expected to be

similar to the growth rate of the working-age population in the near term. The unemployment rate was

expected to remain around 5 per cent through most of the forecast period, before declining to

around 4¾ per cent in 2021.

Members noted that the forecasts for the labour market suggested that there would be some spare

capacity in the labour market throughout the forecast period, although there was uncertainty about how

quickly the spare capacity would decline and how progress would feed into wage pressures. The central

forecast was for wages growth to pick up gradually. In combination, the forecasts for wages growth and

consumer price inflation implied that real consumer wage growth would be low but positive over the

forecast period.

The inflation data in the March quarter CPI release were noticeably lower than expected. The CPI

increased by 0.1 per cent (seasonally adjusted) in the quarter, while the underlying rate of

inflation was ¼ per cent. In year-ended terms, headline inflation was

1.3 per cent, with the underlying rate at 1½ per cent. The earlier exchange

rate depreciation and the drought-related increase in some food prices had led to relatively strong

retail price inflation in the March quarter. However, these inflationary pressures had been more than

offset by broad-based weakness in other CPI components, which was likely to be more persistent.

Rental inflation had remained low, driven by a marked slowing in rental inflation in Sydney; data on

newly advertised rents suggested that rents had started to pick up in Perth. Developer discounts and

incentives had weighed on the prices of newly built homes, particularly in Melbourne and Brisbane. A

range of government policy decisions had contributed to lower inflation in administered prices in recent

quarters. Market and survey-based measures of inflation expectations had declined in recent months, as

had been the case in other advanced economies.

Members noted that the recent CPI data had led the Bank to reassess the disinflationary effects of the

weak housing market. Combined with the lower GDP growth outlook, this had led to a downward revision to

the inflation outlook, although there was also some uncertainty about the persistence of downward

pressure from utilities and administered price changes and the effect of housing market weakness. The

central forecast scenario was for underlying inflation of around 1¾ per cent over 2019,

2 per cent over 2020 and a little higher after that.

Financial Markets

Members commenced their discussion of financial market developments by noting that global financial

conditions were accommodative and had eased significantly since the start of the year. Market

expectations for the future path of monetary policy in a number of economies had declined earlier in the

year, in line with guidance from major central banks that policy was likely to be more accommodative

than previously expected. The expectation that policy rates would remain little changed for some time

had contributed to very low levels of volatility in most financial markets.

In the United States, with inflation close to but a bit below target and the federal funds rate close

to neutral, the Federal Reserve (Fed) had reiterated that it would take a patient and flexible approach

to its policy decisions. While the Fed’s recent forecast update implied that one more policy rate

increase was likely by the end of 2020, market pricing implied that the Fed was expected to lower its

policy rate around twice over that period. At its April meeting, the European Central Bank had

reiterated that it expected policy rates to remain at current levels at least through to the end of

2019. The Bank of Japan had indicated that its very stimulatory policy settings will remain in place

until at least mid 2020. Market participants expected the next moves in policy rates in Canada, New

Zealand and Australia to be down.

Government bond yields remained at very low levels in the advanced economies, having declined since

late 2018 in line with downward revisions to growth and inflation projections, and the lowering of

policy rate expectations by market participants. In Germany and Japan, long-term bond yields were around

zero, close to the record lows of 2016. Members noted that Australian government bond yields had

declined by more than those in other major markets over the preceding six months, following

weaker-than-expected inflation data and a lower expected path for monetary policy. By contrast, Chinese

government bond yields had increased over the preceding month, as signs emerged that policy stimulus

there was providing support to economic activity.

Members noted that, following the brief inversion of segments of the US yield curve in March, the slope

of the US yield curve had increased a little in April. While market commentators had noted that past

episodes of yield curve inversion had tended to precede recessions, the decline in credit spreads and

rise in equity valuations in 2019 suggested market participants did not perceive this to be a particular

risk.

Members observed that financing conditions for corporations remained favourable. In the advanced

economies, corporate bond yields had declined, partly because of a decline in spreads. In addition,

equity prices had increased substantially since the start of 2019 to be at their highest levels in over

a decade, including in Australia.

In China, growth in total social financing had been steady in recent months and a little higher than in

2018, supported by bank lending and bond issuance. Off-balance sheet financing had continued to decline,

reflecting the authorities’ efforts to discourage riskier forms of financing. Members noted that

the Chinese authorities had introduced additional measures to encourage banks to lend to small private

sector firms, which had previously made use of off-balance sheet financing that was now less readily

available. Members also noted the substantial local government bond issuance to finance infrastructure

projects, which was a key part of the authorities’ stimulus measures.

In foreign exchange markets, volatility had remained low over the preceding month, including in most

emerging markets. Members noted, however, that risks remained pronounced for a small number of economies

with specific vulnerabilities, most notably Turkey and Argentina, where financial conditions had

tightened again.

The Australian dollar had depreciated a little following the weaker-than-expected March quarter CPI

release, but overall had been little changed over recent months and remained around the lower end of its

narrow range of the past few years. Members noted that this reflected the offsetting influences of the

rise in commodity prices and decline in Australian government bond yields relative to those in the major

markets over 2019. The difference between long-term government bond yields in the United States and

Australia had increased to a historically large 75 basis points.

Housing credit growth had slowed over the preceding year, but the monthly pace of growth had stabilised

over recent months. In three-month-ended annualised terms, growth in housing lending was around

4½ per cent for owner-occupiers and ½ per cent for investors. Loan

approvals also appeared to have stabilised in recent months. Members noted that, although lending

practices were tighter than they had been for some time, the decline in housing credit growth over the

preceding year had been driven largely by weaker demand for finance, associated with the decline in

housing prices.

The average interest rate charged on outstanding variable-rate housing loans had remained broadly

steady. While banks had increased their standard variable reference rates since mid 2018, rates on

new loans had remained materially below the average of those on outstanding loans. Members noted that

banks had recently reduced the rates charged on new fixed-rate loans.

Funding costs for the major banks had declined to record lows in preceding months, as the increase in

short-term money market rates in 2018 had been fully unwound and retail deposit rates had continued to

edge lower. Despite the low cost of funding, bank bond issuance in 2019 so far had been a little below

the average of recent years. Issuance of bonds by other corporations and of residential mortgage-backed

securities had been broadly in line with the average of recent years.

The pace of growth in business lending had been maintained in recent months at rates that were above

those of the preceding few years, driven by lending to large businesses. Lending to small businesses had

declined over the preceding year. Interest rates on variable-rate loans to large businesses, which are

linked to bank bill swap rates, had declined in the March quarter. Members observed that the rates

charged on small business loans remained markedly higher than those on large business loans, with the

gap between small and large business loan rates having doubled following the global financial

crisis.

Financial market participants’ expectations of cash rate cuts were brought further forward

following the release of the March quarter CPI. Financial market pricing implied that the cash rate was

expected to be lowered by 25 basis points within the next three months and again by the end of

2019.

Considerations for Monetary Policy

In considering the stance of monetary policy, members observed that growth in Australia’s major

trading partners had slowed, driven by a sharp slowing in global trade associated with slower growth in

China. Members also noted, however, that targeted stimulus measures in China appeared to be having an

effect and global financial conditions remained very accommodative. In a number of advanced economies,

labour markets had continued to tighten and wages growth had increased, but inflationary pressures had

remained subdued.

Domestically, members noted that the sustained low level of interest rates over recent years had been

supporting economic activity and had contributed to a decline in the unemployment rate. However,

household income growth had remained low and the March quarter inflation data indicated that the

inflationary pressures in the Australian economy were lower than previously thought.

After updating the forecasts for the new information, the central forecast scenario remained for

progress to be made on the Bank’s goals of reducing unemployment and returning inflation towards

the midpoint of the target, but at a more gradual pace than previously expected. Under the central

scenario, GDP growth had been revised lower in the near term, but was expected to pick up to be around

2¾ per cent over 2019 and 2020. The unemployment rate was expected to remain around

5 per cent over 2019 and 2020

before declining a little to 4¾ per cent in 2021. This implied that spare capacity would

remain in the economy for some time. Given this, and the subdued inflationary pressures across the

economy, underlying inflation was expected to be 1¾ per cent over 2019,

2 per cent over 2020 and a little higher after that.

Members noted that the central forecast scenario was based on the usual technical assumption that the

cash rate followed the path implied by market pricing, which suggested interest rates were expected to

be lower over the next six months. This implied that, without an easing in monetary policy over the next

six months, growth and inflation outcomes would be expected to be less favourable than the central

scenario.

At the same time, members also recognised that there were risks to the forecasts in both directions.

The risks to the global economy remained tilted to the downside, with uncertainty remaining around the

evolution of international trade policy. Domestically, the outlook for household consumption remained a

key uncertainty, with the risks tilted to the downside given ongoing low income growth and the

adjustment occurring in housing markets. On the upside, it was possible that the combined effects of

continued accommodative financial conditions, the increase in Australia’s terms of trade, a

renewed expansion in the resources sector and the expected lift in household disposable income growth

would result in stronger growth in output than in the central forecast scenario.

Members discussed the outlook for the domestic labour market in some detail. As in the previous

meeting, members discussed the scenario where inflation did not move any higher and unemployment trended

up, recognising that in those circumstances a decrease in the cash rate would likely be appropriate. As

noted at the previous meeting, members recognised that the effect on the economy of lower interest rates

could be expected to be smaller than in the past, given the high level of household debt and the

adjustment that was occurring in housing markets. Nevertheless, a lower level of interest rates could

still be expected to support the economy through a depreciation of the exchange rate and by reducing

required interest payments on borrowing, freeing up cash for other expenditure.

In light of the recent run of inflation data, the Board then discussed the likelihood that the economy

could sustain a stronger labour market with lower rates of unemployment than previously estimated, while

achieving inflation consistent with the target. In this context, members observed that the recent

international experience was that inflation had remained low despite historically low rates of

unemployment. Given the international evidence and the recent Australian inflation data, members agreed

that a further decline in the unemployment rate would be consistent with achieving Australia’s

medium-term inflation target. Given this, members considered the scenario where there was no further

improvement in the labour market in the period ahead, recognising that in those circumstances a decrease

in the cash rate would likely be appropriate.

Taking into account all the available information, including the various uncertainties about the

outlook, members judged that it was appropriate to hold the stance of monetary policy unchanged at this

meeting, noting that holding monetary policy steady had enabled the Bank to be a source of stability and

confidence over recent years. In view of the spare capacity that remained in the economy, however,

members agreed that it was important to continue to pay close attention to developments in the labour

market and set monetary policy to support sustainable growth in the economy and achieve the inflation

target over time.

The Decision

The Board decided to leave the cash rate unchanged at 1.5 per cent.

Blog")