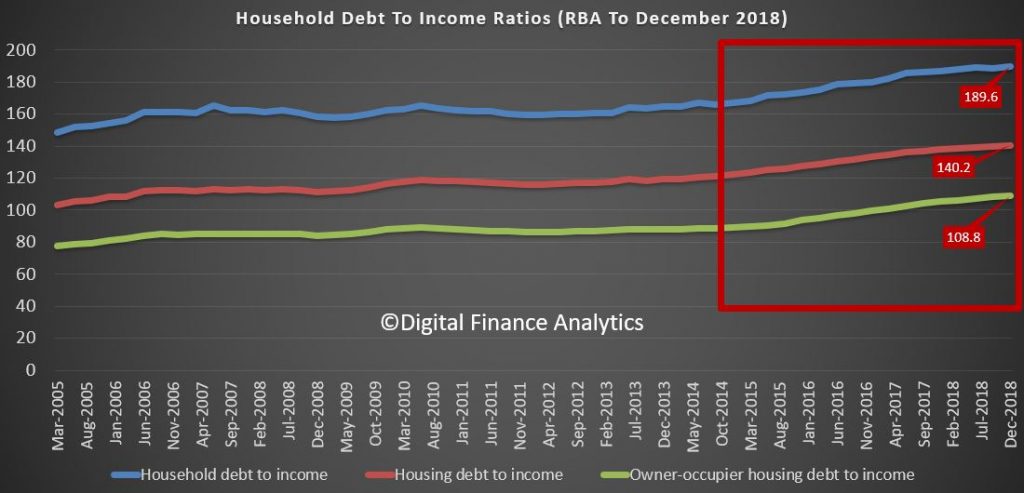

In the latest RBA data series (E2) we get an update on household debt to income and debt to asset ratios, and they are ALL moving in the wrong direction. This is to December 2018.

The household debt to income moved higher to a new record of 189.6, and housing debt to income to a new record of 140.2.

The change in trajectory from 2014/5 is significant, as lending standards were weakened, and interest rates cut (forcing home prices higher).

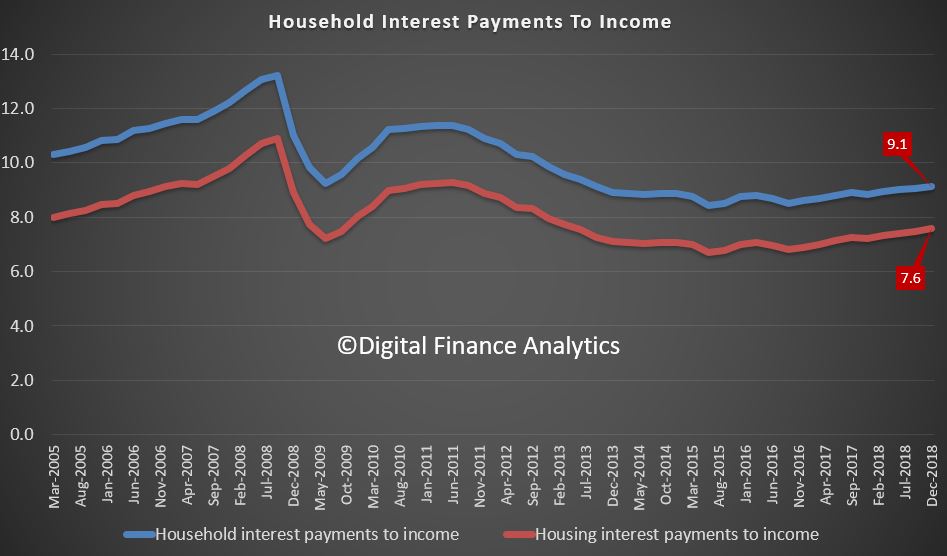

The interest payments to income also rose, thanks to bigger mortgages, slightly higher interest rates, and little income growth.

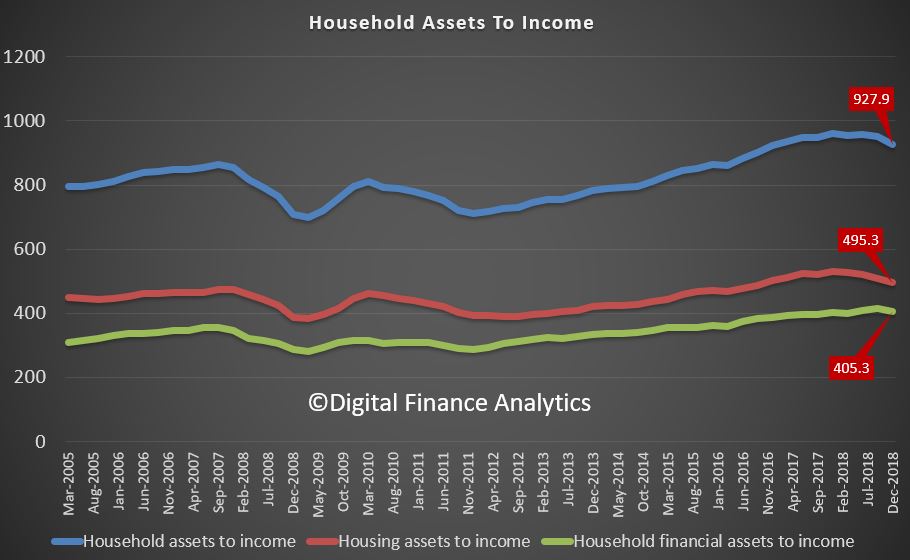

But in contrast, the asset values are falling, so the asset to income ratios are falling. Housing assets in particular are dropping.

All pointing to a higher burden of debt on households. And remember only one third, or there about, have a mortgage, so in fact the TRUE ratios are much much worst. But the trends do not lie in relative terms, and by the way these are extended ratios compared with most western economies. We are drowning in rivers of debt!

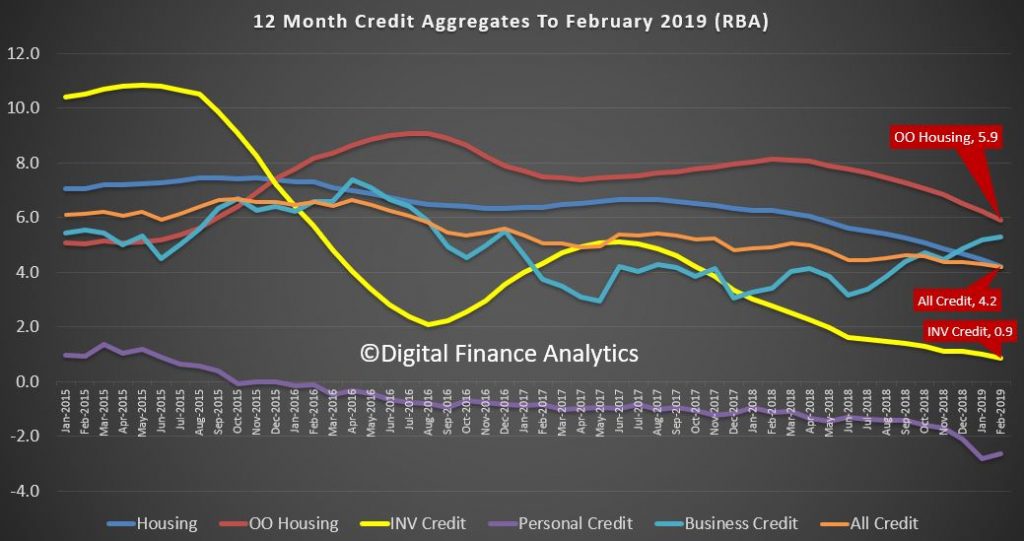

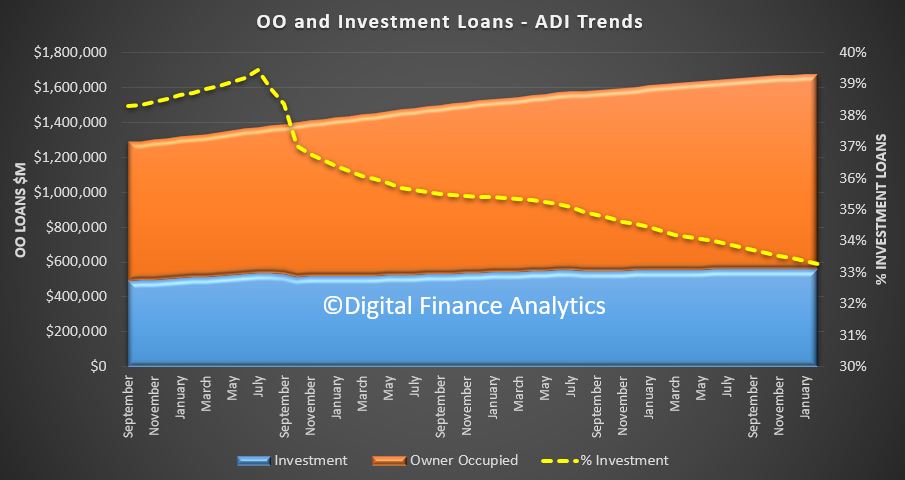

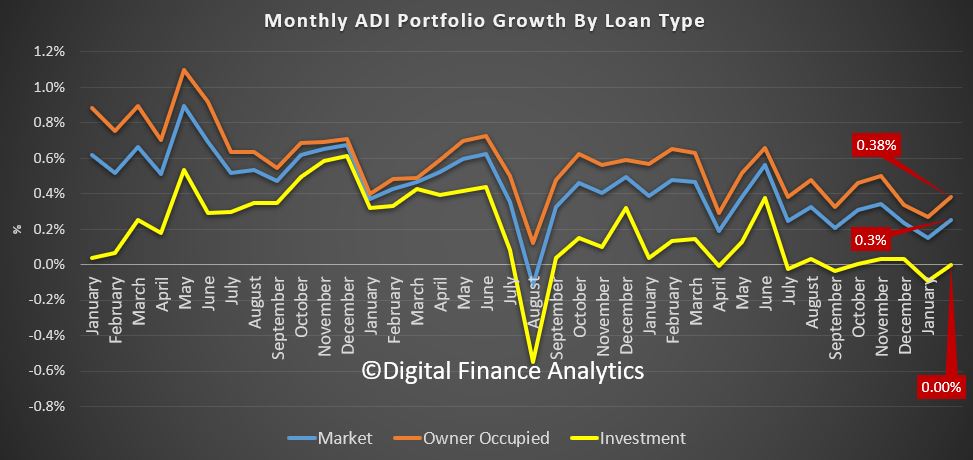

This is quite starkly shown in the RBA’s 12 month series, with total credit annualised growth now standing at 4.2%. Housing credit also fell to the same 4.2% level, from 4.4% a month ago. The fall continues. Within the housing series, lending for owner occupation fell below 6% – down to 5.9% and investment housing lending fell to 0.9% annualised.

The seasonally adjusted RBA data showed that last month total credit for housing grew by 0.31%, up $5.6 billion to $1.81 trillion, another record. Within in that owner occupied lending stock rose 0.42%, seasonally adjusted to $1.22 trillion, up $5.11 billion. Lending for investment property rose 0.09%, or $0.5 billion to $595 billion. Personal credit fell slightly, down 0.07% and business credit rose 0.42% to $960 billion, up $4.06 billion.

The APRA data revealed that ADI growth was lower than the RBA aggregates. Some of this relates to seasonal adjustments plus, as we will see a rise in non-bank lending. The proportion of investment loans less again to 33.3% of loans outstanding.

Total owner occupied loans were $1.11 trillion, up 0.38%, or $4.2 billion, while investor loans were $557 billion, flat compared with last month. This shows the trends month on month, with a slight uptick in February compared to January, as holidays end and the property market spluttered back to life. The next couple of months will be interesting as we watch for a post-Hayne bounce in lending and more loosening of the credit taps, but into a market where demand, is at best anemic.

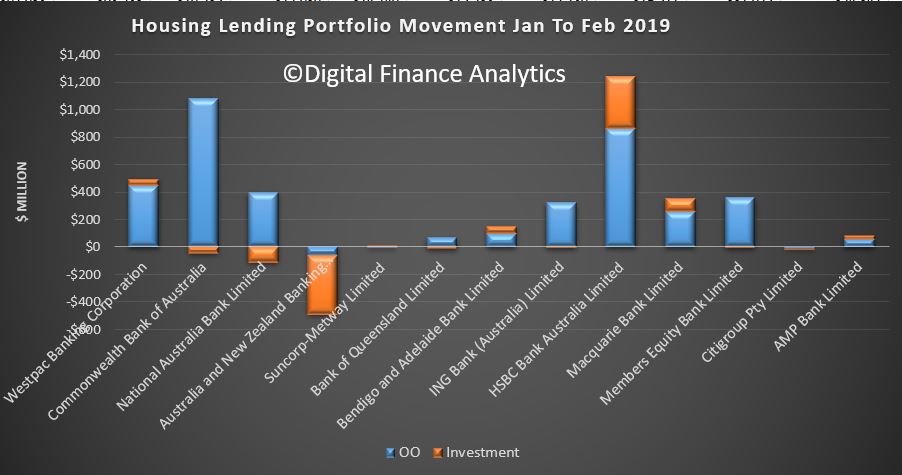

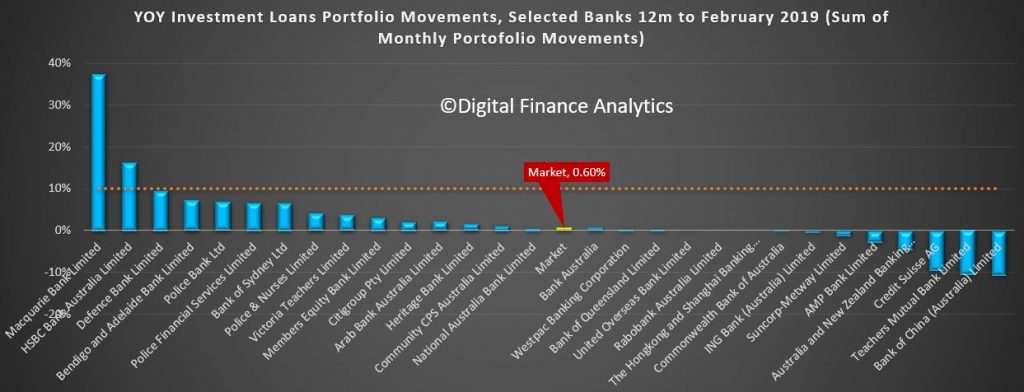

The portfolio movements are interesting (to the extent the data is reported accurately!), with HSBC growing its footprint by more that one billion across both investor and owner occupied lending. Only Westpac, among the big four grew their investor loans, with ANZ reporting a significant slide (no surprise they said they had gone too conservative, and recently introduce a 10-year interest only investor loan). Macquarie and Members Equity grew their books, with the focus on owner occupied loans.

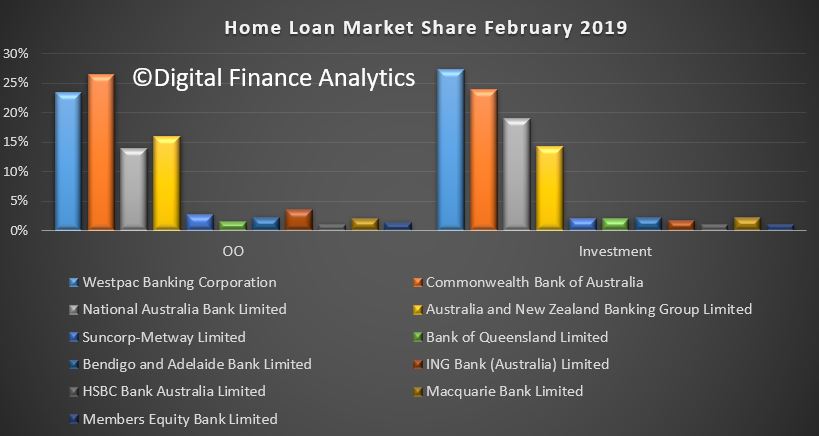

The overall portfolios did not vary that much, with CBA still the largest owner occupied lender, and Westpac the largest investor lender.

The 12 month investor tracker whilst obsolete in one sense as APRA has removed their focus on a 10% speed limit, is significant, in that the market is now at 0.6% annualised.

But the final part of the story is the non-bank lending. This has to be derived, and we know the RBA data is suspect and delayed. But the gap between the RBA and APRA data shows the trends.

Non Bank annualised owner occupied credit is growing at 17.6%, and investor lending at 4.8%. It is clear the non-banks, with their weaker capital requirements, and greater funding flexibility are making hay. Total non bank credit for housing is now around $142 billion or around 7.8% of housing lending. This ratio has been rising since December 2016, and kicked up in line with the tighter APRA rules being applied to the banks.

We have out doubts that APRA is looking hard enough at these lending pools, especially as we are seeing the rise of higher risk “near-prime” offers to borrowers who cannot get loans from the banks.

So to conclude the rate of credit momentum continues to ease – signalling more home prices ahead. The non-banks sector, currently loosely regulated by APRA is growing fast, and just the before the US falls around the GFC, risks are higher here. And finally, and worryingly, household debt is STILL growing… so more stress and financial pressure ahead.

RBA’s Luci Ellis, Assistant Governor (Economic) spoke yesterday “What’s Up (and Down) With Households?“. We examined the conundrum that labour markets are strong, yet the economy is weaker. The disconnect is the household sector – which of course DFA examines closely in our surveys.

One of the most interesting comments relates to household spending slowing, especially on cars and household goods. We regard this as an important indicator. Income of course is under pressure in real terms, costs are rising, and home prices are falling. Households are hunkering down. As the RBA says ” at some point they might conclude that this is not temporary and that low income growth will persist. At that point they would be likely to adjust their spending plans. Consumption growth would then slow“.

This is what she said:

For a little while now, the team at the Bank has been grappling with how one might reconcile

apparently weak national accounts figures with the noticeably stronger labour market data.

The disconnect can be traced to the household sector. Many other parts of the national accounts

measure of output – gross domestic product (GDP) – are actually doing reasonably

well. Outside the mining sector, where some large projects are still winding down, business

investment is growing at a solid pace. Transport and renewable energy projects have been quite

important. Public demand, both consumption and investment, is supporting growth.

There are also some areas of weakness outside the household sector, such as the drought-affected

rural sector, which is weighing on exports at the moment. Droughts and other recent natural

disasters clearly pose difficulties for those directly affected. But the underlying trends in

the broader economy are not determined by these events. So in the main, outside the household

sector, the economy is not doing too badly.

The Labour Market has Unambiguously Improved

This makes sense, because employment has been strong and someone must be hiring all those extra

workers. Over the past year, total employment has increased by more than 2 per cent.

The unemployment rate declined by ½ percentage point over 2018, reaching the level of 5 per cent

before our forecasts implied it would (Graph 1). This is a good outcome. Youth unemployment

has declined and most measures of underemployment have also come down a bit.

Graph 1

Some industries are doing better than others, but overall the strength in employment has been

across a diverse range of sectors (Graph 2). We can see this either by looking at the

industry that people say they work in, or we can use the ABS’s new Labour Account to

triangulate this information with what firms say their industry is. Either way, we see jobs

being added in a range of industries. Employment in health care and social assistance has been

increasing for a while; the rollout of the NDIS is an important driver of this, but not the only

one. More recently, we have also seen employment increase in a number of business services

industries. Construction employment had also been strong for a while, reaching the highest share

of total employment in more than a century of records.

Graph 2

One can be reasonably confident in the steer the labour market data are giving us, because it is

coming from multiple, independently collected data sets. The employment and unemployment data

come from the ABS’s survey of households. But a survey of businesses, also from the ABS,

tells us that the number of job vacancies has been a very high share of the total jobs

available. Separate private-sector surveys of businesses tell us that many firms plan to hire

more workers. Many of our own liaison contacts also tell us that they are hiring.

And as the labour market gradually tightens, we are beginning to see the effects in wages growth.

This has been low for some time, but is gradually trending up now, especially in the private

sector (Graph 3). Part of this shift is that fewer workers are subject to wage freezes than

was the case a year or so ago. Minimum and award wage rises have also increased. Along with

other countries, it’s taking longer and a lower unemployment rate to start seeing faster

wages growth than historical experience might have suggested. Indeed, we still think Australia

is a little way off the levels of the unemployment rate that would induce materially faster

wages growth. But as the experience of other countries has also shown, if the labour market

tightens enough, wages growth does eventually pick up.

Graph 3

Household Consumption Spending is Slowing

In contrast to the positive picture implied by the labour market, growth in household income has

been slow, and growth in consumption has weakened recently (Graph 4).

Graph 4

If we drill down to see which kinds of spending have slowed the most, we can see that spending on

cars and household goods has been particularly affected (Graph 5). Spending on less

discretionary items like food has been less affected.

There has been a deal of talk about the possibility that ‘wealth effects’ from

declining housing prices might be weighing on spending. It’s important to remember, though,

that people’s reaction to a fall in prices is likely to depend partly on how far prices had

increased previously.

Graph 5

Some recent work by colleagues at the Bank suggests that the link is a bit more subtle than

simply that increases in wealth boost spending directly (May, Nodari and Rees 2019). It isn’t

so much that people wake up one morning, realise their home is worth more, and decide to go out

shopping. Rather, if their home is worth more, they can borrow more against it, which matters

for some people’s decisions to buy a car. And because rising housing prices usually occur in

the context of high rates of transactions in the market, spending on home furnishings tends to

rise and fall with housing prices. So when housing prices decline, turnover also declines. This

means there are fewer people moving house and realising their old couch doesn’t fit or they

need new furnishings in the extra bedroom.

Slow Income Growth is a Drag on Household Spending

Beyond this specific link to housing turnover, some slowdown in consumption spending is not

entirely unexpected. For several years now, we have been calling out the issue of weak income

growth and how it might test the resilience of household consumption spending. This is a

particular issue in the context of high household debt and the need to service that debt.

One aspect of economic theory that actually works in practice is the observation that people try

to smooth their consumption in the face of fluctuating incomes. Income growth is noticeably more

volatile than consumption growth. So the usual pattern is that gaps between the two resolve with

shifts in income growth, not shifts in consumption growth.

But there might be limits to how long households can continue expanding their consumption faster

than their income is rising. People are still saving, and they can do so at a slower rate. But

at some point they might conclude that this is not temporary and that low income growth will

persist. At that point they would be likely to adjust their spending plans. Consumption growth

would then slow.

So we need to establish how household income growth might indeed return back towards current

rates of consumption growth or even higher. To do that, we need to understand why it has been so

weak.

Labour Income Growth Has Recovered Somewhat

For some time, part of the story had been that labour income growth was weak. This has been true

across several dimensions. First, the growth of wage rates for particular jobs has been slow

(Graph 6). This is the measure of wages growth captured by the ABS’s Wage Price Index

(WPI). It captures changes in wages paid for a fixed pool of jobs. As I already mentioned,

growth in this measure has started increasing, though only gradually. It is still well below

what one might expect in the longer run, if inflation is to average between 2 and 3 per cent

and if productivity maintains a similar average growth rate to its average over the past decade

or so.

People’s actual incomes include bonuses and other non-wage labour income, and average labour

income depends on whether the mix of jobs in the economy is changing. For a number of years,

these factors combined to make average earnings per hour, as recorded in the national accounts,

increase much more slowly than the mix-adjusted WPI measure. It isn’t unusual for growth in

this measure of earnings to differ from growth in the WPI. They are compiled on different bases.

But in the years following the end of the mining investment boom, this gap was persistently

negative, and quite large.

Graph 6

Some of the compositional change might have been because people were moving out of higher-paid

jobs in mining-related activity, and had gone back to lower-paying work. It’s hard to

pinpoint how important this effect was, because the weakness in average earnings growth was seen

in some industry-level data as well. So at least some people would have had to be switching to

lower-paid jobs in the same industry. Another factor that might have been at work was that fewer

people were actually switching jobs than in the past. Surveys that track people through time,

such as the HILDA survey, show that people who change jobs often see faster income growth in the

year they switched, than people who didn’t change jobs (Graph 7).

Graph 7

This lower rate of job churn accords with some of the evidence we see in business surveys and the

messages coming out of our business liaison program. Many firms report that they find it hard to

find suitable labour, at least for some roles, and that this is a constraint on their

businesses, though usually not a major one (Graph 8). But when we ask our contacts what

they are doing about this problem, paying people more is not the first solution they think of.

Even poaching someone from another firm by enticing them with higher pay is not that common. The

evidence from our liaison program suggests that it has long been the case that firms first

resort to other strategies to deal with labour shortages, and only turn to faster wage increases

when the shortages are severe and persistent (Leal 2019).

Graph 8

But whatever the underlying drivers, the gap between the growth rates of the WPI and average

earnings has closed more recently. Slow wages growth is still a concern, but in terms of its

contribution to income growth, it is less of a puzzle than it was a few years ago. Instead we

need to seek the source of the more recent weakness elsewhere.

Non-Labour Income Remains Weak

If we break household disposable income growth into its components, we can see the drivers of the

more recent weakness (Graph 9). Labour income is not especially strong, but it no longer

seems at odds with growth in employment and other information about wages growth. Rather, growth

in other sources of income has been weak for some time, and this has continued more recently.

Graph 9

Within non-labour income, the main components are social assistance, rental income, other

investment income, and the earnings of unincorporated businesses. It turns out that a confluence

of factors has resulted in growth in most of these categories of income being weak recently. In

some cases, this is a trend change that is likely to persist. Some others are driven by

shorter-term factors that could reverse in coming years.

Social assistance payments have been relatively flat for a number of years (Graph 10). As

the labour market has strengthened and unemployment has come down, it is not surprising that

some forms of social assistance have not been growing. But there are a few other things going on

at the same time. Firstly, the rate of growth of age pension payments has slowed, though it is

still positive. There are a number of probable drivers of this, including the increase in the

eligibility age, as well as more people above the (higher) eligibility age remaining in the

workforce rather than drawing a pension. It is also possible that, as time goes on and the

people who are retiring have had longer to accumulate superannuation balances, more people are

receiving a part-pension together with an income stream from their superannuation.

Graph 10

Secondly, in recent years, growth in social welfare spending by the government has come from new

programs (like the NDIS) that are counted as government consumption, not household income, in

the national accounts. So while both disability payments and other payments to families with

children have been broadly constant in dollar terms for several years, government consumption

has been growing strongly over the same period. If we adjusted for this, the growth in the

social assistance component of household income would look much closer to its average over the

past, rather than well below average.

These factors all relate to the design of programs assisting households, and how they are

classified in the national accounts. So we would not expect them to reverse all of a sudden.

This implies that we should also not expect that measured household income from this source will

bounce back strongly any time soon.

Rental income has also been a bit weak (Graph 11). This is not surprising considering that

rents have been rising only slowly in most cities, and falling for a few years in Perth. But

rental income is only earned by 15 per cent of taxpayers, and lower cash rental income

for landlords is also lower rent paid by renters, leaving them with more money to pay for other

things.[1] So the

weakness in rental income is unlikely to be a large driver of any slowdown in consumer spending.

Income from other kinds of investments has also been a bit weak, but has recovered a bit lately.

Graph 11

Unincorporated business income has also been weak of late. This can be a volatile type of income

and sensitive to conditions in particular sectors. The farm sector represents a large share of

unincorporated business income, compared with their share of the economy. So one reason this

type of income has fallen has been the effect of the drought on farm incomes. A recovery here

will depend on how soon normal seasonal conditions return. Much of the rest of unincorporated

business income comes from sectors related to the property market, including building

tradespeople and real estate agents. They are also seeing lower incomes, as both construction

activity and the volume of sales of existing homes decline. Again, it can be envisaged that

these sources of income might recover at some point, but not in the very near term.

Tax and Other Payments are Dragging on Disposable Income

When we think about household income available for consumption and saving, economists usually

talk about household disposable income. This is income net of taxes, net interest

payments and a few other deductions like insurance premiums. Income payable – the things

deducted from gross income to calculate disposable income – increased by nearly 6 per cent

in 2018. This was significantly faster than growth in gross household income.

Despite the relatively weak picture for household income growth, the tax revenue collected from

households has grown solidly in recent years. It’s normal for growth in tax revenue to

outpace income growth a bit: that is how a progressive tax system works. A useful rule of thumb

is that, in the absence of adjustments to tax brackets to allow for bracket creep, for every one

percentage point of growth in household income, taxes paid by households will on average

increase by about 1.4 percentage points. That’s an on-average figure, though. The

actual ratio can vary quite a bit.

In the past year, taxes paid by households increased by around 8 per cent, more than

double the rate of growth in gross household income of 3½ per cent. So the ratio

is more like a bit over two-to-one at the moment, rather than 1.4 to one. That is at the high

end of the range this ratio reaches, but as this graph shows, it is not unprecedented (Graph 12).

But this effect has cumulated over time, so that the share of income that is paid in tax has

been rising (Graph 12, bottom panel).

Graph 12

What is noteworthy is that for all of the past six years, growth in tax paid has exceeded income

growth by an above-average margin, at a time when income growth itself has been slow (Graph 13).

Graph 13

There are likely to be several things going on here. Aside from the usual bracket creep, some

deductions and offsets have declined, boosting the overall tax take. Interest rates on

investment property loans are now higher than for owner-occupiers, but overall the interest rate

structure on mortgages is lower than it was a few years ago. So landlords will have lower tax

deductions for interest payments on loans on investment properties. At the same time, the

significant run-up in housing prices in some cities over the past decade will have increased the

capital gains tax liability paid by investors selling a property. Turnover in the housing market

has declined. But as best we can tell, the price effect has dominated the effect of declining

volumes, and total capital gains tax paid has increased.

Compliance efforts and technological progress in tax collection have boosted revenue collected

from a given income. The Tax Office reports that its efforts to raise compliance around

work-related deductions have boosted revenue noticeably (Jordan 2019). The next wave of this

effort, focused on deductions related to rental properties, could result in further boosts to

revenue.

Some of these drivers boosting tax paid could persist for a while, but they aren’t permanent.

For example, the earlier period of strong housing price growth will only increase capital gains

tax revenue if the asset was owned during that period. It can be expected to become less

important, the further into history it passes. Similarly, increased compliance increases the

level of tax paid on a given level of income. It is not a change in the trend

growth rate in tax paid. That said, the effect could last for a while as efforts shift to

different aspects of compliance.

Some Recent Policy Changes Might Mitigate the Drag on Consumption

The net of all these effects is that household income growth has remained slow even as labour

market conditions have been improving. Unlike slow wages growth, though, it is less clear how

much weak non-labour income growth will weigh on consumer spending. As I already noted, slow

growth in rental income for landlords means that tenants have more money to spend on other

things. Some of the weakness in social assistance payments is because new programs are being

delivered differently from existing ones, and so they are classified as government consumption.

The net benefit to the recipients could be the same or higher.

So there might be reasons to think that weak non-labour income growth is less worrisome than weak

wages growth. But you would not want to rely on that possibility to underpin your views on the

outlook for consumption. So this is an area we need to watch closely. Household consumption

spending is a large part of economic activity. A significant retrenchment there would lower

growth and feed back into a weaker labour market, as well as into decisions to purchase housing.

Parting Thoughts

My talk today has deliberately not overlapped with what the Bank has recently said about the

housing market. But I think it’s clear that conditions in the household sector more broadly

are highly consequential for the housing sector and thus this audience. Whatever other forces

might be affecting housing market developments, fundamentally demand for housing rests on the

household sector’s confidence and capacity to take on the financial commitments involved in

the purchase or rental of a home. Without enough income, and so without a strong labour market,

that confidence and capacity would be in doubt. This is not the only reason we are watching

labour market developments closely. But the nexus between labour markets, households and housing

are crucial to our assessment of the broader outlook.

Just before the GFC hit, the then Chair of the Fed reassured that everything was going to be fine.

The subprime mess is grave but largely contained, said Federal Reserve Chairman Ben Bernanke Thursday, in a speech before the Federal Reserve Bank of Chicago. While rising delinquencies and foreclosures will continue to weigh heavily on the housing market this year, it will not cripple the U.S. economy, he said. The speech was the Chairmans most comprehensive on the subprime mortgage issue to date.

It of course was not. We are still reaping the QE whirlwind.

So, today, RBA Assistant Governor (Financial System) Michele Bullock spoke in Perth “Property, Debt and Financial Stability”. In Perth, of all places where prices have been falling for many years!

She concludes that “vulnerabilities from the level of household debt, the apartment development cycle and the level of non-residential commercial property valuations continue to present risks for financial stability. While so far, the financial sector has remained resilient, we continue to monitor developments in household debt and in property markets for signs that these might have more broad ranging effects on the financial system”.

As Assistant Governor (Financial System) I oversee the Bank’s work on financial stability.

But what is financial stability and what is the Reserve Bank’s role in it?

The wellbeing of households and businesses in Australia depends on growth in the Australian

economy. And a crucial facilitator of sustained growth is credit – flows of funds from

people who are saving to people who are investing. Credit provides households and businesses

with the ability to borrow on the back of future expected income to finance large outlays, for

example, the purchase of a home or equipment to establish or grow a business. A strong and

stable financial system is important for this flow of funds.

There is no universal definition of financial stability but one way to think about it is to

consider what is meant by financial instability. My colleague Luci Ellis suggested

that this is best thought of as a disruption in the financial sector so severe that it

materially harms the real economy.[1]

This leaves unsaid where the disruption might come from, but we would all recognise the outcomes

of financial stability when we see it. For example, while Australia was spared the worst impact

of the global financial crisis, internationally it demonstrated the impact that financial

instability can have on growth and hence the wellbeing of households and businesses in the

economy.

Most of you will know about the Reserve Bank’s role in conducting monetary policy. But

another key role of the Reserve Bank that you might be less familiar with is promoting financial

stability. In this area, we share responsibility with the Australian Prudential Regulation

Authority (APRA). But it is APRA that has responsibility for the stability of individual

financial institutions and the tools that go along with that. So how does the Bank contribute to

financial stability?[2]

There are a number of things we do. We undertake analysis of the economy and the financial system

through the lens of financial stability, looking for financial vulnerabilities that could result

in substantial negative impacts on the economy, or economic vulnerabilities that could result in

risks to financial stability. We work with other regulators to identify signs of increasing

risks in the financial system and measures to address these risks. Where appropriate, we provide

advice to government on the potential implications for financial stability of policies. And we

talk about the risks we are seeing to help inform other regulators, participants in the

financial system, businesses and the general public of the potential risks that might have an

impact on the economy.

This last action – communicating the risks – is the key purpose of our six-monthly

Financial Stability Review (the Review). While any individual

financial institution, business or household might think the risks they are taking on are

appropriate, they may not be adequately taking into account the risks that are arising at a

systemic level from everyone’s actions. The Review attempts to bring this

system-wide view.

Our most recent Review was published in October last year and we are currently in

the process of drafting the next one, which will come out in April. So, for the remainder of my

talk, I am going to cover some of the key risks that we see at the moment. Given the audience, I

am going to focus on risks related to residential and commercial property. First, I will give an

update on recent developments in these areas. Then I will talk a little about recent concerns

around tighter lending standards. And I will finish up with a few observations on the property

market in Western Australia.

Household Debt

Six months ago in the Review, we noted that global economic and financial conditions

were generally positive and that the Australian economy was improving. At the same time, housing

prices were declining. In this context, we highlighted a number of vulnerabilities –

issues that, were a shock to occur or economic conditions take a turn for the worse, could

manifest in a threat to financial stability. At that time, we highlighted two domestic

vulnerabilities that are relevant to my talk today – the level of household debt, and the

slowdown in housing and credit markets. Six months on, these vulnerabilities remain. If

anything, they are a little more heightened.

The Bank has highlighted the issue of household debt as a potential threat to financial stability

many times over the past few years. Although it does not capture all the important information

about household indebtedness, the ratio of household debt to disposable income is one summary

indicator. This ratio is historically high (Graph 1). The household debt-to-income ratio rose

from around 70 per cent at the beginning of the 1990s to around 160 per cent

at the time of the GFC. The ratio steadied for a few years before starting to rise again around

2013 (around the same time that housing price growth began to accelerate) and is now around 190 per cent.

Graph 1

I have talked previously about some of the reasons why the debt-to-income ratio has risen so much

over the past few decades.[3]

In particular, a structural decline in the level of nominal interest rates and deregulation have

eased credit constraints and increased loan serviceability. And as households have been able to

borrow more, they have been able to pay more for housing. One important driver of high household

debt in Australia is, therefore, housing. There is very little debt related to non-housing loans

such as credit cards or car loans.

Just as housing costs have been an important driver of household debt, so has the ability to

borrow more influenced the price of housing. Over the past decade, housing prices in many parts

of Australia have risen but the rise has been particularly sharp in Sydney and Melbourne, which

account for around 40 per cent of the housing stock (Graph 2). More recently, housing

prices have fallen. Since the peak in mid 2017, housing prices Australia-wide have declined by

around 7 per cent. The falls in Sydney and Melbourne have been larger. The question we

are asking ourselves is, given the high levels of debt and falling housing prices, are there any

significant implications for financial stability?

Graph 2

The answer would be no at this stage – the impacts are not large enough to result in

widespread problems in the financial sector. This is not to downplay the financial stress that

some households are experiencing. But most of the debt remains well secured against property,

even with the decline in housing prices. Total repayments as a share of income remain steady and

a large number of indebted households have built up substantial prepayments over the past few

years. Broadly, the debt is held by households that can afford to service it. Arrears rates,

while increasing a bit over the past few years, remain low. Banks are well capitalised and work

over recent years to improve lending standards has made household and bank balance sheets more

resilient. Loans at high loan-to-valuation (LVR) ratios and interest-only loans are less common

than they were and most households have not been borrowing the maximum amount available.

Apartment Development

One area that we have focused on in recent years in our analysis of financial stability risks is

apartment development. There has been a substantial increase in apartment construction since the

start of the decade in the largest Australian capital cities (Graph 3). In Sydney there have

been more than 80,000 apartments completed over the past few years adding roughly 5 per cent

to housing stock in Sydney. Melbourne and Brisbane have also seen relatively large additions to

the supply of apartments and, while the number of apartments being built in Perth has been small

by comparison, this has been in the context of a fairly small apartment stock.

Graph 3

Our main concern with this from a financial stability perspective is the potential for this large

influx of supply to exacerbate declines in housing prices and so adversely impact households’

and developers’ financial positions. By its nature, high-density development can tend to

exacerbate price cycles. Large apartment developments have longer planning and development

processes than detached housing. Purchasing the land, designing the development, getting

approvals through relevant government bodies and then actual construction of the apartment block

all take time. In a climate of rapidly rising prices, developers are willing to pay high prices

for land on which to build apartments. Households, including investors, are willing to purchase

apartments off the plan, confident that the apartment will be worth more than they paid for it

when it is finally completed. This continues as long as prices are rising. This large increase

in supply, however, ultimately sows the seeds of a decline in prices which, if large enough,

results in development becoming unattractive, new supply falling and the cycle starting again.

This presents two risks. The first is to household balance sheets. A decline in apartment prices

could negatively impact households that purchased off the plan and are yet to settle. They might

find themselves in a situation where the value of the apartment in the current environment is

less than they contracted to pay for it. And as market pricing falls, lenders will revise their

valuations down and so will be willing to lend less. Households will therefore have to

contribute more funds, either from their own savings or loans from other sources.

The second risk is to developers who are delivering completed apartments into the cooling market.

If people who had pre-purchased are having difficulty getting finance, or decide it is not worth

going ahead with the purchase, there would be increasing settlement failures. Developers would

be left holding completed apartments, reducing their cash flow and their ability to service

their loans, and impacting banks’ balance sheets.

Currently, the risks here appear to be elevated but contained. The apartment market is quite soft

in Sydney; apartment prices have declined since their peak, rental vacancies have risen and

rents are falling (Graph 4). In Melbourne and Brisbane, however, apartment prices have so far

held up. Liaison suggests that settlement failures have not increased much and, to the extent

that they have, some developers are in a position where they can choose to hold and rent unsold

apartments. Further tightening in lending standards might, however, impact both purchasers of

new apartments and developers – I will return to this in a minute.

Graph 4

Commercial Property

A final area worth touching on is non-residential commercial property.

Commercial property valuations have, like housing, risen substantially over the past decade, and

much more than rents so that yields on commercial property have fallen to very low levels

historically (Graph 5). This is particularly the case for office and industrial property. One

reason for this is that yields, although they have been historically low in Australia, are high

relative to overseas and to returns on other assets. Furthermore, some markets, such as the

Sydney and Melbourne office property markets, are experiencing strong tenant demand and vacancy

rates are low. But the rapid increase in commercial property prices over the past decade does

pose risks. If transaction prices and valuations were to fall sharply, for example, in response

to a change in risk preferences, highly leveraged borrowers could be vulnerable to breaching

their LVR covenants on bank debt. This could trigger property sales and further price falls,

exacerbating the cycle.

Graph 5

Lending Standards

With that background, I want to turn to an issue that has attracted a fair bit of attention in

recent months – the role that tightening lending standards might have played in the

downturn in credit and the housing market. We published a special chapter in the October 2018

Review on this issue and the Deputy Governor discussed it in a speech in November

last year so I will only cover it briefly here.[4]

Lending standards have been tightening since late 2014, well before housing prices in the eastern

states started to turn down. The initial tightening occurred in December 2014 in response to

very fast growth in lending to housing investors and an assessment by APRA that banks’

lending practices could be improved. APRA required banks to tighten their lending practices in a

number of areas, including interest rate buffers, verification of borrower income and expenses,

and high LVR lending. The measure that got the most attention at that time, however, was

the ‘investor lending benchmark’ in which APRA indicated that supervisors would be

paying particular attention to any institutions with annual investor credit growth exceeding 10 per cent.

The idea was that it would be temporary while APRA worked with the banks on addressing lending

standards.

The benchmark and the tightening of standards didn’t have an immediate impact on the pace of

investor lending. It didn’t really start to bite until the middle of 2015 when banks

introduced higher interest rates for loans to investors. And at that point, growth in lending to

investors slowed sharply (Graph 6).

Graph 6

Once things settled down, however, and banks were comfortable that they were well below the

benchmark, the growth in lending to investors started to pick up again. Then, in March 2017,

APRA introduced restrictions on the share of new interest-only lending as part of its broader

suite of measures to strengthen lending practices. As part of this, APRA reinforced its investor

benchmark. While the interest-only measure was focused on reducing the volume of higher-risk

lending rather than lending to a particular type of borrower, there was a noticeable impact on

the growth in lending to housing investors since interest-only loans tend to be the product of

choice for many investors.

Both the investor lending benchmark and the interest-only lending benchmark have been removed for

banks that have provided assurances on their lending policies and practices to APRA. But the

improvements in lending practices implemented by the banks over the past few years have resulted

in credit conditions being tighter than they were a few years ago. Application processes have

been taking a bit longer as lenders are being more diligent about verifying borrower income and

expenses, borrowers are generally being offered smaller maximum loans and some borrowers are

finding it more difficult to obtain a loan. Banks are more closely adhering to their lending

policies, resulting in fewer exceptions being granted and there are fewer high LVR and

interest-only loans being approved.

There have been some concerns expressed that these developments have been a key reason for the

slowing in credit growth over the past year. Coupled with possibly some increased risk aversion

of front-line lending staff in the wake of the Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry, the concern is that this has been impacting

housing credit growth and, by extension, housing prices. As concluded in the Banks’ February

Statement on Monetary Policy, and noted by the Governor in a recent speech, tighter

credit conditions do not appear to be the main reason for declining housing credit growth.[5] The evidence

points towards declining demand for housing credit as being a more important factor.

Nevertheless, it is possible that tighter lending standards could be impacting developers of

apartments. This could be direct, reflecting banks’ desire to reduce their exposure to the

property market, particularly high-density development. But it could also be indirect by banks

tightening their lending standards for purchases of new apartments, hence impacting pre-sales

for developers and their ability to obtain finance. The Deputy Governor noted this in a speech

in November 2018 and concluded that this was of potentially higher risk to the economy than

household lending standards.

From a financial stability perspective, prudent lending standards are a good thing. They ensure

that households and banks are resilient to changes in circumstances. But there needs to be a

balance. The regulators are not proposing any further tightening in lending standards. And the

appropriate amount of credit risk is not zero – banks need to continue to lend and that

will inevitably involve some credit losses.

Western Australia

Finally, I want to turn my focus to developments in Western

Australia. As you will have seen from some of my earlier graphs, the Western Australian

circumstances are somewhat different to those of the eastern capital cities. There are two

aspects I would like to focus on – household resilience and the commercial property

sector.

Housing prices in Perth have been declining for some years (Graph 7). The peak in housing prices

in Perth was in the middle of 2014. This followed a period of strong housing price growth as the

population of Western Australia increased strongly during the mining investment boom and housing

construction took longer to ramp up. When housing construction did respond, however, population

growth had slowed markedly and housing prices started to fall. Median housing prices have fallen

by around 12 per cent since 2014.

Graph 7

This has clearly been a difficult time for many homeowners in Western Australia. There are some

households that are having difficulty meeting repayments, as evidenced by a rising arrears rate

in Western Australia (Graph 8). At this stage, however, the losses are not large enough to

threaten the stability of the financial sector. We nevertheless continue to monitor the

situation for any potential systemic impacts.

Graph 8

Finally, office property in Western Australia has also been experiencing oversupply. Valuations

have fallen over the past decade (Graph 9). Rents have also fallen reflecting a sharp increase

in office vacancy rates in Perth’s CBD over the past few years (Graph 10). This makes for a

challenging environment for owners of these buildings, particularly for owners of older or lower

quality office buildings as tenants have taken the opportunity to move into newer buildings as

rents have come down. But again, while a difficult time for developers and owners of office

buildings, the financial stability implications seem limited.

Graph 9

Graph 10

Conclusion

Vulnerabilities from the level of household debt, the apartment development cycle and the level

of non-residential commercial property valuations continue to present risks for financial

stability. While so far, the financial sector has remained resilient, we continue to monitor

developments in household debt and in property markets for signs that these might have more

broad ranging effects on the financial system.

The RBA released their minutes today relating top the March 2019 meeting. They called out the market’s view that policy rates would be lower in 2020 (a turn around), lower retail, and slowing housing momentum, despite strong employment.

In considering the stance of monetary policy, members observed that growth in the global economy

had been above trend in 2018, although it had slowed over the second half of the year and timely

indicators suggested that this moderation had extended into 2019. Nonetheless, output growth had

remained sufficient in most advanced economies for labour markets to remain tight, putting

upward pressure on wages. Members noted the tension in a number of economies between slower GDP

growth and resilient labour markets. The transmission of tighter labour market conditions to

inflation pressures was taking longer than might be expected, based on historical experience.

The authorities had responded to slowing growth in China by putting in place policies to

increase the flow of credit to the private sector and easing fiscal policy in a targeted way to

support growth, while continuing to pay close attention to risks in the financial sector.

Slowing growth in China and ongoing trade tensions had led to lower growth in global trade, and

continued to be a source of uncertainty for the outlook for global growth.

The tightening of global financial conditions, associated with higher risk premiums required by

investors around the turn of the year, had eased. Members assessed that global financial

conditions remained accommodative, with financial market pricing indicating that little change

to the accommodative stance of monetary policy in the advanced economies was expected over the

following year or so. The terms of trade for Australia were expected to have remained above

their trough in early 2016 and the Australian dollar had remained within its narrow range of

recent times.

Domestically, there continued to be tension between the ongoing improvement in labour market

data and the apparent slowing in the momentum of output growth in the second half of 2018.

Leading indicators of conditions in the labour market, such as vacancies and hiring intentions,

pointed to further tightening in the labour market in the near term. Private sector wages growth

had picked up further in the December quarter, consistent with the Bank’s forecasts and

survey evidence that a significant share of firms were finding it difficult to attract suitable

labour.

Although output growth had slowed in the second half of 2018, the outlook for business

investment and spending on public infrastructure had remained positive. Growth in consumption

was expected to be supported by an increase in growth in household disposable income. However,

there continued to be considerable uncertainty around the outlook for consumption given the

environment of declining housing prices in some cities, low growth in household income and high

debt levels. Dwelling investment was expected to subtract from growth in output over the

forecast period and, unless pre-sales volumes started to increase, this decline could be sharper

than currently expected.

The process of adjustment in the housing market had continued. Housing prices in Sydney,

Melbourne and Perth had declined further, and turnover in the housing market had fallen

significantly. Rent inflation had remained low across most of the country despite declines in

rental vacancy rates over the previous year, except in Sydney, where rental vacancy rates had

been increasing. Credit conditions had tightened for some borrowers and the demand for housing

credit had slowed noticeably as conditions in the housing market had changed. Mortgage rates had

remained low and there was strong competition for borrowers of high credit quality.

Members noted that the sustained low level of interest rates over recent years had been

supporting economic activity and had allowed for gradual progress to be made in reducing the

unemployment rate and returning inflation towards the midpoint of the target. While the labour

market had continued to strengthen, less progress had been made on inflation. Looking forward,

the central forecast scenario was still for growth in GDP of around 3 per cent over

2019 and a further decline in the unemployment rate to 4¾ per cent over the

next couple of years. This further reduction in spare capacity underpinned the forecast of a

gradual pick-up in wage pressures and inflation. Given this, members agreed that developments in

the labour market were particularly important.

Taking account of the available information on current economic and financial conditions and how

they were expected to evolve, members assessed that the current stance of monetary policy was

supporting jobs growth and a gradual lift in inflation. However, members noted that significant

uncertainties around the forecasts remained, with scenarios where an increase in the cash rate

would be appropriate at some point and other scenarios where a decrease in the cash rate would

be appropriate. The probabilities around these scenarios were more evenly balanced than they had

been over the preceding year.

Members agreed to continue to assess the outlook carefully. Given that further progress in

reducing unemployment and lifting inflation was a reasonable expectation, members agreed that

there was not a strong case for a near-term adjustment in monetary policy. Rather, they assessed

that it would be appropriate to hold the cash rate steady while new information became available

that could help resolve the current tensions in the domestic economic data. Members judged that

holding the stance of monetary policy unchanged at this meeting would enable the Bank to be a

source of stability and confidence, and would be consistent with sustainable growth in the

economy and achieving the inflation target over time.

The Decision

The Board decided to leave the cash rate unchanged at 1.5 per cent.

I will talk about how climate change affects the objectives of monetary policy and some of the challenges that arise in thinking about climate change.

Finally, I will also briefly discuss how climate change affects financial stability.

Let me start by highlighting a few of the dimensions that we need to consider:

We need to think in terms of trend rather than cycles in the weather. Droughts have

generally been regarded (at least economically) as cyclical events that recur every so

often. In contrast, climate change is a trend change. The impact of a trend is

ongoing, whereas a cycle is temporary.

We need to reassess the frequency of climate events. In addition, we need to reassess our

assumptions about the severity and longevity of the climatic events. For example, the

insurance industry has recognised that the frequency and severity of tropical cyclones (and

hurricanes in the Northern Hemisphere) has changed. This has caused the insurance sector to

reprice how they insure (and re-insure) against such events.

We need to think about how the economy is currently adapting and how it will adapt both to

the trend change in climate and the transition required to contain climate change. The

time-frame for both the impact of climate change and the adaptation of the economy to it is

very pertinent here. The transition path to a less carbon-intensive world is clearly quite

different depending on whether it is managed as a gradual process or is abrupt. The trend

changes aren’t likely to be smooth. There is likely to be volatility around the trend,

with the potential for damaging outcomes from spikes above the trend.

Both the physical impact of climate change and the transition are likely to have first-order

economic effects.

Climate Change, Economic Models and Monetary Policy

The economics profession has examined the effects of climate change at least since Nobel Prize

winner William Nordhaus in 1977. Since then, it has become an area of considerably more active

research in the profession.[4]

There has been a large body of research around the appropriate design of policies to address

climate change (such as the design of carbon pricing mechanisms), but not that much in terms of

what it might imply for macroeconomic policies, with one notable exception being the work of

Warwick McKibbin and co-authors.[5]

How does climate affect monetary policy? Monetary policy’s objectives in Australia are full

employment/output and inflation. Hence the effect of climate on these variables is an

appropriate way to consider the effect of climate change on the economy and the implications for

monetary policy. The economy is changing all the time in response to a large number of forces.

Monetary policy is always having to analyse and assess these forces and their impact on the

economy. But few of these forces have the scale, persistence and systemic risk of climate

change.

A longstanding way of thinking about monetary policy and economic management is in terms of

demand and supply shocks.[6]

A positive demand shock increases output and increases prices. The monetary policy response to a

positive demand shock is straightforward: tighten policy. Climate events have been good examples

of supply shocks. Indeed, droughts are often the textbook example used to illustrate a supply

shock. A negative supply shock reduces output but increases prices. That is a more complicated

monetary policy challenge because the two parts of the RBA’s dual mandate, output and

inflation, are moving in opposite directions. Historically, the monetary policy response has

been to look through the impact on prices, on the presumption that the impact is temporary. The

banana price episode in 2011 after Cyclone Yasi is a good example of this. The spike in banana

prices and inflation was temporary, although quite substantial. It boosted inflation by 0.7

percentage points. The Reserve Bank looked through the effect of the banana price rise on

inflation. After the banana crop returned to normal, prices settled down and inflation returned

to its previous rate.

The response to such a shock is relatively straightforward if the climate events are temporary

and discrete: droughts are assumed to end; the destruction of the banana crop or the closure of

the iron ore port because of a cyclone is temporary; things return to where they were before the

climate event. That said, the output that is lost is generally lost forever. It is not made up

again later, but rather output returns to its former level.

The recent IPCC report documents that climate change is a trend rather than cyclical, which makes the assessment much more complicated. What if droughts are more frequent, or cyclones happen more often? The supply shock is no longer temporary but close to permanent. That situation is more challenging to assess and respond to.

Climate Change and Financial Stability

Having talked about the macroeconomic impact of climate change and how that might affect monetary

policy, I will briefly discuss climate through the lens of financial stability implications.[10] Financial

stability is also a core part of the Reserve Bank’s mandate. Challenges for financial

stability may arise from both physical and transition risks of climate change. For example,

insurers may face large, unanticipated payouts because of climate change-related property damage

and business losses. In some cases businesses and households could lose access to insurance.

Companies that generate significant pollution might face reputational damage or legal liability

from their activities, and changes to regulation could cause previously valuable assets to

become uneconomic. All of these consequences could precipitate sharp adjustments in asset

prices, which would have consequences for financial stability.

The reason that I will only cover the implications of climate change for financial stability only

briefly today is that it has been very eloquently discussed by Geoff Summerhayes (APRA) and John

Price (ASIC) including at this forum over the past two years.[11] I would very much

endorse the points that Geoff and John have made. Geoff stresses the need for businesses,

including those in the financial sector to implement the recommendations of the Task Force for

Climate-related Financial Disclosures (TCFD).[12]

I strongly endorse this point. We have seen progress on this front in recent years, but there is

more to be done. Financial stability will be better served by an orderly transition rather than

an abrupt disorderly one.

One area that Geoff highlighted in a recent speech is that there is a data gap which needs to be

addressed:[13] ‘The

challenge governments, regulators and financial institutions face in responding to the

wide-ranging impacts of climate change is to make sound decisions in the face of uncertainty

about how these risks will play out.’ In that regard, Geoff mentions one challenge that I

spoke about earlier in the context of monetary policy. Namely, taking the climate modelling and

mapping that into our macroeconomic models. For businesses and financial markets, that challenge

is understanding the climate modelling and conducting the scenario analysis to determine the

potential impact on their business and investments.

Interesting speech from the RBA Governor today, in which he explains why home prices are falling, and says its all manageable. No mention of too loose credit and too low interest rates. Or the substantial credit tightening of recent times as the credit impulse slows!

Just remember they banked on the household sector to spend big to support the economy after the mining boom faltered, and that housing credit growth was the centre piece. This is a neat piece of misdirection in my view!

The Current State of the Housing Market

Australians watch housing markets intensely, perhaps more so than citizens of any other country.

Over the five years to late 2017, they saw nationwide housing prices increase by almost 50 per cent

(Graph 1). Since then, prices have fallen by 9 per cent, bringing them back to

their level in mid 2016.

Graph 1

Declines of this magnitude are unusual, but they are not unprecedented. In 2008 and 2010, prices

fell by a similar amount, as they did on two occasions in the 1980s. In the 1980s, the rate of

CPI inflation was higher than it is now, so in inflation-adjusted terms, the declines then were

larger than the current one.

These nationwide figures mask considerable variation across the country (Graph 2). The

run-up in prices over recent years was most pronounced in Sydney and Melbourne, so it is not

surprising that the declines over the past year have also been largest in these two cities. In

Perth and Darwin, the housing markets have been weak for some time, affected by the swings in

population and income associated with the mining boom. By contrast, the housing market in Hobart

has been strong recently. In Adelaide, Brisbane, Canberra and many parts of regional Australia,

conditions have been more stable. Given these contrasting experiences, it is pretty clear that

there is no such thing as the Australian housing market. What we have

is a series of separate, but interconnected, markets.

Graph 2

Another important window into housing markets is provided by rental markets. Over recent times,

the nationwide measure of rent inflation has been running at a bit less than 1 per cent,

the lowest in three decades (Graph 3). As with housing prices, there is a lot of variation

across the country. Rents have been falling for four years in Perth and are now around 20 per cent

below their previous peak. By contrast, in Hobart rents have been rising at the fastest rate for

some years.

Graph 3

As is well understood, shifts in sentiment play an important role in housing markets. When prices

are rising, people are attracted to the market in the hope of capital gains. At some point,

though, valuations become so stretched that demand tails off and there is a shift in momentum.

When prices are falling, it’s the reverse. The prospect of capital losses leads buyers to

stay away or to delay purchasing. At some point, though, the lower prices draw more buyers into

the market. First home owners find it easier to buy a home, investors are attracted back into

the market, and trade-up buyers take the opportunity to upgrade to the home they have always

wanted. These shifts in sentiment and momentum are seen in most housing cycles, but their

precise timing is difficult to predict.

Some of these shifts in sentiment are evident in consumer surveys (Graph 4). Over recent

times, the number of people reporting that an investment in real estate is the wisest place for

their savings has fallen significantly. So, it is not surprising that there are fewer investors

in the market. At the same time, the number of people saying it is a good time to buy a home has

increased. Lower prices draw more people in and, eventually, this helps stabilise the market. So

it is worth closely watching these shifts in sentiment.

Graph 4

Explaining the Recent Cycle

An obvious question to ask is what are the underlying, or structural, drivers of the large run-up

in housing prices and the subsequent decline?

There isn’t a single answer to this question. Rather, it is a combination of factors.

Before I discuss these factors, it is worth pointing out that the current adjustment is unusual.

Unlike the other four episodes in which housing prices have declined in recent decades, this one

was not preceded by rising mortgage rates. Nor has it been associated with a rise in the

national unemployment rate. Instead, in New South Wales, where the recent decline in housing

prices has been the largest, the unemployment rate has continued to trend down. It is now at

levels last seen in the early 1970s. The unemployment rate has also trended lower in Victoria.

So, the origins of the current correction in prices do not lie in interest rates and

unemployment. Rather, they largely lie in the inflexibility of the supply side of the housing

market in response to large shifts in population growth.

It is useful to start with the national picture (Graph 5). Australia’s population growth

picked up noticeably in the mid 2000s and it took the better part of a decade for the rate of

home building to respond. It took time to plan, to obtain council approvals, to arrange finance

and to build the new homes. Not surprisingly, housing prices went up. Eventually, though, the

supply response did take place. Over recent times, the number of dwellings in Australia has been

increasing at the fastest rate in more than two decades. Again, not surprisingly, prices have

responded to this extra supply.

Graph 5

The population and supply dynamics are most evident in Western Australia and New South Wales

(Graph 6).

During the mining investment boom, population growth in Western Australia increased from around 1 per cent

to 3½ per cent. This was a big change. The rate of home building was slow to

respond. When it did finally respond, it was just at the time that population growth was slowing

significantly, as workers moved back east at the end of the boom. This explains much of the

cycle.

In New South Wales it is a similar story, although it is not quite as stark. The recent rate of

home building in New South Wales is the highest in decades. At the same time, population growth

is moderating, partly due to people moving to other cities, attracted by their lower housing

prices and rents. By contrast, in cities where population patterns and the rate of home building

have been more stable, prices, too, have been more stable.

Graph 6

Another demand-side factor that has influenced prices is the rise and then decline in demand by

non-residents.

One, albeit imperfect, way of seeing this is the number of approvals by the Foreign Investment

Review Board (Graph 7). In the middle years of this decade, there was a surge in foreign

investment in residential property, particularly from China. This was apparent not just in

Australian cities, but also in ‘international’ cities in other countries. In

Australia, the demand was particularly strong in Sydney and Melbourne, given the global profiles

of these two cities and their large foreign student populations. More recently, this source of

demand has waned, partly as a result of the increased difficulty of moving money out of China as

the authorities manage capital flows.

Graph 7

The timing of these shifts in foreign demand has broadly coincided with – and

reinforced – the shifts in domestic demand. However, making a full assessment of their

impact on prices is complicated by the fact that international property developers were also

adding to supply in Australia at a time of very strong demand. More recently, these developers

have scaled back their activity.

Domestic investors have also played a significant role in this cycle. This is especially the case

in New South Wales, which was the epicentre of strong investor demand (Graph 8). At the

peak of the boom, approvals to investors in New South Wales accounted for half of approvals

nationwide, compared with an average of just 30 per cent over the five years to 2010.

More than 40 per cent of the new dwellings built in New South Wales recently have been

apartments, which tend to be more attractive to investors.

Graph 8

The strong demand from investors had its roots in the population dynamics. Low interest rates and

favourable tax treatment added to the attraction of investing in an appreciating asset. The

positive side to this was that the strong demand by investors helped underpin the extra

construction activity needed to house the growing population. But the rigidities on the supply

side, coupled with investors’ desire to benefit from a rising market in a low interest rate

environment, amplified the price increases.

As I discussed earlier, there is an internal dynamic to housing price cycles, and this one is no

exception. By 2017, the ratio of the median home price to income had reached very high levels in

Sydney and Melbourne (Graph 9). Finding the deposit to purchase a home had become beyond

the reach of many people, especially first home buyers if they did not have others to help them.

At the same time, the combination of high prices and weak growth in rents meant that rental

yields were quite low. So, naturally, momentum shifted. Given the big run-up in prices and the

large increase in supply, a correction at some point was not surprising, although the precise

timing is nearly impossible to predict.

Graph 9

No discussion of housing prices is complete without touching on interest rates and the

availability of finance. The low interest rates over the past decade did increase people’s

capacity to borrow and made it more attractive to borrow to buy an asset whose price was

appreciating. But the increase in housing prices is not just about low interest rates. The

variation across the different housing markets indicates that city-specific factors have played

an important role.

Recently, much attention has also been paid to the availability of credit. This attention has

coincided with a noticeable slowing in housing credit growth, especially to investors (Graph 10).

Graph 10

It is clear there has been a progressive tightening in lending standards over recent years. The

RBA’s liaison suggests that, on average, the maximum loan size offered to new borrowers has

fallen by around 20 per cent since 2015. This reflects a combination of factors,

including more accurate reporting of expenses, larger discounts applied to certain types of

income and more comprehensive reporting of other liabilities. Even so, only around 10 per cent

of people borrow the maximum they are offered. Sensibly, most people borrow less than what they

are offered, so the effect of this reduction in borrowing capacity has not been particularly

large.

It has also been apparent through our liaison that some lenders became more cautious last year.

There was a heightened concern by some loan officers about the consequences to them and their

career prospects of making a loan that might not be repaid if the borrower’s circumstances

changed. So, lenders became more risk averse. This, along with greater verification of expenses

and income, led to an increase in average loan approval times, although some lenders have

invested in people and technology to address this. Our liaison suggests that application

approval rates are largely unchanged.

Overall, the evidence is that a tightening in credit supply has contributed to the slowdown in

credit growth. The main story, though, is one of reduced demand for credit, rather than reduced

supply.

When housing prices are falling, investors are less likely to enter the market and to borrow. So

too are owner-occupiers for a while. Consistent with this, the number of loan applicants has

declined over the past year. There is also strong competition for borrowers with low credit

risk, which is not something you would expect to see if it were mainly a supply story. This

competition is evident in the significant discounts on interest rates on new loans compared with

those on outstanding loans.

Even though the slowing in credit growth is largely a demand story, we are watching credit

availability closely. It is perhaps stating the obvious to say that we want lenders who are both

prudent and who are prepared to take risk. As lenders recalibrated their risk controls last

year, the balance may have moved too far in some cases. This meant that credit conditions

tightened more than was probably required. Now, as lenders continue to seek the right balance,

we need to remember that it is important that banks are prepared to take credit risk. And it’s

important that they have the capacity to manage that risk well. If they can’t do this, then

the economy will suffer.

Impact on the Macroeconomy

This brings me to the issue of how developments in the housing market affect the broader

economy.

Movements in housing prices affect the economy through multiple channels. They influence consumer

spending, including through the spending that occurs when people move homes. They also influence

the amount of building activity that takes place. Changes in housing prices also have an impact

on access to finance by small business by affecting the value of collateral for loans. And

finally, they can affect the profitability of our financial institutions.

Today, I would like to focus on the effect of housing prices on household consumption. My

colleagues at the RBA have examined how changes in measured housing wealth affect household

spending.[1] They

estimate that a 10 per cent increase in net housing wealth raises the level of

consumption by around ¾ per cent in the short run and by 1½ per cent

in the longer run. They have also examined how this wealth effect differs by type of spending.

They find that it is highest for spending on motor vehicles and household furnishings and that

for many other types of spending the effect is not significantly different from zero (Graph 11).

Part of the effect on spending on furnishings is likely to come from the fact that periods of

rising housing prices are often associated with higher housing turnover, and turnover generates

extra spending.

Graph 11

Over recent years, spending by households has risen at a faster rate than household income; in

other words, the saving rate has declined (Graph 12). The results that I just spoke about

suggest that rising housing wealth played a role here. If so, falling housing prices, and a

decline in measured household wealth, could have the opposite effect.

Graph 12

The more important influence, though, is what is happening with household income. For many

people, the main source of their wealth is their human capital; that is, their future earning

capacity. As I have discussed on previous occasions, growth in household income has been quite

weak for a while. It is plausible that, for a time, this didn’t affect people’s

expectations of their future income growth; that is the value of their human capital. So they

didn’t change their spending plans much, despite their current income growth being weak, and

the saving rate fell. However, as the period of weak income growth has persisted, it has become

harder to ignore it. Expectations of future income growth have been revised down and it is

likely that this is affecting spending.

My conclusion here is that wealth effects are influencing consumption decisions, but they are

working mainly through expectations of future income growth. Swings in housing prices and

turnover in the housing market are also having an effect, but they are not the main issue. This

assessment is consistent with the data on housing equity injection (Graph 13). Over recent

years, households have been injecting substantial equity into housing and have not been using

the higher housing prices to borrow to support their other spending. This is in contrast to the

period around the turn of the century, when households were withdrawing equity.

Graph 13

Given this assessment, developments in the labour market are particularly important. A further

tightening of the labour market is expected to see a gradual increase in wages growth and faster

income growth. This should provide a counterweight to the effect on spending of lower housing

prices.

Taking these various considerations into account, the adjustment in our housing market is

manageable for the overall economy. It is unlikely to derail our economic expansion. It will

also have some positive side-effects by making housing more affordable for many people.

A related issue that the RBA has paid close attention to is the impact of lower housing prices on

financial stability.

In 2017, APRA assessed the ability of Australian banks to withstand a severe stress scenario, in

which housing prices declined by 35 per cent over three years, GDP declined by 4 per cent

and the unemployment rate increased to more than 10 per cent.[2] The estimated

impact on bank profitability was substantial, but importantly, bank capital remained above

regulatory minimum levels. This provides reassurance that the adjustment in our housing market