“Reserve Bank governor Philip Lowe is understood to have met with the big bank chiefs in recent weeks to caution them against an overzealous tightening of credit supply in response to lending rules and the Hayne royal commission”.

The RBA is of the view that lenders are turning good business away, and need to take risk on.

Some SME’s are getting caught in the cross fire, and its clear that business is finding it harder to get funding. This was covered in the RBA’s minutes, released yesterday.

Of course the responsible lending obligations have not changed, but now the meaning and obligations are front of mind. Thus banks need to examine income and expenses etc and cannot necessarily rely on HEM or mortgage brokers. So all this is in direct opposition to the RBA’s wishes, and we suspect the risk of legal action, or worse will continue to limit bank lending.

The ASIC Westpac case will be back before the courts in the new year, though as yet is not clear whether HEM will be tested in court, or whether its more about reaching a settlement. And the royal commission recommendations will be out in February

Is the RBA really condoning the bad behaviour and law breaking exposed in the past year?

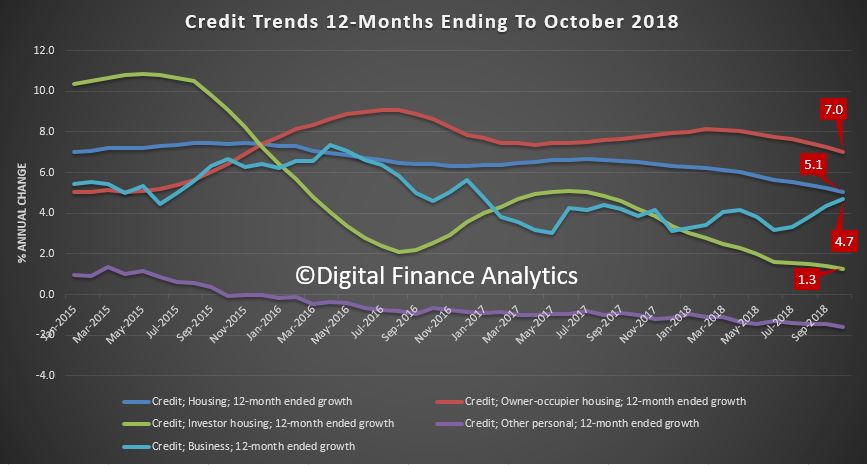

And remember that currently mortgage lending is still running at more than 5% on an annualised basis, according to RBA data.

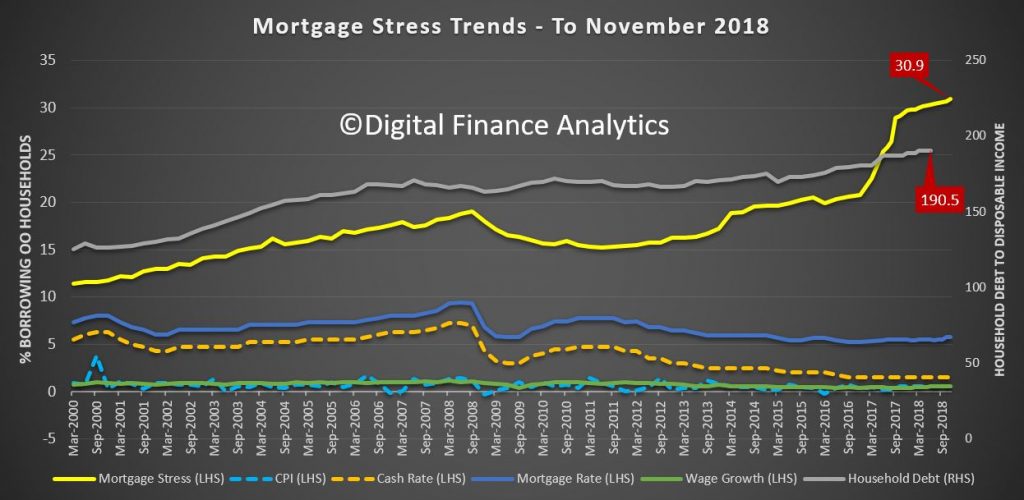

The fundamental problem is the RBA has been responsible for the growth of credit to the point where households in Australia are some of the most leveraged in the world, home prices have exploded and bank balance sheets have inflated. But all this “growth” is illusory. Mortgage stress continues to build and the wealth effect is reversing as home prices slide.

Thus, as we anticipated, we will see a number of “unnatural acts” by the RBA and the Government to try and stop the debt bomb from exploding, by trying to get credit to expand. But this is irresponsible behaviour, in the light of rising global interest rates, high market volatility and building systemic risks.

The RBA minutes today highlighted slowing global growth, GDP growth expectations were stronger than in MYEFO, a decline in the demand for off-the-plan apartments, and average earnings had increased at roughly the same rate as consumer prices over the previous five years or so, leaving real average earnings relatively unchanged despite moderate productivity growth. In addition, there was a pick-up in business lending (mainly to large corporates) by the major bank as growth in their housing lending had continued to slow. The outlook for household consumption continued to be a source of uncertainty because growth in household income remained low, debt levels were high and housing prices had declined. They are still suggesting the next cash rate move is up!

International Economic Conditions

Members commenced their discussion of the global economy by noting that conditions had remained

positive, particularly in the major advanced economies, where growth had remained around or above

potential and labour markets had continued to tighten. However, growth in a number of economies had

slowed this year; softer external demand, at least partly related to trade tensions and the

associated uncertainty, had been a common driver of the slowdown. Bilateral US–China trade had

contracted following the increase in import tariffs between the two countries, while indicators of

external demand, such as new export orders, had softened in the euro area, Japan and other parts of

Asia.

In the major advanced economies, GDP growth outcomes had diverged further in the September quarter,

although there had been some loss of momentum in external demand in all regions. In the United

States, growth had remained strong in the September quarter, driven in part by fiscal stimulus. In

Japan, the pronounced slowing in year-ended GDP growth had been at least partly the result of

disruptions in the wake of natural disasters. One-off factors had weighed on growth in some parts of

the euro area, and business conditions and investment intentions there had also declined.

Employment growth had remained higher than growth in working-age populations across the major

advanced economies and unemployment rates had edged lower from already low levels. Wages growth had

continued to increase, but, with the exception of the United States, this had not yet translated

into higher inflation in underlying terms. Core inflation had remained below target in the euro area

and Japan. Members noted that headline inflation was likely to ease in coming months following the

recent decline in oil prices.

Members noted that it had continued to be difficult to gauge the underlying momentum in the Chinese

economy. Conditions had remained subdued in a number of sectors, including machinery & equipment

production and food & clothing. By contrast, the central authorities’ direction to local governments

to bring forward public spending had contributed to a rebound in infrastructure investment, and the

production of construction-related products had strengthened further. Infrastructure investment was

expected to continue to support growth in coming months. Growth in investment in the real estate

sector had continued to be driven by land purchases.

Elsewhere in east Asia, surveyed business conditions had remained around average and growth in

domestic demand had generally maintained its momentum. However, new export orders had declined and

growth in industrial production and export volumes had also eased somewhat in recent months. Growth

in the Indian economy had eased in the September quarter, but had remained strong in year-ended

terms.

The slowing in global trade and concerns about Chinese demand had been reflected in lower commodity

prices over preceding weeks. Iron ore prices had followed the recent decline in Chinese steel

prices, returning to levels previously seen in mid 2018. Coking coal prices had increased over the

previous month despite the fall in steel prices. Thermal coal prices had declined slightly, while

prices of rural commodities and base metals had been little changed.

Members noted that oil prices had declined by more than 30 per cent since their peak in early

October, mainly reflecting recent and prospective increases in global supply. Oil supply from the

United States had increased rapidly since the trough in oil prices in early 2016 and was expected to

increase further, while production from Saudi Arabia and Russia was expected to be sustained at high

levels. Members observed that the nature of US oil production allowed supply flexibility in response

to changes in oil prices.

Domestic Economic Conditions

Members noted that the national accounts for the September quarter would be released the day after

the meeting. Based on the partial data that were available, GDP was expected to have increased by

more than 3 per cent over the year to the September quarter, above most estimates of potential

growth and in line with the most recent set of Bank forecasts.

In relation to household consumption, members noted that liaison with retailers suggested that

underlying trading conditions had been stable and surveys suggested that households’ views about

their financial situation had remained around average.

Conditions in established housing markets had continued to ease. In Sydney, housing prices had

fallen by around 9 per cent since their peak in July 2017, to be around September 2016 levels. In

Melbourne, housing prices had returned to levels prevailing around March 2017, having fallen by a

little under 6 per cent since their peak in November 2017. Members observed that housing prices had

fallen across all price segments in Sydney, but housing prices had been fairly flat at the lower end

of the market in Melbourne. Auction clearance rates and indicators of private-treaty activity had

also declined a little further in both cities. Housing prices in Perth and Darwin had returned to

levels seen a decade earlier. At the same time, price rises were being recorded in some other

cities.

Preliminary data suggested that dwelling investment had continued around its recent high level in

the September quarter. Given the substantial amount of work outstanding and recent data on dwelling

approvals, dwelling investment was expected to remain around this level for at least the following

year or so before moderating. Liaison with developers indicated that demand for new detached housing

in eastern Australia had eased over the previous year or so and some developers had reported that

this decline in demand had become more pronounced. Demand for off-the-plan apartments had declined

significantly since mid 2017.

Partial indicators, including the Australian Bureau of Statistics (ABS) capital expenditure (Capex)

survey, suggested that both mining and non-mining business investment had declined in the September

quarter. Investment intentions for 2018/19 in the non-mining sector, as reported in the Capex

survey, had been revised higher. Members noted that these revised expectations were consistent with

surveyed business conditions, which had remained above average, and with the relatively high levels

of non-residential building approvals and work yet to be done on non-residential construction

projects.

Members observed that labour market conditions had continued to improve. Employment had increased

solidly in October to be 2.5 per cent higher over the year. This was well above growth in the

working-age population and had been driven largely by growth in full-time employment. Leading

indicators of labour demand had continued to point to employment growth being above average over the

following couple of quarters. The unemployment rate had remained at 5 per cent in October, following

the sharp decline in the previous month. Unemployment rates had fallen in almost all states and

territories over 2018. In trend terms, the unemployment rates in Victoria and New South Wales were

both at their lowest levels in a decade, at around 4½ per cent. Members noted that youth employment

(those aged between 15 and 24 years) had increased significantly over the previous year and the

youth unemployment rate had declined.

Wages growth had picked up a little in the September quarter. The wage price index (WPI) had

increased by 0.6 per cent in the September quarter to be 2.3 per cent higher over the year. This

pick-up had built on the small, gradual increases in WPI growth recorded over the previous two

years. The 3.5 per cent increase in minimum and award wages had contributed to growth in the

September quarter. Joint Reserve Bank–ABS analysis suggested that wages growth for jobs covered by

the other two wage-setting methods, namely enterprise agreements and individual agreements, had also

been stronger than a year earlier. This job-level analysis had also shown that, although there had

been little change over the preceding year in the size of a typical wage increase, the share of the

workforce receiving an increase in any given quarter had increased. Year-ended growth in the WPI had

picked up compared with the previous year across most industries and in all states and territories.

Even so, average earnings had increased at roughly the same rate as consumer prices over the

previous five years or so, leaving real average earnings relatively unchanged despite moderate

productivity growth. This had followed an extended period during the resources boom when real

average earnings had consistently risen faster than productivity. As a result, the gap between real

average earnings and productivity that had opened up during the resources boom had been largely

closed.

Members also discussed a paper on some longer-term trends in the division of aggregate income

between labour and capital. In Australia, the share of total income paid to workers in wages and

salaries (the ‘labour share’) had risen over the 1960s and 1970s but had gradually declined since

then. Over the same period, the share of income accruing to profits (the ‘capital share’) had risen.

Abstracting from fluctuations associated with the terms of trade cycle, the labour and capital

shares had been fairly stable for at least the previous decade. Although the Australian experience

appeared to have been similar to that observed in other advanced economies, the factors driving the

trends had been somewhat different. Members noted that the long-run increase in the capital share in

Australia had stemmed almost entirely from higher profits accruing to financial institutions (since

financial deregulation in the 1980s) and from higher rents paid to landlords and imputed to home

owners (particularly before the 1990s). Members observed that the increasing use of technology to

replace manual effort in the finance sector and long-run increases in the quality and size of homes,

as well as a greater number of dwellings per capita, were likely to have contributed to these

trends. Members also noted the measurement challenges associated with both financial services and

housing services in the national accounts.

Financial Markets

Members commenced their discussion of financial market developments by noting the pick-up in

business credit growth in Australia in the second half of 2018. While foreign banks had been the

main driver of growth in business lending for some time, the major Australian banks had also made a

noticeable contribution to business credit growth in recent months. The pick-up in business lending

by the major banks had occurred as growth in their housing lending had continued to slow. Members

observed that lending to large businesses had accounted for the bulk of the growth in business

credit over preceding years and all of the pick-up in business credit growth in the most recent few

months.

By contrast, lending by banks to small businesses had increased only modestly over the preceding few

years and had been flat in 2018. Moreover, small businesses’ perceptions of their access to finance

had deteriorated sharply over the year, according to the Sensis survey. Members noted that the

Australian Government had recently announced a number of initiatives to support lending to small

businesses.

Turning to housing credit, members noted that growth in lending to investors had remained very weak

and growth in lending to owner-occupiers had continued to ease, to be 5–6 per cent in annualised

terms. The slowing in housing credit growth had been almost entirely accounted for by the major

banks, where the rate of growth in lending had been the slowest in many years. Housing lending by

other financial institutions had continued to grow more strongly.

Members observed that the slowing in housing credit growth appeared to reflect both tighter lending

conditions and some weakening in demand. On the demand side, declining housing prices in some

markets had reduced investor demand. In this context, lenders had continued to compete for borrowers

of high credit quality by offering new loans at lower interest rates than those offered on

outstanding loans. On the supply side, credit conditions were tighter than they had been for some

time. Members noted that the focus on responsible lending obligations in response to the Royal

Commission into Misconduct in the Banking, Superannuation and Financial Services Industry was likely

to have reduced some lenders’ appetite for lending to both households and small businesses.

Mortgage interest rates remained low by historical standards, but had risen a little for many

borrowers in previous months, as most lenders had passed on the increase in their funding costs

resulting from the rise in bank bill swap rates earlier in 2018.

Members noted that financial market pricing implied that the cash rate was expected to remain

unchanged for a considerable period.

Turning to global financial conditions, members noted that financial conditions in the advanced

economies remained accommodative, although they had become less so over the course of the year. A

few central banks had continued gradually to remove monetary policy stimulus and more recently

global equity prices had declined and credit spreads had widened a little (although spreads remained

relatively low).

Expectations regarding policy paths of the major central banks implied by financial market pricing

had been generally little changed over the previous month. However, in the United States the path

for the federal funds rate over 2019 implied by market pricing had moved further below that implied

by the median of Federal Open Market Committee (FOMC) members’ projections published following the

September FOMC meeting. Recent public comments by senior Federal Reserve officials had emphasised

that further withdrawal of monetary stimulus would increasingly depend on how the economy evolves.

Members noted that 10-year government bond yields in major markets had declined in November. In

part, this was likely to have reflected the lowering of market expectations for the federal funds

rate in 2019, as well as the recent sharp decline in oil prices and some easing in expectations for

global economic growth. In the United Kingdom, uncertainty surrounding the approval of a Brexit deal

was also likely to have weighed on long-term bond yields.

Over the year as a whole, diverging central bank policy paths and economic outlooks had seen bond

yields in the United States rise relative to those in Europe and Japan. Consistent with this, the US

dollar had appreciated by 5 per cent over 2018 on a trade-weighted basis.

Global equity prices had declined in October reflecting a range of factors, including US–China trade

tensions, building cost pressures in some countries and a moderation in earnings growth expectations

for 2019. Also, equity valuations in the United States had earlier been somewhat elevated. Members

noted, however, that the US equity market continued to be supported by strong growth in underlying

corporate earnings, with analysts’ expectations for earnings growth in 2019 having been revised down

only a little recently. In Europe, ongoing concerns about Italian fiscal policy settings, as well as

the moderation in growth in the euro area in 2018, had weighed on equity prices, particularly for

companies in the financial sector. Chinese equity prices had been declining throughout 2018,

although they had not fallen further in November. The decline over the year was likely to have

reflected concerns over US–China trade tensions and an easing in growth in economic activity.

Members observed that US corporate credit spreads had widened a little recently, although they

remained low by historical standards. Members noted that this modest tightening in credit market

conditions had occurred against a background of increased corporate leverage, with US non-financial

corporations having increasingly sourced funding from securities markets over the preceding decade

or so. Issuance of investment-grade bonds and, to a lesser extent, leveraged loans had been strong.

Members also observed that securities markets had been increasingly facilitating lending to

lower-rated corporations. While Europe and Australia had also seen increases in investment-grade

bond financing by corporations, banks remained the predominant source of corporate funding in these

markets.

Members noted that, although overall corporate leverage in the United States had increased over

preceding years, it was not high compared with levels in other economies. Nevertheless, high and

rising debt-servicing burdens and the relative increase in debt owed by borrowers of lower credit

quality were likely to have increased the vulnerability of the corporate sector to adverse future

shocks. On the lending side, the non-bank institutional investors that had recently provided most of

the debt financing for corporations tended to have more stable funding and less leverage than banks.

Members discussed implications of this for financial stability, given that, by itself, the reduced

lending role of banks means that the US financial system would be better placed to withstand a

deterioration in credit conditions than in the past. Overall, members agreed that developments in

these markets warranted continued monitoring.

In China, growth in total social financing had slowed through much of 2018, mostly due to a

contraction in non-bank lending, which had previously been a key source of funding for private

firms. This followed earlier measures by the authorities to restrict the availability of credit

provided by non-bank entities in order to reduce risks in the financial system. By contrast, growth

in bank lending, which historically had been disproportionately directed towards state-owned

enterprises, had been stable at a solid rate for a number of years. In recent months, the

authorities had been taking steps to encourage banks to increase their lending to the private sector

(especially smaller enterprises), although members noted that, relative to smaller banks and

non-bank lenders, larger banks were less accustomed to lending to this sector.

Considerations for Monetary Policy

Globally, the economic expansion had continued, although there had been some signs of a slowing in

global trade in the September quarter. In China, the authorities had continued to ease policy in a

targeted way to support growth, while paying close attention to the risks in the financial sector.

Members noted that balancing these considerations remained a key challenge for the Chinese

authorities. Globally, inflation remained low, although wages growth had picked up in economies

where labour markets had tightened significantly. Core inflation had picked up in the United States,

which had experienced a sizeable fiscal stimulus against the background of very tight labour market

conditions, but core inflation had remained low elsewhere. Members noted that the significant fall

in oil prices was likely to reduce global headline inflation over the following year or so, should

it be sustained.

Financial conditions in the advanced economies remained expansionary but had tightened somewhat

because of lower equity prices, higher credit spreads and a broad-based appreciation of the US

dollar over 2018, as the gradual withdrawal of US monetary policy accommodation had continued. In

Australia, there had been a generalised tightening of credit availability. There had been little net

growth in credit to small businesses in prior months. Standard variable mortgage rates were a little

higher than a few months earlier, while the rates charged to new borrowers for housing were

generally lower than for outstanding loans. The Australian dollar remained within its range of

recent years on a trade-weighted basis. Australia’s terms of trade had increased over recent years,

which had helped to boost national income.

Members noted that the Australian economy had continued to perform well. GDP growth was expected to

remain above potential over this year and next, before slowing in 2020 as resource exports were

expected to reach peak production levels around the end of 2019. Business conditions were positive

and non-mining business investment was expected to increase. Higher levels of public infrastructure

investment were also supporting the economy. The drought had led to difficult conditions in parts of

the farm sector.

The outlook for household consumption continued to be a source of uncertainty because growth in

household income remained low, debt levels were high and housing prices had declined. Members noted

that this combination of factors posed downside risks. Notwithstanding this, the central scenario

remained for steady growth in consumption, supported by continued strength in labour market

conditions and a gradual pick-up in wages growth. The unemployment rate was 5 per cent, its lowest

level in six years, and further falls in the unemployment rate were likely given the expectation

that the economy would continue to grow above trend. The vacancy rate was high and there were

reports of skills shortages in some areas.

Conditions in the Sydney and Melbourne housing markets had continued to ease and nationwide rent

inflation was low. Growth in housing credit was very weak for investors and had also eased for

owner-occupiers, reflecting both tighter lending conditions and some softening in demand. Mortgage

rates remained low, and competition was strongest for borrowers of high credit quality.

Taking account of the available information on current economic and financial conditions, members

assessed that the current stance of monetary policy would continue to support economic growth and

allow for further gradual progress to be made in reducing the unemployment rate and returning

inflation towards the midpoint of the target. In these circumstances, members continued to agree

that the next move in the cash rate was more likely to be an increase than a decrease, but that

there was no strong case for a near-term adjustment in monetary policy. Rather, members assessed

that it would be appropriate to hold the cash rate steady and for the Bank to be a source of

stability and confidence while this progress unfolds. Members judged that holding the stance of

monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy

and achieving the inflation target over time.

The Decision

The Board decided to leave the cash rate unchanged at 1.5 per cent.

Marion Kohler the RBA’s Head of Domestic Markets Department spoke at the 31st Australasian Finance and Banking Conference yesterday on “The Long View on Australian Equities“.

She made the point that when interest rates go down, share prices tend to increase, and this increases the wealth of households who hold those equities. In addition, over the long run, equities have been worth much more to investors than other investment options: they have returned about 5 percentage points more than long-term bonds on average each year. Yet the equity market is more volatile than many other markets, so contains more risks. The ASX is bank-heavy and the financial sector more broadly makes up about a third of the exchange by market capitalisation. And finally, on a price-to-earnings ratio basis, Australian equities are not showing signs of heightened valuations.

She perhaps should have added that until recently about half of all dividends came from the finance sector, though that may change in the next few years given the slowing lending market, and the focus on wealth management efficiency and fairness. And she should have shown the distribution of large (international) investors versus smaller local “Mum and Dad” investors who are at structural disadvantage in the equities market.

Here is the speech:

Equities are important for the Australian economy. Today, the equity market is one of Australia’s

largest financial markets. The total value of companies listed here is a bit under $2 trillion;

as you can see in Graph 1 this is more than 100 per cent of GDP. This has not

always been the case: the equity market has rapidly grown as a share of GDP over the past 20

years. Before the 1960s, the government bond market was by far the most important financial

market in Australia.[1]

Graph 1

Equities are also an important part of Australians’ retirement savings. While most people don’t

own shares directly, anyone with superannuation usually holds equities indirectly through their

fund’s investments. Payments from listed companies, in the form of dividends and share

buybacks, were worth almost $100 billion dollars in the past twelve months. By way of

comparison, this is equivalent to about 5 per cent of household income.[2]

Listed companies employ a substantial number of people and many of Australia’s well-known

companies are listed on the stock exchange. This doesn’t mean that the performance of the

stock exchange is the same thing as the performance of the economy. But by understanding

developments affecting listed companies, we can gain timely insights into what’s happening

in the economy more broadly.

And, the Reserve Bank pays close attention to the equity market in particular because it is a

transmission channel for monetary policy. When interest rates go down, share prices tend to

increase, and this increases the wealth of households who hold those equities.[3] Higher share

prices, in turn, make it relatively cheaper for companies to issue shares, allowing them to

expand.

Today I would like to take a step back and look at the Australian equity market through a

longer-term lens. I will focus on returns of equities and the composition of the equity market

through time. I will conclude with some observations on price to earnings ratios. Many of the

graphs and numbers in this presentation draw, in part, from historical datasets compiled by

staff at the RBA. These data – like all historical data – should be interpreted with

some caution. Nonetheless, we think that they are of a sufficient quality to provide some useful

insights and we will soon make them more widely available to interested researchers.

So how do the returns on equity investments compare to other financial assets in Australia? The

return on equity includes gains from both share price changes (or ‘capital gains’)

and dividends paid out. Graph 2 shows cumulative returns on financial assets from $100

invested in 1900, adjusted for inflation. Over the long run, equities have been worth much more

to investors than other investment options: they have returned about 5 percentage points more

than long-term bonds on average each year. This accumulates to a very large amount of money over

a long period of time.[4]

If you had put $100 into the equity market in 1900 in a portfolio that tracked the stock market

index, you would have over $100,000 today after adjusting for inflation; this is more than 100

times what you would have earned from a Government bond or a bank deposit. Perhaps more relevant

to our own investment decisions, if you had put $100 into the equity market when you were 20

years old, given average returns it would have been worth more than $1,000 when you retired at

age 65. If you had invested it in government bonds, it would have been worth only a quarter of

that.

Graph 2

But investing in the equity market comes with risk. The equity market is more volatile than many

other markets: average volatility in the returns generated by equities in Graph 2 is double that

of bonds. This means that at any point in time, investors get a return that can be very

different from the average return. Developments such as the global financial crisis have

emphasised this. In the middle of the financial crisis, share prices fell by around 50 per cent.

If you had a superannuation portfolio based on equities, the value of your retirement funds

would have declined significantly, and remained lower for quite some time. If you were in, or

close to, retirement, you may have had to lock in some of these lower share prices. This

emphasises the value of a diversified portfolio but also the importance of taking a longer-run

view on the equity market.

There are of course different sorts of companies on the stock exchange, and you might expect that

they would provide different return profiles. This is true for some: companies like utilities,

for example, generally have more bond-like properties (and so are quite correlated with bond

prices). At the same time, returns in broader sectors have been remarkably similar over the past

century. You can see this in Graph 3 which shows the cumulative returns on equities in three

broad sectors over the past 100 years – the Reserve Bank often looks at the broad sectors

resources, financials and ‘others’. Indeed, the average annual returns over that

period across the three sectors have been within ½ percentage point of each other. Of

course, resources stocks have been a bit more volatile, in part reflecting their exposure to

volatile commodity prices.

Graph 3

What about compared with overseas? Graph 4 shows the average annual returns on stocks in

Australia, the United States and the United Kingdom since 1900. (The total return is the

dividends – the red bars – and the capital gains – the blue bars – taken

together.) At around 10 per cent, the average annual returns are very similar.[5]

The pattern is not much different if you look at capital gains and dividends separately.

Graph 4

Over shorter periods there is more divergence, as you can see in Graph 5. In particular,

over the past 25 years Australian stock prices have gone up a bit less than the rest of the

world, particularly the United States, as you can see in the blue bars in Graph 5. But

Australian companies pay high dividends, due in part to the specific tax treatment they receive;

I am referring to franking credits, which were initially introduced in 1987.[6] Taking this

into account, Australian stocks have generated above-average returns (the combined red and blue

bars) over the past 25 years.

Graph 5

Let’s have a closer look at the companies that make up the Australian securities exchange

(or, abbreviated, the ASX). Graph 6 compares the concentration of the stock exchange for

different countries. The bars show what share of the total market capitalisation is accounted

for by the top 10 companies. On this metric, the ASX is quite concentrated in large companies,

with the top 10 companies accounting for a bit less than half of the market capitalisation of

the ASX.

Graph 6

You will notice that the countries with the larger concentrations (on the right-hand side of the

graph) tend to be smaller economies.[7]

Among similar-sized exchanges, the level of concentration seen at the ASX is not unusual. It

means, however, that an investor in a market capitalisation-weighted portfolio of equities is

exposed to developments in a smaller set of companies.

This concentration has been a feature of the Australian stock exchange throughout its existence.

In fact, it has been largely the same set of companies that have comprised most of the universe

of Australian stocks over its history. Graph 7 tries to illustrate this point. The top

panel takes all companies listed at the ASX (weighted by market capitalisation) and then

distributes them according to the year the company (or its immediate predecessor) was founded.

The purple section marks companies that are currently in the top 100 companies of the ASX. The

bottom panel does the same aggregated across a number of developed economies. What stands out,

is that for the ASX there are a lot of high purple bars on the left hand side of the panel, that

is a lot of the top 100 companies are old and they are large in terms of market capitalisation.

In fact, the average listed Australian company when weighted by market capitalisation is about

100 years old. This makes our listed companies, on average, substantially older than those in

the United States or Japan (which make up a large share of the graph in the bottom panel). But

it is comparable to the United Kingdom, France and Germany, although stock exchanges there

existed several hundred years before ours.

Graph 7

A striking number of large, still-existing Australian companies were founded in the 1800s, in

many cases before the existence of stock exchanges in Australia. These are mostly the

predecessors of the banks and mining companies, which have their origins in colonial banks and

19th century mining booms, respectively.[8]

By contrast, very few large public Australian companies have been founded in the past 50 years

(and many of the large listings, such as the Commonwealth Bank of Australia and Telstra, have

been privatisations). In this respect, Australian markets are something of an outlier globally.

That said, the stock exchange has not been completely static over the past century, and there

have been substantial compositional shifts at times. Graph 8 shows the ASX shares of the

three large sectors – financials, resources and ‘others’ – through time.[9]

Graph 8

The resources sector (in orange) has tended to expand and contract with mining booms and

commodity prices. During the mining boom of the 2000s, the share of the stock market

capitalisation accounted for by resources companies doubled over a period of about five years:

at their peak, resources companies made up about a third of the ASX 200. But this pales in

comparison with the experience of the late 1960s boom, where the resources sector was worth at

its peak in 1970 around 65 per cent of the exchange by market capitalisation.[10] Of course,

resources booms tend to be followed by busts, and so the large share shrunk within a few years.

On average, the resources sector has a larger weight on the stock exchange than it has in the

real economy.[11]

This could reflect that financing mines can be a speculative, risky investment; equity can be a

more attractive way to finance such investment, allowing investors (with a matching risk

appetite) to share in the potentially large upside without saddling the company with large debt

repayment obligations if the resources discovery (and the associated revenue) disappoints.

The ASX is bank-heavy and the financial sector (in blue) more broadly makes up about a third of

the exchange by market capitalisation: almost exactly the same share as it did 100 years ago.

But, in fact, through most of the 20th century the sector was quite small, reflecting the

regulation following the Great Depression, and only regaining its historical share in the 1980s

and 1990s. The sector has also diversified quite a lot since its early days, with diversified

financials and insurance companies accounting for a much larger share than they used to.

Other sectors (in green) have reflected changes in the industry composition of the Australian

economy over the past 100 years. The rise and fall of manufacturing was reflected on the

exchange, with manufacturers frequently featuring in the top 10 companies through the 1940s and

50s; most of these have since delisted. A company that ferried people across Sydney Harbour was

in the top 50 companies on the exchange for decades, until its business model was disrupted by

the construction of the Harbour Bridge. More generally in the transportation sector, ferries,

steamships and railroads have largely been replaced by road infrastructure and air travel. On

the other hand, some sectors played a significant role in the economy but not on the stock

exchange. Agriculture, forestry and fishing is one example, which for the first half of the 20th

Century accounted for up to 30 per cent of GDP, but has rarely featured in much size

on the stock exchange.

More generally, the size of the equity market relative to GDP – one measure of capital

market development – has fluctuated around about 100 per cent of GDP over the

past two decades. This is broadly in line with the markets of other developed economies.

Australian companies have continued to raise capital on the stock market, and the number of

listed companies has continued to increase, albeit a bit more slowly of late. All this suggests

that equities remain an important source of funds for Australian companies in a wide range of

industries.

Finally, I would like to touch on valuations. In the global low-interest environment of recent

years, some commentators (including the Reserve Bank) have raised the prospect that this has led

to a ‘search for yield’ by global investors, where they bid up the price of risky

assets and thus increase the risk of a sharp correction down the road. One simple way of

measuring this for the equity market is a price-to-earnings ratio, shown here in Graph 9 for

both Australia and the United States. By this measure, Australian equities are not showing signs

of heightened valuations.

Graph 9

This graph also emphasises that, in the long run, share prices are driven by fundamentals, that

is, company profits or ‘earnings’. The Australian share market will likely be

dominated in the future by companies able to sustain profit growth over long periods of time, as

it has been in the past. This may be the current large listed companies, many of whom have

managed to play a role in Australia’s listed equity market for a very long period of time,

as I discussed. Or it may be others.

Some of the points I’ve discussed today are unlikely to change. The stock market will most

likely remain both an important source of funds for Australian corporates, and an investment

vehicle for Australian households and foreign investors. Equities will be more volatile than

safer assets, but will very likely yield higher returns over the long term, and the composition

of the market will continue to broadly reflect the structure of the real economy.

A welcome move, the shadowy Council Of Financial Regulators has started publishing minutes of its quarterly meetings. However, group think, and self-interest is all over it. Specifically the comments about tighter credit, and the need to continue to lend (to keep the debt bomb ticking a bit longer! Also how does independence of the RBA work in this context?

They noted that non-ADI lending for housing has been growing significantly faster than ADI housing lending and there is some evidence that non-ADI lending for property development is also increasing quickly.

As part of its commitment to transparency, the Council of Financial Regulators (the Council) has decided to publish a statement following each of its regular quarterly meetings. This is the first such statement.

The statement will outline the main issues discussed at each meeting. From time to time the

Council discusses confidential issues that relate to an individual entity or to policies still

in formulation. These issues will only be included in the statement where it is appropriate to

do so.

The Council of Financial Regulators (the Council) is the coordinating body for Australia’s

main financial regulatory agencies. There are four members: the Australian Prudential

Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC),

the Australian Treasury and the Reserve Bank of Australia (RBA). The Reserve Bank Governor

chairs the Council and the RBA provides secretariat support. It is a non-statutory body,

without regulatory or policy decision-making powers. Those powers reside with its members.

The Council’s objectives are to contribute to the efficiency and effectiveness of financial

regulation, and to promote stability of the Australian financial system. The Council

operates as a forum for cooperation and coordination among member agencies. It meets each

quarter, or more often if required.

At each meeting, the Council discusses the main sources of systemic risk facing the

Australian financial system, as well as regulatory issues and developments relevant to its

members. Topics discussed at its meeting on 10 December 2018 included the following:

Financing conditions. Members discussed the tightening of credit conditions for households

and

small businesses. A tightening of lending standards over recent years has been appropriate

and

has strengthened the resilience of the system. At the same time, members agreed on the

importance of lenders continuing to supply credit to the economy while they adjust their

lending

practices, including in response to the Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry. Members discussed how an overly cautious

approach by some lenders to incorporating relevant laws and standards into loan approval

processes may be affecting lending decisions.

Members observed that housing credit growth has moderated since mid-2017, with both demand

and supply factors playing a role. The demand for credit by investors has slowed noticeably,

largely reflecting the change in the dynamics of the housing market. In an environment of

tighter lending standards, the decline in average interest rates for owner-occupier and

principal and interest loans suggests that there is relatively strong competition for

borrowers of low credit risk. Credit to owner-occupiers is continuing to grow at 5 to 6 per

cent.

Non-ADI lending. The Council undertook its annual review of non-bank financial

intermediation. Overall, lending by non-ADIs remains a small share of all lending. However,

non-ADI lending for housing has been growing significantly faster than ADI housing lending

and there is some evidence that non-ADI lending for property development is also increasing

quickly. The Council supported efforts to expand the coverage of data on non-ADI lenders,

drawing on new data collection powers recently granted to APRA.

Housing market. Members discussed recent developments in the housing market.

Conditions have eased, but this follows a period of considerable strength in the market.

Housing prices have been declining in Sydney, Melbourne and Perth, but are stable or rising

in most other locations. The easing in the housing market is occurring in a period of

favourable economic conditions, with low domestic unemployment and interest rates and a

supportive global economy. The Council will continue to closely monitor developments.

Prudential measures. APRA briefed the Council on its latest review of the countercyclical

capital buffer, the results of which will be published in the new year. It also provided an

update on its residential mortgage measures, including the investor lending and

interest-only lending benchmarks. In line with APRA’s announcement in April 2018 that it

would remove the investor lending benchmark subject to assurances of the strength of lending

standards, the benchmark has now been removed for the majority of ADIs. The interest-only

lending benchmark, introduced in 2017, has resulted in a reduction in the share of new

interest-only lending, along with the share of interest-only lending that occurs at high

loan-to-valuation ratios.

Financial sector competition. The Council discussed work by its member agencies in response

to the Productivity Commission’s Final Report of its Inquiry into Competition in the

Australian Financial System. The Council strongly supports improved transparency of mortgage

interest rates and a working group is examining a number of options. The Council also

discussed the Productivity Commission’s recommendations relating to lenders mortgage

insurance and remuneration of mortgage brokers.

Both the Productivity Commission and the Financial System Inquiry recommended a review of the

regulation of payments providers that hold stored value – referred to in legislation as

purchased payment facilities (PPFs). The Council released an issues paper in September and held

an industry roundtable in November. Members considered the feedback received from these

processes and received an update on progress with the review.

Limited recourse borrowing by superannuation funds. Members discussed a report to Government

on leverage and risk in the superannuation system, as requested in the Government’s response to

the Financial System Inquiry. The use of limited recourse borrowing arrangements remains

relatively small, but has risen over time. Leverage by superannuation funds can increase

vulnerabilities in the financial system, though near-term risks have reduced with the shift in

dynamics in the housing market.

International Monetary Fund’s Financial Sector Assessment Program (FSAP). The FSAP review of

Australia was conducted during the course of 2018; preliminary findings were presented to the

Australian authorities in November. The Council held an initial discussion of the main FSAP

recommendations and how they could be addressed. The FSAP will be finalised in early 2019, at

which time summary documents will be published. (Further information on the FSAP review was

published in the Reserve Bank’s October 2018

Financial Stability Review.)

Representatives of the Australian Competition and Consumer Commission and the Australian

Taxation Office attended the meeting for discussions relevant to their responsibilities.

He concludes that “Global developments undoubtedly influence Australian financial conditions. In particular, developments abroad can influence the value of the Australian dollar and affect global risk premia. But changes in monetary policy settings elsewhere need not, and do not, mechanically feed through to the funding costs of Australian banks, and hence their borrowers are insulated from such changes”.

But the higher bank funding rate spreads which see here are perhaps more of a reflection of the risks the markets are pricing in, than anything else. Yet this was not discussed. Too low rates here for several years are the root cause (and guess where the buck for that stops?). This led to overheated lending, and home prices, which are now reversing, with obvious pressures on the banks. This leaves the economy open to higher rates, from overseas ahead.

This is the speech:

Australia is a small open economy that is influenced by developments in the rest of the world.

Financial conditions here can be affected by changes in monetary policy settings elsewhere, most

particularly in the United States given its importance for global capital markets. However,

Australia retains a substantial degree of monetary policy autonomy by virtue of its floating

exchange rate. In other words, a change in policy rates elsewhere need not mechanically feed

through to Australian interest rates. While Australian banks raise significant amounts of

funding in offshore markets, they are able to insulate themselves – and by extension

Australian borrowers – from changes in interest rates in other jurisdictions.

Just before delving into the details, some context is in order. First, Australian banks have long

borrowed in wholesale markets, including those offshore. However, they do so much less than used

to be the case (Graph 1).[1]

For a number of reasons, domestically sourced deposits have become an increasingly large share of

overall funding for banks.[2]

Graph 1

Second, to the extent that Australian banks have continued to tap offshore wholesale markets, it

is worth reflecting on some of the characteristics of this borrowing. For instance, some

banking sectors around the world borrow in US dollars in order to fund their portfolios of US

dollar assets.[3] This

can leave them vulnerable to intermittent spikes in US interest rates. However, this is

generally not the case for Australian banks. Rather, a good deal of the borrowing by Australian

banks in US dollars reflects the choice of the banks to diversify their funding base in what are

deep, liquid capital markets. By implication, if the costs in the offshore US dollar funding

market increased noticeably relative to the home market, then Australian banks can pursue other

options. They might opt to issue a little less in the US market for a time, switching to other

markets or even issuing less offshore. They are not ‘forced’ to acquire US dollars

at any price, as some other banks may be. Another important feature of this offshore funding, as

I will address in detail in a moment, is that the banks are not exposed to exchange rate risks

as they hedge their borrowings denominated in foreign currencies.

Independence – It’s an Australian Dollar Thing

As you are well aware, the US Federal Reserve has been raising its policy rate in recent years,

and interest rates in the United States are now higher than in Australia. These developments

reflect differences in spare capacity and inflation: unemployment in the United States is at

very low levels, inflation is at the Fed’s target and inflationary pressures appear to be

building. Since August 2016 – the last time the Reserve Bank changed its cash rate

target – the Federal Reserve has raised its policy rate seven times, by 175 basis points

in total (Graph 2). Yet while Australian banks raise around 15 per cent of their

funding in US dollars, interest rates paid by Australian borrowers since then have been little

changed.

Graph 2

How is it that interest rates for Australian borrowers have been so stable, despite Australian

banks having borrowed some US$500 billion in the US capital markets, in US dollars, paying US

dollar interest rates? The answer lies in the hedging practices of the Australian financial

sector. As I’ll demonstrate, Australian banks use hedging markets to convert their US

interest rate obligations into Australian ones.

The Australian banks fund their Australian dollar assets via a number of different sources. Some

of their funds are obtained in US dollars from US wholesale markets. In order to extend these

USD funds to Australian residents, they convert the US dollars they have borrowed into

Australian dollars soon after the securities are issued in the US. On the surface it would

appear that such transactions could give rise to substantial foreign exchange and interest rate

risks for Australian banks given that:

the banks must repay the principal amount of the security at maturity in US dollars. So an

appreciation of the US dollar increases the cost of repaying the loan in Australian dollar

terms; and

the banks must meet their periodic coupon (interest) payments in US dollars, which are tied to

US interest rates (either immediately if the security has a floating interest rate, or when

the security matures and is re-financed). So a rise in US interest rates (or an appreciation

of the US dollar) would increase interest costs for Australian banks that extend loans to

Australian borrowers.

However, it is standard practice for Australian banks to eliminate, or at least substantially

reduce, these risks. They can do this using a derivative instrument known as a cross-currency

basis swap. Such instruments are – when used appropriately – a relatively

cost effective way of transferring risks to parties with the appetite and capacity to bear them.

Simply put, cross-currency basis swaps allow parties to ‘swap’ interest rate streams

in one currency for another. They consist of three components (Figure 1):

first, the Australian bank raises US dollars in the US wholesale markets. Next, the

Australian bank and its swap counterparty exchange principal amounts at current spot

exchange rates; that is, the Australian bank ‘swaps’ the US dollars it has just

borrowed and receives Australian dollars in return. It can then extend Australian dollar

loans to Australian borrowers;

over the life of the swap, the Australian bank and its swap counterparty exchange a stream

of interest payments in one currency for a stream of interest receipts in the other. In this

case, the Australian bank pays an Australian dollar interest rate to the swap counterparty

and receives a US dollar interest rate in return. The Australian bank can use the interest

payments from Australian borrowers to meet the interest payments to the swap counterparty,

and it can pass the interest received from the swap counterparty onto its bondholders;

At maturity of the swap, the Australian bank and its swap counterparty re-exchange principal

amounts at the original exchange rate. The Australian bank can then repay its bond

holders.[4]

In effect, the Australian bank has converted its US dollar, US interest rate obligations into

Australian dollar, Australian interest rate obligations.

Figure 1

An analogy related to housing can help to further the intuition here. Imagine a

Bloomberg employee who owns an apartment in New York but has accepted a temporary job in Sydney.

She fully expects to return to New York and wishes to keep her property, and she does not wish

to purchase a property in Sydney. The obvious solution here is for her to receive rent on her

New York property and use it to pay her US dollar mortgage. Meanwhile, she can rent an apartment

in Sydney using her Australian dollar income. In other words, our relocating worker can

temporarily swap one asset for another. As a result, she can reduce the risks associated with

servicing a US mortgage with an Australian dollar income.

As I mentioned earlier, it is common practice for Australian banks to hedge their foreign

currency borrowings with derivatives to insulate themselves and their Australian borrowers from

fluctuations in foreign exchange rates and interest rates. The most recent survey of hedging

practices showed that around 85 per cent of banks’ foreign currency liabilities

were hedged (Graph 3). Also, the maturities of the derivatives used were well matched to

the maturities of the underlying debt securities.[5]

This means that banks were not exposed to foreign currency or foreign interest rate risk for the

life of their underlying exposures. By matching maturities, banks also avoided the risk that they

might not be able to obtain replacement derivatives at some point in the future (so called

roll-over risk).

Graph 3

For the very small share of liabilities that are not hedged with derivatives, there is almost

always an offsetting high quality liquid asset denominated in the same foreign currency of a

similar maturity, such as US Treasury Securities or deposits at the US Federal Reserve. Taken

together, these derivative hedges and natural hedges mean than Australian banks have only a very

small net foreign currency and foreign interest rate exposure overall (Graph 4).

Graph 4

So who is bearing the risk?

Despite Australia’s external net debt position,

in net terms Australian residents have passed on – for a cost, as we shall see – key

risks associated with their foreign currency liabilities to foreign residents. Australian

residents have found enough non-residents willing to lend them Australian dollars and to receive

an Australian interest rate to extinguish their foreign currency liabilities. As a result,

Australians are net owners of foreign currency assets, not borrowers.[6] Collectively,

Australians have used hedging markets and natural hedges to (more than) eliminate their

exchange-rate exposures associated with raising funds in offshore markets.

Australians’ ability to find non-residents willing to assume Australian dollar and Australian

interest rate risks is a reflection of the willingness of non-residents to invest in Australian

dollar assets. This in turn reflects Australia’s status as a country that has long had strong

and credible institutions, a high credit rating and mature and liquid capital markets. The

willingness of these non-resident counterparties to assume these risks via a direct exposure to

Australia’s banking system – sometimes for as long as thirty years – reflects the fact that

Australia’s banks are well-capitalised and maintain high credit ratings. In short, Australians

have found a source of finance unavailable domestically (at as reasonable a price), and

non-residents have found an asset that suits their portfolio needs.

Since there are no free lunches in financial markets, there is the question of the cost for

Australian banks to cover these arrangements. One part of this cost is known as the basis.

An imperfect world

Some swap counterparties have an inherent reason to enter into

swap transactions with Australian banks. In other words, such exposures actually help them to

manage their own risks. Non-residents that issue Australian dollar debt – in the so called

Kangaroo bond market – are a case in point. These issuers raise Australian dollars to fund

foreign currency assets they hold outside of Australia. This makes them natural counterparts to

Australian banks wanting to hedge their foreign currency exposures. Similarly, Australian

residents invest in offshore assets. To the extent that they want to hedge the associated

exchange rate exposures, they too would be natural counterparties for the Australian banks.

However, it turns out that these natural counterparties do not have sufficient hedging needs to

meet all of the Australian dollar demands of the Australian banks. So in order to induce a

sufficient supply of Australian dollars into the foreign exchange swap market, Australian banks

pay an additional premium to their swap counterparts on top of the Australian dollar interest

rate. This premium, or hedging cost, is known as the basis. Simply put, the basis is the price

that induces sufficient supply to clear the foreign exchange swap market.[7]

Since the start of the decade, the basis has oscillated around 20 basis points per annum (Graph 5).

Typically, though not always, the longer a bank wishes to borrow Australian dollars, the higher

the premium it must pay over the Australian dollar interest rate.

Graph 5

You may be wondering why Australian banks are willing to pay this premium; why don’t they

instead only borrow Australian dollars in the Australian capital markets to meet their financing

needs? In addition to the prudent desire to have a diversified funding base as I mentioned

earlier, the short answer is that it may not be cost-effective to raise all their funding at

home. What tends to happen is that banks – to the extent possible – seek to equalise

the marginal cost of each unit of funding from different sources. If they were to obtain all of

their funding at home, that would be likely to increase the cost of those funds relative to

funds sourced from offshore. So the all-in-cost of the marginal Australian dollar from domestic

sources will tend to be about the same as the marginal dollar obtained from offshore.

Astute students of finance will also wonder why the basis is not arbitraged away.[8]

The answer is that structural changes in financial markets have widened the scope for market

prices to deviate from values that might prevail in a world of no ‘frictions’. This

is consistent with the concept of ‘limits to arbitrage’ (which the academic

community only started to re-engage with in the past couple of decades). Arbitrage typically

requires the arbitrageur to enlarge their balance sheet and incur credit, mark-to-market and/or

liquidity risk. As Claudio Borio of the BIS has noted: balance sheet space is rented, not free.

And the cost of that rent has gone up.[9]

What about financial conditions more generally?

None of this is to suggest that

monetary policy settings in the United States (and elsewhere for that matter) have no impact on

financial conditions here in Australia. But the link is neither direct nor mechanical.

The primary channel through which foreign interest rates influence Australian conditions is

through the exchange rate. An increase is policy rates elsewhere will, all else equal, tend to

put downward pressure on the Australian dollar, because capital is likely to be attracted to the

higher rates of return available abroad. A depreciation of the Australian dollar in turn will

tend to enhance the competitiveness of our exporters, including those services priced in

Australian dollars like tourism and education. Through various channels, exchange rate

depreciation can also loosen financial conditions in Australia, which is not always the case in

other countries, particularly those for which inflation expectations are not well anchored and

where there are substantial foreign currency borrowings that are unhedged.[10]

Foreign monetary policy settings, particularly those in the United States, can also affect global

risk premia. We are now approaching a period when US monetary policy is moving to a neutral

stance. This follows a lengthy period of very easy monetary conditions, which may have

encouraged investors to ‘search for yield’ to maintain nominal portfolio returns in

an environment of low interest rates. The expectation of low and stable policy rates and

inflation outcomes in turn compressed risk premia across a range of asset classes. In the period

ahead, it seems plausible that term and credit risk premia will rise, which will increase costs

for all borrowers, Australian banks included.

Economist John Adams and I discuss the RBA’s latest speech, in which we see confirmation that they are prepared to cut interest rates and run a QE programme in the event of a crisis.

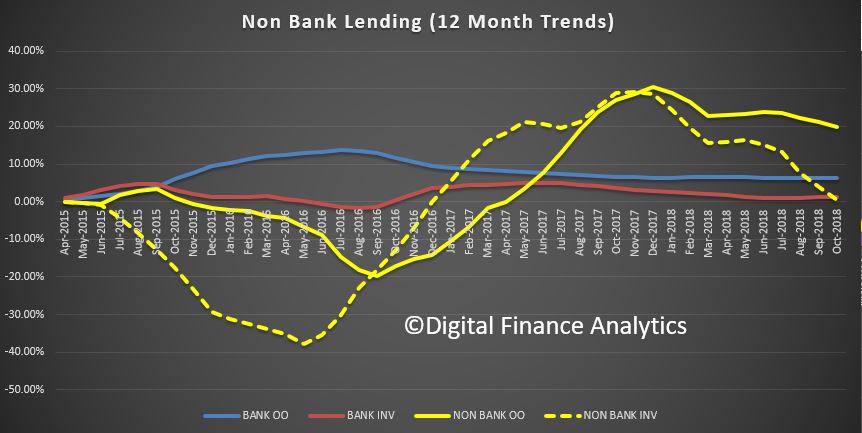

The analysis of the monthly banking stats out last week gives us the opportunity to look across the non-bank sector, relative to the banking sector by comparing the APRA data with the Reserve Bank data series.

We have plotting the rolling 12 month trends, and this chart shows the results.

The striking observation is the relatively stronger growth rate relative to the banks supervised more directly by APRA. Granted APRA does have some responsibilities for the non-bank sector, but appear not to be their main focus.

All lenders have the same obligation with regards to responsible lending, but non-banks are generally more flush with cash, and less constrained by the capital requirements which crimp ADI’s.

Thus we can expect the growth on non-ADI mortgage lending to continue at a faster pace than the bank sector. As a result, we think more risks are building in the financial system.

It was a reflection on 10 years after the GFC. One of the main lessons was an old one: leverage matters.

While acknowledging that household debt is higher in Australia than many other countries, there is little to form a strong conclusion about how much is too much, he said.

Leverage can turn a manageable macroeconomic event into a very hard to manage crisis. The regulatory response has been aimed at addressing this by reducing the leverage in the core of the financial system, while being mindful that the risk and leverage is not excessively relocated elsewhere.

The second lesson is that timely policy responses are effective. In a crisis, go fast and go hard. Don’t die wondering.

The third lesson is that the plumbing can sometimes really matter. Keep the credit pipes flowing.

Fourth, targeted policy responses/interventions are effective. Use Bagehot pricing, where these interventions are priced to work in bad times but not in the good times.

But the questions of how much debt is enough and how much is too much remain unresolved.

The lessons learned from the GFC will be useful, provided they are not forgotten. But there will be new challenges ahead and the source of the next crisis will probably be different.

Some are taking this as a hint the RBA is ready to cut rates and apply stimulus to the economy! Unnatural acts?

It is now just over 10 years since the date that people most associate with the Global Financial Crisis (GFC), namely 15 September, the day that Lehman Brothers filed for bankruptcy.[1] There have been quite a number of articles written in recent months looking back at that time and the period leading up to it.[2] It is interesting to read the differing perspectives on the same set of events, especially those that recount events that I had a ringside seat at, or was even in the ring itself. As I have said recently, it’s a bit like the standard line about the sixties, those who can remember the GFC probably weren’t there. The sleep-deprived haze that was pervasive at the time affects the memory. Critical decisions were made under extreme duress and fatigue, particularly in the US, which by and large stack up well with the passage of time.

Today I am not going to give another detailed account of what happened. I will talk about some of the events, but the main thing I intend to do is to talk about some of the lessons learned and relearned from the crisis. This list of lessons is by no means comprehensive. I will also discuss some questions that arise from the crisis that remain unresolved, at least in my mind. They are questions which I think should be a focus of the economics profession. Answering them will help guide policymakers should they be faced with similar situations to the one we confronted in 2008.

I am going to talk about both macro and finance today. Some events can be seen through mostly a macro lens with finance playing a lesser role (the seventies in Australia is an example), some events can be seen with the spotlight on finance with macro as a sideshow (e.g., the dotcom bubble). I don’t think it is possible to look at the GFC and talk about one without the other.

It is clearly important to integrate finance into macroeconomic analysis. Indeed, the failure to do that is a criticism that is often levelled at central banks and the macroeconomic profession in the aftermath of the crisis. I think this criticism is overstated. One obvious counter example is the work of Ben Bernanke himself on the Great Depression, Japan and the financial accelerator. His large body of work very much informed the Fed’s actions during the GFC.

How should this integration occur? Should finance be built directly into the models that inform (though do not dictate) policymaking decisions? There is a body of work directed at that goal currently underway.[3] Building finance into macro models is one approach but by no means the only one. At the very least though, macroeconomics should have an understanding of finance and vice versa. Macroeconomics is like the model of the engine, finance is the oil that lubricates the engine. One can understand how the engine works without really needing to worry about the oil, as long as the oil is flowing. But at least a basic understanding of the plumbing is useful when the oil dries up.

The key lesson that comes from the crisis that I will highlight today is leverage really matters. Leverage significantly magnifies the effect of any shock that hits the economy. Leverage might not start the fire, but it will pour petrol on a burning platform. At the same time, you need to keep the credit flowing to prevent the economy from seizing up.

Ballad of a Thin Man

Something’s happening here but you don’t know what it is, do you Mr Jones?

That is the Dylan version of the question Queen Elizabeth posed: why didn’t anybody see this coming? There were those who saw the storm clouds on the horizon. Michael Lewis wrote a book about some of them. Though often the storm didn’t quite take the form these people were expecting. Very few appreciated the extent of the financial interconnectedness and what that implied. For example, one common prediction was there would be a US dollar crisis with consequent calamity, but, in the event, the US dollar appreciated through the crisis.

Looking back on how financial markets reacted through 2007, the onset of the crisis is often dated from BNP Paribas shutting three funds with subprime mortgage exposure on 9 August. That caused a short-lived wobble in equity markets, but after that it was onwards and upwards for much of the rest of the year, with the equity market peaking in November. The equity market was the lens through which the public saw events unfold. So by that metric, 2007 was fairly benign.

Macroeconomists generally looked at what was unfolding in the US housing market and expected that its spillover to the rest of the economy would be contained. The slowdown would be mild and, to an extent, welcome in containing the inflationary pressures that had been building.

But the fixed income market took fright and got more and more scared through 2007. Uncertainty increased about the quality and value of asset-backed securities and the assets that underpinned them. There was further uncertainty about whose books these assets resided on, generating a marked rise in counterparty risk aversion amongst financial institutions. That is, institutions became less willing to lend to each other, both because of concerns about the financial strength of the counterparty as well as a desire to hoard any available liquidity, should they themselves need it. The indicator of the tension in fixed income markets is the LIBOR/OIS spread (BBSW/OIS here in Australia), which summarises the unfolding of the crisis well (Graph 1).

Graph 1

These tensions continued to increase with a rolling series of flare-ups, including notably the rescue of Bear Stearns by JP Morgan in March 2008. By this stage, these concerns were increasingly reflected in the equity market too. GDP growth in a number of economies started to slow, but it was not until the fourth quarter 2008 when the economic forces took hold with a vengeance.

Lehmans filed on the Monday morning Australian time. It is interesting to look back at the time. That day was a relatively quiet one in financial markets. Lehmans wasn’t the turning point. The actual zenith of the crisis was still to come in the following weeks. AIG, the poster child of financial connectedness, was rescued. TARP was rejected by Congress and then passed after financial tumult broke out. The prime mutual fund Reserve broke the buck. Washington Mutual failed.

Markets were driven by fear, with huge swings in prices. Many of these swings occurred late in the New York trading day, which was early in the Australian day. The correlation between the Australian dollar and the US equity markets through those periods was indicative of the extremely high degree of co-movement across all markets. Markets regularly recorded ‘25 standard deviation events’ in the words of then Goldmans CFO David Viniar. These sorts of events are only supposed to be happening once in the lifetime of the universe, which says something about the risk models that were being used at the time.

My recollection of the worst of it was in the early hours of Saturday morning 11 October after we had been intervening in the foreign exchange market through the Friday evening to provide liquidity into an almost completely illiquid market. Talking on the phone to the RBA desk in New York, they reported that US Treasuries, the most liquid market in the world, had effectively seized up.

It is worth recounting this, just to recall how dislocative and disruptive these developments were. It was really not clear how this was going to end, except badly.

The fourth quarter of 2008 was bad. Global GDP declined by 1.5 per cent. GDP in the US fell by 2.2 per cent. In Australia, GDP contracted by 0.5 per cent (Graph 2). The impact was particularly severe in global trade, which collapsed as trade finance dried up because of extreme counterparty risk aversion (Graph 3). Companies and banks were unwilling to accept the guarantee of another bank that underpinned the trade lines of credit. They had little confidence they were going to be paid.

Graph 2

Graph 3

The breadth and depth of the impact was remarkable. Output fell by more in the Great Depression, but the Great Depression was not synchronised nor as widespread as this was.

These macroeconomic and financial developments very much underpin the nature of the global policy response, both monetary and fiscal.

There was a fiscal response in many (though not all) countries, buttressed by the G20 leaders meeting in April 2009.[4]

Central banks responded by reducing policy rates rapidly to very low levels. Some of these actions were coordinated in a hitherto unprecedented manner. Central bank balance sheets expanded rapidly (Graph 4). The re-intermediation by central banks mitigated the withdrawal of intermediation by the banking sector. A part of that increase in the balance sheet addressed the large counterparty risk aversion. Central banks were willing to stand between institutions that were unwilling to deal with each other, as well as accommodate the rapid increase in demand for liquidity. That large increase in central bank balance sheets mitigated the large contraction in the financial sector, which goes a long way to explaining why it has still yet to lead to a marked rise in inflation, despite this being foreshadowed by a number of commentators over the past decade.

Graph 4