The Central Bank has finally released details of the landmark prosecution that involved two of its subsidiary companies involved in bribing overseas officials for note-printing contracts, via InvestorDaily.

Following a decision by the Supreme Court of Victoria this week, the Reserve Bank of Australia (RBA) is able to disclose that in late 2011, its subsidiaries – Note Printing Australia (NPA) and Securency – entered pleas of guilty to charges of conspiracy to bribe foreign officials in connection with banknote-related business.

The offences were committed over the period from December 1999 to September 2004.

The RBA and the companies were not permitted to disclose these pleas prior to today due to suppression orders, which have now been lifted. The orders were not sought by the RBA or the companies.

In a statement this week, the RBA said the boards of NPA and Securency decided to enter guilty pleas at the earliest possible time rather than to defend the charges, reflecting an acceptance of responsibility and genuine remorse.

“The decisions to plead guilty were based on material that became available to the boards after allegations about Securency had been referred to the Australian Federal Police (AFP) and followed extensive legal advice. The decisions also took into account the public interest in avoiding what was expected to be a costly and lengthy court process,” the central bank said.

No evidence of knowledge or involvement by officers of the RBA, or the non-executive members of either board appointed by the RBA, has emerged in any of the relevant legal proceedings or otherwise.

“The Reserve Bank strongly condemns corrupt and unethical behaviour,” Reserve Bank governor Philip Lowe said.

“The RBA has been unable to talk about this matter publicly until today, although the guilty pleas were entered in 2011. The RBA accepts there were shortcomings in its oversight of these companies, and changes to controls and governance have been made to ensure that a situation like this cannot happen again.”

In 2011, the Reserve Bank Board commissioned a thorough external review of the RBA oversight of the companies. The RBA oversaw a comprehensive strengthening of governance arrangements and business practices in the two companies.

In early 2013, the RBA sold its interest in Securency, having ensured that all the compliance issues of which the RBA was aware had been addressed.

With the lifting of the suppression orders, the RBA is now also able to disclose that the companies paid substantial penalties as a result of the court proceedings.

NPA paid fines totalling $450,000 and a pecuniary penalty under the Proceeds of Crime Act 2002 of $1,856,710. Securency paid fines totalling $480,000 and a pecuniary penalty under the Proceeds of Crime Act of $19,809,772.

Since the companies entered their pleas, four former employees of Securency have pleaded guilty to charges of conspiring to bribe and/or false accounting. Charges against four former employees of NPA were permanently stayed on the basis that continued prosecution of these individuals would bring the administration of justice into disrepute.

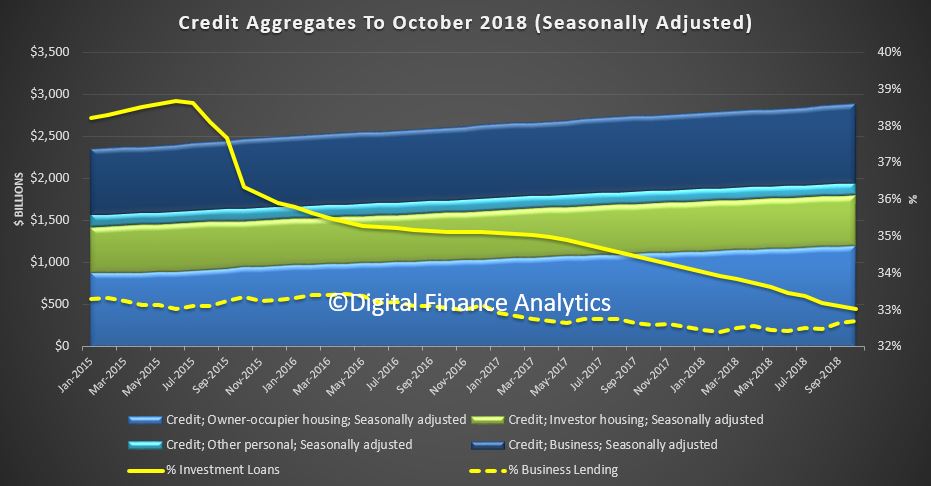

The RBA and APRA both released their statistics today to end of October. The data clearly shows the mortgage flows are easing, which is a key indicator of weaker home prices ahead. Remember it is the RATE of credit growth, or the credit impulse we need to watch. Essentially, for home prices to rise, the rate of credit growth needs to accelerate, and the reverse is also true as can be clearly seen.

The RBA credit aggregates shows that overall credit rose by 0.4% last month, or 4.6% over the past year. Housing credit rose by 0.3% in October, or 5.1% over the past year. Business credit rose 4.7% over the past year and 0.6% in October. Personal credit fell 1.6% over the year, and broad money rose by 1.9%, compared with 6.8% last year – the credit impulse is easing!

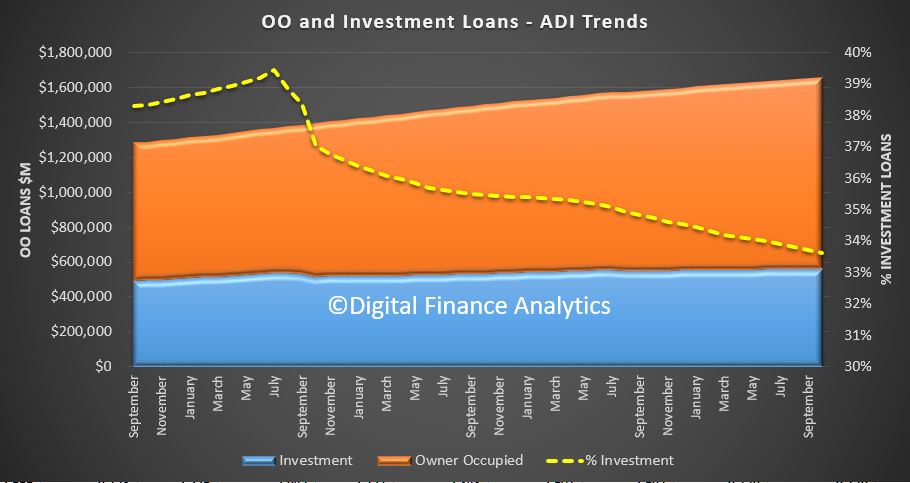

Total housing lending rose by 0.28% to $1.78 trillion. Within that owner occupied lending rose 0.42% or $5 billion to $1.2 trillion while investment lending rose by just 0.1% to $593.6 billion. Investment loans fell to 33% of all loans, down from 38.6% in 2015.

Business lending was 32.7% of all lending, lower than 2015.

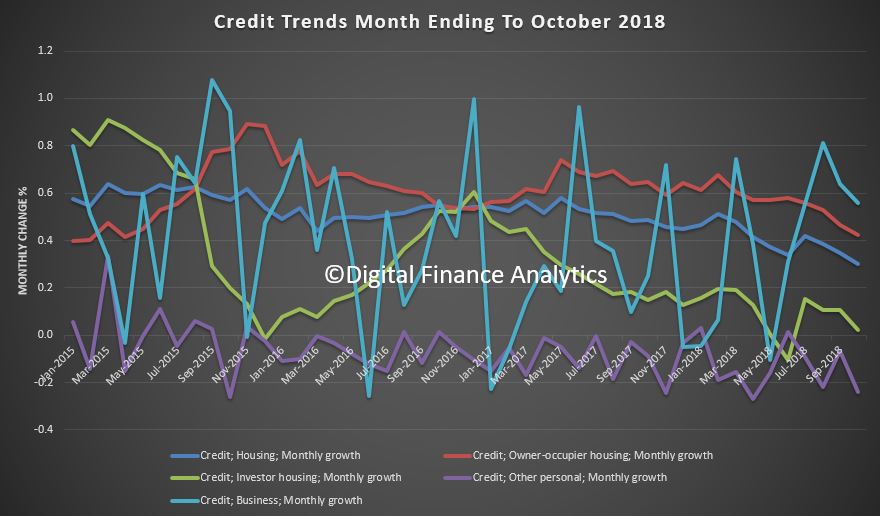

The monthly flows continue to show significant noise…

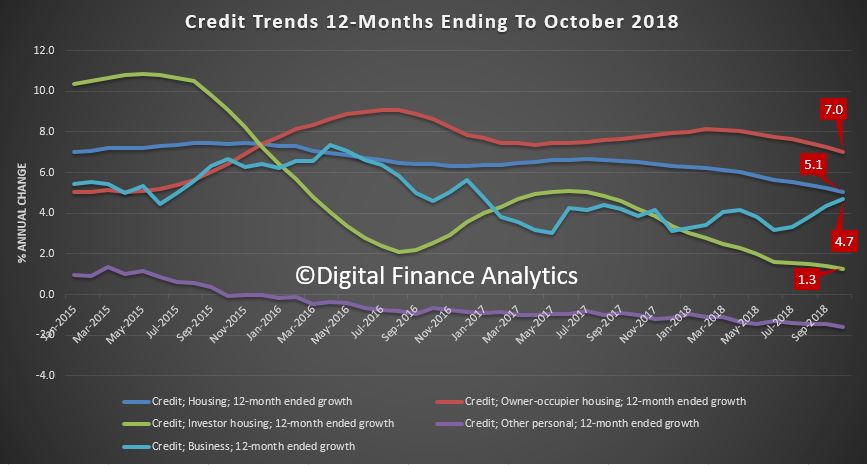

… but the annualised figures show the fall in housing lending across the board.

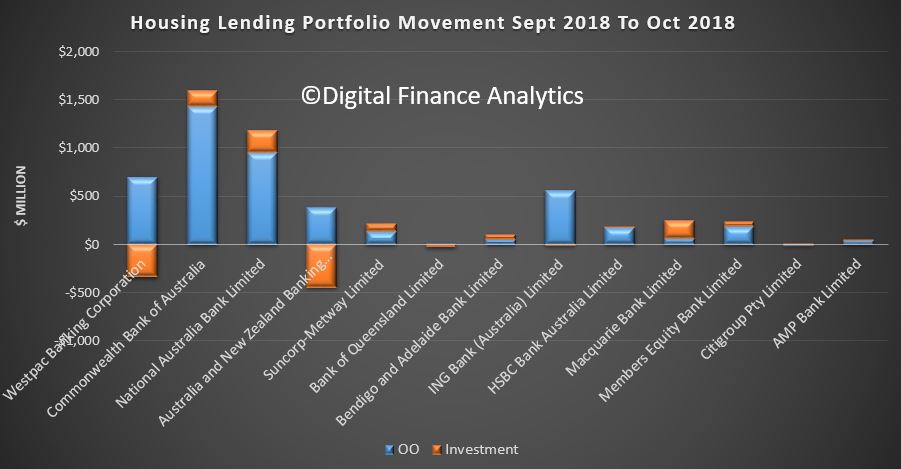

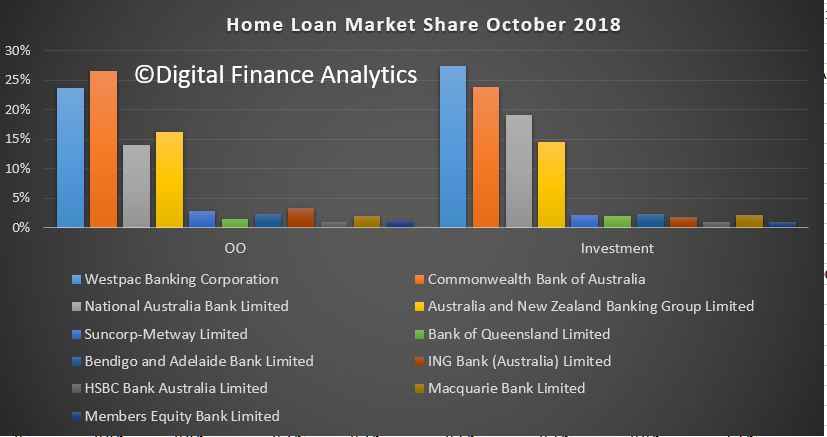

Turning to the APRA banking stats, we can look at individual lender portfolios. We see that Westpac and ANZ both reduced their investor loan portfolios between September and October, while NAB and CBA grew theirs.

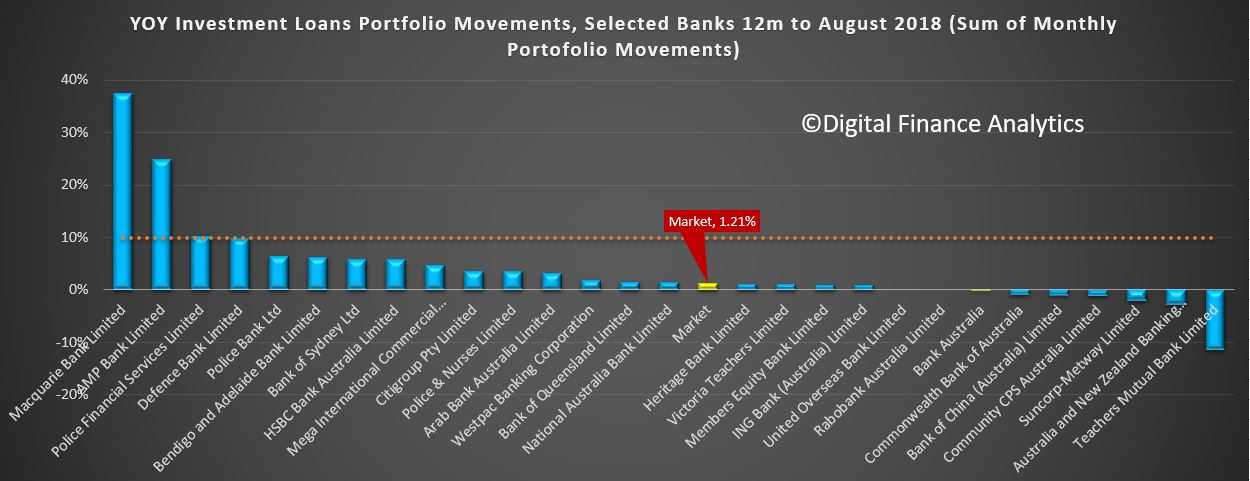

Macquarie Bank is still growing its investor pools (well above the now obsolete APRA 10% speed limit).

ADI portfolios hardly moved overall with CBA still the largest owner occupied lending, and Westpac the largest investment lender.

We can still plot the annualised movements of investor loans, and we see a small number of lenders well above the 10% speed limit (which was removed a few months ago). Significantly many lenders are well below that rate.

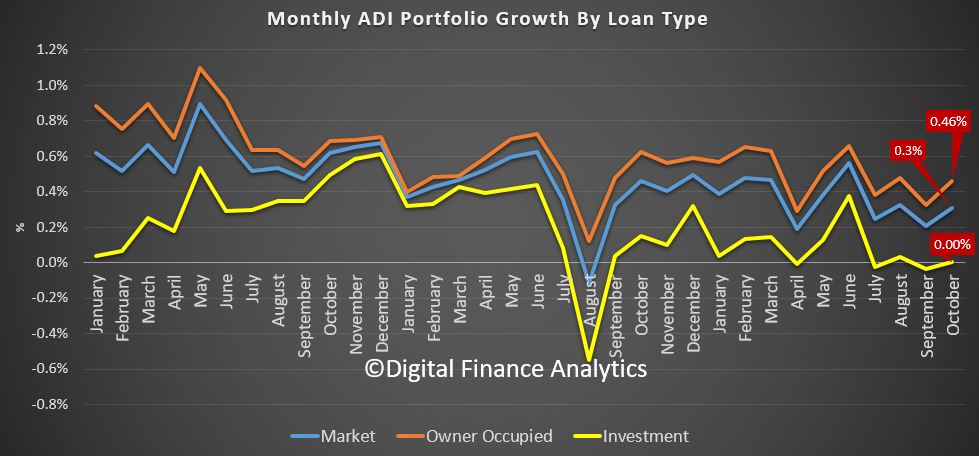

At an aggregate level, lending by ADIs was up 0.3% in the month, with investor loans flat, and owner occupied loans at 0.46%.

The proportion of investor loans fell again in stock terms to 33.6%.

Total ADI lending rose to $1.66 trillion, up 0.3% of $5 billion. Owner occupied loans rose 0.46% to $1.1 trillion and investor loans rose 0.004% to $557.4 billion.

In fact some smaller banks, and non-banks are growing their portfolio faster than the majors, thus the rotation across the sectors continues.

We expect credit to continue to grow more slowly ahead, and this will lead home prices lower.

He suggests a turning point has been reached. It is now easier than it has been to conceive of a world in which banknotes are used for relatively few payments; that cash becomes a niche payment instrument.

This morning I would like to speak about the shift towards electronic payments; or as the title of my remarks says, the journey towards a near cashless payments system. For some decades, people have been speculating that we might one day go cashless – that we would no longer be using banknotes for regular payments and that almost all payments would be electronic. So far, this speculation has been exactly that – speculation. But it looks like a turning point has been reached. It is now easier than it has been to conceive of a world in which banknotes are used for relatively few payments; that cash becomes a niche payment instrument.

Given this, I would like to structure my remarks around three broad points.

The first is that the shift to electronic payments is occurring quite quickly and it is likely to continue. This shift is a positive development that should promote our collective welfare.

The second is that if we are to realise the benefits of moving to a near cashless payments system, the electronic system needs to offer the functionality, safety and reliability that people require. People need to have confidence that the electronic payment system will be operating when they want to make their payments and that it will deliver the payment services that they need.

The third point is that as we undertake this journey towards a near cashless payment system, there will be a greater focus on the cost of electronic payments. If almost all payments are electronic, then the cost of making these payments matters more than it used to. The electronic system needs to be as efficient as it can be and to be characterised by strong competition. In my view, there is further work to be done here.

1. The Shift to Electronic Payments

The Reserve Bank conducts regular surveys of how Australians make their payments. The next survey will be undertaken in 2019. Until then, perhaps the best illustration of the declining use of cash for transactions is the sharp decline in the number and value of cash withdrawals through ATMs (Graph 1). Around the turn of decade, Australians went to an ATM, on average, around 40 times per year. Today, we go to an ATM around 25 times a year and the downward trend is likely to continue.

Graph 1

At the same time as the use of cash for payments has been declining, the number of electronic transactions has been growing strongly (Graph 2). Today, Australians make, on average, nearly 500 electronic payments a year, up from around 100 per year around the turn of the century.

Graph 2

New payment technologies are being developed that will further encourage this shift to electronic payments. Perhaps the most significant of these is the New Payments Platform, which has made it possible for people to make real-time person-to-person payments without using banknotes. A range of payment apps are also under development that would have the same effect. So the direction of change is clear.

There also continues to be a decline in the use of cheques (Graph 3).[1] In the mid 1990s, Australians, on average, made around 45 cheque payments per year. Today, we make around three per person. Given this trend is likely to continue, it will be appropriate at some point to wind up the cheque system, given the high fixed costs involved in operating the system. We have not reached that point yet, but it may not be too far away. Before we do, it is important that alternative payment methods are available. Progress has been made on this front, but more is required.

Graph 3

It is worth pointing out that despite the decline in cash use, the value of banknotes on issue, relative to the size of the economy, is close to the highest it has been in fifty years. For every Australian there are currently around thirty $50 and fourteen $100 banknotes on issue (Graph 4).

Graph 4

So there is an apparent paradox between the declining use of cash and the rising value of banknotes on issue. The main explanation is that some people, including non-residents, choose to hold a share of their wealth in Australian banknotes. The opportunity cost of doing this is less than it used to be because of the low level of interest rates.

While it is difficult to predict the future, I expect that banknotes will remain part of our payments system for some time to come.

In some situations, paying with banknotes is quicker and more convenient than paying electronically, although this advantage is less than it once was. Some people also simply prefer paying in cash – our 2016 survey indicated that around 14 per cent of Australians had a preference for using cash as a budgeting tool.

Banknotes also allow payments to be made anonymously in a way that is not possible in systems that leave an electronic fingerprint. This privacy aspect is valued by some people. In some circumstances this desire for privacy is entirely legitimate, but in others it has more to do with tax evasion and illegal activities.

Perhaps a more important source of ongoing demand is the fact that using cash does not require the internet to be up, electricity to be working and the banks’ systems to be operational. Banknotes are therefore an important emergency or back-up payment instrument. They are particularly useful in the event of natural disasters or failure of the electronic system. Perhaps one day the various systems will be so reliable that a backup will not be needed, but that day still seems some way off.

Overall, the shift to electronic payments that is occurring makes a lot of sense – it is similar to other aspects of our lives where things that used to be physical have been supplemented with, or replaced by, technology. This shift is likely to promote our collective welfare. I say that even though the Reserve Bank is the producer of banknotes and earns significant income, or as it’s known, seigniorage, for the taxpayer from their use. The greater use of electronic payments can bring efficiency benefits, with lower costs and more functionality and choice for users. One example of this is the reduced tender time involved in card transactions due to contactless technology. There are also non-trivial production and distribution costs involved in the cash system. Some of these are fixed costs, so the average cost of cash transactions is likely to rise as the volume of cash transactions falls. Looking ahead, there is also more limited scope for fundamental innovation in the cash system compared with the scope for dynamic innovation in electronic payments. So this journey is in our national interest.

2. Functionality, Safety and Reliability

I would now like to discuss three interrelated factors that will influence how quickly we undertake that journey. These are: the functionality offered by the electronic system; the safety of that system, and the reliability of that system. The other factor that is also relevant is cost, and I will touch on this a little later.

Functionality

The rapid adoption of contactless payments in Australia shows that Australians change how they pay quite quickly when new functionality is offered. Contactless card payments were slow to take off but once critical mass was established, they grew very quickly. In our 2013 consumer payment study they accounted for around over 20 per cent of point of sale card payments; three years later they accounted for over 60 per cent. So the functionality of the electronic payments system is key.

The development of the electronic payment system took a major step forward earlier this year with the launch of the New Payments Platform (NPP). This system allows people to make payments 24 hours a day, 7 days a week, using just a simple identifier such as a mobile phone number or an email address. It also allows a lot of information to accompany the payment. I expect that over time this extra functionality will further reduce the use of cash in the economy and also improve the efficiency of the electronic system.

The number of transactions through the NPP is steadily increasing (Graph 5). After a relatively low-key start, there are now around 400,000 NPP transactions per day. Over 2 million PayIDs have also been registered, and we expect further growth as the banks continue to roll out services to their customers.

Graph 5

The concept behind the NPP is that so-called ‘overlay’ services are developed, and that these overlay services offer new functionality that utilise the real time capability of the NPP. The first overlay service provides for a basic account-to-account payment. Among the subsequently planned overlay services are ones that will allow someone to send a request to pay, perhaps to a friend for their share of a meal out. Another overlay service would allow a link to a document to be sent with a payment; this could be a payslip or a detailed record of the transaction.

It was originally anticipated that these two overlay services would be up and running not long after the NPP launch. Unfortunately, this timeline has slipped. A number of the major banks have also been slower than was originally expected to roll out NPP functionality to their entire customer bases. This is in contrast to the capability offered by smaller financial institutions, which from Day 1 were able to provide their customers with NPP services. Given the slow pace of roll-out by the banks, and the prospect of delays for additional overlay services, I recently wrote to the major banks on behalf of the Payments System Board seeking updated timelines and a commitment that these timelines will be satisfied. It is important that these commitments are met.

It is worth observing that in other countries where banks have been slow to develop payment applications that meet the needs of the public, other possibilities emerge. China is perhaps the best example of this, with the emergence of QR-code-based payments. I expect that the NPP infrastructure will be the backbone of our electronic payments system for many years to come. But for this to be the case, the system will need to provide the functionality that people require, and it will need to do this on a timely basis.

There are a range of fintech firms that are excited by the capabilities offered by the NPP and the potential for it to be used for innovative payment solutions. In October, the RBA issued a consultation paper seeking views on the functionality and access arrangements for the NPP. In particular we are interested in views on whether the various ways of accessing the NPP, and their various technical and eligibility requirements, are adequate for different business models.

A topic that I get asked about from time to time is whether the functionality of the electronic system would be enhanced by the RBA issuing an electronic version of the Australian dollar, an eAUD. I spoke about this issue at this conference last year, concluding that we did not see a public policy case for moving in this direction at the time. In particular, it is not clear that RBA-issued electronic banknotes would provide something that account-to-account transfers through the banking system do not, particularly with the emergence of the NPP. Another important consideration was the implications for financial stability. A year on, our views have not changed.

Security

A second important influence on the rate at which we shift to a more electronic payments system is the public’s confidence in the security of the system.

Given this, a recent focus of the Payments System Board has been the high and increasing level of fraud in card-not-present transactions (Graph 6). Card-not-present fraud rose by 15 per cent in 2017 and now represents 87 per cent of total scheme card fraud losses.[2] In contrast, the industry has had successes in addressing card-present fraud, with the introduction of chip technology and the switch to PINs. Despite this, growth in e-commerce activity has provided new opportunities for would-be fraudsters.

Graph 6

The Payments System Board identified the rise in card-not-present fraud as a priority for the industry. In August this year, the Board was pleased to welcome AusPayNet’s publication of a draft industry framework to mitigate card-not-present fraud, and supports continued collaboration on this issue.

A separate but not unrelated priority for the industry is to progress work on digital identity. This is another area where barriers to effective coordination can arise. I am pleased that AusPayNet is undertaking work here, under the auspices of the Australian Payments Council. Digital identity is likely to become increasingly important as more and more activity takes place online. The RBA is highly supportive of industry collaboration on this issue and views it as important that substantive progress is made.

More broadly, individuals, businesses, governments and financial institutions all need to be aware of cyber risks. In the RBA’s most recent Financial Stability Review we noted the increasing sophistication of cyber attacks and that regulatory authorities have increased their focus on cyber issues.

Reliability

A third factor is the confidence that people have that they will be able to use the electronic system when they need to make their payments. As I noted earlier, people will still want to hold and use banknotes if they can’t be sure that the electronic system will be available when they need it. In our consumer payments survey in 2016, we asked people about why they held cash in places outside of their wallet. The most common response, from nearly half of respondents, was that it was for emergency transaction needs.

Over recent times, there have been a number of serious operational incidents that have interrupted the payments system. On some occasions these have been caused by problems with the telecommunications companies and at other times by problems at the banks. An operational incident at the RBA in August as a result of problems with a routine fire test also saw a number of RBA core systems unavailable for some hours, including the Fast Settlement Service supporting the NPP.

We all need to do better here. As we rely less on cash, outages affecting retail transactions can have a significant impact on businesses and individuals. So continued effort needs to be made by all participants in the payments system to reduce operational problems. If this does not happen, then it is possible that the Payments System Board could consider setting some standards.

3. Increased focus on Cost and Competition

My third broad point is about the cost of electronic payments and the importance of competition.

As we move to a predominantly electronic world, there will be more focus on the cost of operating the electronic payments systems and how those costs are allocated between those making and receiving payments.

Looking forward, I expect that over time the cost of electronic payments will decline further, due to both advances in technology and economies of scale. Even so, there are significant costs to operate the electronic systems, including costs for front- and back-end systems to maintain accounts, and to deliver functionality and convenience to users, as well as costs in preventing fraud and ensuring resilience. How these costs are managed and who pays for them will have a significant bearing on the efficiency of the overall system.

In terms of card payments, merchants in Australia currently pay less than merchants in many other countries. The comparison with the United States is particularly stark (Graph 7). For credit cards, Australian merchants, on average, pay 0.8 per cent of the transaction value for Mastercard/Visa transactions. In the United States the figure is much higher at around 2.2 per cent. There are also differences in the cost of debit cards and American Express cards between the two countries.

Graph 7

The main reason for the lower merchant costs in Australia is our lower interchange fees. These fees were reduced in Australia as a result of regulation by the Reserve Bank commencing in 2003. The RBA’s reforms reduced average interchange fees in the Mastercard and Visa systems by around 45 basis points. This has been reflected in merchant service fees; indeed, these merchant fees have fallen by somewhat more than the cuts to interchange, likely reflecting an increased focus on card acceptance costs by merchants (Graph 8). In addition, as a result of competitive pressure, including from the removal of no-surcharge rules, fees on American Express and Diners Club have also fallen over time.

Graph 8

Notwithstanding the reduction in interchange fees, these fees still represent, on average, around 60 per cent of the total merchant service fee on credit cards. So they remain an important part of the total cost to merchants. Conversely, these fees mean that the cardholder’s bank gets paid each time the card is used. This has meant that the cost to consumers of using these cards is often low; in some cases, cardholders are actually subsidised to use their card, through reward points and/or interest-free credit. The subsidy is provided by the cardholder’s bank, but ultimately paid for by the merchant.

The close link between interchange and merchant costs means that there continues to be significant focus on interchange and its implications for the distribution of costs between merchants and consumers. For example, there have been recent recommendations from the Black Economy Taskforce and the Productivity Commission for the Reserve Bank to consider regulatory action to lower, or even ban, interchange fees. The Payments System Board will again examine the arguments for lower interchange fees when it next conducts a formal review of the card payments system.

On the competition front, one area that merits close attention is the market for acquiring services. This has come into sharper focus as a result of concerns about the costs to merchants in the debit card system, where most cards allow for transactions to be processed by either of the two networks enabled on the card. The longstanding view of the Payments System Board has been that merchants should at least have the choice of sending the debit payment through the lower cost system, whether that be eftpos or the international scheme.

For merchants to be able to do this though, acquirers need to offer terminals and technical systems enabled to allow least-cost routing. Some acquirers have already completed the necessary work and are attracting new merchants. Others, including the major banks, made commitments earlier in the year regarding the timetable for this work to be completed. Partly on the basis of those commitments, the Payments System Board made a decision not to regulate. Since then, I regret to say there has been slippage by some, who have cited technical problems. It is important that the banks get back on track here. A failure to deliver on commitments or to provide the payment services that the community needs will inevitably lead to calls for further regulation.

4. Looking ahead

Looking beyond interchange and acquiring competition, new technologies open up the prospect of new payment options developing. Recently, there has been much discussion on the role that so-called ‘Big Tech’ firms might eventually play.

These firms have potential advantages over existing providers of payments services. In some cases, their technology and systems are more flexible, they have a greater ability to use and process information, they have well established networks which they can leverage and they are often better at interacting with their users and customers. Given this, one scenario is that these firms become significant players in the payments industry. They might be able to do this through developing new payment applications that provide a commercial return, not through charging for payment services, but by commercialising the value of the information that they obtain as a by-product of offering these services. If this scenario were to play out, it could significantly change the payments landscape, providing both merchants and consumers new payment options at low monetary cost. At the same time though it would raise a number of important issues related to data privacy, ownership and security.

The probability of Big Tech firms entering the payments arena is higher if merchants and consumers feel that the existing payment systems do not offer them the services they need and/or the prices that are being charged are too high. As I noted earlier, where banks have been slow to respond, other payment applications have emerged.

This scenario highlights a broader point. The way that people are charged for payments is complex and is changing: among other things, it is influenced by interchange fees, how the value of information is commercialised, and commercial pressures on banks. It is difficult to predict how things will ultimately play out, but these are issues the Payments System Board continues to keep a close eye on.

5. Summing Up

To conclude, I expect the shift to electronic payments will continue. The issues of functionality, security and reliability, and cost are central to the development of the system. The Payments System Board will be keeping a close eye on these issues.

While I have talked about a near cashless payments system, I want to emphasise that we don’t yet envisage a world without banknotes. The RBA is committed to providing cash consistent with demand by users and to support its distribution. Our development of the Next Generation Banknote series is a clear commitment to ensuring that cash continues to have public confidence and to meet the needs of the community.

The launch of the NPP this year was a big step forward for the industry and a credit to all of the staff at participating organisations who worked hard over the life of the project to bring it to fruition. As I mentioned, there are some key things that need to be done for the full benefits of the NPP to be available to end-users, but I am optimistic that these can be achieved and this new infrastructure can provide great functionality for Australia.

He makes the point that non-banks are picking up the investor slack, as reflected in the composition of the collateral underpinning RMBS. The high volume of RMBS issuance by non-banks is consistent with a sizeable increase in their mortgage lending.

More evidence that this sector of the market needs tighter controls?

Today I’ll provide an update on developments in the markets for housing and housing credit. These markets are closely related and both are of considerable interest to those that issue and those that invest in Australian residential mortgage-backed securities (RMBS).

Along the way, I’ll make use of data on residential mortgages from RMBS that are eligible for repurchase operations with the Reserve Bank.[1] Among other things, these data are a useful source of timely information on interest rates actually paid, loan by loan. As I’ll demonstrate, this allows us to infer something about shifts in the supply of, and demand for, housing credit, thereby shedding some light on the different forces driving these markets.

With this background in mind, I’ll also review some recent developments in the RMBS market. And I’ll finish by taking the opportunity to emphasise that RMBS issuers and investors should be prepared for any future changes in the use and availability of benchmark interest rates.

Interactions between the housing market and the market for housing credit

As highlighted recently in a speech by the Deputy Governor, the markets for housing and housing credit are going through a period of significant adjustment.[2] After years of strong growth, housing prices have been declining nationally, driven by falls in Melbourne and Sydney over the past year. Also, there has been a noticeable decline in investor credit growth and an easing in owner-occupier credit growth. The cycles in the growth of overall housing prices and investor credit have moved together quite closely over the past few years (Graph 1).

Graph 1

Underpinning these changes, there have been shifts in the demand for, and supply of housing, as well as in the demand for, and supply of, housing credit.

Credit supply affecting housing demand

The links between these two markets run in both directions, from housing credit to the housing market, and from the housing market to housing credit. Of late, the story more commonly told, though, is that a tightening in the supply of credit over recent years has impinged on the demand for housing.

This story is certainly the more apparent one in terms of its causes and effects. In particular, the measures implemented by regulators over recent years to address the risks associated with some forms of housing lending have worked to mitigate those risks and they have also led to a noticeable slowing of investor credit. This, in turn, has contributed to a decline in the demand for housing.

Again, these links have been discussed by Guy Debelle and are well-documented in the Bank’s latest Financial Stability Review (FSR).[3] In late 2014, the Australian Prudential Regulation Authority (APRA) set a benchmark for investor lending growth at each bank of no more than 10 per cent per annum (Graph 2).[4] Then in March 2017, APRA announced it would require interest-only loans – which are disproportionately used by investors – to be less than 30 per cent of each bank’s new lending. Over the same period, several other measures were implemented, including to tighten up the ways in which banks assessed the ability of borrowers to service their loans, and to limit the share of loans that constituted a large portion of the value of the property being purchased.

Graph 2

Banks responded to these requirements in two key ways. First, for some years now they have been tightening lending standards, thereby reducing the availability of credit to higher-risk borrowers. Second, banks raised interest rates for new and existing borrowers, first on investor loans from 2015, and then on interest-only loans in 2017 (Graph 3). In other words, the banks tightened the supply of credit, most notably for investors.

Graph 3

The FSR presents estimates of the effect of APRA’s first round of regulatory changes from late 2014. The key conclusions of that analysis are that, with the introduction of the 10 per cent investor credit growth benchmark:

the composition of new lending shifted away from investors and towards owner-occupiers, with little change in overall housing loan growth;

and housing prices have grown more slowly in regions with higher shares of investor-owned properties.

So, that’s the story that emphasises the effect of prudential measures on the supply of credit. And, in turn, the effect of tighter credit supply on the demand for housing.

I now want to draw your attention to the story less often told about the important causal link going in the other direction. In particular, the correction in the housing market over the past year or so appears to have been impinging on the demand for credit.

There are a number of reasons for the ongoing adjustment in housing prices:

the aforementioned reduction in the supply of credit;

the large increase in the supply of new housing associated with the high levels of housing construction in Brisbane, Melbourne and Sydney;

weaker demand from foreign buyers due to stricter enforcement of Chinese capital controls and various policy measures in Australia (many of which were implemented by various state governments) that have made it more costly for foreign residents to purchase and hold housing;

and last, but by no means least, the very substantial growth in housing prices over a long period, which had pushed housing prices to record levels as a share of household incomes and raised the prospects for a correction.

In support of this last point, I note that housing prices in Melbourne and Sydney (which had increased by 55 and 75 per cent respectively since 2012) are currently experiencing larger declines than in Brisbane (where housing prices had risen 20 per cent from 2012 to the recent peak; Graph 4).[5] It is also worth noting that housing prices are currently rising in Adelaide and Hobart. In addition, in Melbourne and Sydney house prices had run up further than apartment prices, and it is now house prices that have declined the most.[6]

Graph 4

While there may have been numerous causal factors, after a period of slowing housing price growth, more recently it is clear that housing prices are in decline in a number of major markets. This dynamic would have weighed heavily on the minds of buyers; particularly investors whose only motivation for buying is the return on the asset. An expectation of even a modest capital loss provides a strong incentive for them to delay buying a property, particularly in an environment of relatively low rental yields.

But how can we assess the role of factors affecting credit supply versus those affecting credit demand? Changes in the price of credit – that is, interest rates – can help. Other things equal, a fall in the supply of credit relative to demand can be expected to be associated with higher interest rates on housing loans. In contrast, a fall in the demand for credit (relative to supply) should be associated with a decline in interest rates. Just to be clear, I’m talking about the credit supply and demand curves shifting inwards. The former, by itself, reduces quantities while prices rise as the equilibrium shifts up along the demand curve. The latter, by itself, reduces quantities but decreases prices as the equilibrium shifts down along the supply curve.

So what’s happened to the interest rates borrowers are actually paying? The Securitisation Dataset provides estimates for both owner-occupiers and investors.

There has been a modest broad-based decline in outstanding mortgage rates in the Securitisation Dataset over the year to August (Graph 5). This suggests that banks were responding to weakness in credit demand by competing more vigorously to provide loans to high-quality borrowers. Indeed, looking just at new loans there is some evidence that average variable interest rates declined by more for investors than owner-occupiers, which is consistent with a noticeable decline in the demand for investor credit.

Graph 5

However, compositional changes might also explain why there was a slight decline in interest rates over this period. In particular, the tightening in lending standards has helped to shift the profile of loans away from higher-risk borrowers. This shift would have contributed to the decline in average interest rates paid as better quality borrowers tend to get loans at lower rates. However, it turns out that rates have declined over this period even within the set of low-risk borrowers – for example, those with low loan-to-valuation ratios (LVRs) (Graph 6). So the decline in average rates paid has been driven by factors other than just compositional changes.[7]

Graph 6

While banks began the process of tightening lending standards from around 2015, over the past year or so they have extended these efforts by applying greater rigour to their assessments of the ability of prospective borrowers to service loans. For example, banks have been assessing borrowers’ expenditures more thoroughly, which is likely to have contributed to reductions in the maximum loan sizes offered to borrowers.[8] Notwithstanding these changes, there are two other pieces of evidence that suggest that factors other than just a tightening in constraints on the supply-side have been affecting housing credit and housing market developments over the past year or so:

First, the majority of borrowers had earlier chosen to borrow much less than the maximum amounts offered by lenders. Hence, reductions in the sizes of maximum loans on offer over the past year does not imply one-for-one reduction in credit actually extended.[9]

Second, given that owner-occupiers have lower incomes on average than investors, they are likely to have faced noticeable reductions in maximum loan sizes as a result of the recent tightening in serviceability practices. However, owner-occupier credit growth has remained notably higher than investor credit growth.

In summary, weakness in credit demand – stemming from the dynamics in the housing market – has been a significant development over the past year or so. This is not to say that ongoing weakness of credit supply has not also been at work since then, but that credit supply is not the only part of the story.

Broader developments in the securitisation market

So far I have focused on the prudentially regulated banks. While the non-banks still only account for a modest share of outstanding mortgages, the sector has experienced very strong growth over recent years and is an important source of competition for the banks.

The RMBS market is a major source of funding for the non-bank providers of residential mortgages, and so RMBS issuance provides an indication of the recent growth in this sector. Last year, RMBS issuance was at its highest level since the global financial crisis. Non-banks’ issuance was in line with the high levels issued by this sector in the mid-2000s (Graph 7). In 2018, RMBS issuance in aggregate has been lower, but this has been largely been driven by decreased issuance by banks. Non-banks, by contrast, are continuing to issue close to $4 billion of RMBS per quarter.

Graph 7

This high volume of RMBS issuance by non-banks is consistent with a sizeable increase in their mortgage lending. This is an unsurprising consequence of the tighter supervision and regulation of mortgage lending by banks. This is not to say that non-banks are unregulated. They operate under a licensing regime managed by the Australian Securities and Investments Commission. And, as my colleague Michele Bullock mentioned recently, the members of the Council of Financial Regulators (which includes the Reserve Bank, APRA and ASIC) are monitoring the growth of the non-bank lenders for possible emerging financial stability risks.[10]

The Reserve Bank’s liaison indicates that non-banks have been lending to some borrowers who may otherwise have obtained credit from banks in the absence of the regulatory measures. Consistent with this, the Securitisation Dataset shows that a rising share of non-bank lending has been to investors. Indeed, there has been at least a five-percentage-point increase in the share of investor loans across all outstanding non-bank deals in the Securitisation Dataset over the past two-and-a-half years (Graph 8).[11] This is in contrast to the share of total bank loans to investors, which has been declining over that period.

Similarly, the share of non-bank loans that are on an interest-only basis has been stable over the past couple of years, whereas the share of bank loans that are interest-only has declined significantly over the same period.

Graph 8

The increase in the share of investor housing in deals issued by non-banks is one of the few noticeable changes in the composition of the collateral underpinning RMBS in the past couple of years. Indeed, for deals by non-banks the share of loans with riskier characteristics such as high LVRs or self-employed borrowers has been little changed.

One of the other changes to loan pools in new deals is a fall in seasoning (i.e. the age of loans when the deal is launched). This has been most pronounced for non-banks (Graph 9). It is consistent with non-banks writing a lot more loans. Hence, warehouses of their loans are reaching desired issuance sizes more quickly.

Graph 9

Despite the pull-back in RMBS issuance by the major banks over recent years, the broader stock of asset-backed securities (ABS) on issue increased by around $20 billion over the past 18 months, after remaining broadly stable for the previous 5 years (Graph 10; in addition to RMBS, ABS cover other assets such as car loans and credit card receivables). Demand for these additional asset-backed securities has been driven by non-residents.

Graph 10

As well as a shift in the composition of investors in ABS, we have observed some changes in deal structures over recent years. Of particular note, the average number of tranches per deal has increased from around four to eight (Graph 11). The increase has been broad-based across different types of issuers. This general trend covers deals with a greater number of tranches with differing levels of subordination, as well as deals where the top tranche is split into a number of individual tranches with different characteristics but equal subordination.

Graph 11

We have also seen what might be termed greater ‘specialisation’ of individual tranches. For instance, in recent years the use of one or more tranches with less common features – such as foreign currency, short term or green features – has increased.[12] This increased specialisation is consistent with issuers addressing the needs of different types of investors.

All of these developments point to the evolution of the Australian securitisation market over the past few years, with non-bank issuers playing an increasingly important role and non-resident investors taking an increasing share of issuance.

Benchmark interest rates, RMBS pricing and funding costs

The increase in bank bill swap (BBSW) rates in early 2018 has led to a modest rise in the funding costs of both banks and non-banks.[13] However, the increase in overall funding costs has been a bit greater for non-bank issuers than for banks. This is because banks have a sizeable proportion of their liabilities – such as retail deposits – that do not reprice in line with BBSW rates. Also, the bulk of non-banks’ loans are funded via RMBS issuance, and the cost of issuance has risen by a bit more than BBSW rates (Graph 12). The premium over the BBSW benchmark rate has risen to the level of two years ago. At the margin, these changes mean that non-bank issuers are not able to compete as aggressively on price for new borrowers as banks than was the case a year ago.

Graph 12

Most lenders have passed through modest increases in their funding costs to borrowers over the past few months. Despite these increases, competition for new loans remains strong, and interest rates for new loans are still well below outstanding rates. So credit supply is available to good quality borrowers on good terms and there is a strong financial incentive to shop around.

Interest Rate Benchmarks for the Securitisation Market

One final point I’d like to make on pricing, is that RMBS issuers and investors should be considering the implications of developments in interest rate benchmarks. In light of the issues around benchmarks such as LIBOR (the London Inter-Bank Offered Rate), substantial efforts have been made to reform these benchmarks to support the smooth functioning of the financial system.

BBSW rates are important Australian dollar interest rate benchmarks, and the 1-month BBSW rate is frequently used in the securitisation market. We have worked closely with the ASX and market participants to ensure that BBSW rates are anchored as much as possible to transactions in the underlying bank bill market. However, the most robust tenors are 6-month and 3-month BBSW, which are the points at which banks frequently issue bills to investors. In contrast, the liquidity of the 1-month BBSW market is lower than it once was. This is mainly due to the introduction of liquidity standards that reduced the incentive for banks to issue very short-term paper.

Given this, RMBS issuers should consider using alternative benchmarks.[14] One option would be to reference 3- or 6-month BBSW rates for new RMBS issues. Another option is the cash rate, which is the (near) risk-free benchmark published by the Reserve Bank.[15] Given the underlying exposure in RMBS is to mortgages rather than banks, it could make more sense to price these securities at a spread to the cash rate rather than to BBSW rates, which incorporate bank credit risk.

Issuers and investors globally, including in Australia, should also be prepared for a scenario where a benchmark they are using ceases to be published. In such an event, users would have to rely on the fall-back provisions in their contracts. However, for many products – including RMBS – the existing fall-back provisions would be cumbersome to apply and could generate significant market disruption. This is most urgent for market participants using LIBOR, since the regulators are only supporting LIBOR until the end of 2021. While we expect that BBSW will remain a robust benchmark, it is prudent for users of BBSW to also have robust fall-backs in place. The International Swaps and Derivatives Association (ISDA) recently conducted a consultation on how to make contracts more robust. We would expect Australian market participants to adopt more robust fall-backs in their contracts following this process.

Conclusion

As the housing market undergoes a period of adjustment, it is useful to have an understanding of some of the drivers at play. Much attention has been given to the effect of prudential measures in dampening the supply of credit and how this has affected the housing market. However, it is also important to acknowledge causation going in the other direction, whereby the softer housing market has led to weakness in credit demand. My assessment is that the slowing in housing credit growth over the past year or so is due to both a tightening in the supply of credit and weaker demand for credit. Within that environment, lenders are competing vigorously for high-quality borrowers.

Developments in the RMBS market are consistent with non-bank lenders providing an extra source of supply. While non-banks remain small as a share of total housing lending, developments over the past couple of years show that the sector continues to evolve. The recent increase in issuance spreads may provide some slight headwinds for the sector; however, spreads remain below their levels in early 2016.

Finally, I would urge both issuers and investors to be responsive to the forces affecting benchmarks used to price RBMS and to focus on preparing for the use of alternative benchmarks.

In our latest discussion on Australia’s missing Gold John Adams and I discuss the latest comments from the RBA on our gold, and a range of broader economic questions. Is the RBA myopic?

Members commenced their discussion of the global economy by noting that growth in Australia’s major trading partners had been robust in 2018. Growth was expected to ease a little over the subsequent two years, but to remain above potential in 2019. Although there had been little change to the Bank’s outlook for trading partner growth over recent months, the latest forecasts had incorporated a small negative effect from recent tariff changes on growth in a number of economies, including the United States and some east Asian economies. Members discussed the risks to the global outlook from a further escalation in trade tensions and considered the implications for the Australian economy of a scenario in which wages and inflation in the United States pick up by more than expected, given the strength of the US economy.

Growth in the major advanced economies had remained above potential in 2018. Growth in the United States had been strong, supported by the sizeable fiscal stimulus. While US manufacturers had raised concerns about the effects of rising input costs and their competitiveness, business investment intentions had remained strong. Unemployment rates had declined further in the major advanced economies and wages growth had picked up. In the United States, the increase in wages growth had been boosted by workers changing jobs, but recently workers had also been receiving higher wage increases without changing employers. Members observed that inflation in the major advanced economies had increased as a result of higher oil prices and wages growth. However, core inflation had remained low and little changed in some advanced economies, notably Japan and the euro area, but was close to target in others, including the United States.

Growth in China had moderated a little further in the September quarter, following the tightening of financial conditions in late 2017 and early 2018. Although activity in the Chinese services sector had been resilient, conditions had remained weak in the industrial sector and public investment had declined. In response, the Chinese authorities had implemented targeted monetary and fiscal policies to support growth, while maintaining their commitment to containing risks in the financial system. The adverse effect on the Chinese economy from higher tariffs was likely to have been partly offset by policy measures that had been introduced to support affected trading firms. The depreciation of the renminbi over 2018 had also provided support to the economy overall. Elsewhere in Asia, indicators suggested that growth had eased a little recently. The fact that this easing had been most pronounced in growth in exports and industrial production suggested it may have been affected by US–China trade tensions, given the integration of east Asian economies in global manufacturing supply chains.

Commodity prices, in particular those for bulk commodities, had held up by more than had been expected over the previous year. In part, this reflected a number of unforeseen disruptions to supply, particularly for coking coal. Members noted that, in addition, global steel demand had been stronger than anticipated. Oil prices had also risen, which had increased Australia’s terms of trade. Although Australia is a net importer of oil, Australian exports of liquefied natural gas (LNG) and other oil-related products – the prices of which are linked to oil prices – are larger, following a sustained period of strong growth. Along with a higher starting point as a result of commodity prices having held up, the forecast for Australia’s terms of trade had been revised higher for the next few years owing to a reassessment of the expected strength in global demand for commodities, particularly from China and India.

Domestic Economic Conditions

Members noted that the recent run of economic data suggested that growth in the Australian economy had been higher over the year to the June quarter than earlier forecast, and above estimates of potential growth. Labour market conditions had remained strong and other available indicators pointed to further solid GDP growth in the September quarter. At the same time, inflation in the September quarter had slowed as expected, partly as a result of a large policy-induced decline in childcare prices.

GDP growth was expected to be around 3½ per cent on average over 2018 and 2019. Members noted that growth would be supported by accommodative monetary policy, above-trend growth in Australia’s major trading partners and a stronger profile for the terms of trade. Year-ended GDP growth was expected to ease to around 3 per cent towards the end of 2020 because LNG exports were expected to reach capacity production levels by the end of 2019.

Consumption had continued to grow by around 3 per cent in year-ended terms, despite ongoing low growth in household income. Growth in retail sales had been volatile on a quarterly basis, although in year-ended terms growth had been fairly steady at a relatively modest rate. Conditions had continued to differ across states; retail sales had been relatively strong in Victoria but had declined in Western Australia. Members noted that the strong pace of growth in retail spending online in recent years could be one factor contributing to subdued conditions in retail rental markets. Year-ended growth in household consumption was expected to remain around 3 per cent over the following few years. Growth in household disposable income was forecast to increase to a similar rate.

Although residential building approvals had fallen in the September quarter and liaison indicated that pre-sales had become harder to obtain, the large pipeline of work yet to be done was expected to support dwelling investment at a high level over the following year or two. Members noted that population growth was expected to remain fairly strong over the following few years, and that this would provide some support to housing demand. However, there had been reports that bank financing of large development projects had become more difficult, particularly in areas where there had already been substantial development.

Members noted that established housing prices had fallen further in Sydney and Melbourne. After rising by more than apartment prices in preceding years, house prices had fallen by more than apartment prices since 2017. Conditions in the established housing market had been stable in most other cities, although housing prices had declined a little further in Perth in recent months. Rental vacancies had increased in Sydney, consistent with the additions to the stock of housing over the past year, and rent inflation had remained low across the country.

Members observed that business investment had been stronger than forecast a year earlier. The recent strength in non-mining business investment was expected to continue and to make a significant contribution to output growth over the forecast period. Private non-residential construction was expected to be supported by above-average business conditions and the significant pipeline of non-residential construction work that had been approved. Expenditure on machinery and equipment was also expected to rise over the forecast period. Members noted that mining investment had not fallen by as much as expected over the previous year, largely reflecting additional spending on the remaining LNG projects under construction. The trough in mining investment was still expected to occur in late 2018 or early 2019.

Exports had continued to make a significant contribution to growth in output over the preceding year. Resource exports had increased further, mainly because production of LNG had continued to ramp up. Service and manufacturing exports had been supported by strong global growth and the depreciation of the Australian dollar over 2018. The persistent drought conditions in New South Wales and bordering regions in Queensland and Victoria had led to a short-term boost to rural exports because livestock slaughter rates had increased and some grain crops had been harvested early to take advantage of higher feed prices. However, the medium-term outlook for farm sector production had been revised lower.

Labour market conditions had been stronger than expected. Members noted that much of the employment growth had been in full-time employment and that the participation rate had remained at a high level. The unemployment rate had declined to 5 per cent in September. Unemployment rates in most states had trended lower in recent months and were particularly low in New South Wales and Victoria. The unemployment rate was now expected to decline gradually to around 4¾ per cent by mid 2020, although members noted that some leading indicators of labour demand suggested there could be a more pronounced decline in the unemployment rate in the near term.

The improved labour market outlook had led to a modest upward revision to the outlook for wages growth. The recent increases in award and minimum wages were expected to have provided a small boost to wages growth in the September quarter. Members discussed the wage increases associated with recent enterprise bargaining agreements and uncertainties around the extent to which these and ongoing negotiations might flow through to overall wages growth. Members noted that average real earnings had not increased for six years and that wages growth was a key uncertainty for both future consumption growth and inflation.

Year-ended inflation had remained low in the September quarter. CPI inflation was 1.9 per cent over the year to the September quarter and had been around 2 per cent since early 2017. Underlying inflation was a little below ½ per cent in the September quarter and around 1¾ per cent over the year. As expected, the quarterly outcome incorporated a large decline in administered prices, reflecting a sharp decline in childcare prices owing to changes in government subsidies and a moderation in utilities inflation. The noticeable step-down in administered price inflation from earlier years was expected to be temporary, although members noted that future outcomes depended on possible government initiatives to reduce cost-of-living pressures. Inflation in the cost of new housing and rents had also been subdued in the September quarter. Inflation was still forecast to increase gradually over time as spare capacity in the economy declines. The brighter outlook for economic activity and the labour market, compared with three months earlier, had led to a small upward revision to the inflation forecasts.

Financial Markets

Members commenced their discussion of financial market developments by noting that financial conditions in the advanced economies remained accommodative, although they had tightened somewhat recently.

In October, equity prices had declined sharply across the major markets. Analysts had attributed the fall to a range of factors, including higher bond yields, concerns that the pace of earnings growth would decline given trade tensions and building cost pressures, and elevated valuations (particularly in the United States). Members noted, however, that recent corporate earnings, especially in the United States, had grown strongly and had mostly been above forecasts.

Members observed that there had generally been little spillover from equity markets to other financial markets. Money market and corporate bond spreads had increased a little but remained relatively low. Term premia for sovereign debt and exchange rate volatility also remained low in the major markets. Members noted that the leveraged loan market had grown rapidly, particularly in the United States, and corporate funding had increasingly shifted to the securities markets rather than bank finance.

Monetary policy in the major economies remained accommodative. Members noted that financial market pricing continued to imply that policy settings of central banks are on divergent paths, reflecting differences in spare capacity and/or the inflation outlook across economies. In the United States and Canada, markets were pricing in a further tightening in monetary policy over the coming year. Financial market pricing continued to imply a lower path for the US federal funds rate than suggested by the median projection of Federal Open Market Committee members. Market pricing implied a smaller increase in policy rates over the coming year in the United Kingdom, Norway and Sweden, with rates expected to remain very low in these economies. By contrast, market pricing was consistent with policy rates remaining steady over the following year in Australia and New Zealand, where policy rates had not been lowered to the extent they had in some other economies. In Japan, the euro area and Switzerland, market pricing remained consistent with maintenance of the highly accommodative monetary policy settings in these economies.

Members observed that the divergent monetary policy paths had been reflected in long-term government bond yields, which had increased in the United States and Canada over the prior year, but had been broadly unchanged in other major markets and Australia. Members noted that long-term government bond yields in Australia were now clearly below those in the United States as a result. Members also noted that long-term government bond yields remained low by historical standards in the major markets, with inflation expectations contained and term premia particularly low.

In Italy, the spread of Italian government bond yields over German Bunds had risen further in October, following the rejection by the European Commission of the Italian Government’s draft budget. However, Italian yield spreads remained below the levels seen during the European debt crisis in 2012 and there had been limited spillovers to other European bond markets. Nevertheless, ongoing concerns about Italian fiscal policy settings were likely to remain a focus for financial market participants.

Financial conditions in emerging markets had stabilised recently, as earlier political and macro-financial concerns in Turkey, Argentina and Brazil had eased somewhat. After depreciating sharply since the beginning of 2018, these economies’ exchange rates had appreciated over the preceding couple of months. This followed some corrective policy responses and an easing in perceived political risk. Exchange rate volatility had also declined from its recent peak across emerging market economies more broadly. However, members noted that there remained a risk that capital outflows from emerging markets could broaden and intensify, prompting a more significant tightening of financial conditions.

In China, the authorities had implemented further targeted measures to ease financial conditions in response to slower growth, while balancing their commitment to containing risks in the financial system. In October, banks’ reserve requirement ratios were cut by another 1 percentage point, following earlier measures to ensure ample bank liquidity. The decline in Chinese share prices over 2018 had also recently prompted the authorities to announce measures to support the equity market. The renminbi exchange rate had depreciated over 2018 in response to concerns about trade protection and the outlook for growth, as well as the policy measures targeted at easing financial conditions. However, unlike the 2015 depreciation episode, there had been few signs of large-scale capital outflows or direct foreign exchange intervention by the authorities.

The Australian dollar had depreciated a little over the course of 2018, but remained in the fairly narrow range observed over recent years on a trade-weighted basis. Members observed that this had reflected offsetting effects on the exchange rate from higher commodity prices, on the one hand, and the decline in Australian bond yields relative to those in other major markets, on the other hand.

Members noted that Australian banks’ funding costs remained a little higher than in 2017, reflecting the increase in short-term money market rates over the first half of 2018. More recently, the spread of bank bill swap rates relative to overnight indexed swaps (OIS) had declined marginally over the preceding month, while the spread of US LIBOR to OIS had increased. Information from liaison suggested that there had been little change in domestic money market conditions in recent months. The modest increase in funding costs earlier in the year had been passed on by most lenders to existing borrowers with variable-rate business and housing loans.

The pace of overall credit growth had been maintained in recent months, as slowing housing credit growth had been offset by a pick-up in business credit growth. The easing in growth in housing credit had reflected a slowing in growth in lending by the major banks. By contrast, growth in housing lending by other authorised deposit-taking institutions (ADIs) had picked up. Housing lending by non-ADIs had continued to grow strongly, although these institutions’ share of total housing credit remained small. Members noted that the easing in housing credit growth had been accounted for largely by slower growth in credit extended to investors, which was now close to zero. Growth in lending to owner-occupiers had eased more gradually and remained around 6½ per cent in six-month-ended annualised terms.

Members noted that the easing in housing credit growth was likely to reflect both tighter lending conditions and some weakening in demand. Stricter lending criteria had reduced maximum loan amounts. At the same time, however, interest rates offered on new loans remained lower than interest rates on outstanding loans, consistent with banks continuing to compete for new borrowers.

Financial market pricing implied that the cash rate was expected to remain unchanged for a considerable period.

Considerations for Monetary Policy

As part of a regular annual review process, members considered how the domestic economy had evolved over the preceding year relative to the Bank’s forecasts of a year earlier. Members noted that the magnitude of forecast errors for key variables, including GDP growth, the unemployment rate and inflation, had been smaller than the historical averages. Overall, GDP growth had been higher than expected at the time of the November 2017 Statement on Monetary Policy. While most components of GDP had turned out to be a little stronger than expected, the main source of the upward surprise had been business investment, owing to unexpected strength in both mining and non-mining investment. In addition, the terms of trade had been higher than expected over the previous year and the Australian dollar had depreciated. Consistent with these developments, labour market outcomes had also been stronger than expected a year earlier and more progress had been made in reducing unemployment than expected. Despite this, wages growth and underlying inflation had evolved largely as expected. Overall, members noted that the economic outcomes over the preceding year had been consistent with the economy continuing on its forecast trajectory of gradually declining spare capacity, with a correspondingly gradual increase in wages growth and inflation.

In the context of the annual review of the forecasts, members also reviewed arguments that had been advanced by various commentators during the preceding year for an increase or decrease in the cash rate. Some of these arguments relied on different assessments than had been made by the Board in relation to the benefits of seeking faster progress on the Bank’s inflation and unemployment rate objectives, versus the risks to longer-term sustainable growth from further increases in household debt. Other arguments for a change in the cash rate relied on an alternative assessment about the economic outlook and/or the risks around the outlook. Arguments in favour of an increase in the cash rate included that the economy had more momentum than assessed by the Bank; financial stability risks from high levels of household debt required higher interest rates; and a higher cash rate would create room to cut the cash rate in future in response to an adverse event. The prime argument in favour of a decrease in the cash rate was that easier monetary policy could lead to faster progress in achieving the Bank’s monetary policy objectives.

Members discussed how different scenarios could affect the monetary policy decision, noting that the appropriate policy response would depend on the specifics of the situation, including the underlying factors driving economic developments. For example, in the event of a marked change in the strength of the global economy, the effect on the Australian economy – and thus the appropriate monetary policy response – would depend on any associated move in the exchange rate of the Australian dollar. Members also discussed various scenarios related to the labour market and household expenditure.

Turning to the current month’s decision, members noted that the global economy had continued to grow strongly and global financial conditions remained accommodative, although conditions had tightened somewhat recently. Most advanced economies were growing at above-trend rates and their labour markets had continued to tighten. This had led to a noticeable pick-up in wages growth. In some economies, most notably the United States, inflationary pressures were building. Growth in China had slowed a little and the authorities had responded to weakness in some sectors of the economy with targeted policy measures, while continuing to pay close attention to risks in the financial sector. Members noted that the direction of international trade policy continued to be a significant risk to the global outlook.

Against the background of rising global inflationary pressures, a few central banks, including the US Federal Reserve, were expected to continue to reduce the degree of monetary policy accommodation gradually. Changes in the expected paths of monetary policy over the preceding year had been reflected in changes to financial market pricing, most notably a broad-based appreciation of the US dollar. The associated modest depreciation of the Australian dollar over 2018 was likely to have been helpful for domestic economic growth.

Members noted that economic conditions in the Australian economy had continued to improve and had been a little stronger than expected. The outlook for growth had been revised a little higher, mainly as a result of upward revisions to history and recent strong data. Year-ended GDP growth was expected to remain above 3 per cent over 2019, before slowing to around 3 per cent in 2020. Members observed that the outlook for consumption continued to be a source of uncertainty in an environment of slow growth in household incomes, high debt levels and easing conditions in housing markets in some parts of the country. These conditions warranted close monitoring. At the same time, investment had been stronger than expected over the previous year and business conditions were positive; if the recent momentum were to be sustained, business investment could turn out to be stronger than currently expected. However, the drought had led to difficult conditions in parts of the farm sector.

Conditions in the labour market had also been stronger than expected and forward-looking indicators of labour demand continued to point to ongoing strength in the near term. As a result, the forecast for the unemployment rate had been revised lower and the forecast for wages growth had been revised slightly higher. Members noted that there continued to be uncertainty about the degree of spare capacity in the labour market and the extent and speed of any pick-up in wages growth relative to the gradual increase incorporated in the latest forecasts. They acknowledged that a gradual increase in wages growth was likely to be necessary for inflation to be sustainably within the target range.

Underlying inflation had remained low and stable at around 1¾ per cent, consistent with the previous forecasts, despite stronger-than-expected economic activity. Although there was a possibility of further declines in administered prices in the year ahead, underlying inflation was expected to pick up gradually over the forecast period, to be a little above 2¼ per cent in 2020.

Conditions in the Sydney and Melbourne housing markets had continued to ease, following significant growth over preceding years. Rent inflation had remained low. Housing credit growth had declined, particularly for investors, but had continued to be higher than growth in household income. Credit conditions were tighter than they had been for some time, partly because lending standards had been tightened following the introduction of supervisory measures to help contain the build-up of risk in household balance sheets. At the same time, home lending rates had remained low and there was strong competition for borrowers of high credit quality.

Taking account of the available information on current economic and financial conditions, as well as the latest forecasts, members assessed that the current stance of monetary policy would continue to support economic growth and allow for further gradual progress to be made in reducing the unemployment rate and returning inflation towards the midpoint of the target. In these circumstances, members continued to agree that the next move in the cash rate was more likely to be an increase than a decrease, but that there was no strong case for a near-term adjustment in monetary policy. Rather, members assessed that it would be appropriate to hold the cash rate steady and for the Bank to be a source of stability and confidence while this progress unfolds. Members judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

The Decision

The Board decided to leave the cash rate unchanged at 1.5 per cent.

RBA Deputy Governor Guy Debelle summarised the Bank’s assessment of the various measures put in place to address the risks around housing lending. He argues risks are under control, though external shocks could still hit household balance sheets. Loose ending is not seen as a risk…. Hmmmm! Whilst the regulatory measures have significantly reduced the riskiness of new housing lending, we have masses of loans written under weaker regulation, which are exposed.

The motivation for implementing these various measures was to address the mounting risk to household balance sheets arising from the rapid growth of certain forms of lending, in particular lending to investors and interest-only (IO) lending. The strong growth in investor borrowing was increasing the risk that investor activity could be excessively boosting housing prices and construction and so increasing the probability of a subsequent sharp unwinding. This risk is greater for investor borrowing than owner-occupiers as investors can behave pro-cyclically, withdrawing from the market as it declines. The rise in the prevalence of interest-only borrowing for both investors and owner-occupiers increased the overall risk profile of household borrowing. No principal is repaid during the IO period, and the increase in required repayments can be large when the IO period expires.

I don’t see the riskiness of the borrowing as being the source of the negative shock. My concern is for its potential to be an accelerator to a negative shock from another source. To put it another way, I don’t regard it as likely that household borrowing will collapse under its own weight. Rather, if a negative shock were to hit the Australian economy, particularly one that caused a sizeable rise in unemployment, then the risk on the household balance sheet would magnify the adverse effect of that shock. This would have first order consequences for the economy and hence also for monetary policy.

To repeat the conclusion of the assessment in the FSR: the measures have helped to reduce the riskiness of new borrowing. In turn, this has stemmed the increase in household sector vulnerabilities and improved the resilience of the economy to future shocks. The measures have led to a slowing in credit growth but there is little evidence to suggest that the measures have excessively constrained aggregate credit supply. Housing credit growth has slowed, but it is still running at 5 per cent.

The various measures implemented to address the riskiness of housing lending fall into three categories:[1]

Lending standards or serviceability criteria. This includes tightening up the assessment and verification of borrower income and expenses, the discouragement of high loan-to-valuation ratio (LVR) loans and ensuring that minimum interest rate buffers were being applied, including on existing loans.

Investor lending growth benchmark. A 10 per cent cap on investor lending growth was introduced in December 2014.

A cap on the share of interest-only loans in new lending of no more than 30 per cent.

These measures were introduced progressively over a number of years. The scrutiny on serviceability by both APRA and ASIC has been underway for over four years now. For example, in September 2015, APRA noted that by then, serviceability practices had been tightened, such as the haircutting of various forms of income, including rental income. At the same time, APRA reported that minimum interest rate buffers and floors were also being more consistently applied.

This means that these tighter lending standards have been in place for a while now. They are not a recent phenomenon. But this also makes assessing the overall impact difficult in some cases, though the effect of some of the measures has been obvious. There clearly has also been an interaction between them.

What Has Been the Effect of These Various Measures?

Different interest rates are now charged across the various types of mortgages. Interest rates are higher on investor lending and interest-only lending than they are on owner-occupier lending (Graph 1). Previously there was little, if any, variation in the interest rate charged on different types of loans, beyond the size of the discount that varied with borrower income and the size of the loan.

Graph 1