RBA Assistant Governor (Economic) Luci Ellis spoke about the role of infrastructure from the perspective of someone involved in macroeconomic policy: the policy challenges and opportunities, the work of the G20 and role of infrastructure as not just an engine of growth but, more importantly, an enabler of growth.

What Is Infrastructure?

Before getting into that, it’s useful to define what we are talking about. When macroeconomists think about infrastructure, we think about the capital goods that provide public services. They are shared facilities that help economies function well. These include the structures – that is, the things produced by the construction industry that, unlike buildings, don’t have roofs. But there are also many other shared facilities that promote a well-functioning economy and society. One example of those other important pieces of infrastructure is the New Payments Platform that was launched recently. There are also important social infrastructures such as our legal system, or our frameworks for safeguarding children. But for the purposes of my talk, I will focus on the things that are tangible.

Within this class of tangible physical infrastructure, we can think of various kinds of physical assets. There is transport infrastructure, utilities providing electricity, gas and water, and communications infrastructure. Within each of these groups there are ‘hubs’ or centres, such as airports and railway stations for transport, power stations and reservoirs providing utilities, or telephone exchanges and satellites facilitating communication. Also within each group are ‘paths’ or distribution networks, such as the road and rail networks, power lines and telecommunications networks.

As you all well know, infrastructure of this kind can be provided by either the private or public sectors. The public sector might be involved for a number of reasons. One is that it is generally accepted that there are social benefits to providing these kinds of assets that are not fully captured by a profit-making provider. Without some provision by the state, such infrastructure will be under-provided. Another is the network nature of these facilities. Where there is a network, there is an element of monopoly power, and thus often a role for state regulation if not actually state ownership. At the very least, someone needs to set the rules of the game, whether that is the side of the road we drive on or the protocols used in telecommunications.

Despite the role of the state in the provision and management of these types of infrastructure, they are not ‘public goods’ in the textbook sense. Textbook public goods are non-rival and non-excludable: their benefits aren’t diminished by an extra person enjoying them and, in any case, you can’t prevent people from having those benefits. Clean air and a defence force fall into this category. By contrast, physical infrastructure can clearly suffer from congestion. It is also conceptually possible to exclude free riders from the use of the infrastructure, though this is more easily achieved in some cases than others. It is from these characteristics – congestion, excludability and the underlying monopoly network – that most of the policy challenges around infrastructure arise.

What Policy Challenges Does Infrastructure Pose?

Much like any business decision faced by private firms, decisions about infrastructure involve a lot of uncertainty. Businesses grapple with these questions every day. Should we build it? Is the market big enough? Where should we build it? What design and methods should we use? What price should we set?

It is tempting to think that physical infrastructure is no different. Many of the questions are the same. But there are differences, and the policy challenges around infrastructure stem from that. Firstly, infrastructure can be very long-lived, which compounds the uncertainty about future usage rates and congestion. Secondly, the network element of the infrastructure makes it especially difficult to forecast market size. Thirdly, the social benefits that spill over to the broader economy are harder to quantify than a forecast revenue stream.

All countries face the same challenges of providing enough infrastructure in the right places to serve the needs of their populations. So it is no surprise that infrastructure has been a recurring topic in the deliberations and work of the G20 group of major economies. Australia elevated the topic further during its presidency year in 2014. This year, the Argentine presidency has also included it as one of its key priorities and has re-convened the G20 Infrastructure Working Group, which met in Sydney earlier this month.

One typical challenge is risk management. Infrastructure risk takes many forms. There’s the risk that the project is not built efficiently, that investors are unwilling, that demand is too high – leading to congestion – or not high enough. There are risks that revenue can’t be collected as intended. There are risks that the construction isn’t resilient to natural disasters or just ordinary wear and tear.

Another typical challenge is financing. Most infrastructure assets cost a lot upfront to build, and their monetary return – if any – is only realised over a long period. This can still be an attractive payoff structure for private investors, depending on how the project is structured. Ensuring private sector participation in infrastructure finance has therefore been a priority of the G20.

A common thread in these challenges is that the nature of the risks and funding issues are very different in the ‘build phase’ than in the ‘run phase’, once the infrastructure is being used. This is true of any large construction project and, similarly, one solution can be to have different actors involved in the two stages.

What Policies Might Lessen These Challenges?

The good news is that, if we face common challenges, the solutions are also likely to be common. We can learn from each other. So there is value in sharing information about best practice across countries. For example, during Australia’s G20 presidency in 2014, a Global Infrastructure Hub (GI Hub) was announced, with an aim of, among other things, sharing guidance on best practices. If you think about it, the principles for designing a good road network or locating a railway line don’t really change according to where you live. There will be differences relating to legal frameworks or other national specifics, but most of what constitutes best practice will be universal.

To lessen the financing challenge, G20 authorities have been focusing on initiatives that can make infrastructure an attractive asset class. There is plenty of private sector financing looking for the stable long-term cash flows that certain kinds of infrastructure assets can provide, once they are built. The question is how to bring that financing to the projects that need it, especially in emerging market economies where the need seems to be greatest. Different countries have approached this topic differently (Chong and Poole 2013). The report ‘Roadmap to infrastructure as an asset class’, which G20 Finance Ministers and Governors endorsed in March, proposed several initiatives that should help, including to:

enhance project preparation so that projects are more ‘bankable’

align the risk of projects to the risk profile of investors

increase the data available on projects

promote quality infrastructure and good governance

improve local currency capital markets in emerging markets

explore the creation of standardised contracts for activities such as financing and risk sharing.

Some of these initiatives can work as collaborative efforts with the private sector. Others, such as aligning risks, may require more effective use of credit enhancement from the public sector or from supranational agencies, such as the multilateral development banks (MDBs). This is seen as a way of ‘crowding in’ private finance rather than have the MDBs fund the project themselves.

Here’s where the Australian experience might be instructive. As a central banker, I can look around the world and see that most countries have settled on the idea of having a specialist, independent agency to carry out the kinds of responsibilities that central banks usually have, such as setting monetary policy or running the payments system. The same is true for many kinds of financial regulation. It is less common to have an autonomous agency involved in analysing and assessing microeconomic policy. But in Australia, we do have something like that in the Productivity Commission. And similarly we have an independent statutory authority for assessing and prioritising infrastructure projects, Infrastructure Australia.

As a non-specialist it is not possible for me to quantify what difference this makes. But if common frameworks and rigorous, pre-emptive analysis help – and I believe they do – then Australia’s experience will surely be instructive for other economies wanting to improve their infrastructure.

What Is the Current State of Play in Australia?

In comparison to some countries, international research suggests that Australia is fairly well served by its current infrastructure.[4] But with a strongly growing population, we face a challenge of ensuring that the stock of infrastructure keeps pace with expanding needs. Utilities such as electricity and water, as well as transport links, need ongoing investment to accommodate a rising population.

This challenge has clearly been recognised and, over recent years, governments at both the state and federal level have been increasing infrastructure investment. As can be seen from this graph, public investment in communications infrastructure has increased with the rollout of the NBN. Transport infrastructure – road and rail – has increased even more sharply and is back close to the share of GDP it represented in the years immediately after the global financial crisis.

Graph 1

The recent federal budget foreshadowed additional infrastructure spending. More broadly, investment by the federal government is projected to increase over coming years. Most of the infrastructure spend is by state governments, however. This has already increased noticeably, particularly in the south-eastern states, and according to state budgets it is projected to increase further in the next couple of years. Much of this work is in urban transport projects, both road and rail.

Graph 2

Another area of infrastructure attracting substantial investment at the moment is renewable energy. The value of renewable generation projects slated for the next year or so is similar to the average of recent years’ total investment in electricity generation, distribution and transmission, a much broader set of activities. Most of the investment in renewables is by the private sector. These projects have become more attractive lately as the cost of the underlying technology has fallen. At the same time, the costs of fossil-based inputs to existing generation methods has risen, and so has the price of electricity. So renewable energy projects are becoming increasingly commercially viable. As such, it is an area where the private sector can provide the infrastructure.

And that is indeed what we are seeing. A range of data sources on both capital expenditure and financing show greatly increased activity recently (Graph 3). A few years ago, much of the investment in renewables was in small-scale rooftop solar. More recently, as the economics of these projects has changed, we are seeing more large-scale solar and wind projects being financed and built.

Graph 3

As I mentioned earlier, the risks and challenges of the build phase are very different from those in the run phase. There will be some areas, like renewables, where the private sector will be involved in both phases. In others, the execution and governance risks in the build phase don’t match investors’ desired risk profiles, but the revenue from the operation phase can do so. These kinds of projects will be good candidates for private ownership once construction is complete; some state governments are recycling the revenue from those sales to fund new infrastructure. And finally, there are projects where the social benefits are not easily captured as cash flow. It is important that these kinds of projects are not under-provided, just because they would not be profitable for the private sector to run.

Regardless of the exact approach to funding and management of construction, infrastructure investment can involve significant spillover benefits to the rest of the economy. The Bank has discussed these recently, and they bear repeating (RBA 2018). The direct spillovers derive from the incomes earned by the workers and firms doing the work; most of these projects are built by the private sector on behalf of the public sector. This income gets spent or invested, which in turn generates income for someone else and so on. At a time such as now, when there is still spare capacity in the economy, this ‘fiscal multiplier’ can result in overall demand rising by considerably more than the original spend on the project.

More broadly, and over a longer horizon, the economy benefits from a larger capital stock and the productivity benefits of infrastructure of this type. These are often hard to quantify even after the fact, but some examples might include: new export businesses enabled by the construction or expansion of an airport; higher productivity of logistics firms if their vehicles spend less time in traffic; and better health outcomes from reduced accident rates when roads are made safer.

It is these benefits that are worth focusing on, more than the raw contribution of the building work to GDP growth. As I’ve emphasised on an earlier occasion, it isn’t helpful to think of infrastructure as a new ‘engine of growth’, receiving the handover from the mining investment boom and, later, the apartment building boom (Ellis 2017). By its nature, infrastructure is justified by its contribution to the public good. It is not so much an engine of growth as an enabler of growth. But for this to be true, projects need to be rigorously assessed, carefully designed and appropriately timed. And for that to be possible, it helps if practitioners can learn from each other, for example through forums such as this one and, internationally, the initiatives of the G20.

RBA Governor Philip Lowe discussed the state of the economy today, in a speech “Productivity, Wages and Prosperity“. His remarks included a section on wage growth. He concluded that any pick-up is expected to be only gradual given both the spare capacity that still exists in our labour market and the structural factors at work.

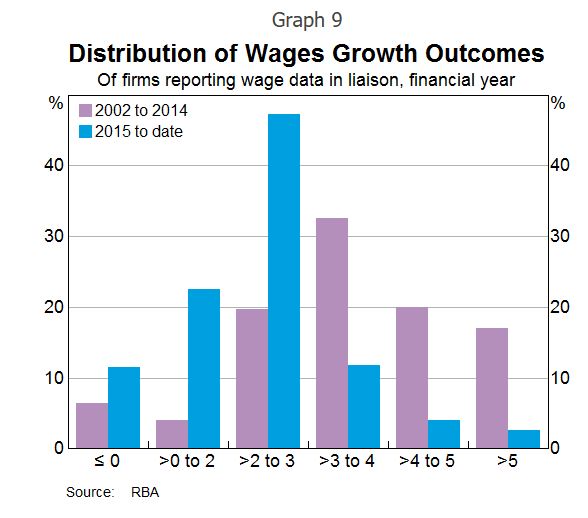

Over recent times, wages growth around the 2 per cent mark has become the norm in Australia. Some time back, the norm was more like 3 to 4 per cent. This downward shift in the rate of wages growth is clearly evident in the wage price index as well as in the more volatile measure of average hourly earnings in the national accounts.

There are both cyclical and structural explanations for why this change has taken place.

From the cyclical perspective, there is still spare capacity in the labour market. The unemployment rate has been around 5½ per cent for a year now. While we can’t be definitive about what constitutes full employment, most conventional estimates for Australia are that it means an unemployment rate of around 5 per cent. It is possible, though, that we could do better than this, especially if we approach the 5 per cent mark at a steady pace, rather than too quickly. Indeed, in a number of other countries, estimates of the unemployment rate associated with full employment are being revised lower as wage increases remain subdued at low rates of unemployment. We have an open mind as to whether this might turn out to be the case here in Australia too. Time will tell.

Broader measures of underutilisation suggest another source of spare capacity in the labour market. Currently, around one-third of workers work part time, with most of these people wanting to work part time for personal reasons. However, of those working part time, around one-quarter would like to work more hours than they do; on average, they are seeking an extra two days a week. If we account for this, these extra hours are equivalent to around 3 per cent of the labour force. This suggests an overall labour underutilisation rate of 8¾ per cent, compared with the 5½ per cent traditional unemployment rate measure based on the number of unemployed people.

Recent experience also reminds us of another important source of labour supply; that is, higher labour force participation. As we have seen over recent times, when the jobs are there, people stay in the workforce longer and others, who had not been looking for jobs, start looking. So the supply side of the labour market is quite flexible, even more so than we expected.

Another cyclical element that has affected average hourly earnings over recent years is the decline in very highly paid jobs in the resources sector as the boom in mining investment wound down. It looks, though, that this compositional shift has now largely run its course.

These various factors go some way to explaining the low wages growth over recent times. When there is spare capacity in the labour market, it is understandable that wages growth is slow.

Yet, alone, these cyclical factors don’t fully explain what is going on. Some structural factors also appear to be at work, with perhaps the most important of these related to competition and technology. I will come back to this in a moment.

The idea that structural factors are at work is supported by this next graph, which shows the wage price index and the responses to the NAB business survey where firms are asked whether the availability of labour is a constraint on output. While there is still spare capacity in the labour market, firms are finding it more difficult to find suitable workers. Yet despite this difficulty, wages growth has not responded in the way that it once did.

A similar pattern is evident overseas. This next graph shows wages growth in the United States and the euro area as well as survey-based measures of labour market tightness (similar to those in the NAB survey). In both economies, wages growth has picked up in response to tighter labour markets, but the response is not as large as it has been in the past.

We are still trying to understand fully why things look different in so many countries and how persistent this will be. Part of the story is likely to be changes in the bargaining power of workers and an increase in the supply of workers as the global economy becomes increasingly integrated. But another important part of the story lies in the nature of recent technological progress.

There are a couple of aspects of this progress that are worth pointing out. One is that it has been heavily focused on software and information technology, rather than installing new and better machines – or on intangible capital rather than physical capital. The second is that the dispersion of technology and productivity between leading and lagging firms has increased, perhaps because of the uneven ability of firms to innovate and use the new technologies. The OECD has done some very interesting work documenting this increasing productivity gap.

Both of these aspects of technological progress are affecting wage dynamics. The returns to those who can develop and best use information technology have increased strongly. These returns, though, are often highly concentrated in a few firms and in only certain segments of the labour market. At the same time, the firms that are not able to innovate and take advantage of new technologies as quickly are slipping behind and they feel under pressure. As a way of remaining competitive, many of these firms are responding by having a very strong focus on cost control. In many cases this translates into a focus on controlling labour costs. This cost-control mentality does not make for an environment where firms are willing to pay larger wage increases.

Over time, we can expect the diffusion of new technology to take place. This is what the historical record suggests. I am optimistic that this diffusion will boost aggregate productivity and lift our real wages and incomes. Advances in information technology, in artificial intelligence and in machine learning have the potential to reshape our economies profoundly and lift average living standards in ways that are difficult to envisage today. But the adoption and the diffusion of these new technologies is a gradual process; it takes time. While it is taking place, the benefits of new technologies are accruing unevenly across the community. In my view, this is one of the key structural factors at work.

Whatever weight one places on these various factors constraining wages growth, it is clear that the slow growth in wages is affecting our economy.

On the positive side of the ledger, it is one of the factors that has helped boost employment growth over recent times. Of course, there are other effects as well.

One is that the low growth in wages is contributing to low rates of inflation in Australia. Indeed, if wages growth were to continue at around its current rate for an extended period, it is unlikely that the rate of inflation would average around the midpoint of the inflation target in the period ahead. Wages growth of 2 per cent and reasonable labour productivity growth are unlikely to make for 2½ per cent inflation on a sustained basis.

Another consequence is that real debt burdens stay higher for longer. Many people who borrowed expected their incomes to grow at something like the old rate rather than the current rate. With their expectations not being realised, the real value of the debt stays higher than they expected and this is likely to affect their spending decisions.

And beyond these purely economic effects, the slow wages growth is diminishing our sense of shared prosperity. If this remains the case, it can make needed economic reforms more difficult.

Given these various effects, some pick-up in wages growth would be a welcome development. It would help deliver a rate of inflation consistent with the target, it would help with the debt situation and it would add to our sense of shared prosperity.

In my judgement, a return, over time, to a world where wage increases started with a 3 rather than a 2 is both possible and desirable. To be clear, this is not a call for a sudden jump in wages growth from current rates to 3 point something. Rather, we will be better off if this increase takes place steadily over time as the economy improves.

There are some signs that we are starting to move in this direction, but it is likely to be a gradual process.

Labour markets in most parts of the country have tightened over the past year. One piece of evidence in support of this is the responses to the NAB survey I showed earlier. There has been a sharp increase in the share of firms reporting the availability of labour as a constraint (Graph 6). The only other time in the past 25 years where this share has been as high as it is now was in the early stages of the resources boom. These survey results are consistent with what the RBA is hearing through our own business liaison program.

One explanation for why firms are reporting that it is hard to find workers with the necessary skills is that the very high focus on cost control over recent times has led to reduced work-related training. With the labour market now tightening, we are perhaps starting to pay the price for this. On a more positive note, a number of businesses and industry associations are now starting to address the skills shortage. Some businesses also tell us that another factor that has made it more difficult to find workers with the necessary skills is the tightening of visa requirements.

It’s reasonable to expect that as the labour market tightens, wages growth will pick up. The laws of supply and demand still work. Consistent with this, we hear reports through our liaison program of wages increasing more quickly in areas where there are capacity constraints, although these reports are still not very common.

As part of our liaison program we also ask firms about their expectations for wages growth over the next year: whether it will be lower, higher or about the same as the recent past. The results are shown in this next graph. There are now more firms expecting a pick-up in wages growth and fewer firms expecting a decline compared with recent years.

So it is reasonable to expect growth in wages to pick up from here. To repeat the point, though, this pick-up is expected to be only gradual given both the spare capacity that still exists in our labour market and the structural factors at work.

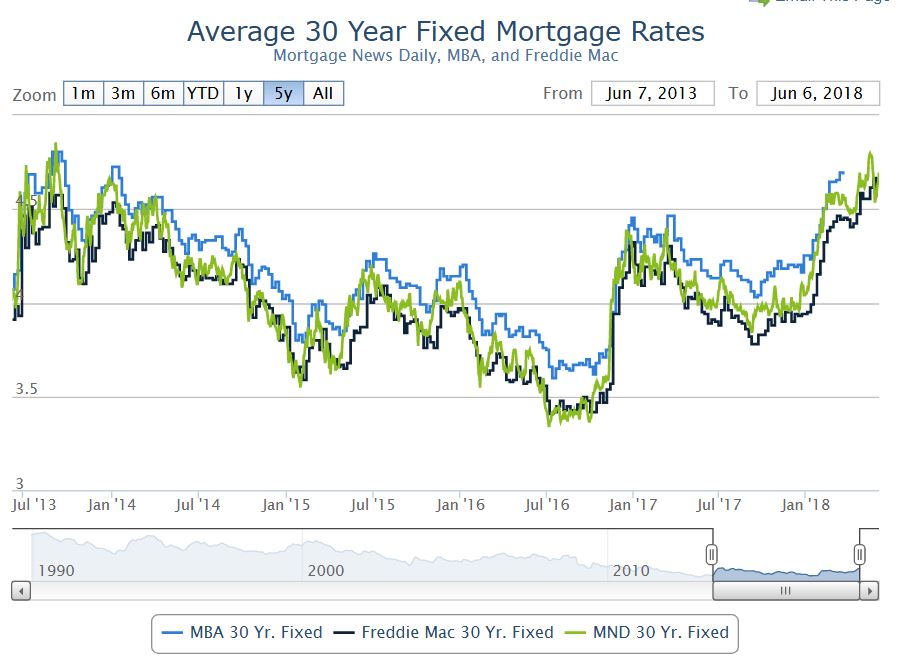

The US 10-year bond rate is moving higher again, with the expectation of more FED rate rises ahead.

US mortgage rates have resumed an upward trend that began last week after political turmoil in Italy began to die down. More simply put, rates had been rising in mid May.

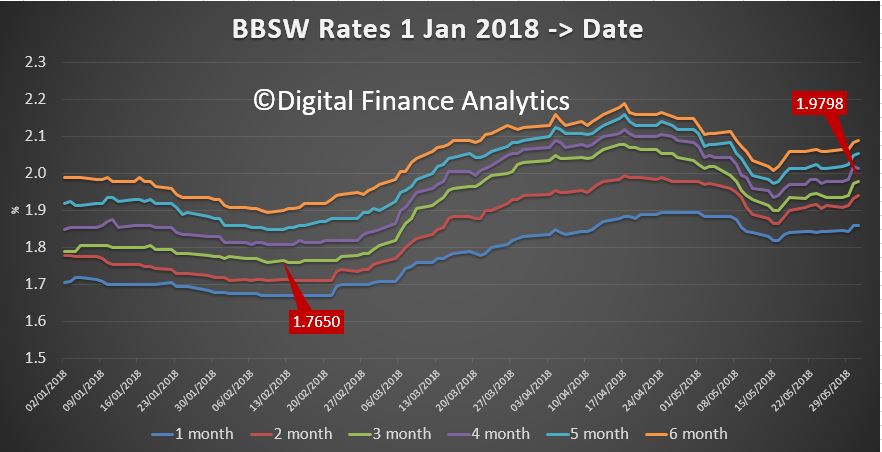

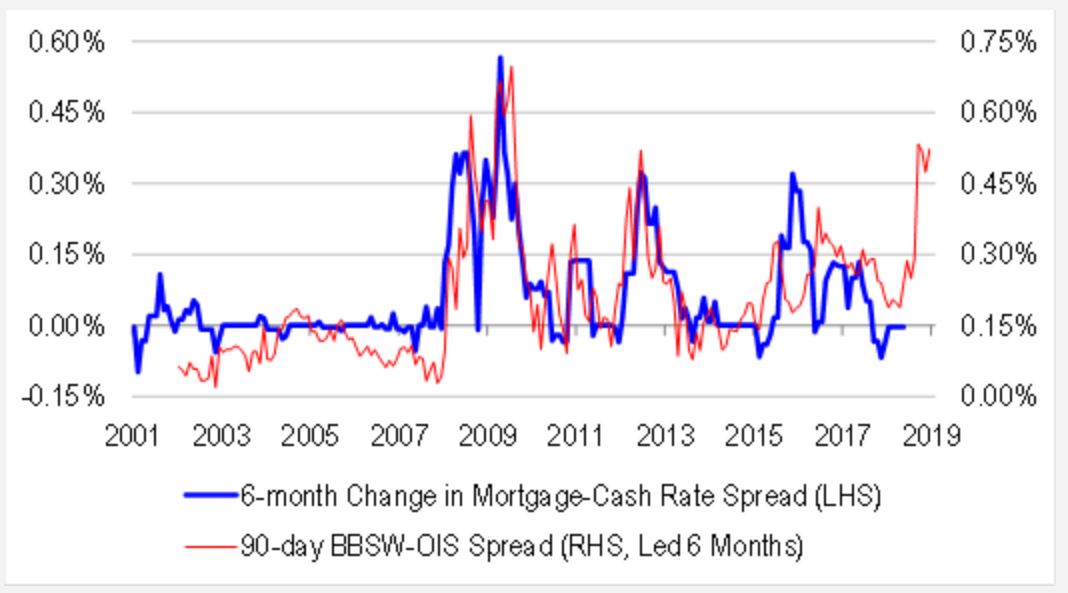

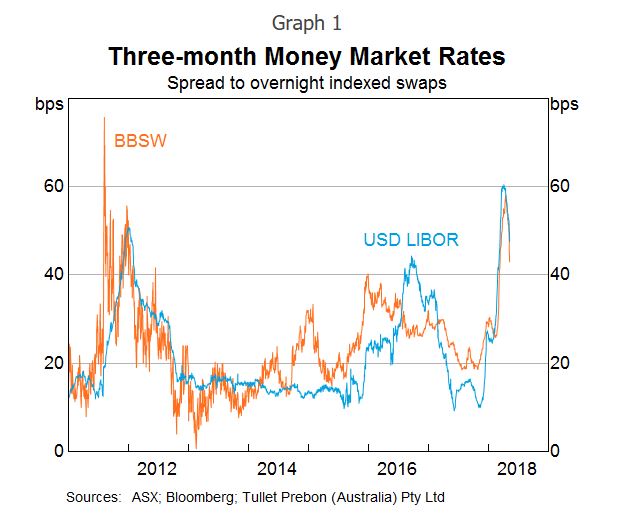

Locally, I continue to track the BBSW (the critical benchmark)..

… and rates are still elevated, if off their highs. This is an indication of the influence of overseas funding, and the question of trust in the local markets following the Royal Commission revelations, recent court cases and now the latest suggestions of cartel behaviour.

But the question is, to what extent are these movements in short term rates hitting Australian bank margins, and will they react by repricing their back books?

There is first the “optics”, given the current focus on their poor behaviour as laid bare in the recent rounds of hearings. Banks who hike rates risk more reputational damage (can it go lower?), although some, such as Suncorp and MyState have already reacted by lifting rates. And if you look carefully average mortgage rates are already a little higher, and deposit rates continue to be cut. But all done quietly, and not enough to repair margins.

Second, the current behaviour we are seeing is the offer of significant discounts for some new and refinanced mortgage loans, especially principal and interest loans with lower LVRs, because banks need to grow their mortgage books to sustain shareholder returns. And mortgage growth is slowing.

Third, its worth understanding what proportion of bank funding is based on short term, and overseas funding. Perfectly timed was a speech – Some Features of the Australian Fixed Income Market, by Christopher Kent, RBA Assistant Governor (Financial Markets) in Tokyo.

The reduced use of offshore funding by the banks has been offset by much greater use of domestic deposits . The big shift away from short-term debt towards deposits started around the time of the global financial crisis. These changes were in response to the demands of the market and those of regulators for banks to make greater use of more stable sources of funding.

While the use of short-term debt (i.e. less than one year) is less than it was, it still accounts for around 20 per cent of banks’ funding. And about 60 per cent of that debt (on a residual maturity basis) is raised offshore. Global money markets, in the United States and elsewhere, provide the Australian banks with a much deeper market with a wider investor base than the relatively small domestic market. This short-term debt is issued in foreign currency terms, but the banks fully hedge their exchange rate (and interest rate) exposures at relatively low cost.

Because Australian banks raise a portion of their funding in US money markets to finance their domestic assets, they responded to higher US rates earlier this year by marginally shifting towards domestic markets to meet their needs. Hence, the rise in the US 3-month LIBOR rate (relative to the Overnight Index Swap (OIS) rate) was closely matched by a rise in the equivalent 3-month bank bill swap rate (BBSW) spread to OIS in Australia; similarly, the two spreads have declined of late by similar orders of magnitude (relative to their respective OIS rates). Equivalent spreads in some other money markets around the world also moved higher, though to a lesser extent than spreads in Australia. In contrast, rates in the euro area and Japan were not affected by the tightness in the US markets. That difference appears to reflect the fact that although European and Japanese banks tap into US money markets, they do so largely to fund US dollar assets.

Changes in BBSW rates in Australia feed through to banks’ funding costs in a number of ways. First, they flow through to rates that banks pay on their short- and long-term floating rate wholesale debt. Second, BBSW rates affect the costs associated with hedging the risks on banks’ fixed-rate debt, with the banks typically paying BBSW rates on their hedged liabilities. Third, interest rates on wholesale deposits tend to be closely linked to BBSW rates.

In short, the costs of a range of different types of funding have risen a bit for Australian banks in the past few months. But they remain relatively low and pressures in short-term money markets have eased, with BBSW about 10 basis points lower than its recent peak (relative to OIS). While some business lending rates are closely linked to BBSW rates – and so have increased a little – there have been few signs to date of changes to rates on loans for housing or small businesses.

Yeh, right…

In summary, banks are exposed to short term funding cost moves, 20% of the funding is short term, and 60% of that off-shore. As for the pressure on rates, well Credit Suisse just put out an interesting note highlighting the state of money markets.

Interbank credit spreads are back at financial crisis highs. And our modelling suggests that we should expect to see both sharp tightening of bank lending standards, and out of cycle rate hikes. Therefore, even without doing anything, the RBA will find that financial conditions are getting tighter.

A quick bit of modelling suggests that banks will need to lift rates, and soon to address the profit compression suggested in the money market movements (yet alone paying the various agreed settlement costs and fees in some banks’ operations). We discussed this a week or so back.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economy has strengthened over the past year. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. The Chinese economy continues to grow solidly, with the authorities paying increased attention to the risks in the financial sector and the sustainability of growth. Globally, inflation remains low, although it has increased in some economies and further increases are expected given the tight labour markets. As conditions have improved in the global economy, a number of central banks have withdrawn some monetary stimulus and further steps in this direction are expected.

Financial markets have been affected by political developments in the eurozone, particularly in Italy. There are also concerns about the direction of international trade policy in the United States and economic developments in a few emerging market economies. Long-term bond yields in most major economies have declined recently and there has been some widening of corporate credit spreads. Overall, though, financial conditions remain expansionary. Conditions in US dollar short-term money markets have eased recently, although they are tighter than earlier in the year, with US dollar short-term interest rates having increased for reasons other than the increase in the federal funds rate. The higher rates in the United States have flowed through to higher short-term interest rates in a few other countries, including Australia.

The price of oil has increased over recent months, as have the prices of some base metals. Australia’s terms of trade are expected to decline over the next few years, but remain at a relatively high level.

The recent data on the Australian economy have been consistent with the Bank’s central forecast for GDP growth to pick up, to average a bit above 3 per cent in 2018 and 2019. Business conditions are positive and non-mining business investment is increasing. Higher levels of public infrastructure investment are also supporting the economy. Stronger growth in exports is expected. One continuing source of uncertainty is the outlook for household consumption. Household income has been growing slowly and debt levels are high.

Employment has grown strongly over the past year, although growth has slowed over recent months. The strong growth in employment has been accompanied by a significant rise in labour force participation, particularly by women and older Australians. The unemployment rate has been little changed at around 5½ per cent for much of the past year. The various forward-looking indicators continue to point to solid growth in employment in the period ahead, with a gradual reduction in the unemployment rate expected. Wages growth remains low. This is likely to continue for a while yet, although the stronger economy should see some lift in wages growth over time. Consistent with this, the rate of wages growth appears to have troughed and there are reports that some employers are finding it more difficult to hire workers with the necessary skills.

Inflation is low and is likely to remain so for some time, reflecting low growth in labour costs and strong competition in retailing. A gradual pick-up in inflation is, however, expected as the economy strengthens. The central forecast is for CPI inflation to be a bit above 2 per cent in 2018.

The Australian dollar remains within the range that it has been in over the past two years. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

The housing markets in Sydney and Melbourne have slowed. Nationwide measures of housing prices are little changed over the past six months, with prices having recorded falls in some areas. Housing credit growth has slowed over the past year, especially to investors. APRA’s supervisory measures and tighter credit standards have been helpful in containing the build-up of risk in household balance sheets, although the level of household debt remains high. While there may be some further tightening of lending standards, the average mortgage interest rate on outstanding loans is continuing to decline.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

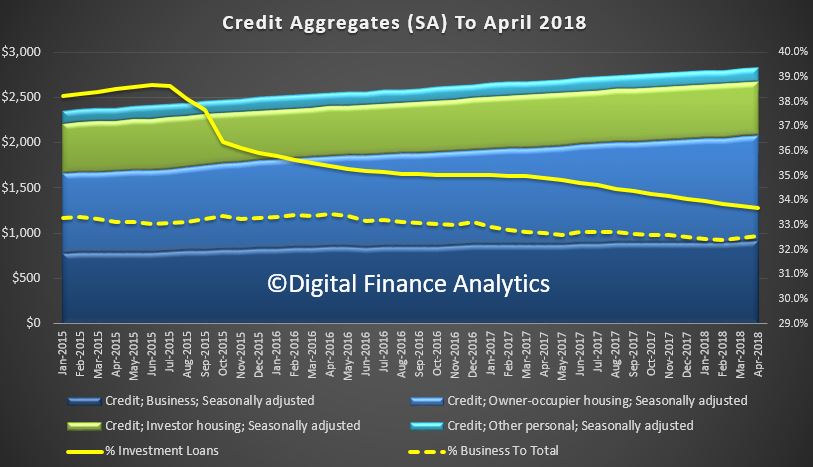

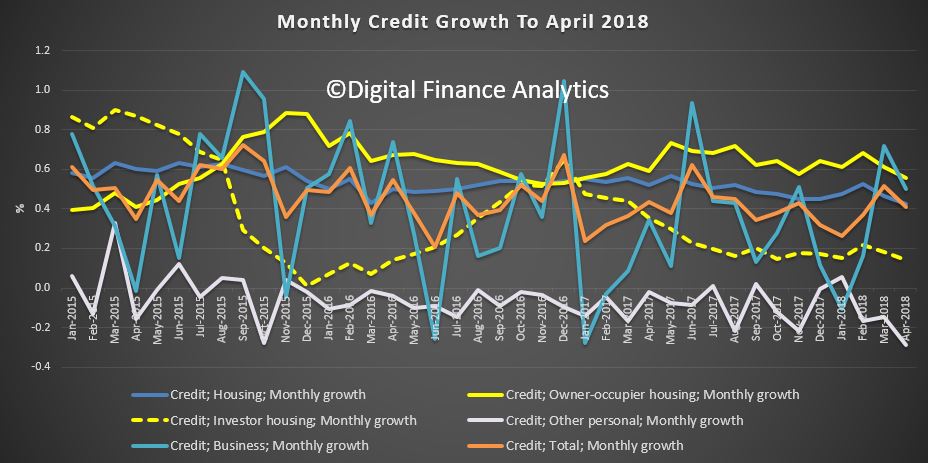

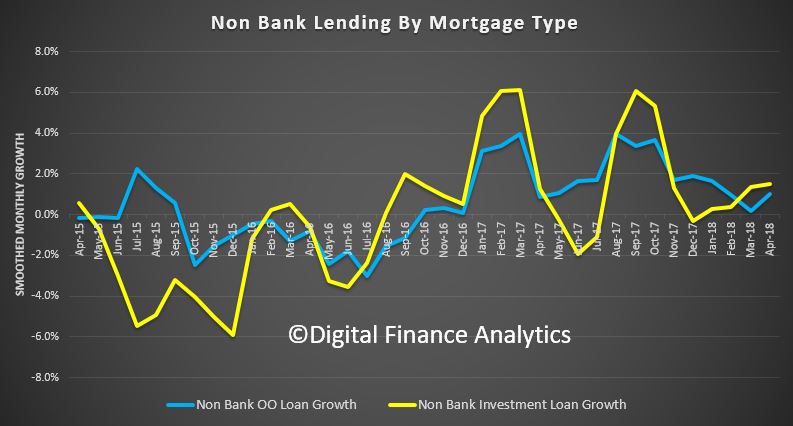

The RBA has released their credit aggregates to April 2018. Total mortgage lending rose $7.2 billion to $1.76 trillion, another record. Within that, owner occupied loans rose $6.4 billion up 0.55%, and investment loans rose 0.14% up $800 million. Personal credit fell 0.3%, down $500 million and business lending rose $6.3 billion, up 0.69%.

Business lending was 32.5% of all lending, the same as last month, and investment mortgage lending was 33.7%, slightly down on last month, as lending restrictions tighten.

The monthly trends are noisy as normal, although the fall in investor property loans is visible and owner occupied lending is easing.

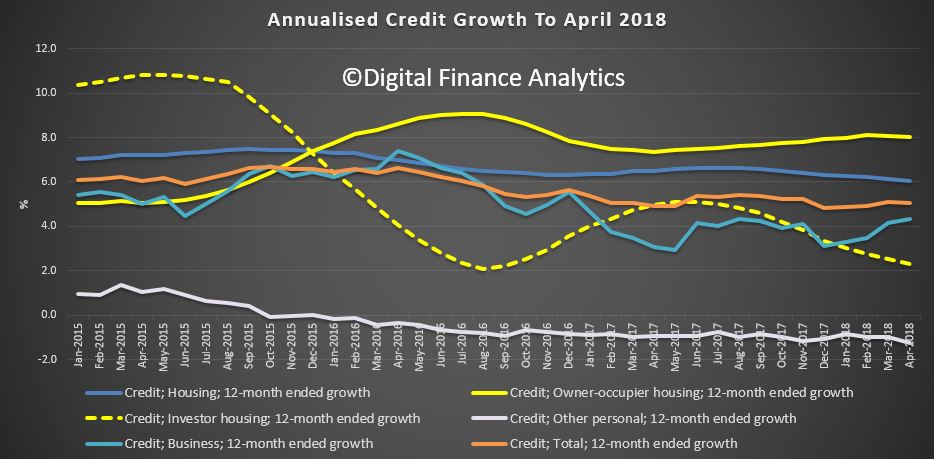

But the annualised stats show owner occupied lending still running at 8%, while business lending is around 4% annualised, investment lending down to 2.3% and personal credit down 0.3%. On this basis, household debt is still rising.

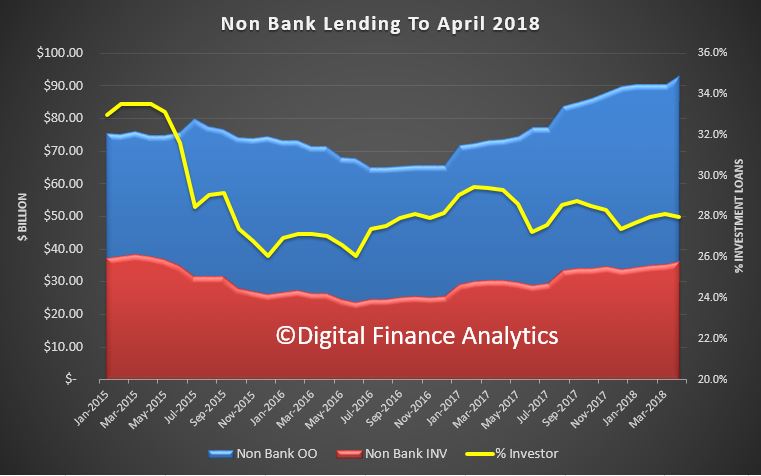

One interesting piece of analysis we completed is the comparison between the RBA data which is of the whole of the market and the APRA data which is bank lending only.

Now this is tricky, as the non-bank data is up to three months behind, and only covers about 70% of the market, but we can get an indication of the relative momentum between the banks and non banks.

We see that non-bank lending has indeed been growing, since late 2016. The proportion of loans for property investors is around 28%, lower than from the banks. Back in 2015, the non-bank investor split was around 34%.

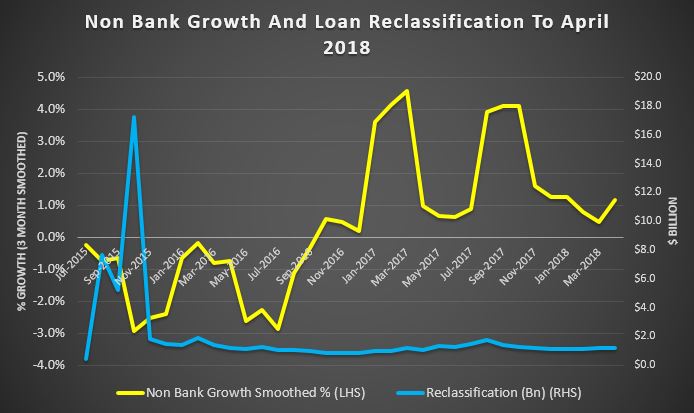

The percentage growth from the non-bank sector appears stronger than the banks. Across all portfolios, loan reclassification is still running at a little over $1 billion each month.

Finally if we look at the relative growth of owner occupied and investment loans in the non-bank sector we see stronger investment lending in the past couple of months. Bank investment property lending actually fell on April according to APRA stats.

As expected, as banks throttle back their lending, the non-banks are filling some of the void – but of course the supervision of the non-banks is a work in progress, with APRA superficially responsible but perhaps not actively so.

We would expect better and more current non-bank reporting at the very least APRA, take note!

The bank bill swap rate (BBSW) rate is a major interest rate benchmark for the Australian dollar and is widely referenced in many financial contracts. Previously, BBSW was calculated from the best executable bids and offers for Prime Bank securities. A major concern over recent years has been the low trading volumes during the rate-set window, the period over which the BBSW is measured.

The new BBSW methodology calculates the benchmark directly from market transactions during a longer rate-set window and involves a larger number of participants. This means that the benchmark is anchored to real transactions at traded prices. ASX, the administrator of BBSW, has consulted market participants on this new methodology. In addition, the ASX has recently conducted a successful parallel run of the new methodology against the existing method.

RBA Deputy Governor Guy Debelle said, ‘The new methodology strengthens BBSW by anchoring the benchmark to a greater number of transactions. This should help to ensure that BBSW remains robust.’

ASIC Commissioner Cathie Armour said, ‘A transaction-based BBSW supports the market’s trust in the robustness and reliability of BBSW.’

‘ASIC and the RBA expect all bank bill market participants – including the banks that issue the bank bills, as well as the participants that buy them – to adhere to the ASX BBSW Guidelines and support the new BBSW methodology. The rate-set window is the most liquid period in the bank bills market, and market participants are therefore likely to get the best outcomes for their institutions and their clients by trading during this time.’

‘We expect market participants to put in place procedures so that as much trading as possible happens during the rate-set window.

This change follows passage through the Parliament in March of legislation that puts in place a framework for licensing benchmark administrators. Consistent with the approach taken in a number of other jurisdictions, it also made manipulation of any financial benchmark, or products used to determine such a benchmark, a specific offence and subject to civil and criminal penalties.

ASIC intends shortly to make financial benchmark rules, on which ASIC consulted in 2017. ASIC also expects to declare BBSW, and a number of other financial benchmarks, as ‘significant benchmarks’ in Australia and to license the administrators of those significant benchmarks.

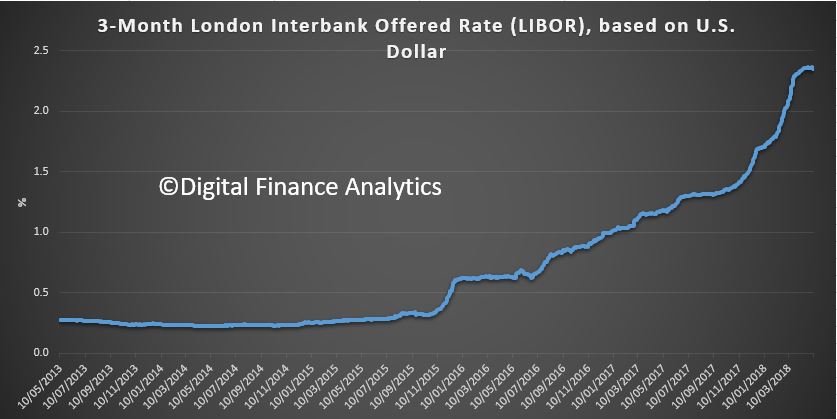

The cost of money continues to rise, and this includes the LIBOR benchmark rate, as shown by this chart. LIBOR or ICE LIBOR (previously BBA LIBOR) is a benchmark rate that some of the world’s leading banks charge each other for short-term loans. As it climbs, it signals rate rises ahead.

But what is LIBOR, and more importantly, will it survive?

ICE LIBOR stands for Intercontinental Exchange London Interbank Offered Rate and serves as the first step to calculating interest rates on various loans throughout the world. LIBOR is administered by the ICE Benchmark Administration (IBA) and is based on five currencies: the U.S. dollar (USD), euro (EUR), pound sterling (GBP), Japanese yen (JPY), and Swiss franc (CHF). The LIBOR serves seven different maturities: overnight, one week, and 1, 2, 3, 6 and 12 months. There is a total of 35 different LIBOR rates each business day. The most commonly quoted rate is the three-month U.S. dollar rate (usually referred to as the “current LIBOR rate”), as shown in the chart.

So, LIBOR is the key interest rate benchmark for several major currencies, including the US dollar and British pound and is referenced in around US$350 trillion worth of contracts globally. A large share of these contracts have short durations, often three months or less. But it’s up for a shakeout as RBA Deputy Governor Guy Debelle Discussed recently.

Last year, the UK Financial Conduct Authority raised some serious questions about the sustainability of LIBOR. That is, apart from the rate fixing problems and the ensuing large fines.

The key problem is that there are not enough transactions in the short-term interbank funding market to reliably calculate the benchmark. In fact, the banks that make the submissions used to calculate LIBOR are uncomfortable about continuing to do this, as they have to rely mainly on their ‘expert judgment’ in determining where LIBOR should be rather than on actual transactions. To prevent LIBOR from abruptly ceasing to exist, the FCA has received assurances from the current banks on the LIBOR panel that they will continue to submit their estimates to sustain LIBOR until the end of 2021. But beyond that point, there is no guarantee that LIBOR will continue to exist. The FCA will not compel banks to provide submissions and the panel banks may not voluntarily continue to do so. There is no guarantee at all that will be the case.

So market participants that use LIBOR need to work on transitioning their contracts to alternative reference rates. The transition will involve a substantial amount of work for users of LIBOR, both to amend contracts and update systems. The process is not straightforward. A large share of these contracts have short durations, so these will roll off well ahead of 2021, but they should not continue to be replaced with another short-dated contract referencing LIBOR. A very sizeable number of current contracts would extend beyond 2021, with some lasting as long as 100 years.

So regulators around the world have been working closely with the industry to identify alternative risk-free rates that can be used instead of LIBOR. These alternative rates are based on overnight funding markets since there are plenty of transactions in these markets to calculate robust benchmarks. Last month, the Federal Reserve Bank of New York began publishing the Secured Overnight Financing Rate (SOFR) as the recommended alternative to US dollar LIBOR. For the British pound, SONIA has been identified as the alternative risk-free rate, and the Bank of England has recently put in place reforms to ensure that it remains a robust benchmark.

But these chosen risk-free rates are overnight rates, while the LIBOR benchmarks are term rates. Some market participants would prefer for the LIBOR replacements to also be term rates. While the development of term risk-free rates is on the long-term agenda for some currencies, they are unlikely to be available anytime soon. This reflects that there are currently not enough transactions in markets for term risk-free rates – such as overnight indexed swaps (OIS) – to support robust benchmarks. Given this reality, it is very important that users of LIBOR are planning their transition to the overnight risk-free benchmarks that are available, such as SOFR for the US dollar and SONIA for the British pound.

For the risk-free rates to provide an alternative to LIBOR, the next challenge is to generate sufficient liquidity in derivative products that reference the risk-free rates. This will take some time, particularly for the US dollar, where SOFR only recently started being published. Nevertheless, progress is being made, with the first futures contracts referencing SOFR recently being launched.

Market participants also need to be prepared for a scenario where the LIBOR benchmarks abruptly cease to be published. In such an event, users would have to rely on the fall-back provisions in their contracts. However, for many products the existing fall-back provisions would be cumbersome to apply and could generate significant market disruption. For instance, some existing fall-backs involve calling reference banks and asking them to quote a rate. To address this risk, the Financial Stability Board has encouraged ISDA to work with market participants to develop a more suitable fall-back methodology, using the risk-free rates that have been identified. But LIBOR is very different from an overnight risk-free rate as it includes bank credit risk and is a term rate. So the key challenge is to agree on a standard methodology for calculating credit and term spreads that can be added to the risk-free rate to construct a fall-back for LIBOR. This needs to be resolved as soon as possible, and we encourage users of LIBOR to engage with ISDA on this important work.

Finally, In Australia, the key InterBank Offer Rate benchmark for the Australian dollar is BBSW. Again we saw a spate of rate manipulations around BBSW, but the RBA and the Australian Securities and Investments Commission (ASIC) have been working closely with industry to ensure that it remains robust. The RBA argues the critical difference between BBSW and LIBOR is that there are enough transactions in the local bank bill market each day to calculate a robust benchmark. Australia has an active bank bill market, where the major banks issue bills as a regular source of funding, and a wide range of wholesale investors purchase bills as a liquid cash management product.

They think that BBSW can continue to exist even if credit-based benchmarks, such as LIBOR, are discontinued in other jurisdictions. But in the event that LIBOR was to be discontinued, with contracts transitioning to risk-free rates, there may be some corresponding migration away from BBSW towards the cash rate. This will depend on how international markets for products such as derivatives and syndicated loans end up adapting in a post-LIBOR world.

The infrastructure is already in place for BBSW and the cash rate to coexist as the key interest rate benchmarks for the Australian dollar. The OIS market is linked to the cash rate and has been operating for almost 20 years. It already has good liquidity at the short end, and the infrastructure is there for longer term OIS. A functioning derivatives market for trading the basis between the benchmarks is important for BBSW and the cash rate to smoothly coexist. Such a basis swap market is also in place, allowing market participants to exchange the cash flows under these benchmarks.

So the bottom line is that these Interbank Offer Rates are not as immutable as might be imagined, and this uncertainty is likely to continue for some time to come.

The Reserve Bank of Australia (RBA) is making an explicit trade-off between inflation and financial stability concerns. And this could be weighing on Australians’ wages.

In the past, the RBA focused more on keeping inflation in check, the usual role of the central bank. But now the bank is playing more into concerns about financial stability risks in explaining why it is persistently undershooting the middle of its inflation target.

In the wake of the global financial crisis, the federal Treasurer and Reserve Bank governor signed an updated agreement on what the bank should focus on in setting interest rates. This included a new section on financial stability.

That statement made clear that financial stability was to be pursued without compromising the RBA’s traditional focus on inflation.

The latest agreement, adopted when Philip Lowe became governor of the bank in 2016, means the bank can pursue the financial stability objective even at the expense of the inflation target, at least in the short-term.

While the RBA board has explained its recent steady interest rate decisions partly on the basis of risks to financial stability, this sits uneasily with what the RBA otherwise has to say about underlying fundamentals of our economy.

It correctly blames trends in house prices and household debt on a lack of supply of housing, and not on excessive borrowing. These supply restrictions amplify the response of house prices to changes in demand for housing. RBA research estimates that zoning alone adds 73% to the marginal cost of houses in Sydney.

Restrictions on lending growth by the Australian Prudential Regulation Authority since the end of 2014 have been designed to give housing supply a chance to catch-up with demand and to maintain the resilience of households against future shocks.

The RBA argues that it needs to balance financial stability risks against the need to stimulate the economy through lower interest rates. But this has left inflation running below the middle of its target range and helps explain why wages growth has been weak.

The official cash rate has been left unchanged since August 2016, the longest period of steady policy rates on record. The fact that inflation has undershot its target of 2-3% is the most straightforward evidence that monetary policy has been too restrictive.

While long-term interest rates in the US continue to rise, reflecting expectations for stronger economic growth and higher inflation, Australia’s long-term interest rates have languished.

Australian long-term interest rates are below those in the US by the largest margin since the early 1980s. This implies the Australian economy is expected to underperform that of the US in the years ahead.

Inflation expectations (implied by Australia’s long-term interest rates) have been stuck around 2% in recent years, below the Reserve Bank’s desired average for inflation of 2.5%.

Financial markets can be forgiven for thinking the RBA will not hit the middle of its 2-3% target range any time soon. The RBA doesn’t believe it will either, with its deputy governor Guy Debelle repeating the word “gradual” no less than 12 times in a speech when describing the outlook for inflation and wages.

Inflation has been below the midpoint of the target range since the December quarter in 2014. On the RBA’s own forecasts inflation isn’t expected to return to the middle of the target range over the next two years.

The Reserve Bank blames low inflation on slow wages growth, claiming in its most recent statement on monetary policythat “labour costs are a key driver of inflationary pressure”. But this is putting the cart before the horse.

In fact, recently published research shows that it is low inflation expectations that are largely to blame for low wages growth.

Workers and employers look at likely inflation outcomes when negotiating over wages. These expectations are in turn driven by perceptions of monetary policy.

Below target inflation makes Australia less resilient to economic shocks, not least because it works against the objective of stabilising the household debt to income ratio. Subdued economic growth and inflation also gives the economy a weaker starting point if and when an actual shock does occur, potentially exacerbating a future downturn.

When the RBA governor and the federal treasurer renegotiate their agreement on monetary policy after the next election, the treasurer should insist on reinstating the wording of the 2010 statement that explicitly prioritised the inflation target over financial stability risks.

If the RBA continues to sacrifice its inflation target on the altar of financial stability risks, inflation expectations and wages growth will continue to languish and the economy underperform its potential.

Author: Stephen Kirchner, Program Director, Trade and Investment, United States Studies Centre, University of Sydney

We got some more data on the state of the Australian Economy today from RBA Deputy Governor, Guy Debelle, which built on the recently released Statement on Monetary Policy (SMP).

There were four items which caught my attention.

First, the recent rise in money market interest rates in the US, particularly LIBOR. He said there are a number of explanations for the rise, including a large increase in bill issuance by the US Treasury and the effect of various tax changes on investment decisions by CFOs at some US companies with large cash pools. This rise in LIBOR in the US has been reflected in rises in money market rates in a number of other countries, including here in Australia. This is because the Australian banks raise some of their short-term funding in the US market to fund their $A lending, so the rise in price there has led to a similar rise in the cost of short-term funding for the banks here; that is, a rise in BBSW. This increases the wholesale funding costs for the Australian banks, as well as increasing the costs for borrowers whose lending rates are priced off BBSW, which includes many corporates.

However, he says the effect to date has not been that large in terms of the overall impact on bank funding costs. It is not clear how much of the rise in LIBOR (and hence BBSW) is due to structural changes in money markets and how much is temporary. In the last couple of weeks, these money market rates have declined noticeably from their peaks. But to my mind it shows one of the potential risks ahead.

Second the gradual decline in spare capacity is expected to lead to a gradual pick-up in wages growth. But when? The experience of other countries with labour markets closer to full capacity than Australia’s is that wages growth may remain lower than historical experience would suggest. In Australia, 2 per cent seems to have become the focal point for wage outcomes, compared with 3–4 per cent in the past. Work done at the Bank shows the shift of the distribution of wages growth to the left and a bunching of wage outcomes around 2 per cent over the past five years or so.

The RBA says that recent data on wages provides some assurance that wages growth has troughed. The majority of firms surveyed in the Bank’s liaison program expect wages growth to remain broadly stable over the period ahead. Over the past year, there has been a pick-up in firms expecting higher wage growth outcomes. Some part of that is the effect of the Fair Work Commission’s decision to raise award and minimum wages by 3.3 per cent. They suggest there are pockets where wage pressures are more acute. But, while those pockets are increasing gradually, they remain fairly contained at this point

But he concluded that there is a risk that it may take a lower unemployment rate than we currently expect to generate a sustained move higher than the 2 per cent focal point evident in many wage outcomes today.

Third, he takes some comfort from the fact that arrears rates on mortgages remain low. This despite Wayne Byres comment a couple of months back, that at these low interest rates, defaults should be even lower! Debelle said that even in Western Australia, where there has been a marked rise in unemployment and where house prices have fallen by around 10 per cent, arrears rates have risen to around 1½ per cent, which is not all that high compared with what we have seen in other countries in similar circumstances and earlier episodes in Australia’s history. To which I would add, yes but interest rates are ultra-low. What happens if rates rise as we discussed above or unemployment rises further?

Finally, the interest rate resets on interest-only loans will potentially require mortgage payments to rise by nearly 30–40 per cent for some borrowers. There are a number of these loans whose interest-only periods expire this year. It is worth noting that there were about the same number of loans resetting last year too. The RBA says there are quite a few mitigants which will allow these borrowers to cope with this increase in required payments, including the prevalence of offset accounts and the ability to refinance to a principal and interest loan with a lower interest rate. While some borrowers will clearly struggle with this, our expectation is that most will be able to handle the adjustment so that the overall effect on the economy should be small.

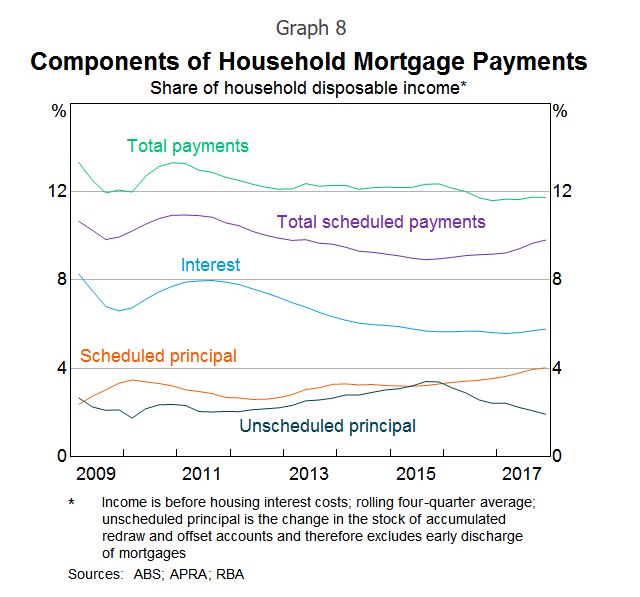

This switch away from interest-only loans should see a shift towards a higher share of scheduled principal repayments relative to unscheduled repayments for a time. We are seeing that in the data. It also implies faster debt amortisation, which may have implications for credit growth.

And there is a risk of a further tightening in lending standards in the period ahead. This may have its largest effect on the amount of funds an individual household can borrow, more than the effect on the number of households that are eligible for a loan. This, in turn, means that credit growth may be slower than otherwise for a time. That he says has more of an implication for house prices, than it does for the outlook for consumption. To which I would add, yes, but consumption is being funded by raiding deposits and higher debt. Hardly sustainable.

So in summary, there are still significant risks in the system and the net effect could well drive prices lower, as credit tightens. And I see the RBA slowly turning towards the views we have held for some time. I guess if there is more of a down turn ahead, they can claim they warned us (despite their settings setting up the problem in the first place).

{kind=link}