The RBA minutes for February 2018 were out today. They highlighted continued momentum in the global economy, with growth up in Australia’s major trading partners. This may put pressure on inflation here. Stronger growth in the world economy had contributed to higher commodity prices over 2017.

Locally, business conditions in the September quarter had been stronger than expected, while conditions in the household sector had been a little weaker. GDP growth was expected to be a little above 3 per cent over both 2018 and 2019.

Growth in consumption had been steady at a modest pace despite relatively weak growth in household disposable income. There was still a risk that growth in consumption might turn out to be weaker than forecast if household income growth were to increase by less than expected. In an environment of high household indebtedness, consumption might be particularly sensitive to adverse developments in household income or wealth.

Conditions in established housing markets had generally eased. Prices for detached houses had fallen in Sydney, especially for more expensive properties, and growth in housing prices had slowed considerably in Melbourne. In Perth and Brisbane, housing price growth had been little changed over prior months. In the eastern capital cities, a considerable additional supply of apartments was scheduled to come on stream over the next couple of years. Members noted that nationwide measures of growth in advertised rents had risen, with rents no longer falling as quickly in Perth. This suggested that rent inflation in the CPI could also be expected to rise gradually over the forecast period.

The unemployment rate was expected to decline a little further over this period to 5¼ per cent, consistent with GDP growth rising to be above potential. This implied that some spare capacity in the labour market would remain over the forecast period. Even though labour market conditions had improved noticeably over 2017, wage growth had remained subdued.

The implied spread between the average outstanding lending and funding rates for Australian banks was estimated to have been stable since mid 2017. Deposit rates had declined somewhat over the course of 2017, as banks’ demand for deposit funding had eased once they had adjusted their balance sheets to comply with the net stable funding ratio (NSFR), which had come into effect at the start of 2018. Banks had also previously increased their long-term debt funding in readiness for the introduction of the NSFR. Bond issuance by Australian banks had remained strong in 2017, with bond tenors increasing further and spreads having continued to decline to the lowest level in 10 years. Issuance of residential mortgage-backed securities had also been strong in 2017 and pricing of these securities had become more favourable to issuers, although the spreads relative to benchmark yields were still above levels seen a few years earlier.

Members observed that, while standard variable interest rates for housing loans had been little changed since mid 2017, the average outstanding variable rate had declined slightly as new and refinanced loans were typically being offered at lower rates. The decline in average outstanding rates had been slightly larger for lenders other than authorised deposit-taking institutions (ADIs), although these rates were still higher on average than those offered by ADIs.

Growth in housing credit had eased over the second half of 2017, driven largely by a slowing in lending to investors. Most of the slowing in housing credit growth had been accounted for by the major banks. Members noted that housing lending by non-ADIs had continued to grow strongly, although these lenders’ share of housing lending remained small.

Financial market pricing suggested that market participants expected the cash rate to remain unchanged during 2018, but had priced in a 25 basis point increase by early 2019.

Over 2017, progress had been made in reducing the unemployment rate and bringing inflation closer to target. The low level of interest rates was continuing to play a role in achieving this outcome. Further progress on these goals was expected over the period ahead but the increase in inflation was likely to occur only gradually as the economy strengthened; the Bank’s central forecast for the Australian economy was for GDP growth to pick up to average a little above 3 per cent over the next two years and for CPI inflation to be a little above 2 per cent in 2018. Members observed that an appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than forecast.

Michele Bullock, Assistant Governor (Financial System), spoke at the Responsible Lending and Borrowing Summit. She downplayed the financial stress in the system and concluded “while there are some pockets of financial stress, the overall level of stress among mortgaged households remains relatively low”. Of course, our own mortgage stress surveys tells a different story, but it does depend on definitions.

Four quick points to note. First, the RBA continues to rely on HILDA data from 2016, despite the changes in living costs, mortgage rates and flat incomes since then. They refer to more timely private datasets, but do not use them, because of “different methodologies.”

Next, she acknowledge that high household debt will be a consideration in terms of interest rate policy, as highly in debt households will be an economic drag on consumption. If debt is considered low, this leaves the door open to rate rises, sooner rather than later.

Third, she perpetuates the view that financial stress is highest among lower income households, but sees little evidence of difficulty among more affluent groups, and argues that many are well ahead with their mortgage repayments. We agree some are, but many more affluent households are also feeling the pinch!

Finally, she is of the view that of households with interest only loans coming up for review, those at risk of not being able to afford a P&I reset, and fall outside current lending standards is quite small (though need watching). That said she highlights risks in the investor portfolios. ” Indeed, the macro-financial risks are potentially heightened with investor lending”. We agree, this is 36% of the portfolio!

So, her conclusion is, move along, nothing to see here! We think the financial stress story is more significant, but there is no authoritative official data covering this topic. Surely a gap the RBA needs to close! Especially if home prices momentum continues to sag.

Thank you for the opportunity to be here today. The title of the summit, ‘Responsible Lending and Borrowing – Risk, Responsibility and Reputation’, really struck a chord with me because there has been much discussion over the past few years about housing prices and the increasing debt being taken on by the household sector.

The Reserve Bank’s interest in this area springs from both its responsibility for monetary policy and its mandate for financial stability. From the perspective of monetary policy, high debt levels will influence the calibration of interest rate changes. The more debt households have, the more sensitive their cash flow, and hence consumption, is likely to be to a rise in interest rates. Households with higher debt levels may also sharply curtail their consumption in response to an adverse shock such as rising unemployment or large falls in house prices, amplifying any economic downturn. My focus today, however, is on the potential risks to financial stability from this build up in debt. One of the key issues we have been focusing on is the extent to which rising household debt might presage stress in household budgets, with flow on effects to financial stability and ultimately to the economy. There has been a lot said and written about this issue in recent times, using a multitude of data sources and anecdotes. What I hope to do today is to put this information into some context to provide a balanced view on the current and prospective levels of household financial stress, and hence the implications for financial stability.

I want to make a couple of points at the outset. The first is that there are clearly households in Australia at the moment that are experiencing financial stress. By focusing on whether financial stress has implications for financial stability, I am not in any way playing down the difficulties some households are experiencing. There is a very real human cost of financial stress.

Second, some of the most financially stressed households are those with lower incomes which typically rent rather than borrow to buy a home. Access to suitable affordable housing for this group is clearly an important social issue. But given the topic of this summit and the potential link to financial stability, I am going to focus in this talk on household mortgage debt and the potential for financial stress resulting from this.

What is Financial Stress?

Definitions of financial stress are many and varied. One definition could be where a household fails to pay its bills or scheduled debt repayments on time because of a shortage of money. This is quite narrow – it captures only those households for which stress has already manifested in missed payments. A much broader definition of financial stress might be a situation where financial pressures are causing an individual to worry about their finances, or where an individual cannot afford ‘necessities’. These definitions might be good leading indicators of failures to meet debt repayments or defaults. So there is a role for a variety of indicators of stress.

One way of thinking about financial stress is in terms of a spectrum or a pyramid, running from mild stress to severe stress (Graph 1). At the mild end, the base of the pyramid, people may perceive that they are financially stressed when they have to cut back on some discretionary expenditure, such as a holiday or a regular meal out. Slightly further up the pyramid, they may not be able to pay bills on time, or might have to seek emergency funding from family. At the top of the pyramid – severe financial stress – a household might be unable to meet mortgage repayments or ultimately be facing foreclosure or bankruptcy.

Graph 1

The pyramid is wider at the bottom than the top reflecting the fact that there will always be more households in milder stress than in severe stress. For some households experiencing milder stress their circumstances might deteriorate and they will move to a more severe form of financial stress. But some others might continue to restrain spending on discretionary items so as to meet essential payments. Others might experience a change in circumstances that improves their financial position.

Triggers and Protections from Financial Stress

Most people don’t consciously set out to put themselves in a position of financial stress. Sometimes people might choose to stretch themselves initially in taking out a loan, perhaps even putting themselves into mild, temporary financial stress. But they would typically be doing so on the expectation that it will become more manageable over time as their income rises. More serious financial stress often only comes about by a combination of what turns out to be excessive debt and changed circumstances. A level of mortgage debt that looked manageable when it was taken out might become unmanageable if, for example, the primary income earner of a household becomes unemployed. Or if life circumstances change, such as through ill health, the birth of a child or breakdown of a relationship.

So what do conditions in the housing sector over the past few years suggest about the potential for financial stress? You are all familiar with the broad story. House prices have been rising rapidly, particularly in Sydney and Melbourne. At the same time, household mortgage debt has been rising while incomes have been growing relatively slowly. As a result, the average household mortgage debt-to-income ratio has risen from around 120 per cent in 2012 to around 140 per cent at the end of 2017 (Graph 2, left panel). Furthermore, the increasing popularity of interest-only loans over recent years meant that by early 2017, 40 per cent of the debt did not require principal repayments (Graph 3). A particularly large share of property investors has chosen interest-only loans because of the tax incentives, although some owner-occupiers have also not been paying down principal. This presents a potential source of financial stress if a household’s circumstances were to take a negative turn.

Graph 2

Graph 3

This is where lending standards come in. There is always a balance to be struck with lending standards. If they are too tight, access to credit will be unreasonably constrained, potentially impacting economic activity and restricting some households from making large purchases that they can afford. If they are too loose, however, borrowers and lenders could find risks building on their balance sheets which, if large enough, might have implications for financial stability. Over the past few years in Australia, regulators have been concerned that lending standards have erred on the more relaxed side. An exuberant housing market in some parts of the country and strong competition among lenders raised the question of whether financial institutions had been appropriately prudent in assessing a household’s ability to meet repayments.

In response, a number of measures were implemented by APRA and ASIC to strengthen mortgage lending standards. These measures have helped improve the quality of lending over the past couple of years. But there is still a large stock of housing debt out there, some of which probably would not meet the more conservative lending standards currently being imposed. How large a risk does this pose to financial stability? It depends on a number of things, including how lax the previous lending standards were, how much of the stock was lent under less prudent standards and the repayment patterns of borrowers. One way of assessing the risk though is to look at the level and trajectory of mortgage stress.

Measures of Financial Stress

There is no single measure that captures the level of financial stress. There are comprehensive surveys, such as the survey of Household, Income and Labour Dynamics in Australia (HILDA) and the Survey of Income and Housing (SIH), that are methodologically robust, but are only available with a lag. A number of private sector surveys are more timely but it can be harder to assess whether their methodologies are well focused on financial stress. There is also information on non-performing loans, insolvencies and property repossessions that is fairly timely and reliable, but is only an indicator of pretty severe stress. I am going to talk through a few measures and see what they imply about the current level of mortgage stress among Australian households.

Let’s start with some high-level data on debt and debt servicing. As I noted above, the average household mortgage debt-to-income ratio has been rising over recent years. In a sense, this is not really surprising. With historically low interest rates, households have been able to service higher levels of debt. Indeed, the debt-servicing ratio (defined as the scheduled principal and interest mortgage repayments to income ratio) has remained fairly steady at around 10 per cent despite the rise in debt (Graph 2, right panel). But these are averages. It is important to look at the distribution of this debt – are the people holding it likely to be able to service it?

Graph 4

The HILDA survey provides information on the distribution of household indebtedness and debt servicing as a share of disposable income. Looking only at owner-occupier households that have mortgage debt, the survey suggests that the median housing debt-to-income ratio has risen steadily over the past decade to around 250 per cent in 2016 (Graph 4, left panel).[1] However, the median ratio of mortgage servicing payments to income has been fairly stable through time, remaining around 20 per cent in 2016 (Graph 4, right panel). In fact 75 per cent of households with owner-occupier debt had mortgage payments of 30 per cent or less of income, which is often used as a rough indicator of the limit for a sustainable level of mortgage repayments.[2] This suggests that, as recently as 2016, mortgage repayments were not at levels that would indicate an unusual or high level of financial stress for most owner-occupiers. But there is a significant minority for whom mortgage stress might be an issue.

Other data sources suggest that the number of households experiencing mortgage stress has fallen over the past decade. The Census data show that the share of indebted owner-occupier households for which actual mortgage payments (that is, required and voluntary payments) were at or above 30 per cent of their gross income declined from 28 per cent in 2011 to around 20 per cent in 2016. And the 2015/16 Household Expenditure Survey indicates that the number of households experiencing financial stress has steadily fallen since the mid 2000s.

Furthermore, a large proportion of indebted owner-occupier households are ahead on their mortgage repayments. We have highlighted this point in recent Financial Stability Reviews. Total household mortgage buffers – including balances in offset accounts and redraw facilities – have been rising over the past few years as households have taken advantage of falling interest rates to pay down debt faster than required. In 2017, total owner-occupier buffers were around 19 per cent of outstanding loan balances or around 2 ½ years of scheduled repayments at current interest rates (Graph 5, left panel)). There is some variation in buffers. While one-third of outstanding owner-occupier mortgages had at least two years’ buffer, around one-quarter had less than one month (Graph 5, right panel). Not all of these loans, however, are necessarily vulnerable to financial stress. If households are building up other assets instead of building up mortgage buffers, they may still be well positioned to weather any change in circumstances.

Graph 5

All of this suggests that a large proportion of households have some protection against financial stress. There are, however, some households that are more vulnerable, probably those with lower income who cannot afford prepayments or those with relatively new mortgages who have yet to make many inroads.

Another way of measuring financial stress is by asking survey respondents to self-assess. For example, a survey might ask about the respondent’s ability to meet payments, the type of financial stress they have experienced, or whether they have had difficulty raising money in an emergency.

The HILDA survey also provides some information on this. In general, measures such as these indicate that financial stress for owner-occupiers with mortgage debt has not changed much over the past decade, and is actually lower than in the early 2000s. Around 12 per cent of such households indicated that they would expect difficulty raising funds in an emergency in 2016 (Graph 6). The survey also asks people what sort of financial difficulties they had experienced over the past twelve months. For example, did they have difficulty paying a mortgage or bills on time? Were they unable to heat their home or did they have to go without meals? Did they have to ask for financial assistance from family or a welfare agency? A bit less than 20 percent of owner-occupier households said they had experienced at least one difficulty in the past 12 months, but only 5 per cent reported experiencing three or more of these difficulties. Most of these indicators also suggest that, in line with some of the earlier data I noted, stress has declined since 2011, which probably largely reflects the fall in interest rates since that time.

Graph 6

Unfortunately, while the HILDA and SIH data are rich in terms of the information provided, they are not very timely. We have, for example, only just received the 2016 data. So much of the discussion on household stress relies on more timely private surveys. These surveys measure stress in different ways. Some focus specifically on mortgage stress. Others look at housing affordability, including for renters. And still others attempt to measure financial ‘comfort’ more broadly than just housing. Many of these suggest that housing stress has been increasing over the past year or so.

Looking at the history for which we have data for both the private and comprehensive surveys, it is a little difficult to reconcile their findings. But there do seem to be some methodological differences that mean some surveys might overstate financial stress somewhat. For example, in some of these surveys, self-assessed living expenses are used. If households include discretionary expenditure that could be cut back in an emergency, the amount of income available to meet scheduled repayments might be understated. Furthermore, if actual mortgage repayments are used, those households that are routinely ahead of their payments schedule might be assessed as having little spare income for emergencies when in reality they have been building up buffers and have surplus cash flow.

Most of the measures I have discussed so far are more in the nature of potential financial stress. For some households this will likely turn out to be temporary until their circumstances change. But others may find themselves in a prolonged period of belt tightening or, in the extreme, having to sell their property or default on their payments. In this latter case, financial stress will show up in non-performing loans on banks’ balance sheets and perhaps even in property repossessions or bankruptcies. What do these data tell us?

Banks’ non-performing housing loans have been trending upwards over the past few years, although they remain very low in absolute terms at around 0.8 per cent of banks’ domestic housing loan books (Graph 7). Much of this rise is attributable to a rise in non-performing loans in the mining-exposed states of Western Australia and Queensland – not unexpected given the large falls in employment and housing prices in some of these regions.

Graph 7

Personal insolvencies as a share of the population have remained fairly stable over the past few years. Applications for property possession as a share of the total dwelling stock have generally declined since 2010, with the exception being Western Australia (Graph 8). This indicates that financial stress has a high cyclical component, and there are likely to be some regions of the country that are in more difficult times than others. But the focus for financial stability considerations is largely a national rather than a regional perspective.

Graph 8

So my overall interpretation of these myriad pieces of information is that, while debt levels are relatively high, and there are owner-occupier households that are experiencing some financial stress, this group is not currently growing rapidly. This suggests that the risks to financial institutions and financial stability more broadly from household mortgage stress are not particularly acute at the moment.

Housing Investors

Most of my focus so far has been on owner-occupiers who account for around two-thirds of housing debt outstanding. But investment in housing has been growing strongly in recent years. So it is worth briefly considering the risk of financial stress emanating from this group of borrowers.

The risks to financial stability associated with investor mortgage debt are probably a bit different from those associated with owner-occupier debt. Investors tend to have larger deposits, and hence lower starting loan-to-valuation-ratios (LVRs) (Graph 9). They often have other assets, such as an owner-occupied home, and also earn rental income. Higher-income taxpayers are more likely to own investment properties than those on lower incomes, so may be better able to absorb income or interest rate shocks.

Graph 9

But investors have less incentive than owner-occupiers to pay down their debt. As noted above, many take out interest-only loans so that their debt does not decline over time. If housing prices were to fall substantially, therefore, such borrowers might find themselves in a position of negative equity more quickly than borrowers with an equivalent starting LVR that had paid down some principal. Indeed, the macro-financial risks are potentially heightened with investor lending. For example, since it is not their home, investors might be more inclined to sell investment properties in an environment of falling house prices in order to minimise capital losses. This might exacerbate the fall in prices, impacting the housing wealth of all home owners. As investors purchase more new dwellings than owner-occupiers, they might also exacerbate the housing construction cycle, making it prone to periods of oversupply and having a knock on effect to developers.

Data from the Australian Taxation Office (ATO) provide some information on housing investors. While not particularly timely, these data show that the share of taxpayers who are property investors has increased steadily over the past few years. In 2014/15, around 11 per cent of the adult population, or just over 2 million people, had at least one investment property and around 80 per cent of those were geared (Graph 10). Most of those investors own just one investment property but an increasing number own multiple properties. There has also been a marked increase in the share of geared housing investors who are over 60. These factors do not necessarily increase the risk of financial stress but they bear watching.

Graph 10

The recent increases in interest rates on investor loans, in response to APRA’s measures to reduce the growth in investor lending, has probably affected the cash flows of investors. Interest rates on outstanding variable-rate interest-only loans to investors have increased by 60 basis points since late 2016. However, over the past few years, lenders have been assessing borrowers’ ability to service the loan at a minimum interest rate of at least 7 per cent. So while interest rates and required repayments have likely risen, many borrowers should be relatively resilient to the recent changes.

Furthermore, a large proportion of interest-only loans are due to expire between 2018 and 2022. Some borrowers in this situation will simply move to principal and interest repayments as originally contracted. Others may choose to extend the interest-free period, provided that they meet the current lending standards. There may, however, be some borrowers that do not meet current lending standards for extending their interest-only repayments but would find the step-up to principal and interest repayments difficult to manage. This third group might find themselves in some financial stress. While we think this is a relatively small proportion of borrowers, it will be an area to watch.

Conclusion

The historically high levels of mortgage debt in Australia raises questions about the resilience of household balance sheets to a change in circumstances and the ability of the financial system to absorb a widespread increase in household financial stress. The information we have suggests that, while there are some pockets of financial stress, the overall level of stress among mortgaged households remains relatively low. Furthermore, the banking system is strong and well capitalised, and is supported by prudent lending standards. The risks to financial stability from this source therefore remain low although we will need to keep an eye on developments. Appropriately prudent lending standards will continue to play an important role in ensuring that the financial system remains stable and households borrow responsibly.

Listen, You Can Hear the Screws Tightening On Mortgage Lending. Welcome to The Property Imperative Weekly to 17th February 2018.

Watch the video, or read the transcript.

In this week’s digest of finance and property news we start with Governor Lowe’s statement to the House of Representatives Standing Committee on Economics. He continued the themes, of better global economic news, lifting business investment and stronger employment on one hand; but weak wage growth, and high household debt on the other. But for me one comment really stood out. He said:

it would be a good outcome if we now experienced a run of years in which the rate of growth of housing costs and debt did not outstrip growth in our incomes in the way that they did over the past five years.

This is highly significant, given the fact the lending for housing is still growing faster than wages, at around three times, and home prices are continuing to drift a little lower. So don’t expect any moves from the Reserve Bank to ease lending conditions, or expect a boost in home prices. More evidence that the property market is indeed in transition. The era of strong capital appreciation is over for now.

There was lots of news this week about the mortgage industry. ANZ and Westpac have tightened serviceability requirements. Westpac recently introduced strict tests of residential property borrowers’ current and future capacities to repay their loans. The change is said to be intended to identify scenarios that might affect borrowers’ capacity to pay back their loans. These scenarios include having dependents with special needs that might require borrowers to spend on long-term care and treatment. ANZ has added “a higher level of approval for some discretions” used in its home loan policy for assessing serviceability, reducing approvals outside normal terms.

Talking of lending standards, APRA released an important consultation paper on capital ratios. This may sound a dry subject, but the implications for the mortgage industry and the property market are potentially significant. As part of the discussion paper, APRA, says that addressing the systemic concentration of ADI portfolios in residential mortgages is an important element of the proposals. They have FINALLY woken up to the risks in the system, just years too late! We have significant numbers of loans in the system currently that would now not pass muster. More about that next week.

Their proposals, which focus in on mortgage serviceability, would change the industry significantly, as lower risk loans will be more highly prized (so expect low rate offers for lower LVRs), whilst investment loans, and interest only loans are likely to cost more and be harder to find. Combined this could certainly move the market! The proposals introduce “standard” and “non-standard” risk categories.

As well as increasing the risk weights for some mortgages, they also continue to close the gap between the advanced (IRB) internal approach used by large lenders, and the standard approach used by smaller players. Those in transition (e.g. Bendigo Bank) may find less of an advantage in moving to advanced as a result. You can watch our separate video on this important topic.

Whilst the overall capital ratios will not change much, there is a significant rebalancing of metrics, and Banks will more investment and interest only loans will be most impacted. So getting an investment loan will be somewhat harder and this will impact the property market. The proposals are for consultation, with a closing data 18 May 2018.

Another data point on the property market came from a new report by Knight Frank which claims that in 2017, one-third of Australian residential development sites were sold to Chinese investors and developers. The share of sales to Chinese buyers has tripled since 2013, but decreased from the 38 per cent recorded in 2016. The level of Chinese investment in residential development sites varied from state to state: in Victoria, 38.7 per cent of residential site sales were to Chinese buyers; in New South Wales, 35.6 per cent of residential site sales were to Chinese buyers, and in Queensland, Chinese buyers comprised 7.4 per cent of total residential site sale volumes. So this is one factor still supporting the market, though in Australia, the Australian Prudential Regulatory Authority has encouraged local financial institutions to impose stricter controls, while in China the government has attempted to moderate capital outflow with China’s Central Bank imposing new rules for companies which make yuan-denominated loans to overseas entities.

The data from the ABS on Lending Finance, the last part of the finance stats for December, really underscores the slowing momentum in investment property lending, especially in Sydney (though it is still a significant slug of new finance, and there is no justification to ease the current regulatory requirements.) The ABS says the total value of owner occupied housing commitments excluding alterations and additions rose 0.1% in trend terms, total personal finance commitments fell 0.2%. Revolving credit commitments fell 1.4%, while fixed lending commitments rose 0.5%. There was a small rise in lending for housing construction, but overall mortgage momentum looks like it is still slowing and the mix of commercial lending is tilting away from investment lending and towards other commercial purposes at 64%, which is a good thing.

There is an air of desperation from the construction sector, as sales momentum continues to ease, this despite slightly higher auction clearance rates last week. CoreLogic said the final auction clearance rate was 63.7 per cent clearance rate across almost double the volume of auctions week-on-week (1,470). Over the week prior, a clearance rate of 62.0 per cent was recorded across 790 auctions. Both auction clearance rate and volumes were lower than what was seen one year ago, when a 73.2 per cent clearance was recorded across 1,591 auctions. There is significant discounting going on at the moment to shift property, and some builders are looking to lend direct to purchases to make a sale. For example, Catapult Property Group launched a new lending division that will help first home buyers get home loans with a deposit of only $5,000. The Brisbane-based company encourages first home buyers in Queensland to enter the real estate market now by taking advantage of the state government’s $20,000 grant that is ending on 30 June 2018. This is at a time when lenders are insisting on larger deposits, and are applying more conservative underwriting standards.

Economic data out this week showed that according to the ABS, trend unemployment remained steady at 5.5%, where it has hovered for the past seven months. The trend unemployment rate has fallen by 0.3 percentage points over the year but has been at approximately the same level for the past seven months, after the December 2017 figure was revised upward to 5.5 per cent. The ABS says that full-time employment grew by a further 9,000 persons in January, while part-time employment increased by 14,000 persons, underpinning a total increase in employment of 23,000 persons. The fact is that while more jobs are being created, it is not pulling the rate lower, and many of these jobs are lower paid part time roles – especially in in the healthcare sector. In fact, the growth in employment is strong for women than men. A rather different story from the current political spin!

In a Banking Crisis, are Bank Deposits Safe? We discussed the consequences of recently introduced enhanced powers for APRA to deal with a bank in distress this week. There were several well publicised Government bail-out’s of banks which got into problems after the GFC. For example, the UK’s Royal Bank of Scotland was nationalised. This costs tax payers dear, so there were measures put in place to try to manage a more orderly transition when a bank gets into difficulty and raises the question of “Bail-in” arrangements. Take New Zealand for example. There regulators have specific powers to grab savings held in the banks in assist in an orderly transition in the case of a failure, alongside capital and other bank assets. And, given the New Zealand position (and the tight relationship between banking regulators in Australia and New Zealand), we should look at the position in Australia. Are deposit funds in Australia likely to be “bailed-in”? Well, the Treasury confirmed that because deposits are not classified as capital instruments, and do not include terms that allow for their conversion or write-off, they cannot be ‘bailed-in’. But we have a catch all clause in APRA’s powers that says they can grab “any other instrument” and deposits, despite the Treasury reassuring words, is not explicitly excluded. So I for one cannot be 100% convinced savings will never be bailed-in. And that’s a worry! I recall the Productivity Commission comment last week, that financial stability had taken prime place compared with competition (and so customer value) in financial services. The issue of bail-in of deposits appears to be shaping the same way. You can watch our separate video discussion on this important topic.

The first round of public hearings for the Banking Royal Commission will focus on lending, including mortgages, credit cards and car loans; we heard during the opening session. The Commission highlighted the large size of the lending market, and the significant number of submissions they have already received on misconduct in this area, including relating to intermediaries, commission and advice. In addition, as part of the opening address, we were told that some of the major players were unable to provide the full range of misconduct information that Commission requested. Some players offered a few case studies, and were then asked to provide more detail over the past 5 years (as opposed to 10) but said they could not meet the required deadline. Based on the opening round, Banks are going to find this a painful process. Not least because The Commission is publishing information on the sector. In its first release, it pointed to declining competition in the banking sector, with the number of credit unions falling due to consolidation and the major banks holding 75 per cent of total assets held by ADIs in Australia. The paper noted that five of the 20 listed companies that make up the ASX20 are banks, noting that the major banks have “generally achieved higher profit margins than other types of ADIs” with a profit margin of 36.4 per cent in the June quarter 2017. They also underscored that Australia’s major banks are “comparatively more profitable” than some of their international peers in Canada, Sweden, Switzerland and the UK.

We expect to hear more from the Royal Commissions on unfair and predatory practices. To underscore this there was some good news for Credit Card holders, with new legalisation passed in parliament to force Credit card providers to scrap unfair and predatory practices. However, the implementation timetable is extended into 2019. The reforms include:

Requiring affordability assessments be based on a consumer’s ability to repay the credit limit within a reasonable period (from July 2018). This tightens responsible lending obligations for credit card contracts.

Banning unsolicited offers of credit limit increases (from January 2019). At the moment, whilst the law forbids providers from making these sorts of offers in writing, offers can be made by phone and other mediums. This loophole has been exploited, but will now be closed.

Simplifying how credit card interest is calculated, especially, banning the practice of backdating interest rate charges. Currently, some providers were attracting new customers with promotional low rate, or no rate offers, say for the first month. But, if a customer failed to pay off in full a credit card bill after the first month, the credit card company was often retrospectively applying the new interest rate to previous purchases. This was allowed in the banks’ small print, but the government said the practice did “not align with consumers’ understanding and expectation about how interest is to be charged”. This will be banned, from next year.

Requiring credit card providers to have online options to cancel cards or to reduce credit limits (from January 2019). At the moment, some card providers force customers to come into a bank branch to reduce limits or terminate cards, and when they did come in were often persuaded not to do it. The asymmetry between fast credit card approvals online, and slow cancellation will end.

So another week highlighting the stresses and strains in the banking sector, and the forces behind slowing momentum in the property market. And based on the stance of the regulators, we think the screws will get tighter in the months ahead, putting more downward pressure on mortgage lending home prices and the Banking Sector. Something which the RBA says is a good thing!

The latest statement from Governor Philip Lowe continues the theme, of better global economic news, stronger employment, but weak wage growth, and high household debt. He says, ” it would be a good outcome if we now experienced a run of years in which the rate of growth of housing costs and debt did not outstrip growth in our incomes in the way that they did over the past five years”.

Since we last met in August, the improvement in the global economy has continued and forecasts for world growth have been revised up. Rather than just one or two economies doing better, the improvement has been broadly based, with a synchronised upswing taking place. Partly as a result, both international trade and commodity prices have picked up and this is helping the Australian economy.

The stronger economic growth has resulted in unemployment rates falling further. In a number of countries, the unemployment rate is now below conventional estimates of full employment. Inflation has remained low, partly reflecting the fact that wage growth has been quite subdued despite the low unemployment rates. Low inflation has meant low interest rates. And for much of past year, volatility in asset prices was also unusually low.

Over recent times, many investors have been proceeding on the basis that this combination of strong growth, low unemployment, low inflation and low interest rates would persist. Many also expected the low volatility in asset prices to continue. A couple of weeks ago we saw a re-evaluation of some of these assumptions by some investors, with the catalyst being a pick-up in wage growth in the United States. The result has been an increase in bond yields, a decline in equity prices and increased market volatility.

While the exact timing of changes in investors’ assumptions is difficult to predict, the fact that some reassessment took place, at some point, is not that surprising. Above-trend growth at a time of low unemployment should be expected to see inflation lift, even if that lift is gradual because of factors that are affecting wage and price pressures globally. To add to the mix, fiscal policy in some countries, most noticeably the United States, is becoming more expansionary. So I expect rising inflation pressures will figure more prominently in discussions of the global economy than they have for some time.

Another important international influence on our economy is what happens in China. Like other economies, China is benefiting from the global upswing. At the same time, there are ongoing efforts to increase the sustainability of China’s economic growth, both in terms of its financing and the environment. These efforts are affecting both the structure of finance in the Chinese economy and commodity markets. The Chinese authorities face the difficult challenge of getting the balance right between containing medium-term risks and supporting near-term growth, and we continue to watch developments there closely.

I would now like to turn to the Australian economy. On balance, the news over the summer has generally had a more positive tone than it has had for a while. For some time we had been expecting GDP growth to be a bit stronger in 2018 and 2019 than in the recent past. The recent data have been consistent with this. Over this year and next we expect GDP growth to be a bit above 3 per cent, which is faster than our current estimate of trend growth for the Australian economy. This outlook has not been affected by the recent volatility in the equity market.

The Australian labour market has been noticeably stronger than we were expecting, which is good news. Over the past year, the number of people with a job increased by 400 000, and there has been a marked increase in the participation rate for women. We don’t expect a repeat of these very strong outcomes in 2018, but we do expect employment growth to be fast enough to see a further gradual reduction in the unemployment rate. The unemployment rate, though, is likely to remain above conventional estimates of full employment in Australia for some time.

A range of business indicators have also improved since we last met. Business conditions have lifted and so too has the outlook for capital expenditure. It would be an exaggeration to say that animal spirits have fully returned, but the mood has certainly brightened in much of the business community. There are a number of reasons for this, but in parts of the country the lift in mood is being helped by the large infrastructure projects underway. Not only are these projects creating jobs today, but they are building much needed productive capacity for the future.

Against this general backdrop of improving conditions, one uncertainty remains the strength of consumer spending. In the September quarter, spending growth was quite weak, especially for discretionary items. More recently, the retail trade figures have been better and suggest a stronger outcome for the December quarter.

Most households are experiencing only slow growth in their incomes and many expect that this will continue for some time yet. This lowering of expectations about income growth is likely to be affecting spending, especially in an environment of high levels of household debt. A pick-up in income growth, by way of ongoing increases in jobs and stronger wage growth should help here.

We continue to look carefully at household balance sheets. On balance, our assessment is that there has been some containment of the build-up of risk in this area. This is a positive development. Lending standards are stricter than they were previously and there has been a welcome decline in the share of interest-only loans, following measures taken by APRA. Housing credit growth has also slowed a bit, especially to investors. In the property market, prices are no longer rising in Sydney, and have fallen for higher-priced houses. The Melbourne market has also cooled somewhat. Increased supply of housing, changes in the nature and availability of financing, and some reduction in foreign demand have all played a role. While the Reserve Bank does not target housing prices or household debt, it would be a good outcome if we now experienced a run of years in which the rate of growth of housing costs and debt did not outstrip growth in our incomes in the way that they did over the past five years.

In terms of CPI inflation, the picture is pretty much the same as it was when we met six months ago. Inflation, in headline and underlying terms, is still running at a little under 2 per cent. This is higher than the inflation rate a year ago, but inflation does remain low.

The most recent data confirmed themes that we have been seeing for some time. Strong competition from new entrants and changes in retailers’ business models are putting downward pressure on the prices of consumer durables and groceries. The prices of many of these goods are lower than they were a few years ago. This is good news for consumers, although not for some retailers. We do expect to see some lessening of this downward pressure on prices at some point, although not for a while yet.

The second ongoing theme is higher prices for utilities and tobacco. Both of these have added materially to the CPI over the past year, and further increases are expected.

The third theme is the subdued increase in wages feeding through into subdued price increases, particularly for a range of market services. This, too, is likely to continue for a while yet.

We have discussed on previous occasions the reasons for the subdued wage increases. These include the continuing spare capacity in the economy after the unwinding of the mining investment boom; the heightened sense of competition due to globalisation and technological change; and changes in bargaining arrangements. These factors are still at work, although through our liaison program we hear reports of pockets where the labour market is tight and firms are finding it hard to find workers with the right skills. In some of these areas wages are now rising more quickly than previously, but many firms remain wary of adding to their cost base in the current environment.

Over time, we expect wage growth to pick up as the labour market strengthens further. The pick-up, though, is likely to be gradual. This increase in wage growth and the more general reduction in spare capacity in the economy are expected to contribute to inflation picking up as well. But to continue the theme, this pick-up, too, is expected to be only gradual. This year and next, we expect CPI inflation to be between 2 and 2½ per cent.

As you would be aware, the Reserve Bank Board has held the cash rate at 1½ per cent since August 2016. This represents an accommodative setting of monetary policy, aimed at supporting the economy and employment, and returning inflation towards the mid-point of the medium-term target range. As we have discussed with this Committee on previous occasions, the Board has sought to strike a balance between these benefits of monetary stimulus and the medium-term risks associated with the increase in the already high level of household debt. We have sought to steer a middle course, promoting sustainable growth in the economy.

Over the past year the economy has been moving in the right direction. Progress has been made in reducing unemployment and having inflation return to around the mid-point of the target range. And on the financial side, the build-up of risks in household balance sheets has been contained, although risks there remain.

Over the coming year we expect to make further progress. Our central scenario for the Australian economy is for a further reduction in the unemployment rate and an increase in inflation towards the mid-point of the target range. Of course, this is just the central scenario, and there are other scenarios as well.

But if this is how things play out, at some point it will be appropriate to have less monetary stimulus and for interest rates in Australia to move up, as is already happening in some other countries. In other words, it is more likely that the next move in interest rates will be up, rather than down.

The timing of any future move will depend upon the extent and pace of progress that we make in reducing the unemployment rate and having inflation return to target. As things currently stand, we expect that progress to be steady, but to be only gradual. Given this assessment, the Reserve Bank Board does not see a strong case for a near-term adjustment of monetary policy. We will, of course, keep that judgement under review at future meetings.

Today, the Reserve Bank of Australia and its Payments System Board (PSB) welcome the public launch of the New Payments Platform (NPP). The NPP is an important addition to Australia’s payments infrastructure and it will provide a platform for innovation and competition in the provision of payment services.

The Reserve Bank and the PSB thank the NPP Australia Board, NPP financial institutions and their thousands of staff who have contributed to the development of the platform over a number of years. It has been a highly collaborative industry program, which has involved considerable planning, effort and investment.

Philip Lowe, Governor and Chair of the PSB, said, ‘The public launch of the NPP represents the delivery of a major piece of national infrastructure. I would like to thank everyone who has been involved in the NPP project and I look forward to the payment innovations it will make possible and the benefits this will generate for all Australians.’

The launch of the NPP means that the industry is delivering on the key strategic objectives that were established by the PSB in June 2012 as part of its Strategic Review of Innovation in the Payments System. In particular, the NPP and the initial overlay service, Osko, will allow financial institutions to provide improved services to Australian businesses and consumers, including to:

make real-time payments, with close to immediate funds availability to the recipient

make and receive payments on a 24/7 basis

have the capacity to send more complete remittance information with payments

address payments in a relatively simple way.

Around 60 banks, credit unions and building societies will begin rolling out services to their customers from today, with the number of financial institutions and accounts linked to the NPP progressively increasing over the coming months.

The Reserve Bank developed new infrastructure, the RITS Fast Settlement Service, to enable the settlement of NPP transactions between financial institutions in real time on a 24/7 basis across exchange settlement accounts at the Reserve Bank. The Reserve Bank is also an NPP participant with newly developed services utilising the NPP for its government customers.

The section on the impact of weak income growth is significant, because it examines why households are under financial pressure, and the impact of this. She says “continued weak income growth presents a particular risk to the consumption outlook in the context of high household indebtedness”.

One aspect of recent developments where Australia’s experience differs, though, relates to household income and consumption. As we discussed in the Statement, consumption growth in the major advanced economies has been quite robust, supported by strong growth in employment. In Australia, we’ve also had especially strong employment growth over the past year – more than double the rate of growth in the working-age population. But that hasn’t translated into strong consumption growth. Household income growth has been weak for a number of years, and that has weighed on consumption growth (Graph 4). Consumption growth hasn’t slowed as much as income growth. This is what you’d expect, given that households generally try to smooth their consumption through episodes of income volatility. But there’s a real question of how long that could continue if income growth stays weak. This clearly has implications for how we think about the risks to our consumption forecasts.

Graph 4

The weakness in incomes goes beyond the downward pressure on wage growth that I’ve already spoken about. Yes, growth in the wage price index (WPI) has stepped down. But the WPI captures a fixed pool of jobs. It abstracts from compositional change. Average earnings as measured in the national accounts have been even weaker than the WPI (Graph 5). This has not occurred because workers shifted between industries; it is also seen within industries. It might be partly driven by the end of the mining investment boom, as workers moved out of mining-related work, including in the construction and business services industries. But it seems to have been broader than that. Our central forecast is that this weakness will end as the drag from the end of the boom dissipates and spare capacity is absorbed, such that average earnings growth recovers. There is no guarantee of this, though, and therein lies the risk.

Graph 5

The living cost pressures that many households feel have therefore been an income story, not a price inflation story. Although utilities prices did increase significantly in some states in recent quarters, much of households’ regular spending has seen relatively little in the way of price increases for a number of years.

Weak income growth can run below consumption growth for a time, but not forever. If households start to see this weakness in income growth as permanent, they are likely to change their spending patterns in response. We might be seeing this in the details of the consumption figures: growth in spending on discretionary items, like travel and eating out, has slowed while growth in spending on essentials has held up (Graph 6).

Graph 6

Continued weak income growth presents a particular risk to the consumption outlook in the context of high household indebtedness. Households do not just wake up one day and collectively decide to pay down their debt. But if incomes turn out weaker than they expect, or some other adverse news should arise, the households carrying the most debt might feel they have to rein in their spending quite a bit.

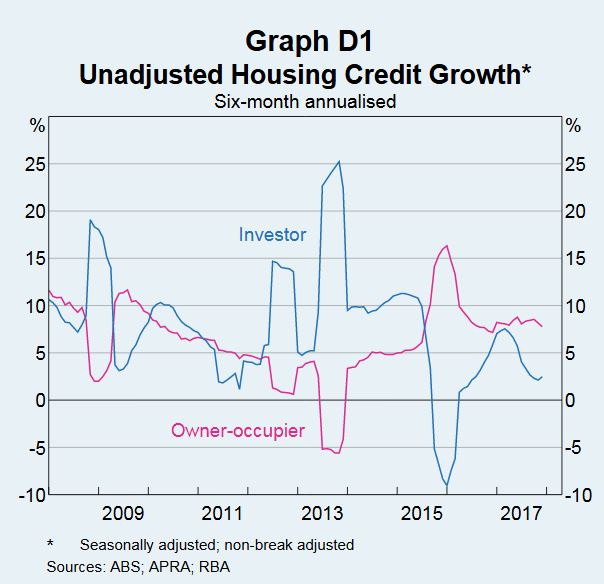

The RBA published their Statement on Monetary Policy today. The key themes were foreshadowed yesterday, but there was in interesting side discussion on the housing loans data. They says it now appears unnecessary to adjust the published growth rates to undo the effect of regular switching flows between owner occupied and investment loans. So now investor loan growth on a 6 month basis has been restated to just 2%. More fluff in the numbers!

Developments in investor and owner-occupier housing credit have attracted considerable attention in recent years. The RBA publishes these data as part of Australia’s Financial Aggregates on a monthly basis.

Measuring the Level and Growth Rate of Housing Credit

The Financial Aggregates statistical release contains data on the levels of credit extended by financial intermediaries to Australian businesses and households, including the levels of investor and owner-occupier housing credit. Sometimes, factors other than demand and supply can affect the growth of these series (Graph D1). Examples include changes in the availability of data from lenders, or changes arising from lenders reporting a reclassification of investor and owner occupier loans at a particular time. Each month, based on information provided by institutions, the RBA makes an assessment about whether any of the changes in the unadjusted data are being driven by such reporting changes. The RBA publishes growth rates adjusted to remove the effect of these breaks in order to aid the interpretation of the underlying growth in credit.

Switching Between Investor and Owner-occupier Housing Loans

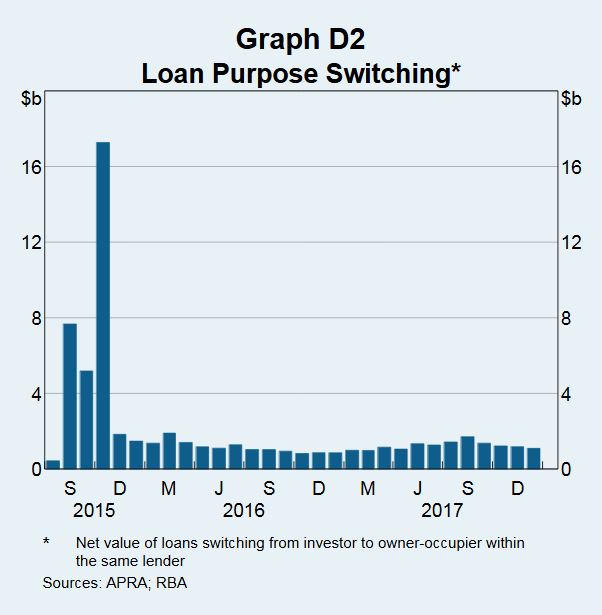

In mid 2015, some banks decided to introduce interest rate differentials between investor and owner-occupier housing loans in response to regulatory measures. For a few months thereafter, a large amount of outstanding housing credit was reported as having switched from investor to owner-occupier (Graph D2).

While the published growth rates for total housing credit were not affected by this switching, it had a substantial effect on the unadjusted growth rates of investor and owner-occupier credit. It was considered likely that many of these loans had switched purpose at some earlier date. But there was a greater incentive to report such switches after the pricing differential came into effect. So a decision was made to adjust the published growth rates for investor and owner-occupier credit to remove the effect of this switching.

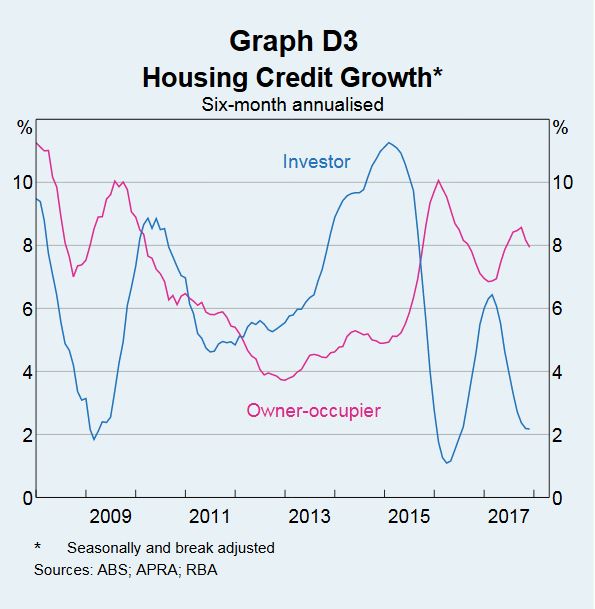

Following the large amount of switching that initially occurred around the second half of 2015, the amount of switching each month has decreased significantly and appears to have been relatively stable for some time now. Indeed, these flows appear to reflect consistent behaviour that occurs from month to month. As a result, it now appears unnecessary to adjust the published growth rates to undo the effect of these regular switching flows. Accordingly, henceforth, adjustments for switching flows will only be applied to the growth figures over the period from mid to late 2015 when reported switching was unusually large, but not thereafter. The resulting break-adjusted growth rates are shown in Graph D3. Additionally, the RBA will publish data on aggregate switching flows to assist with the understanding of this switching behaviour.

The RBA will be releasing our latest economic forecasts tomorrow in the Statement on Monetary Policy. These forecasts will be largely unchanged from the previous set of forecasts. The RBA’s central scenario remains for the Australian economy to grow at an average rate of a bit above 3 per cent over the next couple of years. This outlook has not been affected by the volatility in the stock market over recent days. Indeed, it is worth keeping in mind that the catalyst for this volatility was a reassessment in financial markets of the implications of strong growth for inflation in the United States. For some time, many investors had been working under the assumptions that unusually low inflation and unusually low volatility in asset prices would persist, even with above-trend growth at a time of low unemployment. A reassessment of these assumptions now appears to be taking place against the backdrop of strong economic conditions globally.

On Wage Growth

On balance, though, in the current environment, some pick-up in wage growth would be a welcome development. Ideally, this would be on the back of stronger productivity growth. But even if productivity growth were to be around the average of recent years, a faster rate of wage increase should be possible. Indeed, a lift in wage growth is likely to be necessary for inflation to average around the midpoint of the 2–3 per cent medium-term inflation target. Stronger growth in real wages would also boost household incomes and create a stronger sense of shared prosperity. Our central scenario is for this pick-up in wage growth to occur as the economy strengthens, but to do so only gradually. Through our liaison with business we hear some reports of wage pressures emerging in pockets where labour markets are tight. We expect that over time we will hear more such reports. After all, the laws of supply and demand still work.

Household Debt

A while back we had become quite concerned about some of the trends in household borrowing, including very fast growth in lending to investors and the high share of loans being made that did not require regular repayment of principal. Our concern was not that developments in household balance sheets posed a risk to the stability of the banking system. Rather, it was more that they posed a broader macro stability risk – that is, the day might come, when faced with bad economic news, households feel they have borrowed too much and respond by cutting their spending sharply, damaging the overall economy.

We have worked closely with APRA, including through the Council of Financial Regulators, to address these issues. This work, together with other steps taken by APRA, has helped improve the quality of lending in Australia. In the housing market, there has also been a change. National measures of housing prices are up by only around 3 per cent over the past year, a marked change from the situation a couple of years ago. This change is most pronounced in Sydney, where prices are no longer rising and conditions have also cooled in Melbourne. These changes in the housing market have reduced the incentive to borrow at low interest rates to invest in an asset whose price is increasing quickly.

On balance then, from a macro stability perspective, the situation looks less risky than it was a while ago. We do, however, continue to watch household balance sheets carefully as there are still risks here.

Rate Rises

It’s understandable that some other central banks are raising rates. They lowered their rates by more than us and, in a number of countries, the unemployment rate is now below conventional estimates of full employment at a time when above-trend growth is expected.

Our circumstances are a little different. We are still some way from what could be considered full employment and our central scenario for inflation is for it to remain below the midpoint of the medium-term target range for the next couple of years.

We expect, though, to make further progress in reducing unemployment and having inflation return to the midpoint of the target range. If we do make that progress, at some point it will be appropriate for interest rates in Australia to also start moving up. So, given recent developments in Australia and overseas, it is likely that the next move in interest rates in Australia will be up, not down. If this is how things play out, the likely timing will depend upon the extent and pace of the progress that we make. As I have discussed, while we do expect steady progress, that progress is likely to be only gradual.

As expected the RBA left the cash rate untouched again in today’s statement. For the seventeenth month in a row since August 2016.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

There was a broad-based pick-up in the global economy in 2017. A number of advanced economies are growing at an above-trend rate and unemployment rates are low. Growth has also picked up in the Asian economies, partly supported by increased international trade. The Chinese economy continues to grow solidly, with the authorities paying increased attention to the risks in the financial sector and the sustainability of growth.

The pick-up in the global economy has contributed to a rise in oil and other commodity prices over recent months. Even so, Australia’s terms of trade are expected to decline over the next couple of years, but remain at a relatively high level.

Globally, inflation remains low, although higher commodity prices and tight labour markets are likely to see inflation increase over the next couple of years. Long-term bond yields have risen but are still low. As conditions have improved in the global economy, a number of central banks have withdrawn some monetary stimulus. Financial conditions remain expansionary, with credit spreads narrow.

The Bank’s central forecast for the Australian economy is for GDP growth to pick up, to average a bit above 3 per cent over the next couple of years. The data over the summer have been consistent with this outlook. Business conditions are positive and the outlook for non-mining business investment has improved. Increased public infrastructure investment is also supporting the economy. One continuing source of uncertainty is the outlook for household consumption. Household incomes are growing slowly and debt levels are high.

Employment grew strongly over 2017 and the unemployment rate declined. Employment has been rising in all states and has been accompanied by a significant rise in labour force participation. The various forward-looking indicators continue to point to solid growth in employment over the period ahead, with a further gradual reduction in the unemployment rate expected. Notwithstanding the improving labour market, wage growth remains low. This is likely to continue for a while yet, although the stronger economy should see some lift in wage growth over time. There are reports that some employers are finding it more difficult to hire workers with the necessary skills.

Inflation is low, with both CPI and underlying inflation running a little below 2 per cent. Inflation is likely to remain low for some time, reflecting low growth in labour costs and strong competition in retailing. A gradual pick-up in inflation is, however, expected as the economy strengthens. The central forecast is for CPI inflation to be a bit above 2 per cent in 2018.

On a trade-weighted basis, the Australian dollar remains within the range that it has been in over the past two years. An appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast.

Nationwide measures of housing prices are little changed over the past six months, with prices having recorded falls in some areas. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. To address the medium-term risks associated with high and rising household indebtedness, APRA introduced a number of supervisory measures. Tighter credit standards have also been helpful in containing the build-up of risk in household balance sheets.

The low level of interest rates is continuing to support the Australian economy. Further progress in reducing unemployment and having inflation return to target is expected, although this progress is likely to be gradual. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

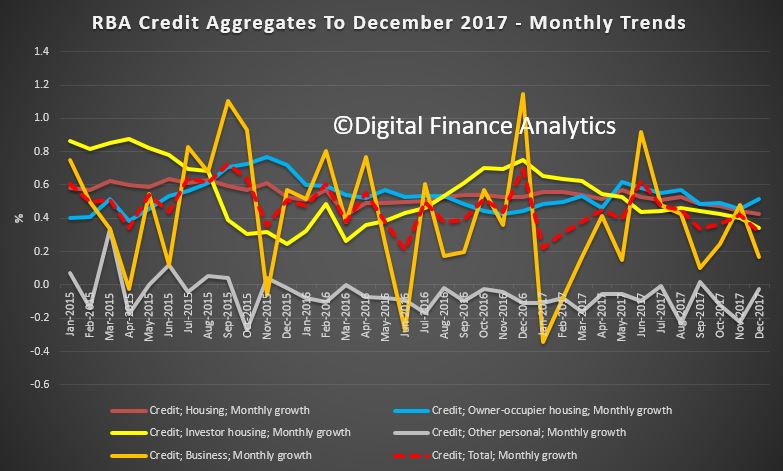

They report that lending for housing grew 6.3% for the 12 months to December 2017, the same as the previous year, and the monthly growth was 0.4%. Business lending was just 0.2% in December and 3.2% for the year, down on the 5.6% the previous year. Personal credit was flat in December, but down 1.1% over the past year, compared with a fall of 0.9% last year. This is in stark contrast to the Pay Day Loan sector, which is growing fast, as we discussed yesterday (and not in the RBA data).

Total credit grew 0.3% in the month, and 4.8% for the year, so mortgage lending is still supporting overall growth, lifting the record household debt even higher. We need still tighter regulatory controls – especially as the costs of living continue to outstrip wage growth.

The annual trends show that investor lending is slowing a little, but still stands at 6.1% seasonally adjusted. Owner occupied lending is running at 6.4% over the last year. 34.1% of loans are for investment purposes.

The monthly data is very noisy as usual.

The value of owner occupied loans was $1.13 trillion, up $6.3 billion or 0.6%, seasonally adjusted; investment loans were $587 billion up $2 billion or 0.3%, seasonally adjusted; other personal credit $151 billion, down 0.2% or 0.3 billion and business lending was $908 billion, up $0.8 billion or 0.1%.

The data contains various health warnings:

All growth rates for the financial aggregates are seasonally adjusted, and adjusted for the effects of breaks in the series as recorded in the notes to the tables listed below. Data for the levels of financial aggregates are not adjusted for series breaks. Historical levels and growth rates for the financial aggregates have been revised owing to the resubmission of data by some financial intermediaries, the re-estimation of seasonal factors and the incorporation of securitisation data. The RBA credit aggregates measure credit provided by financial institutions operating domestically. They do not capture cross-border or non-intermediated lending.

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $62 billion over the period of July 2015 to December 2017, of which $1.1 billion occurred in December 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.