More evidence that negative gearing should be revised was contained in a preliminary paper released recently, having been discussed with the RBA in November. Melbourne University researchers Yunho Cho, Shuyun May Li, and Lawrence Uren suggest their modelling shows that the removal of negative gearing would potentially lift homeownership rates by 5.5%, and that “renters and owner-occupiers are winners, but landlords, especially young with high earning landlords, lose”. They stress this is preliminary, but nevertheless it adds to the weight of evidence that negative gearing should be reformed. Their data also again shows how a small number of affluent landlords are benefiting disproportionately at the expense of the tax payer .

The welfare analysis suggests that eliminating negative gearing would lead to an overall welfare gain of 1.5 percent for the Australian economy in which 76 percent of households become better off.

This is significant, given the annual government expenditure

on negative gearing is estimated to be $2 billion, or 5 percent of the budget deficit for the year 2016. Eliminating negative gearing would reduce housing investments and house prices, and increase the average home ownership rate. The supply of rental properties falls, rents increase but only marginally because its demand also falls.

The data in their report also underlines the significant growth in property investors, and the consequential rise in mortgage lending and negative gearing.

The left panel in Figure 1 shows that the proportion of landlords has risen by around 50 percent over the last two decades. The right panel in Figure 1 shows that the real housing loan approvals have also increased dramatically during the same period. In particular, the loan approvals for investment purposes increased more sharply than that for owner-occupied purposes, surpassing it by around $0.5 billion in the early 2010s.

Figure 2 documents the proportion negatively geared landlords and the aggregate net rental income across the period from 1994 to 2015. The left panel in Figure 2 shows that the proportion of negatively geared landlords has increased from 50 percent in 1994 to around 60 percent in 2015. The right panel in Figure 2 shows that the aggregate net rental income became large negative from the early 2000s onwards. Evidence shown in Figures 1 and 2 suggest that Australian households increasingly participate in the residential property investment and take advantage of negative gearing, reducing tax obligations with the flow loss incurred from their housing investment.

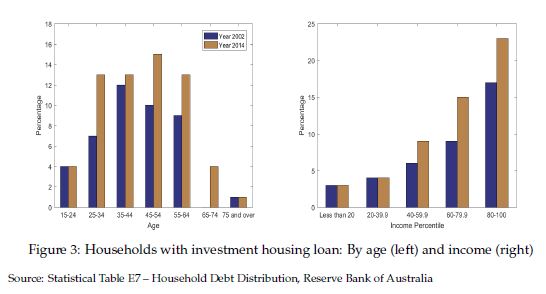

Figure 3 compares the share of households with home loans for investment by age (left panel) and income percentile (right panel) for the years 2002 and 2014. There has been a significant increase in the share, particularly among young to middle-aged households.

The largest increase was occurred in the age group 25 – 35, increased by 85 percent from 7 percent to 13 percent. From the right panel, we find that the share of households with investment housing loans has increased mainly among those in upper income percentiles.

These evidence are in line with the arguments by opponents of negative gearing that the policy essentially benefits the rich households who borrow and speculate in the property market. The fact that the distribution of housing investment loans is different across age and income also motivates our use of a heterogeneous agents incomplete markets model to study the implications of negative gearing.

Finally, of course is the important point, should interest rates rise then the value of negative gearing claimed will rise, putting a heavier burden on the Treasury, at a time when the cost of Government borrowing would be also rising. A double whammy – a multiplier effect.

The latest RBA chart pack, a distillation of data to the end of the year, contains a few gems, which underscore some of the tensions in the consumer sector.

First, relative the the ultra-low cash rate, actual mortgage rates are rising – no surprise given the rise in mortgage stress we are registering.

Next, home loan approvals are on the slide – expect more of this as tighter underwriting standards bite, and many interest only borrowers are forced to switch to higher cost interest and principal loans.

Home price indices are trending lower (but still net positive growth overall at the moment). Expect more falls in the months ahead.

Household debt continues higher. Now double disposable income, and we have some of the most highly in debt households in the world. Lending growth is still three times income, so this is likely to continue higher.

All this is bearing down on household consumption as real income growth stalls. The savings ratio is falling, as households tap these to prop up their finances, OK in the short term, but unsustainable longer term.

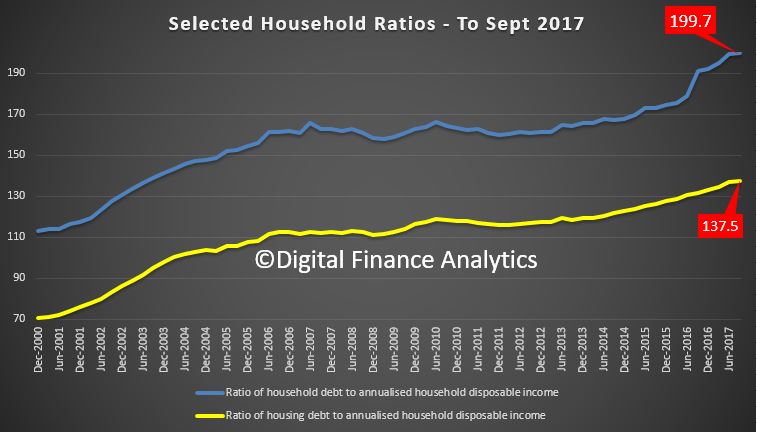

The RBA statistical tables were released just before Christmas, and it included E2 – Selected Household Ratios. This chart of the data tells the story – the ratio of debt to income deteriorated again (no surprise given the 6%+ growth in mortgage debt, and the ~2% income growth). This got hardly any coverage, until now. Since then mortgage debt is up again, so the ratio will probably cross the 200 point Rubicon next quarter.

The ratio of total debt to income is now an astronomical 199.7, and housing debt 137.5. Both are at all time records, and underscores the deep problem we have with high debt. [Note: the chart scale does not start from zero]

Granted in the current low interest rate environment repayments are just about manageable (for some), thanks to the cash rate cuts the RBA made but even a small rise will put significant pressure on households. And rates will rise.

Highly relevant given our earlier post about [US] household spending being the critical economic growth driver, Australia is no different.

The current settings will lead to many years of strain for many households. We are backed into a corner, with no easy way to exit.

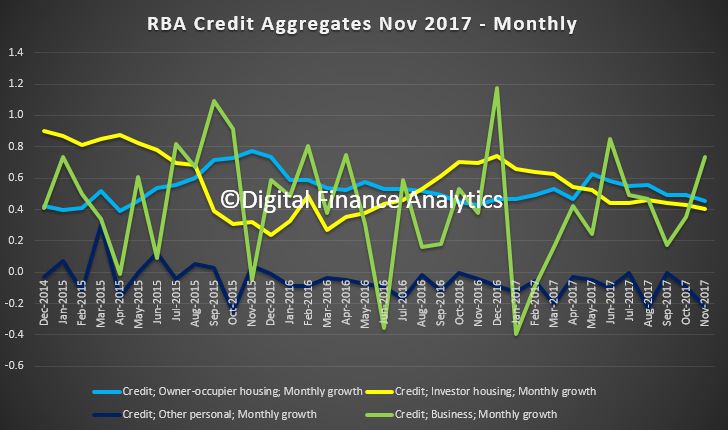

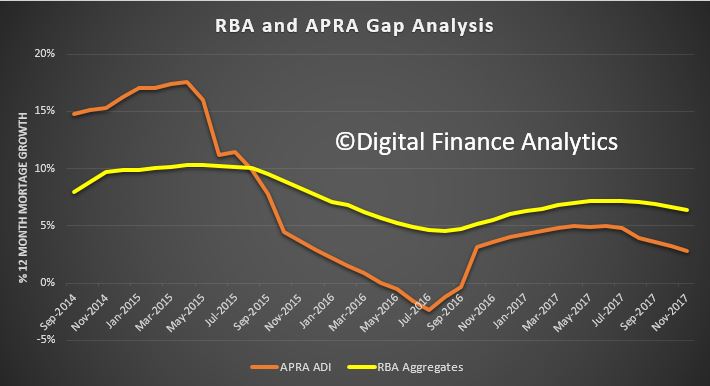

The RBA data for November 2017 was released today. The financial aggregates shows that mortgage lending momentum is easing a little, but more slowly than bank lending, suggesting that the non-bank sector is taking up much of the slack. In addition, more loans were reclassified in the month, taking the total to an amazing $61 billion. Total mortgages are now at $1.71 trillion, another record. Overall growth is still much higher than wage growth, so household debt levels will continue to climb.

The monthly trends are pretty clear, if noisy.

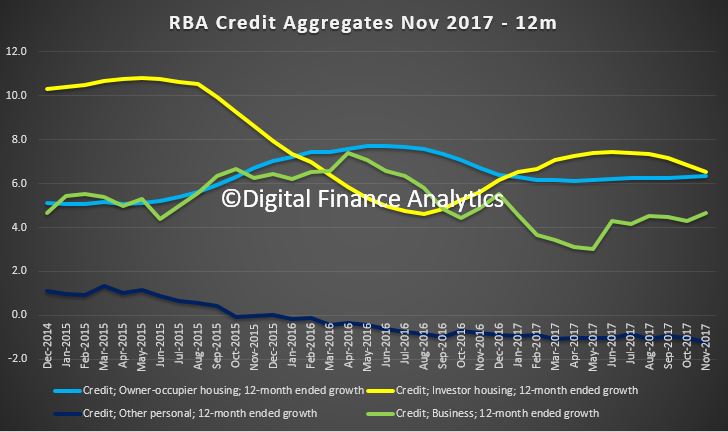

The 12 month view irons out the noise and shows that investor lending has fallen to an annual rate of 6.5%, compared with owner occupied lending at 6.3%. Total housing lending grew at 6.4%. Business lending is lower, at 4.7% and personal lending down 1.2%.

Looking at the values involved, total mortgage lending rose to $1.71 trillion, and investor loans fell to 34.1% of balances, still too high.

Two interesting points to make. First, it is clear mortgage momentum is being support by the non-bank sector, as the RBA aggregate data is significantly higher than the ADI growth from APRA. We have plotted the gap between the two on a 12 month rolling basis.

Second, there is still more “tweakage” in the numbers as loans are re-classified. Total to date now $61 billion, a large proportion of investor loans!

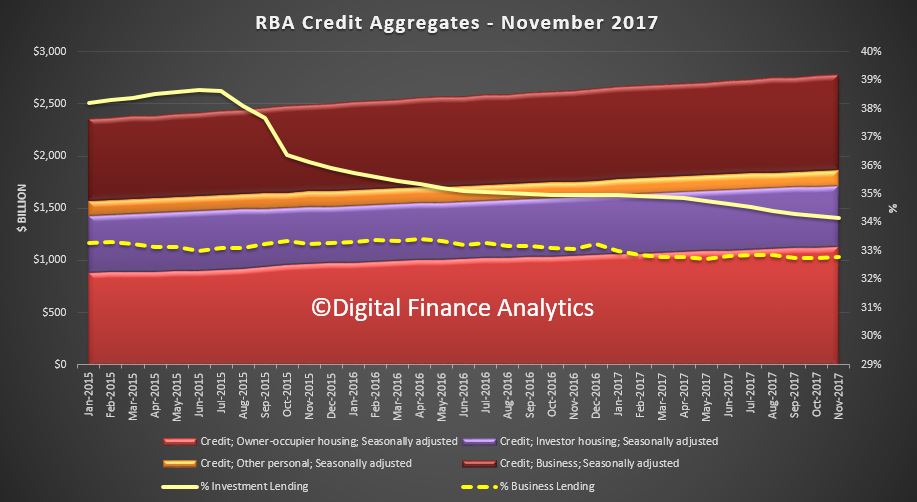

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $61 billion over the period of July 2015 to November 2017, of which $1.2 billion occurred in November 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.

The RBA published the minutes of their last meeting, when the cash rate was held, once again. There is a little more colour in their comments, but nothing has substantially changed in that where the labour market, wage and inflation trends will set their policy direction in 2018. Once again, they mention the medium-term risks associated with high and rising household indebtedness. Significant when wage growth is low, and debt high. No wonder household consumption is moderating.

International Economic Conditions

Members commenced their discussion of the global economy by noting that growth in global industrial production was likely to have increased further in October. The pick-up had been broadly based geographically. Survey measures suggested that conditions in the manufacturing sectors of Australia’s largest trading partners had continued to improve; conditions in the services sectors of the major advanced economies had remained favourable. The strength of industrial production in the high-income economies of east Asia had been associated with very strong growth in exports of electronics, specifically of semiconductors. The strength of demand in electronics-related industries had supported business investment and GDP growth in the region, particularly in South Korea.

GDP growth in the major advanced economies had been above potential, supported by accommodative monetary policies. Members noted that recent growth outcomes for the euro area had been stronger than expected. Growth in business investment had picked up in the major advanced economies over the prior year and further solid growth was anticipated over coming quarters. Consumption growth had remained above average, supported by robust growth in employment.

Conditions in labour markets in a number of major advanced economies had continued to tighten. Employment-to-population ratios had increased and unemployment rates had declined to low levels in Japan, Germany and the United States, among other advanced economies. Members noted that this implied there was limited spare capacity in these economies, based on conventional measures of full employment. However, wage growth had picked up only slightly. While observing that there were typically lags between labour markets tightening and wage pressures emerging, members noted that the wage data might suggest these economies had more spare capacity than implied by conventional measures. More generally, members noted that the nature of work was evolving, driven partly by technological change, and that not everyone was benefiting equally from the recent strength in labour demand. Low wage outcomes had contributed to core inflation in the major advanced economies remaining low, even though producer price inflation had been noticeably higher.

In China, GDP growth had been stronger than expected over the first three quarters of 2017, but more recently growth looked to have eased. This was particularly true of residential construction activity in cities where the authorities had implemented policies to address buoyant housing market conditions. The output of some sectors producing inputs for the construction sector, such as glass and steel products, had fallen in preceding months. Production shutdowns designed to deal with environmental concerns had also affected crude steel production. In combination, these factors had led to some levelling off of Chinese bulk commodity imports, including from Australia. Despite this, spot prices for iron ore had increased over the previous month and Chinese producer price inflation had remained elevated, partly reflecting stronger commodity prices. Although consumer price inflation in China had edged higher, it remained below the authorities’ objective of 3 per cent in 2017.

Domestic Economic Conditions

Members commenced their discussion of the domestic economy by noting that the wage price index continued to suggest that wage growth had been stable at a low rate. The outcome for the September quarter had been slightly lower than expected, despite the 3.3 per cent increase in award and minimum wages in the quarter, as previously determined by the Fair Work Commission. (The award system directly covers around one-quarter of the workforce.) Wage growth in the health and education sectors remained above the national average and a number of sectors had seen an increase in year-ended wage growth compared with a year prior. This had occurred at the same time as spare capacity appeared to have declined and more firms had been reporting difficulty finding suitable labour. The forecast was still for wage growth to increase gradually over the next year or so.

Labour market conditions had remained positive and had been stronger than expected over the previous year. Employment had increased a little in October and growth over the previous year had been well above average. Full-time employment had risen sharply and was growing at around its fastest pace in a decade. The participation rate was notably higher than a year earlier, particularly for women and older workers, who had been staying in the labour force for longer. The unemployment rate had edged lower to be 5.4 per cent in October, which was its lowest level since 2013, and unemployment rates had been on a downward trend in most states. Forward-looking indicators of labour demand suggested employment growth would be somewhat above average over the next few quarters.

Members noted that the September quarter national accounts would be released the day after the meeting and that recent data suggested GDP growth over the year to the September quarter was likely to have picked up to around the economy’s potential growth rate.

Information on components of household consumption indicated that growth in aggregate household consumption had moderated in the September quarter; growth in retail sales volumes and motor vehicle sales to households had been subdued. The growth in the value of retail sales in October was consistent with reports from the Bank’s liaison suggesting that moderate growth in consumption had continued into the December quarter.

Dwelling investment was expected to have fallen marginally in the September quarter. Dwelling investment had fallen over the preceding year in Queensland and Western Australia, but had remained at a high level in New South Wales and Victoria. Residential building approvals had picked up in preceding months, but remained below the levels of a few years earlier. Together with data on the pipeline of work yet to be done, this suggested that dwelling investment would remain at a high level for the following year or so, but that it was not likely to add materially to GDP growth.

Conditions had eased in the established housing market, most noticeably in Sydney, where housing prices had declined in prior months and auction clearance rates had fallen. Housing price growth had also eased in Melbourne, but remained relatively strong, supported by high population growth. Housing prices in Perth and Brisbane had been little changed in preceding months.

Members observed that business conditions in the non-mining sector had been above average for most industries over the preceding year or so and that non-mining profits had been increasing. Non-mining business investment looked to have risen further in the September quarter and the prospects for continued growth were positive: investment intentions had been revised higher, particularly for the business services sector; survey measures of capacity utilisation had remained well above average; and private non-residential building approvals had remained strong. Mining investment looked to have been little changed in the September quarter, although declines were still anticipated over the next few quarters.

Growth in public investment had picked up over the preceding few years, driven by infrastructure investment. Further growth was expected over the following couple of years, based on projections in state and federal budgets. Members considered macroeconomic modelling of a scenario under which public investment was higher than forecast for the following three years. The demand effects of this scenario included the direct contribution to GDP growth of higher public investment, as well as the multiplier effects through higher profits earned by private sector firms and the higher incomes earned by workers on these projects. Members noted the possibility of ‘crowding out’ of other forms of demand, but did not consider this a major risk given that the economy was currently operating with a degree of spare capacity and inflation was low. Indeed, a sustained pick-up in spending on public infrastructure could even ‘crowd in’ additional investment by the private sector firms undertaking those projects on the public sector’s behalf. Members also noted that the higher level of infrastructure investment could boost productivity in the economy.

Financial Markets

Members noted that conditions in financial markets generally had been little changed over the previous month, with volatility having remained at a low level throughout 2017. Financial conditions generally remained very accommodative, despite the gradual withdrawal of monetary stimulus in some economies over 2017. However, there had been a noticeable tightening in financial market conditions in China over the year, including in response to regulatory measures.

Market pricing suggested that market participants expected the US Federal Open Market Committee (FOMC) to increase the federal funds rate at its December meeting, consistent with the median of FOMC members’ projections. However, market pricing continued to suggest a more modest increase in the federal funds rate over 2018 than implied by the median FOMC projection. Members noted that previously announced changes to the composition of the FOMC had not affected market analysts’ expectations regarding the stance of US monetary policy. Regulations – particularly on smaller financial institutions – were under review, although members noted that core reforms relevant to capital, liquidity, stress testing and resolution planning were likely to be preserved.

Members observed that the yield on long-term US government bonds had been little changed over preceding months, whereas the yield on shorter-term US government bonds had increased. This in part reflected expectations for an increase in the federal funds rate and the US Treasury shifting its issuance towards securities at shorter maturities. Long-term government bond yields in other major financial markets had also generally remained little changed at low levels.

Members noted that while yields on Australian 10-year government bonds had been little changed, their spread to US Treasury bond yields had declined to a low level over preceding months.

Financing conditions remained favourable for corporations across major markets. Although spreads of high-yield corporate bonds to government bonds had increased a little in November, they remained at very low levels. Also, equity valuations remained high, having risen over 2017, although there had been small declines in some markets over November.

There had been little change in most major exchange rates over November. The US dollar had appreciated a little since early September on a trade-weighted basis, reflecting increased prospects for both future increases in the federal funds rate and US fiscal stimulus. Members noted that while the Australian dollar had depreciated by around 5 per cent in trade-weighted terms over this period, it had moved within a relatively narrow range over the previous two and a half years and was a little higher than the level of early 2016.

In China, a broad range of policy actions had contributed to a tightening in financial market conditions since late 2016 and a reduction in leverage within the financial system. Recent regulatory announcements had been directed towards managing risks in the shadow banking sector. Members noted that Chinese equity valuations had risen strongly over 2017, but had fallen somewhat in November after the authorities had signalled their concern that some stocks were overvalued.

In Australia, housing credit growth had eased a little over the second half of 2017, as growth in lending to owner-occupiers had slowed somewhat and growth in lending to investors had stabilised at a lower level than in the first half of the year. The easing in housing credit growth had been accounted for by the major banks, which had been more affected by the need to restrain interest-only lending to comply with the supervisory measures announced earlier in the year. Growth in housing lending by non-authorised deposit-taking institutions (non-ADIs) had picked up, although these institutions’ share of overall housing lending remained small. Members noted that these lenders charged higher interest rates on average than ADIs, which is likely to reflect both the borrower risk profile and higher funding costs of non-ADIs.

Issuance of residential mortgage-backed securities, which are an important source of funding for non-ADIs, had been strong in 2017 and pricing of these securities had declined a little. Major banks’ funding costs had declined a little over 2017 and long-term debt funding had grown relatively strongly in the second half of the year.

Members observed that the Australian equity market (on an accumulation basis) had risen in line with global markets over the previous couple of years and that volatility had remained low over the prior year. Australian share prices had been little changed over the preceding month, although banks’ share prices had declined, partly in response to lower-than-expected profit increases.

Financial market prices continued to imply that the cash rate was expected to remain unchanged over the following year or so.

Members concluded their review of developments in financial markets with a detailed discussion of Australian businesses’ access to finance. They noted that external finance had become available on increasingly favourable terms for large businesses over recent years, with foreign banks having added to competition for large business lending. Nevertheless, business borrowing had grown only moderately, reflecting subdued mergers and acquisitions activity, with investment having been funded largely from internal sources of funds. In contrast, many small businesses continued to find it challenging to obtain finance, particularly in their start-up or expansion phases. Members noted that this was likely to reflect the riskier nature of such lending, but also the less competitive market for small business lending. Participants on the Bank’s Small Business Finance Advisory Panel, convened annually, had confirmed the challenges of accessing bank lending. Members observed that equity funding was often more appropriate for the risk profile of start-up businesses, but that there are relatively few avenues for such financing in Australia compared with some other markets. Members were encouraged by the potential for innovations to improve access to finance for small businesses and the willingness of regulators to facilitate these developments, including in the areas of comprehensive credit reporting, open banking and alternative funding platforms.

Considerations for Monetary Policy

In considering the stance of monetary policy, members noted that conditions in the global economy had improved over 2017 and that the outlook had also been upgraded. This improvement had been supported by expansionary financial conditions, notwithstanding some withdrawal of monetary stimulus in a number of economies. In the major advanced economies, labour market conditions had continued to tighten, but wage growth and core inflation had remained low. Members recognised that this combination of strength in economic activity and low inflation was a central issue in the global economy. It was possible that this combination could continue for a while yet, but it was also possible that inflation could pick up by more than expected as spare capacity diminished.

Although the global growth outlook had improved, commodity prices and Australia’s terms of trade were expected to decline in the period ahead, but to remain at relatively high levels. The Australian dollar had continued to fluctuate within its range of the preceding two and a half years. An appreciating exchange rate would be expected to result in a slower pick-up in domestic economic activity and inflation than currently forecast.

Members noted that the low level of interest rates had been supporting the Australian economy. Recent data suggested that GDP growth had been around its trend rate over the year to the September quarter. Output growth was still expected to pick up gradually over the forecast period. Business conditions were positive and capacity utilisation had remained high. The outlook for non-mining business investment had improved further and the pick-up in public infrastructure investment was also supporting overall growth. However, growth in consumption was expected to have slowed in the September quarter and the outlook for household consumption continued to be a significant risk, given that household incomes were growing slowly and debt levels were high.

Growth in employment, particularly full-time employment, had increased and the unemployment rate had fallen to a four-year low. Although wage growth had been a little lower than expected in the September quarter, it appeared to have stabilised at a low rate. Leading indicators of labour demand had been broadly consistent with continuing strength in the labour market. In these circumstances, spare capacity in the labour market was expected to be absorbed gradually and wage growth was expected to pick up over time.

Housing market conditions had generally eased, especially in Sydney. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. To address the medium-term risks associated with high and rising household indebtedness, the Australian Prudential Regulation Authority had introduced a number of supervisory measures earlier in the year and credit standards had been tightened to lower the risk profile of borrowers. Growth in household credit had slowed somewhat, but members agreed that household balance sheets still warranted careful monitoring.

Over the prior year or so, the unemployment rate had fallen and inflation had moved closer to target. Members noted that this had occurred at the same time as risks in household balance sheets had lessened. Recent data had increased confidence that there would be further progress on these fronts over the following year. How far and when stronger conditions in the economy and labour market might feed through into higher wage growth and inflation remained important considerations shaping the outlook. Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

The Decision

The Board decided to leave the cash rate unchanged at 1.5 per cent.

The RBA’s Tony Richards, Head of Payments Policy spoke at the Australian Payment Summit 2017 and discussed the vexed issue of Least Cost Routing for EFTPOS transactions, especially when using Tap-and-Go. Until very recently, acquirers have indicated reluctance to provide least-cost routing to their merchant customers. This is partly due to the expected systems work, including to reprogram terminals. But pressure is mounting, as for example, the recent House of Reps report.

He says indications are that all four of the major banks are moving to providing least-cost routing if requested by merchants, though in some cases they have indicated this could occur on a fairly extended timetable.

So, merchants, do yourself a favour, and ask! You may save on your transaction costs!

Given that payment costs are a significant item for merchants, it is not surprising that merchants pay attention to them. Just as merchants are keen to hold down other business costs, they are also keen to hold down their payment costs. Recently, they have drawn attention to a particular issue that is driving up their cost of payments.

The majority of debit cards issued in Australia are now dual-network cards, which means that authorisation of cardholders’ debit transactions can occur through different networks – the domestic eftpos network or the debit networks of the international MasterCard or Visa schemes. If you look at your debit or ATM card, there is a good chance it will have an international scheme logo on one side and the eftpos logo on the other.

Traditionally, cardholders have determined how their debit transactions are processed, by pressing either the CHQ or SAV buttons for eftpos or the CR button for the international network, before entering their PIN. However, with the shift to contactless or ‘tap-and-go’ transactions, the processing of debit transactions has been shifting to the international networks. This initially reflected the fact that contactless payments were only available for the international schemes. Most cards and terminals are now also activated for eftpos contactless functionality. However, when card-issuing banks send out dual-network debit cards they are programmed with the international scheme as the first-priority network for contactless use and the eftpos network as second priority.

Most cardholders are indifferent about which network processes their contactless transactions. Both networks can link to the same debit account and cardholders do not directly bear the costs of the transactions. Moreover, there are typically no rewards programs associated with debit transactions, and customers receive similar protections from fraud and disputed transactions, based on the ePayments Code and the chargeback policies of the three schemes.

However, many merchants have a preference for transactions to be processed via the eftpos network, because it is typically less expensive for them. Accordingly, many merchants have been calling for their acquirer banks to provide them with ‘least-cost routing’, i.e., terminal functionality that sends contactless debit transactions via the lower-cost network. Terminals might be programmed to always send dual-network card transactions via a particular network or they might use dynamic rules which identify the lower-cost network for each transaction.

The Bank has had discussions with consumer organisations and staff from the Australian Competition and Consumer Commission (ACCC) as to how least-cost routing might be implemented. We consider that it would be desirable for a merchant implementing least-cost routing to disclose this to customers. Depending on how terminals were actually programmed, this could be by a sign that the merchant will typically send tap-and-go debit card transactions via a certain network, but noting that customers wishing to send transactions via a different network could insert or dip their cards and push the button or keypad for their preferred network. A sign such as this would provide consumers with the opportunity to override the merchant’s preferred network if they wished. Such a framework would seem to be a reasonable balance between the rights of merchants and consumers, and it is likely that consumers would quickly become used to the idea that their transactions could be sent via different networks at different merchants.

The Reserve Bank has taken an interest in dual-network card issues because of the Payments System Board’s mandate to promote competition and efficiency. As the Bank and other observers of the payments system have frequently noted, the nature of competition in the payment card market is often such that it tends to drive up costs to merchants, as schemes increase their interchange fees to persuade issuers to issue their cards. Merchants have typically had little ability to offset these pressures (in the absence of regulatory intervention to cap interchange fees or remove schemes’ no-surcharge rules). However, dual-network cards can potentially offset the pressures for payment costs to rise, because the merchant may be able to steer the consumer to use the lower-cost of the two networks on a card. Accordingly, the Bank has indicated that it supports the issue of such cards in Australia, because they are convenient for cardholders and allow stronger competition between networks at the point of sale, facilitating both consumer and merchant choice.

Some disputes over dual-network debit cards emerged between the debit schemes in 2012-13. However, after a series of discussions with the Bank, in August 2013 the three debit schemes made voluntary undertakings to the Bank that addressed some policy concerns. These included commitments:

to work constructively to allow issuers to include applications from two networks on the same card and chip, where issuers wished to do this;

not to prevent merchants from exercising choice in the networks they accept, in both the contact and contactless environments; and

not to prevent merchants from exercising their own transaction routing priorities when there are two contactless debit applications on one card.

As noted above, most terminals and eftpos cards are now enabled for tap-and-go eftpos transactions. Given the Bank’s views about the potential competition and efficiency benefits of dual-network cards, as well as the earlier commitments by the three debit schemes, the Bank has been liaising with a range of stakeholders over recent months to encourage the provision of least-cost routing functionality to merchants.

However, until very recently, acquirers have indicated reluctance to provide least-cost routing to their merchant customers. This is partly due to the expected systems work, including to reprogram terminals.

In addition, some merchants have expressed concern to the Bank that the international schemes might resist the implementation of least-cost routing. To the extent that transactions via the international schemes are currently more expensive to merchants, a possible outcome of least-cost routing becoming available would be for the international schemes to reduce scheme or interchange fees so that merchants have little incentive to send transactions via another network. However, some merchants are concerned about other possible responses, including that the international schemes might respond to a merchant’s decision to implement least-cost routing of debit transactions by increasing the interchange rates that apply to the merchant’s credit transactions. They have also noted that the international schemes might try to preclude least-cost routing by attempting to persuade issuers to stop issuing dual-network cards. The ACCC is aware of these concerns, and is closely monitoring the situation. With the passage of the Harper reforms, which came into effect in November this year, the ACCC now has even stronger powers to investigate and take action in relation to conduct by the international schemes that might hinder competitive conduct by a lower-cost provider.

The Payments System Board has discussed issues involving dual-network cards in recent meetings. At its 17 November meeting, the Board strongly supported calls from a range of stakeholders for acquirers to provide merchants with least-cost routing functionality for contactless transactions using dual-network debit cards. It requested the Bank staff to continue to engage with the payments industry on this issue, noting that ‘a prompt industry solution was preferable to regulation’.

More recently, the Review of the Four Major Banks by the House of Representatives Standing Committee on Economics has made the following recommendation:

“The committee recommends that banks be required to give merchants the ability to send tap-and-go payments from dual-network debit cards through the channel of their choice.

Merchants should be able to choose whether to route these transactions through eftpos or another channel, noting that consumers may override this merchant preference if they choose to do so.

If the banks have not facilitated this recommendation by 1 April 2018, the Payments System Board should take regulatory action to require this to occur.”

Recent indications are that all four of the major banks are moving to providing least-cost routing if requested by merchants, though in some cases they have indicated this could occur on a fairly extended timetable. We expect that some of the smaller acquirers may be able to move more quickly.

Accordingly, the Bank expects that by early in 2018 there will be concrete indications that a critical mass of acquirers are moving to provide least-cost routing and that the international schemes are not attempting to prevent this. However, if this expectation is not met, I expect that the Payments System Board will consider consulting on a regulatory solution that deals with all the relevant considerations. While of course the measures that could be consulted on will be determined by the Board, I can imagine that this could involve considering whether some or all of the following measures might be in the public interest:

a requirement that acquirers must provide merchants with least-cost routing functionality for contactless dual-network debit card transactions

a requirement for enhanced transparency in contractual pricing of acquiring services to merchants

requirements that schemes publish explicit criteria for any preferred or strategic interchange fees and that any such criteria may not be related to acceptance decisions relating to other payment systems

anti-avoidance provisions that ensure adherence to the spirit, as well as the letter, of any standard.

Australia’s housing market is cooling after years of rollicking price growth.

Annual price growth has halved since May, auction clearance rates sit at multi-year lows in Sydney and Melbourne and investor housing credit is declining, coinciding with tougher restrictions on interest-only lending from APRA, Australia’s banking regulator, introduced in March.

The slowdown in the housing market, coming on top of weakness in Australia’s household sector seen in Australia’s recent GDP report, has got many people questioning whether the Reserve Bank of Australia (RBA) should hike interest rates given the current set of circumstances, especially with inflationary pressures close to non-existent.

Rather than hiking interest rates, some have even floated the idea that the RBA may consider cutting interest rates given the sharp deceleration in the housing market.

George Tharenou and Carlos Cacho, Economists at UBS, played devils advocate on that front earlier this month, pointing to the chart below to show that when house prices weakened by a similar amount in the past, it has almost always resulted in the RBA cutting official interest rates.

The pair note that national price growth on a six-month annualised basis is currently running at just 0.7%, an important consideration given that over the past 30 years “when house prices over a 6-month period weakened towards flat or negative, the RBA cut within a few months in 7 of 9 cycles”.

While that’s not UBS’ official call, forecasting instead that the RBA will hike rates in late 2018 with the risks slanted towards a later move, it does pose the question as to whether the current weakness in the housing market will see history repeat.

To ANZ Bank’s Australian economics team, led by David Plank, the answer to that question is almost certainly no.

“There has been quite a lot of focus on the current downturn in house price inflation, with some commentators pointing out that similar downturns in the past have been followed by RBA rate cuts,” the bank says.

“While this might be true, it ignores the key differences between this cycle and previous downturns.

“In particular, previous downturns in house prices followed a succession of RBA rate increases, which pushed mortgage rates sharply higher. Given that RBA tightening cycles typically impact a lot more across the economy than just house prices, we think it is difficult to argue that the slowdown in house price inflation was the primary reason for eventual rate cuts.

“We think a rising unemployment rate was far more important,” it says.

One look at the charts below adds credence to that view.

The first looks at the relationship between annual house price growth and mortgage rates. The latter, shown in orange, has been inverted and advanced by six months.

As opposed to what has been seen previously when house prices tended to decline following a series of interest rate hikes, in recent times, price growth has slowed despite mortgage rates remaining near the lowest levels on record, coinciding with tighter macroprudential restrictions on investor and interest-only lending from APRA.

“The current downturn in house prices has not come after a tightening cycle. Instead we think the most likely cause was the tightening in credit, though with a lag and interrupted by the impact of RBA rate cuts in 2016,” ANZ says.

In comparison, this next chart shows the relationship between the annual change in Australia’s unemployment rate to movements in the cash rate.

While not perfect by any stretch, when unemployment starts to lift, the RBA tends to cut the cash rate, and vice versus.

Australia’s unemployment rate has recently fallen to 5.4%, leaving it at the lowest level in close to five years, going someway to explaining why ANZ is forecasting that the RBA will lift the cash rate to 2% by the end of next year despite the slowdown in the housing market.

“In our view, a [housing] cycle driven by credit is likely to play out very differently from one driven by higher interest rates,” it says.

“Expecting the current housing cycle to play out like those caused by movements in interest rates, strikes us as likely to end in disappointment.”

Indeed, outside of the recent price deceleration caused by credit rather than mortgage rates, ANZ points to a variety of other housing market indicators that suggest there’s little need for the RBA to cut rates.

“The most recent data on auction clearance rates suggest some stability after a period of decline. If this broadly continues then we would expect house annual price inflation to stabilise in the low-to-mid single digits in 2018,” it says.

“Our forecasts have nationwide house price inflation slowing to zero in 2018, but this also includes the impact of the two RBA rate hikes we expect in 2018. If these don’t take place then we would expect less of a slowdown in housing inflation, probably to the low-to-mid single digits mentioned above.”

ANZ says recent strength in Australian building approvals data, supporting the view that credit cycles play out differently from rate hike cycles, provides further evidence why RBA rate cuts are not required on this occasion.

“In late 2016, when approvals were falling sharply, there were a number of dire predictions about what that would mean for housing construction and employment. But it has been clear for some time that the downturn in building approvals was shallower than in previous cycles,” it says.

“We think this is because this cycle was not triggered by higher interest rates. Instead, we think a more likely cause was the tightening in credit that began in 2015.”

According to the ABS, Australian building approvals rose by 0.9% to 19,074 in seasonally adjusted terms in October, leaving the increase on a year earlier at 18.4%. Private sector approvals for houses and other dwellings stood at 10,063 and 8,683, up 6.2% and 37.6% respectively from 12 months earlier.

Given the absence of weakness in other areas of the housing market, differing it from periods in the past when interest rates were cut, it helps explain why ANZ and the vast majority of forecasters believe that the next move in the cash rate will be higher, albeit not for many months.

Christopher Kent, RBA Assistant Governor (Financial Markets), spoke at the 30th Australasian Finance and Banking Conference on The Availability of Business Funding, a subject which was featured in the recent RBA Bulletin.

While his speech covered the gamut of business finance, his comments on small business are important. He acknowledged the need for, and difficulty of getting funding in this sector. Something we have highlighted in our SME Report series, and which are still available. Whilst alternative lenders (Fintechs for example) have a role to play, (and there is massive opportunity in the SME sector in our view), most SME’s still go to the banks, where they have to pay more, for poor products and service. Indeed, if you are a business owner seeking to borrow, without a property to secure against, the options are limited. This is because the banks’ view is, correctly, unsecured risks are higher than secured, and in any case, they prefer to lend to mortgage holders more generally, as the capital required to do so is lower. Therefore many SME’s are at a structural disadvantage, and often end up having to pay very higher interest rates, if they can get finance at all.

There is much to do, in my view, to address the funding needs of SMEs, and this is a critical requirement if we are to seen sustained real economic growth. As Kent suggests, perhaps Open Banking will assist, eventually!

The challenge of obtaining finance has been a consistent theme of the Small Business Finance Advisory Panel. In this context, it is important to distinguish between two types of small businesses. First, there are the many established small businesses that are not expanding. Their needs for external finance are typically modest. Second, there are small businesses that are in the start-up or expansion phase. They are not generating much in the way of internal funding. Accordingly, those businesses have a strong demand for external finance. I’ll focus my comments on the issues relevant to this second group of small businesses.

I should emphasise again that access to finance for small businesses is important because they generate employment, drive innovation and boost competition in markets. Indeed, small businesses in Australia employ almost 5 million people, which is nearly half of employment in the (non-financial) business sector. They also account for about one-third of the output of the business sector.

Compared with larger, more established firms, smaller, newer businesses find it difficult to obtain external finance since they are riskier on average and there is less information available to lenders and investors about their prospects. Lenders typically manage these risks by charging higher interest rates than for large business loans, by rejecting a greater proportion of small business credit applications or by providing credit on a relatively restricted basis.

The reduction in the risk appetite of lenders following the global financial crisis appears to have had a more significant and persistent effect on the cost of finance for small business than large business. After the crisis, the average spread of business lending rates to the cash rate widened dramatically. The increase was much larger and more persistent, though, for small business loans (Graph 9). In part, this increase owed to the larger increase in non-performing loans for small businesses than for large business lending portfolios (Graph 10). It’s not clear, however, whether the increase in interest rates being charged on small business loans relative to those charged on large business loans (over the past decade or so) reflects changes in the relative riskiness of the two types of loans.[11]

Graph 9

Graph 10

Over recent years, there has been strong competition for large business lending, which has resulted in a decline in the interest rate spread on large business loans. Part of the competition from banks for large business loans has been driven by an expansion in activity by foreign banks. Large businesses also have access to a wider array of funding sources than small businesses, including corporate bond markets and syndicated lending.

In contrast, competition has been less vigorous for small business lending. Indeed, some providers of small business finance were acquired by other banks or exited the market following the onset of the crisis. Also, the interest rates on small business loans have remained relatively high. This difference in competitive pressures is evident in the share of lending provided to small business by the major banks, which is relatively high at over 80 per cent. This compares with a share of around two-thirds in the case of large businesses. Small businesses continue to use loans from banks for most of their debt funding because it is often difficult and costly for them to raise funds directly from capital markets.

The RBA’s liaison has highlighted that if small business borrowers are able to provide housing as collateral, it significantly reduces the cost and increases the availability of debt finance. Lenders have indicated that at least three-quarters of their small business lending is collateralised and they only have a limited appetite for unsecured lending. However, there are a number of reasons why entrepreneurs find it difficult to provide sufficient collateral for business borrowing via home equity:

they may actually not own a home, or have much equity in their home if they are relatively young;

similarly, they may not have sufficient spare home equity if they’ve already borrowed against their home to establish a business and now want to expand their business;

and even if they have plenty of spare home equity, using their homes as collateral concentrates the risk they face in the event of the failure of the business.

Many entrepreneurs have limited options for providing alternative collateral, since banks are far more likely to accept physical assets (such as buildings or equipment), rather than ‘soft’ assets, such as software and intellectual property.

Given the higher risk associated with small businesses, particularly start-ups, equity financing would appear to be a viable alternative to traditional bank finance. However, small businesses often find it difficult to access equity financing beyond what is issued to the business by the founders. Small businesses have little access to listed equity markets, and while private equity financing is sometimes available, its supply to small businesses is limited in Australia, particularly when compared with the experience of other countries (Graph 11). Small businesses also report that the cost of equity financing is high, and they are often reluctant to sell equity to professional investors, since this usually involves relinquishing significant control over their business.

Graph 11

Innovations Improving Access to Business Finance

There are several innovations that could help to improve access to finance by: providing lenders with more information about the capacity of borrowers to service their debts, and connecting risk-seeking investors with start-up businesses that could offer high returns.

Comprehensive credit reporting

Comprehensive credit reporting will provide more information to lenders about the credit history of potential borrowers. The current standard only makes negative credit information publicly available. When information about credit that has been repaid without problems also becomes available publicly, the cost of assessing credit risks will be reduced and lenders will be able to price risk more accurately; this may enhance competition as the current lender to any particular business will no longer have an informational advantage over other lenders. It may also reduce the need for lenders to seek additional collateral and personal guarantees for small business lending, particularly for established businesses. Indeed, the use of personal guarantees is more widespread in Australia than in countries that have well-established comprehensive credit reporting regimes, such as the United Kingdom and the United States.

For several years, the finance industry has attempted to establish a voluntary comprehensive credit reporting regime in Australia. Participation has so far been limited.[13] However, several of the major banks have committed to contribute their credit data in coming months. The Australian Government has announced that it will legislate for a mandatory regime to come into effect mid next year.

Open banking

The introduction of an open banking regime should make it easier for entrepreneurs to share their banking data (including on transactions accounts) securely with third-party service providers, such as potential lenders. When assessing credit risks, lenders place considerable weight on evidence of the capacity of small business borrowers to service their debts based on their cash flows. For this reason, making this data available via open banking would reduce the cost of assessing credit risk. A review is currently being conducted with a view to introducing legislation to support an open banking regime.

Large technology companies

Technology firms can use the transactional data from their platforms to identify creditworthy borrowers, and provide loans and trade credit to these businesses from their own balance sheets. This could supply small innovative businesses that are active on these online platforms with a new source of finance. Amazon and Paypal are providing finance to some businesses that use their platforms. For example, Amazon identifies businesses with good sales histories and offers them finance on an invitation-only basis. Loans are reported to range from US$1 000 to US$750 000 for terms of up to a year at interest rates between 6 and 14 per cent. Repayments are automatically deducted from the proceeds of the borrower’s sales.

Alternative finance platforms

Alternative finance platforms, including marketplace lending and crowdfunding platforms, use new technologies to connect fundraisers directly with funding sources. The aim is to avoid the costs and delays involved in traditional intermediated finance.

While alternative financing platforms are growing rapidly, they are still a very minor source of funding for businesses, including in Australia. The largest alternative finance markets are in China, followed by the United States and the United Kingdom. But even these markets remain small relative to the size of their economies (Graph 12).

Graph 12

Marketplace lending platforms provide debt funding by matching individuals or groups of lenders with borrowers. These platforms typically target personal and small business borrowers with low credit risk by attempting to offer lower cost lending products and more flexible lending conditions than traditional lenders. Data collected by the Australian Securities and Investments Commission indicate that most marketplace lending in Australia is for relatively small loans to consumers at interest rates comparable to personal loans offered by banks (Graph 13).

Graph 13

It is unclear whether marketplace lending platforms are significantly reducing financial constraints for small businesses. Unlike innovations such as comprehensive credit reporting, which have the potential to improve the credit risk assessment process, marketplace lenders do not have an information advantage over traditional lenders. As a result, they need to manage risks with prices and terms in line with traditional lenders. Nevertheless, these platforms could provide some competition to traditional lenders, particularly as a source of unsecured short-term finance, since they process applications quickly and offer rates below those on credit cards.

Crowdfunding platforms have the potential to make financing more accessible for start-up businesses, although their use has been limited to date. Crowdsourced equity funding platforms typically involve a large number of investors taking a small equity stake in a business. As a result, entrepreneurs can receive finance without having to give up as much control as expected by venture capitalists. Several legislative changes have been made to facilitate growth in these markets, including by allowing small unlisted public companies to raise crowdsourced equity.

RBA Governor Philip Lowe spoke at the 2017 Australian Payment Summit and explored some of the disruption in the payments system, including falling cash transactions, an eAUD, electronic bank notes and distributed ledger systems. He also said that a convincing case for issuing Australian dollars on the blockchain for use with limited private systems has not yet been made.

A clear lesson from history is that as people’s needs change and technology improves, so too does the form that money takes. Once upon a time, people used clam shells and stones as money. And for a while, right here in the colony of New South Wales, rum was notoriously used. For many hundreds of years, though, metal coins were the main form of money. Then, as printing technology developed, paper banknotes became the norm. The next advance in technology – developed right here in Australia – was the printing of banknotes on polymer.

No doubt, this evolution will continue. Though predicting its exact nature is difficult. But as Australia’s central bank, the RBA has been giving considerable thought as to what the future might look like. We are the issuer of Australia’s banknotes, the provider of exchange settlement accounts for the financial sector, and we have a broad responsibility for the efficiency of the payments system, so this is an important issue for us.

Today I want to share with you some of our thinking about this future and to address a question that I am being asked increasingly frequently: does the RBA intend to issue a digital form of the Australian dollar? Let’s call it an eAUD.

The short answer to this question is that we have no immediate plans to issue an electronic form of Australian dollar banknotes, but we are continuing to look at the pros and cons. At the same time, we are also looking at how settlement arrangements with central bank money might evolve as new technologies emerge.

As we have worked through the issues, we have developed a series of working hypotheses. I would like to use this opportunity to outline these hypotheses and then discuss each of them briefly. As you will see, we have more confidence in some of these than others.

There will be a further significant shift to electronic payments, but there will still be a place for banknotes, although they will be used less frequently.

It is likely that this shift to electronic payments will occur largely through products offered by the banking system. This is not a given, though. It will require financial institutions to offer customers low-cost solutions that meet their needs.

An electronic form of banknotes could coexist with the electronic payment systems operated by the banks, although the case for this new form of money is not yet established. If an electronic form of Australian dollar banknotes was to become a commonly used payment method, it would probably best be issued by the RBA and distributed by financial institutions, just as physical banknotes are today.

Another possibility that is sometimes suggested for encouraging the shift to electronic payments would be for the RBA to offer every Australian an exchange settlement account with easy, low-cost payments functionality. To be clear, we see no case for doing this.

It is possible that the RBA might, in time, issue a new form of digital money – a variation on exchange settlement accounts – perhaps using distributed ledger technology. This money could then be used in specific settlement systems. The case for doing this has not yet been established, but we are open to the idea.

So these are our five working hypotheses. I would now like to expand on each of these.

1. The Shift to Electronic Payments

An appropriate starting point is to recognise that most money is already digital or electronic. Only 3½ per cent of what is known as ‘broad money’ in Australia is in the form of physical currency. The rest is in the form of deposits, which, most of the time, can be accessed electronically. So the vast majority of what we know today as money is a liability of the private sector, and not the central bank, and is already electronic.

With most money available electronically, there has been a substantial shift to electronic forms of payments as well. There are various ways of tracking this shift.

One is the survey of consumers that the RBA conducts every three years. When we first conducted this survey in 2007, we estimated that cash accounted for around 70 per cent of transactions made by households. In the most recent survey, which was conducted last year, this share had fallen to 37 per cent (Graph 1).

Graph 1

A second way of tracking the change is the decline in cash withdrawals from ATMs. The number of withdrawals peaked in 2008 and since then has fallen by around 25 per cent (Graph 2). This trend is likely to continue.

Graph 2

The third area where we can see this shift is the rapid growth in the number of debt and credit card transactions and in transactions using the direct entry system. Since 2005, the number of transactions using these systems has grown at an average annual rate of 10 per cent (Graph 3). This stands in contrast to the decline in the use of cash and cheques.

Graph 3

The overall picture is pretty clear. There has been a significant shift away from people using banknotes to making payments electronically. Most recently, Australia’s enthusiastic adoption of ‘tap-and-go’ payments has added impetus to this shift. In many ways, Australians are ahead of others in the use of electronic payments, although we are not quite in the vanguard. It is also worth pointing out, though, that despite this shift to electronic payments, the value of banknotes on issue is at a 50-year high as a share of GDP (Graph 4). Australians are clearly holding banknotes for purposes other than for making day-to-day payments.

Graph 4

This shift towards electronic payments, and away from the use of banknotes for payments, will surely continue. This will be driven partly by the increased use of mobile payment apps and other innovations. At the same time, though, it is likely that banknotes will continue to play an important role in the Australian payments landscape for many years to come. For many people, and for some types of transactions, banknotes are likely to remain the payment instrument of choice.

2. Banks are likely to remain at the centre of the shift to electronic payments

In Australia, the banking system has provided the infrastructure that has made the shift to electronic payments possible. In some other countries, the banking system has not done this. For example, in China and Kenya non-bank entities have been at the forefront of recent strong growth in electronic payments. A lesson here is that if financial institutions do not respond to customers’ needs, others will.

At this stage, it seems likely that the banking system will continue to provide the infrastructure that Australians use to make electronic payments. This is particularly so given the substantial investment made by Australia’s financial institutions in the NPP. The new system was turned on for ‘live proving’ in late November and the public launch is scheduled for February. It will allow Australians to make payments easily on a 24/7 basis, with recipients having immediate access to their money. The RBA has built a critical part of this infrastructure to ensure interbank settlement occurs in real time. Payments will be able to be made by just knowing somebody’s email address or mobile phone number and plenty of information will be able to be sent with the payment. This system has the potential to be transformational and will allow many transactions that today are conducted with banknotes to be conducted electronically.

Importantly, the new system offers instant settlement and funds availability. It provides this, while at the same time allowing funds to be held in deposit accounts at financial institutions subject to strong prudential regulation and that pay interest. This combination of attributes is not easy to replicate, including by closed-loop systems outside the banking system.

However, the further shift to electronic payments through the banking system is not a given. It requires that the cost to consumers and businesses of using the NPP is low and that the functionality expands over time. If this does not happen, then the experience of other countries suggests that alternative systems or technologies might emerge.

One class of technology that has emerged that can be used for payments is the so-called cryptocurrencies, the most prominent of which is Bitcoin. But in reality these currencies are not being commonly used for everyday payments and, as things currently stand, it is hard to see that changing. The value of Bitcoin is very volatile, the number of payments that can currently be handled is very low, there are governance problems, the transaction cost involved in making a payment with Bitcoin is very high and the estimates of the electricity used in the process of mining the coins are staggering. When thought of purely as a payment instrument, it seems more likely to be attractive to those who want to make transactions in the black or illegal economy, rather than everyday transactions. So the current fascination with these currencies feels more like a speculative mania than it has to do with their use as an efficient and convenient form of electronic payment.

This is not to say that other efficient and low-cost electronic payments methods will not emerge. But there is a certain attraction of being able to make payments from funds held in prudentially regulated accounts that can earn interest.

3. Electronic banknotes could coexist with the electronic payment system operated by the banks

In principle, a new form of electronic payment method that could emerge would be some form of electronic banknotes, or electronic cash. The easiest case to think about is a form of electronic Australian dollar banknotes. Such banknotes could coexist with the electronic account-to-account-based payments system operated by the banks, just as polymer banknotes coexist with the electronic systems today.

The technologies for doing this on an economy-wide scale are still developing. It is possible that it could be achieved through a distributed ledger, although there are other possibilities as well. The issuing authority could issue electronic currency in the form of files or ‘tokens’. These tokens could be stored in digital wallets, provided by financial institutions and others. These tokens could then be used for payments in a similar way that physical banknotes are used today.

In thinking about this possibility there are a couple of important questions that I would like to highlight.

The first is that if such a system were to be technologically feasible, who would issue the tokens: the RBA or somebody else?

The second is whether the RBA developing such a system would pass the public interest test.

In terms of the issuing authority, our working hypothesis is that this would best be done by the central bank.

In principle, there is nothing preventing tokenised eAUDs being issued by the private sector. It is conceivable, for example, that eAUD tokens could be issued by banks or even by large non-banks, although it is hard to see them being issued as cryptocurrency tokens under a bitcoin-style protocol, with no central entity standing behind the liability. So, while a privately issued eAUD is conceivable, experience cautions that there are significant difficulties and dangers associated with privately issued fiat money.

The history of private issuance is one of periodic panic and instability. In times of uncertainty and stress, people don’t want to hold privately issued fiat money. This is one reason why today physical banknotes are backed by central banks. It is possible that ways might be found to deal with this financial stability issue – including full collateralisation – but these tend to be expensive. This suggests that if there were to be an electronic form of banknotes that was widely used by the community, it is probably better and more likely for it to be issued by the central bank.

If we were to head in this direction, there would be significant design issues to work through. The tokens could be issued in a way that transactions could be made with complete anonymity, just as is the case with physical banknotes. Alternatively, they might be issued in a way in which transactions were auditable and traceable by relevant authorities. We would also need to deal with the issue of possible counterfeiting. Depending upon the design of any system, we might be very reliant on cryptography and would need to be confident in the ability to resist malicious attacks.

This brings me to the second issue here: is there a public policy case for moving in this direction?

Such a case would need to be built on electronic banknotes offering something that account-to-account transfers through the banking system do not. We would also need to be confident that there were not material downsides from moving in this direction.

Our current working hypothesis is that with the NPP there is likely to be little additional benefit from electronic banknotes. This, of course, presupposes that the NPP provides low-cost efficient payments. One possible benefit of electronic banknotes for some people might be that they could have less of an ‘electronic fingerprint’ than account-to-account transfers, although this would depend upon how the system was designed. But having less of an electronic fingerprint hardly seems the basis for building a public policy case to issue an electronic form of the currency. So there would need to be more than this.

Among the potential downsides, the main one lies in the area of financial stability.

If we were to issue electronic banknotes, it is possible that in times of banking system stress, people might seek to exchange their deposits in commercial banks for these banknotes, which are a claim on the central bank. It is likely that the process of switching from commercial bank deposits to digital banknotes would be easier than switching to physical banknotes. In other words, it might be easier to run on the banking system. This could have adverse implications for financial stability.

Given these various considerations, we do not currently see a public policy case for moving in this direction. We will, however, keep that judgement under review.

4. Exchange settlement accounts for all Australians?

Another possible change that some have suggested would encourage the shift to electronic payments would be for the central bank to issue every person a bank account – for each Australian to have their own exchange settlement account with the RBA. In addition to serving as deposit accounts, these accounts could be used for low-cost electronic payments, in a similar way that third-party payment providers currently use accounts at the RBA to make payments between themselves. Some advocates of this model also suggest that the central bank could pay interest on these accounts or even charge interest if the policy rate was negative.

On this issue, we have reached a conclusion, rather than just develop a hypothesis. The conclusion is that we do not see it as in the public interest to go down this route.

If we did go down this route, the RBA would find itself in direct competition with the private banking sector, both in terms of deposits and payment services. In doing so, the nature of commercial banking as we know it today would be reshaped. The RBA could find itself not just as the nation’s central bank, but as a type of large commercial bank as well. This is not a direction in which we want to head.

A related consideration is the same financial stability issue that I just spoke about in terms of electronic banknotes. In times of stress, it is highly likely that people might want to run from what funds they still hold in commercial bank accounts to their account at the RBA. This would make the remaining private banking system prone to runs.

The point here is that exchange settlement accounts are for settlement of interbank obligations between institutions that operate third-party payment businesses to address systemic risk – something that is central to our mandate. A decision to offer exchange settlement accounts for day-to-day use would be a step into a completely different policy area.

5. New settlement systems based on distributed ledger technology and central bank money?

One final possibility is for the RBA to issue Australian dollars in the form of electronic files or tokens that could be used within specialised payment and settlement systems. The tokens could be exchanged among members of a private, permissioned distributed ledger, separate from the RBA’s Real-time Gross Settlement (RTGS) system, but with mechanisms for the tokens to be exchanged for central bank deposits when required. Such a system might allow the payment and settlement process to become highly integrated with other business processes, generating efficiencies and risk reductions for private business. As part of this, the tokens might also be able to be programmed and sit alongside smart contracts, enabling multi-stage transactions with potentially complex dependencies to take place securely and automatically. This seems to be the general model that some people have in mind when they talk about ‘putting AUD on the blockchain’, although other technologies might be able to achieve similar outcomes.

Whether a strong case for the development of these types of systems emerges remains an open question. We need to better understand the potential efficiencies for private business and why it would be preferable for such a settlement system to be provided by the central bank, rather than the private sector; why privately issued tokens or files could not do the job. We would also need to understand why any efficiency improvement could not be obtained by using the existing Exchange Settlement Accounts and the NPP.

We would also need to understand whether and how risk in the financial system would change as a result of such a system. It remains unclear which way this could go. On the one hand, these types of processes could use a very different technology from the current system, which is based on account-to-account transfers, so they could add to the resilience of the overall payments system. But there would be a whole host of new technology issues to manage as well.

The recently published RBA Bulletin included an article “Recent Developments in the ATM Industry”. The article shows that the number of ATMs in Australia is very high relative to population, thanks to significant growth in third party fee for service machines. Now that the banks have announced they will not charge for foreign withdrawals, the RBA says third party players – like owners of petrol stations and convenience stores may see a decline in income, and that overall declines in transaction volumes are likely to reduce the number of machines available, especially in regional areas. That said, many independently owned ATMs are in convenience locations not serviced by bank ATMs (such as pubs and clubs) and so they may be shielded somewhat from this competitive pressure. But many consumers will end up paying even higher fees to use these machines, which may be the only options for some.

The ATM industry in Australia is undergoing a number of changes. Use of ATMs has been declining as people use cash less often for their transactions, though the number of ATMs remains at a high level. The total amount spent on ATM fees has fallen, and is likely to decline further as a result of recent decisions by a number of banks to remove their ATM direct charges. This article discusses the implications of these changes for the competitive landscape and the future size and structure of the industry.

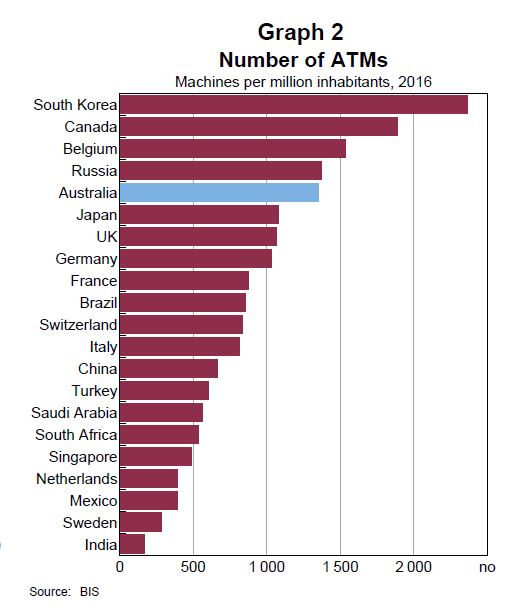

By international standards, we have a large number of ATMs per capita (though not corrected for geographic size).

As at September 2017, there were 32 275 ATMs, only slightly below the peak of nearly 32 900 in December 2016. This represents over 1 300 ATMs per million inhabitant.

The share of the national ATM fleet owned by independent deployers has been rising over the past decade. Independent deployers operate standalone ATM networks that are not affiliated with any financial institution and which are often focused on convenience locations like petrol stations and licensed venues. They rely on the revenue generated by charging fees on all transactions, irrespective of the cardholder’s financial institution, to support their networks.

As at June 2017, 57 per cent of ATMs in Australia were independently owned, up from 55 per cent in mid 2015 and 49 per cent in 2010. The remaining 43 per cent were owned by financial institutions. The increase in the independent deployers’ share reflects strong growth in their ATMs, while the number of bank-owned ATMs has declined over the past few years.

A small number of ATMs that carry financial institutions’ branding but are owned and operated by an independent deployer are recorded in data for independent deployers; other similar arrangements may be recorded under financial institutions. (b) In late 2016, DC Payments acquired First Data’s Cashcard ATM business. (c) NAB, Cuscal and Bank of Queensland, along with a number of other smaller financial institutions, are part of the rediATM network, which allows customers of member institutions to access about 3 000 ATMs (as at June 2017) within that network on a fee-free basis. From August 2017, Suncorp also joined the rediATM network. (d) In November 2017, Stargroup was placed in administration after it was unable to complete a restructure of its debt.