Recently several banks have quietly reduced the value of points within their rewards programmes. So whats going on?

For example, CBA will decrease the rate at which Diamond and Black card holders can earn a Qantas Point from 2 to 2.5 reward points, a 20% loss of value.

ANZ has reduced its rewards on many of its cards, with its Visa version dropping from 2 Points per $1 spent to 1.25 ANZ Reward Points per dollar spend; their Platinum American Express earn rate is falling from 3 to 2 points per dollar spent and their Platinum Visa earning 1 ANZ Rewards Point per $1 rather than the previous 1.5 points per dollar.

They are not alone. Virgin Money says from April 1 2016, the rate at which cardholders can earn Velocity Frequent Flyer Points will be reduced by up to 33%, from one Point per dollar, to 0.66 Points while the Points cap will remain at $1,500 per month. Velocity High Flyer cardholders will also see a drop from 1.25 Points per dollar, to one Point per dollar with a new points cap of $10,000 per month. They also removed rewards from BPay payments (whilst offsetting purchases from Virgin).

Citibank, effective 18th March, lowered Rewards points per A$1 to 1.5 and from uncapped to the first $20,000 spent in each monthly statement period. Credit card BPAY payments no longer earn points and Citibank’s overseas transaction fees rose to 3.4%.

There are two factors in play. First, the interchange fees (that’s the interbank fee for payment processing) has been examined by the RBA, but this is at the discussion stage, and in December 2015, the RBA said

Given the complexity of issues involving interchange fees and companion cards, it is unlikely that the Board will take any formal decision on changes to the interchange standards before its May 2016 meeting … In the case of surcharging, depending on consultation responses, it is possible that the Board may be in a position to make an earlier decision on changes to its standards.

No credit card interchange fee would be able to exceed 0.80 per cent and no debit interchange fee would be able to exceed 15 cents if levied as a fixed amount or 0.20 per cent if levied as a percentage amount.

They also said:

The reduction in interchange fees, especially the cap on the highest credit card rates, is likely to result in some reduction in the generosity of rewards programs on premium cards. It is likely, however, that there would be only limited changes to other elements of the credit card package (e.g. interest rates, interest-free periods). Similarly, the reduction in the high percentage debit/prepaid interchange categories may be likely to result in some reduction in rewards generosity for some of the new debit/prepaid rewards cards. There are unlikely to be other material changes to arrangements for transaction accounts.

The writing is on the wall, and interchange fees, especially for premium cards, are likely to drop.

Second, with banks experiencing margin pressure, fiddling with card reward programmes is a cheap way of growing margins. The intrinsic complexity of the reward programmes (and the fact that not all card holders cash out their rewards anyway) means that changes are so opaque as to be unnoticed by many.

Remember also that credit card interest rates have not followed the target cash rate down.

The truth is, unless you are a devoted points collector, and spend the time to calculate the value (both earn and burn) of the reward points you may gain, you will simply not react to point devaluations. And the RBA interchange intervention provides perfect cover for reducing the value of points.

Expect more cuts in coming months, hikes in some fees and charges and changes to the terms and conditions for rewards points.

RBA Governor Glenn Stevens spoke at the ASIC Annual Forum. His speech covered the normal gamut of macroeconomic analysis, and this section on financial resilience. Two points of interest, first, a fall in house prices in areas of high growth would be “helpful” and foreign banks, who are currently quite active, may become skittish and exit in a downturn.

Turning to financial resilience, Australian banks’ asset quality has generally been improving over the past couple of years. Like their counterparts abroad, in the post‑crisis period the banks have lifted capital resources, strengthened liquidity and reduced use of short-term wholesale funding. So their ability to handle either a funding market shock or an economic downturn has improved compared with the situation in 2008. At this stage we do not see a material problem in Australian financial or non-financial entities accessing capital markets. If anything, net bond issuance by Australian banks has been strong over recent months, and to the extent that banks are able to take advantage of this availability to extend the term of their wholesale liabilities, that will further improve their resilience to any funding disturbances that may eventuate. Wholesale funding is a little more expensive than it was, though marginal funding costs are still no higher than the average cost of the funding being replaced.

On the topic of loan quality, the strengthening of lending standards for housing that has resulted from the actions of both APRA and ASIC was timely. So often over the years, tighter standards tended to come too late and reinforced a downturn after it had begun. These measures have occurred ahead, so far as one can tell, of the point in the cycle when measures of asset quality start to deteriorate. Some moderation in house prices in some of the locations where they had been rising most rapidly, while not the direct objective of the supervisory measures, is also, in my judgement, helpful.

In the business space, the banking system has fairly modest direct exposure to the falls in oil and other commodity prices, with lending to businesses involved in mining and energy accounting for only around 2 per cent of banks’ total lending.

More generally, competition to lend to business has increased over the past couple of years and business credit growth has picked up appreciably. Overall, this is to be expected and is a welcome development at a time when a missing element of the economic growth story is capital spending outside the mining sector, which appears to remain very weak. One notable trend is the aggressive expansion of some of the foreign banks active in the Australian market. Here there is a note of caution. If these are taking opportunities left on the table where local players (or earlier foreign players) were simply too conservative, all well and good. But one is duty‑bound to observe that there is a history of foreign players expanding aggressively in the upswing only to have to retreat quickly when more difficult times come. It is worth remembering that cycle.

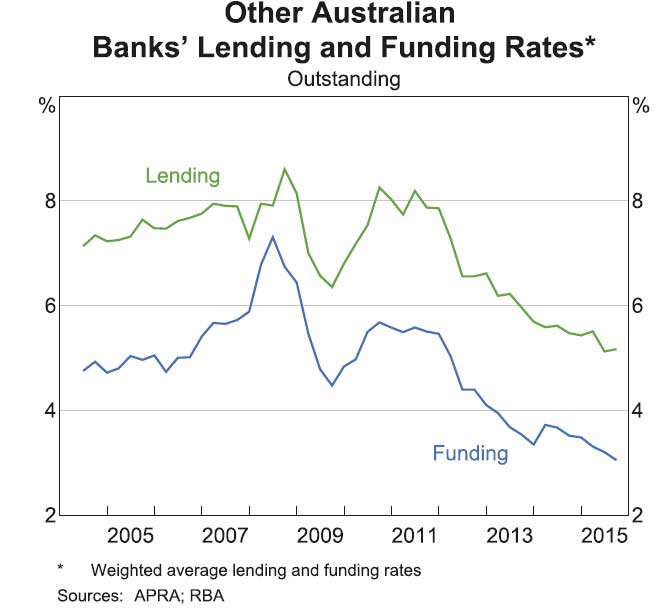

In the RBA Bulletin, released today, there is a section which shows major bank margins have improved. Essentially, the story is one of falling deposit rates, plus change in mix, and rises in home lending rates independent of the cash rate in recent months. Consumers are bearing the burden whilst big business lending rates and margins are being compressed thanks to competition from overseas banks. The big banks are benefiting the most from the margin improvement, which shows again their market power.

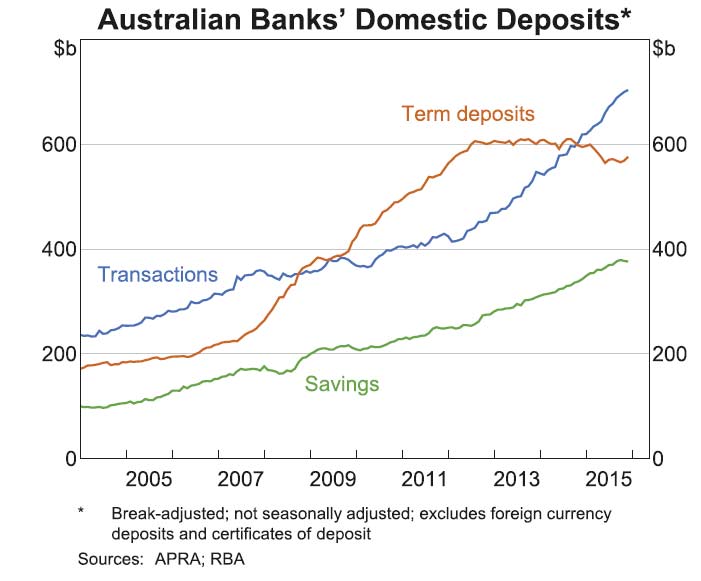

Consistent with the large fall in interest rates on term deposits, the level of term deposits in the system declined in 2015, mostly due to some maturing deposits not being rolled over. In contrast, transaction and at-call savings deposits grew strongly in the year .

Throughout 2015, banks also adopted pricing strategies aimed at reducing deposits from institutional depositors (such as superannuation funds), which are more costly to banks under the LCR framework. The change in the mix of deposit funding lowered the cost of those funds by 3 basis points owing to particularly strong growth in transaction deposits, which carry lower interest payments. In part, this reflects the rapid growth of mortgage offset account balances through 2015, where funds are typically deposited in zero-interest rate accounts but are used to reduce the calculated interest on the associated mortgage. One implication of the increased use of such accounts is the high ‘implied’ cost of funds for banks – equivalent to interest forgone on mortgages. Interest rates on mortgages are much higher than those on deposit products, so banks implicitly pay their customers the mortgage rate on funds held in offset accounts. However, money held in offset only accounts for about 6½ per cent of at-call deposits.

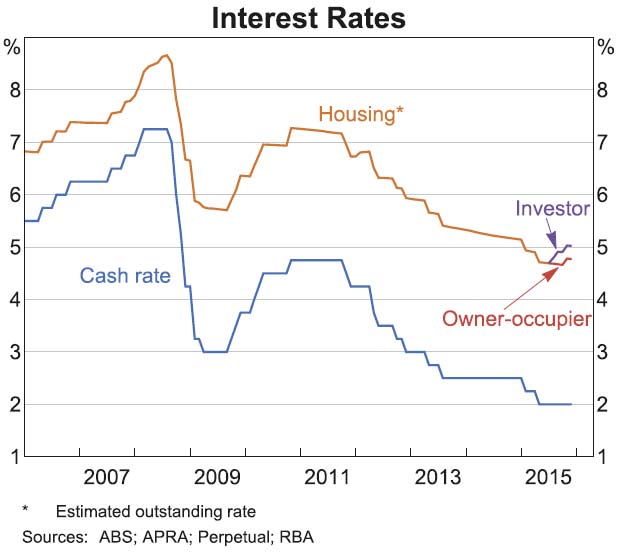

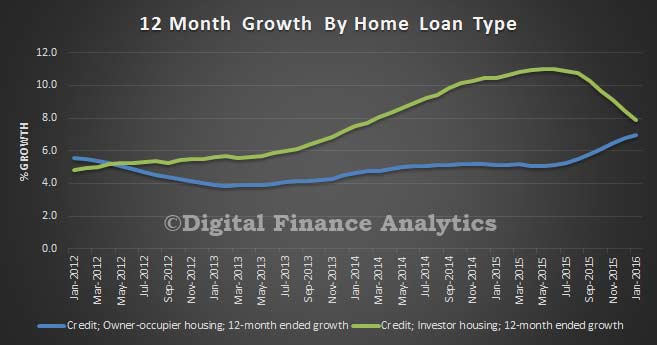

They make the point that housing rates generally declined in line with the cash rate in the first half of 2015, with the average outstanding interest rate on mortgages falling by around 50 basis points over that period. In the second half of the year, however, banks adjusted their lending rates such that the average outstanding housing interest rate for investor loans was only modestly lower over 2015, while rates for owner-occupiers declined by roughly 30 basis points over the year. Interest rates on investor loans were increased midyear, following concerns raised by APRA about the pace of growth in lending to investors. Increases in investor lending rates ranged from around 20–40 basis points, and were applied to both new and existing investor loans.

In November, the major banks raised mortgage rates across both investor and owner-occupier loans by 15–20 basis points, citing the cost of raising additional equity to meet incoming regulatory requirements. Of particular relevance, the Financial System Inquiry’s Final Report recommended higher capital requirements for banks using ‘advanced’ risk modelling (the major banks and Macquarie Bank) in order to reduce a competitive disadvantage relative to other mortgage lenders (FSI 2014). The other Australian banks similarly increased mortgage lending rates, despite not facing the same regulatory costs as the major banks.

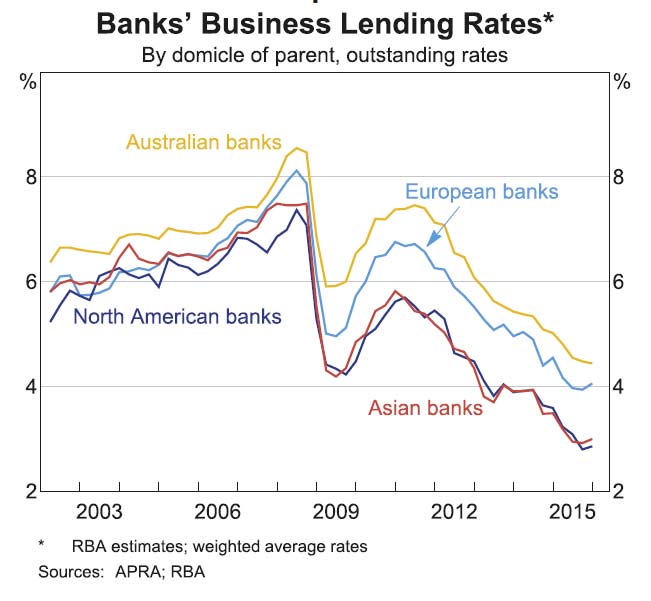

Business rates generally fell by more than the cash rate in 2015, with large business rates falling by around 70 basis points and small business rates by around 60 basis points. These lending rates remain at historic lows. Banks reported that declines in business rates beyond the changes in the cash rate were driven by intense competition for lending, including from the Australian operations of foreign lenders.

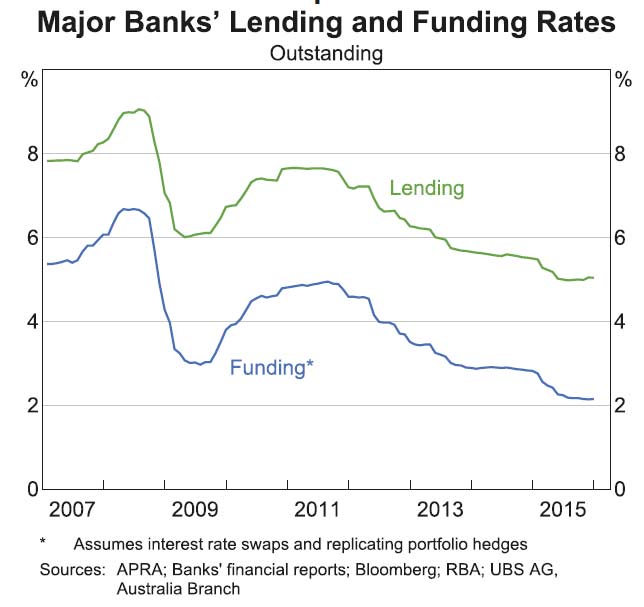

The major banks’ implied spread, being the difference between average lending rates and debt funding costs, increased by around 20 basis points over 2015. This change was driven in roughly equal parts by the decline in average funding costs relative to the cash rate, and an increase in the average lending rate. However, lending rates and debt funding costs tend to move in line with each other in the longer run. The contribution to the aggregate implied spread from higher lending rates was entirely due to increases in housing lending rates, with the implied spread on housing lending now higher than the previous peak in 2009. However, the measure of funding costs used to calculate implied spreads does not account for the increased share of relatively expensive equity funding. As such, the increase in the implied spread for housing lending is likely to overstate the true change in major banks’ margins for this activity. Implied spreads on business lending declined over 2015. Consistent with strong competition, implied spreads on large business lending have returned to pre-global financial crisis levels, when there was strong competition, business conditions were highly favourable and risk premia were compressed. Much of the competition is coming from foreign banks, with the average rate on business loans written by foreign banks significantly lower than the rate being charged by Australian banks.

The average implied spread on other Australian banks’ lending has been around 25 basis points lower than for the major banks since 2005. However, there is considerable variation in implied spreads of the other Australian banks, driven more by the high variation in lending interest rates across banks than variations in funding costs. In contrast to the major banks, the spread on other Australian banks’ lending for housing declined over 2015 with their lending rates falling by more than their funding costs. The other Australian banks’ spread on business lending also decreased in 2015. The spread on business lending remains higher for the other Australian banks, which reflects the fact that these banks generally lend more to smaller business than the major banks, and do not compete as heavily with the major and foreign banks on large business lending.

In considering the stance of monetary policy, members noted that the recent data on the international and domestic economies had been largely consistent with the outlook presented at the previous meeting. Growth in Australia’s major trading partners had remained a little below average in year-ended terms and commodity prices were still significantly lower than they had been a year earlier. Meanwhile, global financial markets had been volatile in the aftermath of the Bank of Japan’s decision to implement negative interest rates and generally there appeared to be more uncertainty about the direction and potency of monetary policy in the major jurisdictions. However, given the usual lags in the data, it was still too early to assess whether the bout of financial market volatility since the turn of the year foreshadowed or would lead to a weakening in global economic conditions. Globally, monetary policy remained very accommodative.

The available data suggested that the domestic economy had continued to grow at a slightly below-trend pace. There had also been further signs of a rebalancing of activity towards non-mining sectors of the economy, aided by the low level of interest rates and the depreciation of the exchange rate over the past couple of years, which had responded to the evolving economic outlook. There was a small decline in employment in January and a modest rise in the unemployment rate, following a run of much better-than-expected outcomes in the December quarter. Leading indicators of employment had increased further and were consistent with employment growth in the months ahead. Wage growth had remained at quite low levels.

Conditions in the established housing market had eased somewhat since September 2015, in part reflecting the effect of supervisory measures implemented in that year. In addition, after rising for some time, the growth in aggregate housing credit had stabilised over the past six months or so, with a significant easing in growth in lending to investors.

Members judged that there were reasonable prospects for continued growth in the economy and that it was appropriate to leave the cash rate unchanged at an accommodative setting. Over the period ahead, new information should allow the Board to assess whether the improvement in labour market conditions was continuing and whether the recent financial turbulence presaged weaker global and domestic demand. Members noted that continued low inflation would provide scope to ease monetary policy further, should that be appropriate to lend support to demand.

APRA has written to all ADI’s with regards to the spate of mortgage reclassification between investment and owner occupied loans which amounts now to around $35bn of adjustments in the past few months. Reclassification seem to emanate from internal review within the banks when APRA introduced 10% speed limit on investment loans, and also is customer initiated following the price differences between owner occupied and investment mortgages which have emerged. These movements are “strange” and may reflect some divergence from the true state of play. The mix of loans clearly has an impact on policy, and has the potential later to impact potential capital requirements.

So APRA’s warning is timely. There are however no overt penalties of inaccurate reporting and some banks have made adjustments without any formal statements, although others did disclose significant recalculations.

A number of ADIs have recently reported significant changes in housing loan purpose between investment and owner-occupied. This letter provides guidance to assist authorised deposit-taking institutions (ADIs) report these data to APRA consistently and accurately.

These data are used in public policy decisions, prudential supervision and statistical publications. Where the change in loan purpose is not reported correctly (i.e. from the period that the change occurred), APRA, the Reserve Bank of Australia (RBA) and the Australian Bureau of Statistics (ABS) are impeded in accurately ascertaining the underlying movements in housing loans.

Reporting of fixed term housing loans must reflect the current purpose of the loan because the split by housing loan purpose is important for monetary policy and financial stability considerations.

Use of data

APRA uses these data for supervision and publication. The data are also used by the RBA and the ABS.

The classification of investment and owner-occupied housing loans is used by the RBA to:

calculate the financial aggregates;

assess the transmission of monetary policy through the financial system;

assess potential risks to financial stability; and

meet international statistical standards and reporting obligations.

The ABS uses the domestic books data to compile Gross Domestic Product, of which ADIs are a major component

Banks’ reporting of Statement of Financial Position ARF 320.0 (ARF 320.0)

In order to report loan data on the ARF 320.0 accurately each period, according to whether a loan is owner occupied or investment housing, ADIs must report data for existing (non-revolving) housing loans by current loan purpose.

The instructions to ARF 320.0 item 5.1.1.1 owner-occupied housing loans state that the figure reported must:

Include:

the value of housing loans to Australian households, for the construction or purchase of dwellings for owner occupation; and

revolving credit or redraw facilities originally approved for a purpose of predominantly owner-occupied housing.

The instructions to ARF 320.0 item 5.1.1.2 investment housing loans state that the figure reported must:

Include:

the value of investment housing loans to Australian households, for the construction or purchase of dwellings for non-owner occupation; and

revolving credit or redraw facilities originally approved for a purpose of predominantly non-owner-occupied housing.

Therefore:

when an ADI becomes aware there is a change in the purpose of an existing (non-revolving) housing loan between investment and owner-occupied, the ADI must report that loan under the new purpose on the ARF 320.0 from the month that the change in purpose occurred; but

for housing loans to households comprising revolving credit secured by residential mortgage, the instructions state that the loan must NOT be reported under the new purpose but continue to be reported under the purpose of the loan for which it was originally approved.

Loans must be reported according to the purpose of the loan. Where the purpose of a loan is not for the purchase or construction of a dwelling, the loan should NOT be recorded under item 5.1.1.1 or 5.1.1.2 of ARF 320.0: the loan should be reported under the relevant loan item elsewhere in ARF 320.0. In particular, non-housing loans that are secured by residential property mortgages should not be reported under item 5.1.1.1 or 5.1.1.2, but reported under the relevant loan item elsewhere in ARF 320.0. For example, a loan to a sole trader business secured by a residential property mortgage would be reported in item 5.3 Loans to non-financial corporations.

Credit unions’ and building societies’ reporting of Statement of Financial Position ARF 323.0 (ARF 323.0)

In order to report data on the ARF 323.0 accurately each period, according to whether a loan is owner occupied or investment housing, ADIs must report data for existing (non-revolving) housing loans by current loan purpose. Switching of purpose between investment and owner-occupied housing loans should be recorded under the new purpose on the ARF 323.0 from the month that the change in purpose occurred.

As per the ARF 323.0 instructions, fixed term housing loans should be reported per the current purpose and therefore should change category when the purpose changes. Revolving credit and redraw facility housing loans should continue to be reported under the purpose that the loan was originally approved for.

Housing Loan Reconciliation ARF 320.8 (ARF 320.8)

Loans which switched purpose between investment and owner-occupied housing loans should be reported under the new purpose in the outstanding stocks on ARF 320.8 Tables 1, 2 and 3.

In Table 1 of ARF 320.8, if the changed purpose of housing loans is recorded in an ADI’s system as an internal refinance, then the change in classification should be reported as ‘Excess repayments due to sale of property or refinancing’ under the original purpose, and also as ‘Drawdowns (new loans and redraws)’ for the new purpose. An example of an internal refinance is when a new contract is signed by the customer. If the reclassifying by housing loan purpose is not recorded in your system as an internal refinance, then the reclassification should be recorded as ‘Other adjustments’ under both the original and new purpose. Once the reclassifying by housing loan purpose has occurred, any other flows related to that loan should be recorded under the new purpose.

In Table 1, the flow for the reporting period should be recorded under the new purpose. Opening balances in Table 1 of the supplementary information template should be reported as nil. In Tables 2 and 3, the balances should be recorded under the new purpose.

As per the Housing Finance ARF 392 series and Personal Finance ARF 394 series instructions, reclassifying by housing loan purposes should not be reported as a new loan approval if there is no change in the property offered as security or the lender. As such, it should not be captured in Table 4.

Housing Finance ARF 392 (ARF 392) series

The general instructions for ARF 392 (page 5) state that institutions should exclude commitments to refinance existing loans where there is no change in the property offered as security and the institution was the original lender. Therefore, switching of purpose between existing investment and owner-occupied housing loans should not be reflected in the housing approvals reported on the ARF 392. Loan purpose switching does not qualify as a new commitment, nor is it an external refinance.

Personal Finance ARF 394 series

Switching of purpose between existing investment and owner-occupied housing loans should not be reflected in new commitments reported on the ARF 394 in ‘Loans for personal investment purposes – dwellings for rent/resale’ and ‘Loans for personal investment purposes – refinancing’. Loan purpose switching does not qualify as a new commitment, nor is it an external refinance.

Banks’ reporting of Impaired Assets ARF 220.0

Loans which switched by purpose between impaired investment and owner-occupied housing loans and between past due investment and occupied housing loans should be recorded under the new purpose categories on the ARF 220.0 Parts 1B and 2B from the reporting period that the reclassification occurred.

There were two important charts contained in the speech by RBA Deputy Governor Philip Lowe today covering the resilience of our own economy, the productivity challenge, the balance in the housing market and the inflation outlook. Real disposable income per capita has been static since 2008, and rent inflation continues to fall. Both indicators of ongoing stress in the economy, especially since household debt is higher than ever, and we have a large share of housing in the investment sector, where we already know some households are in real-terms losing money each month.

While we have done a pretty good job of adjusting to our changed circumstances, the not-so-good news is that growth in real income per capita in Australia has stalled (Graph 5). Indeed, average real income is no higher today than it was in 2008. This follows a 17-year period in which growth averaged a remarkable 3.1 per cent per year. During this earlier period, we benefited from: (i) strong productivity growth in the 1990s; (ii) a very large rise in our terms of trade; and (iii) favourable demographics, which helped increase the share of the population in paid employment.

The increase in supply now looks to be contributing to some moderation in the rate of increase in housing prices in these cities. It is also putting downward pressure on rents, with the CPI measure of rent inflation running at just 1.2 per cent in 2015, the lowest for 20 years (Graph 8). Whether or not these trends are maintained remains to be seen, and so we continue to watch developments in the housing market very closely.

The latest data from the RBA chart pack shows again growing debt, and the reduced debt interest burden thanks to ultra low rates. If rates were to rise by even a small amount, in the current low income and low rental environment, this will be a problem.

Recent information suggests that the global economy is continuing to grow, though at a slightly lower pace than earlier expected. While several advanced economies have recorded improved growth over the past year, conditions have become more difficult for a number of emerging market economies. China’s growth rate has continued to moderate.

Commodity prices have declined very substantially over the past couple of years. This partly reflects slower growth in demand but also, in some key instances, large increases in supply. The decline in Australia’s terms of trade has continued.

Financial markets have once again exhibited heightened volatility over recent months, as participants grapple with uncertainty about the global economic outlook and policy settings among the major jurisdictions. Appetite for risk has diminished somewhat and funding conditions for emerging market sovereigns and lesser-rated corporates have tightened. But funding costs for high-quality borrowers remain very low and, globally, monetary policy remains remarkably accommodative.

In Australia, the available information suggests that the expansion in the non-mining parts of the economy strengthened during 2015 despite the contraction in spending in mining investment. This was reflected in improved labour market conditions. The pace of lending to businesses also picked up.

Inflation is quite low. With growth in labour costs continuing to be quite subdued as well, and inflation restrained elsewhere in the world, inflation is likely to remain low over the next year or two.

Given these conditions, it is appropriate for monetary policy to be accommodative. Low interest rates are supporting demand, while supervisory measures are working to emphasise prudent lending standards and so to contain risks in the housing market. Credit growth to households continues at a moderate pace, albeit with a changed composition between investors and owner-occupiers. The pace of growth in dwelling prices has moderated in Melbourne and Sydney and has remained mostly subdued in other cities. The exchange rate has been adjusting to the evolving economic outlook.

At today’s meeting, the Board judged that there were reasonable prospects for continued growth in the economy, with inflation close to target. The Board therefore decided that the current setting of monetary policy remained appropriate.

Over the period ahead, new information should allow the Board to judge whether the improvement in labour market conditions is continuing and whether the recent financial turbulence portends weaker global and domestic demand. Continued low inflation would provide scope for easier policy, should that be appropriate to lend support to demand.

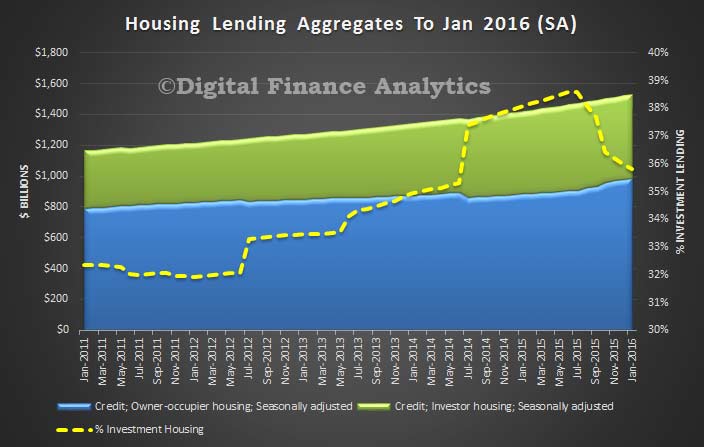

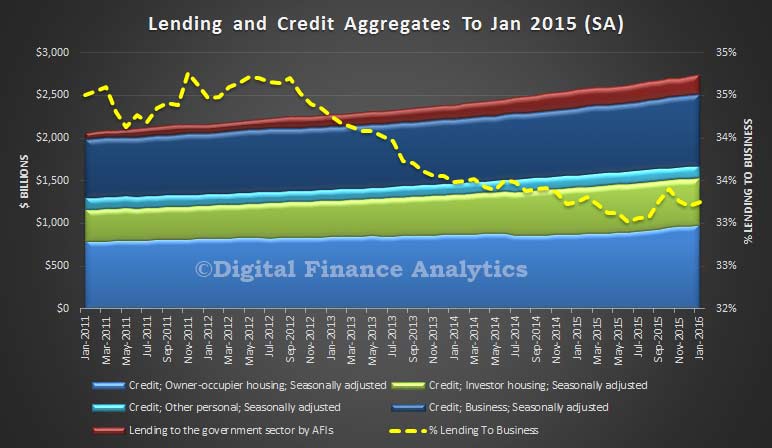

Total home lending was up 0.53% in the month, and $8bn was for owner occupied lending. Investment lending went sideways, but note also though that there were further adjustments between OO and investment loans.

“Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $35.3 billion over the period of July 2015 to January 2016 of which $1.4 billion occurred in January. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes”.

As a result, the proportion of loans for housing investment purposes has fallen a little further, from 35.98% to 35.8%, but this is still a big number.

Turning to the overall aggregates, home lending was up 0.53%, business lending rose 0.63% and personal credit fell 0.79% as households paid off their Christmas binge.

Business investment remains at a relative low level, with one third of all lending going to business, once again showing how debt to households is being relied on to grow the economy.

We know from our own analysis that significant numbers of households would find any rise in interest rates a big problem, and loading up households further with ever more debt is a flawed strategy. When are we going to get serious about getting real long term growth via business investment?

We will discuss the parallel APRA data, also released today, later.

The Australian payments system is evolving, both in terms of some innovative new payment instruments that are on their way and the declining use of some of our older or legacy payment instruments. Tony Richards RBA Head of Payments Policy Department RBA, spoke at the Payments Innovation 2016 Conference on this evolution.

There is a lot happening in the payments industry at present, so my sense is that it would be premature to have a serious discussion about possibly phasing out cheques before the implementation of the New Payments Platform (NPP), which is scheduled to begin operations in late 2017. But if this conference was to revisit this issue in early 2018 with the NPP up and running, it should find significant new payments functionality in place. This will include the ability for end-users to make real-time transfers with immediate availability of funds, to make such transfers on a 24/7 basis, to attach data or documents with payments or payment requests, and to send funds without knowing the recipient’s BSB and account number. These are all aspects that match or exceed particular attributes of cheques.

In addition, by early 2018 another two years will have passed and there will no doubt have been a significant further decline – based on current trends, a further 30 per cent or so – in cheque usage.

By that point, more organisations and individuals will have further reduced their cheque usage. The Bank has recently been doing some liaison with payment system end-users in our Payments Consultation Group and has heard some impressive accounts about how some of the major Commonwealth government departments and some large corporates have largely moved away from the use of cheques. Cheque usage in the superannuation industry has also fallen very significantly as part of the SuperStream reforms.

A shift away from the use of bank cheques is also underway in property settlements. On average, there are around 40 000 property transactions in Australia each month, plus a significant number of refinancings, with most of these requiring at least a couple of cheques for settlement. However, starting in late 2014 and after much preparatory work, electronic conveyancing and settlement is now feasible. This is being arranged by Property Exchange Australia Ltd (an initiative that includes several state governments and a number of financial institutions), with interbank settlement occurring in RITS, the Reserve Bank’s real-time gross settlement system. Volumes have risen steadily and by late 2015 the number of property batches settled in RITS – each batch typically corresponds to a single transaction or refinancing – had reached nearly 4 000 per month. This trend is expected to continue.

In addition, the Bank’s Consumer Use Survey indicates that usage of cheques is falling rapidly for households of all ages. Our survey from late 2013 confirmed that older households continue to use cheques more than younger ones. However, older households are also reducing their use of cheques significantly. And with more and more older households now using the internet, their use of cheques is likely to continue falling. Indeed, I’m sure we all have a story about an older family member or friend who has recently bought or received a tablet or notebook and discovered the benefits of being online.

Graph 8

Graph 9

We will get a further reading on households’ use of cheques and other payment instruments in the Bank’s next Consumer Use Survey, which – if we follow the timetable of recent surveys – will be published in the first half of next year based on data collected late this year.

More broadly, as the industry starts to think about options for the cheque system, it will be important to make sure that those parts of the community that still use cheques are fully consulted so that we can be sure that their payment needs are met by other instruments. This is likely to involve consultations with organisations representing older age groups, the non-profit sector and those in rural Australia.

Cash

Discussions about the declining use of cheques sometimes also touch upon the declining use of cash.

Because transactions involving cash typically do not involve a financial institution, data for the use of cash are actually quite limited. However, one good source of data on the use of cash by individuals is the Bank’s Consumer Use Study. Our most recent study, in late 2013, showed that cash remained the most important payment method for low-value transactions (around 70 per cent of payments under $20). However, it confirmed that the use of cash had declined significantly, with the proportion of all transactions involving cash falling from 70 per cent in the 2007 survey to 47 per cent in 2013.

More recent data on the transactions use of cash are not available, though the ongoing fall in cash withdrawals from ATMs and at the point of sale suggest that it has continued. In addition, the continuing strong growth of contactless transactions and the growing acceptance of cards for low-value transactions are also suggestive of a further decline in the use of cash.

Graph 10

Graph 11

However, that is where the parallels with cheque usage end. While the use of cash in transactions has been declining, the demand to hold cash has continued to grow. This is the case for low denomination banknotes as well as high denomination ones. Indeed, in recent years there has been a modest increase in the rate of growth of banknotes on issue, to an annual rate of around 7 per cent over the past couple of years. More broadly, over the longer term, growth in banknote holdings has been largely in line with nominal growth in the overall economy.

Graph 12

Graph 13

The growing demand for holdings of cash suggest that it continues to have an important role as a store of value and there is some evidence – from demand for larger denomination notes – that this increased following the global financial crisis. So, despite the decline in use in transactions, cash is likely to remain an important part of both the payments system and the economy more broadly for the foreseeable future. In particular, significant parts of the population appear to remain more comfortable with cash than with other payment methods in terms of ease of use for transactions or transfers, as a backup when electronic payment methods may not be available, or as an aide for household budgeting.

Given the important ongoing role of cash in the payments system, the Bank is currently undertaking a major project to upgrade the existing stock of notes. Counterfeiting rates of the current series of banknotes remain low by international standards but have been rising and there are some signs that the counterfeiters are getting a bit better with new and cheaper scanning, printing and image manipulation technology. Accordingly, the program for the next generation of banknotes includes major security upgrades that should ensure that Australia’s banknotes remain some of the world’s most secure. The first release of the new banknotes will occur in September this year, with the release of the new five dollar note.

Australia is not alone in continuing to invest to ensure that the public can continue to have confidence in its banknotes. The United States has also done so recently, and Sweden – which is often cited as being furthest along the path to a cashless or less-cash society – is also in midst of introducing a new series of notes.

Digital currencies and distributed ledgers

As the use of cash and cheques continues to fall, the Bank will – subject to there not being any overriding concerns about risk – be agnostic as to what payment methods replace the legacy systems, consistent with its mandate to promote competition and efficiency.

In the short run, it is likely that we will see further growth in the existing electronic payment methods, including payment cards in their various form factors. In the medium term, it is likely that we will see growth in new payment methods and systems, including those that will be enabled by the NPP.

Let me stress that the Bank has not reached a stage where it is actively considering this, but in the more distant future it is even possible that we may we see a digital version of the Australian dollar. As the Bank has noted in the past, it seems improbable that privately-established virtual currencies like Bitcoin, with its significant price volatility, could ever displace well-established, low-inflation national currencies in terms of usage within individual economies. Bitcoin has, however, served to stimulate interest in the potential offered by distributed ledgers, extending to the possibility of central-bank-issued digital currencies. A plausible model would be that issuance would be by the central bank, with distribution and transaction verification by authorised entities (which might or might not include existing financial institutions). The digital currency would presumably circulate in parallel (and at par) with banknotes and other existing forms of the national currency.

A few countries have explicitly discussed the possibility of digital versions of their existing currency. Both the Bank of England and Bank of Canada have indicated that they are undertaking research in this area. And a recent announcement from the People’s Bank of China indicated that it has plans for digital currency issuance, though few specifics were provided.

The Bank will be interested to see what proves to be possible and what proves to be problematic, as countries consider going down the path of digital currency issuance. Given the various cybersecurity and cryptography risks involved, my personal expectation is that full-scale issuance of digital currency in any country, as opposed to limited trials, is still some time away. And I think it remains to be seen if there is real demand for a digital equivalent of cash and what it might offer end-users relative to what will be offered by the various forms of real-time payments that are being developed in many countries through projects like the NPP.

I should also touch briefly on another potential application of blockchain or distributed ledger technologies, namely in the settlement of equity market transactions. As the overseer of clearing and settlement facilities licensed to operate in Australia, the Bank obviously has a keen interest in the plans of the ASX Group to explore the use of distributed ledgers. Along with the Australian Securities and Investments Commission and other relevant public sector organisations, we will be working closely with ASX as it considers whether a distributed ledger solution might be the best way to replace its existing CHESS infrastructure.

Review of Card Payments Regulation

I will conclude with a few comments on the ongoing Review of Card Payments Regulation.

The Bank issued a consultation paper containing some draft changes to standards in late 2015. It has received substantive submissions from 43 different stakeholders, with a number of parties providing both a public submission and additional confidential information. 33 non-confidential submissions have been published on the Bank’s website.

The submissions indicate that most end-users of the payments system are broadly supportive of the Bank’s reforms over the past decade or more. Some submissions have indeed suggested that the Bank could have gone further in its proposed regulatory changes. Financial institutions and payment schemes have expressed a range of views. For the most part they have recognised the policy concerns that the Bank is responding to. In some cases there is a fair bit of common ground in areas where they have made suggestions for changes to the draft standards, but in others there are conflicting positions that correspond to the different business models of the entities that have responded to consultation.

The Payments System Board discussed the Review at its meeting last Friday, focusing on issues that stakeholders have highlighted in submissions. As we always do when regulatory changes are proposed, Bank staff will be meeting with a wide range of stakeholders to discuss submissions. Indeed, we have already had a significant number of meetings, sometimes multiple meetings with particular firms as they were preparing their submissions.

Some of the issues to be explored in consultation meetings include: the treatment of commercial cards and domestic transactions on foreign-issued cards in the interchange benchmarks; the proposed shift to more frequent compliance to ensure that average interchange rates remain consistent with benchmarks; and the calculation of permissible surcharges for merchants (such as travel agents or ticketing agencies) that are subject to significant chargeback risk when they accept credit or debit cards.

One other issue that I would like to flag ahead of our consultation meetings relates to the proposed reforms to surcharging arrangements. The Bank’s proposed new surcharging standard has been drafted to be consistent with amendments to the Competition and Consumer Act 2010 which were passed by the House of Representatives on 3 February and by the Senate yesterday.

The proposed framework envisages that merchants will retain the right to surcharge for expensive payment methods. However, the permitted surcharge will be defined more narrowly as covering only the merchant service fee and other fees paid to the merchant’s bank or other payments service provider. Acquirers would be required to provide merchants with easy-to-understand information on their cost of acceptance for each payment method, with debit/prepaid and credit cards separately identified. The draft standard would require that merchants would receive an annual statement on their payment costs which they could use in setting any surcharge for the following year. The information in these statements should allow the Australian Competition and Consumer Commission (ACCC) to easily investigate whether a merchant is surcharging excessively.

The objectives of the proposed changes to the regulation of surcharging received widespread support in submissions. However, a number of financial institutions have argued that it would be difficult to provide statements to merchants on their average acceptance costs for each payment system. Some have said that their billing process draws on multiple systems within their organisations (and sometimes from third parties), so that it is not straightforward to provide the average cost information proposed by the Bank. Some have indicated that they do not currently provide annual statements to merchants, so this would be a significant change. Accordingly, a number have suggested that they would prefer a significant implementation delay before they are required to provide merchants with the desired transparency of payment costs. Bank staff will be testing these points in our consultation meetings with acquirers. In doing so, we will be looking to see what might be done to ensure that the standards can take effect as soon as possible, in order to meet community expectations about the elimination of instances of excessive surcharging.

More broadly, the Board also discussed a possible timeline for concluding the Review. The Bank’s expectation is that a final decision on any regulatory changes should be possible at the May meeting. It is too soon to give much guidance on the date when any changes to the Bank’s standards might take effect, but the Board recognises that an implementation period will be necessary for the industry.

The principal interest rate benchmark in Australia is the bank bill swap rate (BBSW), but there are questions about its accuracy (and we know overseas, other benchmark rates – such as LIBOR – have been rigged). So Guy Debelle RBA Assistant Governor (Financial Markets) spoke at the KangaNews Debt Capital Markets Summit and both discussed domestic reforms around the benchmark, and mentioned the possibility of introducing a ‘risk-free’ interest rate for the domestic market, as a complement to BBSW. He did not talk about the investigations that ASIC is currently undertaking into conduct around BBSW.

Given its wide usage, BBSW has been identified by ASIC as a financial benchmark of systemic importance in our market. It is important there is ongoing confidence in it. Without that, we have a serious problem, given its integral role in the infrastructure of domestic financial markets.

As you may know, BBSW was calculated for a number of years by, each day, asking a panel of banks to submit their assessment of where the market was trading in Prime Bank paper at a particular time of the day. While it was a calculation based on submissions, it differed from LIBOR in that BBSW submitters were asked about where the market for generic Prime Bank paper was trading that day. In contrast, LIBOR submitters were asked about where they thought their own bank’s cost of funds was that day.

In response to the prospect of a large number of the participants on the submission panel no longer being willing to provide submissions, the calculation of BBSW was reformed in 2013 in line with the IOSCO Principles for Financial Benchmarks, which were issued in July 2013.

Since 2013, the Australian Financial Markets Association (AFMA) has calculated BBSW benchmark rates as the midpoint of the (nationally) observed best bid and best offer (NBBO) for Prime Bank Eligible Securities, which are bank accepted bills and negotiable certificates of deposit (NCDs). Currently, the Prime Banks are the four major Australian banks. The rate set process uses live and executable bid and offer prices sourced from interbank trading platforms approved by AFMA, These platforms are currently ICAP, Tullett Prebon and Yieldbroker. The bids and offers are sourced at three points in time around 10.00 am each day.

Trading activity during the daily BBSW rate set has declined over recent years to very low levels. There are quite a number of days where there is no turnover at all at the rate set. The low turnover in the interbank market raises the risk that market participants may at some point be less willing to use BBSW as a benchmark. This is the motivation for the CFR’s consultation to ensure that BBSW remains a trusted, reliable and robust financial benchmark.

The likely key change to the methodology proposed is to calculate BBSW directly from market transactions – that is, calculating BBSW as the volume-weighted average price (VWAP) of market transactions during the rate set window. Given the objective is to better anchor BBSW to transactions in the underlying market, the RBA supports moving the calculation methodology to the VWAP.

With regards to the risk-free benchmark:

Next I would like to briefly raise some issues around whether the use of BBSW needs to be quite as widespread as it is. In a number of instances, BBSW has become the default reference rate without much thought being given as to whether it is the most appropriate reference rate. BBSW is a credit‑based reference rate. It is based on the borrowing costs of the major banks, with the credit risk that entails embodied in the rate.

For a number of purposes, a credit‑based rate is completely appropriate. However, for other purposes, a rate that is closer to risk‑free may be more appropriate. For instance, in recent years, market participants have moved to use overnight-indexed swap (OIS) rates more often when discounting the cash flows in their swaps. The FSB, through its official sector steering group (OSSG) on benchmark reform, is encouraging market participants to contemplate switching from credit‑based benchmark rates like BBSW or LIBOR to risk‑free rates, where appropriate.

In the local market, there appears to be growing interest in using risk-free rates as benchmarks. Such a rate could be backward looking, like the cash rate, or forward looking, like OIS rates. As a first step, some market participants have indicated that a total return index of the cash rate would be a useful backward-looking benchmark. Implementing this would be straightforward, since the RBA already calculates and publishes the cash rate. Some market participants are also interested in referencing a forward-looking rate with equivalent tenors to BBSW, and we will continue to work with AFMA on the development of such a benchmark.

One example where a change in reference rate could be contemplated is for floating rate notes (FRNs) issued by governments. FRN coupon payments are typically priced at a spread to BBSW. While referencing BBSW makes sense for FRNs issued by banks, it is less clear why governments should tie their coupon payments to a measure of bank funding costs.

That is one example worthy of consideration. There are a number of others. I know this is not necessarily an issue you may have thought that much about until now. At the very least, I would encourage you to at least ask the question whether the product you are issuing or holding is using the most appropriate reference rate.