The latest on the Cash Restrictions Bill – with Treasury hiding a key submission from KPMG, the architect of the ban… I discuss with Robbie Barwick from the Citizens Party.

Currency (Restrictions on the Use of

Cash) Bill 2019

I have carefully reviewed the latest iteration of this legislation

and am gratified that the Senate has chosen to review the proposals, which I strongly

oppose.

Not only is the bill significantly eroding our civil

liberties, but the conduct of Treasury needs to be called out by suggesting

that 3,400 of the 3,500 submission they received during their brief 2 week

exposure review submission period were part of a campaign “by the CEC, a

political party”. While there was indeed a campaign to oppose the draft

legislation, I have evidence that submissions were made by many concerned

individuals and businesses with no links to the CEC. Indeed, my own submission,

some of the contents I am using here again, is based on my own independent

research and analysis. I have no

financial or political association with said CEC. I believe Treasury tried to

play down the considerable opposition which exists within the community. This

bill is, in my view toxic.

Digital Finance Analytics is a boutique research and analysis firm specialising in the financial service sector. We undertake primary research through our surveys, as well as deep research from the global literature relating to financial services. We publish regularly via our online channels at Digital Finance Analytics[1] as well as preparing reports on a range of related subject matters for our clients, and we collaborate with a number of academics.

My objections are centred around the following points.

Civil Liberties Are Being Eroded. Further public debate on these measures are warranted as they are fundamentally restricting personal freedoms. Today I can use and hold cash as I please. If passed, my freedom will be eroded. This is one in a series of measures which have been taken (including media freedoms) which are curtailing the hard-won freedoms Australians used to enjoy. Public hearings should be held by the Senate to judge community reactions to the bill as part of the current review.

There Is No Cost Benefit. The stated objective of the bill is to close tax avoidance and money laundering loopholes. But there is no quantification of the potential “savings” – and this is also true of the earlier Black Economy Taskforce report. It appears that simply stating these desired objectives is seen as sufficient to justify the bill. What is the cost benefit of such a measure, bearing in mind that transactions which fall outside the exemptions would need to be tracked and examined?

Increased Surveillance Will Be Required.

In some form, monitoring of offending transactions would be required if the

Bill were passed. This is not explained,

nor how it would be policed. Who would police them, at what cost? Further, the bill proposed a draconian set of

penalties designed to deter. Treasury admitted this in their FOI’d response.

Existing Laws Are Not Enforced. The true

size of the black economy is much in dispute, but indications are that it is

already falling. In addition, much of the tax leakage and avoidance would be

covered by existing legalisation if it were being policed effectively. We

support the view, recently aired by Andrew Wilkie in the debate on the floor of

the house, that:

“There’s already a requirement

to report transactions over $10,000. The problem is that those laws are not

being implemented and enforced[2].”

There are other more pressing areas of tax

leakage and AML risk. According to the OECD report “Implementing The OECD

Anti-Bribery Convention” released as part of the OECD Working Group on Bribery,

Real Estate is identified as at “significant risk” of being used for money

laundering. Among a raft of recommendations, is one saying Australia should be

“Taking urgent steps to address the risk that the proceeds of foreign bribery

could be laundered through the Australian real estate sector. These should

include specific measures to ensure that, in line with the FATF standards, the

Australian financial system is not the sole gatekeeper for such transactions”. To date these loopholes, remain open, as do those

relating the corporates and big business who, partly thanks to the assistance

of the large international accounting firms are responsible for the lions share

of tax leakage and AML activity. Our research suggests that Government, under

heavy corporate and business lobbying is deliberately letting this slide,

preferring to target in on a relatively inconsequential area of tax leakage

relating to cash transactions.

The Legislation Would Be Ineffective. Beyond

that, it is clear from our wider research of a range of sources that such a

proposed cash ban would have very little impact on hard core tax leakage. For example,

Professor Fredrich Schneider, a research fellow at the Institute of Labor

Economics at the University of Linz, Austria, a leading international expert on

the black economy has stated that there is a lack of empirical evidence that

cash transaction bans will help reduce the black economy. Schneider published a

paper in 2017[3] “Restricting or Abolishing Cash: An Effective

Instrument for Fighting the Shadow Economy, Crime and Terrorism” in which he

made this specific point.

There Is Another Agenda. In addition, while the Bill is silent on the connection to implementing negative interest rates as part of unconventional policy, the link was made clearly in the 2016 Geneva Report by the International Centre Monetary and Banking Studies (ICBM) titled: What else can Central Banks do?[4] This paper which was drafted by officials from international organisations such as the IMF/BIS and multiple central banks + commercial banks. In addition, within the original Black Economy Taskforce Report there was mention of the benefits of a cash transaction ban in relationship to monetary policy – yet this link was denied by Treasury in their recent FOI release.

The IMF Shows Why. The same thematic came through in recent IMF Blogs and working papers. In April 2019, the IMF published a new working paper on how deeply negative interest rates work. In previous papers, the IMF has suggested that nominal interest rates may have to go deeply negative, for example, -3% – 4%. First, they say “In summary, ten years after the crisis, it is clear that the zero-lower bound on interest rates has proved to be a serious obstacle for monetary policy. However, the zero lower bound is not a law of nature; it is a policy choice. We show that with readily available tools a central bank can enable deep negative rates whenever needed—thus maintaining the power of monetary policy in the future.” Next they declare “Our view is that, when needed, deep negative rates are likely to be worth the political cost. While the complete abolition of paper currency would indeed clear the way for deep negative interest rates whenever deep negative rates were called for, such proposals remain difficult to implement since they involve a drastic change in the way people transact.”

The Bill Is Connected to Negative Interest

Rates. The connection is obvious in that in a negative interest rate

environment households and businesses will be likely to withdraw funds from the

banking system and transact in cash. If enough cash is extracted, negative

interest rates will simply have no effect. We believe the measures proposed in

the current Bill are truly about enabling negative rates, yet this is not

mentioned within the Bill. This is misleading and deceptive. The true

motivations should be on the record. But it explains the short time frames.

Households and Businesses Would Be Trapped In The Banking System. If such a ban was introduced households and businesses would be forced to use the banking system, meaning that bank charges could not be avoided, which benefits banks, not their customers. In addition, we have seen recent system and power failures which have caused disruption to the electronic payments systems. If cash is less available and restricted, a failure would be even more significant and inconvenient and could damage the economy. Once in the banking system, funds can be monitored and controlled (seen by the Taskforce as a positive move – we disagree), but such control could limit access to cash and transactions in general in a crisis. And we note from our SME surveys that many businesses, especially in rural and regional Australia regularly use cash as electronic alternatives are not available. Finally, offering cash for a discount, which is part of legitimate everyday business (because bank charges are avoided) would be removed.

The Structure Allows Change by Regulation Subsequently. The structure of the Bill enables parameters to be changed subsequently by regulation (not via Parliament). This opens the door to removing some of the concessions contained in the current drafting by agencies without full scrutiny. The bill is therefore open ended with regards to crypto, precious metals and other carveouts. In addition, we note surprisingly, government transactions, and cash transactions in Casinos are carved out, which again flags concerns about the structure and limitations of the bill.

A Reduced Limit Could Be Waived Through. Whilst we note that the $10,000 limit would require Parliamentary approval, in practice this could be made without full debate – as illustrated by the passage on the recent APRA bill, or as part of an omnibus “procedural” bill which masks the true intent. It is important to note that where cash transaction bans have been introduced, the value ceiling has been lowered. France has legally prohibited cash transactions above 1,000 euros, Spain has legally prohibited cash transactions above 2,500 euros, Italy has legally prohibited cash transactions above 3,000 euros, and the European Central Bank ended the production and issuance of its 500 euro note at the end of 2018.

In summary, my overriding concern is that Parliamentarians

will only consider the narrow tax efficiency aspect of the Bill and vote it

through without grasping the true intent and consequences. Civil liberties are

being eroded, and the trap will be set to force households and businesses to

transact within the banking system, thus facilitating experimental monetary

policies, via the back door.

Economist John Adams and Analyst Martin North discuss the recent Treasury FOI response relating to the Cash Restriction legislation which was open (briefly) for public comment.

There is still time to make a submission, and stop this from becoming law. Our civil liberties depend on it.

Here’s how you make a submission: email economics.sen@aph.gov.au

Address to: Senate Standing Committees on Economics, PO Box 6100, Parliament House, Canberra ACT 2600

Some points to consider:

Civil liberties – cash is legal tender and you have the right to privacy and to not use a bank; you don’t want government and banks to “monitor and measure” everything you do.

Practical benefits of cash – power supplies and communications technology not always reliable; instant settlement of payments so can be better for commerce, good for discounts etc; whatever else.

Excuses for the law are false. Eliminating the black economy is a lie and won’t work: Australia’s black economy is small and shrinking, and cash restrictions have not reduced black economies in Europe, in fact the opposite.

Restricting cash won’t stop tax evasion, because the majority of evasion is done by large corporations and bank, assisted by the Big Four accounting firms – who want this ban. As Andrew Wilkie said, the government has enough laws to crack down on money laundering and the black economy – use them.

Real reason is to trap Australians in banks. This is explicit from the IMF: Cashing In: How to Make Negative Interest Rates Work. Won’t be able to escape negative interest rates, or bail-in.

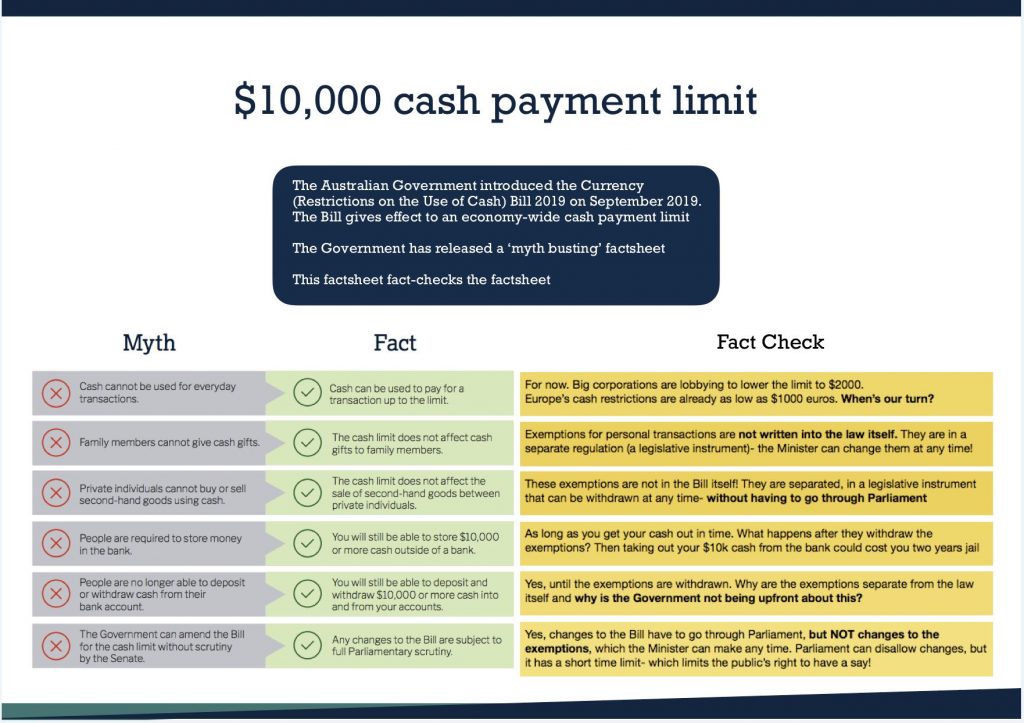

Finally, government’s reassurances are fake, not guarantees. Treasury issued a fact sheet, which Melissa Harrison quickly refuted: exemptions aren’t contained in the legislation, just in the regulation that is easily changed.

Here is a show about my submission to the Senate Inquiry into Audit in Australia, where I focus in on the key issues, show some of the gaps in the current system and suggest reform. Submission close on 28th October if you want to have your say!

Submissions close on 28 October 2019. DFA has made a submission.

Introduction.

We welcome the current inquiry and note the similar

initiatives underway in several other jurisdictions. This is an important

issue.

We believe there is a need to refocus the auditing practices

which are currently deployed by the “big four” firms in particular and the

industry more widely. We reach these conclusions, having analysed the financial

sector for more than 30 years, as a consultant, financial firm employee and a

partner within Arthur Andersen before its dissolution.

There are many threads to the argument, but, these large

audit firms are in our opinion too close to management of large companies, as

they both advise them on strategy and tax minimisation, and separately provide

audit services. In addition, these big four firms are responsible for the

evolution of accounting standards, including off-balance sheet minimisation, as

well as providing advisory services to companies and Government, and they also offer

auditing capabilities. Conflicts abound.

Whilst in theory audit practices should be separated from

other commercial and advisory operations of the big four, I have seen examples

when company account planning sessions have included cross discipline

discussions, from advisory, consulting, services AND audit, to craft strategies

to maximise the commercial benefits to the audit and consulting firm. This

happened regularly at AA.

In addition, the audit of large companies are executed in a

formulaic and superficial way, where the main test is the need to meet relevant

accounting standards, not separately confirming independently that the business

is functioning as advertised from a financial and compliance perspective. Who audits the auditors?

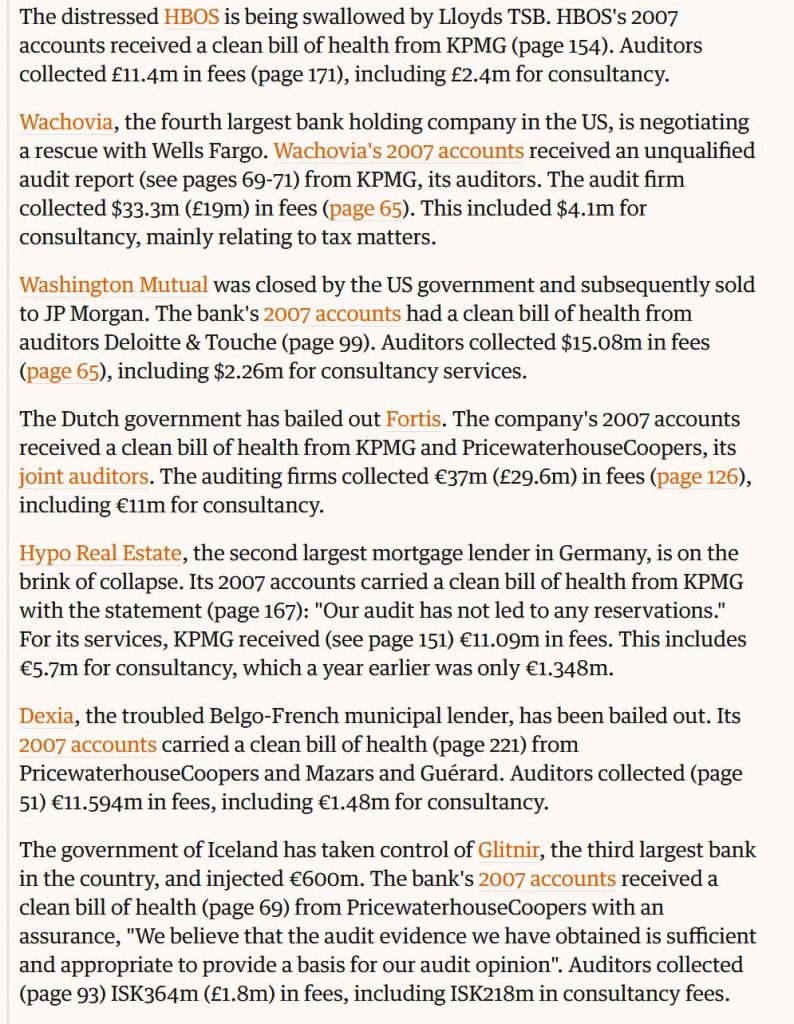

Remember that in 2008 several banks failed, despite having

been given an unqualified audit in the months prior. Others required

substantial Government bail-out or were absorbed by other industry players.

Nothing has changed (other than the quantum of debt and other exposures have

increased substantially) since then.

A Financial Services Example.

To illustrate the limitations of audit, I will highlight

four areas, where from my research and experience current banking sector audits

are deficient.

Financial Derivatives Exposure.

According to recent RBA data Australian banks have some $48

trillion of gross derivatives exposures. This will include services to client,

but also position taking on a trading basis within the bank’s treasury

operations. Recent BIS research highlighted that in a low interest rate

environment, banks will tend to lend less and trade more to try to bolster

profits[i]. Plus, some window-dress their books for

quarter end.[ii]

Derivatives gross exposures dwarf the capital and assets

held within banks. This gross exposure is not reported clearly within the

accounts, because most is held off balance sheet. Moreover, the true

net-exposure which a bank may face will be determined by market movements and

relative trading positions. But even net exposures are not adequately reported.

We only get a glimpse of the true positions (and risks) when capital is applied

under the Basel rules, but this does not tell the full story, yet are within

current accounting standards, and off-balance sheet rules. We see no evidence

of auditors picking through the derivatives book and validating or reporting

these gross exposures. In a crisis this may well hit the financial position of

an individual bank, and trigger the need for a restructure, bail-in or

bail-out. Current audit rules and

approaches are designed to minimise disclosure and obscure the true risks. APRA does not provide an alternative route to

disclose such risks.

Internal Risk Models

Major banks can use their own “internal risk models” to

estimate the amount of capital applied to the business, under the Basel rules.

These models are complex and “tuned” by the institutions to enables

institutions’ to maximise their use of capital. However, we are not convinced

these models are functioning as intended, and they are not subject to regular

audit, either by external auditors, or APRA. Thus, the data is taken as

accurate from the “black-box” and this may lead to higher risks in the business

than are disclosed. Again, the true

position will not be exposed until a crisis hits.

Property Portfolio Revaluations

Large financial companies hold significant portfolios of

mortgages backed by residential property. An initial valuation is used in the

underwriting process. However, unless there is a material refinancing event,

subsequent portfolio adjustments, (because for example property prices move

down) are applied only at an aggregate level (for example state level). As a result,

there is a significant risk the property portfolio is overstating the real

current value of the underlying security, and this may translate to bigger

risks in a downturn. In addition, the amount of capital held under Basel rules could

well be understated. There may be offsetting benefits in a rising market, but

the standard portfolio analysis is not very accurate. But once again external

auditors will be not examining the operation practices of portfolio valuations

yet will sign off on the accounts as true and accurate.

Household versus Loan Risks

Households often hold multiple loans across a lender or

lenders. APRA only considers the status of individual loans. Reporting for

audit purposes will be at a loan, not household level. Indeed, there are cases when loans are

deliberately split to reduce the overall loan to value results. Once again this

is an area where auditors will not tread, but the risks in the system are

higher than those reported in the accounts. Again, the true position will not

be exposed until a crisis hits.

These are just examples of pain points which the current

audit processes will not adequately examine. There are many others.

Final Observations

The role of an auditor should be more than just checking

with the accounting standards and signing off. They should be seeking out

material issues, independently from management. But in the four cases above the

results are wanting.

The solution would be to create an independent audit

function, perhaps within the Auditor General’s domain, to provide accurate and

independent analysis of large financial players. In addition, we believe that

the audit functions of major firms should operate as separate service businesses

and should NOT be also be allowed to offer creative accounting and off-balance

sheet techniques as part of their service suite. The conflicts and limitations

are obvious and concerning.

However, the true impact of such deficiencies would only be

revealed in a crisis, mirroring 2008, by which time it is too late. Changing

management and audit practices as suggested would place our important financial

sector companies on a firming footing. Such changes could well benefit other

industry sectors as well.

Changes to audit practice and structure are essential!

[iii]

Digital Finance Analytics is a boutique research and advisory firm. More

details are available via our Blog. https://digitalfinanceanalytics.com/blog/

We discuss recent development in the proposed cash transaction ban, with the help of a recent Saturday paper article and CBA’s systems failures today. Cash is king!

APRA took a question on notice relating to the average size of mortgages from Senator Peter Whish-Wilson during Budget Estimates, and the answers have just been released.

The questions are sensible, the answers once again show how myopic the data APRA produces is. They only report the value of loans and number of loan accounts on the ADI’s books). Nothing about household exposure across multiple loans. Who then is, I ask?

Questions:

What method does APRA use to calculate the “average balance of housing loans” as provided in the publication Quarterly ADI Property Exposures?

How does APRA account for mortgage offset (redraw) accounts in its method?

How does APRA account for instances where there is more than one loan on a property (‘loan splitting’) in its method? Does APRA tally the total of all loans against a property; or does APRA tally individual loans, regardless of whether there is more than one loan on a property?

What is the extent of ‘loan splitting’? How many properties have more than one loan against them? How many properties have more than two loans against them?

What is the average value of loans where there is more than one loan against a property?

Where there is more than one loan against a property, what proportion is fixed interest and what proportion is variable interest?

Where there is more than one loan against a property, what is the average value of fixed interest loans and what is the average value of variable interest loans?

What is the extent of ‘loan splitting’ being undertaken by different ADIs? In particular: what is the extent of ‘loan splitting’ by the major banks?

Answer:

The average balance of housing loans in Quarterly ADI Property Exposures (QPEX) is a simple average calculated as the aggregate balance of all housing loans, gross of offsets and provisions, divided by the number of loans. It is important to note that QPEX reports data from the ADI’s perspective and not the customers (e.g. the value of loans and number of loan accounts on the ADI’s books).

APRA does not consider the average loan size to be a reliable indicator of risk. ADIs are required to assess the borrower’s ability to service each loan, and the amount of security against each loan taking into account all borrower liabilities. APRA’s expectations are set out in Prudential Practice Guide APG 223 Residential Mortgage Lending (APG 223). ADIs are required to report to APRA on the value of new loans originated without fully meeting the ADI’s serviceability standards.

Offset accounts are considered a deposit liability and do not reduce an ADI’s housing loan exposure.

APRA does not adjust for loan splitting in QPEX reporting. However, under APG 223 the ADI is expected consider the customers’ aggregate exposure in the serviceability calculation and available security when originating housing loans.

APRA does not collect information on loan splitting, by loan type, or across institutions. In addition the focus on the LOAN not the customer exposure.