BANKING red tape is robbing more than 880,000 of Australia’s two million small and medium sized businesses of four weeks’ productive work time a year, costing the national economy almost $7 billion annually, new research has found.

This equates to an extra 20 working days a year – or the entire annual holidays of the average employee.

Tyro’s Exploring banking inefficiencies for SMEs report has found that 44 per cent of Australian SMEs, or 880,000 businesses, spend more than three hours every week checking, entering, paying and reconciling data, costing each business an average of $7,800 a year.

The findings of the survey reveal the seven major pain points in terms of productivity when it comes to online business banking and related activities.

Tyro’s report also found that:

700,000 businesses, or 35% of SMEs, believe their bank could be doing a better job.

One million, or 50%, of SME owner/operators are doing their own bookkeeping.

400,000, or 20%, of SME owner/operators don’t use any form of accounting software.

“Large companies, with more than 200 employees, make up only 0.3% of businesses operating in Australia,” Tyro CEO Jost Stollmann said today. “By comparison, small and medium sized businesses are the creative and innovative heart of the Australian economy, generating more jobs than any other sector. “But SMEs are drowning under the burden of inefficient online business banking processes, that are robbing them of three hours a week, or 20 days a year.

“This means SMEs have to work a 13-month year, or give up the equivalent of four weeks’ annual holiday to compensate for banking inefficiencies.”

The findings explain why a staggering 700,000 SMEs are unhappy with their business bank’s performance. Mr Stollmann said efficient online banking was critical to the success of SMEs and for a large proportion of Australian businesses their bank was letting them down. “Banks need to try harder to reduce the burden on Australian businesses,” he said. “It is clear that business banking requires a rethink. It needs to be mobile, embedded into business and accounting software and fully automated. “The winners in the business banking of the future will marry deep technology and banking know-how.”

Despite SMEs playing a critical role in the Australian economy, their contribution to GDP has slowed since 2012.

Mr Stollmann said the priority was to establish what the major pain points were for the industry and help SMEs drive future growth.

Billions of dollars have been spent by the private and public sector to assist SMEs, particularly around improving workplace participation.

However, very little has been done to address the issues of access to capital or business and banking improvement processes.

Mr Stollmann said SME banking was an industry in transition, and the major providers needed to make it easier for customers to do business.

“Australia’s small and medium sized businesses are developing into the most attractive banking customers in the country.

“From a market that was once considered very niche and challenging to serve, SMEs have now become a strategic target for banks,” he said.

“This flows on from the 2008 financial crisis, when banks began to shift their focus away from large corporates in an effort to seek high yields in a low interest rate environment.

“Banks now see SMEs as core to their business.

“Australia should be looking at action to improve SME productivity, in recognition of the changing terms of trade and resources decline. We should help SMEs operate more efficiently.”

Commonwealth Bank of Australia CEO Ian Narev acknowledged this recently when he said CBA had to innovate or die.

“If we don’t innovate successfully, we’re toast,” Mr Narev told free-market think tank The Centre for Independent Studies in June.

“Not we’ll lose a bit of profit, we’ll lose a few customers — we’re toast. And I’m talking over a decade, not over six months, but it is an existential imperative for us to innovate.”

I had the opportunity to catch up with the joint CEO’s of the SME digital market place, Proquo – Carl Spurling, from NAB and Ricky Lam from Telstra, to discuss the development of the platform and their future plans.

Proquo was formally launched a couple of months ago, following research in 2015 with SME’s from NAB’s SME Village and Telstra’s Gurrowa Labs. It uses a custom built software platform to enable SME’s to build a network of contacts and to trade with each other, for cash or in kind. Proquo say they are well on their way to acquiring their target of 2,000 customers in the first six months, from across the country.

We discussed the motivation for the launch of the business. Both NAB and Telstra have strong interest in the SME sector, and recognise the importance of getting SME’s digitally enabled. They cited research showing that 40% of SME’s were not online at all. They said they had identified a real need to provide an onramp for SME’s, and so spotted the opportunity to create the marketplace.

Now Proquo offers small business owners and accounting experts access to a range of services from other providers. Users can create briefs for the work they need, provide quotes, manage payments and publish reviews, all on the one platform. Micro and small business owners, as well as experts in the accounting industry are invited to register for free to take advantage of this tool to aid networking and help their business thrive. The services offered under the accounting umbrella include: Budgeting, Book keeping, Xero, tax and many more.

They want to focus, rightly, on getting the core platform running smoothly, and acquiring new customers. However, we discussed some of the potential extension strategies which might be considered later.

First, the data which is being captured in the system has the potential to be used for many purposes. For example, individual SME’s could be rated, just like other digital marketplaces, as part of building a network of trusted contacts. They have no firm plans to offer loans, but with the NAB connection, it is certainly an option for later.

Another angle could be the consolidation of purchases, via ecommerce, thus enabling individual businesses to gain group discounts. Again, for now, group buying is not enabled, but could be in the future.

We also discussed the thorny tax issues around offering services in kind. The ATO of course says that barter transactions will have a tax implication. So it will be important to track and manage this aspect. Whilst Proquo can generate a range of documents, they will not be offering tax advice. That said, within the network there could be Accountants who could help. We think there is an opportunity for Proquo to embed this type of tax reporting in the system.

Finally, today the platform is web based, and optimised for mobile, tablet and PC. Down the track, they may well consider a dedicated app, but only once the core functionality has been bedded down.

For now, Proquo is focussing on getting established with a high-quality portfolio of businesses. They will measure success by how successful customers on the platform will be, and how much value SME’s gain from it. Whilst it is a for-profit business in the long term, their initial focus is on building momentum and value for their customers.

We think this is an excellent example of digital innovation, and has the potential to assist many SME’s, who in the early years especially find building a network of customer’s hard work, and funding difficult. In fact, half will fail in their first five years in business. Proquo looks like a good catalyst and the SME sector should welcome the innovation it represents.

Kabbage is one of the most interesting platform lenders offering loans to SME’s in the US, and now Canada, Mexico and via white label platforms other countries, including Australia. Their analytic platform takes business activity data such as online sales and accounting information to facilitate fast underwriting in just a few minutes. Loans of up to $100,000 are available to businesses with a turnover of $50,000 or more.

The Kabbage platform has originated more than US$1.6 bn in loans, via Kabbage, the SME platform, Karrot, their consumer lending business and via white labeling to third party lenders. Kabbage is funded and backed by leading investors including Reverence Capital Partners, SoftBank Capital, Thomvest Ventures, Mohr Davidow Ventures, BlueRun Ventures, the UPS Strategic Enterprise Fund, ING, Santander InnoVentures, Scotiabank,and TCW/Craton.

In 2015 Kabbage announced plans to move into the Australian market with a white-label offering of its small business lending technology. The launch in Australia represents Kabbage’s first foray into the Asia-Pacific region, having already been in operation in both the U.K. and the U.S.

The service in Australia is operated by Kikka Capital, which licensed the platform and manages marketing, funding, and loan servicing. Kabbage handles underwriting and management of the loans.

Here is an interesting post where Kabbage discuss small business funding options. We have previously discussed the difficulty SME’s face in getting access to funding, and the role of fintechs have in changing the lending landscape. The latest Disruption Index measures the growth in momentum for SME lending in Australia.

Many small business owners might at some point find it difficult to get working capital or a small business loan from a traditional bank – and in that situation, it’s important to know about the various alternative loan options that are available.

According to a recent article in the Harvard Business School “Working Knowledge” blog, as of May 2014, only 13 percent of applicants for small business loans at big banks were getting approved. The SCORE organization has found that small business owners are less likely to get a bank loan if their business is young (less than 2 years in business), if they have less than perfect credit (credit score below 640) and if they are seeking a relatively small loan amount (less than $250,000). Big banks tend to prefer to issue larger loans than most small business owners need, because the banks’ costs of issuing loans are not much smaller for small loans than they are for big loans.

According to a survey published in an article in the Wall Street Journal, 19 percent of small business owners have postponed investments in their businesses because of lack of loan funding, and only 18 percent could get a bank loan – faced with a lack of funding from traditional sources, 17 percent of business owners borrowed money via credit cards, and 13 percent asked their friends and family for loans. Small business owners are starting to get more creative in looking for alternative loan options when they cannot get what they need from the traditional bank lenders.

One of the biggest new trends in helping business owners find alternative loan options is the rise of platform lending. With platform lending, borrowers can get the money they need without relying on the traditional bank system. A study from Harvard Business School found that in 2014, although the total loan volume of small business bank loans decreased by 3.1 percent, overall online lending to small businesses grew by 175 percent. This is a sure sign that platform lending is on the rise and is taking the place of traditional lenders.

With so many business owners seeking loans and finding it more difficult to get approved by traditional bank lenders, it’s no wonder that new options like platform lending are starting to fill the gap. Platform lending is an innovative new way to get loans, where people can sign up online, go through a faster, efficient approval process and get the funds they need more quickly than a typical bank loan.

If you’re looking for a small business loan and wondering how to navigate the alternative loan options such as platform lending, here are a few guidelines on how to evaluate each of your options:

Loan from Family and Friends

Borrowing from family and friends is often a first-resort loan for many small business owners. After all, the people who know and love you best are often eager to support you in your business endeavors. If you want to let your family and loved ones in on a great investment opportunity, selling equity in your business or asking for a small business loan could be one way to get the cash you need.

Advantages: Friends and family typically know you best, and they will believe in you and support your vision of success, even if a traditional bank lender cannot offer you a loan. It’s natural to want to turn to your inner circle first. And your family might be willing to give you more favorable payment terms – lower interest rate, longer time to pay off the loan, etc. – than a typical bank would.

Drawbacks: First of all, it can be hard to raise enough money just by asking your family and friends. Unless your family are a bunch of angel investors, they might not have enough money to spare to be able to fund a significant business investment. And even if you can get enough money from them, borrowing from friends and family can be risky – not only in a financial sense, but also emotionally risky. After all, what if your business idea doesn’t work out? What if you lose your family’s money? What if your business becomes a source of hurt feelings and damaged relationships with the people you love most? It’s often better to keep business and family concerns separate from each other.

Crowdfunding

Other small business owners look for alternative loan options by using crowdfunding. By setting up an online crowdfunding campaign, your business can ask your social media followers, friends and fans to contribute money to help fund your business’ next phase of growth.

Advantages: Online crowdfunding platforms like Kickstarter, GoFundMe and others give you the power to raise money to support your business, whether it’s funding for new product development or for any other specific purpose. By giving away prizes and using other participation strategies, you can motivate people to give more money – for example, by giving donors a special behind-the-scenes experience or an early-stage sample of your new product.

Drawbacks: Crowdfunding is flexible and adaptable, but that same flexibility can also make the results unpredictable: according this Kabbage article, the typical crowdfunding campaign takes about 9 weeks and raises an average of $7,000. Depending on how much time you have and how much money you need, crowdfunding might not be the best fit for your goals.

Platform Lending

With banks making it more difficult for small business owners to get loans, a variety of online services known as “platform lending” services have come onto the market. Kabbage is one of these online platform lenders where business owners can get loans more quickly and often more effectively than they could from a traditional lender.

Advantages: Platform lending is often a good option for people who have less-than-perfect credit. Also the loan amounts offered by platform lending services are often a better fit with what small business owners are seeking – for example, $40,000 to $100,000. Another advantage of platform lending is that the approval process is more flexible and relevant to small businesses than the traditional bank loan process; for example, platform lenders tend to look at a business’ online sales and social media following and other metrics to show the creditworthiness of the business that are separate from the traditional approach of looking at credit scores.

Drawbacks: Platform lending tends to charge a slightly higher interest rate than a typical bank small business loan. Make sure to do your research and understand the fine print of any platform lending agreement before you sign – just like you would if you were signing up for a new credit card or other financial product.

If your business is struggling to get approved for a bank loan, don’t get discouraged – get money! There are more alternative loan options than ever before, especially if you are able to be creative and flexible and pursue some new services like platform lending.

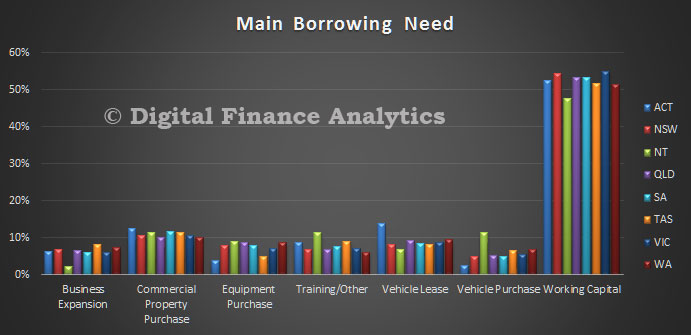

The DFA SME survey underscores that payment terms for many businesses continues to extend, creating real headaches in terms of cash flow, profitability and sustainability.

Using date from our latest results, from 26,000 business owners, we see that working capital is the main reason to borrow.

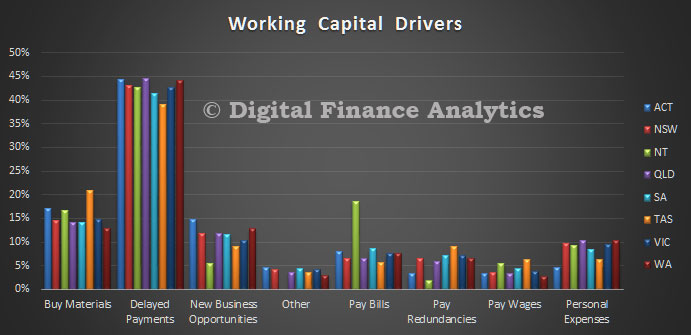

The main driver of working capital is delayed payments. There are significant variations by industry, with those in the transport sector the worst hit.

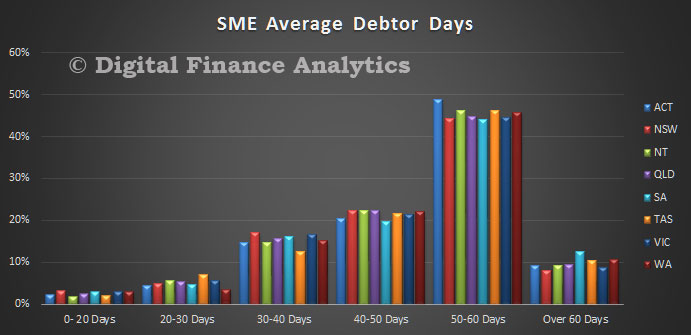

Nearly half of payments are received between 50 and 60 days after billing. Over 60 days includes some payments to more than 120 days due.

Businesses told us that they are getting squeezed harder as larger companies and government departments hold up their payments for longer. You can read the last SME report, released in late 2015. The next edition will be released shortly.

We are not the only ones highlighting this issue. According to The West Australian today:

Up to eight contracting businesses are going under each week, an equipment hire industry figure says, with late payment by clients the main cause.

Sally McPherson, chief executive of online equipment broker iSeekplant, called on governments to crack down on ballooning payment periods.

Ms McPherson said two to three members of iSeekplant had failed per week in WA over the past six weeks. Information about the other collapses came from the broker’s State office.

The victims ranged from owner-operator outfits in construction and mining to businesses with about 150 machines.

Many were mid-market players with 20 to 40 trucks, loaders and excavators.

Ms McPherson said some collapsed operators were re-emerging as new companies after escaping debts.

“We’re seeing definitely the worst conditions in the plant and equipment market for 30 years,” she said.

She blamed client payment periods of 90 to 120 days.

“It’s the number one factor,” Ms McPherson said. “Big companies are leaning on these tiny enterprises for their cash flow.

“The margins on hire in WA, if at all profitable, are razor-thin. These companies go under just purely because of cash flow. The bank doesn’t ever give them a 120-day break on their payments. It’s not fair.”

Ms McPherson said small contractors agreed to such contract terms because of the larger companies called the shots.

“Government should step in and stipulate what’s a fair term considering that it’s government money,” she said.

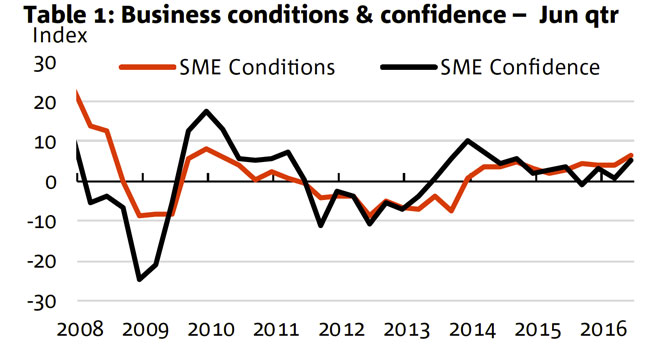

The latest NAB Quarterly SME Survey, to June 2016, suggests the non-mining recovery is broadening to include smaller businesses, with SME business conditions highest in six years, and confidence above long-term average despite some increased pressure on cash flow, and falling forward orders.

Business conditions for SMEs gained further traction in Q2, rising by 2 points to +6 index points, a level not seen since 2010 and comfortably above the long-run average of +4. It is especially encouraging that low and mid-tier firms reported notable improvements in conditions and confidence in the quarter. In particular, low-tier firms reported positive business conditions for the first time in 2 years.

All three components of business conditions rose in the quarter. Trading and profitability conditions surged ahead, reaching levels not seen since 2009. Employment conditions however remain lacklustre. The optics of conditions by firm size were also quite encouraging, with all size categories reporting positive results for trading and profitability conditions, although demand for labour by low-tier firms remains soft.

Meanwhile, SME business confidence rebounded to +5, above the long-term average of +2 index points and more than reversing the fall in the previous quarter. It is worth pointing out that the survey was conducted prior to the Brexit decision and federal election and therefore does not reflect the possible shifts in sentiment due to these political events. However, our latest monthly NAB Business survey for June, which was polled during Brexit (but before the election), did not show an adverse impact on confidence.

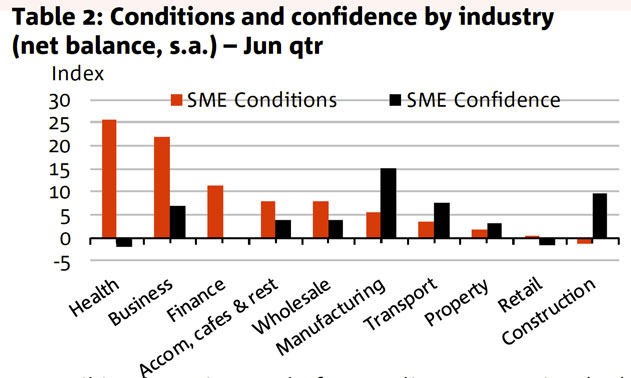

In level terms, all SME industries except for construction reported positive business conditions in Q2. The health sector outperformed other industries in the quarter, followed closely by business services, while retail was the weakest after construction. Meanwhile, there has been more evidence of late that the wholesale sector is experiencing a recovery in its business conditions.

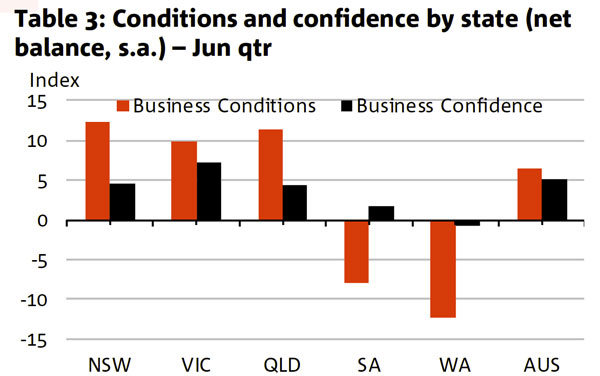

All states, except for WA, reported better business conditions in Q2, with QLD showing the biggest improvement again (up 10 points to +11). NSW and VIC continued to outperform, while WA has lagged further behind the national average. All states were more confident in the quarter, with VIC being the standout, while WA was the least confident and the only state to report negative confidence.

Leading indicators were stronger in the quarter as well, with capacity utilisation rising to levels last seen in 2011, while capex reached the highest level since 2007. Overall, SME input price indicators point to relatively contained price pressures, while easing price growth for retailers is consistent with the subdued inflation outlook.

“We’re continuing to see an increasing number of contacts from the Australian SME sector. These contacts have been particularly concerned about misleading conduct by other firms, consumer guarantees, and agricultural issues,” ACCC Deputy Chairman Dr Michael Schaper said.

The ACCC’s six-monthly Small Business In Focus report #12 has been released today, providing an update on key developments in the small business, franchising, and agriculture sectors.

For the first time, information on the agriculture sector has been included. The ACCC received more than 200 agriculture-related enquiries and complaints, principally focussed on potential misleading conduct or false representations made by other business operators.

Other key developments in the last six months are also highlighted in the report:

there have been more than half a million visits to the ACCC’s business web pages;

the ACCC continues to receive reports of losses to scams targeting small businesses, with $1.6m lost;

Coles, Woolworths, and Aldi are now required to comply with the entire Food and Grocery Code

there were more than12,000 users of the ACCC’s online education programs.

“The number of small businesses contacting the ACCC with concerns has risen steadily over the past few years. The current review of the Australian Consumer Law (ACL) provides a valuable opportunity for small business to speak up and ensure that their concerns are taken into account during that process,” Dr Schaper said.

“Concerns about changes to new credit card surcharging laws in September, and new changes to the ACL that will extend protections from unfair contract terms in business-to-business dealings in November are expected to generate significant interest from the Small Business community.”

Accounting software developer Reckon has announced it will offer loans through an agreement with small business online lender Prospa, as the company extends its suite of financial services accessible to its customers. The introduction of business loans adds to recent news flow, with Reckon partnering with OFX to provide low-cost international payments and PayPal to unlock online credit card payments for companies without card processing facilities.

Small businesses loans of between $5,000 and $250,000 will be available, with terms range between three and twelve months and with daily and weekly payment options available.

Applications are made via Reckon and assessed by Prospa who can give approval inside 24 hours. The health of a business is evaluated by Prospa using a proprietary technology platform to rapidly determine the borrowers lending capacity. The process is significantly faster than traditional loan approvals.

“Data from accounting software used to evaluate cash-flow is seen as the best measure of business fundamentals, helping to determine the businesses ability to repay and manage risk during the life of a loan”, Reckon CEO Clive Rabie said.

“This ability to provide data to a bank or fintech player so that they can do a real-time credit check and provide safer loans to small business is disrupting this space,” said chief operating officer Daniel Rabie.

Reckon will continue to look for additional services and partnerships.

Established in 2011, Prospa has funded more than $150 million small businesses loans.

Non-major lender Suncorp Bank has launched online submissions for small business lending, in a move which it touts as an “industry first”.

Brokers lodging small business loan applications to Suncorp will now be able to do so electronically via NextGen.Net’s ‘ApplyOnline’ system. The non-major says this will translate to increased efficiencies, faster turnaround times and improved functionality for brokers.

Suncorp’s national small business manager, Robynne Frost, said the new process is one the solutions Suncorp is offering as a part of its commitment to support brokers diversify into small business lending.

“Suncorp Bank is committed to investing in technology to improve the lending experience for brokers and their customers,” she said.

“The addition of small business lodgement through ApplyOnline enables brokers to easily transition from home loans to small business with a streamlined ‘combination’ application.”

The non-major is also offering SME Masterclasses, BDM support and improved commissions for brokers operating in the SME sector.

“The SME sector represents a significant opportunity for our broker partners and Suncorp Bank is committed to supporting them as they look to expand and diversify their businesses,” Frost said.

NextGen.Net sales director Tony Carn said this announcement is market leading.

“Suncorp Bank has again shown market leadership in the broker channel through the rollout of ApplyOnline electronic lodgement for small business loans.

“In such a competitive and ever-changing market it is great to see Suncorp Bank going above and beyond to meet the needs of Australian brokers.”

According to The Australian Business Review, PayPal Working Capital has extended more than $85m to about 3,000 small businesses since launching in Australia in late 2014.

In contrast, Prospa — the biggest “fintech” online small business lender — in May revealed it had cracked the $150m mark after four years of operations.

SocietyOne, the biggest “marketplace” lender, which has also been in business for four years, pushed through $100m personal loans in April.

There’s a one-off upfront fee and repayments come out of daily sales, typically between 10 per cent and 30 per cent of turnover.

Interest rates are typically in the “teens and 20 per cent” range, differing based on merchants’ repayment choices and risk.

Including the US and Britain, PayPal Working Capital recently surpassed $US2 billion ($2.6bn) in loans. While Australia makes up a small piece of the pie, the business is profitable.

The ACCC alleges that ABFC website, and its sales representatives, purport to offer access to an online database of the Australian government grants and loans available to small businesses. Small business owners paid fees ranging from $497 to $701 to access the database, only to find there were no suitable grants or that they were ineligible for grants listed.

The Public Warning Notice alleges ABFC has made false or misleading representations about the service’s capability and quality, and the role the service has played in assisting small businesses gain government grant funding.

The website also prominently features a range of “success stories” from actual Australian small businesses, but when those businesses were contacted by the ACCC, they said the stories were used without their permission and that they had not obtained any government funding via ABFC.

“The ACCC is issuing a warning in relation to ABFC’s conduct including its australiangovernmentgrants.org website. We are very concerned that small businesses are paying ABFC for a service that does not provide the information and assistance they are have paid for,” ACCC Acting Chair Dr Michael Schaper said.

“Similar websites targeting small businesses in other countries have also come to the attention of regulatory authorities in New Zealand and Canada.”

“Small businesses should take care when assessing offers to assist them in obtaining government grants. The bottom line is that information relating to government grants is generally available free of charge from a variety of state and federal resources online,” Dr Schaper said.

The ACCC says despite the australiangovernmentgrants.org including an Australian address, it is operated by ABFC’s sole director who is based overseas.

Legitimate information about government grants can be obtained for free at www.business.gov.au and other websites ending with .gov.au.

Tyro’s report also found that: