FinTech Moula Money has announced that it has closed a $30m investment round led by Liberty Financial Pty Ltd, NCN Investments and a group of private investors. Moula was the first lender of its kind in Australia, providing small businesses with access to funding by using multiple data sources to rapidly assess creditworthiness. They also increased the available loan size to $100k. We covered Moula’s business model in a recent post.

Tag: SME

Why the Small Business Tax Break Could Pay for Itself

The immediate tax deduction for small business announced in the Federal Budget has been broadly welcomed, but what may have been missed is the fact that what the Government doesn’t collect now, it will collect later, according to The Conversation.

As part of the $5.5 billion small business package at the centre of its latest Budget, the Federal Government announced it would allow businesses with turnover less than $2 million to immediately deduct the cost of any individual asset purchased up to the value of $20,000, from Budget night through to the end of June 2017. The estimated cost of this accelerated depreciation measure to revenue is estimated at $1.75 billion over the four years of forward estimates.

But what should be noted about this measure is that it doesn’t change the eligibility for tax deductions of these assets; it simply changes how quickly a small business is able to receive the tax deduction.

Under the existing simplified depreciation rules for small business, an asset costing over $1000 would be depreciated at 15% for the first year, and 30% thereafter, until the taxable value of the asset pool is $1000 or less, at which point the full amount can be written off.

For a $20,000 asset, this would mean a $3,000 deduction would be allowable in the first year, and it would take around 10 years to fully depreciate it for tax purposes. This compares to a $20,000 deduction in the first year under the proposed measure.

Bear in mind, too, that small businesses fall into two general categories: those that are incorporated (companies), and those that aren’t (sole traders and partnerships). The taxable profits of small companies are taxed at a flat rate, which – assuming the announced 1.5% tax cut passes – will be 28.5%.

Unincorporated small businesses don’t get the 1.5% tax cut, as their income is included in the assessable income of the owners and taxed at their marginal rate of tax. Instead they’ll get a tax discount of 5% of business income up to $1000 a year.

Here, we’ll focus on small companies, where the flat rate of tax makes analysis easier.

For a small, incorporated business, and assuming the 28.5% tax rate, its tax bill would be reduced by $5,700 in the first year, as compared to only $855 under the existing regime. This is a total upfront benefit of $4,845, and supports the government’s argument that the change will improve cash flow for small business as compared to existing arrangements.

But the timing aspect also has a benefit for the Government, and there is evidence of this in the Budget Papers. Over the first three years of the forward estimates, the expected cost to revenue totals $1.9 billion. However, in the final year of the forward estimates (2018-19), this cost begins to reverse, and the Government expects to bring in an extra $150 million in revenue.

The reason for this reversal can be explained with respect to a hypothetical $20,000 asset purchased on July 1, 2015, by a small incorporated entity. Under the proposed rules, the company would have reduced its tax payable by $5,700 in the first year, as compared to only $855 under the existing rules.

The reason for this reversal can be explained with respect to a hypothetical $20,000 asset purchased on July 1, 2015, by a small incorporated entity. Under the proposed rules, the company would have reduced its tax payable by $5,700 in the first year, as compared to only $855 under the existing rules.

This means the Government would collect $4,845 less tax from this company in respect of the 2015-16 tax year. However from the 2016-17 tax year onwards the Government will collect more, under the proposed measure, as this company has no further depreciation tax deductions available to it in respect to that asset.

This means that while over the forward estimates period, allowing this company to immediately deduct the cost of the asset in 2015-16 will cost the Government $1,662, it will subsequently collect $1,662 more in tax in the period beyond the forward estimates.

Mechanically, the total deduction for the asset under either the original simplified depreciation rules for small business or the proposed immediate write-off, will still be $20,000. In other words, whatever the Government doesn’t collect now it will collect later.

For the Government this is a good outcome politically for three reasons.

For the Government this is a good outcome politically for three reasons.

First, it allows it to say it is supporting small businesses to “have a go”, as Treasurer Joe Hockey puts it.

Second, even though there is a cost to revenue in the forward estimates period, over the following years this measure will have a positive impact on revenue. However, because this increase in revenue is primarily outside the forward estimates it is not visible in the Budget Papers.

This increase in revenue has to be equal to the cost – so the $1.75 billion net cost in the next four years will lead to an increase in revenue of $1.75 billion beyond the forward estimates.

Third, the Budget Papers contain only information on government decisions that involve changes since the previous Mid-Year Economic and Fiscal Outlook. So while this measure will mean the Government will collect more revenue over the years 2019-20 and onwards, this increase won’t register as a change in next year’s Budget and therefore this increase won’t be quantified there as such.

SME’s Can Get Some Moula

I caught up with Aris Allegos, co-founder of Moula, the Australian online unsecured lender to small business which has been operating for about a year. In that time, business has been growing, with about 250k a week being lent currently, to about 30% of applicants who apply. As we highlighted previously, alternate funding for SME’s is on the rise, with players like PayPal and P2P players eyeing the market.

Moula’s business model mirrors the successful US business Ondeck, using algorithms to assess business applicants based on cash flow and credit history. By linking customers business’ data to Moula, they can automatically view transaction data and make a decision very quickly, and lend to businesses which the banks would not find attractive.

They currently offer loans of between $1,000 and $50,000 for a six month term, with repayments of principal and interest made each fortnight to pay the loan down. Loans are made on balance sheet, so it is not a P2P lender, but is a great example of an emerging online financial player (fintech is the buzz word).

They can lend to a small business or company, but not to an individual, which avoids the Australian consumer credit complexity. An ABN or ACN is required. Applicants on behalf of a company are required to provide a personal guarantee. Moula is regulated by ASIC, not APRA (no deposits, so not a bank), but of course they still have to run AML checks on applicants.

Interest is charged on a fortnightly basis, at 1% per fortnight, or 26% APR. At the moment they have a single rate, although the algorithm they have built supports risk based pricing, and Aris thinks it is likely they will begin to tailor the rate charged in the future, while still ensuring pricing is both fair and transparent.

Borrowers receive the funds into their account, and are given access to the Moula portal, where they can track their transaction. Moula uses Yodlee’s safe, encrypted service to download transaction data from the businees’s bank account. Yodlee provides these services to 9 of the 15 largest banks in the US and 2 of the 4 largest banks in Australia and is considered a world leader in this technology. Interestingly, though about 50% of potential borrowers are reluctant to share security information, so Moula can also hand manual bank statements.

They expect to grow substantially because they are addressing a sweet spot in the market, as banks find it uneconomic to make small unsecured loans to business (especially on the Basel III framework), and many SME’s need short term funding for working capital and other purposes.

According to Aris, so far despite dealing with a few late payers, they have not had to write off any loans, so losses are zero! This would seem to be related to the fact that the SMEs attracted to Moula are experienced, well-run businesses. Moreover, being developed in Australia for Australian SMEs, Aris is confident that their underwriting model is well honed to the domestic experience.

We think this is a good example of an online business which is likely to do well in the Australian market. Not least because the DFA SME research shows that business owners are migrating online fast, and have significant need for short term funding in the current low growth environment.

Customers seem to be happy with the experience, “I’m very happy to recommend Moula. I think they’ve got a great idea. There’s plenty of little e-commerce businesses that can use some extra cash without the headache of reams of paperwork. Moula’s website is attractive and easy to use. The loan approval was super fast & the money was in our account within 24hrs. The whole process was pain free, safe, fast, & affordable. Thank you”.

Finance Through a Fintech is Fast, but Ask These Questions First

Interesting article in the BRW by Neil Slonim, of thebankdoctor.com that aligns with my earlier post on Online Lending for SMEs.

There has been considerable recent discussion about fintechs injecting much needed competition into the SME lending market. For those unfamiliar with this new word, fintech (financial technology) is a line of business using software for the purpose of disrupting incumbent players such as banks. ASIC Chairman Greg Medcraft recently said “the time is ripe for digital disruption and ASIC wants to make it easier for fintechs to navigate the regulatory system”. Notwithstanding these encouraging developments it is still early days and small business owners would be wise to resist the lure of quick and easy money from fintechs until they really understand how they work.

The attraction of fintechs is the expectation of a “quick yes” via a streamlined online approval process. Fintechs usually offer business loans between $5k and $300k and terms generally range from 7 days to 12 months. They make funds available in a matter of days and sometimes even hours. Rates vary from around 9 per cent to 30 per cent and often well beyond. Most loans are made without property security. Fintechs are generally not suited for businesses that have requirements for long-term debt and if you have property security you will get a better rate elsewhere.

Some business owners will try a fintech if the bank either rejects them or can’t make a decision in the time frame required. Others will by-pass the bank based on a preconceived belief that the banks wont help them.

For better or worse most SMEs know what to expect when dealing with banks. They know the big banks have been around forever and have large and strong balance sheets but this new breed of lender is an entirely different species.

Unlike the banking sector where four well known players and their offshoots control around 90 per cent of the market there are already many fintechs in the SME space with new entrants constantly popping up as entrepreneurs see the opportunity to disrupt the big four oligopoly. As more players enter this field, it will be interesting to see how they go about developing and conveying a distinctive customer value proposition.

Australian owned fintechs currently operating in the SME space include Moula, Prospa, getcapital, and ucapital. The US online lender Ondeck is establishing a local operation in conjunction with MYOB and some well-known local investors. The barriers to entry are relatively low and the level of regulation is not as stringent as for banks. Issues such as funding, liquidity and fraud will no doubt come to the fore when the first fintech fails. Liquidity events could lead to unscrupulous fintechs embarking on a Ponzi scheme but we can safely assume that no fintech will be the beneficiary of a ‘too big to fail’ government bailout. If you borrow from a fintech that gets into difficulty how would you refinance a loan that a bank wouldn’t touch?

Borrowing from fintechs is expensive due to relatively high funding costs plus high default rates. Ondeck US’s operation has a default rate of 6 to 7 per cent and when an unsecured loan falls into default, the lender’s recovery prospects plummet.

Potential borrowers need to be mindful of all these issues. So how does a business decide if fintech borrowing is right for them and if so which is the most suitable lender? Here are three tips for SMEs to consider:

1. DO YOUR DUE DILIGENCE

Do your DD as you would if you were looking for any new major supplier or stakeholder. Some of your queries will be able to be satisfied via the lender’s website but if you’re not sure about anything, call them. Ask questions like:

•Who are your shareholders and management?

•What qualifications and experience do you have?

•How much capital have you committed?

•Can I speak to some existing clients?

•How reliable is your funding source?

2. BE SURE YOU UNDERSTAND AND CAN AFFORD TO PAY THE FEES

Ensure you understand all the fees and charges. For instance, fintechs often quote an interest rate based on the term of the transaction so a 3 per cent rate which might look fair to you could in fact be 3 per cent on a loan of 30 days which represents an annualised rate of interest of 36 per cent.

Once you understand all the costs, re-visit your forecasts to ensure you can still make an acceptable profit. No point in working just for your financier!

3. CONSIDER WHAT WILL HAPPEN IF THINGS GO WRONG.

You probably have a good idea of what happens if you cant meet your obligations to a bank. How would this work with a fintech? How open would they be to extending the term of your financing arrangements if for instance a debtor is slow to pay? What dispute resolution procedures do they have?

HOW ARE THE BANKS RESPONDING?

The banks recognise they are burdened with legacy cost structures that place them at a disadvantage relative to disruptors who have lower cost and more scalable systems. They are acutely aware of the threat and are monitoring developments closely. Fintechs are not yet taking market share from the banks but clearly the potential exists for serious inroads once this business model becomes established.

In time banks will respond by acquiring the better structured and performing fintechs. Another bank strategy will be to take equity in start up fintechs backed by big name players with deep pockets as Westpac has done with the online personal lender Society One.

It’s still early days but over time fintechs will become a significant alternative funding source for SMEs. In the meantime SMEs contemplating borrowing from a fintech would be well advised to first ensure they understand exactly what they are getting themselves into.

Neil Slonim is a banking advisor and commentator and founder of theBankDoctor.com.au , a not for profit online source of independent banking advice for SMEs.

Mirrored with permission of the author.

Why Online Lending Will Take Off With Small Business Owners

Interesting recent article from Fortune Insider with a relevant perspective on the potential for online lending for small business though from a US perspective.

At a minimum, banks are perfect partners in the new game.

Earlier this month, the momentum behind the online lending industry was in full view at LendIt—an industry gathering that didn’t exist four years ago, but grew from about 700 attendees last year to more than 2,500 this year. What was clear is that it’s no longer a question of whether these disruptors will change the game in small business lending, but how quickly.

In fact, in his remarks at LendIt attendees in New York City, former Treasury Secretary Larry Summers predicted that online lenders could eventually capture upwards of 70% of the small business lending market. That may be an overly optimistic prediction, but one thing is clear online lending is a welcome innovation in the small business sector.

Dozens of new companies have jumped in from FundBox to Square, joining longer term players like OnDeck, Lending Club and Funding Circle. At the same time, the entrance of big money from hedge funds and institutional investors has created an energy that has gotten the attention of long-time observers of the financial industry.

Small business owners were the hardest hit in the Great Recession due in part to their reliance on available credit. In the years following, the sluggishness of the overall economic recovery in many ways was a result of these important job creators still not being able to readily access the capital they needed from their traditional sources – banks.

Many banks make loans today pretty much the way they did 50 years ago, relying on expensive personal underwriting and a mountain of paperwork. That makes small dollar loans not economical. Yet, loans under $250,000 are what most small businesses want. Add to that, the number of community banks – a critical source of small business loans – has been shrinking, from 14,000 in 1984 to less than 7,000 today.

As is often the case throughout our nation’s history, in step the entrepreneurs with dozens of new companies entering the lending space with a new approach. Much of the innovation behind these new startups is based on using technology to deliver a more streamlined application and approval process. They use new algorithms to access and analyze more data from different sources about a borrower than the traditional bank.

Today borrowers fill out an online application that typically takes 30-60 minutes. They get a response within hours and can be funded in days. This customer service is winning the attention of frustrated small business owners who on average were spending 26 hours on the loan process and waiting weeks or even months for an answer from a bank. The word is beginning to spread. In a recent Federal Reserve survey 18% of small business owners reported seeking capital online with a 38% approval rate, compared to a 31% approval rate at large national banks.

Ease of use doesn’t grow an industry all on its own, though, but available capital does. Yes, interestingly, what’s really fueling the growth of accessible capital for small business owners is accessible capital itself. Peer-to-peer capital has given way to hedge funds and institutions looking for yield, and a hungry finance industry ready to package and syndicate the funding.

Despite the bright outlook, some worrisome questions remain. What happens to all this new capital in a downturn or when yield is available elsewhere? Can the new algorithms really predict which small businesses will succeed and which will fail? What about the high cost of some of these new loans? Regulation is largely absent in this new industry. How can small businesses really know how to pick the right product and do they know much they are paying?

How will traditional banks respond? Don’t count them out yet. There are several factors that actually could give the established players a competitive advantage. For instance, while new online lenders are spending considerable sums to find small business customers, traditional banks have thousands of those customers and have mountains of data about them.

At a minimum, banks are perfect partners in the new game. They can connect customers to the online platforms, share information for the credit approval processes and they can even put their capital to work as investors.

Needless to say, transformation is coming, and it’s coming in an industry that is not known for it. As Summers noted last week, former Federal Reserve Chair Paul Volker once pointed out that the only useful innovation in finance in the past generation has been the ATM.

All indicators are that this transformation will only continue to pick up its pace. As it does, one thing is clear – while investors may see gains, in all likelihood, small businesses will be the biggest winners.

Urgent Action Required To Boost Business Lending

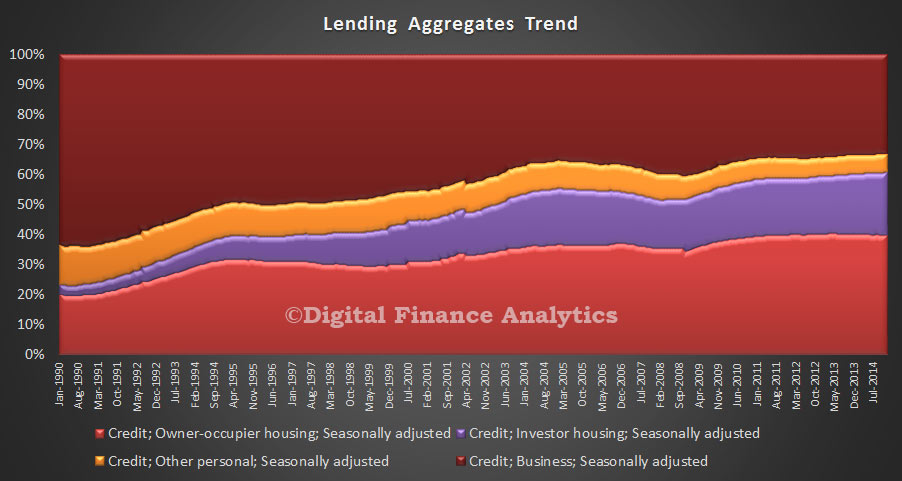

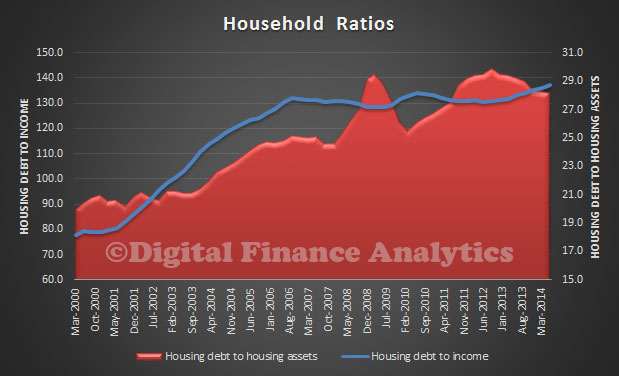

Today the data from RBA and APRA showed the strength of lending in the housing sector, and only 33% of lending is business related. This over-emphasis on property investment in particular is a systemic problem, and must be addressed if we are to drive growth in the right direction. Business needs more focus.

To illustrate the point, the mix between business lending and housing (both owner occupied and investment) is worth examining from 1990 onwards. Back then, business lending accounted for about 65% of all lending. Today it is 33%. As a result we know from our SME surveys that many businesses are finding it difficult to get funding on reasonable terms. On the other hand, we see lending for housing, and especially investment lending inflating the banks balance sheets and house prices, but this is not truly productive.

To illustrate the point, the mix between business lending and housing (both owner occupied and investment) is worth examining from 1990 onwards. Back then, business lending accounted for about 65% of all lending. Today it is 33%. As a result we know from our SME surveys that many businesses are finding it difficult to get funding on reasonable terms. On the other hand, we see lending for housing, and especially investment lending inflating the banks balance sheets and house prices, but this is not truly productive.

Its time to impose additional controls on investment lending, and to re-balance lending towards businesses who will be able to generate real economic growth for the country. The current situation, where household net worth grows…

… thanks to over-high house prices is not sustainable when it is powered by ever more household debt.

… thanks to over-high house prices is not sustainable when it is powered by ever more household debt.

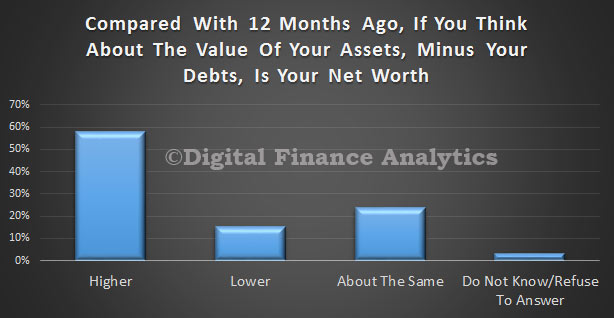

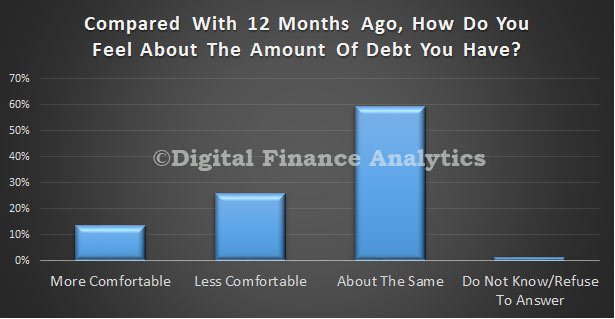

From our surveys, a quarter of households are less comfortable with the amount of debt they have compared with 12 months ago.

Any further interest rate cuts without these measures would be irresponsible.

Any further interest rate cuts without these measures would be irresponsible.

SME Working Capital Courtesy Of PayPal

In the recent DFA SME survey we highlighted the pressure many SME’s are under with regards to funding working capital. We also highlighted that in Australia, SME’s have few places to go to get financial assistance, hence the fact that the big banks have lifted their lending criteria and interest rates into the captive market.

So the recent announcement by PayPal that they intend to launch their working capital solution for business in Australia is significant. PayPal Working Capital will be introduced to a limited number of PayPal merchant partners between now and the end of the year, followed by a broader roll out in 2015. This service has been launched already in the US and more recently in the UK. You can watch a video about the service on their site. Since the US launch in September 2013, via lender WebBank the PayPal Working Capital programme has provided more than $140 million in loans to SMEs and according to The PayPal Working Capital Customer Satisfaction Survey conducted in June, 2014.

So the recent announcement by PayPal that they intend to launch their working capital solution for business in Australia is significant. PayPal Working Capital will be introduced to a limited number of PayPal merchant partners between now and the end of the year, followed by a broader roll out in 2015. This service has been launched already in the US and more recently in the UK. You can watch a video about the service on their site. Since the US launch in September 2013, via lender WebBank the PayPal Working Capital programme has provided more than $140 million in loans to SMEs and according to The PayPal Working Capital Customer Satisfaction Survey conducted in June, 2014.

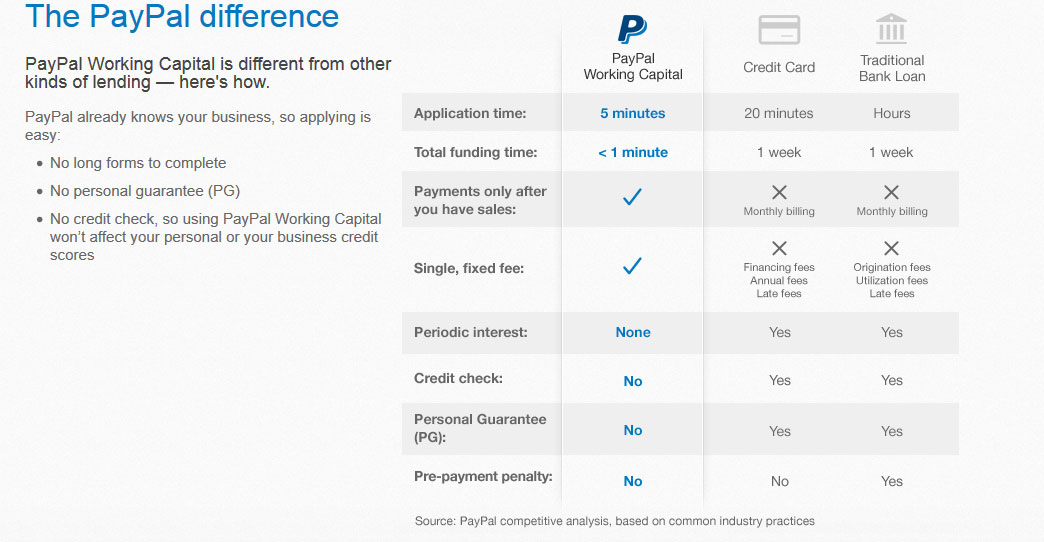

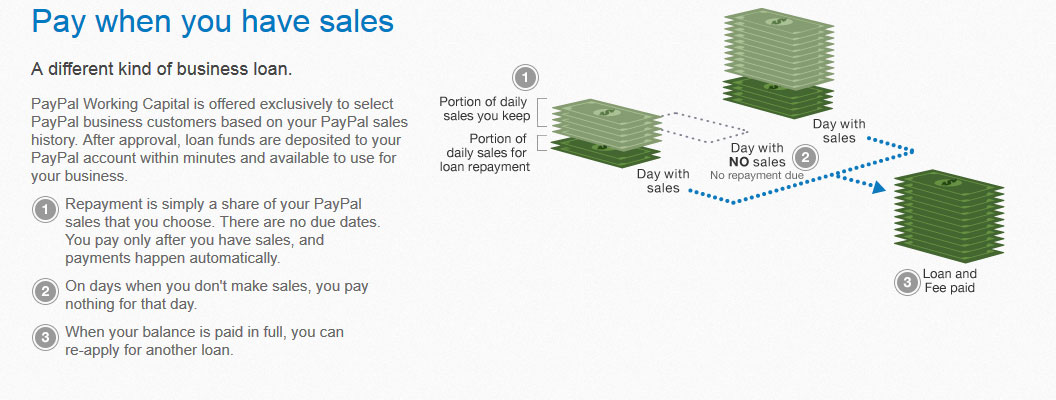

The PayPal solution is not your average overdraft.

PayPal Working Capital gives businesses access to the capital they need, but it’s faster and easier than traditional loans. It’s available to select businesses that already process payments through PayPal. If your business qualifies, the lender reviews your PayPal cash flow history to customize a special offer.

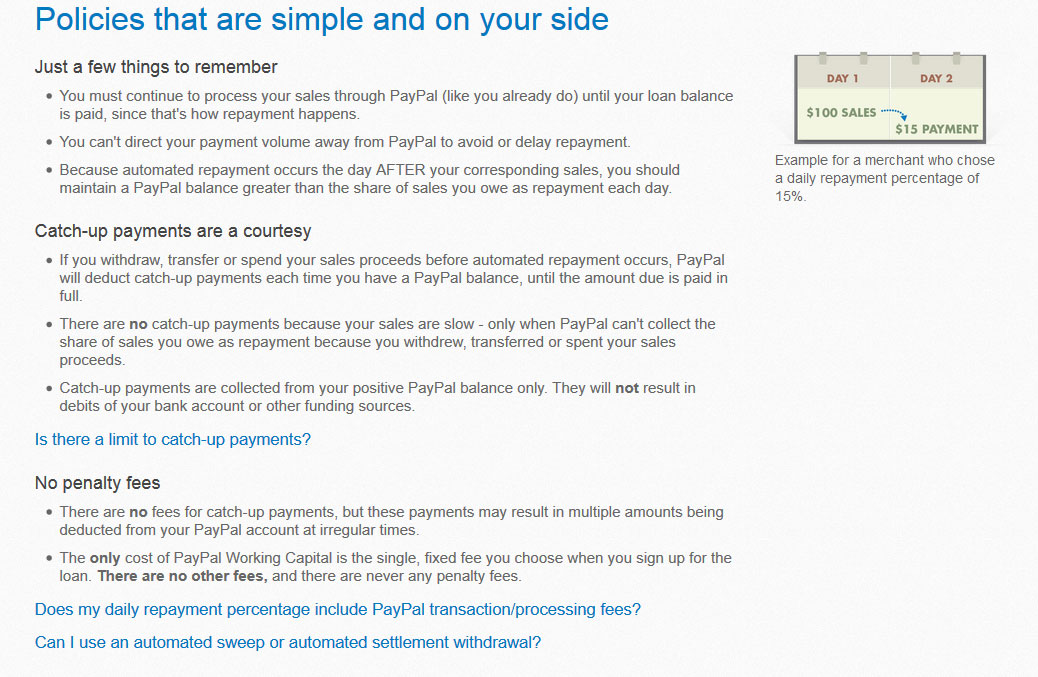

PayPal Working Capital is a business loan of a fixed amount, with a single fixed fee. There are no due dates, minimum monthly payments, periodic interest charges, late fees, pre-payment fees, penalty fees, or any other fees.

The process is easy:

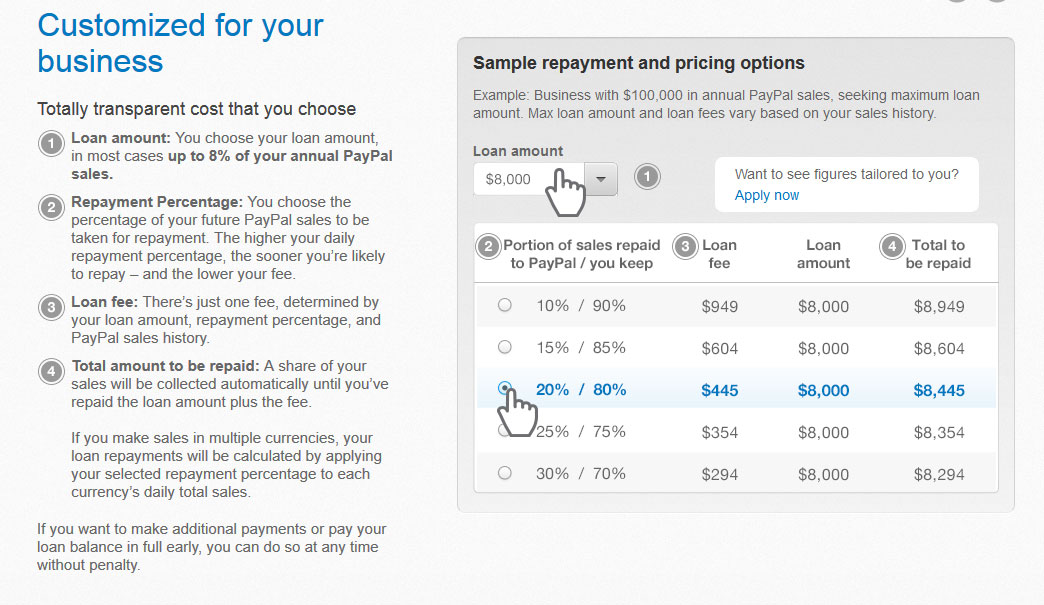

- Select your loan amount. In most cases, your max loan amount is up to 8% of your PayPal sales over the past 12 months.

- Choose the percentage of your future PayPal sales that you want to go toward repayment of the loan amount and the loan fee.

- Get the loan amount deposited to your PayPal account within minutes to use for your business.

- Start making repayments as a percentage of your daily sales until your balance is paid in full. You can also make additional payments or even pay the loan in full early without penalty.

The lender reviews your PayPal sales history to determine your loan amount. In most cases, your maximum loan amount is up to 8% of the sales your business processed through PayPal in the past 12 months. The maximum amount may be less for new or larger businesses, or for businesses with volatile or seasonally variable sales.

Unlike traditional loans, PayPal Working Capital charges a single, fixed fee that you’ll know before you sign up. No periodic interest, no hidden fees, no set payment plan, no payment due dates, and no late fees. You’re charged a single, fixed fee on your loan, not a traditional periodic interest rate. The lender determines your eligibility based on your business’s PayPal sales history, not your business or personal credit score. Applying for or using this loan won’t impact either credit score.

SME’s who decide to consider this option will need to flow transactions via PayPal, so redirecting traffic through the PayPay system. It may prove attractive to SME’s who struggle to get unsecured loans in the current (despite low rate) environment.

SME’s who decide to consider this option will need to flow transactions via PayPal, so redirecting traffic through the PayPay system. It may prove attractive to SME’s who struggle to get unsecured loans in the current (despite low rate) environment.

Australian player Moula, already offers online loans to business, and have plans to expand offline, but a player with the credentials of PayPal (soon to be split from eBay, its current owner) could start a welcome shake-up of SME lending. The winners could be the small business owners in Australia, and the banks perhaps the loosers. According to DFA bank modelling, SME lending is more profitable, on average than retail mortgages, so the banks will be watching development carefully. It also highlights again the digital disruption coming to the industry, alongside peer-to-peer lending, retail payments and online channels as featured in our recent Quiet Revolution report.

SME’s Business Grinds On

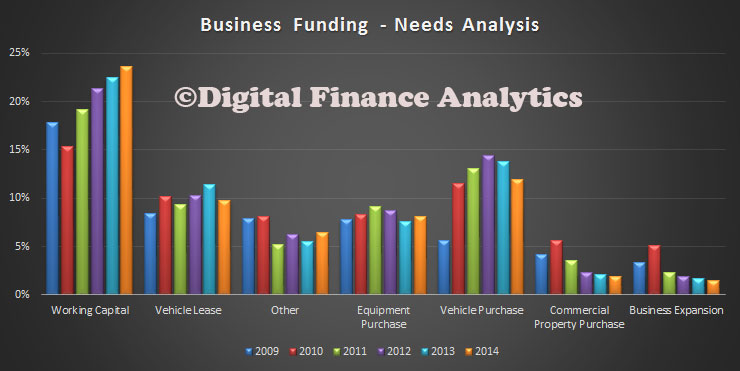

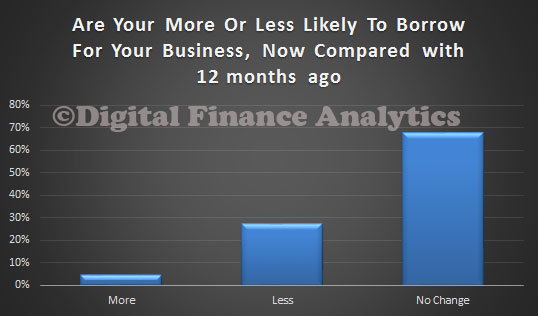

We have just received the latest findings from our Small and Medium Business surveys, which shows that many are still running hard to stand still and are unwilling or unable to borrow more. The sector is an important bell-weather for the broader economy, because nearly half of all Australian households are reliant in part or in full on income from the sector, as either an owner of a small business, or employed by one.

We asked them about their likelihood to borrow (slightly more than half need to fund their businesses from loans) and 28% were less likely to borrow than a year ago.

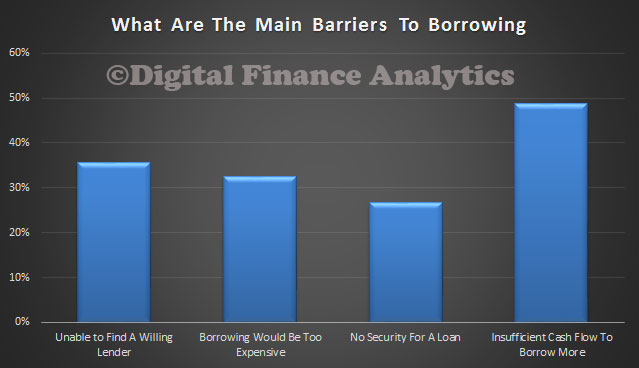

Barriers to funding included the inability to find a lender, lack of security for a loan, the expense of borrowing, or simply maxed out already based on cash flow.

Barriers to funding included the inability to find a lender, lack of security for a loan, the expense of borrowing, or simply maxed out already based on cash flow.

The main requirement was for working capital, rather than funding for business growth. Finance for vehicles was down a little compared with last year.

The main requirement was for working capital, rather than funding for business growth. Finance for vehicles was down a little compared with last year.

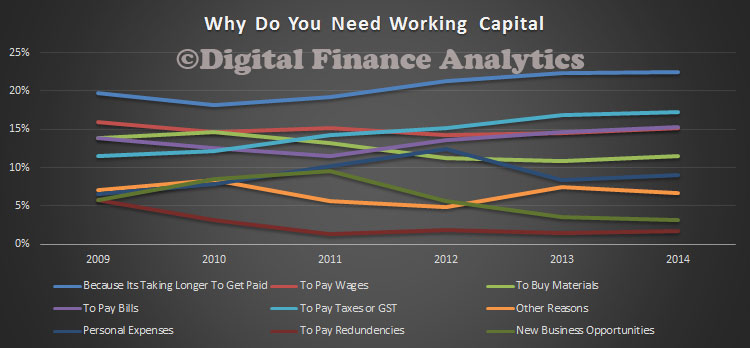

The demand for working capital was driven by many reasons, but the length of time to get paid was most significant, followed by borrowing to pay GST or tax.

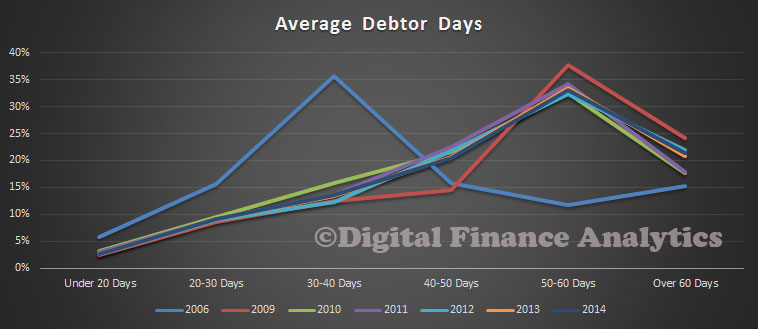

The average debtor days remains significantly higher than pre-GFC, and clearly extended days chimes with the need for more working capital.

The average debtor days remains significantly higher than pre-GFC, and clearly extended days chimes with the need for more working capital.

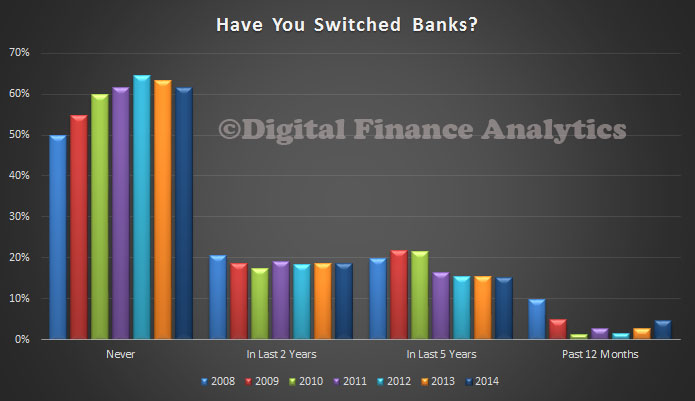

Finally, there is a small rise in bank switching, but still many SME’s do not. More than 60% have never switched banks.

Finally, there is a small rise in bank switching, but still many SME’s do not. More than 60% have never switched banks.

We will publish some more detailed analysis in later posts. Meantime, you can read about our SME research programme, and last report here.

We will publish some more detailed analysis in later posts. Meantime, you can read about our SME research programme, and last report here.

Latest DFA/JP Morgan SME Report Launched Today

The latest report, volume 7 of the SME Report series was released today. As well as over-viewing current industry trends, this time we focus on sectoral rotation, with SME’s in the construction industry feeling more confident, whilst other sectors remain patchy. We do not see a significant rise in demand for credit anytime soon.

JPM authored their report using DFA research data as detailed in the DFA SME Report already published and available on request from DFA. Because of compliance issues the final JPM version of the report is only available direct from them.

Go here for more details of our research programmes, and for media requests, go here.