From SmartCompany.

Small business owners, banks and fintechs can all gain valuable insights from a recent survey of SMEs conducted by research company Digital Financial Analytics (DFA).

The results reinforce the critical importance of cash flow management and identify a number of telling behavioural and demographic trends within this all important sector.

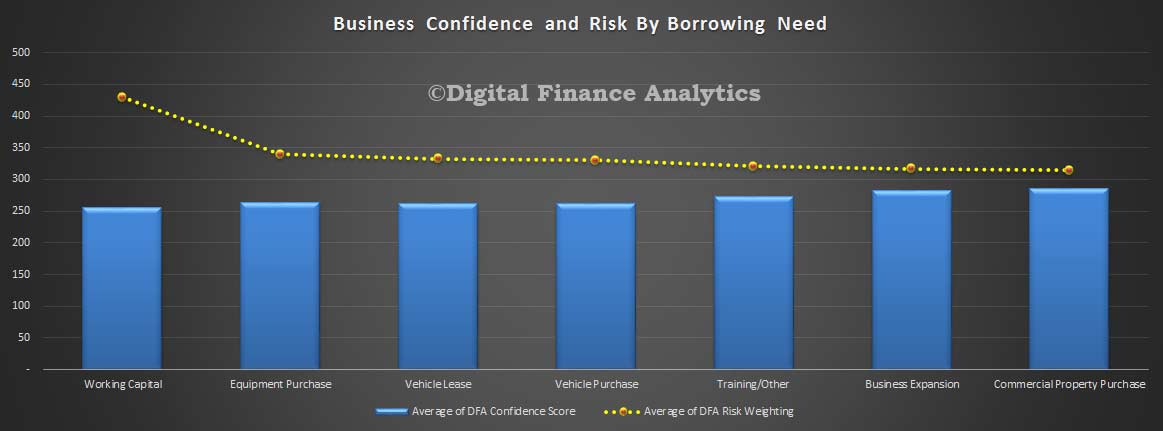

The DFA Small & Medium Business Survey 2015 of 26,000 businesses with turnover of less than $5 million reveals 57% of all business borrowing is for working capital.

Extended payments terms and late payments are the main reasons why managing cash flow has become one of the biggest challenges facing SMEs.

With average debtor days running at between 50 and 60, managing cash is a juggling act that can be made even more difficult by some big customers that display little regard for the plight of their smaller suppliers.

This is where the relationship between the SME and the bank becomes so critical. The extent to which business owners feel their bank is there to support them in tight times is one of the key determinants of satisfaction levels and also the propensity to switch banks.

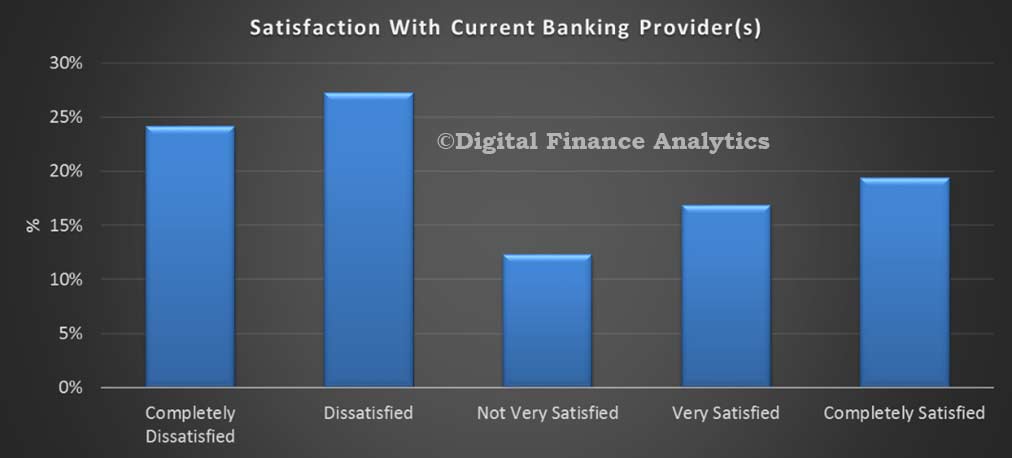

Satisfaction and switching

Thirty-five per cent of SMEs surveyed by DFA are either “satisfied” or “completely satisfied” with their bank, so clearly many customers are happy.

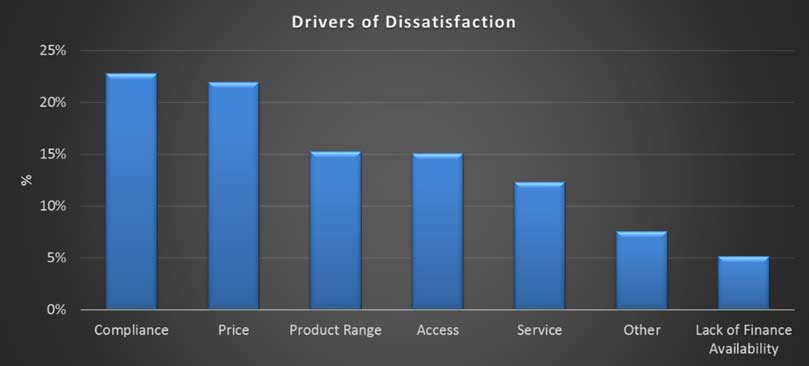

But this also means that two in every three business customers have at least some level of dissatisfaction with their bank. The main causes of frustration can be traced to lack of service, compliance requirements and poor understanding by banks of their needs.

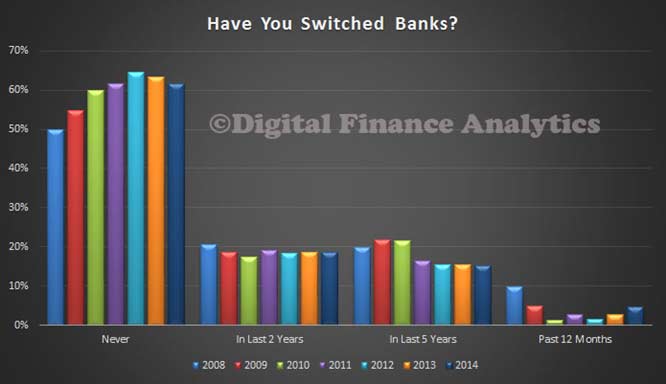

So how does satisfaction translate into shifting intentions? Seventy five per cent of SMEs indicated a preparedness to shift for a better deal yet 60% have never changed banks.

This begs the question: why don’t more SMEs change banks?

Possible explanations are that SMEs don’t proactively seek alternative financing proposals because they either feel “it’s all too hard” or “all the banks are pretty much the same anyway”.

Others may have tried to move but have found no joy because they overestimated their attractiveness to another bank.

When it comes to how much profit banks make from their SME customers, 20% of customers generate around 80% of bank profits.

Perhaps surprisingly, 30% of all SMEs are actually unprofitable for the banks. The problem for many business owners is that they don’t know how attractive they are as a customer and this makes it tricky when it comes to negotiating with banks.

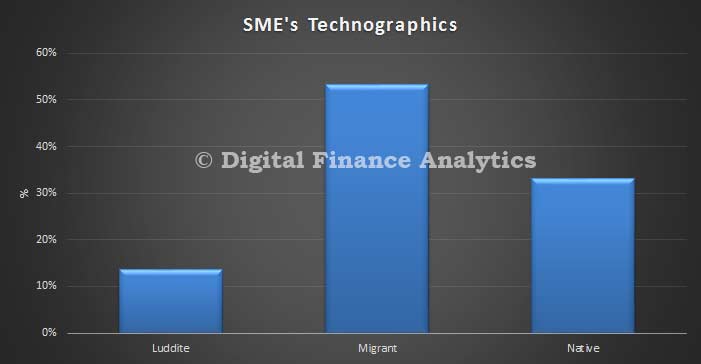

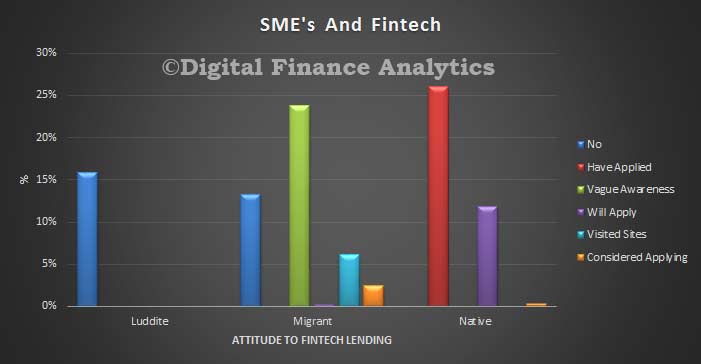

Luddites, migrants and natives

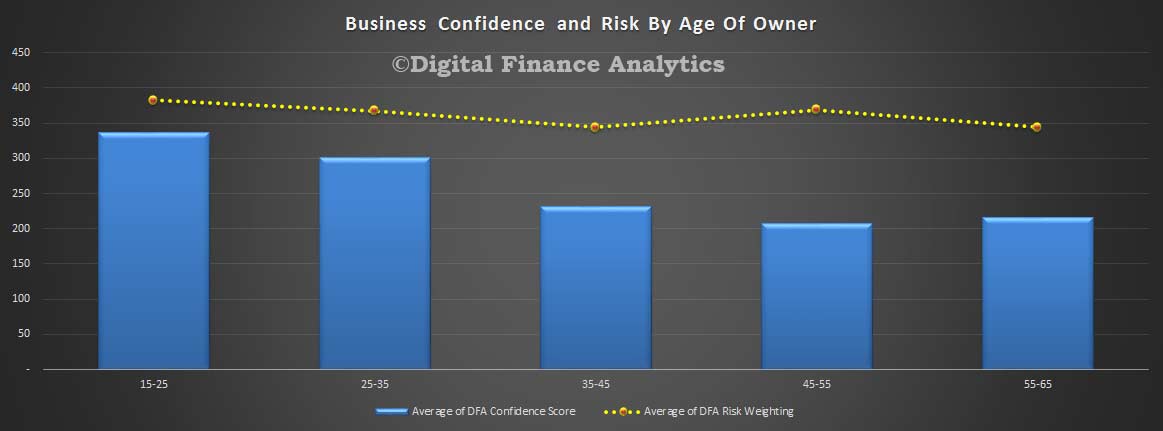

DFA divides business owners into luddites (14%) who are late adopters of technology and hardly use smart devices and services at all; migrants (52%) who are now active users but have had to learn new skills and adapt to the new services; and natives (34%) who have always been digitally aligned. Age is a good proxy for digital take-up with younger business owners firmly in the native category, whilst those over 45 are more likely to be luddites.

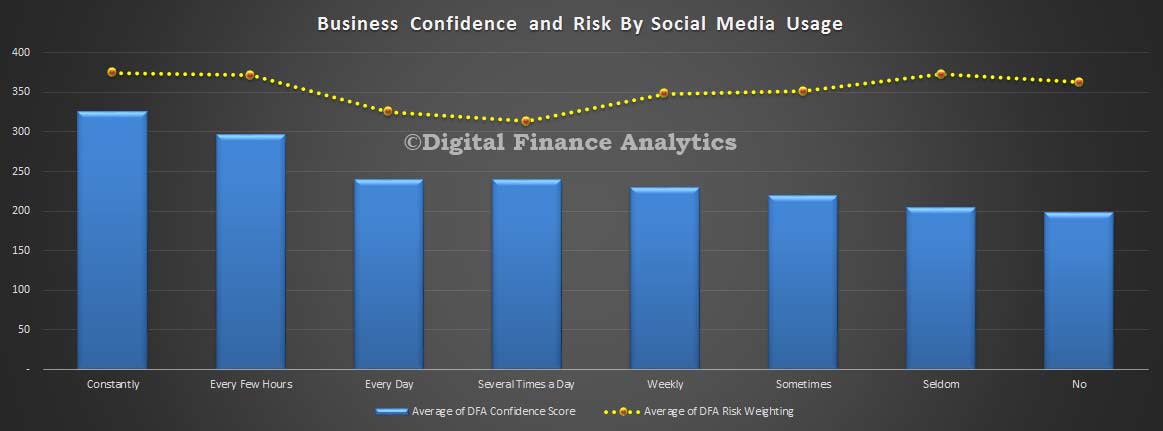

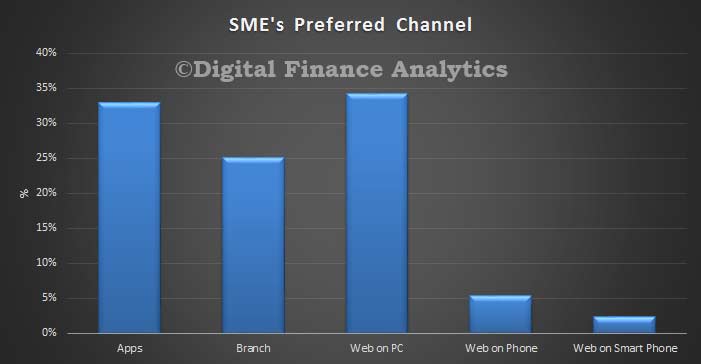

Natives are more likely to borrow than migrants, who are more likely to be credit avoiders. The natives also spend considerably more time connected to online services and want all their banking (from product purchase through to service) via smart devices. Natives are significantly more profitable customers for banks in relative terms.

Migrants have a mix of channels with 20% still preferring the bank branch whilst luddites are strong champions of branch access. Luddites provide profitability for branches but as the proportion of luddites decline, it will become even increasingly expensive for banks to support the remaining numbers.

With 86% of businesses either natives or migrants, the future is digital.

Fintechs

Financial Technology (fintech) is a term used to describe the range of innovative digital businesses including online lending and payments platforms.

Creating awareness is one of the many challenges faced by online lenders although many digital natives are very aware and are considering applying or already have applied for an online business loan. Migrants have mixed attitudes to online lenders whilst luddites are just not aware or interested.

Natives are also most likely to consider borrowing via payments platforms like PayPal’s cash flow services, whereas migrants are only using PayPal to make payments and luddites are not engaged at all.

Natives are well advanced in their use of cloud-based services whilst migrants are on the journey. Luddites have not yet started to engage.

Gender

According to the DFA survey, 73% of all SMEs are run by men and the bigger the business, the more likely a male will be the boss.

Only 8% of businesses run by females have more than 100 employees, compared with 16% of businesses run by males.

The proportion of SMEs run by females is increasing slowly from 23% in 2006 to 26% in 2010 and now 27%.

Credit cards

Businesses that employ less than four people rely heavily on debt from personal credit cards. This is usually unsecured debt and with 60% of bank write-offs being for unsecured lending. This partly explains why credit card debt is more expensive than secured business debt.

Failure

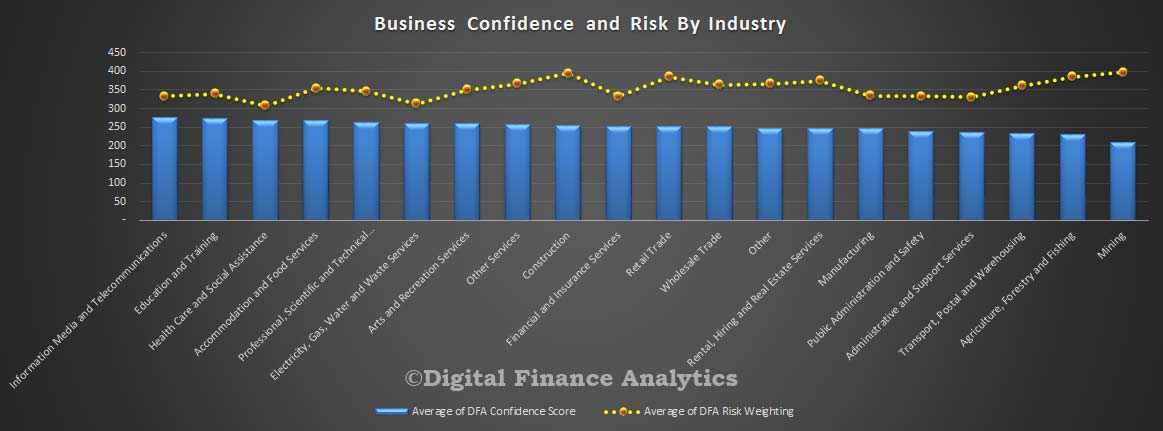

Half of all SMEs will fail within five years of starting up. Failure rates are highest amongst businesses involved in transport, financial services and information media and telecommunications, whist businesses in accommodation, food services and healthcare are less likely to fail.

Technology is changing the game

As challenging as it is to run an SME these days, technology is opening up possibilities for those business owners keen to embrace it.

Banks remain dominant players in lending and payments but increasingly SMEs are able to tap into new avenues of funding and transacting business.

The banks will innovate and also collaborate with fintechs in order to maintain their standing. Despite the advantages the new players possess, we haven’t yet seen how they operate in a severe economic downturn and it’s going to take time for them build critical mass, earn the trust of their customers and produce an acceptable ROE for shareholders.

There will be casualties along the way.

DFA concludes there is a significant opportunity available to players who construct compelling offers to the SME sector.

Understanding the needs and aspirations of small business owners is paramount and the parties who best articulate and most importantly deliver on this this will be the ones that come out on top.

But business owners cannot afford to sit back and wait for things to happen, they need to invest time and effort in exploring what options are available and best suited to their own immediate and future needs.

Neil Slonim is a business banking advisor and commentator and thefounder of theBankDoctor.org, a not-for-profit online resource centre for SMEs dealing with the challenges of funding a small business.