Once taken for granted by the mainstream, home ownership is increasingly precarious. At the margins, which are wide, it is as if a whole new form of tenure has emerged.

Whatever the drivers, significant and lasting shifts are shaking the foundations of home ownership. The effects are far-reaching and could undermine both the financial and wider well-being of all Australian households.

Over the course of 100 years, Australians became accustomed to smooth housing pathways from leaving the parental home to owning their house outright. However, not only did the 2008-09 global financial crisis (GFC) underline the risk of dropping out along the way, but more recent Australian evidence has shown that the old pathways have been displaced by more uncertain routes that waver between owning and renting.

The Household, Income and Labour Dynamics in Australia (HILDA) Survey indicates that, during the first decade of the new millennium, 1.9 million spells of home ownership ended with a move into renting (one-fifth of all home ownership spells that were ongoing in that period). It also shows that among those who dropped out, nearly two-thirds had returned to owning by 2010. Astonishingly, some 7% “churned” in and out of ownership more than once. Many households no longer either own or rent; they hover between sectors in a “third” way.

The drivers of this transformation include an ongoing imperative to own, vying with the factors that oppose this – rising divorce rates, soaring house prices, growing mortgage debt, insecure employment and other circumstances that make it difficult to meet home ownership’s outlays.

Those who use the family home as an “ATM” are at added risk. This relatively new way of juggling mortgage payments, savings and pressing spending needs makes some styles of owner occupation more marginal – as the tendency is to borrow up, rather than pay down, mortgage debts over the life course.

A retirement incomes system under threat

Since its inception, the means-tested age pension system has been set at a low fixed amount. Retired Australians could nevertheless get by provided they achieved outright home ownership soon enough. The low housing costs associated with outright ownership in older age were effectively a central plank of Australian social policy.

Moreover, developments in the Australian housing system could undermine a second retirement incomes pillar – the superannuation guarantee. An important goal of the superannuation guarantee is financial independence in old age. But if superannuation pay-outs are used to repay mortgage debts on retirement, reliance on age pensions will grow rather than recede.

Such policy interest is not surprising. Housing wealth dominates the asset portfolios of the majority of Australian households, boosted by soaring house prices. If home owners can be encouraged or even compelled to draw on their housing assets to fund spending needs in retirement, this will ease fiscal pressures in an era of population ageing.

However, the welfare role of home ownership is already important in the earlier stages of life cycles. Financial products are increasingly being used to release housing equity in pre-retirement years. This adds to the debt overhang as retirement age approaches. It also increases exposure to credit and investment risks that could undermine stability in housing markets.

A gender equity issue

A commonly overlooked angle relates to gender equity. Australian women own less wealth than men, and they also hold more housing-centric asset portfolios.

Hence, women are more exposed to housing market instability associated with precarious home ownership. Single women are especially vulnerable to investment risk when they seek to realise their assets.

A neglected economic lever

Housing and mortgage markets played a central role in the GFC. Today, it is widely agreed that resilient housing and mortgage markets are important for overall economic and financial stability. There are also concerns that the post-GFC debt overhang is a drag on economic growth.

However, the policy stance in the wake of the GFC has been “business as usual”. There has been very little real innovation in the world of housing finance or mortgage contract design in recent years. This might change if housing were steered from the periphery to a more central place in national economic debates.

Forward-looking policy response is needed

Growing numbers of Australians clearly face an uncertain future in a changing housing system. The traditional tenure divide has been displaced by unprecedented fluidity as people juggle with costs, benefits, assets and debts “in between” renting and owning.

This expanding arena is strangely neglected by policy instruments and financial products. Politicians cling to an outdated vision of linear housing careers that does little to meet the needs of “at risk” home owners, locked-out renters, or churners caught between the two.

The hazards of a destabilising home ownership sector are wide-ranging, rippling well beyond the realm of housing. Part of the answer is a new drive for sustainability, based on a housing system for Australia that is more inclusive and less tenure-bound.

Author: Rachel Ong, Professor of Economics, School of Economics and Finance, Curtin University; Gavin Wood, Emeritus Professor of Housing and Housing Studies, RMIT University; Susan Smith,

Honorary Professor of Geography, University of Cambridge

So much of Australia’s history and success is built on immigration. Migrants have benefited incumbent Australians by raising incomes, increasing innovation, contributing to government budgets, smoothing over population ageing and diversifying our social fabric. But it is also true that immigration is affecting house prices and rents.

Australian governments are squandering the gains from migration with poor housing and infrastructure policies. Our new report, Housing affordability: re-imagining the Australian dream, shows what’s at stake. Unless the states reform their planning systems to allow more housing to be built, the Commonwealth should consider tapping the brakes on Australia’s migrant intake.

Since 2005, net overseas migration – which includes the increase in temporary migrants – has averaged 200,000 people per year, up from 100,000 in the previous decade. It is predicted to be around 240,000 per year over the next few years.

Immigrants are more likely to move to Australia’s big cities than existing residents, which increases demand for scarce urban housing. In 2011, 86% of immigrants lived in major cities, compared to 65% of the Australian-born population.

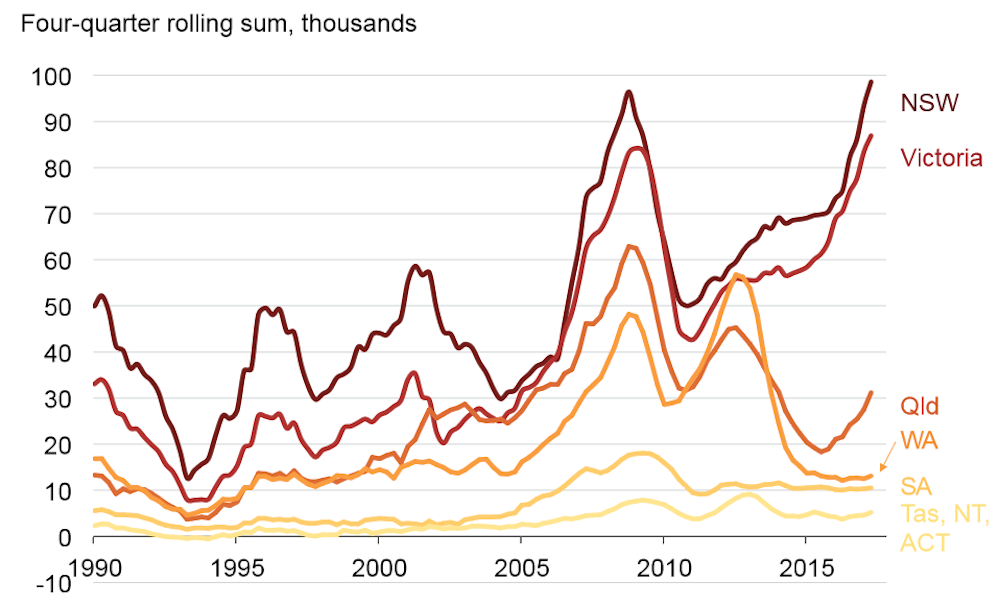

Chart 1. Migration has jumped, and so have capital city populations

Grattan Institute, Author provided

Not surprisingly, several studies have found that migration increases house prices, especially when there are constraints on building enough new homes.

The pick-up in immigration coincides with Australia’s most recent housing price boom. Sydney and Melbourne are taking more migrants than ever. Australian house prices have increased 50% in the past five years, and by 70% in Sydney.

Chart 2: Net overseas migration into NSW and Victoria is at record levels

Grattan Institute (Data source: ABS 3101.0 – Australian Demographic Statistics), Author provided

Of course immigration isn’t the only factor driving up house prices and rents. Housing also costs more because incomes rose, interest rates fell and banks made it easier to get a loan. But adding 2 million migrants in the past decade has clearly increased how many new homes are needed.

We haven’t built enough homes

Housing demand from immigration shouldn’t lead to higher prices if enough dwellings are built quickly and at low cost. In post-war Australia, record rates of home building matched rapid population growth. House prices barely moved.

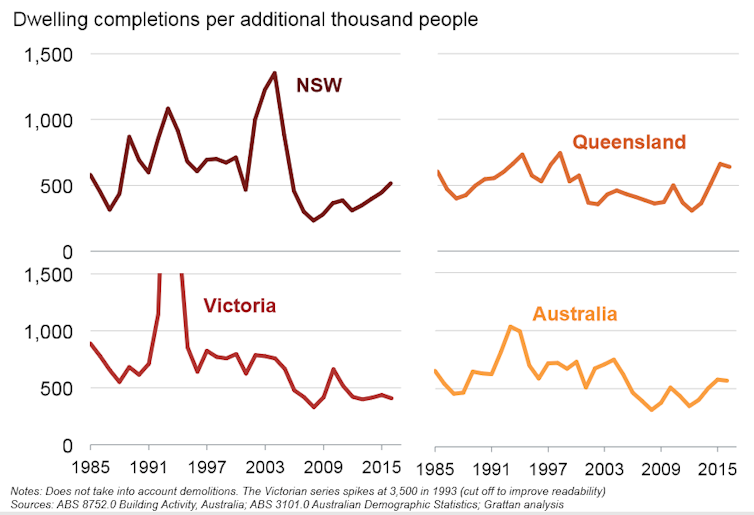

But over the last decade, home building did not keep pace with increases in demand, and prices rose. Through the 1990s, Australian cities built about 800 new homes for every extra 1,000 people. They built half as many over the past eight years.

We estimate somewhere between 450 and 550 new homes are needed for each 1,000 new residents, after accounting for demolitions. And because more families are breaking up and the population is ageing, more homes are needed to accommodate households with fewer members.

Chart 3: Housing construction lagged population in the last decade, but has picked up

Grattan Institute, Author provided

Only in the past couple of years has construction started to match population growth, especially in Sydney. It’s no coincidence that Sydney house prices have finally moderated in the past six months.

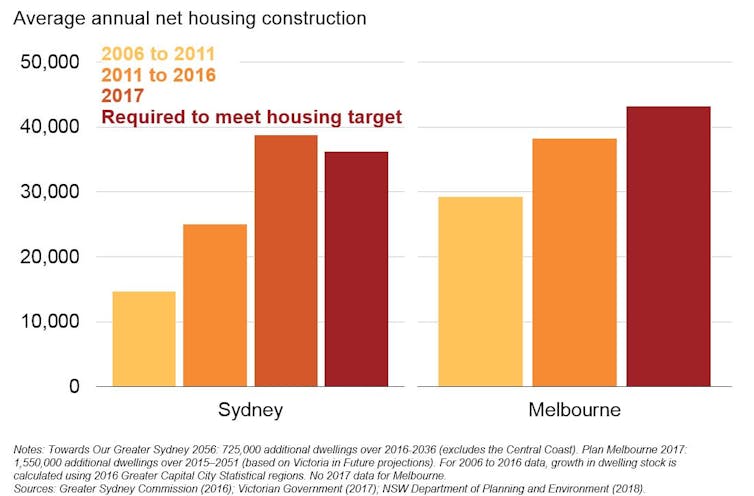

But the backlog of a decade of undersupply remains. Development at today’s record rates is the bare minimum needed to meet record population growth built into Sydney’s and Melbourne’s housing supply targets over the next 40 years.

Chart 4: Strong housing construction will need to be maintained to meet city plan housing targets

Grattan Institute

So what should governments do?

Building more housing will improve affordability the most – but slowly. Even at current record construction rates, new housing increases the stock of dwellings by only 2% each year. But building an extra 50,000 homes a year nationwide for a decade would lead to national house prices between 5% and 20% lower than otherwise. Do it for longer and prices will fall even further.

State governments need to fix planning rules to allow more housing to be built in inner and middle-ring suburbs. More small-scale urban infill projects should be allowed without council planning approval. And state governments should allow denser development “as of right” along key transport corridors. The Commonwealth can help with financial incentives for these reforms.

But the politics of planning in our major cities is fraught. Most people in established middle suburbs already own their houses. Prospective residents who don’t already live there can’t vote in council elections, and their interests are largely unrepresented.

If we want to maintain current migration levels, along with their economic, social and budgetary benefits, we need to do better at planning to allow more housing to be built.

What does this mean for the migrant intake?

The Australian government should develop a population policy, as the Productivity Commission recommended. It should articulate the appropriate level of migration given its economic, budgetary and social benefits and costs. This should include how it affects the Australian community living with the reality of land use planning policy – and contrasting this with the effect of optimal planning policy.

If planning and infrastructure policies don’t improve, the government should consider cutting the migration intake. This would reduce demand for housing, but would also reduce the incomes of existing residents.

The best policy is probably to continue with Australia’s demand-driven, relatively high-skill migration and to build enough homes for the growing population. But Australia is in a world of third-best policy: rapid migration and restricted housing supply are imposing big costs on people who don’t already own their homes. If the states are not going to reform planning rules to increase the number of homes built, then the Australian government should consider whether reducing migration is the lesser evil.

Any reduction should be modest and targeted at the parts of the migration program that provide the smallest benefit to Australian residents and migrants themselves. Balancing these interests is difficult, because each part of the program has different economic, social and budgetary costs and benefits.

Cutting back family reunion visas would have substantial social costs. Limiting skilled migration would hurt the economy and many businesses. Restricting growth in international students would reduce universities’ incomes.

There are also broader costs to cutting the migrant intake. It would hit the Commonwealth budget in the short term. Most migrants are of working age and pay full rates of personal income tax. And many temporary migrants, such as 457 visa holders, can’t draw on a range of government services and benefits, including welfare and Medicare. More importantly, cutting back on younger, skilled migrants is likely to hurt the budget and the economy in the long term.

But there is no point denying that housing affordability is worse because of a combination of rapid immigration and poor planning policy. Rather than tackling these issues, much of the debate has focused on policies that are unlikely to make a real difference. Unless governments own up to the real problems, and start explaining the policy changes that will make a real difference, Australia’s housing affordability woes are likely to get worse.

Authors; John Daley, Chief Executive Officer, Grattan Institute; Brendan Coates, Fellow, Grattan Institute; Trent Wiltshire, Associate, Grattan Institute

Australia should cut its immigration intake, according to Tony Abbott in a recent speech at the Sydney Institute. Abbott explicitly cites economic theory in his arguments: “It’s a basic law of economics that increasing the supply of labour depresses wages; and that increasing demand for housing boosts price.”

But this economic analysis is too basic. Yes, supply matters. But so does demand.

And while migrants do live in houses, the federal government’s fondness for stoking demand and the inactivity of state governments in increasing supply are the real issues affecting affordability.

The economy isn’t a fixed pie

Let’s take Abbott’s claims about immigration one by one, starting with wages.

It’s true that if you increase labour supply that, holding other factors that affect wages constant, wages will decline. However, those other factors are rarely constant.

Notably, if the demand for labour is increasing by more than supply (including new migrants), then wages will rise.

This is a big part of the story when it comes to the relationship between wages and migration in Australia. Large migrant numbers have been an almost constant feature of Australia’s economy since the end of the second world war, if not earlier.

But these migrants typically arrived in the midst of economic growth and rising demand for labour. This is particularly true in recent decades, when we have had one of the longest periods of unbroken growth in the history of the developed world.

In our study of the Australian labour market, we found no relationship between immigration rates and poor outcomes for incumbent Australian workers in terms of wages or jobs.

Australia uses a point system for migration that targets skilled migrants in areas of high labour demand. Business is suffering in these areas. Migrants into these sectors don’t take jobs from anybody else because they are meeting previously unmet demand.

These migrants receive a higher wage than they would in their place of origin, and they allow their new employers to reduce costs. This ultimately leads to lower prices for consumers. Just about everybody benefits.

There’s an idea called the “lump of labour fallacy”, which holds that there is a certain amount of work to be done in an economy, and if you bring in more labour it will increase competition for those jobs.

But migrants also bring capital, investing in houses, appliances, businesses, education and many other things. This increases economic activity and the number of jobs available.

Furthermore, innovation has been shown to be strongly linked to immigration. In the United States, for instance, immigrants apply for patents at twice the rate of non-immigrants. And a large number of studies show that immigrants are over-represented in patents, patent impact and innovative activity in a wide range of countries.

We don’t entirely know why this is. It could be that innovative countries attract migrants, or it could be than migrants help innovation. It’s likely that the effect goes both ways and is a strong argument against curtailing immigration.

Abbott’s comments are more reasonable in the case of housing affordability because here all other things really are held constant. Specifically, studies show that housing demand is overheated in part by federal government policies (negative gearing and capital gains tax exemptions, for instance) and state governments not doing enough to increase supply.

Governments have responded to high housing prices by further stoking demand, suggesting that people dip into their superannuation, for instance.

In the wake of Abbott’s speech there has been speculation that our current immigration numbers could exacerbate the pressures of automation, artificial intelligence and other labour-saving innovations.

But our understanding of these forces is nascent at best. In previous instances of major technological disruption, like the industrial revolution, the long-run effects on employment were negligible. When ATMs debuted, for example, many bank tellers lost their jobs. But the cost of branches also declined, new branches opened and total employment did not decline.

In his speech, Abbott said that the government needs policies that are principled, practical and popular. What would be popular is if governments across the country could fix our myriad policy problems. Abbott identified some of the big ones – wages, infrastructure and housing affordability.

What would be practical is to identify the causes of these problems and address these directly. Immigration is certainly not a major cause. It would be principled to undertake evidence-based analysis regarding what the causes are and how to address them.

A lot of that has already been done, notably by the Grattan Institute. What remains is for governments to do the politically difficult work of facing the facts.

Authors: Robert Breunig, Professor of Economics, Crawford School of Public Policy, Australian National University; Mark Fabian, Postgraduate student, Australian National University

The argument that cutting the Australian company tax rate will lead to higher investment and wages, more employment and faster GDP growth does not have solid empirical or theoretical backing.

A close look at the economic research in this area shows a lack of consensus. Different studies, looking at different samples of countries, over different periods of time, reach different conclusions.

And the predictions made by theoretical models are sensitive to the underlying assumptions and structures built into the models themselves.

Many of the issues surrounding tax cuts remain unsettled – such as the size or length of the impact, how it affects inequality and the relationship with other government policies.

In short, the IMF acknowledges that the recent US tax cuts will have a positive impact on economic growth in 2018-19. However, this is conditional on the US government not cutting expenditure, is likely to be short-lived, and will come at the cost of increased government deficits.

In this light, corporate tax cuts seem to be a long-term pain for a short-term gain, which is probably not what we need in Australia.

Conflicting information

Let’s start with the point that is probably least controversial – that a reduction in the corporate tax rate will lead to an increase in wages.

Think of the output produced by a corporation as a pie. This pie is shared among shareholders (in the form of dividends), banks and other lenders (in the form of interest paid on loans), workers (in the form of wages) and the government (in the form of taxes).

If we reduce the government’s share then there is more for everybody else, including workers. And some data do suggest that wages increase when corporate tax rates decline.

Yet economists disagree on the extent to which wages would actually increase in response to a tax cut.

Some research suggests that this increase might be small, even in a country like Germany, which is often used as an example of the beneficial impact of tax cuts on wages.

Certain aspects of the German economy and industrial relations system make it more likely that German workers will benefit from corporate tax cuts compared to Australian workers.

This means German workers have a stronger say when it comes to sharing the pie. For any given decrease in the slice of the government, German workers are more likely to get a bigger slice for themselves. This is not necessarily the case in Australia.

It is therefore difficult to draw implications for Australia from studies that look at the experience of Germany or other countries with significantly different institutional arrangements.

Furthermore, the fact that wages should increase in response to a corporate tax cut does not automatically imply that other economic variables will also respond positively. For instance, the more wages increase in response to a corporate tax cut, the smaller the increase in employment is likely to be.

This leads to an even more controversial question: what is the effect of corporate tax cuts on real economic activity, such as employment and GDP growth?

The trickle-down effect of corporate tax cuts rests on the idea that business investment would increase once taxes are cut, which in turn leads to the creation of more jobs and faster economic growth.

Many other factors come into corporate investment decisions, such as the quality of institutions, the proximity to important markets, and the cost of labour (wages).

Because of these other factors, the impacts of tax cuts on employment and growth can be small, short-lived, or conditional on other government policy actions, such as managing debt.

In a similar vein, recent theoretical work that incorporates more realistic assumptions about the economy (such as the distribution of entrepreneurial skills in the population) suggests that a tax cut only has a significant impact on economic growth when the tax rate is initially high.

This means that even within a given country, the effect of a corporate tax cut can change depending on initial economic and policy conditions.

Putting tax cuts in a broader context

Beyond growth and employment, the effects of corporate tax cuts should also be considered in terms of deficit and inequality.

From the point of view of the public budget, a cut in the tax rate has to be somehow financed. How?

A first possibility is that the tax cut pays for itself. This is essentially the idea that as the tax rate goes down, the increase in the tax base (e.g. pre-tax corporate profit) is sufficiently large to ensure that the total tax revenue increases.

However, an increase in the tax base would require a significant and sustained increase in business investment, which, as we have already seen, does not necessarily happen.

The government could increase other taxes, but this means the government would effectively be taking from one group of taxpayers (possibly workers themselves) to give to corporations.

Another option is to reduce some government expenditures. But this could also involve taking from one group to give to another. If the decision is made to cut social welfare and public goods like education and health, then more vulnerable segments of the population will bear the cost of lowering the corporate tax rate. This means more inequality in the economy.

Of course the government could decide to just let the deficit be. This would result in higher debt. But can Prime Minister Turnbull (or President Trump for that matter) accept that?

The central economic challenge for Australia is to promote long-term, inclusive growth. Are we confident that this is what corporate tax cuts will deliver? Based on the economic research that I have read, the answer is no.

Author: Fabrizio Carmignani, Professor, Griffith Business School, Griffith University

Australia’s credit rating system is failing both borrowers and lenders. Many borrowers are unaware of their own credit scores and our research shows they have trouble applying for suitable loans. Lenders are also struggling with too little information, causing them to extend loans to those they shouldn’t and restrict loans to worthy borrowers.

Upcoming changes to Australia’s credit reporting system could remedy these issues.

Under the new credit reporting regime, both lenders and borrowers will have access to more data, such as monthly payment histories on loans and credit cards. This will help consumers understand their own creditworthiness, improve their credit scores and shop around for lower interest rates.

The new data will arm banks and other lenders to make better lending decisions. But it should also level the playing field by giving new entrants more information, helping them to compete with the established lenders.

My research with Luke Deer examined loan applications to SocietyOne. This is a peer-to-peer lending marketplace that specialises in unsecured personal loans.

Borrowers are only accepted onto the SocietyOne platform if their credit scores can be verified. Substantial “underwriting” is required to ensure borrowers are of sufficient credit quality.

Underwriting involves evaluating a borrower’s income and cash flow, based on bank statements and other public information.

Despite this labour-intensive and time-consuming process, which requires individuals to submit copies of their documents to third-party lenders, lenders do not receive a complete picture of the potential borrower’s financial situation.

A borrower may report only part of their true financial situation – for example, by sharing information from only one of multiple accounts. Without an accurate picture of creditworthiness, lenders could be extending loans to borrowers that should be rejected, and others might not receive loans they should qualify for.

This is where the new credit reporting regime comes in – there will be much more data. In addition to monthly payment histories, there will be red flags on any missed payments of more than 14 days. The current system only flags missed payments of more than 60 days or bankruptcies only.

Credit reports will include information about current accounts you hold, what accounts have been opened and closed, the date that you paid any default notices, and how well you meet your repayments.

The shift towards comprehensive credit reporting should reduce the time required to underwrite loans and allow loans to be priced more efficiently. This is in part because it will reduce the risk of lending to people who are risky borrowers, and so will lower costs.

While this means that borrowers with good credit history will benefit from good behaviour, lower credit quality customers may face higher borrowing costs, or be left searching for alternatives.

But it also opens up more opportunity for borrowers to improve their credit rating by acting on any red flags.

More innovation ahead in mortgage lending

Australia has lagged other developed countries in adopting positive credit reporting. Up to this point, the large banks have had a significant informational advantage over new entrants. Because many of us have accounts with the larger banks, they simply had access to information that other lenders don’t.

As well as opening up the market to new borrowers and lenders, the new comprehensive credit reporting regime will also likely lead to the automation of more financial services and the inclusion of more data sources.

For higher-risk borrowers, novel techniques to assess credit risk (such as analysis of social media accounts) may be the answer to distinguish good borrowers from bad.

This will partially eliminate the need for costly processes in loan underwriting. But prior experience from an over-reliance on credit scores in the United States shows that careful assessment of borrowers remains vital.

It could also have the side effect of reducing the prospects of misconduct by either borrower or lender at this stage.

Comprehensive credit reporting should lead to, in aggregate, lower borrowing rates for lower-risk individuals and incentives for higher-risk individuals to improve their position. However, it remains to be seen whether this will lead to a greater degree of exclusion or predatory loans for riskier borrowers.

Author: Andrew Grant, Senior Lecturer, University of Sydney

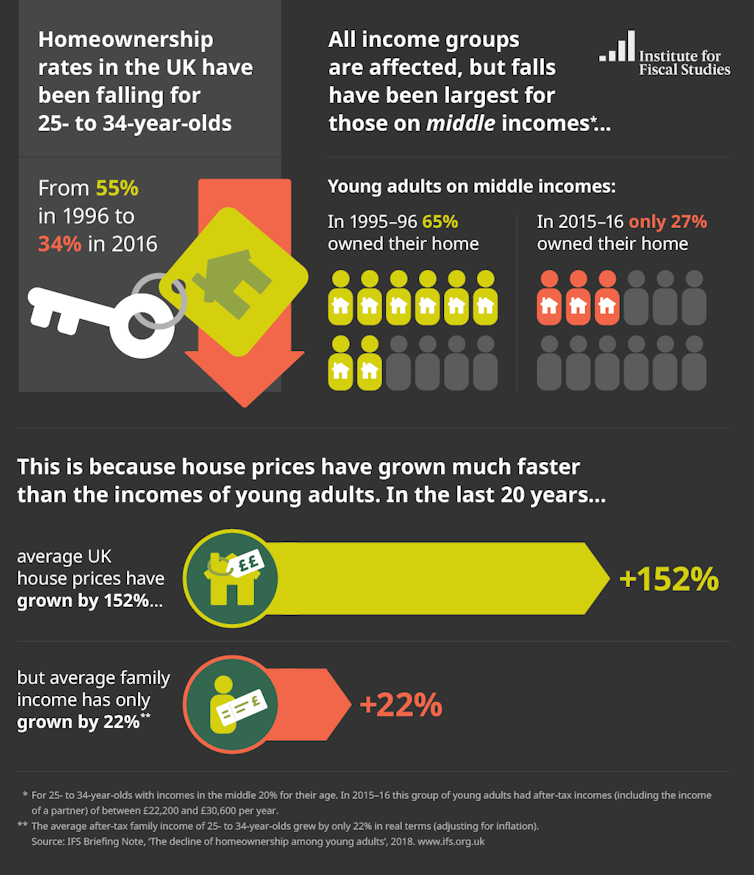

Speaking to the Conservative Party conference in September 2017, the UK prime minister, Theresa May, gave a stark assessment of the UK housing market which made for depressing listening for many young people: “For many the chance of getting onto the housing ladder has become a distant dream”, she said.

Now a new report by the Institute of Fiscal Studies (IFS) provides further, clear evidence of this. The study finds that home ownership among 25 to 34-year-olds has declined sharply over the past 20 years. Home ownership rates have declined from 43% at age 27 for someone born in the late 1970s, to just 25% for someone aged 27 who was born in the late 1980s.

The most significant decline has been for middle-income young people, whose rate of home ownership has fallen from 65% in 1995/6 to 27% now – most significantly hitting aspirant buyers in London and the South-East.

Causes and consequences

The IFS study lays the blame for all this on the growing gap between house prices and incomes. Adjusting for inflation, house prices have risen 150% in the 20 years to 2015/16, while real incomes for 25 to 34-year-olds have grown by 22% (and almost all of that growth happened before the 2008 crash).

But, as the report acknowledges, the problem goes much deeper than this. Home ownership rates differ by region. Although there has been a decline in home ownership rates for young people across all areas of Great Britain, the decline is less significant in the North East and Cumbria as well as in Scotland and the South West. The biggest decline in ownership has been in the South-East, the North-West (excluding Cumbria) and London.

So a person aged 25 to 34 is more than twice as likely to own their own home in Cumbria, as their counterpart in London. Worse, young people from disadvantaged backgrounds are less likely to own their own homes – even after controlling for differences in education and earnings. Home ownership continues to reflect a deeper inequality of opportunity in our society.

More houses needed

Part of the problem is that both Labour and Conservative governments have seen housing as a single, stand-alone market and have focused their attention on what is happening to prices in London. But housing is a number of different markets, which have regional variations and different interactions between the owner-occupier, private rented and social rented sectors.

Regional variations in house prices for similar sized properties reflect the imbalances of the economy: it is heavily reliant on financial services, which are concentrated in London, while the public sector makes up a significant share of many local economies – particularly in the North. Migration from across the UK to overcrowded and expensive areas – such as London and the South-East – have put property prices in those areas even further out of reach for would-be buyers.

To make matters worse, both Labour and Conservative governments have routinely failed to build enough houses. While the current government’s aim to build 300,000 new properties a year by 2020 is welcome, it is simply not enough to meet the backlog in demand – let alone address the fundamental affordability problem.

Where homes are being built, they’re often the wrong types of homes, in the wrong places. Family homes are being built, despite there being some four million under-occupied such properties across the country.

Not that long ago, government was reducing the housing stock in many parts of the North, through the disastrous Housing Market Renewal programme. Houses are currently being sold in smaller cities such as Liverpool and Stoke-on-Trent for just £1. And none of the government’s actions suggest that ministers understand these issues, or are prepared to address them.

House price inflation – and the awful affect it is having on home ownership rates for young people – is part of a wider problem of the global asset bubble. This bubble has seen huge increases in the price of assets – stocks, housing, bonds – in high income countries such as the UK. Successive governments have helped to fuel this through quantitative easing, ultra-cheap money and successive raids on pension funds.

What’s needed to address this asset bubble is a substantive increase in interest rates. But while this may slow the growth in house prices, the sad truth is it will do nothing to make housing more affordable for most young people.

Author: Chris O’Leary, Deputy Director, Policy Evaluation and Research Unit and Senior Lecturer, Manchester Metropolitan University

Following mounting pressure from Labor and some National Party MPs, the Turnbull government in December established a Royal Commission into misconduct in the banking, superannuation and financial services industry. Public hearings are now underway.

At the same time, the Australian Bankers’ Association (ABA) has been running a national advertising campaign in which bank branch staff talk about who benefits from bank profits.

The advertisements – broadcast on national television, published in newspapers, shared on social media and displayed on ATMs – state that “nearly 80% of all bank profits go straight back to shareholders and the majority of those shareholders are everyday Australians who own bank shares through their super funds”.

The ABA says bank profits “don’t belong to the banks, they belong to everyday Australians like you”.

Is that right?

Checking the source

The Conversation contacted the Australian Bankers’ Association requesting sources and comment, but did not receive a response.

On the “Australian Banks Belong To You” campaign website, the association cites these references:

The “nearly 80%” figure refers to the dividend payout ratio of the 8 key Australian retail banks averaged over 2016 and 2017. The data are sourced from bank annual reports. The dividend payout ratio is calculated as the sum of the dividends paid divided by the sum of cash earnings.

According to the ATO more than 14.8 million Australians have at least one superannuation fund account (around 40% have more than one). It’s safe to say that many super funds invest in Australian bank shares as part of their portfolio.

This means that millions of Australians own bank shares.

Verdict

The Australian Bankers’ Association claimed that “nearly 80% of all Australian bank profits go straight back to shareholders”. While we can’t say whether that’s correct for all Australian banks, the statement is broadly correct for Australia’s eight largest retail ABA member banks over the last five years.

The association’s claim that “the majority of those shareholders are everyday Australians who own bank shares through their super funds” is reasonable.

But if you read those statements together as meaning 80% of profits go to Australian shareholders, that would be incorrect. That’s because a proportion of dividend payouts go to non-resident shareholders.

For example, if a dividend was paid on 31 December 2017 by Australia’s ‘Big Four’ banks, non-resident investors would have received between 21.21% and 26.5% of any dividends declared – meaning Australian investors would have received closer to 60% of profits.

Do ‘nearly 80% of bank profits go straight back to shareholders’?

The Australian Bankers’ Association (ABA) is an advocacy group representing the interests of the Australian banking industry. The ABA has 24 member banks, but the claim about what percentage of profits are paid to shareholders doesn’t cover all of its 24 members.

On the “Australian Banks Belong To You” campaign website, the ABA said it based its “nearly 80%” claim on “the dividend payout ratio of the eight key Australian retail banks averaged over 2016 and 2017”, with the numbers sourced from bank annual reports.

Dividends are cash payments that listed companies make to their shareholders. The cash payments are often made regularly. The “dividend payout ratio” is the sum of the dividends paid to shareholders in a year, divided by the sum of the cash earnings the company made.

In other words, the dividend payout ratio is the portion of corporate profits that are paid directly back to shareholders. Companies retain the rest of profits, usually to finance future growth.

While the ABA didn’t name the banks it based its claim on, the eight largest retail banks in the ABA are the Commonwealth Bank, National Australia Bank, ANZ, Westpac, Bank of Queensland, Bendigo Bank, Suncorp and Macquarie Bank.

If we look at dividend payout ratios for those eight banks since 2013, we can see that the overall average payout has consistently hovered around 80% for the past five years.

The same is true of the average payout of the ‘Big Four’ Australian banks – Commonwealth Bank, Westpac, ANZ and National Australia Bank.

In 2012, an outlying dividend payout caused the average dividend payout to appear abnormally high. In the preceding five-year period from 2007 to 2011 payout ratios were lower, as you can see in the chart below.

Do profits ‘belong to everyday Australians’?

The ABA claimed that of those bank profit distributions, the “majority” go to Australians, including “millions of everyday Australians who own bank shares through their super funds”.

The ABA did not define what it meant by “everyday Australians”. In justifying its claim, the ABA correctly cited Australian Tax Office data that shows that as of June 30, 2016, more than 14.8 million Australians had at least one superannuation fund account.

On its website, the ABA stated it’s “safe to say that many super funds invest in Australian bank shares as part of their portfolio”.

Superannuation funds do typically hold a balanced portfolio that represents the major members of the Australian Stock Exchange (ASX). A typical superannuation portfolio might invest in bonds, and in a portfolio of the largest 200 stocks on the ASX, which would include the major banks. This can be subject to individuals’ investment preferences.

For example, say the fund invests in the largest 200 companies on the ASX, and invests in proportion to the companies’ size (that is – the largest companies get the largest investment). Then, the big four banks would be four of the five largest investments.

Obviously, not all superannuation accounts invest in bank stocks, and portfolios can be structured in different ways. For example, some superannuation funds allow their members to invest only in bonds, and people with self managed superannuation funds choose their own investments.

Some wealthy shareholders, and overseas shareholders, also benefit from holding Australian bank shares. As with all companies, shareholders benefit in proportion to their shareholding. Listed banks have no say over whether wealthy Australians, or overseas buyers, purchase their shares.

But it is fair to say that “millions of everyday Australians who own bank shares through their super funds” benefit from dividend payouts. – Mark Humpherey-Jenner

Blind review

The Australian Banking Association claimed that nearly 80% of all Australian bank profits go back to shareholders, and that the majority of those shareholders are everyday Australians who own bank shares through their super funds.

Those claims are valid when read independently, as set out above. But they should not be read together as indicating that nearly 80% of profits go to Australian shareholders.

The proportion of dividends that go back to Australians, either directly or through their investment portfolios, would be less than 80% of bank profits.

Reviewing the investor profiles of ANZ, CBA, NAB and Westpac shows that on December 31, 2017, Australian investment ranged from 73.5% to 78.79% across the big four banks, and institutional investment, which includes superannuation funds and other financial institutions, represented slightly under half of investors.

The high representation of domestic institutional holdings demonstrates the significance of bank shares in most investment portfolios, including superannuation funds.

Foreign ownership of Australian banks. NAB presents the data in a different way to the other banks.Author provided based on reports from ANZ, CBA, NAB, Westpac

So if a dividend had been paid on 31 December 2017 for Australia’s ‘Big Four’ banks, non-resident investors would have received between 21.21% and 26.5% of that dividend declared, meaning Australian investors would have received closer to 60% of profits. – Helen Hodgson

Author: Mark Humphery-Jenner, Associate Professor of Finance, UNSW; Reviewer, Helen Hodgson, Associate Professor, Curtin Law School and Curtin Business School, Curtin University

Australians will finally enjoy the ability to send each other money in “real time”, with the launch of the New Payments Platform (NPP) today. The platform is a mixture of new processes for settling transactions between banks, guided by the Reserve Bank of Australia.

But while this may make payments faster, it could also make them less safe.

And data from the United Kingdom’s real-time payments platform, Faster Payments, show the take-up of Australia’s system may not be that strong. Although it was launched 10 years ago, Faster Payments has not yet become the most popular payment method in the UK. The most popular is still the traditional system, which takes three days to clear.

Research into the Faster Payments platform shows it is rife with fraud and scams. Part of the problem in the UK is that banks have trouble identifying potentially fraudulent transactions.

The New Payments Platform will also change how you transfer money. BSB and account numbers will still exist, but individuals and businesses can create other identifiers, called “PayID”. This means mobile numbers or email addresses can also be used as a way to identify yourself, both to pay and be paid by others.

The platform will also remove the delays caused by weekends and public holidays and mean you can make transfers after business hours.

The impetus for a real-time payment platform came from a 2012 review by the Reserve Bank of Australia. It found that Australia’s payment system lagged behind even less developed nations, such as Mexico.

But not all banks have signed on to the new payments platform. Those taking a wait-and-see approach include Bank of Queensland, Suncorp and Rabobank. Even some of the subsidiaries of one of the big four banks, Westpac (such as Bank of Melbourne and St George), will not be involved in the launch of the New Payments Platform.

Fraud and abuse in real time

Before the New Payments Platform, numerous safeguards were built into Australia’s payment system that limited fraud and abuse. For instance, if you were planning to buy a car, you would likely go into your bank and ask for a bank cheque. This cheque would be made out to the name of the dealership or person selling the car.

A number of protections are built in to this system. The money is guaranteed by your bank and will clear within three days once deposited. If someone with a different name tries to deposit the cheque, then the cheque will not be accepted and hence the payment will be revoked.

Under the terms and conditions issued by one of the participating banks, banks are not liable for losses that are a result of you giving the wrong account information. Furthermore, a transfer instruction given by you, once accepted by your bank, is irrevocable.

This also applies if you were fraudulently induced to make a transfer via the New Payments Platform. In this case your bank might be able to help you recover the funds, but the recipient of the funds (potentially a fraudster) will have to consent to repay your funds. So if you have a dispute with a recipient of your funds transfer, you will need to resolve the dispute directly with that person or organisation under the new scheme.

It is likely that similar terms and conditions will apply to all the institutions that are members of the New Payments Platform.

The problem will only get worse as the “cap” on transactions is lifted. This happened in the United Kingdom once the Faster Payments cap was raised to £250,000 in 2015.

According to the managing director of the UK Payment Systems Regulator, Hannah Nixon: “There is no silver bullet for [authorised push payment] scams and some people will still, unfortunately, lose out.” Nixon added that account holders also need to take “an appropriate level of care” in protecting themselves.

The UK experience shows that the New Payment Platform is likely to speed up transactions. It took two years for Faster Payments to pass 500 million transactions, but it sped up and passed 5 billion transactions in just over seven years.

In June 2017, Faster Payments processed 135.7 million payments, which was a 15% increase on the previous June. These payments amounted to a total of £115 billion for that month.

But Faster Payments is still not the biggest payment platform in the United Kingdom. Although we don’t know exactly why, there are many possible reasons – including customers not wanting to switch from something they are used to and a fear of fraud.

It could also be that British financial institutions are not promoting Faster Payments to their customers as they can charge higher fees on the traditional payment platform.

Above all, the big concern is detecting fraudulent activity in real time – something that will concern banks’ risk management and which may have led to some choosing to hang back. Payments on the New Payments Platform may be faster and easier to make, but will they be safer? It could just make fraud faster and easier for fraudsters, and harder to undo for victims.

Author: Steve Worthington, Adjunct Professor, Swinburne University of Technology

A suitable construction funding model is the critical missing ingredient needed to deliver more affordable housing in Australia. Aside from short-lived programs under the Rudd government, we have seen decades of inconsistent and fragmented policies loosely directed at increasing affordable housing. These have failed to generate anything like enough new supply to meet outstanding needs.

Our latest research looked at recently built, larger-scale affordable housing projects in contrasting markets across Australia. We examined each scheme’s cost, funding sources and outcomes. We then developed a housing needs-driven model for understanding the financial and funding requirements to develop affordable housing in the diverse local conditions across the country.

Up to now, the key stumbling block has been the “funding gap” between revenue from rents paid by low-income tenants and the cost of developing and maintaining good-quality housing. The Commonwealth Treasury acknowledged this problem last year. And the problem is greatest in the urban areas where affordable housing is most needed.

What does the new model tell us?

The Affordable Housing Assessment Tool (AHAT) enables the user to calculate cost-effective ways to fund affordable housing to meet specified needs in different markets. It’s a flexible interactive spreadsheet model with an innovative feature: it enables users to embed housing needs as the driver of project and policy, rather than project financial feasibility driving who can be housed.

Affordable housing developments have recently been relatively sparse. However, our research highlighted the varied and bespoke funding arrangements being used.

Despite this variety, too often project outcomes are driven purely by funding opportunities and constraints, rather than by defined housing needs. One notable constraint is the fragmented nature of affordable housing subsidy frameworks both within and across jurisdictions.

Our case study projects generated a diversity of housing outcomes. This can be seen as an unintended positive of the bespoke nature of affordable housing provision as a result of the need to “stitch together” gap funding from multiple sources on a project-by-project basis.

Equally though, the lack of policy coherence and fit-for-purpose funding added cost and complexity to the development process. By implication, this leads to a less-than-optimal outcome for public investment. Despite providers’ best efforts, current approaches are not the most efficient way to deliver much-needed affordable housing.

What are the lessons from this research?

We applied the model to typical housing development scenarios in inner and outer metropolitan areas and regions. By doing so, we identified six key lessons for funding and financing affordable housing delivery.

1) Government help with access to land is central to affordable housing development and enhances long-term project viability.

Especially in high-pressure urban markets, not-for-profit housing developers cannot compete with the private sector for development sites. High land costs, particularly in inner cities where affordable housing demand is most extreme, can render financial viability near impossible. Having access to sites and lower-cost land were two of the most important components of feasible projects.

2) Government equity investment offers considerable potential for delivering feasible projects and net benefit to government.

How governments treat the valuation of public land with potential for affordable housing development must be reviewed. Conventionally, even where affordable housing is the intended use, governments typically insist on a land sale price based on “highest and best use”.

It would be preferable in such cases to treat the below-market value assigned to public land as a transparent subsidy input. This would mean the sale price reflects the housing needs that the development seeks to meet. That is, the land value should be priced as an affordable housing development for a specific needs cohort.

By retaining an equity stake, government could account for its input as an investment that will increase in value over time as land values appreciate.

3) Reducing up-front debt load and lowering finance costs are critical to long-term project viability.

Debt funding imposes a large cost burden over a project’s lifetime. This is ultimately paid down through tenant rents. Reducing both the cost and scale of private financing can have a significant impact on project viability.

The analysis reinforces the rationale for the Australian government’s “bond aggregator” facility for reducing financing costs for affordable housing projects. But this must come in tandem with other measures to reduce up-front debt.

4) Delivery across the range of housing needs helps to meet overall social and tenure mix objectives. This also can help improve project viability through cross-subsidy.

Mixing tenure and tenant profiles can enable affordable housing providers to produce more diverse housing that meets the full range of needs.

Cross-subsidy opportunities arising from mixed-tenure and mixed-use developments can also enhance project feasibility. By improving a provider’s financial position, this helps advance their long-term goal of adding to the stock of affordable housing. And, by providing welcome flexibility, this enables organisations to better manage development risk across different markets and cycles.

5) The financial benefit of planning bonuses is limited

Inclusionary zoning mechanisms impose affordable housing obligations on developers through the planning system. This approach potentially offers a means of securing affordable housing development sites in larger urban renewal or master-planned areas.

However, our research demonstrated that planning bonuses allowing increased dwelling numbers in return for more affordable housing have little beneficial impact on project viability. This is because the additional dwellings allowed generate additional land and/or construction costs but no matching capacity to service a larger debt.

However, planning bonuses can be useful as part of a cross-subsidy approach. In this case, they may support project viability, without necessarily resulting in any additional affordable dwellings.

6) Increasing the scale of not-for-profit provision offers financial benefits that help ensure the long-term delivery of affordable housing.

Our analysis supports the case for targeting public subsidy to not-for-profit developers (government or non-government) to maximise long-term social benefit. Investing in permanently affordable housing ensures the social dividend of affordable housing can be continued into the future.

Comparable subsidies are not preserved when allocated to private owners. They will seek to trade out at some stage, capitalising the subsidy into privatised gain.

The results of our case study analyses and modelling highlight the need to develop comprehensive funding and subsidy arrangements that account for different costs in different locations. These arrangements also must be integrated nationally to support affordable housing delivery at scale.

This study reiterates the common finding of research over the last decade: both Commonwealth and state/territory governments need to develop a coherent and long-term policy framework to provide housing across the full spectrum of need.

Authors: Laurence Troy, Research Fellow, City Futures Research Centre, UNSW; Bill Randolph, Director, City Futures – Faculty Leadership, City Futures Research Centre, Urban Analytics and City Data, Infrastructure in the Built Environment, UNSW; Ryan van den Nouwelant, Senior Research Officer – City Futures Research Centre, UNSW; Vivienne Milligan, Visiting Senior Fellow – City Futures Research Centre, Housing Policy and Practice, UNSW

There’s more than 30 years of research showing financial consumers have behavioural biases that can lead to poor decisions. Financial providers and banks have known this too, and have designed some products to take advantage of consumer habits rather than benefit them.

Legislation soon to be introduced to parliament is intended to curb these practices, but credit products are being left out to consumer detriment.

Regulators have relied on two strategies to help consumers with this problem. Disclosure of the nature and prospects of the products providers offer. Also, encouraging consumers to seek financial advice.

Neither of these has worked well. The Financial System Inquiry in 2014 recognised that disclosure hasn’t closed the gap in consumer capability. Worse, the providers of these products may have incentives through remuneration which may not serve the customer’s interest and only about 25% of financial consumers seek advice.

The Productivity Commission’s report on competition in financial services, illustrates many of these points in arguing for regulation of mortgage brokers. Brokers are supposed to be the customer’s agent to scout for and advise on the best mortgage terms and cost. Instead they are remunerated by mortgage providers (like the banks), take commissions and, according to the Productivity Commission, generally cost more than loans directly from a bank.

Bias in financial decision-making

Consumers are prone to a range of biases which may also impair their financial decisions. For example overconfidence may cause them to ignore new information or hold unrealistic views about how high returns will be.

As we age or as our circumstances change, our tolerance for risk also changes. As we get older our tolerance for risk decreases, while having a higher income increases it. Men are also more risk tolerant than women.

Consumers may also give too much weight to recent events and things they know already and can be unduly influenced by the opinions of friends and family.

This sort of consumer decision-making is no match for providers’ knowledge of financial conditions and product features. Banks and other financial service providers have learned from experience, but most of all their own command of consumer behaviour research.

The latter leaves providers able to design and sell products that benefit from consumers not overcoming mistakes, or at times, exacerbating mistakes.

Helping customers make better choices

In a bill soon to be before the Australian parliament, those selling financial products will have to make a “target market determination”. This records and describes the market for a product (those who would buy it). It must also set out any conditions under which the product must be distributed, for example that it can only be sold with advice.

It’s designed so that financial products meet the needs and financial situation of the people acquiring them.

There are criminal and civil penalty sanctions for failing to make and ensure products are sold in accordance with a determination. Also, for failure to revise and reissue it, if circumstances change.

Twinned with this requirement are new intervention powers for the Australian Securities and Investments Commission (ASIC). ASIC will be able to make interim rules, effectively prohibiting sales or imposing conditions, if continued sale would result in “significant detriment” to financial consumers.

Product regulation is no panacea. This version has a large gap, as credit products (for example credit cards or mortgages) do not require a target market determination. It’s not difficult to read the politics of regulation in this omission. There is also a risk that target market determinations will become pro-forma and add to compliance and not to consumer benefit. Although a description of the target market must be in the advertising, it’s not clear it must be in formal disclosure, so consumers may never read it.

Product intervention powers apply across investment, insurance and credit products but it will never be easy for ASIC to prove the risk of “significant consumer detriment”. Intervention orders also expire in 18 months unless made permanent by parliament.

The regulation of product design and distribution in the spirit of consumer safety has been commonplace (if imperfectly realised) in car, pharmaceuticals and other consumer markets, for decades. There are modest grounds for optimism that in Australia financial product safety might catch on too, but the government needs to include credit products as well.

Authors: Dimity Kingsford Smith, Professor of Law, UNSW