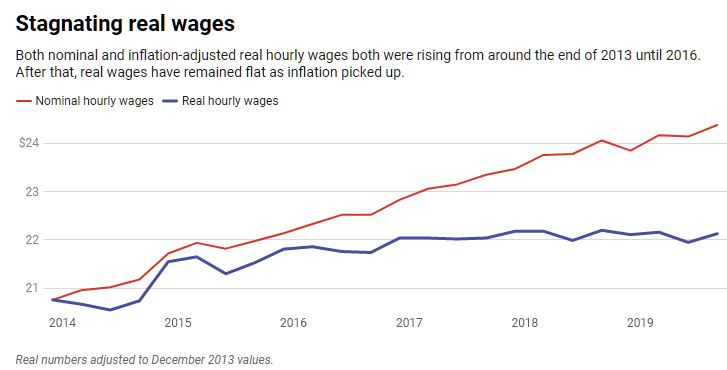

At first glance, the latest data – which came out on Feb. 7 – look pretty good. They show nominal hourly earnings rose 3.1% in January from a year earlier.

But the operative word here is nominal,

which means not adjusted for changes in the cost of living. Once you

factor in inflation, the picture changes drastically. And far from

representing a “blue collar boom” – as the president put it in his State of the Union address – the real, inflation-adjusted data show most U.S. workers have not benefited from the growing economy.

As an economist who studies wage data, I think it’s paramount that we take a step back and look at what the data really show.

Business journalists and financial markets

tend to focus on the monthly data. These figures are only reported in

nominal or current terms because the inflation data doesn’t come out

until later.

A more complete set of wage and pay data

is reported quarterly. The latest release came out in December for the

third quarter. These figures are not only adjusted for inflation but

also include fringe benefits, which account for just under a third of

total compensation.

At first blush, it makes sense to focus

primarily on the first set. Newer data is, well, newer, and market

participants and companies prefer the latest information when making

decisions about investments, hiring and so on.

But the effect of inflation means that the same US$1 bill buys less stuff over time as prices increase.

From December 2016 to September 2019, nominal wages rose 6.79% from $22.83 to $24.38. But after factoring in inflation, average wages barely budged, climbing just 0.42% in the period.

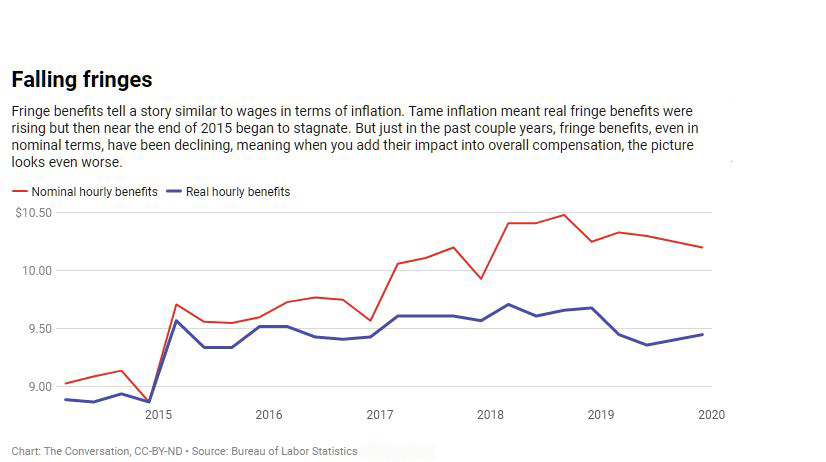

Incorporating fringe benefits into the picture adds another wrinkle.

The inflation-adjusted or real value of

fringe benefits, which include compensation that comes in the form of

health insurance, retirement and bonuses, declined 1.7% in the

three-year period.

Altogether, that means total real compensation slipped 0.22% from the end of 2016 to September 2019.

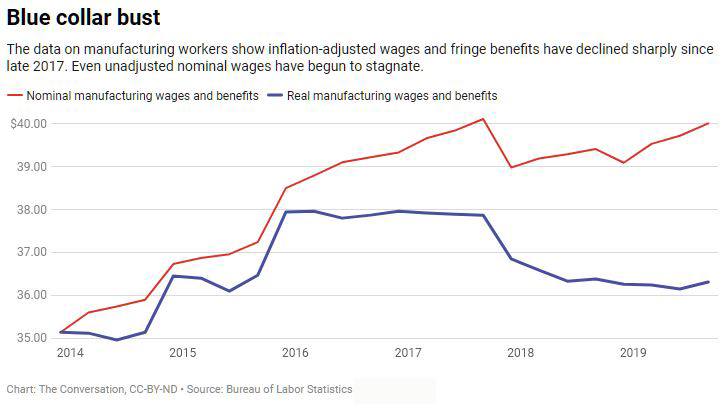

Of course, workers in different sectors

have fared differently. The Trump administration has singled out

manufacturing workers – who it says are the main beneficiaries of its

trade war and other policies intended to support the sector – as having

benefited from a “blue collar boom” in wages.

The nominal data for manufacturing workers

hardly support a boom but they do show an increase of 2.22% since

Donald Trump took office.

The adjusted data, however, make it look

more like a bust, with wages plunging 3.88% in the period. And, again,

the situation is worse when we add in fringe benefits, which brings the

decline to 4.33%.

So next time you read a story about a rise in pay, try to see if it reports the wage data in nominal or real terms, and if it includes fringe benefits too. If it’s only nominal wages, the numbers may mean a lot less than they seem.

Author: David Salkever, Professor Emeritus of Public Policy, University of Maryland, Baltimore County

In our survey of 600 private renters in

different areas of Sydney and Melbourne, we asked: “Many people are

renting privately for longer periods (10+ years). Do you think this is a

positive trend?”

About a third responded in mainly positive terms. Their main reasons were:

For a more in-depth understanding, we

interviewed 60 long-term private renters in low, medium and high-rent

areas in Melbourne and Sydney. Almost all who chose to rent mentioned

flexibility as a key advantage.

“Choosers” highly valued the freedom to move or travel at will. Zygmunt Bauman’s concept of liquid modernity highlights the increasing desire for transience. As he explains:

Transience has replaced durability at the

top of the value table. What is valued today (by choice as much as by

unchosen necessity) is the ability to be on the move, to travel light

and at short notice. Power is measured by the speed with which

responsibilities can be escaped. Who accelerates, wins; who stays put,

loses.

Renters in their own words

Patricia*, who lives in a high-rent part of Melbourne, has always rented.

Well since I came to Australia in 1977, I

rented. I didn’t want to buy. Got close [to buying] a couple of times,

but changed my mind.

I just travel anywhere and everywhere. I

thought […] if you’ve got a house you’re stuck there, and I thought, no.

I work hard for my money, so that money that I work hard for is for me,

not to have a [permanent] roof over my head. […] Renting has been good

for me because I can still do what I want.

Myra lives in a studio apartment in a

high-rent area in Sydney and has no desire to own a home. She is single,

in her mid- to late 30s, and earns well. The possibility of being asked

to vacate did not bother her.

Maybe I’ve been lucky, but every situation

has always sorted itself out. You know a lot of people would have

freaked out if they had to move out […] It didn’t concern me in the

slightest, yeah. I mean not at all. There’s always somewhere to stay. So

it suits my lifestyle. I wouldn’t want to buy [a property], even if I

had the money.

Leanne inherited a third of a house.

Rather than using the proceeds to buy a property, she decided to move to

Melbourne’s inner city (a high-rent area) and continue renting.

So I thought rather than put money into a

house […] I would invest it and I could travel and go to concerts and

live the life I wanted to lead, so that’s basically what I did and I’m

still renting.

Pam was renting in a low-rent area in outer Sydney. She felt her situation required the flexibility of renting:

The relationship was rocky and you can’t predict the future, but I knew it wasn’t going to end up in marriage and kids and all that kind of crap […] We were both working, both earning good money and we could have afforded to buy a house between us […] But for me it was like, no. I don’t know where this [her relationship] is going, so no way, I’m not going to put myself in that predicament and then have to go through court to go, “This is mine, this is yours”, all that crap. But so it was my choice to rent and to stick to it […] I’m not going to rely on anybody else for anything, no way.

Her renter status allowed Pam to make a rapid, clean break.

I just got up one day and walked cos I

knew he was going to ask me to marry him the next day, so I said: “I’m

just going to go to the shops to get a packet of cigarettes.” I left

everything behind. I went for a walk, never went home.

For the families with children who choose

to rent long-term, the key reason is it allows them to live in highly

desirable areas where they cannot afford to buy. Gabrielle and her

partner earn well and live in a high-rent area in Sydney:

Sure it [home ownership] provides you with

security and you don’t have that stress of […] having to move. I get

that, but at the same time, you know for us, for example, if we wanted

to buy we’d be paying four times what we pay at the moment in a mortgage

[…] It doesn’t really make financial sense to go and do that […] You’d

have to live somewhere. So I choose to live in a nice area where my

children are [at school].

They also did not want the burden of a large mortgage:

[…] I have no desire to put myself in a

position where I have a $2 million mortgage and have to work for the

rest of my short life to pay for it […]

Although probably only a small proportion

of people choose to rent long-term, this option may be gaining ground.

Young, well-paid professionals in particular see the flexibility of

private renting as attractive.

Location also seems to be a critical

factor. Most of the choosers rented in desirable inner suburbs of Sydney

and Melbourne, which would otherwise be inaccessible. An estimated one-in-eight private renters are “rentvestors” who rent where they want to live and buy elsewhere to get a foothold in the housing market.

*All names used are pseudonyms.

Authors: Alan Morris, Research Professor, University of Technology Sydney; Hal Pawson, Associate Director – City Futures – Urban Policy and Strategy, City Futures Research Centre, Housing Policy and Practice, UNSW; Kath Hulse, Research Professor, Centre for Urban Transitions, Swinburne University of Technology

Those who say “I told you so” are rarely welcomed, yet I am going to say it here. Australian scientists warned the country could face a climate change-driven bushfire crisis by 2020. It arrived on schedule. Via The Conversation.

For several decades, the world’s scientific community has periodically assessed

climate science, including the risks of a rapidly changing climate.

Australian scientists have made, and continue to make, significant

contributions to this global effort.

Today, I will join Dr Tom Beer and Professor David Bowman to warn that Australia’s bushfire conditions will become more severe. We call on Australians,

particularly our leaders, to heed the science.

The more we learn, the worse it gets

Many of our scientific warnings over the

decades have, regrettably, become reality. About half of the corals on

the Great Barrier Reef have been killed by underwater heatwaves. Townsville was last year decimated by massive floods. The southeast agricultural zone has been crippled by intense drought. The residents of western Sydney have sweltered through record-breaking heat. The list could go on.

How serious might future risks actually be? Two critical developments are emerging from the most recent science.

First, we have previously underestimated the immediacy and seriousness of many risks. The most recent assessments

of the Intergovernmental Panel on Climate Change show that as science

progresses, more damaging impacts are projected to occur at lower

increases in temperature. That is, the more we learn about climate

change, the riskier it looks.

The city I live in, Canberra, experienced

an average seven days per year over 35℃ through the 1981-2010 period.

Climate models projected that this extreme heat would more than double

to 15 days per year by 2030. Yet in 2019 Canberra experienced 33 days of temperatures over 35℃.

Second, we are learning more about ‘tipping points’,

features of the climate system that appear stable but could

fundamentally change, often irreversibly, with just a little further

human pressure. Think of a kayak: tip it a little bit and it is still

stable and remains upright. But tip it just a little more, past a

threshold, and you end up underwater.

Features of the climate system likely to

have tipping points include Arctic sea ice, the Greenland ice sheet,

coral reefs, the Amazon rainforest, Siberian permafrost and Atlantic

Ocean circulation.

Heading towards ‘Hothouse Earth’?

These tipping points do not act

independently of one another. Like a row of dominoes, tipping one could

help trigger another, and so on to form a tipping cascade. The ultimate

risk is that such a cascade could take the climate system out of human

control. The system could move to a “Hothouse Earth” state, irrespective of human actions to stop it.

Hothouse Earth temperatures would be much

higher than in the pre-industrial era – perhaps 5–6℃ higher. A Hothouse

Earth climate is likely to be uncontrollable and very dangerous, posing

severe risks to human health, economies and political stability,

especially for the most vulnerable countries. Indeed, Hothouse Earth

could threaten the habitability of much of the planet for humans.

Tipping cascades have happened in Earth’s history. And the risk that we could trigger a new cascade is increasing: a recent assessment showed many tipping elements, including the ones listed above, are now moving towards their thresholds.

It’s time to listen

Now is the perfect time to reflect on what science-based risk assessments and warnings such as these really mean.

Two or three decades ago, the spectre of

massive, violent bushfires burning uncontrollably along thousands of

kilometres of eastern Australia seemed like the stuff of science

fiction.

Scientists are warning that the world

could face far worse conditions in the coming decades and beyond, if

greenhouse gas emissions don’t start a sharp downward trend now.

Perhaps, Australia, it’s time to listen.

Author: Will Steffen, Emeritus Professor, Australian National University

When the world’s

largest fund manager tells its clients that it plans to swiftly exit its

thermal coal investments over the next six months, this should tell us

something important.

BlackRock

manages around USD$7 trillion of funds on behalf of investors and up to now has

been cautious in its response to climate change and slow to participate in

investor campaigns. But that just

changed, for good economic reasons. Recent analysis published by the Institute

for Energy Economics and Financial Analysis (IEEFA), estimated that BlackRock

lost as much as USD$90 billion in investment value due to poor investments in

fossil fuel companies in 2019. The IEEFA

assessment also found that investments in just four fossil fuel companies,

ExxonMobil, Chevron, Royal Dutch Shell and BP accounted for around

three-quarters of the USD$90 billion loss.

Now, in a

letter to clients, BlackRock’s Global Executive Committee, led by company

founder and CEO Laurence Fink, explained that the company would be withdrawing

its investments in thermal coal producers, including any company that sources

more than a quarter of its revenue from thermal coal production.

Announcements

of this kind have come out steadily over the past couple of years. Virtually

all the major Australian and European banks and insurers, and many other global

institutions, have already announced such policies. According to the Unfriend

Coal Campaign, insurance companies have stopped covering roughly US$8.9

trillion of coal investments – more than one-third (37%) of the coal industry’s

global assets, and stopped offering reinsurance to 46% of them.

A

separate letter to CEO’s starts with a clear reference to BlackRock’s

‘fiduciary duty’ to its investors. BlackRock’s own analysis shows global

financial markets will be materially impacted by climate change, reflected in

the Bank of England’s analysis of $20 trillion at risk. “BlackRock concludes

that this stranded asset risk is not yet priced into the market, so as a

fiduciary, BlackRock really has no choice but to act.”

“Thermal

coal is significantly carbon intensive, becoming less and less economically

viable, and highly exposed to regulation because of its environmental impacts.

With the acceleration of the global energy transition, we do not believe that

the long-term economic or investment rationale justifies continued investment

in this sector,” the letter says.

“As a

result, we are in the process of removing from our discretionary active

investment portfolios the public securities (both debt and equity) of companies

that generate more than 25% of their revenues from thermal coal production,

which we aim to accomplish by the middle of 2020.

Environmental,

Social, and Governance (ESG) Criteria are coming to the fore – Environmental –

a set of standards for a company’s operations that consider how a company

performs as a steward of nature. Social – examines how a company manages

relationships with employees, suppliers, customers, and the communities where

it operates. Governance – how its deals with a company’s leadership, executive

pay, audits, internal controls, and shareholder rights.

“As part

of our process of evaluating sectors with high ESG risk, we will also closely

scrutinize other businesses that are heavily reliant on thermal coal as an

input, in order to understand whether they are effectively transitioning away

from this reliance.”

The move

will see the investment giant dump around USD$500 million (A$725 million) in

thermal coal investments.

And firms

should note that Blackrock is going to flex its influence. “Given the groundwork we have already laid

engaging on disclosure, and the growing investment risks surrounding

sustainability, we will be increasingly disposed to vote against management and

board directors when companies are not making sufficient progress on

sustainability-related disclosures and the business practices and plans

underlying them,” Fink said.

So,

Blackrock’s Fink seems to have figured out the huge impact that climate change

will have on not just money, but the world.

“Will

cities, for example, be able to afford their infrastructure needs as climate

risk reshapes the market for municipal bonds?” Mr Fink wrote in his letter to

CEOs.

“What

will happen to the 30-year mortgage – a key building block of finance – if

lenders can’t estimate the impact of climate risk over such a long timeline,

and if there is no viable market for flood or fire insurance in impacted areas?

What happens to inflation, and in turn interest rates, if the cost of food

climbs from drought and flooding? How can we model economic growth if emerging

markets see their productivity decline due to extreme heat and other climate impacts?”

he said.

BlackRock

also announced that it would join the Climate Action 100+ initiative, that

supports investors to actively engage with the companies they are invested in

to assess, disclose and address the risk that climate change and the energy transition

poses to the company and the value of investments. The Climate Action 100+

initiative includes the Australian based Investor Group on Climate Change,

which supports Australian institutional

In 2019,

the UK-based think tank InfluenceMap released a report that showed

BlackRock was the leader of the asset management pack in terms of fossil fuel

ownership. As at June 2018, the oil, gas and thermal coal reserves controlled

by fossil fuel producers it holds represented an aggregated 9.5 gigatonnes of

carbon dioxide emissions equivalent, with just under half of these emissions in

thermal coal and equivalent to 30 per cent of total global energy-related

carbon emissions in 2017.

“Among

the 10 asset management groups with the largest aggregate fund AUM,

BlackRock holds the most coal-intensive portfolios,” the report said. A -100%

indicates full divestment while positive values indicates adding coal to the

portfolio during the period 2011-2016.

“However,

there are key differences between BlackRock’s passively and actively managed

funds,” the report noted. “The group’s passively managed funds show a thermal

coal intensity in 2018 of 680 t/US$m AUM, while its actively managed funds show

a much lower TCI of about 300 tons/$m AUM, well below the global fund

benchmark.”

And significantly

ESG investment strategies are growing in profitability, with new geographic

trends adding to their value, according to Amundi Asset Management who analysed

the performance of 1,700 companies across five investment universes. Their

research – ESG investing in recent years: New insights from old challenges

– found that ESG strategies tended to penalise ESG investors between 2010 and

2013, but rewarded investors after 2014. “We have observed a massive

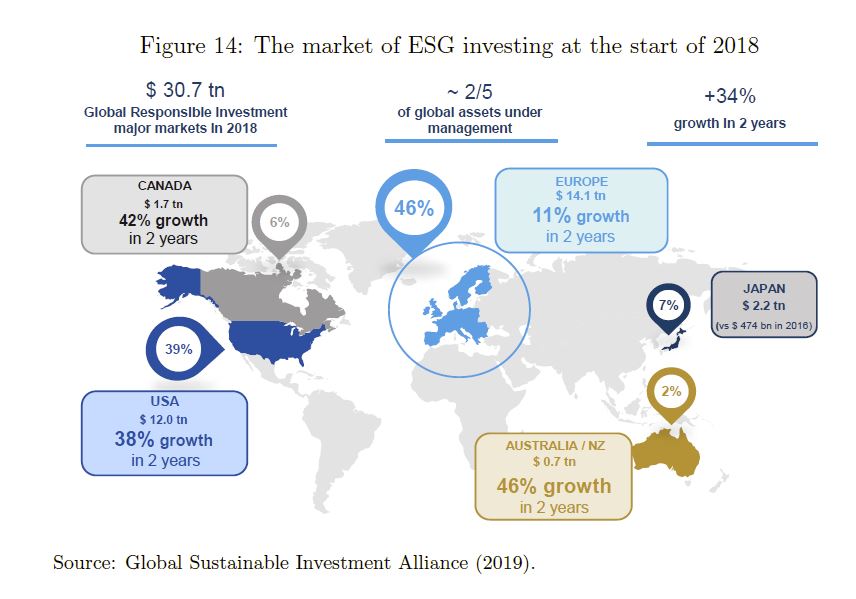

mobilisation of institutional investors on ESG,” they said. The global responsible investment is

estimated to be $30.7 trillion USD, or two fifths of assets under management.

This is a 34% growth in two years.

But here

is the problem. Most of the money that BlackRock manages is wrapped up in

passive investments, which track indexes. Indexes tend to contain the shares of

the sort of companies that BlackRock’s active arm is now divesting from. So, what

exactly BlackRock can do about that? Is this more than greenwash?

Mr Fink

has said that BlackRock will be doubling its offerings of ESG ETFs and will work

with index providers to expand and improve the universe of sustainable indices.

The company will also simplify the process by which investors can integrate ESG

into their existing portfolios by adding a fossil fuel screen and has also

expanded its impact investment strategy.

But the

contradiction between the company’s new activist stance and the passive

replication of an energy-heavy index such as Australia’s is obvious. One

solution might be for large mining companies such as BHP to dump their coal

assets in order to remain part of both Blackrock’s actively managed (stock

picking) and passively managed (all stocks) portfolios. This was discussed in a

recent “The Conversation” article.

Another

might be the development of index funds from which firms reliant on fossil

fuels are excluded. It is even possible that the compilers of stock market

indexes will themselves exclude these firms.

But once

bond investors follow the lead of Blackrock and other financial institutions,

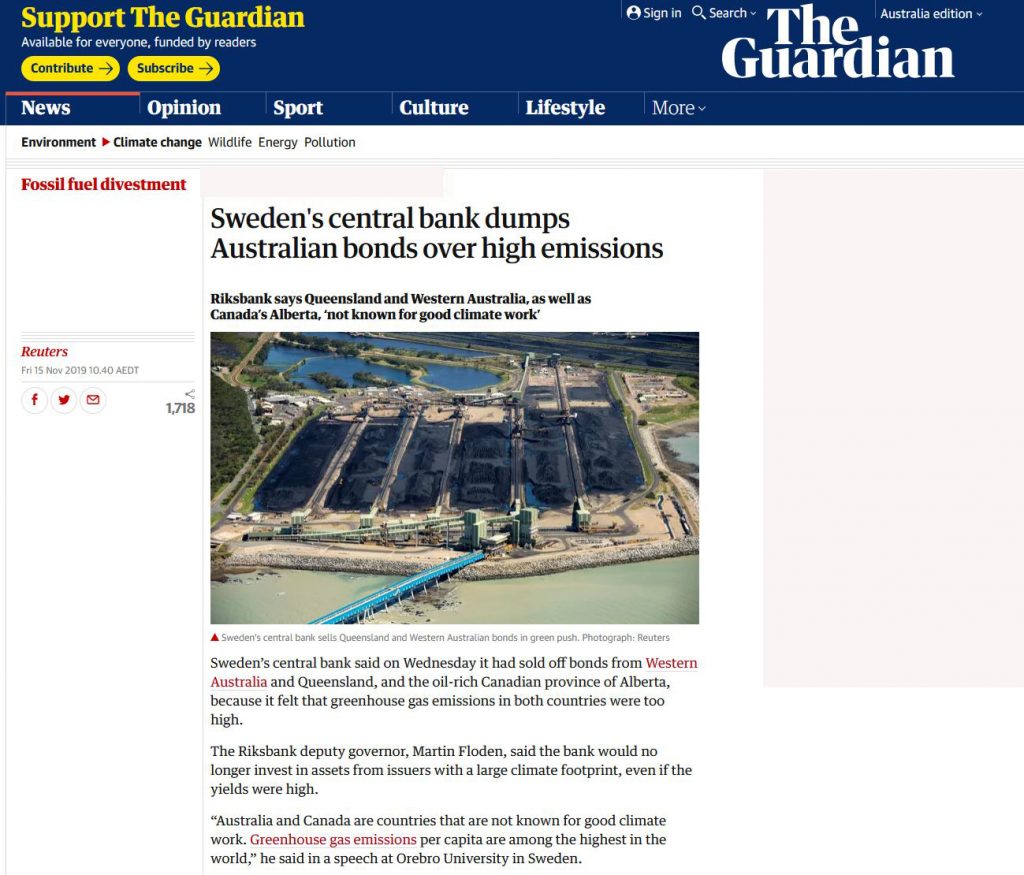

divestment of Australian government bonds will likely follow. This process has

already started, with the decision of Sweden’s central bank to unload its holdings of

Australian government bonds.

Taken in

isolation, Sweden’s move had virtually no effect on Australia’s bond prices and

yields. But the most striking feature of the divestment movement so far is the

speed with which it has grown from symbolic gestures to a severe constraint on

funding for the firms it touches.

The

effects might be felt before large-scale divestment takes place. Ratings

agencies such as Moody’s and Standard and Poors are supposed to anticipate risks

to bondholders before they materialise.

Once

there is a serious threat of large-scale divestment in Australian bonds, the

agencies will be obliged to take this into account in setting Ausralia’s credit

rating. The much-prized AAA rating is likely to be an early casualty.

That

would mean higher interest rates for Australian government bonds which would

flow through the entire economy, including the home mortgage rates mentioned in

the Blackrock statement.

So the government’s case for doing nothing about climate change (other than cashing in on past efforts) has been premised on the “economy-wrecking” costs of serious action. But as investments associated with coal are increasingly seen as toxic, we run an increasing risk that inaction will cause greater damage. So yes, Blackrock’s announcement is a real wake-up call, like it or not.

We look at the latest estimates for the costs of the bushfires, especially as they relate to tourism, and consider the problem of smoke pollution, which is something which Australia has been battling for years, but which appears to be at a new level now.

From The Conversation. As someone who has studied Australian climate policy and politics closely, this summer’s bushfire crisis have been both heartbreaking and bewildering. The grave warnings politicians ignored for so long have now come to pass.

The fires may be without precedent, but

these dark weeks have also brought an overwhelming sense of déjà vu.

It’s hard to believe, but the Morrison government’s fumbling response to

the fires and the broader climate crisis is in many ways history

repeating.

From the disastrous optics of Prime

Minister Scott Morrison’s trip to Hawaii to blaming conservationists for

the fires, our politicians keep making the same blunders and rolling

out the same failed strategies.

Here are five recurring themes in Australian politics when it comes to climate change and bushfires:

1. Blaming ‘greenies’

As the fire season ramped up in November last year, New South Wales Nationals leader John Barilaro accused the Greens of preventing governments from conducting hazard reduction burning, implying the party should shoulder blame for the fires.

“We’ve got to do better and I know that we

don’t do enough hazard reduction […] because of the ideological

position from the Greens,” he said.

Such sentiment, which has been thoroughly debunked, regularly surfaces when bushfires rage.

Following the 2003 Canberra fires and 2009 Victorian fires, the forest industry said conservationists were preventing state governments from conducting hazard reduction burns.

After Victoria’s fires, former West Australian MP Wilson Tuckey also blamed the Greens, and parties seeking their preferences, for preventing controlled burns and causing the crisis.

McCormack continues a long tradition of

those opposed to strong climate action claiming only inner-city dwellers

care about the issue.

It began in the late 1980s, when the the

“greenhouse effect” first became a public issue. Some politicians

derided it as just another greenies scare campaign, including

frontbencher in the Hawke Labor government, Peter Walsh.

Walsh, contemptuous of the Greens movement, continued to rail against climate action after leaving politics. He reportedly described the science around global warming as “highly speculative” and as late as 2008 claimed action on climate “would land us in Middle Ages.”.

3. Experts ignored by politicians

Since April last year,

former fire chiefs have implored the Morrison government to act on

climate change and better prepare the nation for extreme fire seasons

ahead. The government would not meet the experts to hear the advice, let

alone implement it.

Successive governments have form when it

comes to ignoring experts on climate matters. In September 1994 the

CSIRO’s then top climate scientist, Graeme Pearman, briefed the Labor government’s cabinet

about the likely impacts of climate change, as a debate over whether to

institute a carbon tax heated up. Despite the warning, no tax was

implemented.

Morrison’s decision to take a family holiday in Hawaii as the bushfire crisis grew lost him serious political skin.

Some argue, rightly, that symbolism is less important than substance, and so Morrison’s trip is itself irrelevant. But symbolism creates or destroys both morale, and the possibility of stronger political action.

In 1992 newly minted Labor prime minister Paul Keating sent environment minister Ros Kelly to the Rio Earth Summit, prompting one journalist to observe

he was “preoccupied with winning the upcoming election (and) said he

wasn’t going all the way to Rio to give a six-minute speech”.

It made Australia the only OECD nation not represented by its head of state, and sent the message that Australia was not taking a serious approach to the discussions.

5. ‘Jobs, jobs, jobs’ mantra

The Bureau of Meteorology this week confirmed

this season’s horror bushfire crisis is linked to climate change.

Planetary warming is clearly a threat to the nation’s economic

well-being.

However Australian governments have

routinely created a false dichotomy between environmental protection and

jobs. Most recently, we’ve seen it in the Coalition government’s

support for the Adani coal mine in central Queensland, and its repeated

mantra of “jobs jobs jobs”.

The strategy has been used before. After

the Franklin Dam fight in 1983, concern over environmental issues

entered the political mainstream. But as former Labor science minister Barry Jones said later, that changed in 1991 when economic recession hit.

“Jobs, jobs, jobs became the priority and

in some quarters there was a cynical reaction suggesting that

environmental issues were luxuries which characterised affluent times

[…] This is a criminally short-sighted view,” he said.

What to do?

Only sustained citizen pressure will

prevent a repeat of the past 30 years of political failures on climate

change. The public must stay informed and demand better from our elected

representatives.

Politicians can, when pressed, make better decisions. In April last year, the New Zealand government banned offshore oil and gas exploration after years of public pressure. And the following month, the UK Parliament declared a climate emergency after months of protests by activist group Extinction Rebellion.

It’s often said those who fail to learn from history are doomed to repeat it. But the world must act radically in the next decade to avoid catastrophic global warming. We cannot afford another 30 years of the same old mistakes.

Author: Marc Hudson, Researcher on sociomaterial transformations, social movements, Keele University

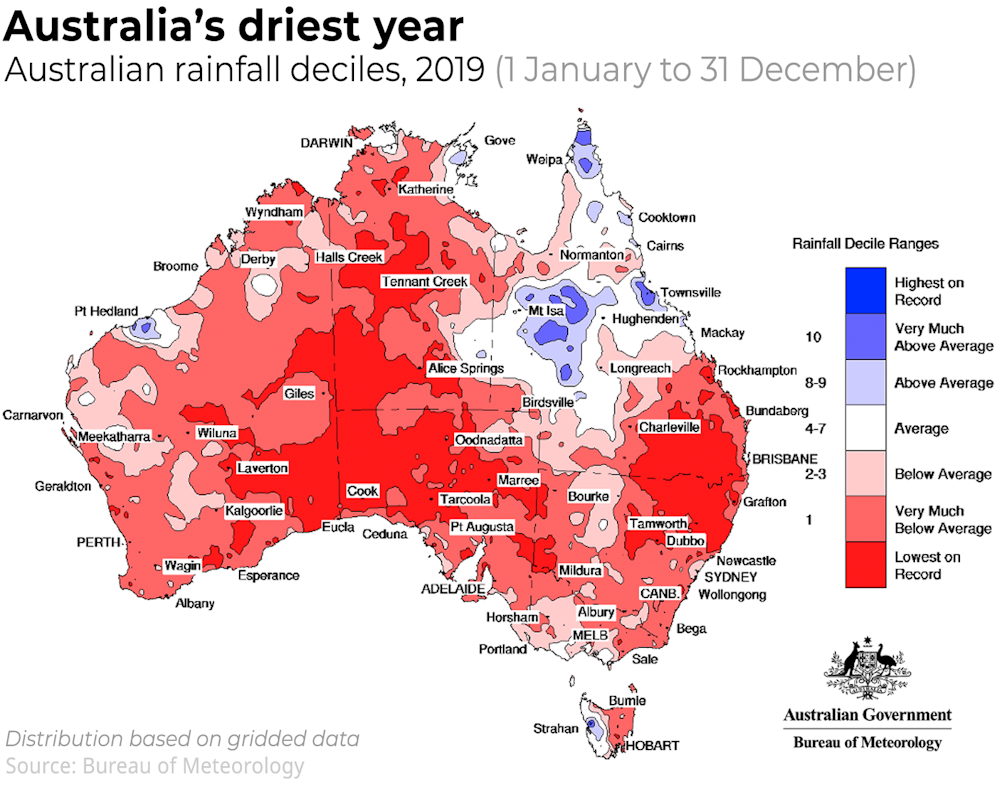

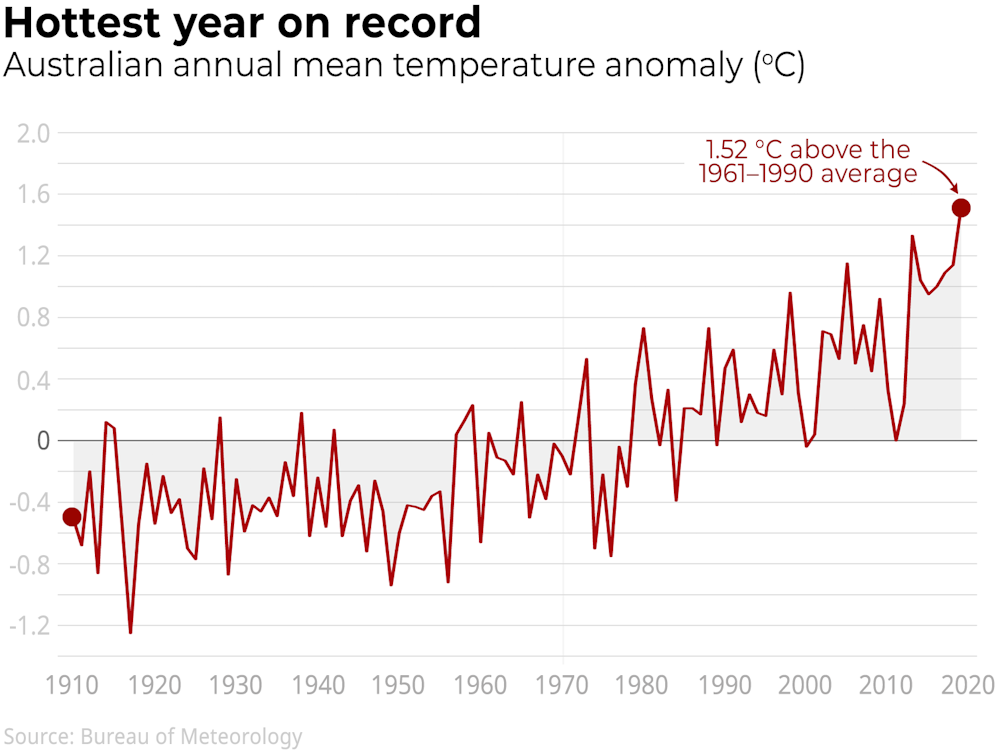

The Bureau of Meteorology’s annual climate statement just released confirms 2019 was the nation’s warmest and driest year on record. It’s the first time since overlapping records began that Australia experienced both its lowest rainfall and highest temperatures in the same year. Via The Conversation.

The national rainfall total was 37mm, or

11.7%, below the 314.5 mm recorded in the previous driest year in 1902.

The national average temperature was nearly 0.2°C above the previous

warmest year in 2013.

Globally, 2019 is likely to be the

second-warmest year, with global temperatures about 0.8 °C above the

1961–1990 average. It has been the warmest year without the influence of

El Niño.

Across the year, Australia experienced

many extreme events including flooding in Queensland and large hail in

New South Wales. However, due to prolonged heat and drought, the year

began and ended with fires burning across the Australian landscape.

The effect of the long dry

Bushfire activity for the 2018–19 season

began in late November 2018, when fires burned along a 600km stretch of

the central Queensland coast. Widespread fires later followed across

Victoria and Tasmania throughout the summer.

Persistent drought and record temperatures

were a major driver of the fire activity, and the context for 2019 lies

in the past three years of drought.

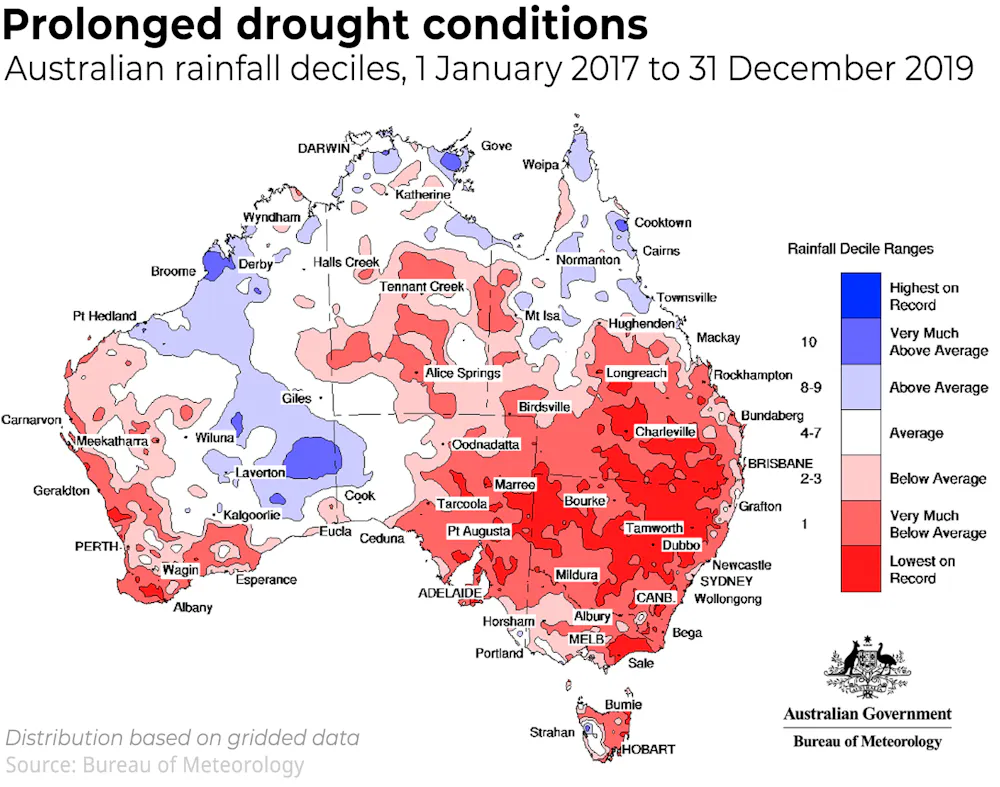

The dry conditions steadily worsened over

2019, resulting in Australia’s driest year on record, with area-average

rainfall of just 277.6mm (the 1961–1990 average is 465.2 mm).

Almost the entire continent experienced rainfall in the lowest 10th percentile over the year.

Record low rainfall affected the central

and southern inland regions of the continent and the north-eastern

Murray–Darling Basin straddling the NSW and Queensland border. Many

weather stations over central parts of Australia received less than 30mm

of rainfall for the year.

Every capital city recorded below average

annual rainfall. For the first time, national rainfall was below average

in every month.

Record heat dominates the nation

2019 was Australia’s warmest year on

record, with the annual mean temperature 1.52°C above the 1961–1990

average, surpassing the previous record of 1.33°C above average in 2013.

January, February, March, April, July,

October, November, and December were all amongst the ten warmest on

record for Australian mean temperature for their respective months, with

January and December exceeding their previous records by 0.98°C and

1.08°C respectively.

Maximum temperatures recorded an even

larger departure from average of +2.09°C for the year. This is the first

time the nation has seen an anomaly of more than 2 °C, and about half a

degree warmer than the previous record in 2013.

The year brought the nation’s six hottest

days on record peaking at 41.9°C

(December 18), the hottest week 40.5 °C (week ending December 24),

hottest month 38.6 °C (December 2019), and hottest season 36.9 °C

(summer 2018–19).

The highest temperature for the year was

49.9 °C at Nullarbor (a new national December record) on December 19 and

the coldest temperature was –12.0°C at Perisher Valley on June 20.

Keith West in southeast South Australia

recorded a maximum 49.2°C on December 20, while Dover in far southern

Tasmania saw 40.1°C on March 2, the furthest south such high

temperatures have been observed in Australia.

Accumulating fire danger over 2019

The combination of prolonged record heat

and drought led to record fire weather over large areas throughout the

year, with destructive bushfires affecting all states, and multiple

states at once in the final week of the year.

Many fires were difficult to contain in

regions where drought has been severe, such as northern NSW and

southeast Queensland, or where below average rainfall has been

persistent, such as southeast Australia.

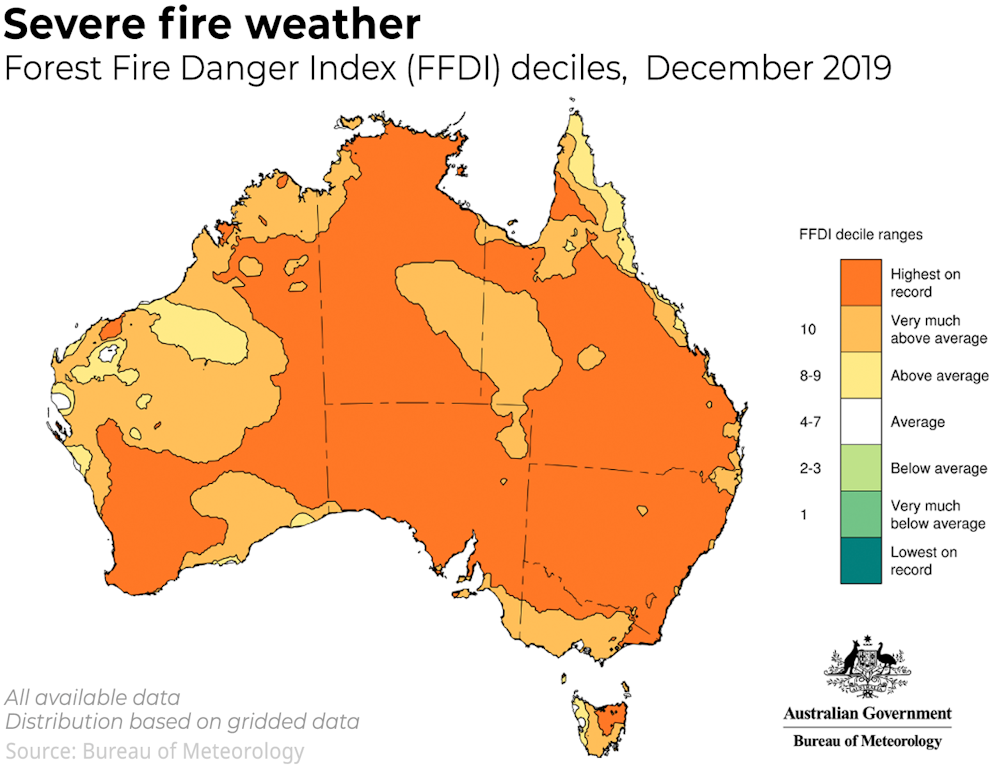

The Forest Fire Danger Index, a measure of

fire weather severity, accumulated over the month of December was the

highest on record for that month, and the highest for any month when

averaged over the whole of Australia.

Record-high daily index values for

December were recorded at the very end of December around Adelaide and

the Yorke Peninsula in South Australia, East Gippsland in Victoria and

the Monaro in NSW. These regions which experienced significant fire

activity.

Don’t forget the floods

Amidst the dry, 2019 also included significant flooding across Queensland and the eastern Top End.

Heavy rain fell from January into early

February, with damaging floods around Townsville and parts of the

western Peninsula and Gulf Country.

Tropical cyclone Trevor brought further

heavy rainfall in April in the eastern Northern Territory and

Queensland. Floodwaters eventually reached Lake Eyre/Kati Thanda which,

amidst severe local rainfall deficiencies in South Australia,

experienced its most significant filling since 2010–11.

There was a notable absence of rainfall on

Australia’s snow fields during winter and spring which meant less snow

melt. Snow cover was generous, particularly at higher elevations.

What role did climate change play in 2019?

The climate each year reflects random

variations in weather, slowly evolving natural climate drivers such as

El Niño , and long-term trends through the influence of climate change.

A strong and long-lived positive Indian

Ocean Dipole – another natural climate driver – affected Australia from

May until the end of the year, and played a major role in suppressing

rainfall and raising temperatures for much of the year.

Spring brought an unusual breakdown of the

southern polar vortex which allowed westerly winds to affect mainland

Australia. This reduced rainfall, raising temperature and contributing

to the increased fire risk.

Climate change continues to cause long-term changes to Australia’s climate. Conditions in 2019 were consistent with trends of declining rainfall in parts of the south, worsening fire seasons and rising temperatures.

Authors: David Jones, Climate Scientist, Australian Bureau of Meteorology; Karl Braganza, Climate Scientist, Australian Bureau of Meteorology; Skie Tobin, Climatologist, Australian Bureau of Meteorology

We look at data from our household surveys in the light of a recent The Conversation article. Many households are underinsured, and may be caught out in a crisis.

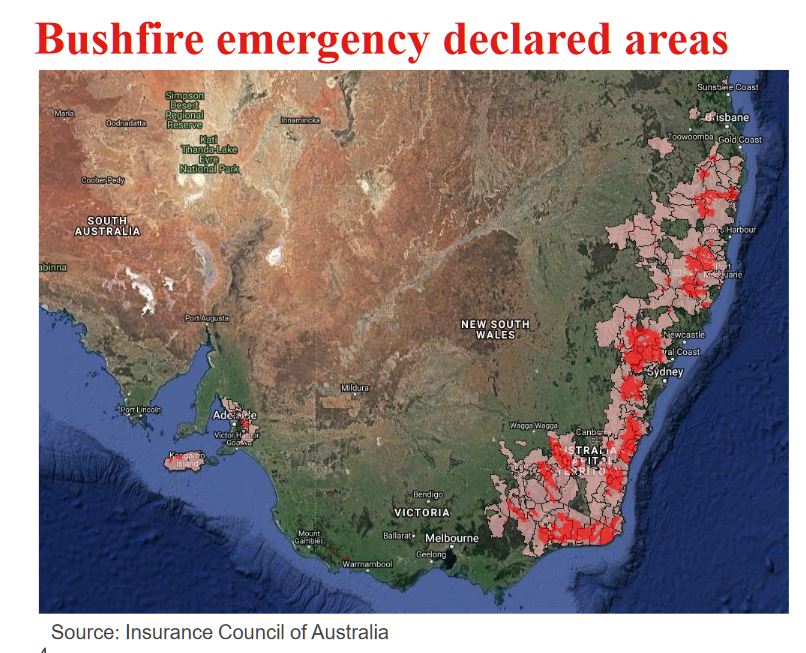

Australia is in the midst of a bushfire crisis that will affect local communities for years, if not permanently, due to a national crisis of underinsurance. Via The Conversation.

Already more than 1,500 homes have been

destroyed – with months still to go in the bushfire season. Compare this

to 2009, when Victoria’s “Black Saturday” fires claimed more than 2,000

homes in February, or 1983, when the “Ash Wednesday” fires destroyed

about 2,400 homes in Victoria and South Australia, also in February.

The 2020 fire season could end up surpassing these tragedies, despite the lessons learned and improvements in preparedness.

One lesson not really learned, though, is

that home insurance is rarely sufficient to enable recovery. The

evidence is many people losing their homes will find themselves unable

to rebuild, due to lack of insurance.

Research published by the Victorian government in 2017, meanwhile, estimated just 46% Victorian households have enough insurance to recover from a disaster, with 28%

underinsured and 26% having no insurance.

The consequences aren’t just personal.

They potentially harm local communities permanently, as those unable to

rebuild move away. Communities lose the vital knowledge and social

networks that make them resilient to disaster.

Miscalculating rebuilding costs

All too often the disaster of having your

home and possessions razed by fire is followed by the disaster of

realising by how much you are underinsured.

As researchers into the impact of fires,

we are interested why people find themselves underinsured. Our research,

which includes interviewing those who have have lost their homes, shows it is complicated, and not necessarily due to negligence.

For example, a woman who lost her home in

Kinglake, northeast of Melbourne, in the 2009 fires, told us how her

insurance calculations turned out to bear no resemblance to the actual

cost of rebuilding.

“You think okay, this is what I paid for

the property,” she said. “I think we had about $550,000 on the house,

and the contents was maybe $120,000.” It was on these estimates that she

and her partner took out insurance. She told us:

You think sure, yeah, I can rebuild my

life with that much money. But nowhere near. Not even close. We wound up

with a $700,000 mortgage at the end of rebuilding.

An extra mortgage

A common issue is that people insure based on their home’s market value. But rebuilding is often more expensive.

For one thing there’s the need to comply

with new building codes, which have been improved to ensure buildings

take into account their potential exposure to bushfire. This is likely

to increase costs by 20% or more, but is rarely made clear to insurance customers.

Construction costs also often spike following disasters, due to extra demand for building services and materials.

A further contributing factor is that

banks can claim insurance payments to pay off mortgages, meaning the

only way to rebuild is by taking out another mortgage.

“People who owned houses, any money that

was owing, everything was taken back to the bank before they could do

anything else,” said a former shop owner from Whittlesea, (about 30km

west of Kinglake and also severely hit by the 2009 fires).

This meant, once banks were paid, people had nothing left to restart.

She told us:

People came into the shop and cried on my

shoulder, and I cried with them. I helped them all I could there. That’s

probably why we lost the business, because how can you ask people to

pay when they’ve got nothing?

Undermining social cohesion

In rural areas there is often a shortage

of rental properties. Insurance companies generally only cover rent for

12 months, which is not enough time to rebuild. For families forced to

relocate, moving back can feel disruptive to their recovery.

Underinsurance significantly increases the

chances those who lose their homes will move away and never return –

hampering social recovery and resilience. Residents that cannot afford

to rebuild will sell their property, with “tree changers” the most

likely buyers.

Communities not only lose residents with local knowledge and important skills but also social cohesion. Research in both Australia and the United States suggested this can leave those communities less prepared for future disasters.

This is because a sense of community is

vital to individuals’ willingness and ability to prepare for and act in a

threat situation. A confidence that others will weigh in to help in

turn increases people’s confidence and ability to prepare and act.

In Whittlesea, for example, residents

reported a change in their sense of community cohesion after the Black

Saturday fires. “The newer people coming in,” one interviewee told us,

“aren’t invested like the older people are in the community.”

Australia is one of the few wealthy

countries that heavily relies on insurance markets for recovery from

disasters. But the evidence suggests this is an increasingly fraught

strategy, particularly when rural communities also have to cope with the

reality of more intense and frequent extreme weather events.

If communities are to recover from bushfires, the nation cannot put its trust in individual insurance policies. What’s required is national policy reform to ensure effective disaster preparedness and recovery for all.

Authors: Chloe Lucas, Postdoctoral Research Fellow, Geography and Spatial Sciences, University of Tasmania; Christine Eriksen, Senior Lecturer in Geography and Sustainable Communities, University of Wollongong; David Bowman, Professor of Pyrogeography and Fire Science, University of Tasmania

Following the monumental Conservative election victory, now is the time for the economics to work through. Mark Carney is due to leave his post as governor of the Bank of England at the end of January after six and a half years in charge, and the chancellor, Sajid Javid, will be choosing a replacement soon – perhaps before Christmas. Via the UK Conversation.

This will be a pivotal decision for the

chancellor – no doubt in close consultation with Boris Johnson and his

advisers. Whoever they pick should not expect a honeymoon period. They

are arriving against the backdrop of Brexit, widening regional inequality and the prospect of a downturn in the global economy.

The frontrunners are said to be Minouche Shafik, director of London School of Economics; Kevin Warsh, a former top official at the US Federal Reserve; and Andrew Bailey, chief executive of UK regulator the Financial Conduct Authority. Add to these names Jon Cunliffe and Ben Broadbent,

both currently deputy governors at the Bank. Behind this sits a couple

of more alternative candidates: Santander chair and former Labour

minister Shriti Vadera and Boris Johnson’s former economic adviser, Gerard Lyons.

An alternative governor may be just the

required medicine at present, since there is a strong case for someone

willing to think differently about central bank management. With

interest rates still very low in the UK and most other developed

economies, there are widespread concerns that central banks will be unable to fight another downturn using the classic response of cutting rates.

Beyond this, there are arguments for

revising the entire model of central banking. In recent years, the trend

has been for them to manage rates without any political interference

and to concentrate purely on keeping inflation low. Indeed, it is almost

30 years to the day since the Reserve Bank of New Zealand became the first central bank to make inflation the sole priority.

In times of inflation, this system made sense. But since the 2007-08 financial crisis, the world has found itself in a situation where economic growth is much weaker and deflation is more of a risk than inflation.

The Bernanke exception

As former Federal Reserve chair Ben Bernanke said in a speech in Tokyo

in 2003, “in the face of inflation … the virtue of an independent

central bank is its ability to say ‘no’ to the government”, but with

protracted deflation of the kind that has continually dogged Japan, “a more cooperative stance” by central banks towards the government is required.

His argument was essentially that it’s

hard to sustain inflation by manipulating interest rates, and that

you’re more likely to be successful using the fiscal levers of

government spending and tax cutting. The same approach is arguably required in the UK today and across the developed world.

Having lost the ability to properly

stimulate the economy using interest rates, the Bank of England and

other central banks have taken it in turns to resort to quantitative

easing – essentially creating money with which to buy mainly government

bonds from banks and other financial institutions. This was supposed to

drive extra liquidity into the economy, but mainly it has just been used

to bid up prices in the likes of the bond market and stock market and

exacerbate the wealth gap.

As an alternative, some commentators are now touting “helicopter money”:

this would involve central banks creating money that would be handed

straight to the public via government tax cuts or public spending – thus

requiring them to coordinate their policies in a way that does not

happen at present.

This could be pursued in conjunction with a novel concept called “modern monetary theory”,

which envisages government targets to boost demand and inflation

financed by a disciplined central bank that keeps interest rates at

zero. We are already seeing signs of the government moving in the same

direction by shifting away from austerity towards more generous spending.

As for the Bank of England’s own targets,

greater policy cooperation with the government would provide wiggle room

for focusing beyond inflation. In particular, the Bank could play a

role in addressing regional inequality. The UK already has the one of the worst rates

of regional inequality in the developed world, with areas like the

north of England and West Midlands bringing up the rear. This will be heightened by leaving the EU, since these same areas are key to international supply chains and expected to be the worst hit.

The answer is for the government to pursue

an industrial policy that aims to improve productivity in regions where

it is weakest, through the likes of targeted tax breaks and economic

development zones, with an accommodating Bank of England providing the

funding to facilitate.

More productive areas attract more capital, which is the reason behind

the north-south divide in the first place. Such an industrial policy

would encourage more investment in these areas, produce real-wage

increases, boost local demand and stimulate regional development. In

short, it would help counteract the impact of Brexit.

Long-term thinking

Two central criteria for the appointment

of the next Bank of England governor stand out. First, they must

understand the deeper economic and social circumstances that have led to

Brexit and the UK’s shift to the right. They must act as governor for

the whole country and not just for London plc: a move away from focusing

on smoothing short-term fluctuations towards prioritising long-term

growth.

Second, the job specification for the next governor says that the candidate should have “acute political sensitivity and awareness”. This might suggest that the government does not want another governor with such outspoken views on say, the economic risks from Brexit. Be that as it may, policy coordination needs to be a priority. I don’t rule out the possibility of the leading candidates being able to work like this, but I worry that they will be too orthodox for the challenge. The government should recognise the shifting sands in central bank policy and appoint someone who is willing to lead from the front.

Author: Drew Woodhouse, Lecturer in Economics, Sheffield Hallam University