I am today

making an official complaint about the behaviour of the Australian Treasury

relating to disclosures as a result of a Freedom of Information request (FOI

2580 – Document 1) relating to Economy Wide Cash Payment Limit (CPL).

The basis of

good Government is effective consultation and engagement with the public. The

evidence suggests this has been actively avoided in this case to drive a

specific agenda.

The

Submission provided Minister Sukkar and the Treasurer Frydenberg with a

briefing on the outcomes of the public consultation Treasury facilitated

concerning the Currency (Restrictions of the Use of Cash) Bill 2019, the

Currency (Restrictions on the Use of Cash – Excepted Transactions) Instrument

2019 and other associated documentation. The public consultation was conducted

by Treasury from 26 July 2019 to 12 August 2019.

Specifically,

in the advice, Treasury informed the Minister and the Treasurer that:

“Treasury

has received over 3,500 submissions during the two-week public consultation

period. Over 3,400 of these submissions are part of a campaign by the Citizens

Electoral Council.”

This is a

factually incorrect statement, in that I have evidence that many of the

submissions, whilst they might echo some of the sentiments voiced by the CEC, were

not directly or indirectly associated with the CEC or their campaign.

Indeed,

Digital Finance Analytics, a boutique research and consulting firm made a

direct submission, and we are also aware of a significant number of other individuals

and firms who also made submissions. I have not financial or political

alignment with the CEC.

But we all

hold the firm view that the bill as presented eroded our civil liberties, did

not provide factual justification for the $10,000 cash limit, and the

connection with monetary policy and negative interest rates – as articulated

for example by the Black Economy Taskforce itself as well as agencies such as

the IMF – was not discussed in the explanatory memorandum.

This appears

to be a blatant attempt to dilute the very strong community concerns about the

propose bill, whilst displaying a strategy like that executed a couple of year

ago when the revisions to APRA’s powers were nodded though in the Senate. In

each case the CEC was used as an excuse to ignore very real community concerns.

So, I am

seeking a formal apology for this error, confirmation of the true count of

independent submissions and specifically that my own submission was NOT

bucketed into the CEC campaign count. When

will the submissions be made public so I can confirm this? Clearly your advice would also need to be

updated.

It is no

wonder that public trust in Government is at an all time low.

I will be

making the same point as part of my submission to the current Senate Inquiry.

Martin L North, Principal Digital Finance Analytics

Over the past year global growth has slowed. Several major economies,

notably Germany and the United Kingdom, as well as close trading

partners in our region such as Korea and Singapore, have recently

experienced negative quarters of growth. There has been little growth in

global trade volumes this year, and manufacturing activity in a number

of economies has weakened noticeably.

As a result, the IMF and the OECD have recently revised down their

outlook for global growth over the next couple of years. Forecasts for

global growth in 2019 are for the slowest rate of growth since the

Global Financial Crisis. That said the forecasts for global growth in

2020 is for a pick up to the region of 3.0 to 3.4 per cent which is

still reasonable.

At play have been a number of factors, chief among them the ongoing,

and still evolving, trade tensions between the United States and China.

There is no doubt that trade tensions are having real effects on the

global economy, which you see in trade data from the US and China. The

IMF estimates that trade tensions could reduce world GDP by about

0.8 per cent by 2020.

But trade tensions are not the only story. There are a number of

other factors, including Brexit, financial stability concerns in some

economies, the ongoing turmoil in Hong Kong, and geopolitical and

economic difficulties in a number of emerging market economies.

Combined, these factors are leading to an increased level of uncertainty around the outlook for the global economy.

Concerns around global trade have been further compounded by a

downturn in the global electronics cycle – which has led to particularly

poor trade outcomes in the East Asia region – as well as a downturn in

automotive production.

Central banks and governments across the world have responded to slowing global growth to support their economies. A large number of central banks, including our own, have loosened monetary policy this year. And some countries, including South Korea and Thailand, have also provided more supportive fiscal policy.

Domestic economic conditions

Here in Australia growth slowed in the second half of 2018 before

growing more strongly in the first half of 2019. The June quarter

National Accounts showed real GDP grew by 1.4 per cent through the year

to the June quarter, and in year-average terms the economy grew by 1.9

per cent in 2018-19.

A number of factors, which are temporary, have contributed to recent weakness in the economy.

Household consumption, the largest component of the economy, grew by

1.4 per cent through the year to the June quarter. A couple of factors

are contributing to slower consumption growth. Household income growth

has been modest, with strong growth in employment outcomes partly offset

by weak wage and non-wage income growth.

In more recent years, the decline in housing prices has also played a role.

This can directly affect spending via reducing confidence and increasing borrowing constraints.

The recent downturn in the housing market has had other, more direct, impacts on the Australian economy.

Dwelling investment has fallen, as expected, by around 9 per cent

over the past three quarters and continued weakness in residential

building approvals suggests that dwelling investment is likely to

continue to fall through 2019-20.

Low rates of housing market turnover have led to significant falls in

ownership transfer costs, which is a small component of GDP associated

with the transfer of assets. Ownership transfer costs detracted 0.3

percentage points from total economic growth in the year to June 2019.

Turning to business investment, in 2018-19 mining investment fell by

almost 12 per cent, detracting around 0.4 percentage points from real

GDP growth over the year. Most of this fall reflects the completion of a

number of large LNG projects that had been holding up activity.

Non-mining business investment was weaker than expected in 2018‑19.

This is consistent with an easing in business conditions and confidence.

Despite the recent weakness in household consumption and investment, there are reasons to be optimistic about the outlook.

Recent data have shown early signs of recovery in the established housing market. Combined capital city housing prices have risen for the past three months for which we have data. Housing market turnover and auction clearance rates have also picked up.

In addition, the recently legislated personal income tax cuts and declines in interest rates are providing support to disposable household incomes. We expect this to flow through to increased consumption.

Although we have some indicators of consumption available for the

September quarter, which have not shown a particularly large

improvement, these are only partial. And it is difficult to know what

these indicators would have been had the tax cuts not been implemented.

We will continue to assess the data on consumption as it becomes

available, but it is worth noting that even if households initially use

the tax cuts to pay down debt faster, this will still bring forward the

point at which households could increase their spending.

The substantial investment in mining production capacity continues to

boost exports and there remains significant demand for our education

and tourism services. In addition, the prospect for mining investment is

positive. We expect mining investment to grow this year for the first

time since the peak of the mining construction boom.

Public sector spending has made a substantial contribution to

economic growth in recent times, contributing 1 per cent to real GDP

growth in 2018-19 and an average of 1.1 percentage points per year over

the past four years. This compares with an average contribution of

0.8 percentage points over the past 20 years.

Unfortunately, dry weather conditions have generally persisted in

drought-affected areas. The drought conditions being experienced across

large parts of Australia have weighed on domestic activity, with farm

output directly detracting around 0.2 percentage points from real GDP

growth in 2018‑19, consistent with the PEFO forecast.

As a result, the latest forecasts from the Australian Bureau of

Agricultural and Resource Economics and Sciences (ABARES) predicted that

the farm sector will continue to experience weakness, with the gross

value of farm production expected to fall by nearly 5 per cent in

2019‑20.

Despite modest economic growth overall, labour market outcomes have

been very positive. Employment growth has continued to be strong,

increasing by more than 300,000 over the past year.

While we have seen strong growth in employment, the unemployment rate

has been broadly flat. This is because near-record rates of people are

being drawn into employment and the labour force.

We have seen a step up in participation in particular parts of our

labour market — for those in older age cohorts and for women returning

to the labour market after having children.

While strong employment growth is very welcome, it does give rise to

an issue that is not unique to Australia, that of recent low

productivity growth.

Labour productivity growth in Australia has slowed from an average rate of 1.5 per cent annually over the past 30 years to just 0.7 per cent annually over the past 5 years. Noting this rate is higher than all the G7 countries.

There is no single explanation for the slower rate of productivity

growth, and we are unsure of how much of the current slowing is cyclical

and how much is structural. This is an area of ongoing analysis and

research in Treasury and elsewhere.

We do know that business investment is important to supporting

productivity growth, with capital deepening – that is having more

capital available for each worker — accounting for around ⅔ of labour

productivity over the past 30 years in Australia.

Given historically low interest rates around the world it is somewhat

of a puzzle that business investment has not grown faster. Partly this

could reflect that the rates of return businesses use when looking at

the viability of new opportunities, so called ‘hurdle rates’, have

remained high despite lower interest rates. The current uncertainties

surrounding the global economy and significant technological

advancements may be contributing to this.

Structural factors may also be at play — it is not clear what

business investment looks like in a world where more than two-thirds of

our economy is now services based.

Another issue in the Australian context is also one shared globally.

In Australia, as elsewhere, inflation rates have remained subdued. In

part this is related to slower wage growth, which has been slower than

forecasters around the world expected. And while no‑one has come up with

a complete explanation, there are a range of explanations that go some

way to shedding light on the phenomenon.

One factor that may be affecting the relationship between

unemployment and wage growth in Australia is that the traditional

relationship between spare capacity in the labour market and the

unemployment rate may be changing. One tangible way we can see this is

that the rate of underemployment, which typically moves with the

unemployment rate, has not declined to the same extent as the

unemployment rate in this cycle as it has in the past.

A number of other long‑running changes in the labour market may also

be affecting the relationship between unemployment and wage growth. An

increasing concentration of economic activity in services industries,

the effects of demographic and technological change and globalisation

may also have played a role. Ultimately, it is difficult to draw firm

conclusions on the effect of these structural factors on wage growth,

given these factors have been occurring over a long timeframe and yet

slow wage growth globally is a more recent phenomenon.

With these uncertainties in mind, the pace of the pick-up in wage growth, and its relationship to the labour market, is likely to continue to be different than in previous economic cycles.

Fiscal outlook

Turning now to the fiscal outlook, last month the Government released

the 2018‑19 Final Budget Outcome. This showed the Budget was broadly

balanced, with an underlying cash deficit of $690 million. This was an

improvement of $13.8 billion compared with the estimate at the time of

the 2018‑19 Budget.

In light of discussions at the IMF Annual Meetings, which I attended

last week, on fiscal stance and its impact on growth, I thought it may

be useful to make a couple of remarks about the interaction of

medium-term fiscal frameworks, discretionary fiscal actions, and

structural reforms.

Medium-term fiscal frameworks are designed to deliver sustainable

patterns of taxation and government spending. As is the case in

Australia, they usually also look to minimise the need for taxation.

Medium-term fiscal frameworks reflect an assessment that apparent

short term economic weakness or unsustainably strong growth are best

responded to by monetary policy. Within a medium-term fiscal framework,

automatic fiscal movements will still assist in stabilising the economy.

For example, revenues will weaken and payments strengthen when an

economy experiences weakness – these automatic movements are called

automatic stabilisers. Allowing these automatic stabilisers to work is

entirely consistent with a medium-term fiscal objective.

In an open economy such as Australia’s, a medium-term fiscal

framework in concert with a medium-term monetary policy objective has

long been held to be the most effective way to manage the economy

through cycles.

In periods of crisis, there is a case for further temporary fiscal

actions. It is important to consider separately broader policy

objectives and temporary responses to crisis, as confusing these

objectives can lead to unintended consequences. The circumstances or

crisis that would warrant temporary fiscal responses are uncommon.

The case for structural reform is ever present. Improvements in

employment and wages, and in the profitability of businesses are the

most obvious and important drivers of this case. The most important long

term contribution to wage growth is labour productivity.

The presence of weak global and domestic growth, low interest rates,

and heightened global trade and geopolitical tensions, has elicited a

discussion of fiscal responses and structural reform and an interweaving

of the two issues.

For example, calls for additional infrastructure expenditure as part

of supply side or structural reform and to assist in stimulating the

economy sound straight forward but in practice are difficult to achieve.

The timing requirements of fiscal stimulus are hard to give effect to

while ensuring large projects are well planned and executed, and cost

and capacity pressures are managed. There are some opportunities though,

usually related to smaller projects and maintenance expenditure. The

Commonwealth and State Governments are currently actively exploring

these opportunities.

In developing policy we need to be mindful of the particular

circumstances present in the economy. A feature of the current weakness

in the global and domestic economy is heightened uncertainty among

consumers and businesses.

Given this uncertainty, medium-term fiscal and monetary policy

frameworks can play an important role in contributing to a stable and

predictable environment that is supportive of growth.

Organisational priorities

Before finishing up and moving onto questions, I would like to

briefly take the opportunity to highlight to the Committee some of the

current organisational priorities for Treasury.

The Council on Federal Financial Relations recently agreed a program

of work to boost Australia’s productivity in the areas of transport,

health, skills and environmental regulation. Treasurers also agreed to

continue work on the areas identified by the Productivity Commission in

its Shifting the Dial report. This work will complement

existing Australian Government initiatives to boost productivity through

public infrastructure investment and reforms to vocational education,

health, and regulation.

An important part of the Government’s regulatory reform and

productivity agenda is the Deregulation Taskforce. The role of the

taskforce is to identify and remove unnecessary regulatory barriers to

investment, job creation and economic growth. Initial areas of focus

announced in September include: reducing the regulatory burden for food

manufacturers who want to export; getting major infrastructure projects

up and running sooner; and making it easier for sole traders and micro

businesses to employ their first person.

Just as one example of why this is important, the taskforce has found

that food manufacturers currently have to deal with approximately 200

pieces of legislation administered by 30 different agencies governing

the movement of goods in and out of Australia, as well as multiple audit

requirements, duplicated certification and a lack of recognition of

prior compliance.

Within Macroeconomic Group, a new Centre for Population was

established on 1 July 2019 and formally launched by the Minister for

Population, Cities and Urban Infrastructure on the 4th of October 2019.

The aim of the new Centre is to provide a central, consistent and expert

perspective on population issues, which will help all levels of

government understand population changes right across Australia, and how

to plan for those changes into the future. The Centre will release an

annual National Population Statement, the first of which will be

released in 2020.

In Markets Group, the Financial Services Reform Taskforce Division is

working closely with our law design and retirement income teams as well

as with ASIC, APRA, the Office of Parliamentary Counsel and other key

stakeholders to implement the recommendations of the Royal Commission

into financial services. Implementing these recommendations will

dominate Treasury’s legislative program to at least next year.

As recommended by the Productivity Commission, the Government

announced in late September a review of the retirement income system.

The review, which will cover the current state of the system and how it

will perform in the future as Australians live longer and the population

ages, will be conducted by an independent three‑person panel. This

panel will be chaired by Mr Michael Callaghan and includes Ms Carolyn

Kay and Dr Deborah Ralston as panel members, with Treasury providing

secretariat support to the panel from within Fiscal Group. A

consultation paper is scheduled for release in November this year, ahead

of a final report to Government by June 2020.

These major pieces of work take place alongside Treasury’s ongoing

priorities, which in coming months will include preparing the 2019-20

MYEFO that will include an update of the economic and fiscal outlook.

The Treasurer has now (finally) released the proposed timetable for implementation of the recommendations from the Royal Commission made back in February.

It is entitled “Restoring Trust In Australia’s Financial System”, but of course the big question is, will these measures once implemented really get to the heart of the issue – we doubt it.

This is because the final Commission report ducked the critical conflict of interest issue between selling financial services products and delivering them.

There is first the issue of unequal power between a consumer and a financial services organisation.

We know from the Commission that financial services players consistently sought to maximise their returns, even when the best interests of consumers are businesses are voided.

And we know that the general level of financial knowledge and expertise in the community is very low – indeed many do not understand, for example the concept of compound interest, the impact of fees on returns, and even what annual percentage benchmarks really mean.

So, my view is that the RC implementation will not be necessary and sufficient to restore trust in the financial system, even if the large players chose to address their cultural deficits in relation to doing right by their customers. And industry bodies are still fighting rear guard actions to avoid significant change.

Which then takes us back to the weak and compromised regulatory system we have, where APRA and ASIC appear to land more on the side the financial system rather than consumers. So, out of all this, who is minding the back of households and businesses?

In other words Frydenberg’s introduction to this small (14 page) document has a hollow ring to it – or as bankers use to write on bad cheques “words and figures differ!”:

On 4 February 2019, I released Restoring trust in Australia’s financial system, the Morrison Government’s comprehensive response to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. In it, the Government committed to take action on all 76 of the Royal Commission’s recommendations and, in a number of important areas, go further. It represents the largest and most comprehensive corporate and financial services law reform package since the 1990s. Of the Royal Commission’s 76 recommendations, 54 were directed to the Government, 12 to the regulators and 10 to the industry. Of the 54 recommendations directed to the Government, over 40 require legislation.

In addition to the Commission’s 76 recommendations, the Government in its response announced a further 18 commitments to address issues raised in the Final Report.

The Government has implemented 15 of the commitments it outlined in response to the Royal Commission’s Final Report. This comprises eight out of the 54 recommendations that were directed to the Government and seven of the 18 additional commitments the Government made as part of its response. Significant progress has also been made on a further five recommendations with draft legislation either introduced to the Parliament, released for comment or detailed consultation papers issued.

The Government’s implementation timetable is ambitious. Excluding the reviews that are to be conducted in 2022, under the Implementation Roadmap by mid-2020, close to 90 per cent of our commitments will have been implemented. By the end of 2020 remaining Royal Commission recommendations requiring legislation will have been introduced.

In this Implementation Roadmap, we set out how we will deliver on the remaining Royal Commission recommendations and additional actions committed to. This will provide clarity and certainty to consumers, industry and regulators on the roll out of the reforms. Of course, the Government’s actions alone will not be sufficient to address the widespread misconduct identified by the Royal Commission. Individual firms must make the changes needed to their culture and remuneration practices to put consumers at the core of their business. I expect industry to also align with the urgency and priority the Government is giving to its implementation task.

The Government will ensure that key firms in the financial sector continue to address the issues identified by the Royal Commission.

At the request of Government, the House of Representatives Standing Committee on Economics will inquire into progress made by major financial institutions, including the four major banks, and leading financial services associations in implementing the recommendations of the Royal Commission. As previously announced, we will also establish an independent review in three years’ time to assess the extent to which changes in industry practices have led to improved consumer outcomes.

The Government is delivering lasting change in the financial sector to ensure public confidence is restored.

Finally, the Australian Banking Association came out with this:

Australia’s banks have welcomed the Government’s timetable for legislative change following the Hayne Royal Commission and will work with the Commonwealth to continue implementing the Commission’s recommendations.

While the forward agenda for the required legislative changes was announced this morning, banks are well down the track of implementing recommendations for which they are responsible to improve customer outcomes and earn back the trust of the Australian community.

Of the Commission’s 76 recommendations, 54 were directed to Government and more than 40 of those recommendations require legislative change. 12 are to be taken forward by the regulators, 10 are for industry to implement – eight of these are specific to the banking industry.

ABA CEO, Anna Bligh said: “Since the Final Report was handed down six months ago, banks have been working to make changes to ensure that the recommendations become part of their operating fabric.

“Make no mistake, banks understand what the community and Government expects of them and are raising their standards to rightly meet those expectations.

“The recommendations included six changes to the Banking Code. All six are underway. The ABA has already drafted provisions implementing five of the changes, had them agreed to by banks and submitted them to the regulators for approval. These are now on track for full implementation by March 2020,” Ms Bligh said.

The sixth change relates to the definition of small business. Consistent with the Commission’s recommendation, the definition was recently changed in the new Banking Code to include businesses with fewer than 100 employees and this measure is now fully operational. The further recommendation to change the financial threshold from $3M to $5M will be subject to a review that will be overseen by ASIC who will examine the potential impacts on the provision of credit to small business. The review is underway and expected to be completed in early 2021.

“In relation to culture within banks, many, including the major banks, have already completed reviews. These banks have also introduced mechanisms for the ongoing tracking of culture to determine whether actions are having the necessary impact. But banks understand that effective cultural change is not going to come about through implementing the Royal Commission recommendations alone. It will only be achieved by putting the customer at the heart of every decision our banks make.

“In addition, all banks continue to review how they remunerate staff, with a focus on good customer outcomes, not just meeting financial targets,” Ms Bligh said.

Following the release of the Final Report, the ABA established a dedicated Royal Commission Taskforce to oversee the industry’s implementation of the recommendations. This Taskforce has met six times over the past six months and will continue to meet regularly to ensure the industry responds swiftly to the Government’s legislative processes and acts to fully implement the recommendations

I discuss the draft legislation which was released last Friday, after hours, by Treasury, and consider the implications, with Robbie Barwick from the CEC.

The Council just updated their charter, and published their latest minutes. At least there is some minimal disclosure now, though high-level. Note the fact that Treasury is one of the members, alongside the RBA, ASIC and APRA.

The Council of Financial Regulators (the Council) is the coordinating body for Australia’s main financial regulatory agencies. There are four members: the Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC), the Australian Treasury and the Reserve Bank of Australia (RBA). The Reserve Bank Governor chairs the Council and the RBA provides secretariat support. It is a non-statutory body, without regulatory or policy decision-making powers. Those powers reside with its members. The Council’s objectives are to promote stability of the Australian financial system and support effective and efficient regulation by Australia’s financial regulatory agencies. In doing so, the Council recognises the benefits of a competitive, efficient and fair financial system. The Council operates as a forum for cooperation and coordination among member agencies. It meets each quarter, or more often if required.

The updates charter says:

The Council of Financial Regulators (CFR) comprises APRA, ASIC, the RBA and Treasury. It aims to facilitate cooperation and collaboration between member agencies, with the ultimate objectives of promoting stability of the Australian financial system and supporting effective and efficient regulation by Australia’s financial regulatory agencies. In doing so, the CFR recognises the benefits of a competitive, efficient and fair financial system.

The CFR provides a forum for:

identifying important issues and trends in the financial system, with a focus on those that may impinge upon overall financial stability;

exchanging information and views on financial regulation and assisting with coordination where members’ responsibilities overlap;

harmonising regulatory and reporting requirements, paying close attention to regulatory costs;

ensuring appropriate coordination among the agencies in planning for and responding to instances of financial instability; and

coordinating engagement with the work of international institutions, forums and regulators as it relates to financial system stability.

The CFR will draw on the expertise of other non-member government agencies where appropriate for its agenda, and will meet jointly with the ACCC, AUSTRAC and the ATO at least annually to discuss broader financial sector policy.

Their latest minutes:

At its meeting on 5 July 2019, the Council of Financial Regulators (the Council) discussed systemic risks facing the Australian financial system, regulatory issues and developments relevant to its members. The main topics discussed included the following:

Financing conditions and the housing market. The Council discussed credit conditions and ongoing adjustment in the housing market. Housing credit growth has stabilised at a relatively low level, with lending to investors remaining weak, particularly from the major banks. Demand for housing credit has been subdued, though there has also been some tightening in credit supply. Business credit growth has weakened recently, with lending to small businesses declining over the past year. Lenders are themselves applying stricter verification of expenses and income to small businesses, and lending may be affected by declining collateral values as housing prices decline.

Council members discussed the signs of stabilisation in the Sydney and Melbourne housing markets, evident in both housing prices and auction clearance rates. They observed that the adjustment over the past two years has been sizeable and conditions in most other capital cities continue to be soft. Risks to lenders from housing price falls have to date been limited by the strength of the labour market, low interest rates and the improvement in lending standards in recent years. Housing loan arrears have continued to edge higher, but with significant variation between regions.

Members were updated on ASIC’s public consultation on its responsible lending guidance. The responsible provision of credit is a cornerstone of consumer protection and is important to the Australian economy. It was noted that the consultation is not about increasing requirements; but rather, clarifying and updating guidance on existing requirements. For example, ASIC may further clarify areas where the law does not require responsible lending requirements to be applied (e.g. in small business lending). The Council agencies will continue to closely monitor developments in financing and the housing market.

ASIC’s product intervention powers. ASIC updated the Council on its proposed approach to the new product intervention power, legislation for which passed in April 2019. This gives ASIC the power to proactively intervene where a financial product has resulted or is likely to result in significant detriment to consumers. ASIC has launched a public consultation on its approach. Council members discussed possible applications of the new power given it is now available for use.

Product design and distribution obligations. The Council also discussed the implications of new product design and distribution obligations for retail holdings of bank-issued Additional Tier 1 (AT1) instruments. Members encouraged issuers to review their practices for issuing AT1 instruments ahead of the commencement of the new obligations in April 2021. They noted that APRA would continue to treat all AT1 instruments as regulatory capital, capable of absorbing losses in the unlikely event of a bank failure. Members discussed the importance that all holders of AT1 instruments, particularly retail investors, recognise that AT1 instruments could be written down or converted to equity.

Policy developments. Members discussed a number of policy developments, including the implementation of the recommendations of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. APRA provided an update on its policy work, including changes to its guidance on the minimum interest rate used in serviceability assessments for residential mortgage lending (announced on the morning of the meeting). APRA also updated the Council on its planned increases in the loss-absorbing capacity of ADIs to support orderly resolution. Members discussed proposals by New Zealand authorities to significantly increase Tier 1 capital ratios for banks in New Zealand.

Financial market infrastructure (FMI). The Council’s FMI Steering Committee provided an update on the design of a crisis management legislative framework for clearing and settlement facilities. This will ensure the necessary powers to resolve a distressed domestic clearing and settlement facility. A second consultation is now planned for late 2019. The Committee has also considered proposals for enhancements to the agencies’ supervisory powers and other changes to improve the regulatory framework in relation to market infrastructures. The results of the Council’s consultation findings will be provided to Government, to assist with policy design and the drafting of associated legislation (the draft of which would also be consulted on before being introduced to Parliament).

Stored-value payment facilities. The Council discussed elements of a potential regulatory framework for payment providers that hold stored value, following a public consultation in 2018. Discussion focused on suitable criteria to determine the regulatory regime that should apply to providers of stored-value facilities, along with the adequacy of consumer protection arrangements. Once completed, the conclusions of this work will be provided to the Government for consideration.

Competition in the financial system. Council agencies and the Australian Competition and Consumer Commission (ACCC) are developing an online tool to improve the transparency of the mortgage interest rates paid on new loans. This follows a recommendation of the Productivity Commission’s inquiry into Competition in the Australian Financial System. The tool relies on a new data collection and is expected to be available in 2020.

Climate change. Council members noted the work undertaken by regulators to address the implications of the changing climate, and society’s response to those changes, for the Australian financial system.

Updated Charter. The Council agreed to adopt an updated Charter, which is being published today. The Charter emphasises the Council’s financial stability objective, while also recognising the benefits of a competitive, efficient and fair financial system. It also highlights the Council’s focus on cooperation and collaboration to support the activities of its member agencies.

In conjunction with the Council meeting, the Council agencies held their annual meeting with other Commonwealth regulators of the financial sector. This included representatives from the ACCC, the Australian Taxation Office and the Australian Transaction Reports and Analysis Centre (AUSTRAC). Topics discussed included enforcement and data initiatives affecting the financial sector.

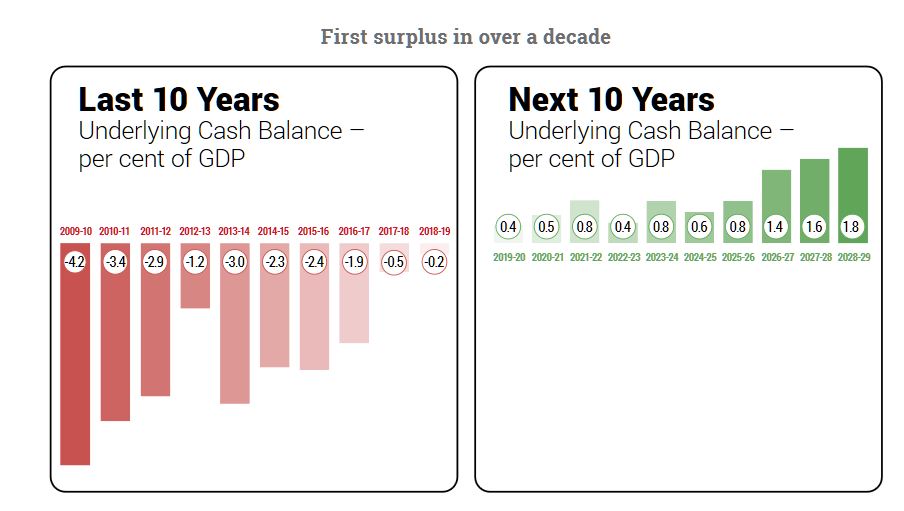

The Treasurer Josh Frydenberg has given his budget speech tonight, and he said that for the first time in 12 years the federal budget has returned to surplus.

His first budget includes billions of dollars for tax cuts, major road upgrades and health care. But actually, it is due to return to surplus in the NEXT financial year, and project small surpluses in subsequent years.

He is also spending big ahead of the election, so yes this is political (and in some regards intimating Labor’s policies in places) . This is a “boots and all” approach to try and gain election ground. Reminds me of Howard and Costello!

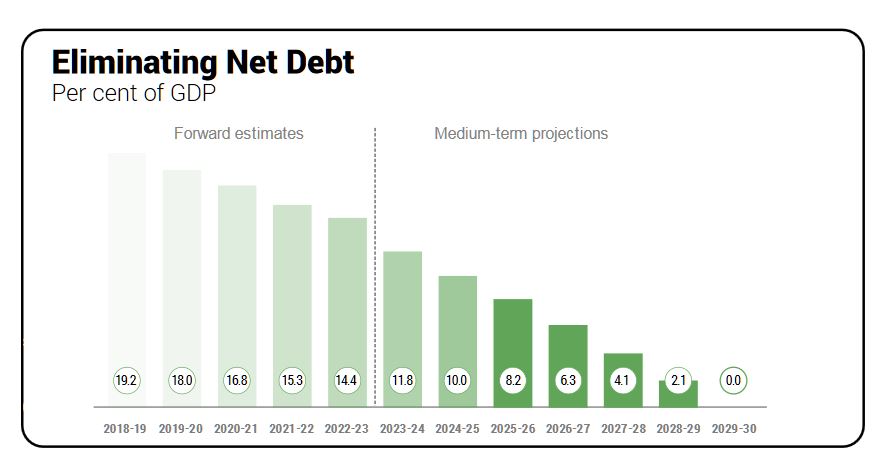

Net debt is forecast to be $360 billion next financial year, but the Coalition is promising to eliminate it by 2030 if it retains government (if the aggressive assumptions and no slow-down occurs in that time).

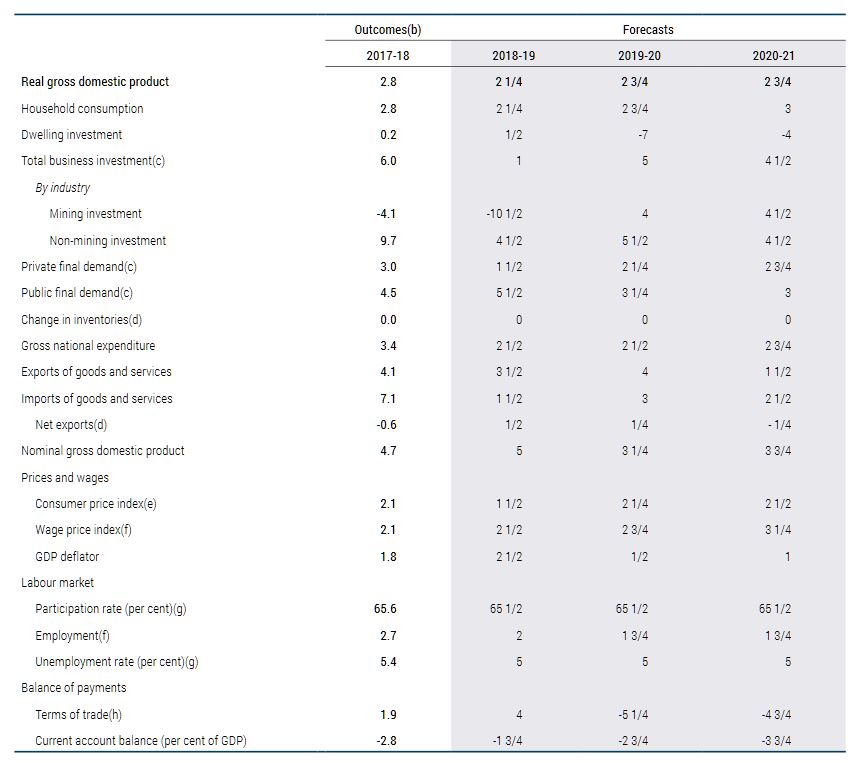

But it forecasts lower wages growth, then a jump back to higher rates (why?) and the same is true of economic growth at 2.75% next year, then higher later. Plus a promise for another 1.25 million jobs in the next 5 years (what type of jobs?).

“The budget is back in the black and Australia is back on track,” the treasurer said, announcing that the coalition delivered a $7.1 billion surplus

The Budget forecasts surpluses in each year over the forward estimates, reaching as high as $17.8 billion in 2012-22.

But the budget recognizes a number of risks locally and internationally and is under-funding the NDIS by $3 billion in the next two years.

“The residential housing market has cooled, credit growth has eased and we are yet to see the full impact of flood and drought on the economy.”

The mantra though the speech was that the budget would restore the nation’s finances without raising taxes.

“We are reducing the debt and this interest bill, not by higher taxes, but by good financial management and growing the economy.”

The truth is the budget may go into surplus next year thanks to very high iron ore export prices to China. This was lucky, and is explained by supply disruption from other sources lifting prices.

He makes the point that Australia has a significant national debt which is currently costing $18 billion, and this with interest rates ultra low!

Last year the coalition had announced plans to reduce income taxes for Australians by $144 billion. Now the Treasurer said the government would deliver more than $150 billion in income tax cuts.

From 1 July 2024 taxes will be reduced from 32.5 per cent to 30 per cent for those earning between $45,000 and $200,000.

“Taxes

will always be lower under the coalition,” Mr Frydenberg said, adding

that small businesses will also get tax relief from the 2019 budget.

“Small

business taxes have been reduced to 25 per cent and the instant asset

write-off will be increased from $25,000 to $30,000 and can be used

every time and asset under that amount is purchased.

“The instant asset write-off will also be expanded to businesses with a maximum turnover of $50 million.”

The coalition will also boost infrastructure spending to $100 billion over the next ten years.

Finally, the Government has matched Labor’s commitment to end a freeze on the Medicare rebate for GP visits from the first of July, as part of a $1.1 billion primary healthcare plan.

While the banks would hope the fall-out from the Royal Commission can now be contained, and business as usual can apply, it seems another Inquiry is on the cards down the track, further evidence of continued pressure on the sector.

Treasurer Josh Frydenberg has told the banks and regulators that they will face an inquiry down the track to ensure they have lifted their game post-royal commission; via InvestorDaily.

In a letter to the ABA, ASIC and APRA, Mr Frydenberg directed the organisations to implement Commissioner Kenneth Hayne’s recommendations from the final report directed at them.

The Treasurer sent out three letters to the heads of the organisations and made it clear that the government wanted to see lasting change within the sector.

“We will establish a follow-up independent inquiry, commencing in three years, to assess changes in industry practice and consumer outcomes since the royal commission,” said Mr Frydenberg.

Alongside implementing recommendations, Mr Frydenberg underlined the importance of ASIC changing its approach to enforcement, particularly shifting to a ‘why not litigate’ stance.

“I am aware that change is already underway, including through the establishment of the Office of Enforcement within ASIC, the move to a ‘why not litigate’ approach to enforcement and the introduction of initiatives such as close and continuous monitoring, to more intensively supervise the sector,” Mr Frydenberg wrote.

Mr Frydenberg committed to ASIC it’s continued support in providing new powers, expanding its role as a super regulator, removing barriers and strengthening penalty provisions.

“The government remains committed to ensuring that ASIC has the resources it needs, and will give further consideration to ASIC’s resourcing needs as part of the 2019–20 budget,” he said.

ASIC and ABA were also told by Mr Frydenberg to work together to create an enforceable banking code of conduct.

“I also expect the ABA to work co-operatively with ASIC to have the relevant provisions of the banking code approved as ‘enforceable code provisions’ as soon as practicable after legislation providing ASIC with these powers has been enacted,” he said.

In a letter to the ABA, the treasurer said he expected the banking code to be amended to support more inclusive practices, expand the definition of small business and eliminate default interest from being charged on loads declared to be impacted by natural disasters.

Mr Frydenberg told ABA chief executive Anna Blight that it was imperative that its members commit to putting customers at the heart of their business.

“I ask that you work with your members to take action and truly commit to restoring trust in the financial system. Only strong and decisive action of the kind that leads to lasting change, will ensure that the misconduct revealed by the royal commission is not repeated and that the public’s trust is regained,” he said.

Mr Frydenberg also called on APRA to strengthen its regulating and enforcement approach and prompted the authority to act on issues relating to the prudential standards, ADI responsibilities and supervision of regulated firms.

“It is my expectation that APRA will consider seriously the findings that the royal commission has made, echoed in the Productivity Commission’s superannuation inquiry, including whether its supervisory approach is appropriate for its mandate with regard to superannuation,” he said.

The Treasurer reiterated the governments support for the body and said it would give further powers and funding to the authority as needed.

The letters come as the opposition party has accused the government of not moving fast enough to implement Commissioner Hayne’s findings.

Labor had tried to force Parliament to hold extra sitting weeks to pass legislation the dealt with the royal commission recommendations but has been unable to get the support of the crossbench.

The office of the Treasurer has revealed that the final report will not be released on Friday.

According to the release, the Australian Government will still

receive the final report of the Royal Commission into Misconduct in the

Banking, Superannuation and Financial Services Industry on Friday 1

February 2019.

However, it will not be released publicly until 4.10pm on Monday, 4

February. Following its release, the Treasurer will hold a press

conference at Parliament House.

The interim report was released in September, when Treasurer Josh Frydenberg released the report the same day.

During his speech at the time he called the report “frank and scathing” and thanked the commissioner for his work.

He said the Royal Commission was announced last year because “the culture, conduct and the compliance of the sector is well below the standard the Australian people expect and deserve”.

The final report from the

financial services royal commission could be released later than

expected, after Treasurer Josh Frydenberg said government will “take

into account” its potential market impacts when determining when to

release it.

While Commissioner Hayne is

said to be “on track” to deliver the final report of the Royal

Commission into Misconduct in the Banking, Superannuation and Financial

Services Industry to the Governor-General by the agreed deadline of 1

February, there is still uncertainty as to whether the government will

release the final report next Friday.

Writing to the Treasurer, Chris Bowen MP said: “It

is in the national interest for the Australian people and victims of

banking scandals to be able to access the Hayne banking royal

commission’s final report and form their own views, at the earliest

opportunity, and that means on Friday, 1 February.

“I have written to the Treasurer

requesting the release of the final report and related documents of the

banking royal commission as soon as practicable after it is received by

the government.”

He continued: “The Liberal Party has

no excuses not to release the final report of the Hayne royal commission

when they receive it on 1 February.

“Josh Frydenberg released the royal commission’s interim report on the day they received it – and that was appropriate,” he noted.

“Refusing

to release the royal commission’s final report immediately would

unnecessarily politicise the handling of the report and give rise to

potential material market risks around leaks of all or part of the

report,” the Shadow Treasurer added.

The

Adviser asked the federal Treasurer when the final report from the

financial services royal commission would be publicly released.

In a statement, Mr Frydenberg said

that any public release of the report and its recommendations would

“take into account” its potential market ramifications.

Treasurer Josh Frydenberg said: “The

government looks forward to receiving Commissioner Hayne’s final report

by 1 February and considering its recommendations as we continue to

reform the financial sector.

“The government recognises the

potential market sensitivity of the final report and will take this into

account in considering the timing of its release.”

This could suggest that the

report may be released when the Australian Securities Exchange is

closed, for example, in order to protect the stock market.

If the report is released after

ASX trading hours, this would make the earliest release of the final

report approximately 4pm Sydney time on 1 February, if not later.

However, no particulars have been disclosed by government.

The federal Treasurer added: “One

wonders why Chris Bowen is so focused on the timing of the release of

the report given last time we released a major report, with the

Productivity Commission’s thousand page study into superannuation, he

effectively ruled out one of their key recommendations to reform the

default system 15 minutes after it was tabled and clearly before he had

even read it.”

Further, the Treasurer told an audience at The Sydney Institute on Tuesday (22 January) that the central tenet of the government’s eventual response to the final report would be “restoring trust in the financial system by delivering better consumer outcomes”.

He continued: “This

requires a culture of compliance and accountability, regulators that

are fit for purpose and an acknowledgement by the sector that people

must be put before profits. All of this must be achieved without

inadvertently strengthening the position of incumbents or unduly

restricting the flow of credit or other vital financial services that

Australians need and the economy relies on.

“In his interim report, Commissioner Hayne makes the telling

observation that “much more often than not, the conduct now condemned

was contrary to the law”. He makes clear that while behaviour was poor,

misconduct when revealed was insufficiently punished or not punished at

all.

“This raises the issue as to whether new laws are required or whether

existing laws simply need to be better enforced. Simplification may be,

according to the commissioner, a better route rather than adding ‘an

extra layer of legal complexity to an already complex regulatory

regime’,” Mr Frydenberg concluded.

As expected we are seeing the Government do “unnatural acts” to support the banking sector, in an attempt to alleviate the home price falls and lending freeze ahead of the election next year. The proposed $2 billion funding pool is small beer in the estimated $300 billion SME lending sector.

There is precedent a decade ago when the government’s $15 billion co-investment with the private sector into the residential mortgage-backed securities market during the GFC.

The federal government has announced a new, $2 billion Australian Business Securitisation Fund to help provide additional funding to small business lenders, via The Adviser.

In a joint statement, Treasurer Josh Frydenberg and the Minister for Small and Family Business, Skills and Vocational Education, Michaelia Cash, have announced that the Australian Business Securitisation Fund (ABSF) will “significantly enhance” the ability for small businesses to access funds by providing “significant additional funding to smaller banks and non-bank lenders to on-lend to small businesses on more competitive terms”.

The Australian Business Securitisation Fund will be administered by the Australian Office of Financial Management (AOFM), which was previously involved in the Residential Mortgage Backed Securities Market in 2008.

Speaking on Wednesday (14 November), the two ministers said: “Small businesses find it difficult to obtain finance other than on a secured basis – typically, against real estate. Small businesses that have already obtained finance secured against real estate, but wish to continue to grow, also find it difficult to access additional funding.

“Even when small businesses can access finance, funding costs are higher than they need to be.

“To overcome this and ensure that small businesses are able to fulfill their potential and continue to underpin economic growth and employment, the Australian Business Securitisation Fund will invest up to $2 billion in the securitisation market, providing significant additional funding to smaller banks and non-bank lenders to on-lend to small businesses on more competitive terms.”

The government has also reiterated that it will “encourage the establishment of an Australian Business Growth Fund to provide longer term equity funding”.

It is now in consultation with the prudential regulator (APRA) and several financial institutions in regard to the establishment of the fund, which could likely emulate overseas counterparts, such as the UK’s Business Growth Fund. This fund has reportedly invested around $2.7 billion in a range of sectors across the economy.

The ministers said: “Many small businesses find it difficult to attract passive equity investment which enables them to grow without taking on additional debt or giving up control of their business.

“A similar fund has not emerged in Australia, in part, as a result of the unfavourable treatment of equity for regulatory capital purposes.”

APRA has reportedly suggested that it is “willing to review these arrangements” to assist in facilitating the establishment of the Australian Business Growth Fund.

The government has said that it will host a series of meetings with stakeholders during the next sitting period in Canbera to “fast track” the establishment of the growth fund.

“With more than three million small businesses employing around seven million Australians, enhancing small business access to funding is part of the Coalition Government’s plan for a stronger economy,” the ministers said in a joint release.

Several players in the finance sector have welcomed the announcement, with NAB’s chief customer officer, business and private banking, Anthony Healy, saying that “the country’s largest business bank recognised that for Australia to continue to grow, SME businesses need better and easier access to capital”.

Mr Healy highlighted that NAB had been providing unsecured lending to small businesses through its QuickBiz channel, “helping SMEs borrow against the strength and cash flow of their business rather than physical bricks and mortar”.

He continued: “The Australian Business Growth Fund can help this further by providing a way in which SMEs can receive long term equity capital investments to grow their business, invest in new technology and create more jobs, which is why NAB is supportive of the concept.

“We do believe there is more that can be done to provide SMEs with access to equity capital, and we take confidence from the UK Business Growth Fund having operated successfully for several years.

“We look forward to further discussions with the federal government and other participants about the fund’s potential establishment soon,” said Mr Healy.

Likewise, Spotcap’s managing director, Lachlan Heussler, said: “Mr Frydenberg’s proposal meets a real financial need and is a win-win for both Australian small business owners and for the alternative lending industry in Australia.

“Without sustainable lending and affordable finance options, small and medium-sized businesses will struggle to grow, innovate and create more jobs for our economy.”

Mr Heussler continued: “Australia’s 2.2 million small and medium-sized businesses are the beating heart of our economy but are starved of working capital and under-served by traditional lenders who require security.

“By lowering borrowing costs, the proposed fund is a good step in increasing competition between the dominant, big lenders and online, unsecured lenders, such as Spotcap”.

The Council of Small Business Organisations Australia (COSBOA) likewise welcomed the news, with CEO Peter Strong stating: “We congratulate the hovernment, and the Treasurer Josh Frydenberg, on this decision. It’s a well needed game changer for financing of small businesses.”

Mr Strong said that securing access to affordable capital had become the “number one” challenge for small business owners in Australia, particularly as some banks had “relied solely on past earnings rather than taking future earnings potential into account”.

“As a result, if the business owner doesn’t have a house (or other major asset) to put on the line as security then they are stuck – and Australia misses out on the employment that can be generated by the future growth of these businesses,” he said.

Mr Strong continued: “Small business owners often tell me that the only time they can get a loan is when they no longer need it. Others have told me that they have had to travel overseas to get finance and, using the same business plan as they used in Australia, they get their loan. This was a crazy and damaging situation.”

Mr Strong continued: “It is by no means ‘free money’ but small businesses that are sound and have good growth potential will finally have access to affordable finance.”

Touching on the new growth fund, the COSBOA CEO stated: “Importantly, the Treasurer understands that the announcement would fail if the process of managing the funds is convoluted and complex.

“We, with others, have already been asked to join in designing the system to make sure it is fit for purpose and not made unfit by interference from those who don’t understand our sector. We look forward to working with the Morrison Government, the Treasurer, the Small Business and Family Enterprise Ombudsman and other stakeholders to make these two funds accessible for small business owners and start-ups.”