For those who do not know, a mugwump is “a bird who sits with its mug on one side of the fence and its wump on the other.”

That came to mind as I read the Treasury submission to the Royal Commission into Financial Services misconduct which was released recently on three matters:

the culture and governance of financial (and other) firms and the related regulatory framework;

the capability and effectiveness of the financial system regulators to identify and address misconduct; and

conflicts of interest arising from conflicted remuneration and integrated business models.

They say these three issues were drawn from the case studies to date that point to: numerous failures by firms to adhere to existing regulatory obligations and deal openly and honestly with the regulators; an indifference by a number of firms to delivering good consumer outcomes, as well as a lack of investment by some firms in systems and processes to monitor product performance and staff conduct; and at times an unsatisfactory attitude and approach to remediation where issues have been identified.

These outcomes reflect instances of failures of leadership, governance and accountability at an industry, firm and business unit level. Where misaligned incentives and conflicts of interest have been present, the underlying failings and the poor outcomes have been exacerbated.

Competitive forces have been unable to fully temper these problems and hold firms to account. In part this is due to the advantages of incumbency and continuing barriers to entry for new firms. It also reflects a lack of effective demand-side pressure. Consumers, when interacting with the financial system, face products and services that are inherently (or by design) complex, opaque and typically have long durations; conflicted advice can worsen the problem. With ineffective competition, profitability can remain high for financial firms even if consumer outcomes are poor. Their shareholders (both retail and institutional) can remain largely complacent about governance and culture, and consequently poor conduct can persist.

The evidence suggests that while financial system regulators have been alert to the problems and have taken action, they have not yet been able to change the underlying behaviours of many of the firms and industries involved.

In our view, the financial system and the regulatory framework cannot perform efficiently when there is a disregard by financial firms to adherence to the law and broader community standards and expectations regarding their trustworthiness. Fundamentally, responsibility for complying with the law rests with those to whom the obligations apply.

Turning the the Mugwump in Action.

They say that ASIC and APRA are world class regulators, and they were across the issues. The problem lies within the culture of the firms. And, by the way, the Council of Financial Regulators (of which Treasury is a member) is acting just fine. “At a structural level, Australia’s ‘twin peaks’ model of financial regulation – where responsibility for conduct and disclosure regulation lies with ASIC and responsibility for prudential regulation with APRA – has clearly served the financial system and economy well and remains appropriate. Similar architecture has been adopted in other jurisdictions and ASIC and APRA are well-regarded by peer-regulators in other countries and by international standard setting

bodies and organisations.

They do say it is clear that the current regulatory framework and its enforcement are not delivering satisfactory outcomes and that shareholders’ interests do not necessarily coincide with customers’ interests, particularly in the short-term; indeed much of the misconduct has generated significant returns to the firms that have flowed through to healthy dividends. But the problem is accountability in firms and the complexity of the law. Extending the BEAR, or a like regime, to a wider range of entities may be one way to lift standards of behaviour and conduct across the financial sector. But the fundamental limitation of such reform is that it relies on shareholders to agitate when remuneration policies do not serve consumer interests — and they may not do so.

But they also warn that over time, a financial system that is overburdened by regulation will fail to deliver on its objectives of meeting the financial needs of the community and facilitating a dynamic, stable and growing economy. Thus reforms to ensure consumer confidence through strong respected regulators must balance the efficiency and ability of the financial system as a whole to succeed.

With regards to conflicted remuneration, again they acknowledge that wrong incentives can lead to bad customer outcomes, yet fall short of supporting the idea of, for example, removing broker commissions and trails, warning darkly of unintended consequences.

All remuneration structures and business models can give rise to conflicts of interest, even if its form differs or the parties concerned vary. When markets function well, commercial practices evolve to best manage the multiplicity of interests and potential conflicts. Hence, overly prescriptive interventions —not taking account of all the trade-offs involved — can give rise to costs and unintended consequences.

Our judgment — subject to evidence in future hearings — is that recent structural changes in the industry, recently introduced or soon to be introduced reforms, other potential reforms the Commission could recommend, and heightened attention by firms and ASIC, should be sufficient to mitigate the systemic risks involved — subject to further ongoing scrutiny by regulators. Structural separation would also be complex and disruptive, and could have unintended consequences.

That said, There is clear evidence from the hearings and ASIC that vertically integrated firms have often not appropriately managed these conflicts, despite general legal obligations to do so.

Brokers are currently paid by lenders (via aggregators) using a standard commission model. This model includes upfront and trailing commissions which are proportional to the size of the loan, and subject to clawback arrangements which allow lenders to recover some or all of upfront commissions if a loan goes into significant arrears or is terminated within a specified period. These commissions have also been supplemented by volume and campaign-based bonuses, as well as non-monetary benefits that are predominately determined by volume targets. These features of the standard model give rise to conflicts of interest for brokers that could lead directly to poor consumer outcomes and reduce competition.

There is a risk that brokers working under vertically integrated aggregators may recommend specific in-house loan products that may not provide the best outcome for a consumer. Again, they are also suggestive of a potential negative effect on competition in the mortgage market at the expense of customers more generally.

Proposals for upfront, flat fees can involve up to three distinct changes to current industry practices:

a move away from remuneration set by reference to loan size, to one of a fixed dollar amount per loan (possibly still varying with loan or lender type or characteristics);

ending the practice of trail commissions; and

requiring the payment to be made by the consumer and not the lender.

The first of these would directly target the incentive to encourage customers to take out larger loans, though in practice the consequence of this incentive may be quite limited. It would create some other misaligned incentives that would also need to be managed, such as the need to limit the splitting of a loan into multiple loans to generate additional broker fees.

The industry argues that a larger loan size correlates with greater complexity and hence effort on the part of the broker. If this is correct, brokers could have an incentive under a flat fee to service only those customers with straightforward needs, disadvantaging those with more complex needs such as first home buyers. The correlation between loan size and broker effort is, however, not obvious and commissions can already vary according to product and lender characteristics and flat fees could also do so.

The second change, of removing trail commissions, would have the potential advantage of removing incentives for brokers to inappropriately recommend larger loans that take longer to pay back (though, again, how significant this incentive is in practice is unclear), and brokers would have greater incentives to assist customers to refinance.

The removal of trails would, however, also reduce incentives for brokers to guard against arranging non-performing loans and to not unnecessarily switch consumers to alternative loans that do not provide for a better deal. Refinancing is not a costless exercise, with real costs for both lenders and borrowers. In the United Kingdom, where trails are not used, concern over churn has led lenders to pay retention fees to brokers to encourage consumers not to switch lenders but refinance at a different rate.

Services provided by brokers to customers after a loan has been arranged could also be affected if trailing commissions were removed.

The third change, of requiring consumers rather than lenders to pay the broker, would be the most radical. Without any significant remuneration from lenders, brokers’ loan products and lender recommendations are more likely to align with the consumers’ best interests or be more transparent if they do not. Some specific payments from lenders to brokers may, however, need to be retained if they were to continue to provide specific services to the lender.

The standard commission structure represents a balancing of commercial interests and responsibilities between lenders, aggregators and brokers, as well as the interests of consumers. Too prescriptive and fixed a model risks being commercially inefficient, particularly as the market develops over time and technological and other innovations arise, and negatively affecting competition. While the online and technology based mortgage broker start-ups remain nascent, they are also innovating with remuneration structures (such as rebating commissions to customers) as a point of competitive advantage.

As brokers act as trusted advisers for customers with respect to housing finance, there is an in-principle case for introducing a positive duty on brokers to act in the interests of their customers. While responsible lending obligations provide protection against customers being recommended loans that are too large or otherwise not suitable for them, the purpose of a positive duty would be to counteract incentives to, for example, recommend a particular lender and loan type because the commission available to the broker is higher or because the loan is an in-house or white label product.

Applying a positive duty to brokers would not, however, necessarily be best achieved by attempting to replicate the financial advice best interests duty given differences between brokers and financial advisers, and the existence of responsible lending and other obligations. If it was to be introduced, careful consideration would again need to be given to an approach that mitigates conflicts of interest risks while avoiding unnecessary compliance costs, and to what extent it can rely on industry efforts or providing ASIC with some discretion or rule-making power.

Finally, with regard to employee incentives, the Treasury paper says that given the impending introduction of new powers for ASIC and the efforts of the banking industry to undertake significant reform itself, it is not clear that further regulatory interventions are merited at this stage. While the policy focus has traditionally been around remuneration, it is also relatively easy for firms to reward staff that are high-sellers (or to penalise poor-sellers) without resorting to a direct link to remuneration. As general obligations already exist to manage such conflicts, the broader issue raised is that of firm culture and governance.

S0, reading the submission, I felt the Treasury was firmly sitting on the fence, acknowledging the issues raised (they could do no other), but falling back to incremental changes, warning of unintended consequences, and pointing the figure at cultural bad practice in financial firms. The regulators escaped scot-free.

Frankly I found the submission all rather embarrassing… and rather missed the point!

According to the Treasury, the retirement phase of the superannuation system is currently under-developed and needs to be better aligned with the overall objective of the superannuation system of providing income in retirement to substitute or supplement the Age Pension. The Government is addressing this through the development of a retirement income framework.

The first stage in this framework is the introduction of a retirement income covenant in the Superannuation Industry (Supervision) Act 1993, which will require trustees to develop a retirement income strategy for their members. The covenant will codify the requirements and obligations for superannuation trustees to consider the retirement income needs of their members, expanding individuals’ choice of retirement income products and improving standards of living in retirement.

They have published a position paper which outlines the principles the Government proposes to implement in the covenant and supporting regulatory structures. Consultations close 15 June 2018.

The retirement income framework

The retirement phase of the superannuation system is currently under-developed and needs to be better aligned with the overall objective of the superannuation system of providing income in retirement to substitute or supplement the Age Pension. The Government is addressing this through the development of a retirement income framework. The framework is intended to:

enable individuals to increase their standard of living in retirement through increased availability and take-up of products that more efficiently manage longevity risk, and in doing so increase the efficiency of the superannuation system and better align the system with its objective; and

enable trustees to provide individuals with an easier transition into retirement by offering retirement income products that balance competing objectives of high income, flexibility and risk management.

In December 2016, a discussion paper on Comprehensive Income Products for Retirement (CIPRs) was released for consultation[1]. Submissions closed on 7 July 2017. The Department of the Treasury (Treasury) received 57 written submissions on the discussion paper, and met with more than 100 organisations.

That consultation revealed that there is broad agreement on the importance of what the CIPRs policy is seeking to achieve, but divergent views on the best way to achieve the objectives.

In addition, some stakeholders stressed the importance of finalising the social security treatment of pooled lifetime income products first. The Government announced the treatment of the social security means test rules for new and existing pooled lifetime income products in the 2018‑19 Budget.

Having taken steps to remove barriers to the introduction of pooled lifetime income products, the Government plans to prioritise progress on the development of a retirement income covenant.

The Government has also announced it will progress the development of simplified, standardised metrics in product disclosure to help consumers make decisions about the most appropriate retirement income product for them. Other elements of the framework will be developed progressively:

reframing superannuation balances in terms of the retirement income stream they can provide, by facilitating trustees to provide retirement income projections during the accumulation phase; and

a regulatory framework to support the other elements of the retirement income framework including definitions, any necessary safe harbours, requirements for managing legacy products and other details.

Retirement income covenant

On 19 February 2018 the Minister for Revenue and Financial Services, the Hon Kelly O’Dwyer MP, announced the establishment of a consumer and industry advisory group to assist in the development of a framework for CIPRs.

The central task of the advisory group was to provide advice to Treasury on possible options and scope of a retirement income covenant in the Superannuation Industry (Supervision) Act 1993 (SIS Act). The group strongly supported the idea of a retirement income covenant and provided advice on the proposed framework. This feedback has helped shape the proposed approach set out in this paper.

As part of the Government’s More Choices for a Longer Life Package in the 2018-19 Budget, the Government has committed to introducing a retirement income covenant as a critical first stage to the Government’s proposed retirement income framework. This will codify the requirements and obligations for superannuation trustees to improve retirement outcomes for individuals.

Existing covenants in the SIS Act include obligations to formulate, review regularly and give effect to investment, risk management and insurance strategies; but not a retirement income strategy.

Introducing a retirement income covenant will require trustees to consider the retirement income needs and preferences of their members. It will ensure that Australian retirees have greater choice in how they take their superannuation benefits in retirement. This should allow retirees to more effectively choose a retirement product that aligns with their preferences, improving outcomes in retirement. The proposed obligations for inclusion in the covenant are outlined in the section ‘Covenant principles’.

The covenant will be supported by regulations to provide additional guidance and outline in more detail how trustees will be required to fulfil their obligations. Appropriate enforcement will also be part of the framework. The ‘Supporting principles’ section outlines the principles and guidelines that would be included in regulations (and possibly prudential standards). Implementation of these regulations may require adjustments to existing regulations and instruments.

Finally, additional principles have been identified that may be appropriate for inclusion in the retirement income framework, but which are not being fully developed at this time. These principles will form part of the regulatory framework to be progressed at a later date.

The covenant and supporting principles would apply to trustees of all types of funds except Australian eligible rollover funds (ERFs) and defined benefit (DB) schemes that offer a DB lifetime pension. The Government considers that it would not be appropriate to require trustees of these fund types to develop a retirement income strategy because ERFs do not have any members in retirement and a DB lifetime pension already reflects an implicit retirement income strategy.

While all members of the advisory group provided valuable input and insights which have helped inform this position paper, the positions expressed in this paper are those of the Government.

The retirement income framework, including the covenant, will be implemented with an appropriate transition period to allow sufficient time for industry to adjust. The Government proposes to legislate the covenant by 1 July 2019 but to delay commencement until 1 July 2020. This timing would allow the market for pooled lifetime income products to develop in response to the changes to the Age Pension means test arrangements announced as part of the 2018-19 Budget and for other elements of the framework to be settled.

[1] Treasury, Development of the framework for Comprehensive Income Products for Retirement, Canberra, 2016.

On 9 May 2018, the Government agreed to the recommendations of the Review, both for the framework of the overarching Consumer Data Right and for the application of the right to Open Banking, with a phased implementation from July 2019.

The Government will phase in Open Banking with all major banks making data available on credit and debit card, deposit and transaction accounts by 1 July 2019 and mortgages by 1 February 2020.

Data on all products recommended by the Review will be available by 1 July 2020. All remaining banks will be required to implement Open Banking with a 12-month delay on timelines compared to the major banks. The Australian Competition and Consumer Commission (ACCC) will be empowered to adjust timeframes if necessary.

The Treasury will be consulting on draft legislation, the ACCC will be consulting on draft rules, and Data61 will be consulting on technical standards over the coming months.

From The Budget

The government has unveiled its 2018-19 federal budget, which revealed plans to support an open banking framework; the acceleration of the GovPass program; exploring the use of blockchain for government; and the promotion of the industry.

The government will pledge $44.6 million across four years from 2018-19 for the creation of a “national consumer data right”.

The CDR will help “consumers and small to medium enterprises to access and transfer their data between service providers in designated sectors,” the budget papers said.

Over four years, the $44.6 million – which also includes $1.4 million in capital funding in 2018-19 – will be split across three government agencies:

The Australian Competition and Consumer Commission (ACCC) will receive $19.6 million;

CSIRO will receive $11.6 million; and

The Office of the Australian Information Commissioner (OAIC) will receive $12.1 million.

A fact sheet from industry body FinTech Association said the ACCC’s role would be to “oversee sectors that will be subject to the CDR”.

Meanwhile, CSIRO would set data standards, with the funds going into innovation centre Data 61; and the OAIC will “assess the privacy impact” of the CDR.

Credit card providers will be forced to scrap unfair and predatory practices – after the legislation passed through the parliament on Thursday. However, the implementation timetable is extended into 2019. It also included a package of other measures.

The reforms include:

Requiring affordability assessments be based on a consumer’s ability to repay the credit limit within a reasonable period (from July 2018). This tightens responsible lending obligations for credit card contracts.

Banning unsolicited offers of credit limit increases (from January 2019). At the moment, whilst the law forbids providers from making these sorts of offers in writing, offers can be made by phone and other mediums. This loophole has been exploited, but will now be closed.

Simplifying how credit card interest is calculated, especially, banning the practice of backdating interest rate charges. Currently, some providers were attracting new customers with promotional low rate, or no rate offers, say for the first month. But, if a customer failed to pay off in full a credit card bill after the first month, the credit card company was often retrospectively applying the new interest rate to previous purchases. This was allowed in the banks’ small print, but the government said the practice did “not align with consumers’ understanding and expectation about how interest is to be charged”. This will be banned, from next year.

Requiring credit card providers to have online options to cancel cards or to reduce credit limits (from January 2019). At the moment, some card providers force customers to come into a bank branch to reduce limits or terminate cards, and when they did come in were often persuaded not to do it. The asymmetry between fast credit card approvals online, and slow cancellation will end.

The Treasurer said:

This legislation will protect vulnerable Australians from predatory behaviour which seeks to make a quick buck from people’s misfortune, and compound their financial hardship. This is the first phase of reforms outlined in the Government’s response to the Senate Inquiry into the credit card market, which seeks to put more power in the hands of consumers.

The Bill will also materially boost competition in the banking sector by allowing small lenders to call themselves banks; a significant change that will entice new lenders and challenger banks to enter the market. This will provide greater choice for Australians and put downward pressure on the cost of banking products and loans.

In lifting the ban on the use of the word ‘bank’, any lender with an ADI licence will now be able to market themselves as a bank, whether they have bricks and mortar branches or operate exclusively online. Off the bat, this reform paves the way for more than 60 current Australian lenders and credit unions to call themselves banks.

The Bill – the Treasury Laws Amendment (Banking Measures No. 1) 2017 – also strengthens financial stability by providing the Australian Prudential Regulation Authority (APRA) a new reserve power over the lending activities of non-banks. It modernises APRA’s legislative framework by making clear APRA’s roles and responsibilities under the Banking Act 1959.

This Bill accompanies the Turnbull Government’s Banking Executive Accountability Regime, which brings greater accountability to our banks by introducing tough new rules for banks and their executives, and the Crisis Management Bill, which strengthens APRA’s crisis management powers.

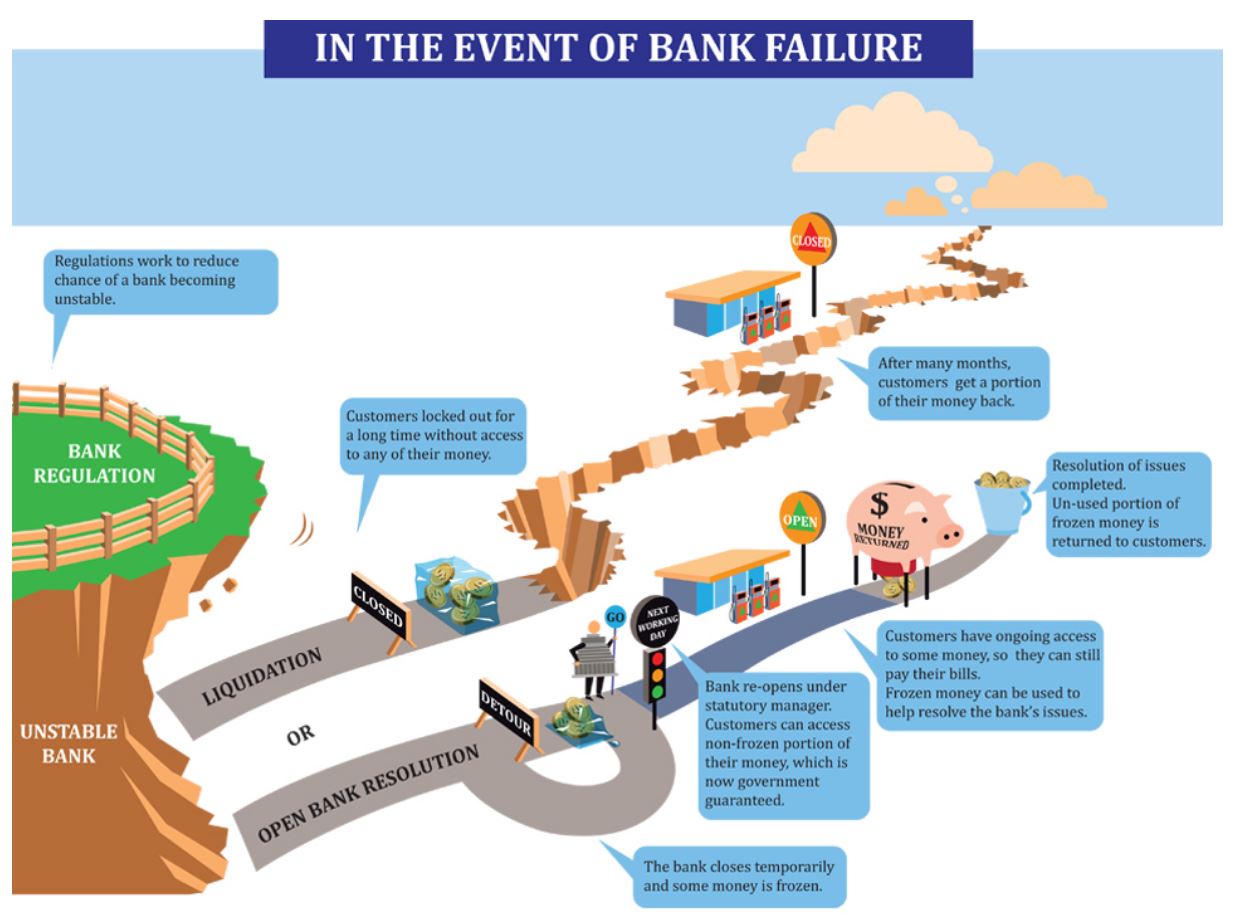

There were several well publicised Government bail-out’s of banks which got into problems after the GFC. For example, the UK’s Royal Bank of Scotland was nationalised. This costs tax payers dear, so there were measures put in place to try to manage a more orderly transition when a bank gets into difficulty.

In October 2011, the Financial Stability Board (FSB) issued its Key Attributes of Effective Resolution Regimes for Financial Institutions (Key Attributes). These Key Attributes set out the ‘core elements that the FSB considers to be necessary for an effective resolution regime. There followed legislation in a number of jurisdictions.

But note the chilling words “the bank closes temporarily and some money is frozen. Bank re-opens under statutory manager. Customers can access non-frozen portion of their money, which is now Government protected. Frozen money can be used to help resolve the bank’s issues. Resolution of issues completed. Un-used portion of frozen money is returned to customers”.

Or in other words, customers money, held as savings in the bank are able to be grabbed to assist in the resolution. This is of course what happened to people with bank deposits in Cyprus a few years back.

The thinking behind it is simple. Banks need an exit strategy in case of a problem, and Government bail-outs should not be an option. So a manager can be appointed to manage through the crisis. They can use bank capital, other instruments, like hybrid bonds and deposits to create a bail-in. This approach to rescuing a financial institution on the brink of failure makes its creditors and depositors take a loss on their holdings. This is the opposite of a bail-out, which involves the rescue of a financial institution by external parties, typically governments using taxpayers money.

So, given the New Zealand position (and the tight relationship between banking regulators in Australia and New Zealand), we should look at the position in Australia. Are deposit funds in Australia likely to be “bailed-in”?

It all centered on the powers which were to be given to APRA to deal with a banking collapse. “The bill seeks to strengthen the powers of the Australian Prudential Regulation Authority (APRA) to facilitate the orderly resolution of an authorised deposit-taking institution (ADI) or insurer so as to protect the interests of depositors and policyholders, and to protect the stability of the financial system in case of crisis”. The Treasurer had argued that by “affording APRA the power to work with ADIs and insurers in order to plan for economic stress events, the cost to the taxpayer will be significantly

reduced in the event of a financial crisis”.

The Senate review and consultation elicited a significant number of submissions, and they made two main points in opposition to the bill: firstly, they believed that this bill gives APRA the power to ‘bail-in’ depositors’ savings to stabilise a failing financial institution; secondly, in place of the bill, the Australian Parliament should legislate a Glass-Steagall style separation of the banks.

Specifically, Dr Wilson Sy, a former analyst with APRA, considered that the bill was not clear enough on the topic of depositors’ savings. Dr Sy suggested that deposit protection is to be balanced against financial system stability, without the law clearly stating which has higher priority’. Dr Sy claimed that the bill is ‘designed to confiscate bank deposits to ‘bail-in’ insolvent banks to save the financial system.

It came down to the meaning of “any other instrument” in the draft bill. Treasury said, “the use of the word ‘instrument’ in paragraph (b) is intended to be wide enough to capture any type of security or debt instrument that could be included within the capital framework in the future. It is not the intention that a bank deposit would be an ‘instrument’ for these purposes”. Treasury confirmed that because deposits are not classified as capital instruments, and do not include terms that allow for their conversion or write-off, they cannot be ‘bailed-in’.

The committee concluded:

The committee believes that the protection of depositors’ interests is paramount and does not consider that the bill would allow the ‘bail-in’ of Australians’ savings and deposits. The stability of the financial system depends on its depositors having confidence in its financial institutions. By ensuring the security of depositors’ savings, the overall protection of the financial system can be ensured.

But there are a few questions to consider.

Why not expressly exclude deposits from the bill, the current vague wording appears to leave the door open for a deposit grab in case of financial instability? We may have some reassuring words from the regulators, but is it enough?

How does this fit with the NZ model, where deposits can be targeted, especially, as the regulators in the two countries are closely aligned, and in fact most banking in New Zealand is provided by Australian Bankers. In case of failure would customers of a bank operating in both countries be different?

And two wider questions.

The NZ model expressly says depositors should weight up the risks of placing money with specific lenders but can savers really do this?

The issue of hybrid bonds needs more careful consideration, in that in Australia (unlike some other countries) these bonds have been sold to retail investors, people looking to savings with good returns, and who probably do not understand the bail-in risks they may face. So even if deposits are excluded there is a risk that investors in hybrids will get a nasty shock.

Seems to me this is a messy area, and I for one cannot be 100% convinced savings will never be bailed-in. And that’s a worry!

I recall the Productivity Commission comment last week, that financial stability had taken prime place compared with competition (and so customer value) in financial services. The issue of bail-in of deposits appears to be shaping the same way.

Treasurer Morrison has release the report by King & Wood Mallesons partner Scott Farrell today in to open banking which aims to give consumers greater access to, and control over, their data. It mirrors recent UK developments, and is another nail in the competitive advantage the large players currently have. Later the scheme could be widened to other industry sectors, such as energy or telecommunications.

This “open banking” regime mean that customers, including small businesses, can opt to instruct their bank to send data to a competitor, so it can be used to price or offer an alternative product or service.

The report recommends that the open banking regime should apply to all banks, though with the major banks to join it first. For non-banks and fintechs, the report wants a “graduated, risk-based accreditation standard”. Superannuation funds and insurers are not included for now.

In fact, all authorised deposit-taking institutions (ADIs) will automatically be accredited to receive data.

There are exclusions. For example, value added data which is created by banks as a result of their analysis will not be included in the regime. Know your customer data though should be sharable. De-identified aggregate data would not be sharable.

Data provided under the regime will initially be “read only”, but the successful adoption of open banking “could also lead to ‘write access’ reforms” in the future. The following products are called out as in scope.

Transfer of data should be made free of charge, the report says.

Safeguards will be important, including under the Privacy Act, and a customer’s consent under Open Banking must be explicit, fully informed and able to be permitted or constrained according to the customer’s instructions. Joint accounts will need some special considerations in terms of authority, and advice.

An appropriate data standard will need to be agreed, and a clear and comprehensive framework for the allocation of liability between participants in Open Banking should be implemented. This framework should make it clear that participants in Open Banking are liable for their own conduct, but not the conduct of other participants. To the extent possible, the liability framework should be consistent with existing legal frameworks to ensure that there is no uncertainty about the rights of customers or liability of data holders.

In terms of implementation, data holders should be required to allow customers to share information with eligible parties via a dedicated application programming interface, not screen scraping.

The starting point for the Standards for the data transfer mechanism should be the UK Open Banking technical specification.

A period of approximately 12 months between the announcement of a final Government decision on Open Banking and the Commencement Date should be allowed for implementation. From theCommencement Date, the four major Australian banks should be obliged tocomply with a direction to share data under Open Banking. The remaining AuthorisedDeposit-taking Institutions should be obliged to share data from 12 months after the

Commencement Date, unless the ACCC determines that a later date is more appropriate.

The ACCC as lead regulator should coordinate the development and implementation of a timely consumer education programme for Open Banking. Participants, industry groups and consumer advocacy groups should lead and participate, as appropriate, in consumer awareness and education activities.

The ABA welcomed the report:

Banks are excited to enter the Open Banking age that will spark new innovations and deliver cutting edge products, with customers the big winner.

The Farrell Report into Open Banking released by the Treasurer today recognises both the opportunities and challenges that data sharing will bring. While the Australian Bankers’ Association has some concerns surrounding the implementation, the report lays out a broadly sensible path to Open Banking. Mr Farrell’s report should be commended for its focus on customers and its commitment to work with stakeholders to design a safe and secure data sharing framework.

Giving customers greater access to their own data will boost choice in banking and further simplify the application process for a financial product.

Australians have one of the most innovative and technologically advanced banking systems in the world. Examples of this is 24-hour banking, payWave and the soon to be launched PayID and New Payments Platform.

As the Productivity Commission affirmed this week, Australian banks are at the forefront of global innovation which has delivered a superior customer experience. Investments in how banks use data are already leading to new innovations that are improving the customer experience and this is set to continue under Open Banking.

A reform as large as Open Banking must be carefully considered and properly implemented.

Research shows that Australians trust their banks with personal information, more than online retailers, social media companies and even governments. It’s important that banks maintain this trust and ensure that the open data reforms don’t place personal information at risk.

Banks will continue to work with stakeholders like consumer groups, FinTech’s, regulators and government to get this right so it is a good model for all industries and customers are protected.

The ABA looks forward to carefully analysing Mr Farrell’s report and working with members and stakeholders to address any challenges to ensure its success. Banks would also like to thank Mr Farrell for his thorough and thoughtful inquiry

The Treasury has released draft legislation to require the big four banks to participate fully in the credit reporting system by 1 July 2018. They say this measure will give lenders access to a deeper, richer set of data enabling them to better assess a borrower’s true credit position and their ability to pay a loan.

We note that there is no explicit consumer protection in this bill, relating to potential inaccuracies of data going into a credit record. This is, in our view a significant gap, especially as the proposed bulk uploading will require large volumes of data to be transferred.

It does however smaller lenders to access information which up to now they could not, so creating a more level playing field. Consumers may benefit, but they should also beware of the implications of the proposals.

The Government is seeking views on the exposure draft legislation and accompanying explanatory materials, which implements this measure. Closing date for submissions: 23 February 2018

The Bill amends the Credit Act to mandate a comprehensive credit reporting regime such that from 1 July 2018 large ADIs and their subsidiaries must provide comprehensive credit information on open and active consumer credit accounts to certain credit reporting bodies. It also expands ASIC’s powers so it can monitor compliance with the mandatory regime. The Bill also imposes requirements on the location where a credit reporting body must store data.

Since March 2014, the Privacy Act has allowed credit providers and credit reporting bodies to use and disclose ‘positive credit information’ or ‘comprehensive credit information’ about a consumer.

This includes information about the number of credit accounts a person holds, the maximum amount of credit available to a person and repayment history information.

Prior to March 2014, the information that could be shared was limited to ‘negative information’. This includes details of a person’s overdue payments, defaults, bankruptcy or court judgments against that person.

However, the Privacy Act does not mandate the disclosure of comprehensive credit information by credit providers to credit reporting bodies.

The 2014 Murray Inquiry and the Productivity Commission Inquiry into Data Availability and Use recommended that the Government mandate comprehensive credit reporting in the absence of voluntary participation. Comprehensive credit reporting is expected to enable credit providers to better establish a consumer’s credit worthiness and lead to a more competitive and efficient credit market.

In the 2017-18 Budget, the Government committed to mandating a comprehensive credit reporting regime if credit providers did not meet a threshold of 40 per cent of data reporting by the end of 2017.

On 2 November 2017 the Treasurer announced that he would introduce legislation for a mandatory regime as it was clear the 40 per cent target would not be met.

The Bill amends the Credit Act to establish a mandatory comprehensive credit reporting regime which will apply from 1 July 2018. The amendments do not require or allow disclosure, use or collection of credit information beyond what is already permitted under the Privacy Act and Privacy Code.

Currently, Australia’s credit reporting system is characterised by an information asymmetry. A consumer has more information about his or her credit risk than the credit provider. This can result in mis-pricing and mis-allocation of credit.

The Bill seeks to correct this information asymmetry. It lets credit providers obtain a comprehensive view of a consumer’s financial situation, enabling a provider to better meet its responsible lending obligations and price credit according to a consumer’s credit history.

The Government expects that the mandatory regime will also benefit consumers. Consumers will have better access to consumer credit, with reliable individuals able to seek more competitive rates when purchasing credit. Consumers that are looking to enter the housing market will be better able to demonstrate their credit worthiness. Consumers that possess a poor credit rating will also be able demonstrate their credit worthiness through future consistency and reliability.

The mandatory regime applies to ‘eligible licensees’ which initially will be large ADIs and their subsidiaries that hold an Australian credit licence. An ADI is considered large where its total resident assets are greater than $100 billion. Other credit providers will be subject to the regime if they are prescribed in regulations.

Eligible licensees are required to supply credit information on 50 per cent of their active and open credit accounts by 28 September 2018. The information on the remaining open and active credit accounts, including those that open after 1 July 2018, will need to be supplied by 28 September 2019.

The bulk supply of information must be given to all credit reporting bodies the eligible licensee had a contract with on 2 November 2017. In this way the credit provider has an established relationship with the credit reporting body and will have an agreement in place on the handling of data to ensure it remains confidential and secure.

Following the bulk supply of information, large ADIs and their affected subsidiaries must, on a monthly basis, keep the information supplied accurate and up-to-date, including by supplying information on accounts that have subsequently opened. This information must be supplied to credit reporting bodies the credit provider continues to have a contract with.

Credit providers that are not subject to the mandatory regime will be able to access credit information supplied under the regime by voluntarily supplying comprehensive credit information to a credit reporting body or becoming a signatory to the PRDE.

The security and privacy of a consumer’s credit information will be preserved and protected. The Bill relies on the existing protections established by the Privacy Act and Privacy Code and the oversight of the Australian Information Commissioner. The Bill also places a new obligation on credit reporting bodies on where data is stored. In addition, the Bill places an obligation on credit providers to be satisfied with the security arrangements of the CRBs prior to supplying information.

ASIC will be responsible for monitoring compliance with the mandatory regime. It has new powers to collect information and require audits to confirm the supply requirements are being met. ASIC will also have the ability to expand the content to be supplied under the mandatory regime and prescribe the technical standards for the format of the information.

The Treasurer will also receive statements from large ADIs, their affected subsidiaries and credit reporting bodies to demonstrate that the initial bulk supply requirements, as well as the ongoing supply requirements, have been met.

The mandatory comprehensive credit regime, implemented by this Bill, recognises that industry stakeholders have already taken a number of steps to support sharing comprehensive credit information. This includes the PRDE and supporting ARCA Technical Standards.

The mandatory regime includes the ‘principles of reciprocity’ and the ‘consistency principle’ that have been developed by industry. To the extent possible, the mandatory comprehensive credit reporting regime operates within the established industry framework but also provides scope for future technological developments.

An independent review of the mandatory regime must be completed by 1 January 2022. The review will table its report in Parliament.

Labor MPs might be rubbing their hands together with glee at a Treasury memo that shows the federal opposition’s negative gearing policy will have a “small” impact on the property market. But insights from behavioural public policy, as highlighted by the 2017 Economics Nobel laureate – Richard Thaler and his colleague Cass Sunstein, tell us that how people respond to this policy will be more about how the government frames it.

The Treasury memo showed the Labor policy of limiting negative gearing to existing homeowners will have a limited impact as the changes are unlikely to encourage investors to sell quickly. Also, owner-occupiers dominate the housing market and the costs of selling are high.

However, this assumes that people are forward-looking, well-informed, good with numbers and perfectly responsive to new information. Behavioural economics shows us that people do not always think so deeply and logically about their choices.

How any changes to negative gearing are sold to us – as a loss or gain, as a one-off or ongoing, in terms of short versus long term costs and benefits – will impact how Australians react.

Most of us aren’t whizzes with mathematics. As Nobel prize winner Herbert Simon has shown, in place of complex mathematical algorithms we use heuristics. These are simple rules of thumb that draw on our intuitions, experience and gut feel.

Heuristics and biases

One common example of a heuristic is the availability heuristic. This is when we make decisions based on easily available information such as recent events and highly emotive experiences. Our brains work better with narratives and stories than with facts and figures.

Nobel economics laureates George Akerlof and Robert Shiller have applied a similar insight to analyse people’s perceptions of housing market fluctuations. They noted that we hear lots of stories about how house prices are on an upward trend. Via the availability heuristic, we easily remember these emotionally engaging stories, much better than we can remember the dry facts about the history of house price instability and housing market crashes.

This leads us to overestimate the chances of continuing house price rises, and to underestimate the chances of a fall, driving unsustainable house price increases – as witnessed, for example, in the American sub-prime property markets before the global financial crisis.

While heuristics can help us to decide quickly, they sometimes lead us into systematic mistakes – “behavioural biases”. This does not mean that we’re all hopelessly irrational. But for negative gearing it matters how a potential change is framed, and how that fits into our heuristics and biases.

Most economists (including those at Treasury) assume that one dollar is a perfect substitute for any other dollar. Whether we save A$100 via a tax break, win A$100 from a scratch card or earn A$100 from working overtime, it makes no difference.

Contrary to this view, behavioural economics has shown that the way we treat money is different depending on the contexts in which we earn and spend it. We have different “mental accounts” for consumption, wealth, regular income and windfalls. We are more likely to splurge money we’ve won from a scratch card than money we’ve earnt doing overtime.

This is another reason why framing is important. How the government frames a negative gearing change will determine the mental account to which we assign it, and therefore how we respond.

If negative gearing changes are considered a one-off hit – the opposite of a scratch card windfall – then property owners won’t worry so much. On the other hand, if the change to negative gearing is seen as an ongoing drain on our incomes, then they will worry a lot.

Another factor that will come into play is loss aversion – people are much more likely to worry about losses than gains. Evidence from behavioural experiments shows that home-owners over-estimate the value of their properties. This makes them reluctant to sell at reduced prices in a falling market.

It also means that Australians will resist negative gearing changes if these are framed as a loss, creating political pressures for a policy u-turn. It is difficult to predict how people might respond, but behavioural economics shows that any ructions might be avoided if the negative gearing change is framed as a gain.

For instance, Treasury predicts that the additional revenue raised from restricting negative gearing could be up to A$3.9 billion. Therefore, the negative gearing changes could cover more than 80% of federal government expenditure on veterans and their families.

In the long and short term

Treasury’s modelling notes there might be downward pressure on house prices in the short term from changing negative gearing, but that this will be small overall.

But a range of models and experiments have shown that people are disproportionately focused on tangible, short-term outcomes. For example, most of us find it hard to persuade ourselves to go the gym: the short-term costs are inconvenience and discomfort and the benefits seem intangible and distant. This is called “present bias”.

Recent work in behavioural economics confirms that framing (alongside a range of other socio-psychological influences) has a strong impact on our choices. Framing will determine how we perceive the policy, which mental account we will use to process it and how the various heuristics and biases identified by economics and psychologists will play out.

In the debates around negative gearing policy changes, these behavioural insights have not been highlighted. So perhaps Treasury could have added some psychology, alongside the economics, in arguing that house price falls are likely to be limited.

Author: Michelle Baddeley , Research Professor at the Institute for Choice, University of South Australia