The latest UBS study, the fifth in their series looking at lending standards, and based on a survey of around 900 home loan applicants reveals that (perhaps surprisingly) there was a rise in “porkys” being told as part of the mortgage application, despite the Banking Royal Commission.

As a result, more than a third of Australian home loans could have ‘liar loans’ based on inaccurate information.

UBS Analyst Jonathan Mott said:

While asking detailed questions appears to be prudent, it does not appear to be effective as many factually inaccurate mortgages are still working their way through the process.

Of the borrowers who said their application was not completely factual in the past year, 20 per cent overstated their income, 23 per cent understated debts, 34 per cent understated their living costs, and 23 per cent misstated multiple categories.

Now, this is consistent with the DFA surveys where true incomes and costs are often higher than might be expected. And the extra granularity now required by the banks (many categories of costs, more detail on incomes etc) can create a false sense of accuracy – especially when many households are making best guesses to provide information to support their applications.

And financial intermediaries still appear to be part of the story, with a higher percentage of borrowers who misstated information on applications through a mortgage broker (40 per cent) than through the banks (27 per cent).

UBS said that a “large number” of survey respondents indicated their mortgage consultant advised them to misrepresent elements of their application.

At a time when the mortgage growth stops are being pulled, and lower rates are expected in a highly competitive market, this will simply create a bigger bust later.

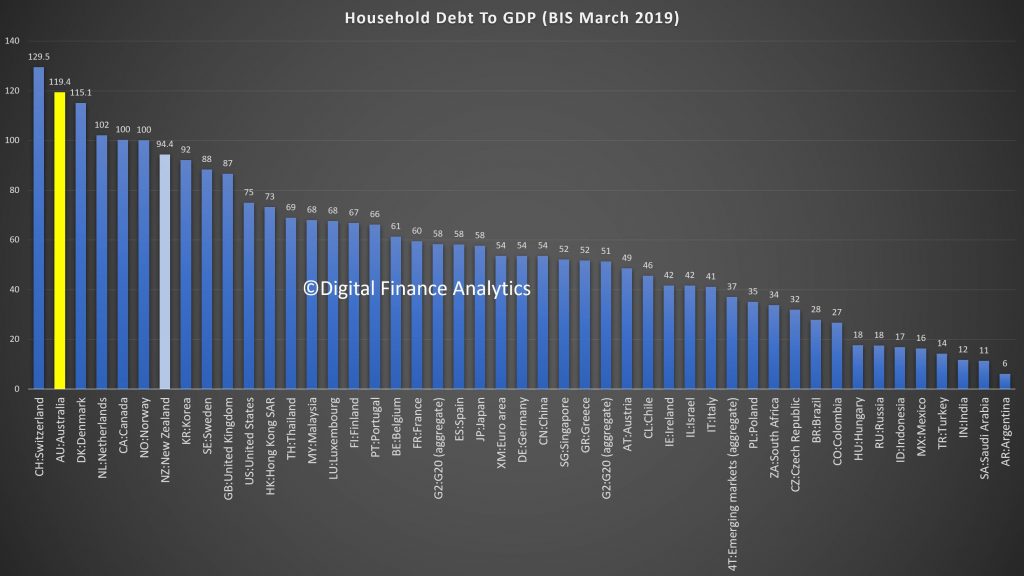

And remember that on an international basis, we are right at the top of the international benchmarks in terms of household debt.

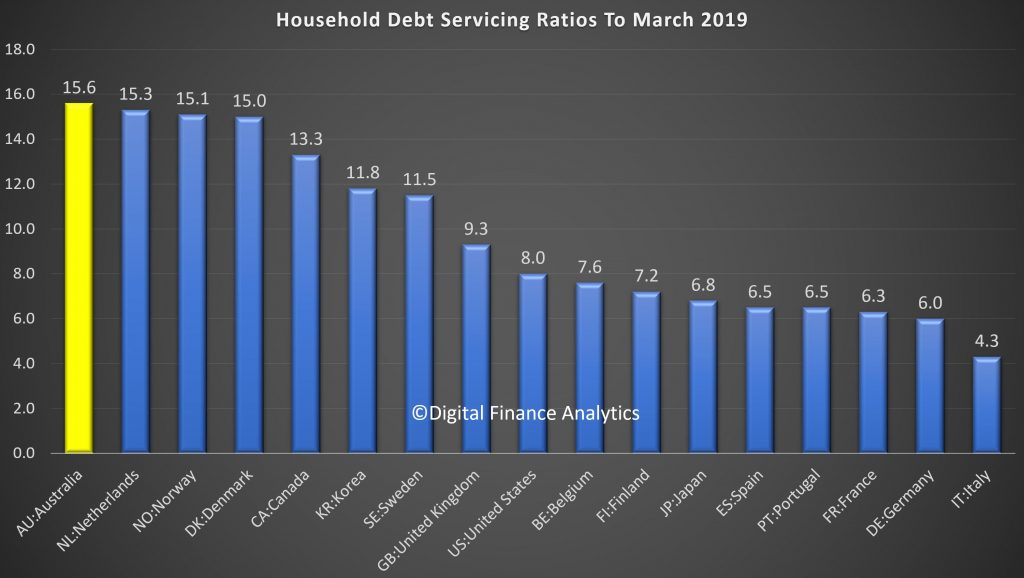

In fact according to the latest BIS data we lead in terms of debt servicing ratios.

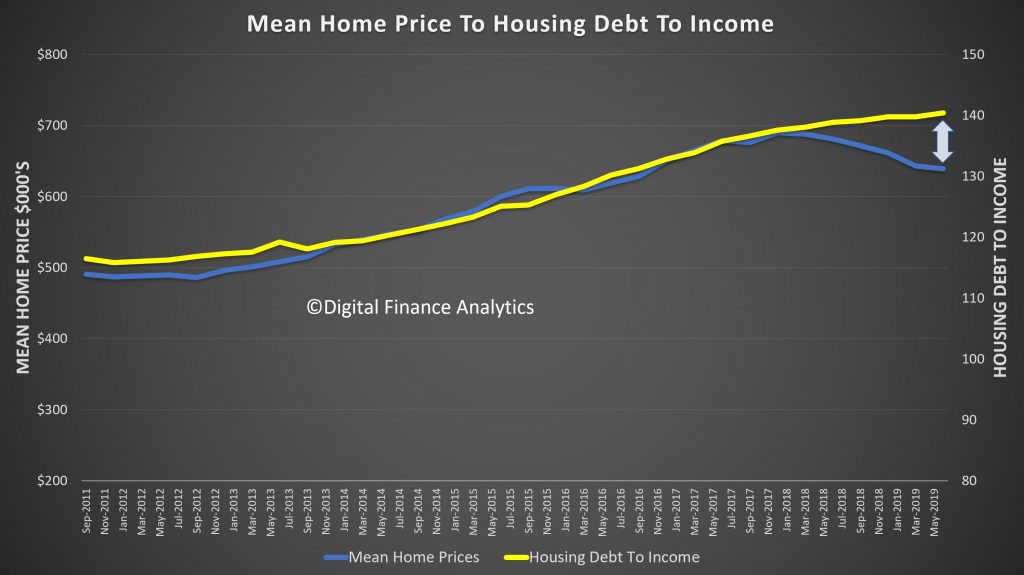

And the falls in prices have created a significant gap which highlights the risks in the system.

You can watch our recent show where we look at household debt in more detail including the data above.

A new UBS report has said that regulators getting tougher on capital is a threat to dividends, particularly those of the major banks. Via InvestorDaily.

UBS

reported that it was cautious on the Australian big four banks as the

low rates environment made it harder for the banks to generate a lending

spread and challenged the return on equity.

“If the housing

market does not bounce back quickly, this could put material pressure on

the banks’ earnings prospects over the medium term, implying that the

dividend yields investors are relying upon come into question once

again,” said the report.

Recent regulatory actions had also not

helped the outlook, with the recent confirmation by APRA that it was

going ahead with its proposal to reduce related party exposure limits to

25 per cent, in a move already impacting one bank’s capital abilities.

ANZ

announced shortly after the confirmation that it would have limited

capacity to inject fresh capital into NZ as its NZ subsidiary would be

at or around the revised limit.

The

$500 million operation risk change for ANZ, NAB and WBC would lead to a

16-18 bps reduction in CET1, with Westpac revealing in its third

quarter report that it was running thin on capital, with UBS reducing

it’s CET1 forecast in the bank to just 0.49 per cent, below APRA’s

unquestionably strong minimum.

Of the major banks, UBS estimated

that Commonwealth Bank was the in the best capital position, followed by

ANZ, but both NAB and Westpac were in trouble.

Part of the

capital position of CBA and ANZ was due to asset sales that would boost

sales; however, UBS did note that these divestments had not yet been

completed and there was uncertainty around its settlement.

UBS

said many of these behaviours were due to APRA’s interpretation of the

Murray report that said the regulator should set capital standards that

kept institutions unquestionably strong.

“This recommendation,

which was subsequently accepted by the government, was interpreted by

APRA to mean that the major banks’ level 1 CET1 ratios are at least 10.5

per cent.

“However, we believe that if the Australian banks

(level 1) hold substantial positions in their New Zealand subsidiaries,

which are treated as a 400 per cent risk weight rather than a capital

deduction, then double-gearing of capital brings this ‘unquestionably

strong’ mandate set by the FSI into question.”

UBS said a simpler

test was needed to ensure banks did not become overly reliant on capital

repositioning strategies, which effectively double-counted capital in

Australia and New Zealand.

Until this was done, UBS predicted

that banks would continue to cut dividends and that investors would see

through various strategies to ensure double-gearing did not occur.

“We expect CBA and WBC to join ANZ and NAB in cutting dividends should rates continue to fall.”

The world is one step away from a global recession, according to UBS who has questioned if the markets are ready. Via InvestorDaily.

UBS

has released global research paper where the investment bank reveals it

is anticipating major changers to their forecasts, which would result

in a global recession.

“We estimate global growth would be 75bp

lower over the subsequent six quarters and that the contours would

resemble a mild ‘global recession’,” said UBS.

The cause behind this will be the continued escalation of the US-China trade war.

“Unless

a deal is struck soon, the global weighted average tariffs will reach

levels last seen in 2003 and the US weighted tariffs will revert to 1947

levels,” found UBS.

UBS

compared this recession to the Eurozone collapse or the mid-’90s

“Tequila” crisis as opposed to more recent events like the ’08 crash.

If

UBS is right on the growth impact, all major central banks would ease,

which we have already seen the RBA do with a 25-basis-point cut made at

the start of June.

UBS predicted the Fed would cut an additional

100 basis points, on top of an expected 50-basis-point July cut, which

would send the economy dangerously low to the ground but would avoid

recession.

However, eyes will be on the escalation of trade

conflicts, which would push global equities down by 20 per cent and hurt

US growth.

“As trade tensions escalate, growth and policy rates

are likely to decline more in the US than in Europe. Such a scenario is

typically negative for the USD, but growth differentials matter less for

the dollar when we fall below the 30th percentile of global growth,”

said UBS.

Over half of the impact would be on “innocent

bystanders”, said the report, as spillovers from lower growth in US and

China impacts the rest of the world.

UBS is currently watching a

few world events that will inform its forecast, including recent public

hearings on China tariffs and the Fed meeting in July.

It also

looked forward to the G20 summit where it expected President Trump and

President Xi will have made enough progress to forestall tariff

escalation and in fact will likely announce tariffs by July.

If

the trade situation escalates, UBS predicted the US growth and policy

rates will come down by more than those in Europe but would push global

growth into the bottom quartile, which would see the USD top out against

G10 currencies in the middle of 2020.

Overall, UBS did not

predict too much change for Australia, with both US-China tariffs or

Mexico tariffs not having too great an impact on the base case.

It

did note that, previously, Australia had been buffered from external

shocks due to substantial fiscal and monetary policy flexibility.

However,

the low cash rate and a post-GFC low for the AUD may see this buffer

weakened and the external shocks having more of an impact.

The Swiss bank has revealed plans to launch a comprehensive strategic wealth management partnership in Japan, via InvestorDaily.

UBS

and Sumitomo Mitsui Trust Holdings Inc. (SuMi Trust Holdings) have

agreed to establish a joint venture, 51 percent owned by UBS, that will

offer products, investment advice and services beyond what either UBS

Global Wealth Management or SuMi Trust Holdings is currently able to

deliver on its own.

The JV will open UBS’s current wealth

management customer base to a full range of Japanese real estate and

trust services, while SuMi Trust Holdings’ clients – one of the largest

pools of high-net-worth (HNW) and ultra-high-net-worth (UHNW)

individuals in Japan – will be able to access UBS’s wealth management

services, including securities trading, research and advisory

capabilities.

“No wealth management firm today provides this range

of offerings to Japanese clients under a single roof. UBS expects the

new joint venture to fill this gap by offering expanded products and

services to clients from both franchises,” UBS said in a statement.

“This

is the Japanese market’s first-ever wealth management partnership

developed between an international financial group and a Japanese trust

bank. Subject to receiving all necessary regulatory approvals, the two

companies plan to begin offering each other’s products and services to

their respective current and future clients from the end of 2019. Also

subject to approvals, these activities will ultimately be incorporated

into a new co-branded joint venture company by early 2021.”

UBS Group CEO Sergio P. Ermotti said the Swiss banking giant has over 50 years of history in Japan.

“This

landmark transaction with a top-level local partner will ideally

complement our service and product offering to the benefit of clients,”

he said. “The joint venture is a blueprint for how complementary

partnerships can unlock value for clients as well as shareholders.”

Zenji

Nakamura, UBS’s Japan country head, said the transaction is a boost for

the group’s overall business in Japan, bringing reputational benefits

to its investment banking and asset management units, which fall outside

the alliance.

“It is a new milestone that sends a clear message of long-term commitment to the Japanese market.”

UBS

will contribute all of its current wealth management business in Japan

to the new company, while SuMi Trust Holdings will extend its trust

banking expertise and refer relevant clients to the new joint venture.

Sumitomo

Mitsui Trust Holdings is Japan’s largest trust banking group, with

Sumitomo Mitsui Trust Bank Limited serving as its core business. It

offers a range of services, including banking, real estate, asset and

wealth advisory to individuals and corporate clients. As of end March

2018, it held 285 trillion yen in assets under custody – Japan’s largest

such pool – and a significant portion of those assets come from HNW and

UHNW clients.

UBS boasts over US$2.4 trillion in assets under management. It operates from locations in Tokyo, Osaka and Nagoya.

The two companies have agreed not to disclose the financial details of the transaction.

Around 17 per cent of Aussie large cap companies downgraded guidance this reporting season as cost pressures weighed on major financial institutions and industrials, via InvestorDaily.

In its final analysis of the February 2019 reporting season, UBS

Global Research notes that EPS revisions for the market ex-resources and

ex-financials were the weakest since 2010.

“In aggregate, ASX 100 FY19 earnings expectations were revised down

0.1 per cent through reporting season, with the strong performance of

the market in February entirely driven by an expansion in the PE

multiple,” the report said.

“FY19 EPS revisions for the Resources were resilient at +6.6 per

cent. However, the Industrials ex-Financials were much weaker, with EPS

revised down 2.8 per cent, the weakest reporting season since 2010. The

1.9 per cent downward revision to Financials EPS was also the weakest

since 2011.”

The main upside surprise this reporting season came from

better-than-expected capital management, according to

UBS, that estimates that around 21 per cent of ASX 100 companies

delivered larger than expected dividends.

However, the report flagged cost pressures as the main downside this season.

“Pockets of cost pressure were the key downside surprise,

particularly among insurance and other financials, which have

experienced growth in remediation, restructuring and compliance charges

related to the royal commission (in addition to revenue headwinds), as

well as a mixed bag of Industrials, namely gaming (Crown Resorts and

Tabcorp), health care (Ansell and CSL) and materials (Boral, Brambles

and James Hardie). Some modest cost pressure also appears to be emerging

for the Resources. Companies affected include Alumina, Northern Star

Resources and Oil Search,” the report said

In its ‘Reporting Season Progress Update’, UBS flagged that analysts

were less optimistic on the outlook than company guidance implied.

“However, as reporting season progressed, companies downgraded

guidance significantly to the weakest February reporting season in four

years,” the bank said.

UBS estimates that 15 per cent of large cap companies upgraded guidance, while 17 per cent downgraded guidance.

“Among large cap companies that upgraded guidance, Ansell,

Computershare, Goodman Group, South 32 and Worley Parsons were well

received by the market.

“Among large cap companies that downgraded guidance, AMP, Coles

Group, REA Group, Scentre Group, Suncorp, Unibail-Rodamco-Westfield,

Woolworths, and Whitehaven Coal were not received well.”

“The biggest large cap positive surprises, in our view, have come

from Cleanaway Waste Management, Fortescue Metals Group, Goodman Group,

Insurance Australia Group, Magellan Financial Group and Ramsay Health

Care.

Negative surprises have, in our view, come from AMP, Bendigo and

Adelaide Bank, Crown Resorts, ResMed, Unibail-Rodamco-Westfield and

Woolworths.”

According to UBS’ Australian Banking Sector Update on 19 September, which involved an anonymous survey of 1,008 consumers who took out a mortgage in the last 12 months, 18 per cent stated that they “don’t know” when their interest-only (IO) loan expires, while 8 per cent believed their IO term is 15 years, which doesn’t exist in the Australian market, via InvestorDaily.

The research found that less than half of respondents, or 48 per cent, believed their IO term expires within five years.

The investment bank said that it found this “concerning” and was worried about a lack of understanding regarding the increase in repayments when the IO period expires.

The Reserve Bank of Australia (RBA) earlier this year revealed that borrowers of IO home loans could be required to pay an extra 30 per cent to 40 per cent in annual mortgage repayments (or an additional “non-trivial” sum of $7,000 a year) upon contract expiry. The central bank noted that the increase would make up 7 per cent, or $120 billion, of the total housing credit outstanding.

According to the RBA, 2020 is the year that most of the 200,000 at-risk IO loans will reset.

UBS’ research, which was conducted between July and August this year, revealed that more than a third of respondents, or 34 per cent, “don’t know” how much their mortgage repayments will rise by when they switch to principal and interest (P&I) contracts.

More than half, or 53 per cent, estimated that their repayments will increase by 30 per cent once their IO term ends, while 13 per cent expected their repayments to rise by more than 30 per cent, which is the base case for most IO borrowers.

“This indicates that the majority of IO borrowers remain underprepared for the step-up in repayments they will face,” UBS stated in its banking sector update report.

Further, nearly one in five respondents to the UBS survey, or 18 per cent, said that they took out an IO loan because they can’t afford to pay P&I.

“With a lack of refinancing options available and the banks reluctant to roll interest-only loans, these mortgagors will have to significantly pull back on their spending, sell their property, or [they] could potentially end up falling into arrears,” the investment bank stated in its report.

UBS also found it concerning that 11 per cent of respondents said they expected house prices to rise and planned to sell the property before the IO period expires.

“This is a risky strategy given how much the Sydney and Melbourne property markets have risen, and have now begun to cool,” the investment bank said.

Overall, the top two motivations for taking out an IO loan, according to UBS survey participants, were “lower monthly repayments gives more flexibility on my finances” (44 per cent) and “to maximise negative gearing” (43 per cent).

The second motivation was selected by 32 per cent of owner-occupier borrowers who cannot benefit from negative gearing as the tax incentive applies to investors, 53 per cent of which cited this benefit.

Most banks yet to implement tighter expense checks

The investment bank reiterated in its banking sector update that it expects mortgage underwriting standards to tighten further in the next 12 months. It claimed that, contrary to comments by regulators that “heavy lifting on lending standards is largely done”, most banks are yet to fully verify a customer’s living expenses and a large number of customers are still not submitting payslips and tax returns.

“As a result, we believe there is likely to be much work required for the banks to comply with the royal commission’s likely more rigorous interpretation of responsible lending and improve mortgage underwriting standards. We expect this is likely to play out over the next 12 months,” UBS stated in its update report.

UBS went on to maintain its belief that Australia is at risk of experiencing a “credit crunch” in the next couple of years, but it is waiting on a number of “signposts” to make a more calculated judgement. These include the Hayne royal commission’s interim and final report, major bank policies around living expenses, details from the Australian Prudential Regulation Authority on debt-to-income caps, the federal election, changes in property prices, and sentiments from the RBA.

“We remain very cautious on the Australian banks,” the investment bank concluded in its update report.

“After a prolonged 26 years of economic growth, many excesses have developed in the Australian economy, in particular the Sydney and Melbourne housing market.

“We believe the royal commission creates an inflection point and credit conditions are tightening materially. Whether Australia can orchestrate an orderly housing slowdown remains to be seen, and we think the risks of a credit crunch are rising given the significant leverage in the Australian household sector.”

A substantial reduction in reported “misstatements” was primarily due to a “material improvement” in the quality of loan applications submitted via the broker channel, according to a new UBS report; via The Adviser.

According to the investment bank’s latest Australian Banking Sector Update, which involved an anonymous survey of 1,008 consumers, there was a “sharp fall” in the number of “misstatements” reported in mortgage applications over the fourth quarter of 2018 (4Q18).

The survey revealed that 76 per cent of respondents reported that the mortgage applications were “completely factual and accurate”, up from 65 per cent throughout the first three quarters of 2018.

According to UBS, the improvement in lending standards was largely driven by the scrutiny placed on the industry by the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, and not off the back of regulatory intervention.

“We believe this implies that despite the efforts of the regulators and banks to tighten underwriting standards from 2015 onwards, these appear largely ineffective,” UBS noted.

“Our survey suggests that improvements in factual accuracy in mortgage applications have only come in response to the royal commission.”

The bank stated that the improvement was spurred by a “material improvement” in quality of mortgages submitted through the broker channel.

The research found that 26 per cent of borrowers who applied for a mortgage via the broker channel in 4Q18 “misstated” their loan application, down from 41 per cent in previous quarters.

However, UBS noted that fewer borrowers reported misstatements in loans submitted via the propriety channel (19 per cent).

Despite the improvement, UBS claimed that it’s concerned about the 10 per cent of respondents that reported that their broker-originated applications were “partially factual and accurate”, which it considers a “low benchmark”.

Moreover, UBS stated that it continues to find that a “substantial number of applicants state that their mortgage consultant suggested that they misrepresent on their mortgage applications”.

According to the figures, of those who misstated their broker-originated loan applications, 40 per cent said that their broker suggested that they misrepresent their application, which UBS claimed implies that 15 per cent of all mortgages secured via the broker channel were “factually inaccurate following the suggestion of their broker”.

“This is concerning given the heightened scrutiny on the industry, in particular following findings of broker misconduct and broker fraud in the royal commission,” UBS added.

Additionally, the report noted that 15 per cent of respondents who misrepresented information in a broker-originated application said that they exaggerated their household income, and 31 per cent said that they under-represented their living costs.

Turnaround times

The UBS research also revealed that 63 per cent of respondents who submitted a loan application via the direct channel received approval for the mortgage in one week or less, compared to 48 per cent of respondents who submitted via the broker channel.

Further, UBS stated that 31 per cent of direct-channel applicants received approval for a mortgage in two to four weeks, compared to 43 per cent of those who applied for a loan through the broker channel.

However, the investment bank added that when examining the approval duration between those who were completely factual and accurate on their application and those that misstated, “there was no statistically significant difference in mortgage approval duration”.

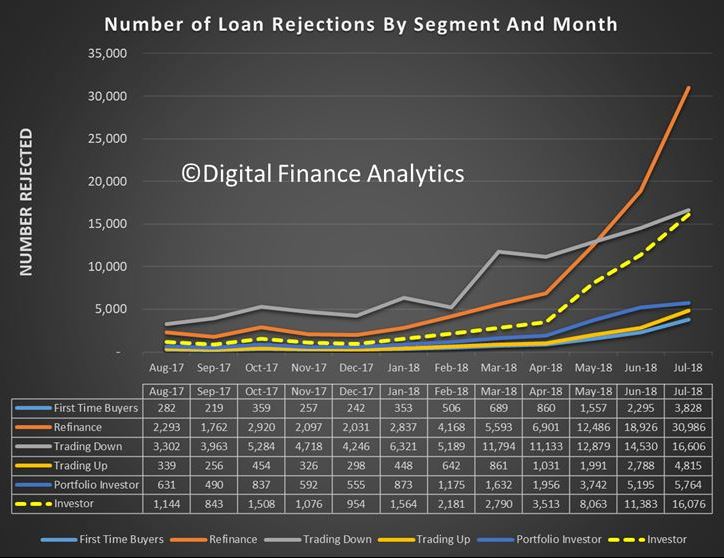

DFA research was featured in a number of the weekend papers, discussing the rising number of mortgage loan applications which are being rejected by lenders due to tighter lending standards, meaning that many households are unable to access the low refinance rates currently on offer.

NEARLY half of all homeowners are now shackled to their mortgage, with refinance rejections up significantly cent in less than a year as banks rattled by the royal commission drastically tighten borrowing rules.

Loan sizes are being slashed by 30 per cent, trapping many financially stressed customers including some who have been slugged with “out of cycle” interest rate rises. House hunters are also being hit by the credit crunch, with dramatic implications for property markets. The crunch stems from two big shifts in the way banks judge borrowers.

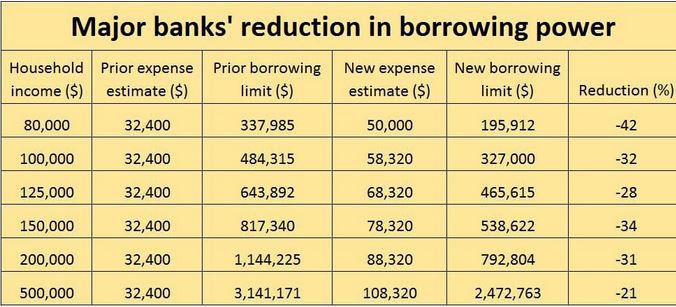

Expense estimates have been raised substantially — the minimum outgoings for an average household are now assumed to be a third higher, according to bank analysts UBS.

On top of this, granular cost breakdowns must be provided. After the royal commission revealed in March that expense checks were so lax as to be borderline illegal, new tests have been imposed requiring in some cases detail of weekly, fortnightly, monthly, quarterly and annual spending in as many as 37 categories from alcohol and haircare to shoes and pets, as well as doctor visits.

As a result, we think that now four in 10 households would now have difficulty refinancing. That means you are basically a prisoner in the loan you’ve currently go. This is based on our 52,000 household surveys plus data from a range of official sources. We estimate that 31,000 households’ refinance applications were rejected in July versus 2,300 in August last year.

Comparison service Mozo’s lending expert Steve Jovcevsk said . “There’s such a huge pool of people who are in that boat.” The most common motivation among those seeking to refinance was to save money by finding a better deal. Many were feeling the pinch because living costs were rising faster than wages and rates on interest-only or investment loans had increased.

The main issue these households are facing in seeking a new deal was banks’ definition of a “suitable loan now is different to six months ago because of the royal commission” and a clampdown by the Australian Prudential Regulation Authority. So there has been a big rise in loan rejections, particularly refinancing.

The borrowing power of hosueholds are being crimped, as shown on the banks website mortgage calculators. Those calculators, compared to a year or 18 months ago, are now on average showing a 30 per cent lower number. For some, the reduction in borrowing power is even greater. The head of UBS’s bank analysis team Jon Mott said that for a household with pre-tax income of $80,000 would get 42 per cent less from a bank; for a $150,000-a-year household, would get 34 per cent less.

Mozo’s Mr Jovcevski said in one example he was personally aware of, a person pre-approved to borrow $630,000 last year was recently offered just $480,000. The would-be borrower’s job and income hadn’t changed.

The implications for property markets were severe, Mr Jovcevski said. “There are fewer qualified buyers,” Reduced borrowing power would drag down selling prices and eventually cut valuations.

“It’s a double whammy for those mortgage prisoners,” Mr Jovcevski said. “Their valuations come in lower so their equity may end up being less than 20 per cents so they have to pay lenders mortgage insurance again” if they refinance.

Australian Banking Association CEO Anna Bligh said banks had to make reasonable inquiries to satisfy APRA’s strengthened mortgage lending standards but she said the term ‘home loan prisoners’ does not represent the facts of a fiercely competitive home loan market where everyday banks are seeking to attract new customers.

Mozo’ Jovcevski said homeowners seeking to give themselves the best chance of successfully refinancing should reduce their expenses in the months prior to applying and ensure all bills have been paid on time.

Mark Hewitt — general manager of broker and residential at AFG which arranges 10,000 home loans a month — said would-be borrowers whose budgets were at breaking point or beyond could still get a loan if they had equity, a clean repayments history and the ability to ditch key expenses such as fees for private school if under the pump.

Some people seeking their first home loan are signing documents in which they promise to cut their spending if a new loan is approved.

“When you get a mortgage you make sacrifices — you continue some of your discretionary spending but not all of it,” said Brett Spencer, head of Opica Group, which sells software to brokers that works out how much a prospective customer can cut back.

A figure is agreed between the broker and the would-be borrower which is then provided to the bank, which would otherwise rely on the higher, raw expense figures.

This makes in interesting point, mortgage brokers will be diving into household expenses more than ever before, but of course, household saying they will cut their expenses to get a loan is not the same a clear cash flow.

Thus even in this tighter market, the industry is still trying to find ways to bend the affordability rules. And it’s worth remembering that according to the latest figures from APRA more than 5% of new loans currently being written are outside standard assessment criteria.

This suggests that even now; bank lending standards are still too lose. All this points to more home prices falls ahead. This is reinforced by the latest Domain auction clearance rate data which was released yesterday, and shows that the final auction clearance rate last week in Sydney, Melbourne and Nationally ended up below 50% way lower on both volume and clearance rates than a year ago.

Yet despite all this, some are still sprooking the market, saying it’s a great time to buy. We do not agree.

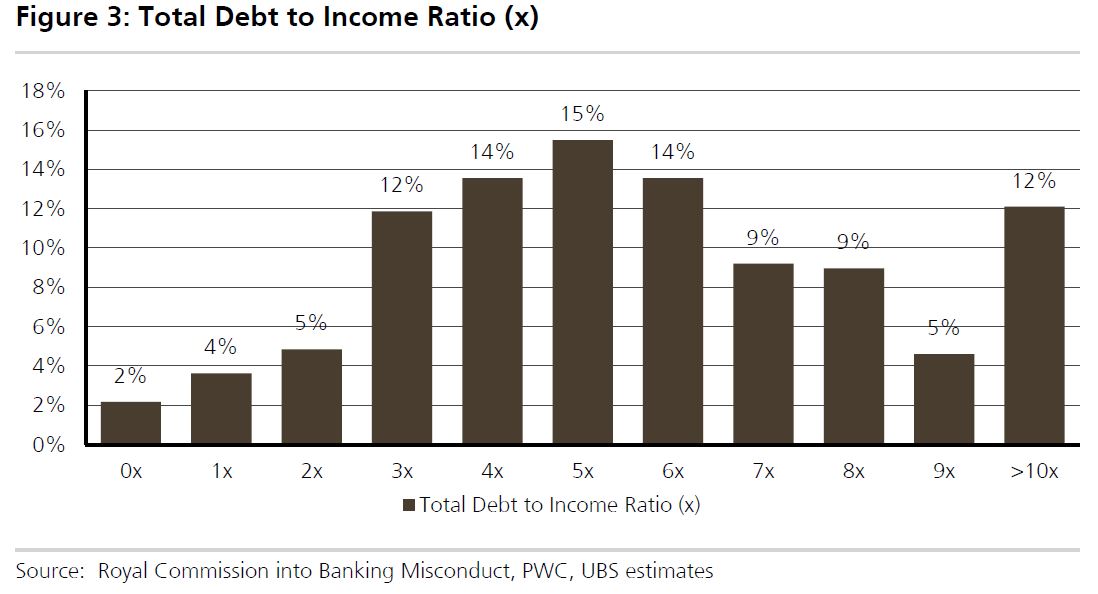

UBS continues their forensic dissection of the mortgage industry with the release of their analysis of data from Westpac, which the lender provided to the Royal Commission. This was representative data from the bank of 420 WBC mortgages analysed by PwC as part of APRA’s recent review. APRA Chairman Wayne Byres found WBC to be a “significant outlier”, with

PwC finding 8 of the 10 mortgage ‘control objectives’ were “ineffective”.

UBS says for the first time information on borrower’s Total Debt-to-Income ratios (not Loan-to-Income) has been made available. They found WBC’s median Debt-to-Income at 5.4x, with 35% of the sample having Debt-to-Income ratios of >7x. Further 46% of the mortgage applications had an assessed Net Income Surplus of <$250 per week.

This data raises questions regarding the quality of WBC’s $400bn mortgage book (70% of its loans). While WBC has undertaken significant work to improve its mortgage underwriting standards over the last 12 months, we expect it and the other majors to further sharpen underwriting standards given the Royal Commission’s concerns with Responsible Lending. This could potentially lead to a sharp reduction in credit availability.

This raises two questions. First how much tighter will credit availability now be. We continue to expect an absolute fall in loan volumes, and this will translate to lower home prices.

Second, is this endemic to the industry, or is Westpac really an outlier? From our data we see similar patterns elsewhere, so that is why we continue to believe we have systemic issues.

Income is being overstated and expenses understated.

Customers have multiple loans across institutions and these are not always being detected, so their total debt burden is higher than the bank sees.

Combined these are significant and enduring risks. Chickens will come home to roost! Especially if rates rise.