As the country continues its inexorable march towards a cashless society, it’s important to remember the downsides. Via The Adviser.

Australia

has been just a few years away from being a cashless society for a

couple of decades now, but it will eventually get there. Legislation

currently before the Senate aims to ban transactions over $10,000 in a

bid to hinder the black economy. From there, it’s not difficult to

imagine that the ubiquity of digital payment systems – and efforts the

by government – will see hard cash disappear at some point in the

future.

One of the supposed benefits of a cashless society is

that it cuts down on crime, the logic being that if there’s less cash to

steal, less cash is stolen. Laundering dirty money is also harder, as

every transaction is logged in some form or another.

But a cashless society comes with a number of negatives that might well outweigh the positives.

“As

payments move online, there would be an increased risk of crimes such

as identity theft, account takeover, fraudulent transactions and data

breaches, due to the higher volume of cashless transactions and more

points of exposure for the average consumer,” Dr Richard Harmon,

managing director of financial services at Cloudera, told Investor

Daily.

“Hackers

and other criminals now have new ways to get access to accounts and to

potentially set up synthetic accounts to facilitate more sophisticated

money laundering activities.”

And that’s just the risk posed by hackers. According to the UK’s access to cash report, a cashless society could heighten the risks of financial abuse. Elderly people, who might lack understanding of digital technology, would be particularly vulnerable. Couples with joint bank accounts are also at risk – money can be tracked and controlled by one person. These issues are already of great concern, but they’d be even worse in a cashless society.

That’s

not to mention that digital systems rely on topnotch digital

infrastructure, something that Australia doesn’t exactly have in spades.

That infrastructure also has to be more or less impervious to cyber

attacks, which may be carried out by state-sponsored actors with an

interest in crippling a country’s entire financial system. In the face

of that existential threat to the economy, a little bit of money

laundering doesn’t seem so bad.

A cashless society could also

make things worse for workers and the most vulnerable. It’s only a short

jump from cashless to “cashier-less”, and a cashless society would have

to deal with an explosion of unemployed low-skill individuals.

Meanwhile, those who lack access to banks – or prefer not to use them – are also at risk.

“Let

me highlight that one of the concerns about becoming a cashless society

– at least as we transition into this state – is the ability for the

underbanked or unbanked to have sufficient access to function properly

as they would within a cash-based system,” Dr Harmon said.

“This would be a key concern from a societal perspective.”

The

idea of a cashless society is promising. But hidden in that promise are

a number of caveats that any country – let alone Australia – would be

foolish to ignore.

This Act places restrictions on the use of cash or cash-like products

within the Australian economy. The Act imposes criminal offences if an

entity makes or accepts cash payments in circumstances that breach the

restrictions.

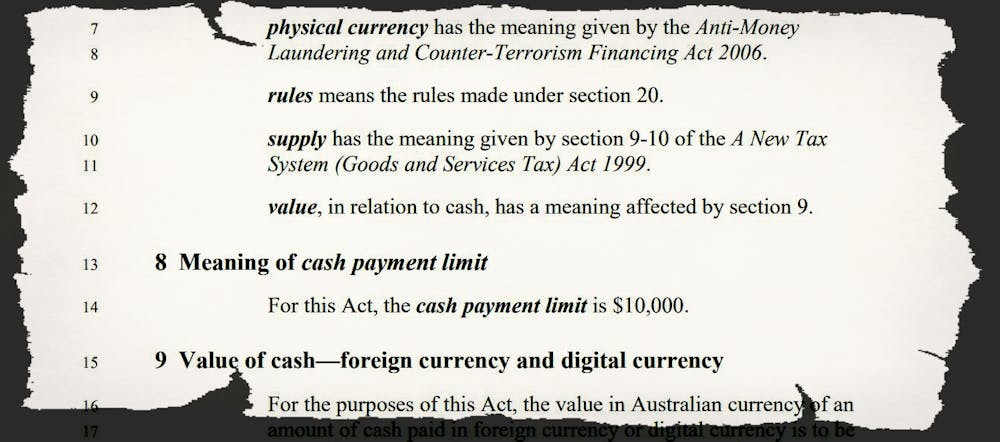

The proposed limit is A$10,000. Section 8 would make it an offence to make or accept cash payments of $10,000 occurring either as one-offs or in a linked sequence.

In parliament the minister said the $10,000 limit would not apply to

person-to-person transactions, such as private sales of cars.

But these exceptions are not included in the the Bill. What is

included is the phrase “specified by the rules”. Section 20 puts those

rules in the minister’s hands. Future ministers may narrow exceptions

and change rules.

It would remain legal to withdraw and hold more than $10,000. The stated intent of this Bill is to modify the use of cash, not the holding of cash.

All Australians will continue to be able to deposit and withdraw cash

in excess of $10,000 into and from their accounts, and to store more

than $10,000 of their money outside a bank.

Cash overboard

What’s proposed would limit competition (Visa, Mastercard, and PayPal would face a lesser competitor, for example) and limit long-held rights.

Everyday behaviour at present protected by the law would be criminalised.

In some cases, and perhaps many, the onus of proof would be reversed, with an “evidential burden” imposed on cash-using defendants.

Each partner in a partnership, each committee member of an

incorporated association and each trustee of a trust or superannuation

fund might become individually culpable for their entity’s use of cash.

Oddly, “bodies corporate and bodies politic” are treated differently

(Part 3), and the government itself cannot be prosecuted, an uneven

application of the law which has attracted little attention.

In my submission to the Senate inquiry (Submission 146) I argue the provisions would, among other things:

undercut the ability of banks to head off a banking crisis by providing a trusted and useful form of money

funnel more financial traffic through the equivalent of private toll roads

remove a guaranteed and always available fallback from electronic transactions

increase societal ill-ease and polarisation as citizens realise

their rights have been eroded for not particularly compelling stated

reasons.

Each point and many presented in other submissions need serious consideration, including in public Senate hearings.

The rationale presented

The speech to parliament introducing the bill was built around the hardly-new observation that cash payments can be “anonymous and untraceable”.

The government’s Black Economy Taskforce produced no detailed analysis but recommended the ban as a means of fighting tax avoidance, to:

make it more difficult to under-report income or charge lower prices and not remit good and services tax.

The speech also asserted that “more crucially”

the ban

would fight organised crime syndicates, although organised crime was not

mentioned in the part of the taskforce report that dealt with the

problem the limit was meant to address.

The guarantee dishonoured

Every pound note and then every dollar note issued by the

Commonwealth Bank and then Reserve Bank of Australia bears this

unconditional promise signed by the head of the bank and the head of the

treasury:

This Australian note is legal tender throughout Australia and its territories.

The bank’s website suggests the promise is ongoing:

All previous issues of Australian banknotes retain their legal tender status.

Its note printing arm was mortified earlier this year at the apparently accidental omission of the last letter “i” from the word “responsibility” on the new more secure $50 note.

The Bill before the Senate contains many and much more serious errors.

Cash has been one of the few things we can absolutely rely on,

whatever our status, situation or access to other payment means.

Removing (and dishonouring) that guarantee, while criminalising

reliance on it, should not be done lightly in a mad rush to an arbitrary

date.

Until now public debate about the proposal has been light, but concern is growing, even among quiet Australians.

Each Senator should ensure that last “i” in responsibility isn’t missing here either.

Author: Mark McGovern, Visiting Fellow, QUT Business School, Economics and Finance, Queensland University of Technology

As the member of the Executive Board of the Deutsche Bundesbank responsible for cash management, I arguably very much represent what many of you may consider the “”old world of payments””. A world in which there is limited space for innovation and progress. A world that is generally high in risk but low in reward. That is what is often claimed, at least.

In giving you my European and my German perspective, in particular, let me tell you: this case is not as straightforward as it may seem. In Germany and the euro area at large, the circulation of cash remains on the rise. The Bundesbank has issued more than half of the value of euro banknotes currently in circulation. Handling and distributing cash is a major operational task performed by national central banks in the euro area – particularly the Bundesbank. This also means that we need to continue investing in our cash infrastructure.

Cash serves various economic functions – making payments is just one of them. Our estimates suggest that roughly one out of ten banknotes issued by the Bundesbank is used for making payments in Germany. This limits the size of the pie that is up for grabs by the various non-cash payment alternatives.

Let us focus on cash as a payment instrument nonetheless. Usage of cash as a means of payment is declining – this is true both internationally and in Germany. But the level of cash usage is still high in many countries – and especially so in Germany. There may be less cash around, but we are far from being cashless. So why is it that, as of yet, physical cash has not disappeared beneath the waves in the vast ocean of digital payment methods?

2. Cash as an independent means of payment

In my view, this has to do with the special features that cash offers. We regularly monitor payment behaviour in Germany to understand households’ motives for using particular forms of payment over others. Protection against financial loss, personal privacy and a clear overview of spending are crucial features that households expect from payment instruments. Cash scores favourably in all of these areas, according to our surveys. My interpretation of these results: German households value independence – and physical cash offers three unique forms of independence, which distinguishes it from digital payment systems.

First, independence from one’s socio-economic background. Cash is tactile and does not require any technical equipment. The use of cash is easily understood across the generational divide. It is this haptic nature of cash, which, in my view, is an important element of strengthening financial inclusion. Ensuring access to cash may be particularly relevant in rural areas with insufficient banking or technological infrastructures. Cash is, in that sense, also a means of safeguarding social cohesion.

Second, independence from technological ecosystems. Given the still fragmented payments landscape in Europe, cash currently remains the one truly universal means of payment when it comes to P2P transactions in the euro area. Fintech companies are shaking up the traditional banking system in Europe. These companies can often leverage their global reach and huge customer base. This may bring benefits for consumers, for instance regarding cross-border payments. But it also means that customers are becoming locked into particular payment ecosystems. Cash offers an easy way out, at least for certain transactions.

Third, independence from social control and data collection. As legal tender, cash is fully backed by the domestic central bank. Cash is the obvious choice of payment method when it comes to personal privacy. This strengthens individual freedom. At the end of the day, digital payment systems work by using personal data. Collecting data is not harmful per se. But in the age of Big Data, collecting detailed data means obtaining valuable information which, in turn, makes it possible to construct patterns of individual behaviour. From a consumer protection point of view, the question arises as to how much information is necessary to carry out a particular transaction. From an economic point of view, personal data may be seen as an additional source of transaction costs to be factored in when comparing the underlying cost structures of different payment methods.

3. Retailing – the source of future transformations?

Payment methods tend to evolve in stages. For example, the adoption of mobile payment solutions is typically preceded by the widespread use of credit and debit cards. This is the case in Germany, where contactless payments have just started to catch on. China, on the other hand, seems to be a case in its own right. A comparative study in China and Germany supports this. The evidence reported there for the year 2017 suggests that cash and debit card payments account for the bulk of German retailers’ revenue. Mobile-based payment solutions did not play a noticeable role at that time. The reverse picture emerges for Chinese consumers in major cities. Third-party mobile payment providers clearly dominate here, having leapfrogged debit and credit card payments.

Payment habits in China are still in a state of flux as payment technologies continue to evolve. Seamless payment methods are on the rise. These methods essentially try to counter the “pain of paying” with a physical smile. To what extent similar shopping experiences are becoming popular in Germany remains to be seen. There are serious concerns surrounding data protection, and these would need to be alleviated first. In my view, the transition towards a society with less cash has to be driven by the user and not the supplier. It appears that, at least in Germany, consumers value the existing diversity of payment options. Cash continues to be an important part of this. In the bank-centred financial system in Germany, commercial banks are a major actor in the provision of a payment infrastructure that can cater for both cash and its digital alternatives.

Retailing in Germany is transforming, too. On the one hand, German retailers are increasingly turning to Chinese providers of mobile payment solutions, with a particular view to increasing sales to Chinese tourists. On the other hand, retailers have also increased the scope of their activities by closing the cash cycle in Germany. Nowadays, more and more shops are providing basic banking services for their customers such as cash withdrawals and deposits at the counters. To me, this shows that the transformation of the payments landscape is anything but complete.

4 CBDC as a cash substitute?

In the digital era, it should not be surprising that central banks, too, are discussing the potential merits and drawbacks of digital forms of a central bank currency (CBDC). There are currently many operational issues relating to CBDC that remain unresolved. This pertains, for example, to the technology implemented. Blockchains and the underlying distributed ledger technology seem promising, and central banks are open to them in principle. There are several potential use cases in settlement and payment systems, for instance, which are worth exploring further. But handling and safely storing vast amounts of data does not necessarily require distributed ledgers. We need to understand the underlying technologies better in terms of operational risk.

Also, the exact set-up of a CBDC needs to be thought through as the specifications may determine the potential effects. Broadly speaking, there are two conceivable variants of a CBDC. The wholesale type restricts access to CBDC to selected financial market participants for a specific purpose. The retail type, on the other hand, could grant domestic or even non-domestic non-banks access to CBDC on a wide scale.

The wholesale variant may be seen as an improvement on existing structures in terms of processing securities trading and foreign exchange transactions, but it would have little or no effect on monetary policy. The retail variant, however, could potentially mean a paradigm shift in the economic relationships between households, commercial banks and central banks that have evolved to date. uch a fundamental shift is not free of risks, and it requires careful consideration.

There is also the question of how strong households’ appetite for such a form of CBDC would actually be. This user perspective should not be left out in the discussion.

We need to see matters in perspective. After all, many of these debates have been fuelled by the plans announced by the Libra consortium. To me, what this shows, first and foremost, is the need to offer fast and cost-efficient systems for cross-border payments. We should go one step at a time. There are already several innovative market solutions that have the potential to be transformed into an efficient pan-European digital payment solution. In addition SEPA instant credit transfers could serve as a basis for pan-European payment solutions. We should develop these systems further before contemplating further, more radical steps.

5. Conclusion

The old world of payments versus the new world. This story is not new. At the turn of the millennium, there was a strong admiration for what was referred to as the new economy in Germany. New economy was a term used to describe internet start-ups which often relied on little physical capital to generate, at times, staggering market valuations. This was in contrast to the old economy. Think of brick-and-mortar car plants with, in some cases, considerable overheads. At this point, we can say that “”the new has become a bit old and the old has become a bit new””. Economic structures have integrated. The basic market forces still apply: the companies that survive are those that are competitive and offer a unique product. I view the world of payments in very much that spirit. To me, digital payments offer exciting prospects. But that does not necessarily imply the extinction of existing payment methods. It may very well actually increase the diversity of payment methods. Cash offers these unique forms of independence from social and electronic networks, which suggests to me that it will continue to enjoy great popularity in the euro area.

The Victorian Liberal Party held their state council meeting in Ballarat where a motion was put forward calling on the Government to abandon their $10,000 cash transaction ban policy.

We discuss the implications of this move, with Steve Holland who is a member of the Victorian Liberal Party and who moved the motion at the State Council Meeting.

The latest on the Cash Restrictions Bill – with Treasury hiding a key submission from KPMG, the architect of the ban… I discuss with Robbie Barwick from the Citizens Party.

Currency (Restrictions on the Use of

Cash) Bill 2019

I have carefully reviewed the latest iteration of this legislation

and am gratified that the Senate has chosen to review the proposals, which I strongly

oppose.

Not only is the bill significantly eroding our civil

liberties, but the conduct of Treasury needs to be called out by suggesting

that 3,400 of the 3,500 submission they received during their brief 2 week

exposure review submission period were part of a campaign “by the CEC, a

political party”. While there was indeed a campaign to oppose the draft

legislation, I have evidence that submissions were made by many concerned

individuals and businesses with no links to the CEC. Indeed, my own submission,

some of the contents I am using here again, is based on my own independent

research and analysis. I have no

financial or political association with said CEC. I believe Treasury tried to

play down the considerable opposition which exists within the community. This

bill is, in my view toxic.

Digital Finance Analytics is a boutique research and analysis firm specialising in the financial service sector. We undertake primary research through our surveys, as well as deep research from the global literature relating to financial services. We publish regularly via our online channels at Digital Finance Analytics[1] as well as preparing reports on a range of related subject matters for our clients, and we collaborate with a number of academics.

My objections are centred around the following points.

Civil Liberties Are Being Eroded. Further public debate on these measures are warranted as they are fundamentally restricting personal freedoms. Today I can use and hold cash as I please. If passed, my freedom will be eroded. This is one in a series of measures which have been taken (including media freedoms) which are curtailing the hard-won freedoms Australians used to enjoy. Public hearings should be held by the Senate to judge community reactions to the bill as part of the current review.

There Is No Cost Benefit. The stated objective of the bill is to close tax avoidance and money laundering loopholes. But there is no quantification of the potential “savings” – and this is also true of the earlier Black Economy Taskforce report. It appears that simply stating these desired objectives is seen as sufficient to justify the bill. What is the cost benefit of such a measure, bearing in mind that transactions which fall outside the exemptions would need to be tracked and examined?

Increased Surveillance Will Be Required.

In some form, monitoring of offending transactions would be required if the

Bill were passed. This is not explained,

nor how it would be policed. Who would police them, at what cost? Further, the bill proposed a draconian set of

penalties designed to deter. Treasury admitted this in their FOI’d response.

Existing Laws Are Not Enforced. The true

size of the black economy is much in dispute, but indications are that it is

already falling. In addition, much of the tax leakage and avoidance would be

covered by existing legalisation if it were being policed effectively. We

support the view, recently aired by Andrew Wilkie in the debate on the floor of

the house, that:

“There’s already a requirement

to report transactions over $10,000. The problem is that those laws are not

being implemented and enforced[2].”

There are other more pressing areas of tax

leakage and AML risk. According to the OECD report “Implementing The OECD

Anti-Bribery Convention” released as part of the OECD Working Group on Bribery,

Real Estate is identified as at “significant risk” of being used for money

laundering. Among a raft of recommendations, is one saying Australia should be

“Taking urgent steps to address the risk that the proceeds of foreign bribery

could be laundered through the Australian real estate sector. These should

include specific measures to ensure that, in line with the FATF standards, the

Australian financial system is not the sole gatekeeper for such transactions”. To date these loopholes, remain open, as do those

relating the corporates and big business who, partly thanks to the assistance

of the large international accounting firms are responsible for the lions share

of tax leakage and AML activity. Our research suggests that Government, under

heavy corporate and business lobbying is deliberately letting this slide,

preferring to target in on a relatively inconsequential area of tax leakage

relating to cash transactions.

The Legislation Would Be Ineffective. Beyond

that, it is clear from our wider research of a range of sources that such a

proposed cash ban would have very little impact on hard core tax leakage. For example,

Professor Fredrich Schneider, a research fellow at the Institute of Labor

Economics at the University of Linz, Austria, a leading international expert on

the black economy has stated that there is a lack of empirical evidence that

cash transaction bans will help reduce the black economy. Schneider published a

paper in 2017[3] “Restricting or Abolishing Cash: An Effective

Instrument for Fighting the Shadow Economy, Crime and Terrorism” in which he

made this specific point.

There Is Another Agenda. In addition, while the Bill is silent on the connection to implementing negative interest rates as part of unconventional policy, the link was made clearly in the 2016 Geneva Report by the International Centre Monetary and Banking Studies (ICBM) titled: What else can Central Banks do?[4] This paper which was drafted by officials from international organisations such as the IMF/BIS and multiple central banks + commercial banks. In addition, within the original Black Economy Taskforce Report there was mention of the benefits of a cash transaction ban in relationship to monetary policy – yet this link was denied by Treasury in their recent FOI release.

The IMF Shows Why. The same thematic came through in recent IMF Blogs and working papers. In April 2019, the IMF published a new working paper on how deeply negative interest rates work. In previous papers, the IMF has suggested that nominal interest rates may have to go deeply negative, for example, -3% – 4%. First, they say “In summary, ten years after the crisis, it is clear that the zero-lower bound on interest rates has proved to be a serious obstacle for monetary policy. However, the zero lower bound is not a law of nature; it is a policy choice. We show that with readily available tools a central bank can enable deep negative rates whenever needed—thus maintaining the power of monetary policy in the future.” Next they declare “Our view is that, when needed, deep negative rates are likely to be worth the political cost. While the complete abolition of paper currency would indeed clear the way for deep negative interest rates whenever deep negative rates were called for, such proposals remain difficult to implement since they involve a drastic change in the way people transact.”

The Bill Is Connected to Negative Interest

Rates. The connection is obvious in that in a negative interest rate

environment households and businesses will be likely to withdraw funds from the

banking system and transact in cash. If enough cash is extracted, negative

interest rates will simply have no effect. We believe the measures proposed in

the current Bill are truly about enabling negative rates, yet this is not

mentioned within the Bill. This is misleading and deceptive. The true

motivations should be on the record. But it explains the short time frames.

Households and Businesses Would Be Trapped In The Banking System. If such a ban was introduced households and businesses would be forced to use the banking system, meaning that bank charges could not be avoided, which benefits banks, not their customers. In addition, we have seen recent system and power failures which have caused disruption to the electronic payments systems. If cash is less available and restricted, a failure would be even more significant and inconvenient and could damage the economy. Once in the banking system, funds can be monitored and controlled (seen by the Taskforce as a positive move – we disagree), but such control could limit access to cash and transactions in general in a crisis. And we note from our SME surveys that many businesses, especially in rural and regional Australia regularly use cash as electronic alternatives are not available. Finally, offering cash for a discount, which is part of legitimate everyday business (because bank charges are avoided) would be removed.

The Structure Allows Change by Regulation Subsequently. The structure of the Bill enables parameters to be changed subsequently by regulation (not via Parliament). This opens the door to removing some of the concessions contained in the current drafting by agencies without full scrutiny. The bill is therefore open ended with regards to crypto, precious metals and other carveouts. In addition, we note surprisingly, government transactions, and cash transactions in Casinos are carved out, which again flags concerns about the structure and limitations of the bill.

A Reduced Limit Could Be Waived Through. Whilst we note that the $10,000 limit would require Parliamentary approval, in practice this could be made without full debate – as illustrated by the passage on the recent APRA bill, or as part of an omnibus “procedural” bill which masks the true intent. It is important to note that where cash transaction bans have been introduced, the value ceiling has been lowered. France has legally prohibited cash transactions above 1,000 euros, Spain has legally prohibited cash transactions above 2,500 euros, Italy has legally prohibited cash transactions above 3,000 euros, and the European Central Bank ended the production and issuance of its 500 euro note at the end of 2018.

In summary, my overriding concern is that Parliamentarians

will only consider the narrow tax efficiency aspect of the Bill and vote it

through without grasping the true intent and consequences. Civil liberties are

being eroded, and the trap will be set to force households and businesses to

transact within the banking system, thus facilitating experimental monetary

policies, via the back door.

Blog")