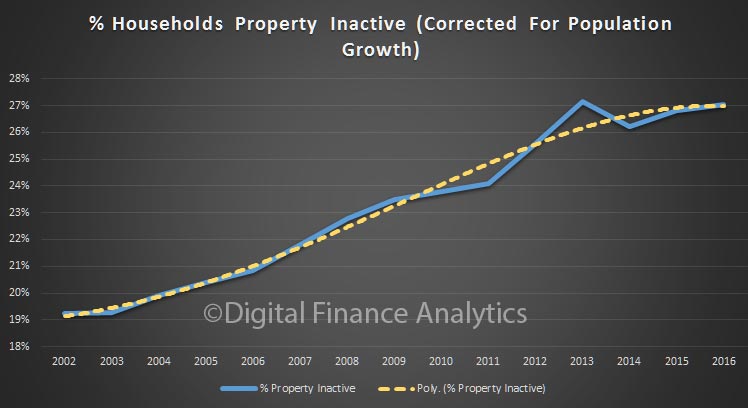

The proportion of households in Australia who own a property is falling, more a renting, or living with family or friends. We track those who are “property inactive”, and the trend, over time is consistent, and worrying.

It is harder to buy a property today, thanks to high prices, flat incomes and higher credit underwriting standards. Whilst some will go direct to the investment property sector (buying a cheaper place with the help of tax breaks); many are excluded.

It is harder to buy a property today, thanks to high prices, flat incomes and higher credit underwriting standards. Whilst some will go direct to the investment property sector (buying a cheaper place with the help of tax breaks); many are excluded.

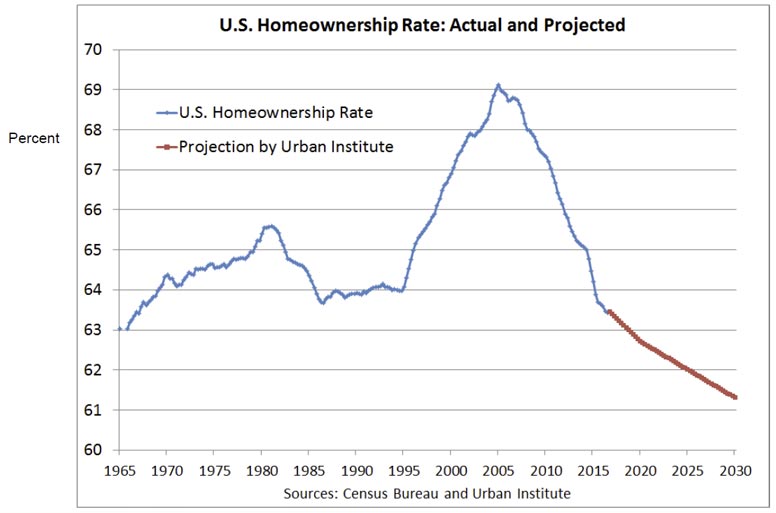

This exclusion is not just an Australian phenomenon. The Federal Reserve Bank of St. Louis just ran an interesting session on “Is Homeownership Still the American Dream?” In the US the homeownership rate has been declining for a decade. Is the American Dream slipping away? They presented this chart:

A range of reasons were discussed to explain the fall. Factors included: the Great Recession and foreclosure crisis; tougher to get a mortgage now (but probably too easy before the crash); older, more diverse American population; stagnation of middle-class incomes; delayed marriage and childbearing; student loans and growing attractiveness of renting for some.

A range of reasons were discussed to explain the fall. Factors included: the Great Recession and foreclosure crisis; tougher to get a mortgage now (but probably too easy before the crash); older, more diverse American population; stagnation of middle-class incomes; delayed marriage and childbearing; student loans and growing attractiveness of renting for some.

Yet, there is very little association between local housing-market conditions experienced during the recent boom-bust cycle and changes in attitudes toward homeownership. The desire to be a homeowner remains remarkably strong across all age, education, racial and ethnic groups. To remain a viable option for all groups, homeownership must become more affordable and sustainable.

They went on to discuss how to address the gap.

Tax benefits are “demand distortions.” Most economists agree that tax preferences for shelter (especially homeownership) push up prices: Benefits are “capitalized” into price or rent. Tax benefits of $150 bn. annually are skewed toward homeowners in high tax brackets via tax deductibility or exclusion. Tax changes likely in 2017—lower rates and higher standard deduction—will reduce tax benefits for homeownership, perhaps slowing or reducing house prices.

There also are “supply distortions” in housing that push up prices/rents. Land-use regulations/restrictive building codes increase construction costs, making housing less plentiful and less affordable. Local governments could reduce these constraints, and housing of all types and tenures would become cheaper.

Tightening Underwriting Standards. Unsuccessful homeownership experiences stem from shocks (job loss, divorce, sickness) that expose unsustainable financing—i.e., too much debt and too little homeowners’ equity (HOE). Reduce the risk of financial distress and losing a home by encouraging or requiring higher HOE and less debt. This would increase the age of first-time homebuyers and reduce homeownership but also reduce the risk of foreclosures.

You can watch the video here. But I think there are some important insights which are applicable to the local scene here. Not least, you cannot avoid the discussion around tax – both negative gearing and capital gains benefits need to be on the table. Supply side initiatives alone will not solve the problem.