From The Federal Bank of St. Louis Blog.

Have you ever wondered whether it makes sense to borrow for college? Or how much debt is worth taking on to get that dream home?

Well, we at the Center for Household Financial Stability did. Accordingly, we organized, along with the Private Debt Project, a research symposium back in June to see if there exist tipping points at which taking on more debt could be too financially risky. After all, if debt doesn’t lead to more income and wealth, what’s the point? Asking these questions is one of the driving forces at the Center because we don’t think enough attention is being paid to the debt side of family balance sheets.

For the symposium, we commissioned several new papers from Fed and non-Fed economists. The papers—along with my summary and reflection—were released last week.

The research findings were both interesting and often counterintuitive. Let me mention just a few.

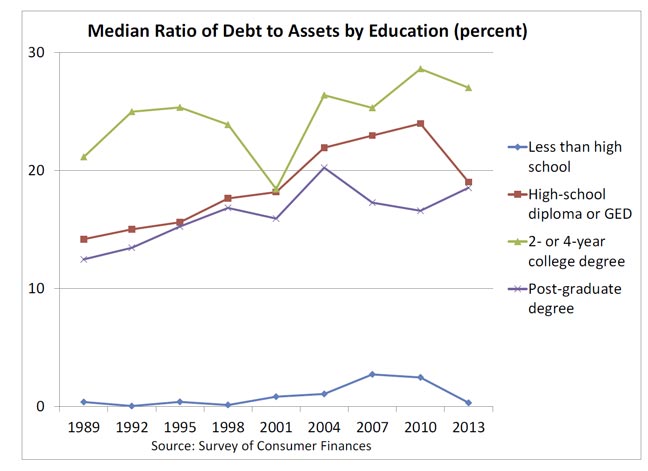

My colleagues Bill Emmons and Lowell Ricketts looked at loan delinquencies. Reflecting our Center’s ongoing work on the demographics of wealth, they found that younger, less-educated and nonwhite families were more likely to tip into delinquency. No huge surprise there. But then the co-authors posed what I think is a groundbreaking framing question, including for many Fed economists: Are these struggling families at this greater risk because they make riskier financial choices or because of structural, systemic forces that are largely shaping their financial behavior? In other words, is our tipping points question whether more financial education is primarily needed or whether a change in public policy is primarily needed?

Neil Bhutta and Benjamin Keys also discerned some alarming tipping points by looking at the nearly $1 trillion in home equity extractions between the boom years of 2002-2005. Extractors, they found, were more likely to default on their mortgages, even after controlling for credit scores and other risk factors. Even more surprising, extractors were more than twice as likely to become severely delinquent on their mortgage debts and almost 40 percent more likely to become delinquent on other kinds of debt.

We didn’t just look at the numbers but also the psychology of tipping points. Christopher Foote, Lara Loewenstein and Paul Willen found that, leading up to the financial crisis, excessive mortgage borrowing was fueled not by a financial indicator (the amount of income needed for a mortgage) but by a psychological one (the expected increase in future housing prices).

The symposium also opened up new ways to think about tipping points: At what point, for example, is an aspiration given up because of too much debt? And do different generations—say Gen Xers and millennials—think differently about how much debt is good or bad?

Several trends suggest families will be struggling with high debt levels for years to come, and it behooves all of us to think more about when debt goes from being productive to destructive. The financial health of families and our economy may depend on it.

I hope you’ll have a chance to read all of the papers, each one novel and forward-looking.

Additional Resources

On the Economy: Mortgage Debt’s Share of Total Debt Keeps Declining

On the Economy: How Consumer Debt Has Evolved in the Nation and the Eighth District