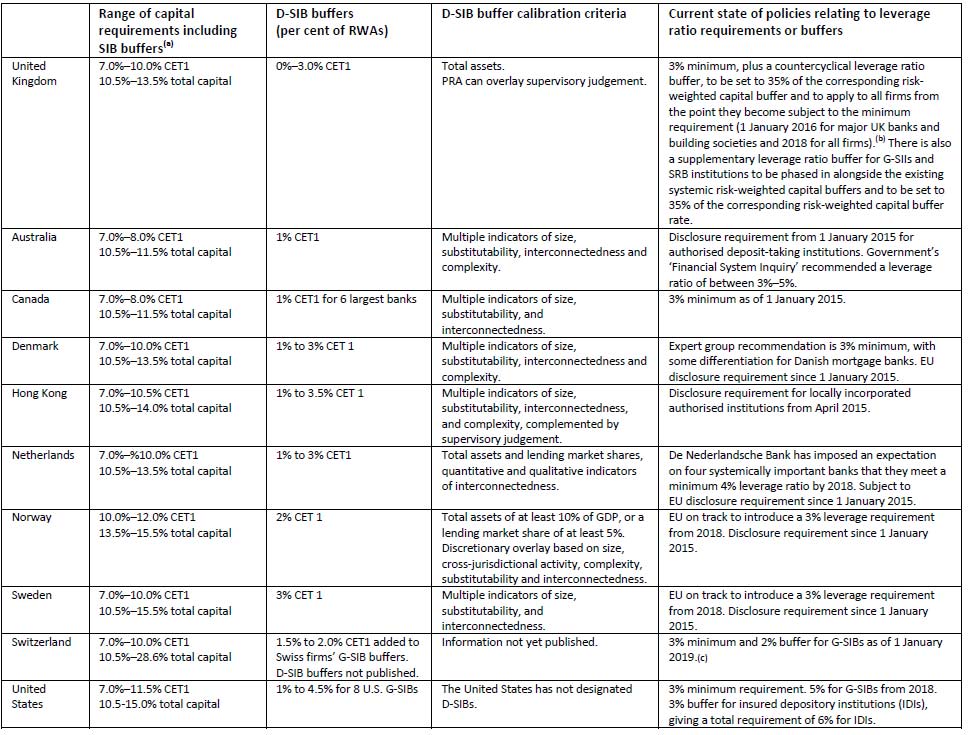

The UK’s Financial Policy Committee (FPC) has released the final version of its Systemic Risk Buffer (SRB) framework for banks relating to Domestically Significantly Important Banks) (D-SIB). It also shows Australian Banks relatively weaker capital position.

The framework highlights again that further risk capital will need to be held so that financial firms will be able to absorb losses while continuing to provide critical financial services. In the UK, depending on the size of the institutions, the buffer will be set between 0 and 3%. The SRB increases the capacity of UK systemic banks to absorb stress, thereby increasing their resilience relative to the system as a whole. The FPC judges that the appropriate Tier 1 capital requirement for the banking system is around 13.5% of Risk Weighted Assets.

Note, separately, an additional capital weight, per the Basel framework will apply for global systemically important banks (G‐SIBs).

Of special interest to Australian Banks is this table which shows that on a comparable basis, local banks here currently are required to hold less capital than peers in many other countries. Is the D-SIB here at 1% correctly calibrated? – especially, given 63% of all bank lending is residential property related?

The UK document just released, sets out the framework for the SRB that will be applied by the PRA to ring‐fenced banks, and large building societies that hold more than £25 billion in deposits and shares (excluding deferred shares), jointly, ‘SRB institutions’. The aim of the SRB is to raise the capacity of ring‐fenced banks and large building societies to withstand stress, thereby increasing their resilience. This reflects the additional damage that these firms could cause to the economy if they were close to failure. The FPC intends that the size of a firm’s buffer should reflect the relative costs to the economy if the firm were to fall into distress. The PRA will apply the framework from 1 January 2019 and later this year will consult on elements relating to the implementation of the SRB.

Overall, based on an analysis of the economic costs and benefits of going concern bank equity, the FPC judged the appropriate non‐time‐varying Tier 1 capital requirement for the banking system, in aggregate, should be 11% of RWAs, assuming those RWAs are properly measured. As up to 1.5 percentage points of this can be met with additional Tier 1 contingent capital instruments, the appropriate level of common equity Tier 1 capital is around 9.5% of RWAs. This judgement was made on the expectation that some of the deficiencies in the measurement of risk weights would be corrected over time. Until remedies are put into place to address this, the appropriate level of capital is correspondingly higher. On current measures of risk weighting, the FPC judges that the appropriate Tier 1 capital requirement for the banking system is around 13.5% of RWAs. This assessment refers to the structural equity requirements applied to the aggregate system that do not vary through time. In addition to baseline capital requirements, the FPC intends to make active use of the countercyclical capital buffer that will apply to banks’ UK exposures.

Under the SRB Regulations, the FPC is required to produce a framework for the SRB at rates between 0 and 3% of risk‐weighted assets (RWAs) and to review that framework at least every two years. The legislation implements the recommendation made in 2011 that ring‐fenced banks and large building societies should hold additional capital due to their relative importance to the UK economy. The FPC has considered its equality duty, and has set out its assessment of the costs and benefits of the framework.

Systemic importance is measured and scored using the total assets of ring‐fenced bank sub‐groups and building societies in scope of the SRB, with higher SRB rates applicable as total assets increase through defined buckets.

Those with total assets of less than £175bn are subject to a 0% SRB. The FPC expects the largest SRB institutions, based on current plans, to have a 2.5% SRB initially. Thresholds for the amounts of total assets corresponding to different SRB rates could be adjusted in the future (for example, in line with nominal GDP or inflation) as part of the FPC’s mandated two‐year reviews of the framework.

In July 2015, the FPC issued a Direction and a Recommendation to the PRA to implement the leverage ratio framework for UK G‐SIBs and other major UK banks and building societies on a consolidated basis. The FPC anticipates that the leverage ratio framework will be applied to UK G‐SIBs and other major UK banks and building societies at the level of the ring‐fenced bank sub‐group from 2019 (where applicable), as well as on a consolidated basis.