The latest print of the VIX or fear index highlights the switch in sentiment over the past week.

Given the ongoing gyrations in the major markets, (US down more than 4% today) it appears that the explanation of the correction as a flash crash thanks to programme trading is too simplistic.

Given the ongoing gyrations in the major markets, (US down more than 4% today) it appears that the explanation of the correction as a flash crash thanks to programme trading is too simplistic.

This is going to play out over weeks and months, and it is all about interest rate hikes.

This is going to play out over weeks and months, and it is all about interest rate hikes.

The Bank of England inflation statement over night also underscored rates are on the up, though they kept the rate at 0.5% and movements will be gradual

Any future increases in Bank Rate are expected to be at a gradual pace and to a limited extent. The Committee will monitor closely the incoming evidence on the evolving economic outlook, and stands ready to respond to developments as they unfold to ensure a sustainable return of inflation to the 2% target.

The US T10 Bond Yields are still elevated, and signals higher rates ahead.

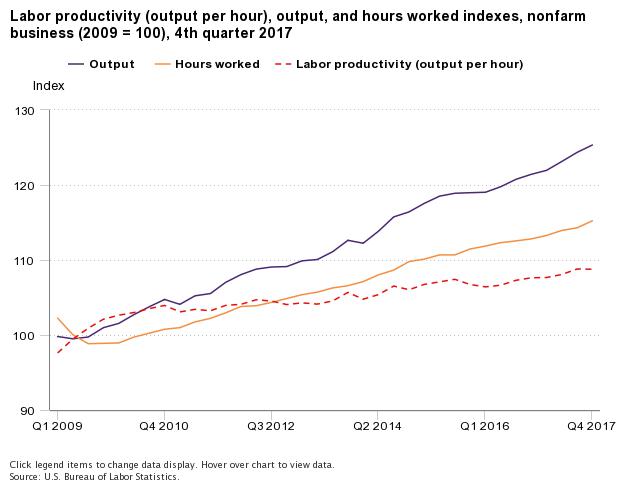

The latest data from the US Bureau of Labor signals more economic momentum, and supports the rate rise thesis.

The latest data from the US Bureau of Labor signals more economic momentum, and supports the rate rise thesis.

From the fourth quarter of 2016 to the fourth quarter of 2017, nonfarm business sector labor productivity increased 1.1 percent, reflecting a 3.2-percent increase in output and a 2.1-percent increase in hours worked. Annual average productivity increased 1.2 percent from 2016 to 2017.

From the fourth quarter of 2016 to the fourth quarter of 2017, nonfarm business sector labor productivity increased 1.1 percent, reflecting a 3.2-percent increase in output and a 2.1-percent increase in hours worked. Annual average productivity increased 1.2 percent from 2016 to 2017.

See my comments from earlier in the week: