Westpac released their 3Q16 update today, with a focus on capital, funding and asset quality. Pretty similar to other recent bank updates, with some rising delinquencies, but stronger capital. They also face higher capital risk weights later, and higher funding costs.

One point of note was a potential 5% fall in non-interest income, thanks to lower levels of debt market transactions in the institutional bank and higher insurance claims.

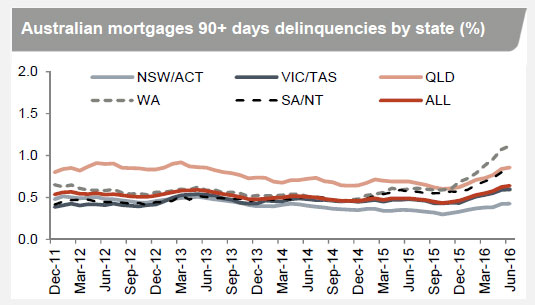

Looking at housing loans, they show higher 90+ delinquencies, especially in the mining heavy states.

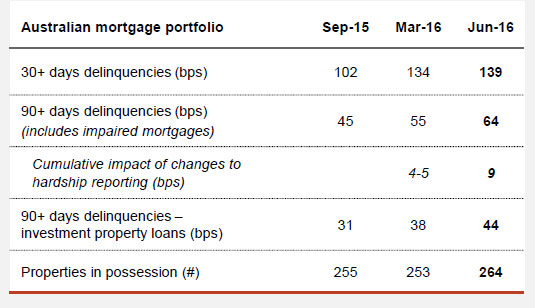

This translated into higher portfolio risks, and a small rise in the number of properties in possession.

This translated into higher portfolio risks, and a small rise in the number of properties in possession.

That said, WBC has a higher proportion of their portfolio in the lower risk states.

That said, WBC has a higher proportion of their portfolio in the lower risk states.

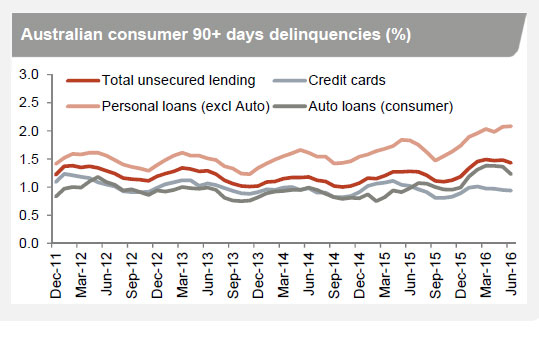

Consumer credit delinquencies are also on the rise.

Consumer credit delinquencies are also on the rise.

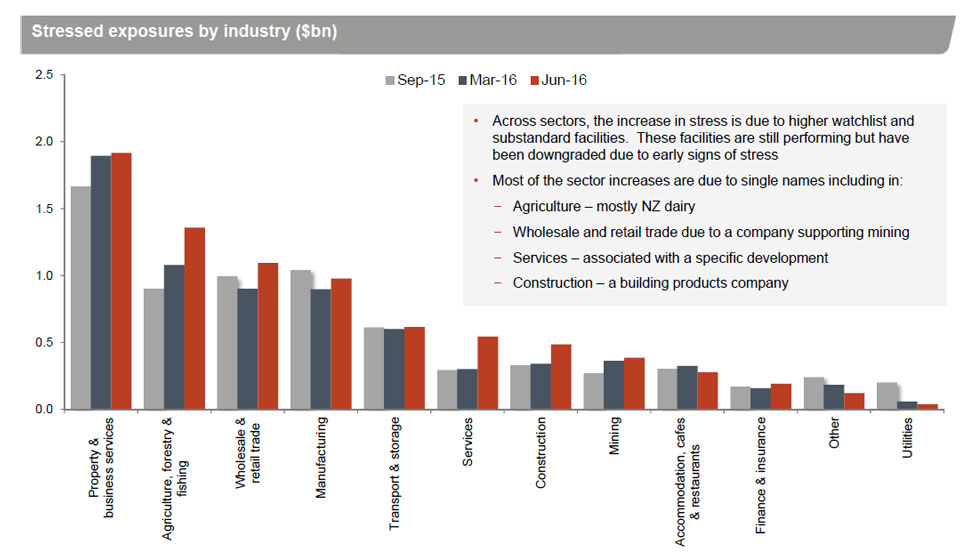

Looking at the commercial lending sector, we see some stress points, especially in agriculture (mainly NZ dairy), wholesale and retail trade in mining related areas, services and construction, where there are some specific single name issues. 1.36% of the mining portfolio is impaired and 3.15% graded as stressed. 14.28% of the NZ Dairy portfolio is graded as stressed, up from 10.04% in March 2016.

Looking at the commercial lending sector, we see some stress points, especially in agriculture (mainly NZ dairy), wholesale and retail trade in mining related areas, services and construction, where there are some specific single name issues. 1.36% of the mining portfolio is impaired and 3.15% graded as stressed. 14.28% of the NZ Dairy portfolio is graded as stressed, up from 10.04% in March 2016.

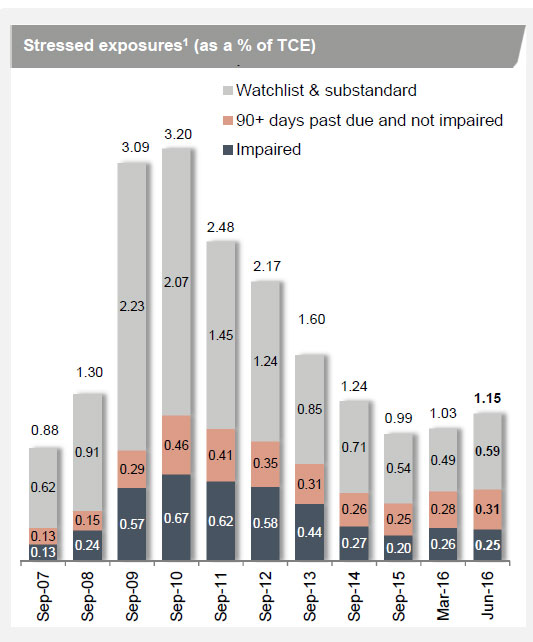

Taking a step back, stressed exposures were up 12 basis points to 1.15%, although impaired assets were $52m lower. The watch list and substandard assets (though fully performing) was up $1.4bn.

Taking a step back, stressed exposures were up 12 basis points to 1.15%, although impaired assets were $52m lower. The watch list and substandard assets (though fully performing) was up $1.4bn.

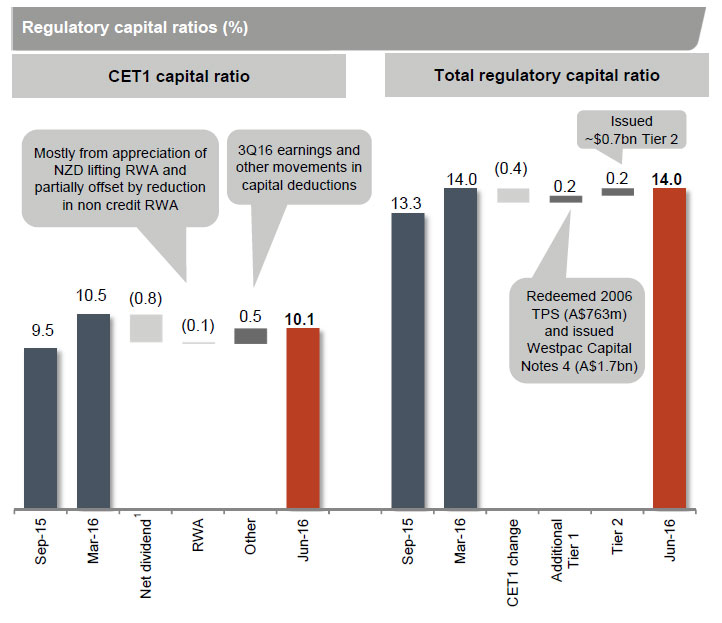

Westpac’s common equity Tier 1 (CET1) capital ratio was 10.1% at 30 June 2016, down 40 basis points. from 31 March 2016. The (CET1) capital ratio on an internationally comparable1 CET1 capital ratio was 14.1%. This places them in the top quartile globally.

Westpac’s common equity Tier 1 (CET1) capital ratio was 10.1% at 30 June 2016, down 40 basis points. from 31 March 2016. The (CET1) capital ratio on an internationally comparable1 CET1 capital ratio was 14.1%. This places them in the top quartile globally.

Changes in the calculation of RWA for Australian residential mortgages are

expected to see the ratio of total mortgage RWA to EAD rise to 25% from currently around 16%. This will reduce the CET1 capital ratio by approximately 110bps.

Westpac’s APRA leverage ratio was 4.9%, down 10 basis points since 31 March 2016. The decrease was primarily due to growth in exposures over the quarter and a $0.2 billion reduction in Tier 1 capital due principally to the determination of the 2016 interim dividend partially offset by Additional Tier 1 capital raised from the issue of Westpac Capital Notes.

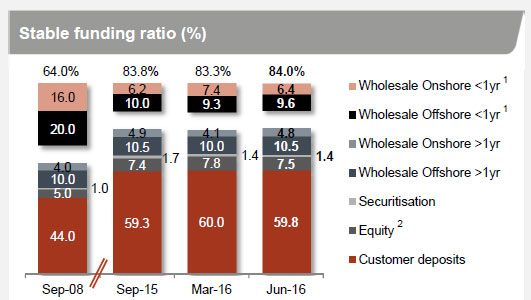

Westpac stable funding ratio was 84% at 30 June 2016, up 70bps over 3Q16 and the liquidity coverage ratio was 126% at 30 June 2016, compared to 127% at 31 March 2016. They noted that funding costs are rising across both wholesale markets and customer deposits.

Westpac stable funding ratio was 84% at 30 June 2016, up 70bps over 3Q16 and the liquidity coverage ratio was 126% at 30 June 2016, compared to 127% at 31 March 2016. They noted that funding costs are rising across both wholesale markets and customer deposits.

Changes to factors for determining interest rate risk in the banking book (IRRBB) after 30 June 2016 will be impacted by:

Changes to factors for determining interest rate risk in the banking book (IRRBB) after 30 June 2016 will be impacted by:

• Basel Committee on Banking Supervision expected to finalise new arrangements (Basel IV) by end 2016. These include:

– Adjustment to advanced models for credit risk

– Revised standardised credit risk

– Advanced RWA floors based on standardised approach

– Fundamental review of trading book

– Counterparty credit risk changes

– Operational risk to standardised approach

• APRA consultation on Basel IV expected to commence in 2017 with implementation from 2018