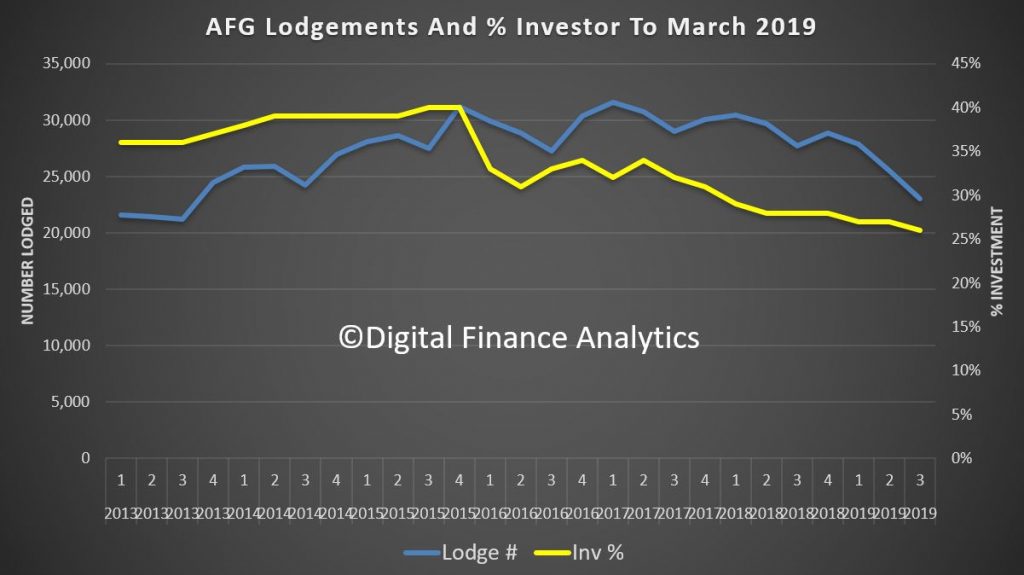

AFG provides fresh evidence of the fragile state of Australia’s home loan market emerged today, with new figures revealing national lending activity has slumped to the lowest levels in five years.

Whilst its myopic in one sense as it tracks business via AFG, it does provide further evidence of the slowing pace.

The AFG Mortgage Index and Competition Index released today showed

lending volumes across Australia in the first three months of 2019

dropped 10 per cent on the previous quarter. Volumes in the March

quarter were 15 per cent lower than the same period last year.

The 23,049 loans lodged during the quarter represented the lowest

number in six years, while the $11.6 billion volume was the lowest

quarterly figure since 2014.

AFG Chief Executive Officer David Bailey said “Today’s numbers

provide stark evidence that the lending environment has significantly

deteriorated. It’s a wake-up call for policymakers. The softening of the

residential market across the country is a real concern, with Sydney

and Melbourne driving the downturn and some states enduring a prolonged

period of falling activity.

“Despite moves by regulators to encourage activity, investment

lending remains at an all-time low of 26 per cent amid the well-

documented concerns around property values, particularly on the eastern

seaboard.

“Today’s data confirms we have reached a critical time in the housing

market cycle and we would urge policy makers to tread carefully in any

regulatory responses flowing from the Royal Commission. This is a time

for considered policy formulation that considers the full potential

impact on the lending market. It is clear, the broader implications for

the Australian economy are huge if we get it wrong.

“The volume of loans written in WA for the quarter of just over $1.3

billion represents the lowest volume seen in WA since the inception of

the AFG Mortgage Index. Whilst there has been some talk of WA moving

into a brighter resources-led period of sunshine, it is clear the local

economy needs broader stimulus.”

The tight lending market and falling house prices have contributed to

a decline in NSW volumes of almost 20 per cent on the same quarter in

2018. Victoria is down 16 per cent over the same period.

All other states are also much lower than the same time last year.

The only lift in volume over the quarter was seen in the Northern

Territory, with an increase in the average loan size and a decrease in

Loan to Value Ratios.

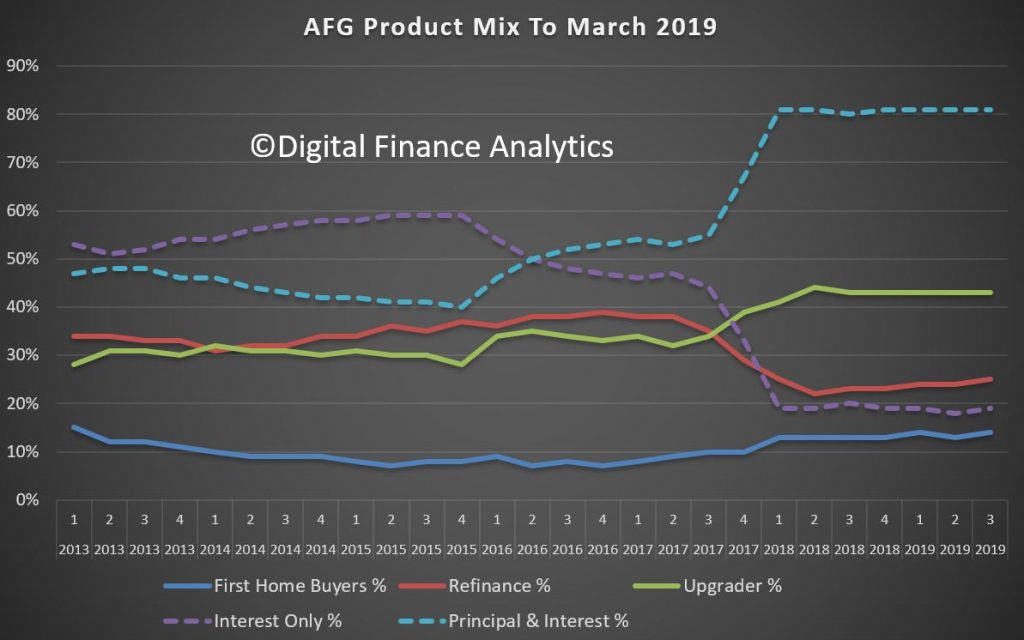

Following the relaxation of APRA-imposed caps on Interest Only (IO)

lending, AFG noted a small lift in IO lending driven by the major

lenders.

Four years ago, fuelled largely by strong investor demand, Interest

Only loans accounted for around 60 per cent of all loans written. Now,

with investor loans accounting for a quarter of new business, Interest

Only loans account for just 19 per cent of lodgements.

The breakdown of mortgages between major lenders – the ‘big four’

banks and their affiliated brands – and non-majors highlights the

crucial role mortgage brokers play in delivering competition to the home

loan sector.

The AFG Index showed the market share of non-majors has now been

locked in above 40 per cent for more than a year despite a marginal

increase for the majors to 58.6 per cent of total lodgements.

Mr Bailey said “The value mortgage brokers deliver by facilitating a

competitive lending environment is most starkly shown by the ongoing

decline in the market share of the major banks, which peaked in Q3 of

2013 at 78.2 per cent. Outside of the mortgage broking channel, the

majors have control and dominate the market. The distribution capability

provided by mortgage brokers enables the country’s non-major lenders to

compete.

“With the sole exception of First Home Buyers, who remain the last

bastion of major bank lending, the growth in non-major lending has been

broadly uniform across all other customer types.”

Major lenders are ahead on fixed-rate loans, with a steady increase

across the quarter, leaving four out of five homebuyers that chose the

certainty of fixing their interest rates doing so with a major lender.

Examination of the overall volumes going to the major bank reveals

the big losers over the past six months have been ANZ and NAB. NAB’s

share has halved over the past six months to now be as low as five per

cent.

The Westpac stable of brands emerged as big winners, as has Bankwest –

whose renewed focus on broker and customer service has paid strong

dividends in Western Australia. Bankwest accounts for more than one in

every five WA originations. Together with CBA, Bankwest has a

stranglehold on more than 35 per cent of all loans written in the State.

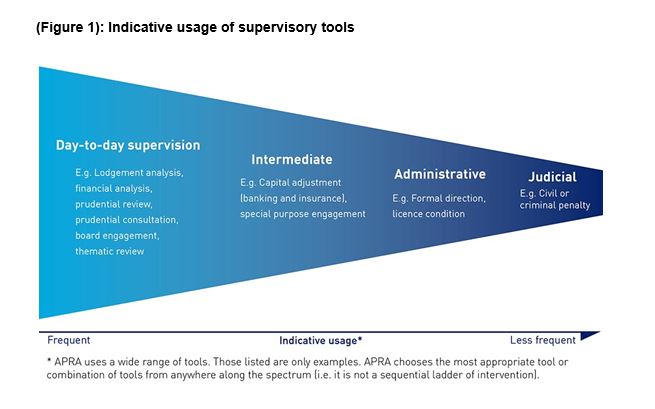

The Australian Prudential Regulation Authority (APRA) has released details on the future role and use of enforcement activities in achieving its prudential objectives.

Guiding principals include “risk-based”, “forward-looking”, “outcomes-based” and deterrence impact. Of course the question is, will it really make any difference? Here is the release.

APRA’s new Enforcement Approach, published today, sets out how APRA will approach the use of its enforcement powers to prevent and address serious prudential risks, and to hold entities and individuals to account.

The new Enforcement Approach is founded on the results of its Enforcement Review, which has also been published today. The Review, conducted by APRA Deputy Chair John Lonsdale, made seven recommendations designed to help APRA better leverage its enforcement powers to achieve sound prudential outcomes.

The APRA Members formally commissioned the Enforcement Review last November in response to a range of developments, including the creation of the Banking Executive Accountability Regime, the Prudential Inquiry into Commonwealth Bank of Australia, evidence presented to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, and proposals to give APRA expanded enforcement powers, particularly in superannuation. Mr Lonsdale led the Review, supported by a secretariat within APRA. Mr Lonsdale also utilised an Independent Advisory Panel comprising Dr Robert Austin, ACCC Commissioner Sarah Court and Professor Dimity Kingsford Smith to provide external perspectives and advice.

While APRA’s appetite for taking enforcement action is closely linked to a number of other components of its supervisory approach, the Review was focused on enforcement activity and not APRA’s wider operations

APRA Chair Wayne Byres

said APRA would implement all the recommendations, including:

adopting a “constructively tough” appetite to enforcement and setting it out in a board-endorsed enforcement strategy document;

ensuring APRA supervisors are supported and empowered to hold institutions and individuals to account, and strengthening governance of enforcement-related decisions;

combining APRA’s enforcement, investigation and legal experts in one strengthened support team, and ensuring resources are available to support the pursuit of enforcement action where appropriate; and

strengthening cooperation on enforcement matters with the Australian Securities and Investments Commission (ASIC).

Mr Lonsdale said the Review found APRA had, on the whole, performed well in its primary role of protecting the soundness and stability of institutions. But he said APRA could achieve better outcomes in the future by taking stronger action earlier where entities were not cooperative or open, and by being more willing to set public examples.

“APRA’s strong focus on financial risk has ensured the ongoing stability of Australia’s financial system, even during periods of financial and market stress, and protected the interests of bank depositors, insurance policyholders and superannuation members. But to remain effective, we must continue to evolve and improve, especially in response to the ways in which non-financial risks, such as culture, can impact on prudential outcomes.

“The recommendations of the Review will still mean that APRA as a safety regulator remains focused on preventing harm with the use of non-formal supervisory tools. However, APRA will be more willing to use the full range of its formal powers – such as direction powers and licence conditions – to achieve prudential outcomes and deter unacceptable practices,” Mr Lonsdale said.

Mr Byres thanked Mr Lonsdale and the APRA Review team for delivering a valuable piece of work that would sharpen APRA’s ability to hold entities and their leaders to account. He said enforcement activity is not intended to be a separate or stand-alone function, but rather a set of tools that APRA supervisors would use more actively, particularly in the case of uncooperative institutions. (See Figure 1)

“Having joined APRA only last October, John brought a fresh set of eyes to the task of examining APRA’s historical approach to enforcement. The Review acknowledges that as a supervision-led prudential regulator, APRA’s primary focus will always be on resolving issues before they cause problems for depositors, insurance policyholders and superannuation members, rather than relying on backward-looking actions after harm has occurred. In most cases, we will continue to achieve this through non-formal tools.

“However, formal enforcement is an important weapon in our armoury when non-formal approaches are not delivering prudential outcomes. Particularly as our powers have recently been strengthened in a number of areas, the new Enforcement Approach will ensure we make use of those powers as the Parliament intended. That means that in future, APRA will be less patient with the time taken by uncooperative entities to remediate issues, more forceful in expressing specific expectations, and prepared to set examples using public enforcement to achieve general deterrence.

“With the release of APRA’s revised Enforcement Approach today, the new enforcement appetite comes into effect immediately,” Mr Byres said.

Mr Byres indicated support for the recommendations on legislative change, and that these would be referred to the Government for its consideration. He also welcomed the recent passage of the Treasury Laws Amendment (Improving Accountability and Member Outcomes in Superannuation Measures No 1) Bill 2019 as a useful complement to APRA’s renewed enforcement appetite.

The Panel, led by Graeme Samuel, currently undertaking a Capability Review of APRA will take into account APRA’s new Enforcement Approach in its work.

Following an ASIC investigation, Citigroup will refund over $3 million to 114 retail customers for losses arising out of structured product investments offered by Citigroup between 2013 and 2017. Citigroup will also write to over 1000 customers remaining in the products to provide them an opportunity to exit early without cost.

ASIC investigated Citigroup’s sale and provision of general advice to

customers for fixed coupon structured products, which are complex,

capital at risk products tied to the performance of reference shares.

ASIC was concerned that while Citigroup considered its financial

advisers to be providing general advice, elements of its practice may

have led some customers to believe that Citigroup was providing personal

advice.

Citigroup’s practices included its advisers asking customers about

their personal circumstances, such as their tolerance for risk, and

providing financial education about benefits and risks to customers who

had no previous experience of investing in structured products.

Financial advisers have higher obligations and disclosure requirements

when providing personal advice.

From 1 January 2018, as a result of ASIC’s investigation, Citigroup

ceased selling structured products to retails clients under a general

advice model.

Citigroup will shortly start contacting affected customers. The

remediation will be completed by 10 September 2019, will be

independently assured and Citigroup will report to ASIC once the process

is complete.

A quick reminder we are running our live event tomorrow, where we update our property and finance scenarios and answer questions from the audience in real time. You can send questions beforehand, via the DFA blog, or in the live chat on during the session.

Here is a direct link to the event (where you can set a reminder).

ASIC has warned Australian financial services licensees that offer over-the-counter derivatives to retail investors located overseas could be breaking laws abroad, with Chinese authorities having alerted the watchdog that some online platforms have engaged in illegal activity, via InvestorDaily.

Regulators

in jurisdictions including Europe, Japan, North America and China have

restricted or prohibited the provision of certain OTC derivatives, such

as binary options, margin foreign exchange and other contracts for

difference (CFDs) to mitigate harm to retail investors.

ASIC has

expressed concern that some OTC derivative issuers that hold AFSLs may

be marketing or soliciting overseas clients to open accounts with

Australia-based licensees on the basis of avoiding overseas intervention

measures.

The regulator said is it considering whether breaching

overseas laws is consistent with obligations under Australian law to

provide services ‘efficiently, honestly and fairly’.

ASIC is also

considering whether it will see AFSL holders could be making misleading

or deceptive statements about the scope or effect of their license.

“AFS licensees who break the law in overseas

jurisdictions, or who mislead retail investors about their services

undermine the integrity of the Australian licensing regime,”

commissioner Cathie Armour said.

“ASIC will not tolerate that conduct.”

Chinese

authorities have already informed ASIC that “some online platforms are

illegally engaged in forex margin trading activities”.

Under Chinese law, no institution or agency has approval to carry out margin foreign exchange trading.

Temporary

product intervention measures have also been extended in Europe by the

European Securities and Markets Authority, with authorities in the UK

and Germany introducing permanent measures including anti-avoidance

provisions.

“AFS licensees offering OTC derivatives to overseas

retail clients should, as a matter of priority, seek advice on the

legality of their offerings to these clients,” commissioner Armour said.

“Any non-compliant activities should cease immediately and be notified to ASIC and the relevant overseas authorities.”

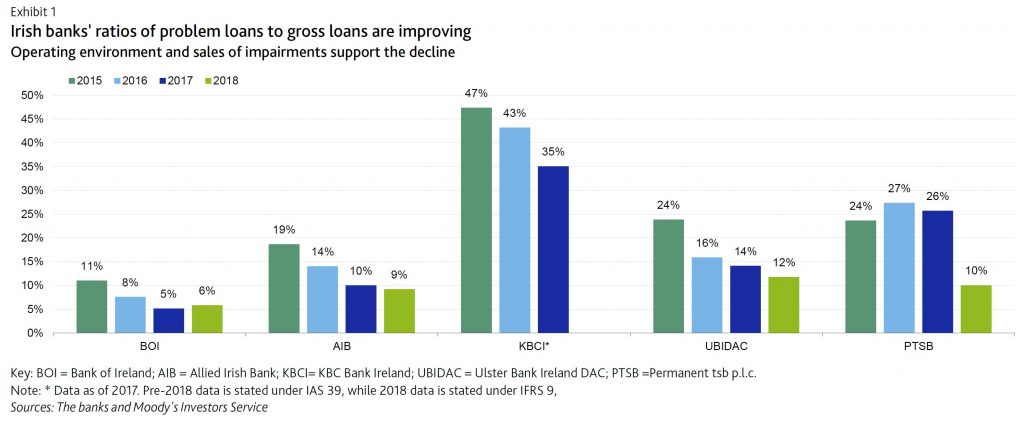

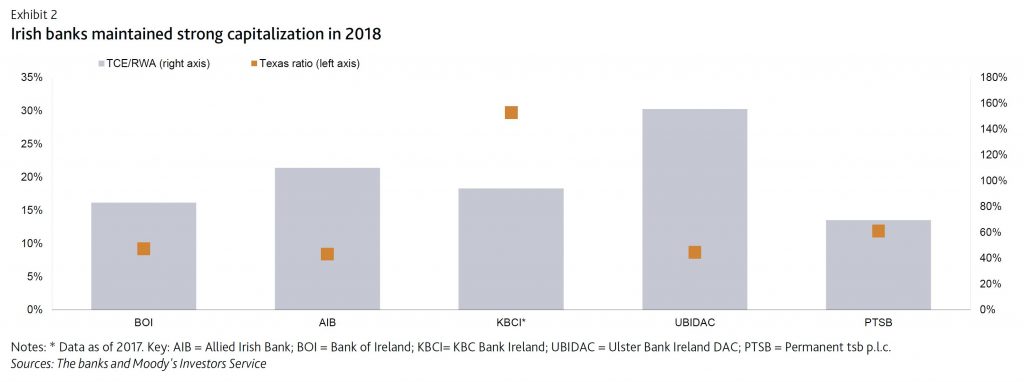

According to Moody’s, on 10 April, Bank of Ireland Group plc, the holding company of Bank of Ireland, announced that it had entered a securitization agreement involving €370 million of legacy nonperforming buy-to-let mortgages. The transaction, which is scheduled to close on 18 April, is credit positive because it will reduce the bank’s problem loans ratio and modestly improve asset risk, which remains a constraint on the bank’s standalone credit strength.

They estimate that following the transaction, the bank’s ratio of problem loans to gross loans will improve to 5.4% from 5.9% as of year end 2018, a step closer to European Central Bank guidance of 5%. The bank is on track to achieve the 5% nonperforming exposure target by end of this year. As of year-end 2018, the bank’s domestic peers reported problem loan ratios of 5.9%-11.9%, with BOI having the strongest ratio.

The transaction will boost BOI’s ratio of tangible common equity (TCE) to risk-weighted assets (RWAs) by 30 basis points from the 18.3% it reported for 2018 owing to the reduction in RWAs. The transaction will also improve the bank’s Texas ratio, the ratio of problem loans to loan-loss reserves and TCE, to 40% from 44% in 2018, which is one of the strongest among its peers.

Overall, these improvements strengthen BOI’s solvency and provide an improved base to support new lending. Moody’s expecst Ireland’s operating environment to remain supportive over the next 12-18 months, and that new lending will outweigh bad loan sales, leading to modest growth in the bank’s overall loan book this year.

The securitization of the impaired loans is an alternative to a direct sale, and allows BOI to maintain the customer relationship as the mortgage servicer. So far, in other impaired-loan securitizations, the originator has not stayed on as mortgage servicer. The BOI assets are notionally impaired performing loans which generate good predictable cashflows, and will typically not require active management, making them suitable for securitization.

In Ireland, banks must give borrowers at least 60 days’ notice before a change of servicer can can take place, and the transaction cannot close until this period has elapsed. During this period, the bank retains the assets on its balance sheet. However, since BOI is continuing to service the securitized loans, this notice period is not required, and NPL reduction is recognized the day the deal closes.

The sale of owner-occupied nonperforming mortgage loans has attracted close political scrutiny in Ireland amid claims that debt purchasers have taken a more aggressive approach to borrowers in arrears, including repossessing properties, than traditional banks.

However, Permanent tsb p.l.c. and Ulster Bank Ireland DAC last year each successfully completed sales of NPL portfolios backed by residential mortgages that helped reduce their legacy impairments. Allied Irish Banks, p.l.c. recently announced an agreement to sell a pool of nonperforming mortgages that are primarily investment properties. Irish banks have been taking solid steps to reduce their impaired assets we expect this to continue, resulting in improving asset risk for the sector.

The final results continue the trend of lowish total clearances on low volumes. National final clearance was 49.8% with 753 sales. Holidays of course get in the way at this time of year.

Canberra listed 61, reported 44 and sold 27, with 12 withdrawn, giving a Domain clearance of 48%.

Adelaide listed 83, reported 43 and sold 31, with 12 withdrawn, giving a Domain clearance of 56%.

Brisbane listed 104, reported 53 and sold 27 with 12 withdrawn, giving a Domain clearance of 42%.

The RBA released their Financial Stability report today, and even with the rose tinted RBA glasses there are a number of worrying issues touched on. Though none new. But their analysis of negative equity is over optimistic. So we will look at what they say, and highlight some additional considerations.

The RBA said:

Domestic economic conditions remain broadly supportive of financial stability. The unemployment rate has remained around 5 per cent since the previous Review and corporate profit growth has also been strong.

However, GDP growth in Australia also slowed in the second half of 2018. In particular, consumption growth eased and the outlook for consumption is uncertain.

Conditions in the housing market remain weak. Nationally, housing prices are 7 per cent below their late 2017 peak, although they are still almost 30 per cent higher since the start of 2013.

Growth in housing credit was slightly lower over the six months to February than the preceding half year, with investor credit hardly growing at all.

Nationally, falling housing prices have been driven by weaker demand and increased housing supply. The tightening in the supply of housing credit from improved lending standards has played a smaller part. Importantly, these more rigorous lending standards have seen the quality of new loans improve in recent years.

Measures of financial stress among households are generally low and households remain well placed to service their debt given low unemployment, low interest rates and improvements to lending standards. However, there has been an increase in housing loan arrears rates. The increase in arrears has been largest in Western Australia, where the decline in mining related activity has seen housing prices fall for nearly five years and unemployment increase.

They did in “deep dive” on negative equity using their securitised loan data.

Large housing price falls in parts of Australia mean some borrowers are facing negative equity – where the outstanding balance on the loan exceeds the value of the property it is secured against. Negative equity creates vulnerabilities both for borrowers and lenders. A borrower having difficulty making loan repayments who has negative equity cannot fully repay their debt by selling the property. Negative equity also implies that banks are likely to bear losses in the event that a borrower defaults. Evidence from Australia and abroad suggests that borrowers who experience an unexpected fall in income are more likely to default if their loan is in negative equity.

At present, the incidence of negative equity remains low. Given the large increases in housing prices that preceded recent falls and the decline in the share of mortgages issued with high loan to- valuation ratios (LVRs), housing prices would need to fall significantly further for negative equity to become widespread. However, even if this did occur, increased defaults would be unlikely if the unemployment rate remains low, particularly given the improvements in loan serviceability standards over recent years.

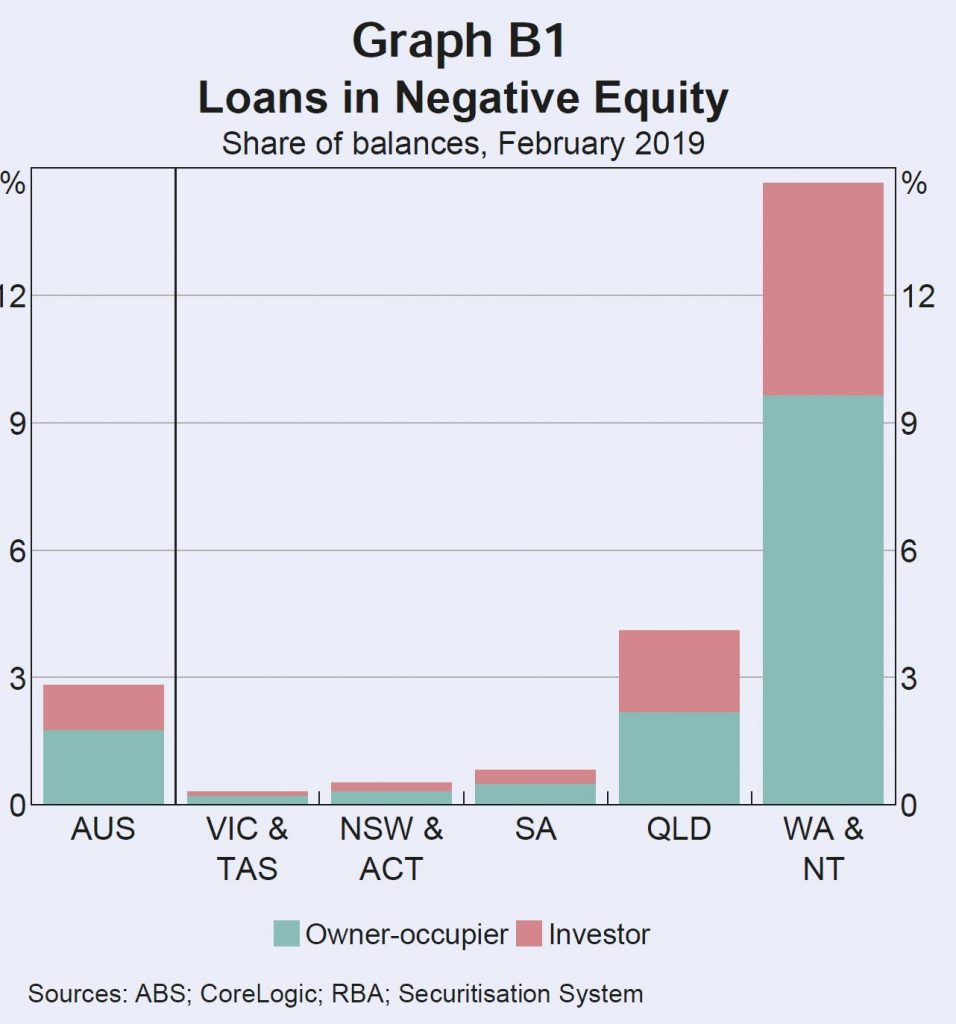

Estimating the share of borrowers with negative equity requires data on current loan balances and property values. The RBA’s Securitisation Dataset contains the most extensive and timely data on loan balances and purchase prices.

The Securitisation Dataset includes about one-quarter of the value of

all residential mortgages, or around 1.7 million mortgages.

This data can be combined with regional data on housing price movements to estimate the share of loans that are currently in negative equity. This suggests that nationally, around 2¾ per cent of securitised loans by value are in negative equity (just over 2 per cent of borrowers). The highest rates of negative equity are in Western Australia, the Northern Territory and Queensland, where there have been large price falls in areas with high exposure to mining activity. Almost 60 per cent of loans in with negative equity are in Western Australia or the Northern Territory. Rates of negative equity in other states remain very low.

Estimates of negative equity from the Securitisation Dataset may, however, be under or overstated. They could be understated because securitised loans are skewed towards those with lower LVRs at origination. In contrast, the higher prevalence of newer loans in the dataset compared to the broader population of loans, and not being able to take into account capital improvements on values, will work in the other direction. Some private surveys estimate closer to 10 per cent of mortgage holders are in negative equity. However, these surveys are likely to be an overestimate for a number of reasons; for instance, by not accounting for offset account balances.

DFA Says: Of course DFA estimates 10% of households in negative equity, after taking offset balances into account, and also adding in the current forced sale value of the property and transaction costs.

Information from bank liaison and estimates based on 2017 data from the Household Incomes and Labour Dynamics of Australia (HILDA) survey suggest rates of negative equity are broadly in line with those from the Securitisation Dataset.

DFA Says: The HILDA data is at least 2 years old, so before the recent price falls – so this set will understate the current position.

The continuing low rates of negative equity outside the mining exposed regions reflect three main factors: the previous substantial increases in housing prices; the low share of housing loans written at high LVRs; and the fact that many households are ahead on their loans, having accumulated extra principal payments.

Housing prices in some areas of Sydney and Melbourne have fallen by upwards of 20 per cent from their peak in mid to late 2017. But only a small share of owners purchased at peak prices, and many others experienced price rises before property prices began to fall. Properties purchased in Sydney and Melbourne since prices peaked account for around 2 per cent of the national dwelling stock. Looking further back, properties purchased in these two cities since prices were last at current levels still only account for around 4½ per cent of the dwelling stock.

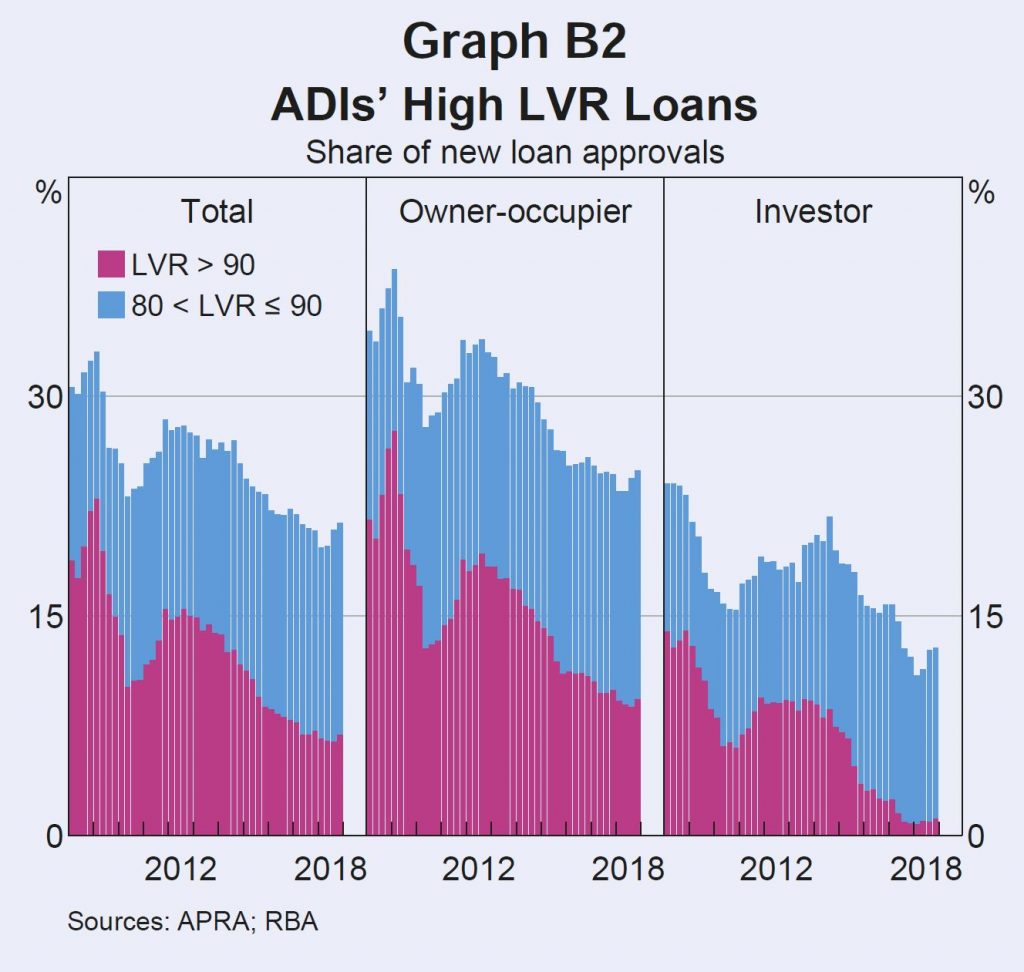

Few recent borrowers had high starting LVRs. Over the past five years, the share of loans issued by ADIs with LVRs above 90 has roughly halved. Since 2017, it has averaged less than 7 per cent (Graph B2). Around 80 per cent of ADI loans are issued with an LVR of 80 or less. Around 15 per cent of owner-occupier borrowers and 20 per cent of investors take out a loan with a starting LVR of exactly 80.

Given most borrowers do not have high starting LVRs, housing price falls need to be large for widespread negative equity. Only 15 per cent of regions have experienced price declines of 20 per cent or more from their peaks. Around 90 per cent of these regions are in Western Australia, Queensland and the Northern Territory.

If a borrower has paid off some of their debt, then price declines will need to be larger still for them to be in negative equity. Most borrowers have principal and interest loans that require them to pay down their debt and many borrowers are ahead of their repayment schedule. Around 70 per cent of loans are estimated to be at least one month ahead of their repayment schedule, with around 30 per cent ahead by two years or more.

When a borrower is behind on repayments and their loan is in negative equity, banks classify the loan as ‘impaired’. Banks are required to raise provisions against potential losses from impaired loans through ‘bad and doubtful debt’ charges. Currently the proportion of impaired housing loans is very low, at 0.2 per cent of all residential mortgages, despite having increased of late (Graph B3).

Queensland, Western Australia and the Northern Territory together account for around 90 per cent of all mortgage debt in negative equity. These states have regions that experienced large and persistent housing price falls over several years.

This has often been coupled with low income growth and increases in unemployment, which have reduced the ability of borrowers to pay down their loans. Loans currently in negative equity were, on average, taken out around five years ago and had higher average LVRs at origination, of around 85 per cent. This made them particularly susceptible to subsequent falls in property values. Investment loans are also disproportionately represented, despite typically having lower starting LVRs than owner-occupier loans. Investors are more likely to take out interest-only loans in order to keep their loan balance high for tax purposes. Around 10 per cent of loans in negative equity have interest only terms expiring in 2019, which is double the share for loans in positive equity. For these borrowers, the increase in repayments from moving to principal and interest may be difficult to manage, especially as loans in negative equity are already more likely to be in arrears. Having more borrowers in this scenario is distressing for the borrowers themselves and for the communities they live in. However, it is unlikely to represent a risk to broader financial stability given it remains largely restricted to mining-exposed regions, which represent a very small share of total mortgage debt.

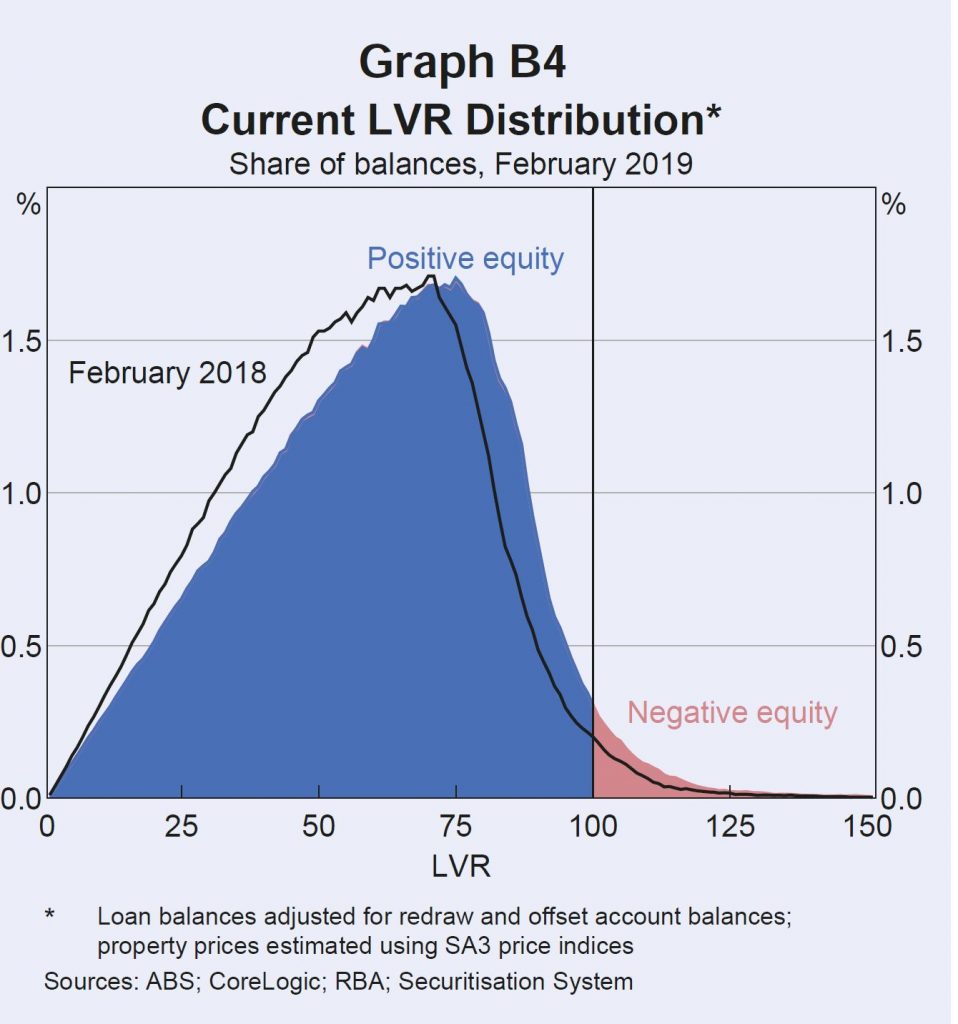

Continued housing price falls would be expected to increase the incidence of negative equity, particularly if they affect borrowers with already high LVRs. Around 11/4 per cent of loans by number (and 13/4 per cent of loans by value) have a current LVR between 95 and 100, making them likely to move into negative equity if there are further housing price falls (Graph B4).

However, compared to the international experience with negative equity during large property downturns, the incidence of negative equity in Australia is likely to remain low. Negative equity peaked in the United States at over 25 per cent of mortgaged properties in 2012 and in Ireland it exceeded 35 per cent, as peak to trough price falls exceeded 30 and 50 per cent respectively.

However, high origination LVRs were far more common in these countries than they have been in Australia.

DFA Says: Except we know there were high levels of mortgage fraud and incorrect data supporting loan applications. Higher than in Ireland.

Even if negative equity was to become more common in the larger housing markets of Sydney and Melbourne, impairment rates for banks are unlikely to increase significantly while unemployment and interest rates remain low.

DFA Says: you need to get post code granular to see what is going on. As our earlier heat map showed.

Just days after CBA announced it was cutting its rates and stepping away from its competitors, another big four has matched the changes across the board – and likely triggered a continued decrease in fixed rates at lenders of all sizes.

The newly announced decreases go into effect at Westpac tomorrow for

fixed rate loans paying P&I and are open to both new and existing

customers switching into a fixed rate.

“As expected, it hasn’t taken Westpac long to match the fixed rate cuts this week from Commonwealth Bank,” said Steve Mickenbecker, Canstar group executive of financial services.

“These decreases are a further sign that the big banks are wanting to

fight back to regain the market share losses to the local arms of

foreign banks and other domestic lenders over the past 12-months.”

At Westpac, the three- and five-year fixed rates for owner occupiers

paying P&I are to decrease by 0.10% while the four-year rate will

drop by 0.20%.

Fixed rates will also decrease for investors paying P&I, by 0.06%

for two-year, 0.20% for three-year, and 0.10% for five-year,

demonstrating “the bank’s desire to increase investment lending in the

face of declining demand,” according to Mickenbecker.

Other lenders have already been making moves of their own to stay competitive.

Suncorp has announced a discount for its three-year fixed package

rates for eligible new home lending, meaning the non-major currently has

the lowest three-year fixed rate in the market at 3.49% for owner

occupied and 3.69% for investment.

“We are now eagerly awaiting the response from the other two major

banks and the rest of the market, in light of these competitive fixed

rates from the country’s two biggest lenders,” concluded Mickenbecker.