We just released a new show on “In The Interests Of The People“, in which Economist John Adams, Property Expert Edwin Almeida and I discuss the problem of fake news, and why so many spruikers are pushing a line.

The first week of the federal election campaign has been dominated by heated disputes about the numbers behind both government and opposition policies, via The Conversation.

Both sides are under pressure. Notably, the cost of Labor’s 45% emissions-reduction target has been rightly questioned.

Opposition leader Bill Shorten’s answer to reporters that “our 45%

reduction, including international offsets, has the same economic impact

as the Liberals’ 26%” didn’t exactly engender confidence.

But the folly of Labor’s environmental plans is another tale for another column.

Our focus here is on how the Coalition is going to cut personal income tax by A$158 billion and balance the budget.

Wild assumptions

Earlier this week the Grattan Institute pointed out

the Coalition’s budget assumption that expenditure will fall from 24.9%

of GDP in 2018-19 to 23.6% during the next decade amounts to cutting

spending by more than A$40 billion a year in 2029-30.

This raised the natural question of exactly where those cuts will

come from. According to the government, it’s from things such as lower

welfare payments and lower interest payments on government debt.

The Grattan Institute’s Danielle Wood described these assumptions as “heroic”. Yup.

Now, you might wonder why the Coalition’s plan to cut personal income

tax doesn’t fully kick in until 2025. Or, for that matter, why its

“enterprise tax plan” on corporate tax is scheduled to be phased in over

a decade.

Playing outside the rules

The short answer is that for the four years following a budget – the

so-called “forward-estimates period” – there are rules about banking

spending cuts.

During those four years, cuts need to be specified, or economic

parameters need to be varied. And with good reason. That way the actual

assumptions the government is making, however fanciful they may be, are

plain for all to see.

But beyond the four-year period no such discipline applies. This

allows governments of all stripes to make very specific claims about,

for example, tax cuts they plan to deliver without having to be at all

specific about how they are going to pay for them.

This is all just a conjuring trick. Politicians try to get us to

focus on the tangible, specific thing we want – tax cuts, more money for

hospital or schools, free cancer treatment – while obfuscating how they

are going to pay for it.

It’s dirty pool. It’s not cricket. It’s the kind of thing a mob accountant does. Pick your favourite metaphor.

Bipartisan failure

Of course, treasurer Josh Frydenberg and finance minister Mathias

Cormann didn’t invent this unscrupulous practice. Wayne Swan and Penny

Wong, as treasurer and finance minister respectively, were guilty of

these kind of shenanigans too.

The specifics of the current round can’t even be debated properly,

because ten-year “guesses” don’t lay out specific assumptions that can

be checked for internal consistency and plausibility.

Sadly, it seems futile to hope for cultural change among politicians and a shift to integrity.

To some extent, we need to be the change we want.

The fact both sides of politics so brazenly play us for suckers is as

much our fault as it is theirs. If politicians thought there were real

consequences at the ballot box for this sort of behaviour, they would

think twice.

But there aren’t. When both sides are guilty it’s understandable that

voters become so cynical that they just factor it in and look to other

issues.

If more voters were willing to make “cooking the books” a decisive issue, that might change.

Need for incentives

Politicians respond to incentives. My favourite illustration of that

is how United Nations officials used to be exempt from parking tickets

in New York City. As economists Ray Fisman and Ted Miguel showed,

when norms alone governed behaviour, officials from corrupt countries

basically parked wherever they wanted. Once city authorities got the

ability to confiscate diplomatic licence plates of violators, things

improved radically.

So as long as the mainstream media refuses to issue our politicians

with the moral equivalent of parking tickets for cooking the books of

public debate, politicians are going to keep doing it.

Now, many commentators do exactly that – and some of them are

brilliant and fearless. But other folks, on the right and on the left,

seem to have the attitude that both sides play fast and loose with the

facts so it’s fine for them to call out whichever side they personally

like the least.

Actually, scratch “seem to have the attitude”. They’ll tell you that to your face.

When Australian cricket captain Steve Smith and vice-captain David

Warner got caught in a ball-tampering racket, there were consequences.

When our elected representative do something similar, but with our

nation’s finances –with consequences for growth, employment, welfare

benefits, retirement incomes, and climate change – they get a pass.

That’s got to stop; and we’ve all got our part to play.

Author: Richard Holden, Professor of Economics, UNSW

NAB says that an additional charge of $525 million after tax ($749 million before tax) relating to its customer remediation programme. As a result 1H19 cash earnings will drop by around $325 million and earning from discontinued operations by $200 million.

They say they have made around 360,000 payments to customers with a total valuer of $145 million, and the remediation team is building from 350 to around 500 across NAB.

Of the 1H19 charges, 90% relate to wealth, the remainder banking. IN combination with provisions raised in 2H18, total provisions for customer related remediation to 31 Match 2019 is $1,102 million.

The items responsible for this include:

Consumer credit insurance

Non-compliant advice to wealth customers

Adviser service fees by NAB advice partnerships (does not include allowance for customer refunds)

Adviser service fees charged by NAB Financial Planning

Banking related matters such as incorrect fee take on fee expect transactions.

These costs are to be held below the line as it were, but clearly investors and potentially customers will have to pay for this litany of poor practice.

It begs the question, can the NAB behaviourial norms be turned around? And at what cost?

The ABS has reported that Australia’s trend estimate of employment increased by 20,700 persons in March 2019, with:

the number of unemployed persons increasing by 3,000 persons;

the unemployment rate remaining steady at 5.0%;

the underemployment rate remaining steady at 8.2%;

the underutilisation rate remaining steady at 13.2%;

the participation rate remaining steady at 65.6%; and

the employment to population ratio remaining steady at 62.4%.

Over the past year, trend employment increased by 299,100 persons (or

2.4%), which was above the average annual growth rate over the past 20

years of 2.0%. Over the same 12 month period the trend employment to

population ratio, which is a measure of how employed the population

(aged 15 years and over) is, increased by 0.4 percentage points (pts) to

62.4%.

Trend employment increased by 20,700 persons between February and March

2019. This represents an increase of 0.16%, similar to the monthly

average growth rate over the past 20 years (0.17%), and less than the

monthly average growth rate over the past five years (0.22%).

Underpinning these net changes in employment is extensive dynamic

change, which occurs each month in the labour market. In recent months

there has been around 300,000 people entering and leaving employment.

There is also further dynamic change in the hours that people work,

which results in changes in the full-time and part-time composition of

employment.

Trend full-time employment increased by 18,000 persons between February

and March 2019, and part-time employment increased by 2,700 persons.

Compared to a year ago, there are 252,800 more persons employed

full-time and 46,300 more persons employed part-time. This compositional

shift led to a decrease in the part-time share of employment over the

past 12 months, from 31.7% to 31.3%.

The trend estimate of monthly hours worked in all jobs increased by 4.3

million hours (or 0.2%) in March 2019, to 1,776.8 million hours. Monthly

hours worked increased by 2.4% over the past year, equal to the

increase in employed persons (2.4%). The average hours worked per

employed person was 138.9 hours per month, or around 32.0 hours per

week.

The trend unemployment rate remained steady at 5.0% in March 2019. The

number of unemployed persons increased by 3,000 to 675,700 persons. Over

the past year, the trend unemployment rate decreased by 0.5 pts, with

the number of unemployed decreasing by 51,100 persons.

The trend participation rate remained steady at 65.6% in March 2019,

which was equal to March 2018 (65.6%). The female participation rate

remained steady at 60.6% and the male participation rate remained steady

at 70.9%.

The labour force includes the total number of employed and unemployed

persons. Over the past year, the labour force increased by 248,000

persons (1.9%). This rate of increase was above the rate of increase for

the total Civilian Population aged 15 years and over (360,500 persons,

or 1.8%).

The trend participation rate for 15-64 year olds, which controls (in

part) for the effects of an ageing population remained steady at 78.1%.

The gap between male and female participation rates in this age range is

less than 10 pts, at 82.8% and 73.6% respectively, continuing the long

term convergence of male and female participation.

The trend participation rate for 15-24 year olds (who are often referred

to as the “youth” group in the labour market) remained steady at 68.0%.

The unemployment rate for this group remained steady at 11.4% in March

2019 and decreased by 0.7% over the year.

The trend series smooths the more volatile seasonally adjusted estimates

and provide the best measure of the underlying behaviour of the labour

market.

SEASONALLY ADJUSTED ESTIMATES

Seasonally adjusted employment increased by 25,700 persons from February

to March 2019. The underlying composition of the net change was an

increase of 48,300 persons in full-time employment and a decrease of

22,600 persons in part-time employment. Since March 2018, full-time

employment increased by 289,800 persons, while part-time employment

increased by 14,900 persons.

Seasonally adjusted monthly hours worked in all jobs increased by 13.2

million hours (or 0.7%) in March 2019 to 1,785.4 million hours.

The seasonally adjusted employment to population remained steady at

62.3% in March 2019, and increased by 0.4 pts from the same time last

year.

GRAPH 1. EMPLOYMENT TO POPULATION RATIO, PERSONS, March 2009 to March 2019

The seasonally adjusted unemployment rate increased by 0.1 pts to 5.0%

in March 2019. The participation rate increased by 0.1 pts to 65.7%.

STATE AND TERRITORY ESTIMATES

TREND ESTIMATES

In March 2019, increases in trend employment were observed in all states

and territories except Western Australia (down 200 persons) and

Tasmania (down 100 persons). The largest increases were in Victoria (up

7,600 persons), followed by New South Wales (up 6,800 persons) and

Queensland (up 4,900 persons).

Over the past year, increases in employment were also observed in all

states except Tasmania (down 2,300 persons). Both territories recorded

falls with the Australian Capital Territory (down 1,600 persons) and

Northern Territory (down 4,800 persons). The largest increases were in

Victoria (up 127,500 persons), New South Wales (up 118,500 persons),

Queensland (up 36,100 persons). The highest annual employment growth

rates were in the Victoria at 3.9%, followed by New South Wales at 3.0%

and Queensland at 1.5%. For most states and territories, year-on-year

growth in trend employment was below their 20 year average, the

exceptions being New South Wales and Victoria.

The monthly trend unemployment rate increased by 0.1 pts in Tasmania

(6.5%) and the Australian Capital Territory (3.6%). It remained

unchanged in New South Wales (4.3%), Victoria (4.6%) and South Australia

(5.9%). It decreased by under 0.1 pts in Western Australia (6.1%) and

Queensland (5.9%), and fell 0.2 pts in the Northern Territory to 4.4%.

The monthly trend underemployment rate increased in the Northern

Territory (up 0.2 pts to 5.4%), Victoria (up 0.1 pts to 8.4%) and

Tasmania (up less than 0.1 pts to 10.1%). Decreases of up to 0.1 pts

were seen in New South Wales (7.5%), South Australia (8.9%), Queensland

(8.6%), Western Australia (8.9%) and the Australian Capital Territory

(5.9%).

Monthly trend participation rate decreases were observed in Northern

Territory (down 0.2 pts to 73.8%), Western Australia (down 0.1 pts to

67.8%) and Australian Capital Territory (down 0.1 pts to 69.2%). The

monthly trend participation rate increased less than 0.1 pts in New

South Wales (65.2%) and Victoria (66.1%). It remained unchanged in all

remaining states.

SEASONALLY ADJUSTED ESTIMATES

In seasonally adjusted terms, the largest increase in employment was in

Queensland (up 10,400 persons), followed by Victoria (up 10,000 persons)

and South Australia (up 8,500 persons). The largest decrease was in New

South Wales (down 2,600 persons) followed by Tasmania (down 1,800

persons).

The seasonally adjusted unemployment rate increased in Queensland (up

0.7 pts to 6.1%), South Australia (up 0.2 pts to 5.9%), Tasmania (up 0.2

pts to 6.7%), Western Australia (up 0.1 pts to 6.0%) and New South

Wales (up 0.1 pts to 4.3%). The only decrease in the unemployment rate

was observed in Victoria (down 0.1 pts to 4.6%).

The largest underemployment rate increase in seasonally adjusted terms

was seen in Queensland (up 0.9 pts to 8.9%) followed by South Australia

(up 0.4 pts to 8.8%), Western Australia (up 0.3 pts to 8.9%) and

Tasmania (up 0.2 pts to 9.9%). The only decrease was seen in New South

Wales (down 0.2 pts to 7.4%).

The largest increases in the seasonally adjusted participation rate were

in South Australia (up 0.7 pts to 63.2%) and Queensland (up 0.6 pts to

65.6%). The seasonally adjusted participation rate decreased in

Tasmania (down 0.4 pts to 60.3%), New South Wales (down 0.1 pts to

65.1%) and Victoria (down 0.1 pts to 66.0%).

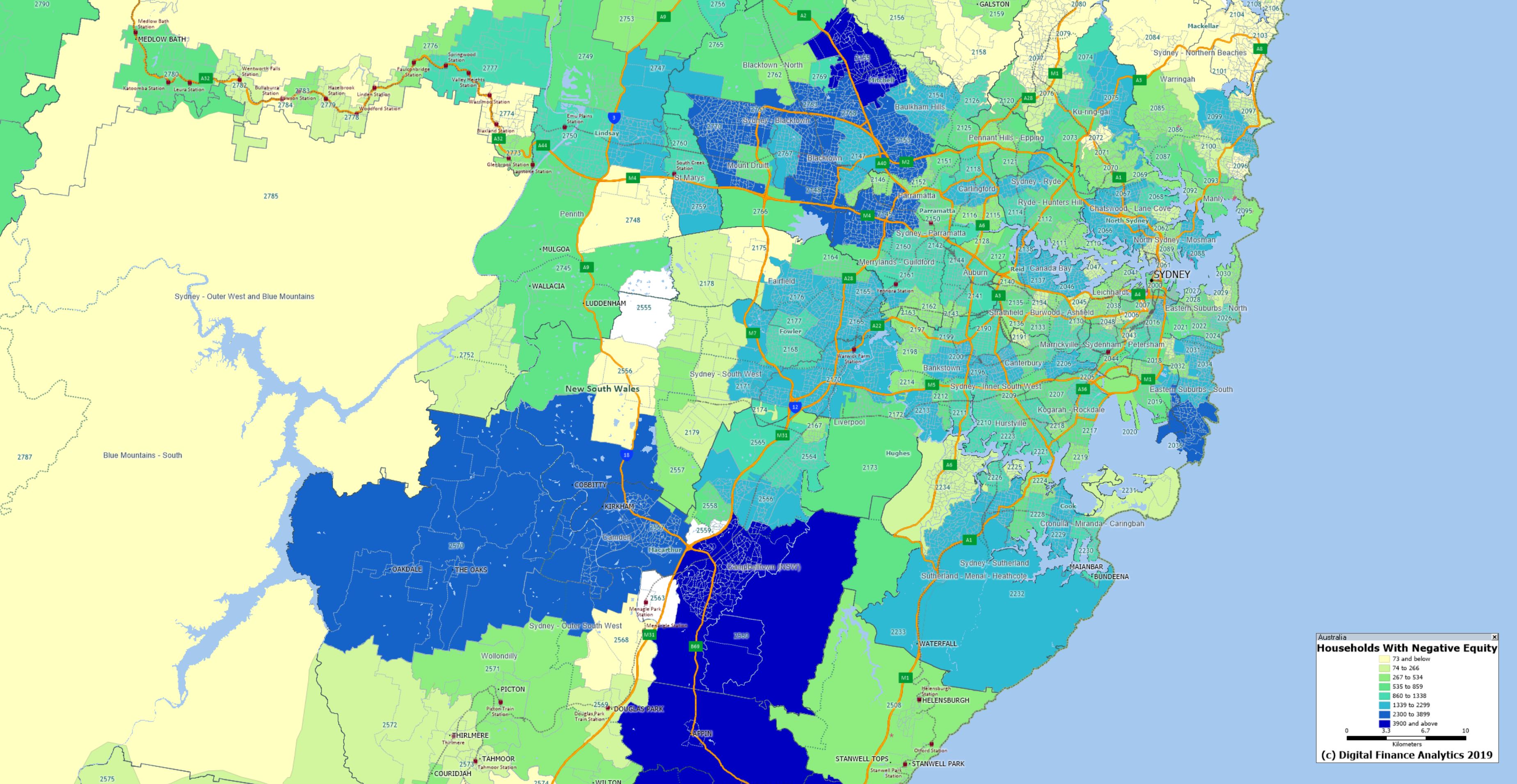

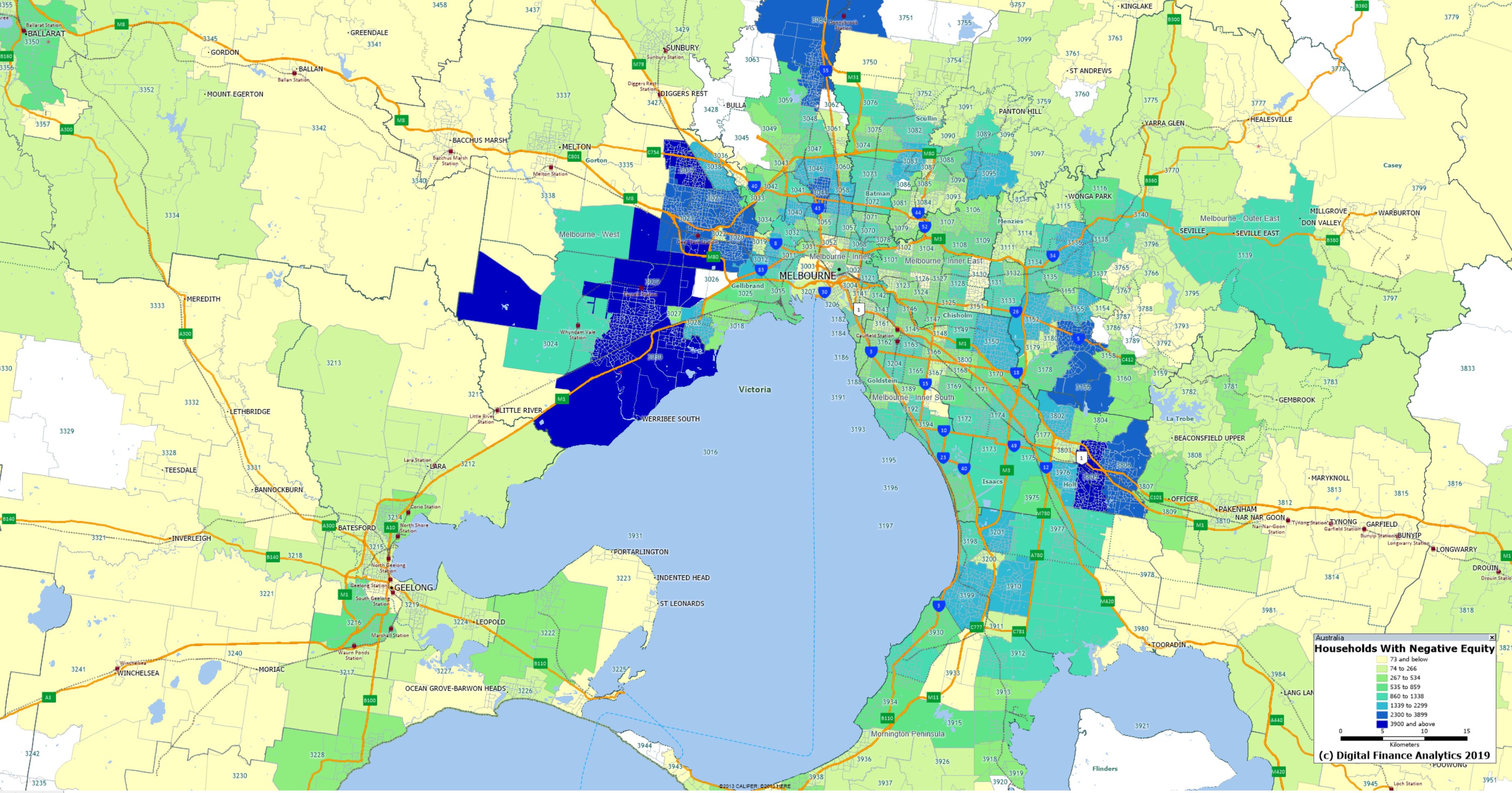

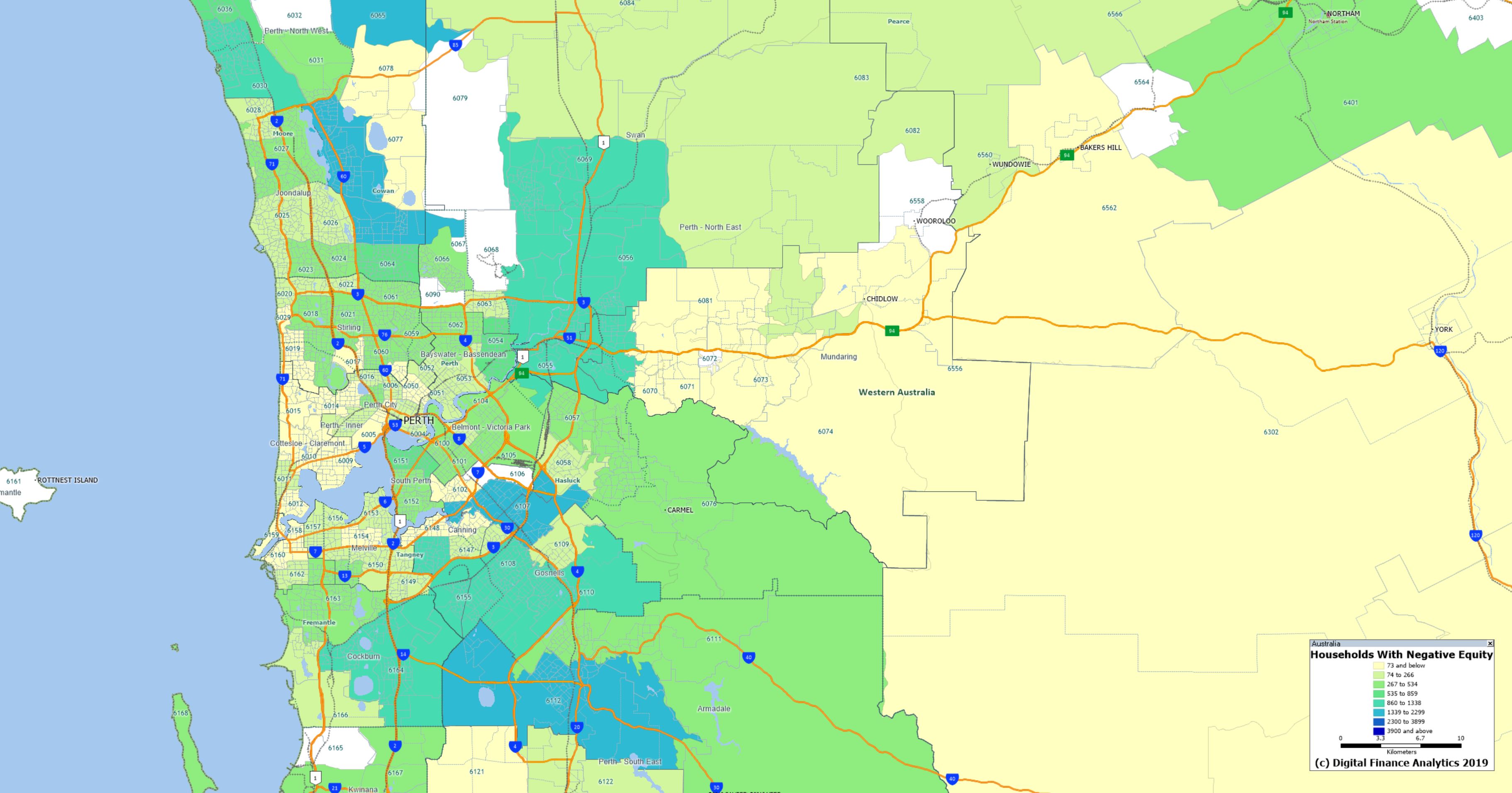

Following 7/30’s report last night I have received a number of requests for access to the maps. So here are the high resolution versions for Sydney, Melbourne and Perth. If they are reproduced elsewhere, please attribute DFA.

As discussed in my video, this is based on the number of households in each post code recording at least one property in negative equity – where the current mortgage (net of any offset accounts) in greater than the estimated current forced sale value plus sale costs. The analysis is based on results from our 52,000 household surveys nationwide.

The major

banks have seen their reputations significantly downgraded in an annual

perception survey, with AMP placing last out of 60 Australian companies.

The

Reputation Institute’s Australia RepTrak 2019 list examined 60 of the

top revenue making Australian firms, which saw all of the big four banks

and AMP ranked within the bottom ten.

The list was based on a

survey with around 10,000 respondents giving ratings across factors such

as trust and respect to generate overall reputation, in addition to

seven parameters: products/services, innovation, workplace, citizenship,

governance, leadership and performance.

AMP scored the lowest out of any company across all seven dimensions, dropping by 18 rankings from 2018.

NAB was the next lowest bank, falling at 58th place and having fallen 15 rankings from the year before.

Commonwealth Bank of Australia remained at its spot of 57th, while Westpac fell nine places to 55th.

ANZ fared the best of the big four, coming in at 51st, having fallen 16 places.

“In

the past 12 months we’ve seen many issues raised about corporate

behaviour and consumer trust,” Oliver Freedman, vice president and

market leader, Reputation Institute said.

“As a result, the reputations of our major banks and some financial services organisations have taken a major hit.”

Meanwhile,

Bendigo and Adelaide Bank rose seven places to 11th, which Mr Freedman

said was due to a strong performance in the individual measurements of

citizenship and governance.

“This proves that you can be a bank

and still have a strong reputation if you are focused on reputation

drivers that resonate with customers and increase trust,” he added.

Macquarie on the other hand came in at 42nd, down five places, as Allianz fell seven places from the year before to 37th.

New addition to the list Rest Super ranked 21st,while the Reserve Bank of Australia placed 18th, having risen by eight places.

AustralianSuper was down eight places to 15th.

“The

banking sector has a long road to recovery and could learn a lot from

those with consistently strong rankings, like Qantas and Air New

Zealand,” Mr Freedman said.

A brief segment on the ABC today which includes DFA data on negative equity, the Kouk, and reference to the RBA data.

They missed two important points I made in my interview, first my data is households not loans, and second the falls in value should require banks to mark to market their portfolios.

The maps can be seen here. This video walks through the mapping in detail.